tristezas das florestas tropicais - illegal logging · 2 table of contents 1. introduction 2....

TRANSCRIPT

1

Tristezas Tropicais:

More Sad Stories from the Forests of Zambézia

Catherine Mackenzie with Daniel Ribeiro

May 2009

Amigos de Floresta and Justica Ambiental

2

Table of Contents 1. Introduction 2. Annual allowable cut and volumes licensed 3. Decrease in the number of simple licence operators 4. Increase in the number of concessions

4.1 Status of the concessions 4.2 Ownership of the concessions 4.3 Quality of concession management plans 4.4 Quality of concession management 4.5 Reforestation 4.6 The Permanent Forest Estate 4.7 Community Concessions

5. Forest Law Enforcement 5.1 Checkpoints 5.2 Cooperation with local communities 5.3 SPFFBZ computerised data base 5.4 Infractions: Official accounts 5.5 Auction of illegal timber 5.6 Infractions: unofficial accounts and local opinion

6. “The 20%” 6.1 Problems 6.2 Irregularities

7. In-country processing, industrial capacity and employment 7.1 Sawn wood production, sawmills and industrial capacity 7.2 Markets for sawn timber in China 7.3 Employment in the Forest Sector 7.4 Government Support for industry: China vs Mozambique

8. Control of Timber Export 8.1 Port Management 8.2 Customs 8.3 Official statistics 8.4 Cases of illegal export

9. Remaining stocks of commercial timber 10. Conclusions and Recommendations

3

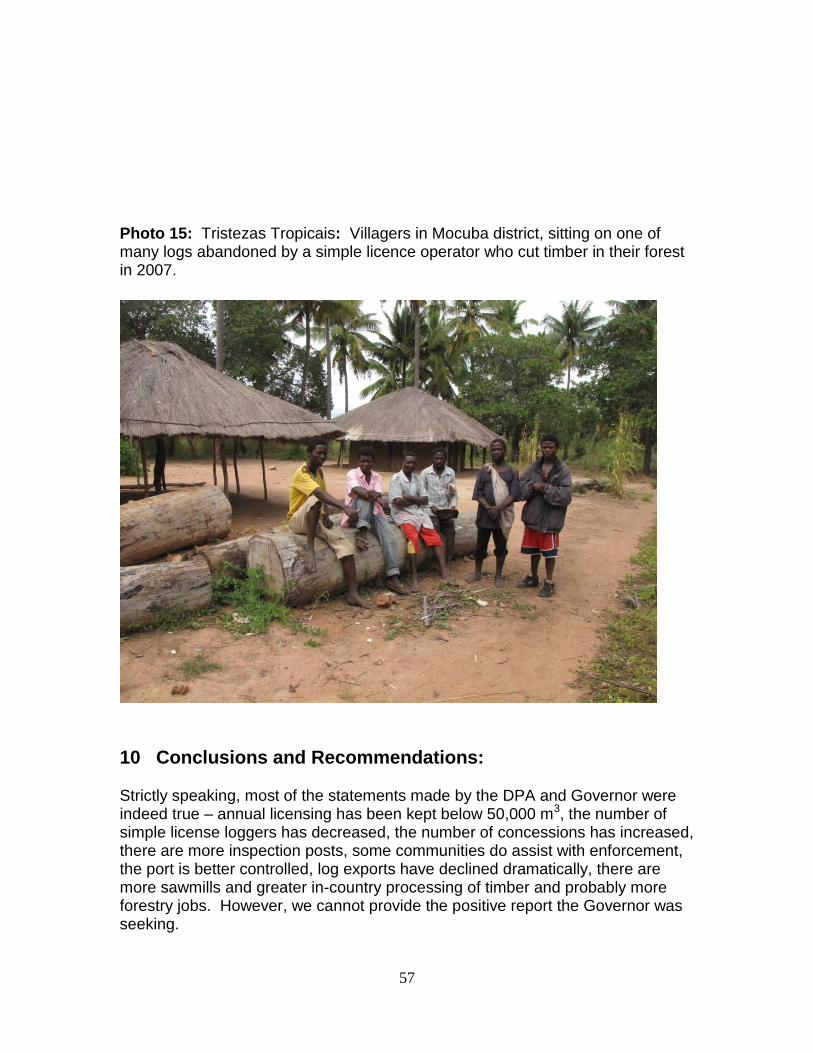

Table 1: Actual licensing and harvesting in Zambézia; 2000 – 2007 Table 2: Number of simple licences and concessions issued, and volumes licensed in Zambézia, 2003-2007 Table 3: National origin of concession holders (with approved management plans) Table 4: Government reforestation efforts: nurseries, seedlings and areas forested, 2000-2007. Table 5: Forest law enforcement in Zambézia: Staff numbers, infractions, products seized and total fines, 2001-2007 Table 6: Progress on Distribution of the 20% to communities in Zambézia, 2005-2008 Table 7: Production of sawn timber in Zambézia, 2001-2007 Table 8: Export prices from Quelimane for sawn Umbila (fob) Table 9: Official statistics on export of timber and sawnwood: SPFFB, Customs and Cornelder, 2002-2007 Table 10: Pau preto licensees, licensing and legal entitlement Table 11: Customs records of export of pau preto Table 12: Under-reporting of pau preto exports Figure 1: Export of logs and sawn timber from Quelimane in four quarters of 2007 Figure 2: Export of logs and sawn timber from Quelimane 2004 – April 2009 Photo 1: Spatial control of timber cutting by SPFFBZ Photo 2: Public auction of seized timber: starting price of around $100/m3, about 1/3 of the local market value of the timber. Photo 3: Truck loaded with chanfuta timber, leaving the illegal trade point in Licuari Photo 4: “Sawn timber” of pau ferro en route to Quelimane port Photo 5: Cheap quality sawmill of an Asian timber buyer in Quelimane. Photo 6: Mozambican and other African logs in a wholesale logyard near Zhang Jia Gang Port, near Shanghai Photo 7: Mondzo used to make ornate furniture, near Shanghai Photo 8: Jambire used to make cheap footstool for tourists, Nanxun, near Shanghai Photo 9: Antique Chinese table showing matching of grain Photo 10: High quality Chinese carving, incorporating character of raw material Photo 11: Semi-processed furniture components originating from Viet Nam, in a factory near Shanghai Photo 12: Chinese sawmills operations and their products are not all high-tech Photo 13: Pau Preto from Zambézia in a warehouse at the Furen Market, Shanghai, China Photo 14: Pau preto log end, with sigla of Zambézian simple licence logger Photo 15: Villagers in Mocuba district, sitting on one of many logs abandoned by a simple licence operator who cut timber in their forest in 2007.

4

Box 1: Story of a Simple Licence Logger Box 2: On managing a concession Box 3: Comments on Law Enforcement by Acting Head of SPFFBZ, Eng Chibite Box 4: Story of a “Furtivo” Box 5: Story of a community: Bive/Makwia Box 6: An exporter – TTT Timber Box 7: Setting up a forest industry in Zambézia Acknowledgements The research for this study was a collaboration between Justica Ambiental, ORAM and Amigos de Floresta. Eduardo Nhabanga of Justica Ambiental and Gil Jaime of ORAM Zambézia collaborated in the field work in Zambézia. Daniel Ribeiro also participated in the field work in China, where Shao Yang and Zhang Xue Mei provided invaluable technical advice, logistic support, translation and great companionship for the 2 week field work. Toby Dewar, of Christian Aid in Mozambique provided logistic support during the study. The final document was translated into Portuguese by BESTEX. Many others, who wish to remain nameless, gave generously of their time and information, for which we are grateful. Like the original study, this work was generously funded by Christian Aid, and thanks are due to Salomao Maxeiai for his support. Oxfam Novib kindly supported the field work in China. Abbreviations AAC – Annual Allowable Cut DDA – Director Distrital de Agricultura/District Director of Agriculture DNFFB – Direccao Nacional de Florestas e Fauna Bravia/National Directorate for Forests and Wildlife (became DNTF in 2006) DNTF – Direccao Nacional de Terras e Florestas/National Directorate of Lands and Forests DPA - Director Provincial de Agricultura/Provincial Director of Agriculture MTN – Meticais Novo (April 2008 $US 1 = 24 MTN) OIIL - Orcamento de Investimento de Initiativos Local/Local Initiative Investment Fund ORAM – Associacao Rural de Ajuda Mutua/Rural Self-Help Association (local NGO) PROAGRI – Sector-wide donor support programme for agriculture. SPFFBZ – Servicos Provincias de Florestas e Fauna Bravia da Zambézia/Provincial Forest and Wildlife Services

5

Tristezas Tropicais:

More Sad Stories from the Forests of Zambézia

1. Introduction: An End to Forestry or a new beginning? “Nao ha mais madeira!” (There’s no more timber!) One industrial concessionaire we spoke to was adamant that this was the way we should begin our update on “Chinese takeaway!”1, the 2004 study of forestry in Zambézia province in Mozambique. “It’s not even worth the trouble you doing this research now,” he continued, “it’s all too late. The valuable timber is all in China already; only the small and poor quality trees are left. There’s no future to the processing industry here now”. Other industrial operators agreed with him, adding “The forest sector is much worse than four years ago.” and “Everything is out of control. The situation is already “post-crisis””. “Things have improved greatly since 2004.” This is how the Governor of Zambézia,,Carvalho Muaria began his reply to our introductory question about the performance and developments in the forestry sector in the province over the last 4 years. He and the Provincial Director of Agriculture (DPA), Mohamad Vala. went on to explain how 3 new forestry check-points had been established at strategic places in province and more were planned, an international company had rehabilitated and taken over management of the port, so timber export was much better controlled, communities had started receiving the 20% of the licence fees as required by the 1999 Law, the number of annual simple licences was being brought down and the number of 50-year concessions was increasing in

their stead2. Licensing is now well within the annual allowable cut established by

the Zambézia inventory, and all of the 7 main commercial species now have to be processed in-country before export, resulting in much greater industrial

1 It would be fairer to say “takeaway to China” – emphasising the destination rather than the actors.

Not all the traders are actually Chinese, there are also Indians, Malaysian, Singaporeans,Taiwanese,

European and some multinationals are involved – such as OLAM. As with other parts of the economy, the

wood processing industry in China includes many foreign investors who are manufacturing in China to

supply a foreign market.

2 Under Mozambican law, there are two “regimes” for forest harvesting, simple licences, and

concessions. Simple licences are valid for one year, for a maximum of 500 m3 in a specific area of around

5000 ha and only Mozambican nationals are eligible. Applications must be made by January of any year,

and the approval process includes demonstration of an operator’s technical capacity. Concessions are valid

for 50 years and should be large enough to support an industry. International individuals and companies

are eligible. Applications can be initiated any time. The approval process should take about 9 months, and

involves various steps, which include preliminary approval at the provincial level, preparation of a forest

inventory and management plan which establish the annual harvesting quota and its approval by DNTF,

and culminates in an official contract between the operator and SPFFB and the establishment of an

industry. Government policy is to phase out simple licences.

6

capacity and employment generation. Nurseries for native species were operational and the Provincial Forests and Wildlife Services (SPFFBZ) and DPA had good working relations with civil society. He hoped that our report would be positive. On the face of it, these were encouraging words. Indeed, the points raised responded to some of the main concerns and recommendations in the “Chinese Takeaway” report, and seemed to go some way to explaining why many government officials had dismissed the report, as “out-of-date”, at its launch in Mozambique in early 2007. How to make sense of such dramatically opposing viewpoints? This paper sets out to explore the facts behind both sets of answers, and other developments in the forestry sector between 2004 and 2008. Like ”Chinese Takeaway!”, this report is kept as objective as possible: there is no advantage in criticism for its own sake, and great disadvantages if it leads to the abandonment of positive initiatives. We also want to be practical and realistic about what can be achieved in Zambézia, and not let “the best become the enemy of the good”. To keep this report brief, we simply take each of the 8 main assertions made by the Governor and the DPA regarding progress in the forest sector governance, review the situation in 2004, and examine the facts behind the situation found in 2008. We finish off with a few conclusions and recommendations3. Methods The field work in Zambézia took place from 28 April to 27 May 2008. Some additional information obtained in April 2009 is also included, and a separate report is available on the impact of the global financial crisis on the forestry sector in Zambézia (Mackenzie 2009). As in 2004, the main methods employed were analysis of secondary data, mostly from government sources, key informant interviews, field visits to forest communities and direct observation. Although in 2004 some people were caught unaware and were quite candid with us, this time many key informants were much more guarded, and numerous people refused or avoided meeting with us. As described below, we received poor cooperation from the DPA and SPFFB Zambézia, but Customs and Cornelder (the private company managing the port) were quite open and helpful. For this update report, we had the fascinating opportunity to follow Mozambican timber into the forest product markets and factories of China, to see some of the realities of the incredibly successful forest industry there and to explore the feasibility of processing by community concessions in Zambézia. Findings from that visit will be incorporated in this report where relevant, and a full report will be available separately.

3 For those interested, a fuller 60 page version of this report is available, but only in English.

7

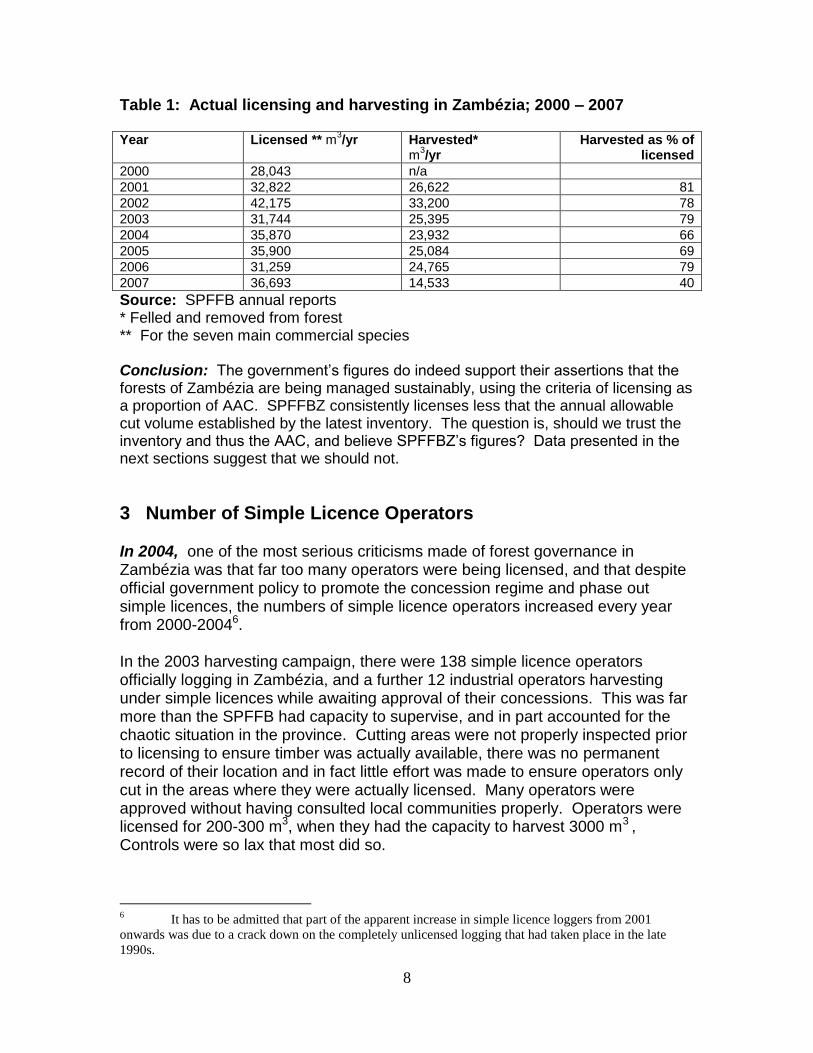

2 Annual allowable cut and volumes licensed In 2004, the annual allowable cut (AAC) for Zambézia was a contentious issue and was discussed in detail in “Chinese Takeaway”. The inventory then in official use was the 1994 national inventory of Saket which prescribed an AAC for Zambézia of 17,600 m3 for the seven most important commercial species. Despite this, as Table 1 indicates, from 2000-2004, SPFFBZ routinely licensed by 65-239% above that limit. Some industrial operators objected that this was already overharvesting. A new provincial inventory, conducted in 2002-044, concluded that Saket had been a massive under-estimate, and recommended quadrupling the AAC for those species to 72,533 m3 5. Although National Directorate for Forests and Wildlife (DNFFB) admitted there were technical problems with the results, and delayed officially releasing it until 2005, SPFFBZ started using the figures in 2004 to justify its high levels of licensing. We argued then that the new AAC was not sustainable, and that given the methodological problems it should be subject to independent technical review. By 2008, the new AAC was firmly established, as further illustrated in Table 1. Against these extraordinarily high estimates of sustainable harvest, the assertion of the Governor and DPA that licensing remained within the AAC is thus ostensibly correct. Moreover, official licensing reported by SPFFBZ is actually substantially less than the new AAC – typically around 35,000 m3/yr - which SPFFBZ uses to claim its approach to management is positively conservative. Furthermore, according to SPFFBZ annual reports, in most years only 70-80% of the volume licensed is actually harvested.

4 The inventory was part of the Finnish-supported Projeto Maneio Sustentavel de Recursos

Florestais/ 5 Details of the AAC are provided in Appendix 1, breaking down the quota by species and district.

What is not immediately apparent from the AAC figures is that it covers all forest types and the entire

provincial forest area of 12 million ha. Only the L1 and L2 forest types are dense enough to be

commercially exploitable, and only 44% of the commercial volume is found here.

8

Table 1: Actual licensing and harvesting in Zambézia; 2000 – 2007 Year Licensed ** m

3/yr Harvested*

m3/yr

Harvested as % of licensed

2000 28,043 n/a

2001 32,822 26,622 81

2002 42,175 33,200 78

2003 31,744 25,395 79

2004 35,870 23,932 66

2005 35,900 25,084 69

2006 31,259 24,765 79

2007 36,693 14,533 40

Source: SPFFB annual reports * Felled and removed from forest ** For the seven main commercial species Conclusion: The government’s figures do indeed support their assertions that the forests of Zambézia are being managed sustainably, using the criteria of licensing as a proportion of AAC. SPFFBZ consistently licenses less that the annual allowable cut volume established by the latest inventory. The question is, should we trust the inventory and thus the AAC, and believe SPFFBZ’s figures? Data presented in the next sections suggest that we should not.

3 Number of Simple Licence Operators In 2004, one of the most serious criticisms made of forest governance in Zambézia was that far too many operators were being licensed, and that despite official government policy to promote the concession regime and phase out simple licences, the numbers of simple licence operators increased every year from 2000-20046. In the 2003 harvesting campaign, there were 138 simple licence operators officially logging in Zambézia, and a further 12 industrial operators harvesting under simple licences while awaiting approval of their concessions. This was far more than the SPFFB had capacity to supervise, and in part accounted for the chaotic situation in the province. Cutting areas were not properly inspected prior to licensing to ensure timber was actually available, there was no permanent record of their location and in fact little effort was made to ensure operators only cut in the areas where they were actually licensed. Many operators were approved without having consulted local communities properly. Operators were licensed for 200-300 m3, when they had the capacity to harvest 3000 m3 , Controls were so lax that most did so.

6 It has to be admitted that part of the apparent increase in simple licence loggers from 2001

onwards was due to a crack down on the completely unlicensed logging that had taken place in the late

1990s.

9

In 2008, according to the Governor and DPA, one of the most significant changes that had occurred since 2004, was a decrease in the number of simple licence operators, and a concomitant increase in the number of concessions. This shift in the balance between the two licensing regimes, they asserted, demonstrates not only that government policy is being implemented, but also that forest management is moving onto a more rational and sustainable basis. The DPA and SPFFBZ denied us access to the data on licensing (by operator, species and district) that we needed to accurately assess their assertions, and so we have had to rely on the information available in SPFFBZ annual reports. As in 2004, these reports are incomplete and the information in them inconsistent from year to year. The summary in Table 2 shows that the number of simple licence operators dropped from a maximum of 138 in 2003 to 91 in 2006, but then increased again to 99 in 2007. SPFFBZ could only estimate that there would be around 100 in 2008. This represents a total reduction of 28%. The proportion of the timber licensed to simple licence holders as opposed to concessions has also decreased from 92% to 61%. But does this demonstrate a move towards more sustainable forest management, and fulfilment of government policy? Table 2: Number of simple licences and concessions issued, and volumes licensed in Zambézia, 2003-2007

2001 2002 20031

2004 2005 20063

2007

Number of licences issued 276 336 706 863 115 101 113

Number of LS operators licensed 57 124 138 128 104 91 99

Number of concession applicants using LS licenses

20 16 n/a n/a n/a

Number of concessions licensed 2 2 11 10 14

Total Number of Operators 160 146 112 101 113

Volume licensed LS 32,682 42,175 29,4772

n/a 20,983 23,1514

22,203

Average Volume per LS 186 215 254 224

% total volume to LS 92 65 74 61

Volume licensed CF 2,267

11,340 8,1084

14,490

% total volume to CF 8 38 26 39

Average volume per CF 1,134 1,030 811 1,035

Total Volume licensed 32,682 42,175 31,744 35,870 32,323 31,259 36,693

Source: SPFFB Annual Reports; 1 some figures from Mackenzie (2006). 2 includes 3721 m3 to concession applicants using simple licences; 3 From 2006, the practice of issuing multiple licences to an individual operator ended. 4 data from DNTF annual report 2006.

The first thing to note, as mentioned above, is that while a reduction in simple licences did take place between 2003 and 2006, it increased again in the subsequent two campaigns. Similarly, while the proportion of timber harvested by simple licence loggers dropped from 93% to 65% between 2003 and 2006, it

10

has remained persistently high, at over 60% since then, despite the increasing number of concessions7. So, implementation of government policy has at least stalled, and perhaps even reversed. The key question, however, is whether official licensing represents all the loggers active in Zambézia. According to most informants we spoke to, there has been an explosion in illegal licensing and completely unlicensed logging. In 2004, the Asian buyers secured their logs by providing simple licence operators with credit to pay for their licences and operational costs. But giving credit became too risky. Too many operators were side-selling, or defaulting entirely and, as described in more detail below, in 2005, the Asian buyers began to acquire their own concessions, and obtain licences of their own. So, many of the old simple licence loggers have had to start acquiring licences in other ways (See Box 1).

Box 1: Story of a Simple Licence Logger Sr A has been in the logging business since 2005, working in Zambézia and neighbouring Nampula, using his own simple licences, licences of others and buying/selling of wood from simple license holders. Before starting in logging, he was in the hotel business where he trained staff on how to serve guests, specially for the restaurant. After that he worked as a warehouse stock controller and he became a trader. He first started with buying meat from Malawi and selling it to Mozambican butchers and buying Mozambican maize and selling it to Malawi. In 2005 he got involved with wood. He started working with Pau ferro, Mondzo and Muaga and then added Jambire, Chanfuta and Umbila, which he sells into the local market in Beira. This year he is going to buy a simple license from someone else. He will either agree to organize and do all the work and then share the profit with license holder or he will pay double on the licence fees. He prefers the second option. Profits are going down. In 2005 transport cost was around 15,000 MTN, labour was around 5000 MTN and profits per truck load could reach around 10,000 MTN. In 2006, the costs were similar, but the better prices allowed for higher profits reach around 15,000 MTN per truck load. In 2007, the costs when up a lot, especially for transport. Tractors rent increased by 500mt per day, and because the timber is so sparsely distributed, they are indispensible. Trucks prices increased from 25,000 MTN to 35,000 MTN. Timber prices, however, stayed similar or decreased, so profits really went down and now its rare to get 10,000 MTN per truck load Many operators didn’t make profits, but he did, because he loaded the truck well… getting 35-45 logs. He has his own chainsaw and cut some of his wood, but got most of his logs from communities. He paid 100 MTN for each log and only took good ones (on average 6 -7 logs out of 10). Only good logs make good profit because the Chinese discount a lot in the measurement. Also truck space is expensive, and it’s a waste to take bad logs. It is becoming very difficult to find good quality pau ferro, and mondzo has become rare …. He’s now looking into other species and the national market. He cut pau ferro last year when demand was high. In total he cut one truck load of 11 tons and

got $300/ton from Olam. He made 20,000 MTN ($833) profit with that one truck load.

7 On average, a concession holder still only harvests around 1000 m

3 per year – this is just double the

maximum legal entitlement of simple licence loggers, and four times the volume they are reported to cut.

11

One popular way to get a licence is to buy it illegally from SPFFBZ staff in Quelimane or from the field inspectors. Apparently, this kind of corruption is now common, with many more unauthorised staff issuing licences illegally, forging the signature of the head of SPFFBZ. One observer quipped that you are much more likely to see forestry staff out on the street cutting deals with loggers, than in the office doing their real jobs. Buying transport permits (guias de transito) or whole licences from another logger is another option, which seemed to be more prevalent in 2008. Part of the phenomenon appears that many simple licences are awarded year after year to people who are not actually loggers. They are typically closely connected with government and FRELIMO, and simply sell their licences on at a profit, effectively, getting money for nothing. This calls into question another assertion of SPFFBZ made in 2004 to demonstrate their sound management practices, that they award licences according to a logger’s years of experience, giving more experienced loggers bigger quotas. There has also been an increase in “furtivos”, the completely unlicensed loggers. Some furtivos cut and sell wood themselves, but many communities are also involved in this. Furtivos go around buying logs straight from villages, and sell them at various collection points, or to licensed operators. Sometimes communities cut on order from furtivos, and sometimes communities cut first and then go looking for a market. One concession holder reported being offered 100 m3 of pau preto from a community logger in the recent boom (see below). The regulation of simple licence logging was designed to ensure some level of sustainable harvest, operator competence and community consent. The illegal licensing described above bypasses all these checks and balances and brings chaos to Zambézia’s forests. In 2004, another major problem with simple licence loggers was overharvesting, and this is still happening, probably to a greater degree. The issues are basically the same. No operator gets the full entitlement of 500 m3 and most get only 200-300 m3. This quota can be exhausted in a couple of weeks, but the season lasts 9 months, and the logging teams (if they exist) just keep cutting. Sometimes, the unlicensed timber remains abandoned in the forest, because there’s no transport permit (or cash) to get it through the checkpoint and into town. Conclusion: According to the official figures, it is certainly true that the number of simple licence operators has declined by 28% since 2003, but it appears that this has been accompanied by an explosion in the number of illegal licences and “furtivos”. Overcutting by licensed operators still continues. The intended impact of the measure, to bring the sector under greater control, is still a very distant goal.

12

4 Increase in the number of concessions In 2004, there were only 2 concessions operating in Zambézia, Madal and Sociedade Moveis Licungo, and a third management plan, that of Timberworld in Pebane had been approved. “Chinese Takeaway” demonstrated that two of the approved plans were technically unsound and would not ensure sustainable management. At that time, there were another 34 concession applications by 20 companies, in the approval process. Many had been in process for several years and some were simply ruses, never seriously pursued, but which enabled operators to obtain exclusive harvesting rights over a large area for a few years. Some serious operators complained their applications were delayed because the cost of preparing management plans - made prohibitively high by the government’s limiting of the number of consultants authorised to prepare them. At this time, the majority of Asians in Quelimane were only buying timber. Although some 15 companies with Asian connections had concession applications, they were not entitled to simple licences, so instead, to obtain timber, they financed local people to get their simple licences and equipment, and bought the timber from them. In 2008, the Governor and DPA told us the number of concessions has now increased. Although the official data on concessions is inconsistent and based on unclear definitions 8 according to our review of it and concession applications, there were 32 approved and contracted concessions, covering over 1.2 million hectares. According to the Acting Head of SPFFBZ, 21 of these concessions (with a total area of 908,288 ha) have established the required industry and are officially in operation. This is around 10 times more than in 2004, and a 70% increase over 2007. Information about these concessions, abstracted from management plans and SPFFBZ files, is summarised in Appendix 2. Another 16 concessions, covering a 611,545 ha are in the approval process. Applicants include 2 community concessions (see below), one Mozambican national and 3 local Zambézian industrial operators, 2 long established simple licence operators, 1 Malawian, 2 Libyans and 5 Chinese. One reason for this increase in concessions, is undoubtedly because the government finally had to enforce the deadline for completing application processes, in order to fulfil performance indicators set by donors for PROAGRI II. By 2004, operators had already been allowed to drag out what is supposed to be a 9 month application process, for up to 3 years. Following various protests from donors and promises from the government, 13 plans were produced and

8 A disturbing feature of the official statistics on concessions is how inconsistent they are between years

and between agencies. The annual reports of both DNTF and SPFFBZ more obfuscate than clarify the

situation. The terms used are “approved concession”, “approved management plans”, but not “contracted”

and “operating concessions". Neither agency actually states how many concessions are actively operating,

nor reports the species and volumes licensed to each one.

13

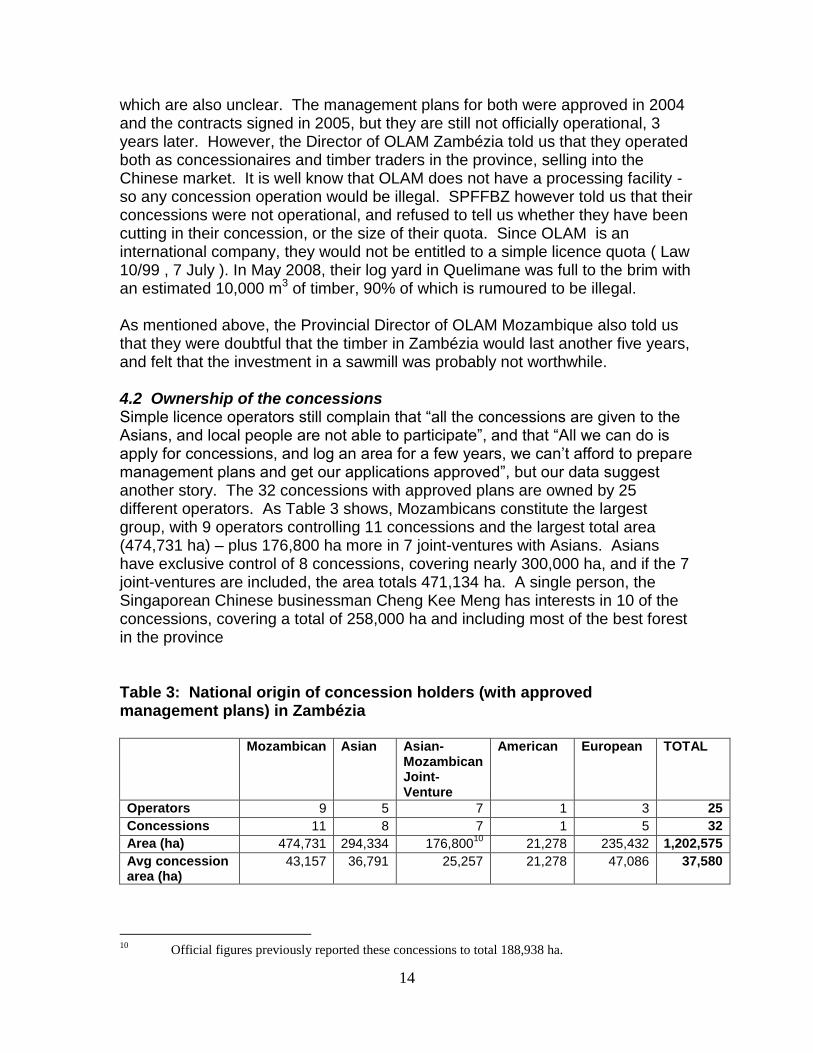

approved in a single batch in early 2005 and a further 10 in late 2006. The Finnish-funded forestry project in Zambézia also provided a technical adviser to assist reviewing the plans at the provincial level, which helped push the process along. Another reason is that the price of preparing management plans dropped from about $1/ha to about $0.30/ha. Surprisingly, this happened without the government significantly increasing the number of consultants authorised to prepare plans. So, the number of concessions has indeed increased, as reported by the Governor and DPA. But, as with the decrease in simple licences, the important question to ask is whether these licensing changes have brought the claimed improvements to management and governance of the forests, and the intended industrial development. For evidence, the next section examines the status of the concessions, the status of the whole forest estate in Zambézia, the quality of the concession management plans and their implementation, including the issue of replanting after harvest. 4.1 Status of the concessions Of the 32 approved and contracted concession, 11 have not yet established industries required to start operations. These include three influential companies, Green Crown, Timber World and Olam, some of which appear to have started cutting in their concessions anyway. The Green Crown group comprises 7 of these non-operational concessions, and all are joint-ventures between the Singaporean Chinese businessman, Cheng Kee Meng, and people closely connected to the Government and FRELIMO. Together they cover some of the best remaining forest in the province (see Mackenzie 2006: ). The original concept for Green Crown was prepared and the concession applications made back in 2002. The management plans for these concessions were approved between August 2003 and October 2006, and the contracts signed between March 2005 and December 2006. The process has been drawn out over 6 years to ensure the partners kept control of these valuable forests, while they lobbied government and waited for the repair and re-opening of a strategic bridge near Mocuba, which would make the forests easily (and cheaply) accessible. Cheng Kee Meng also controls two concessions under the company Timberworld. Timberworld has not yet established its industry (SPFFBZ annual report 2007), yet SPFFBZ admitted that Timberworld was cutting in its concession in 2007 (Chibite, pers com.). OLAM Mozambique, part of the Singaporean multinational agricultural commodity company9, has two concessions covering 65,000 ha, the positions of

9 OLAM works in 56 countries round the world and has offices in Shanghai and Guangzhou to

distribute its timber to the Chinese markets. OLAM also has well-developed Corporate Social and

Environmental Respsonsibility statements: see: http://www.olamonline.com/home/home.asp

14

which are also unclear. The management plans for both were approved in 2004 and the contracts signed in 2005, but they are still not officially operational, 3 years later. However, the Director of OLAM Zambézia told us that they operated both as concessionaires and timber traders in the province, selling into the Chinese market. It is well know that OLAM does not have a processing facility - so any concession operation would be illegal. SPFFBZ however told us that their concessions were not operational, and refused to tell us whether they have been cutting in their concession, or the size of their quota. Since OLAM is an international company, they would not be entitled to a simple licence quota ( Law 10/99 , 7 July ). In May 2008, their log yard in Quelimane was full to the brim with an estimated 10,000 m3 of timber, 90% of which is rumoured to be illegal. As mentioned above, the Provincial Director of OLAM Mozambique also told us that they were doubtful that the timber in Zambézia would last another five years, and felt that the investment in a sawmill was probably not worthwhile. 4.2 Ownership of the concessions Simple licence operators still complain that “all the concessions are given to the Asians, and local people are not able to participate”, and that “All we can do is apply for concessions, and log an area for a few years, we can’t afford to prepare management plans and get our applications approved”, but our data suggest another story. The 32 concessions with approved plans are owned by 25 different operators. As Table 3 shows, Mozambicans constitute the largest group, with 9 operators controlling 11 concessions and the largest total area (474,731 ha) – plus 176,800 ha more in 7 joint-ventures with Asians. Asians have exclusive control of 8 concessions, covering nearly 300,000 ha, and if the 7 joint-ventures are included, the area totals 471,134 ha. A single person, the Singaporean Chinese businessman Cheng Kee Meng has interests in 10 of the concessions, covering a total of 258,000 ha and including most of the best forest in the province Table 3: National origin of concession holders (with approved management plans) in Zambézia Mozambican Asian Asian-

Mozambican Joint-Venture

American European TOTAL

Operators 9 5 7 1 3 25

Concessions 11 8 7 1 5 32

Area (ha) 474,731 294,334 176,80010

21,278 235,432 1,202,575

Avg concession area (ha)

43,157 36,791 25,257 21,278 47,086 37,580

10

Official figures previously reported these concessions to total 188,938 ha.

15

4.3 Quality of Concession Management Plans In 2004, the management plans of Timberworld and Madal were analysed in some detail, and heavily criticised for their failure both to follow the law and to promote sound management. Particularly, the plans proposed to strip out the valuable commercial timbers within the first 5 – 10 years. Despite this, the plans were approved. In 2008, over 20 concession management plans were examined. Despite the publication of a new concession management manual in 2005, and SPFFB’s significantly greater institutional experience, no improvement was found. The majority of the plans (62%) have been prepared by Dr J Bunster of TraForest, a Chilean forester who has worked in Mozambique for several decades and who prepared the Timberworld management plan in 2002. His plans now follow a very standardised format, and while this standardisation in itself is not a problem and could even simplify the approval and monitoring of concessions, unfortunately, the technical management prescriptions are all standardised too. So, although forest scientists are agreed that the cutting cycle in Zambézia should be at least 30 years, all the management plans are based on a 20-year rotation, and many propose to take all the presently valuable timber in the first 5-10 years. When asked about this, Dr Bunster admitted that the cutting cycle was too short. He explained that if the proper rotation were used, the profit would be too low for the businesses concerned. Furthermore he said that the previous head of DNTF, Arlito Cuco, had agreed with this shorter rotation. Once this precedent was set, all other concessions followed. When asked why the concessions were not simply made larger he replied that large concessions were expensive to establish (especially the cost of management plans), difficult to control, and investors didn’t want them. So, in short, the forest sustainability is being sacrificed to commercial convenience and profit.

16

Photo 1: Spatial control of cutting by SPFFBZ in 2008. Section of map showing the official record of concessions and simple licence loggers in the area east of Mocuba.

4.4 Quality of Concession Management In 2004, the main concession under management was the 94,000 ha operation of Madal. Although there were problems, it was at least a centralised operation, with Madal organising labour and equipment. In 2008, the majority of the concessions in Zambézia are themselves in chaos. Many Asians, who in 2004 were timber buyers and obliged to work through simple licence operators to get their timber, have now become concession holders, and have rights to thousands of cubic metres worth of timber licences a year. But it appears most of them do not oversee operations in their concessions. They simply provide licences to loggers they trust, or sell off the licences (for around $10 more than the official fee) and then they buy back the timber. No one knows how many operators are out there, who is entitled to cut how much or from where. As described above, “furtivos” work many of the concessions. Villagers also cut for furtivos, making 100 MTN per log, regardless of whether the species sells for $120 or $450. Really, the concessions are

17

turning into a way of informally sub-contracting to simple licence holders, and there has been a complete loss of transparency and accountability in the process. There are too many actors and no control. What in 2004 was the malaise of the simple licence areas has now spread to the concessions.

Box 2: On managing a concession My concession is difficult to protect. There’s agricultural encroachment on one hand, and poaching of timber on the other. One poacher is one of my own workers! Local villagers cut trees, and break down the logs into boards. Once there’s a truck load, someone comes. The wood probably goes to local markets. Chinese only take logs. And they take everything, any quality. Spoils the market. In Pemba, the South African traders only take good stuff. Payments (bribes) are common place. At the Nicoadala checkpoint you have to pay something to get through. It creates goodwill, and is part of living together. At Alfandega, you might want to pay 500 MTN ($20) to speed up the process. The Chinese pay no taxes or social security – it’s impossible to compete with them. We get taxed on everything – we cannot even discount our legitimate business expenses against our gross profit, because out in the bush, half the services come from the informal sector.

There appear to be only 4 concessions that are operating according to the intended regime, that is cutting timber with their own workforce, processing it in a proper sawmill, and exporting sawn timber or manufactured products – creating jobs and value addition. These are the long-standing companies in Zambézia: Madal, MAZA, DANMO TTC and Sociedade Moveis Licungo, In addition a few concessions and their associated sawmills are supplying processed timber and simple furniture exclusively into the local market. Even in these “managed” concessions, the basics of good management are still not followed. SPFFZ does not demand and operators do not work on planned annual cutting coupes. Even the best seem to rely on experienced tree spotters to tell them where to cut each year. So just as in 2004, there is no spatial control of timber harvest. The result, as mentioned above, is that while there may be timber remaining in Zambézia, but no one really knows where it is. Some operators believe it is increasingly likely to be too dispersed to exploit economically. What measures does the government take to address problems and promote sound concession management? The only action we heard of was a joint task force preparing to visit all concessions during June 2008 – to ensure they had installed their identification signboards. Instead, as Box 2 demonstrates, the government makes things more and more difficult for the few legitimate operators (see Box 2). When asked about concession management, the Director of DNTF, Raimundo Cossa admitted to us that there were a lot of problems with the concession system, particularly those contracted to the Asian operators. He said that

18

through a new Finnish project, they would establish an auction system for any concession over 30,000 ha, through new detailed inventory in each province to identify natural forest clusters appropriate for management. 4.5 Reforestation Reforestation is a big issue in the sector, but largely for the wrong reason. Operators pay an additional 15% of royalties for this purpose, but SPFFBZ does almost no replanting and certainly none in the actual concessions. In 2008, the Governor and DPA cited operational nurseries of native species as an indicator of improvement in forest management. Table 4 presents data on seedling production and reforestation for the last 8 years. This shows how attention to reforestation has see-sawed over the years – with the best performance in 2000, when the Italian NGO Nuovo Mundo was running community-based nursery projects. Furthermore, most of the reforestation has been casuarina along the beach in Zalala. The number of seedlings of native species produced was just 110 in 2006 and 400 in 2007. This is insignificant. At 4m x 4m spacing, it takes 650 seedlings to plant up a single hectare! The concessions are still not being replanted (or managed to promote natural regeneration), so the actual commercial forest estate remains unmanaged in any significant way. Concession operators are asking that the 15% be waived, and they should use the money saved to do their own replanting. For simple licence areas, the money could be used to fund communities to establish nurseries and do the planting. Table 4: Government reforestation efforts: nurseries, seedlings and areas forested, 2000-2007. Year No. Nurseries No. seedlings Area reforested (ha)

2000 2 + 31 450,000 190

2001 2 35,000 30

2002 2 64,000 20

2003 3 55,000 Not reported

2004 6 325,000 Not reported

2005 4 130,800 9

2006 4 33,400 6

2007 4 319,200 58

Source: SPFFB annual reports 4.6 The Permanent Forest Estate “Now all of Zambézia is concessions!” Map 2 shows why people think this. Yet, a permanent forest estate for Zambézia, based on sound participatory land use planning, still has not been thought about, let alone formally delimited. There are still only perfunctory efforts to control shifting cultivation and charcoal production. The only spatial control of concessions is provided by hand-drawn boundaries on

19

a topographic map in SPFFBZ (see figure 2), despite the availability of geographic information systems (GIS) facilities in the offices of the Provincial Services for Geography and Cadastre. There is still no cumulative, geographically referenced record of the species and volumes cut. No one knows how much timber remains, or where it is. 4.7 Community Concessions Since 2004, we have been arguing for communities’ rights to manage their own forests, as a basis for promoting rural development and the generation of real jobs. Since the Land Law does not give communities direct rights to the timber on their own lands, they need support to acquire their own commercial concessions through official channels. ORAM has been working with two communities Muzo (in Maganja da Costa) and Nipiodes (in Mocuba) since 2005. Their applications have been awaiting approval since early 2008. The Muzo application is being blocked at District level by a technicality, and the Nipiodes application, although supposedly supported by the Governor, has still not gone through. Conclusion: There are ten times more concessions than before, but forest management has actually only got worse. Meanwhile, short rotations and over-cutting are now institutionalised through the approval of 32 technically unsound management plans. Concessions were supposed to bring a degree of control of harvesting operations not possible under simple licence regime, but the concessions are now over-run by small operators, working the concessionaires’ licences, or other licences, or with no licences at all. SPFFBZ makes only ineffectual token gestures to controlling the concessions. Concessionaires are allowed to cut before establishing their industries. The only concessions that approach the intention on linking forest management with industrialisation and job creation, are the old Mozambican companies that have been operating for over a decade. None of the new much-vaunted international investment has resulted in anything of value! Neither the concessionaires nor the government do any replanting. In their efforts to develop themselves through forest management, communities continue to be thwarted and betrayed by their own government.

5 Forest Law Enforcement (Fiscalizacao) In 2004, forest law enforcement was ineffective and easily corruptible, but had admittedly improved considerably since the totally lawless days of the late 1990s. Computerised systems were in place to enable monitoring and control of licensing and harvesting and enforcement of the law, if the political and professional will existed. Here lay the problems. Many civil servants, politicians, party supporters and even military were illegally involved logging, and together with the Asian buyers and the forest services, constituted a timber mafia, that

20

was bypassing the control system and local industry, stripping the valuable timber from the forest and exporting raw logs to the hungry markets of China. In 2008, the Governor and DPA asserted that enforcement had improved greatly, citing particularly the increase in the number of checkpoints and improved relationship between communities and forest officers. The Acting Director of SPFFBZ also reported that he was not aware of any corruption amongst his staff – although in theory, he accepted that it might exist. We look first at the points raised by the Governor and DPA, and then some other key aspects of forest law enforcement, which they did not mention. 5.1 Checkpoints It is true that the number of checkpoints has increased. In 2004 there were three: Nicoadala, Port of Quelimane and Chimuara-Mopeia at the Zambezi River crossing. In 2008, two more inspection posts have been established at Lua Lua in Mopeia, and at Namacurra. In addition, the Nicoadala checkpoint has been fully refurbished. Mobile phones have greatly facilitated communication between field inspectors and headquarters, and amongst the forest officers themselves. However, what was not mentioned, was that one of most important checkpoints, the one in the Port of Quelimane, has been seriously downgraded. When the port was refurbished in 2005, SPFFB’s checkpoint there was demolished and has yet to be rebuilt. Where previously, facilities comprised a couple of air-conditioned rooms and computer terminals, their checkpoint now consists of a table beneath a tree beside the main gate. Rebuilding the checkpoint is the responsibility of the DPA, and “it is going to be done” (Chibite, pers comm.)11. While the number of checkpoints has increased, the number of staff appears to have decreased. Table 5 presents available data for 2001-2007. After the scandals of the late 1990s, staff numbers were built up from 6 to 31, and during the period of the Finnish funded MSRN project (2001-04), numbers were increased to a maximum of 34, because funds were available to employ staff on short contract. The number was increasing, donors were interested, and so this was reported. But since 2004, reporting on staff numbers has stopped. According to the Acting Head, there are now 28 staff in SPFFBZ12.

11

According to Cornelder, it is was actually their responsibility (Cornelder’s) to provide this

accommodation and in June 2008, a room was made available to SPFFBZ. It contains one desk and two

chairs, but no computers. A most rent is charged, but it includes all utilities. 12

In early 2009, the DPA proposed to increase the number to 106. Industrial operators complained

that it was not so much the number of inspectors, but their training, professionalism and honesty that was

important!

21

At any rate, the number of checkpoints does not equate with law enforcement, and based on previous performance, new checkpoints simply result in new rent-seeking. For instance, despite the new inspection posts and improved communication, a lot of illegal umbila, chanfuta and jambire is still leaving the province southwards, over the Zambezi River to the local markets in Beira. The regulations have even been loosened to accommodate this. In the past, to move timber between provinces, the local transport permit had to be submitted, and a special transit permit obtained. Now, the local permit is sufficient. 5.2 Cooperation with local communities SPFFBZ and the DPA reported good cooperation between communities and the forest officers; communities inform the authorities about infractions, and the forest officers respond quickly. Both officers and communities should share in proceeds from the fine. However, when pressed, SPFFBZ could only cite one case where this had happened, in Muzo. The lack of cases, they said, was an indication of how good law enforcement was. The community in Muzo has an interesting account of this case. They are particularly focused on forest law enforcement because they have an application for a community concession and thus an economic asset to protect. Community members found 2 Asian loggers with a truck load of pau ferro in their forest. They called the local forestry office and someone came and took the documents of the truck. The officer told them later that the offenders had paid a fine. When the community asked for their 20% of the value of the fine, they were told that it had gone to government. In a second case, they found chain sawyers at work in their proposed concession. They seized the saw, but it turned out to belong to the District Director of Agriculture (DDA) of Mocuba. Forestry officer came and took it, and they heard nothing more. The same DDA was also caught hunting kudu. The community wrote asking about the outcome of these three cases. The only reply was from the DDA, about the hunting, explaining that they were “controlling the population”. 5.3 SPFFBZ computerised data base Data handling is key to effective regulation and law enforcement, In 2003 and 2004 a computerised database was maintained of each operator’s quota, all their cutting licences, transport permits and the volumes brought into town through the Nicoadala checkpoint13. Another database was kept on infractions. The Acting Head of SPFFBZ told us that the system developed problems in 2005 and has not been used since. In 2008, SPFFBZ staff were experimenting with a new computerised system, but for the time being, we were told, only paper records are kept and we were denied

13

At that time licences were issued for each species, and operators could pay for cutting licences in

stages until they had reached their entire quota.

22

access to them. The new system was indeed impressive14, enabling profiles of individual operators to be produced, as well as summaries of quotas and licences15. Although computerised systems are open to abuse, and in 2004 there was clear evidence of this abuse, they at least offer the possibility of good control. Control could be strengthened by linking the database to a system for printing out the licences, so the data from each licence issued is automatically entered into the database. 5.4 Infractions: Official accounts We were not allowed access to SPFFBZ records on infractions – the only information available was from the annual reports, summarised in Table 5, and an interview with the Acting Head of SPFFBZ, Eng Chibite, summarise in Box 3. Table 5: Forest law enforcement in Zambézia: Staff numbers, infractions, products seized and total fines, 2001-2007 Year No. staff No. Infractions Products seized Total fines (MTN)

2000 6 37 Logs 88,177

2001 31 96 Not reported 315,451

2002 31 220 Not reported 1,807,041

2003 34 Not reported Not reported 795.828

2004 Not reported 267 1,116,842

2005 Not reported 300 1182 m3 logs

8 m3 sawn timber

3,955,352

2006 Not reported 169 1.898.471

2007 Not reported (28)

177 143 m3 logs

63 m3 sawn timber

1.245.081

Source: SPFFBZ annual reports

The year 2000 represented a turning point. Although total fines were relatively low, only 88,177 MTN, they represented a 96% increase on 1999 – the height of the chaos. In 2005, detected transgressions rose to a maximum of 300, consisting of: 1% cutting during the rainy season, 9% cutting outside the designated area, 15% incorrectly completed transport permit, 5% cutting without a licence and 70% cutting and transporting more than 10% in excess of authorised volume. The latter infraction is consistently reported as the most frequent, but no special analysis is made and no particular strategy is ever proposed for addressing it. In 2003 and 2004, SPFFBZ reported that in response to an “avalanche of transgressions” the DPA had joined forces with the provincial police and the

14

Interestingly, the demonstration given used the data of one of the industrial operators. Although

these companies are the ones actually making the greatest investment in the sector and the greatest

contribution to provincial employment and economy, they are the ones most closely policed by SPFFB. 15

According to SPFFBZ, it is now ready to be used in the 2009 campaign, but with the economic

crisis, no one is buying licences.

23

professional associations to form a Timber Commission and created joint mobile enforcement teams constituted of forest officers and police (SPFFBZ annual report 2004). No details were ever given of this team’s activities, and it is not mentioned again in subsequent reports16. Interestingly, there are no reports of arrests, trials and convictions. It appears that in most cases people are simply fined, to transgress again. But one informant commented:

“there are always a few cases each year, of people being arrested and punished. If you are well connected and someone acts illegally to hurt your interests, the authorities will act. It’s a win-win situation: good for the statistics and good for relationships. If you’re not well connected, don’t expect results. You might get a response from SPFFB, but typically, it’s too little and too late. Since one has to pay the expenses for their field inspection, it is in the interests of officers to go, but by turning up late enough to ensure evidence has disappeared, it need not disrupt the system. It’s also win-win. Good for statistics and not damaging to key relationships.”

Data on infractions are actually a poor indicator of the quality of law enforcement, quite apart from frequent inaccuracies. When the number of infractions increases, the government explains it as improved detection; if the number decreases, they explain it as improved governance in the sector. “Win-win” reporting.

16

Experience in Cabo Delgado shows that multi-sectoral enforcement teams can be effective. In

2007, officers from customs, DPA, police and labour with NGO observers carried out a day of raids on

sawmills, logyards and exporting companies, finding a lot of illegal logs and illegal Chinese workers.

Unfortunately, under political pressure from Maputo, the team was disbanded and the fines were annulled.

24

Box 3: Comments on Law Enforcement by Acting Head of SPFFBZ, Eng Chibite Illegal operators “furtivos” do exist. Cutting in the wrong area also takes place – but some of this – say 20 -25% - is just accidental crossing over into a neighbouring area. SPFFBZ hasn’t licensed any new operators in since 2003. What’s happening, is that some of these experienced operators sell on to cowboys. This is illegal, but it’s a fine line between this, and sub-contracting, which isn’t necessarily illegal. Overcutting is difficult to control. An operator might get 200 m3 for a year, but his team just keeps cutting. Often, the unlicensed timber remains abandoned in the forest, because there’s no licence to get it through the checkpoint and into town. SPFFB is controlling the situation as best it can. Corruption is debatable. Sad to say, but it is real. That said, he admits no direct personal knowledge of corruption. Officers should not be suspected just because they appear to have lots of expensive things. Most are obtained honestly, from savings for instance. It is important that get the facts and analyse them first, and not jump to conclusions. Regarding the 30 containers seized in Quelimane: Well, “stealing is stealing” it happens. Timber gets sold in public autions, overseen by GIP (Gabinete de investimento da provincial; Provincial Investment Office) Illegal export is happening, just like before (2004). At the moment, no proper SPFFB post exists in the port. Officers just have a desk under a tree by the main gate. DPA is going to provide a proper checkpoint building soon. Forest law enforcement is not just about giving fines – in fact, if its going well, then the number of fines should decrease! And that’s what we are seeing. Coordination is much better, and since the advent of the 20%, communities are sensitized for conservation and good management.

5.5 Auction of illegal timber In 2005 and 2007, SPFFBZ reported on its seizure of illegal products. One has to conclude that this is primarily for cosmetic purposes – as it has little effect on illegal activity. The logs are eventually auctioned off, with great publicity, but usually the previous owner is allowed to buy them back at a knock-down price and then can export them as usual. It’s an unspoken agreement amongst operators - like “honour amongst thieves”. So, the seizure just an inconvenience and additional expense.

25

Photo 2: Notice of public auction of seized timber: starting price of around $100/m3, about 1/3 of the local market value of the timber.

5.6 Infractions: unofficial accounts and local opinion on forest law enforcement and corruption Operators, communities and NGOs we spoke with were almost unanimous that law enforcement and corruption had got much worse in the last four years, not just in Zambézia, but across the country. An illegal logger told us about his operations (Box 4).

In Gile, a northern district bordering Nampula, one foreign-owned company, Green Timber, was found to have actually constructed a bridge across the Ligonha River into the neighbouring province of Nampula, to enable them to take their timber out through Nacala. The port here is famous amongst the Chinese, for being the most relaxed in Mozambique, where Customs and the DPA are most interested in taking bribes.

Licuari (between the SPFFBZ check points of Nicoadala and Chimuru) is a well known collection point for illegal timber in Zambézia. Small trucks collect timber from communities and furtivos, and move it at night. We found it easily, and a large truck piled with logs drove out as we drove in (Photo 3). The man running the site buys and sells species for local market, primarily chanfuta and umbila. He buys for around 2000 MTN/ m3delivered, from unlicensed operators and sells on at 4000MTN/ m3 and 8000/m3 in Maputo. He sells mostly to truckers who have brought goods from Maputo and want to avoid returning south empty. He estimated that 50% of timber harvested in Zambézia is illegal.

26

Photo 3: Truck loaded with chanfuta timber, leaving the illegal trade point in Licuari

“Corruption in all sectors is now much worse”, an industrial operator told us. “There is a chain of corruption. At Ministerial level, you get money by approving big concessions. At DNFFB, you get money by changing regulations. At the provincial level you get money from simple licences, and the Asian operators.”

“In Zambézia any improvement in forest management is going to be difficult, because senior provincial officers are not interested. In fact the day things improve, they and the people they protects are going to lose the opportunity to do their business. There’s a lot of political protection; that’s why they are so arrogant.”

“Corruption in Zambézia’s timber business runs from selling a simple log to money laundering, including trafficking and marketing of hard drugs.”

“Everyone knows the previous Head of Law Enforcement (Nemane) in SPFFBZ was on the take. And his brother is one of the biggest illegal loggers in the province!”

Most sobering, we were told: “FRELIMO has a big responsibility in all this, and we “sinned” a lot in this regard. We advised the party not to get involved in this scenario, but unfortunately, the interest in easy accumulation of wealth and greed drove us into it. Now, its going to be

27

very difficult to reverse the scenario, because foreigners, mostly the Chinese, already dominate in our country, including the borders, with economic power growing every day, which enables them anytime and place, to bribe any miserably paid government officer, to facilitate the documentation they need to export timber in any form from any place, without any problem.”

Box 4: Story of a “Furtivo” Lots of communities cut timber. A regulo (traditional village leader) might demand up to 1500 MTNfor access to his community. Then, he buys mondzo for about 250 MTN($10) per log, and arranges the collection and loading. Tractors cost 500 MT/day, for 3 days; loading costs 250 MT/person for 12 people, or 3000 MTN per truck holding 15 m

3. A “fuso” truck takes 2 days and

52,000 MTN to get to Quelimane (from a point 350 km away). He has to acquire a licence. This is often done by taking over someone else’s licence and splitting the profits with them. This way, he might earn 5000 MTN($200) per load, but also might lose everything. You can also work without a licence and transport permit, but sometimes you have to pay half the value of the load to get through Nicoadala. You have to call ahead and arrange it. Only well known people can pass without licences. Chinese then discount $10/ m

3 for

buying illegal wood. Usually, the licence holder goes to the Chinese to sell – so he can lie about how much he was paid. Sometimes trucks with illegal load travel in convoy with trucks with legal loads. Those with all the proper documentation lead the way, but report to trucks behind. If the inspection is serious, the following trucks may leave the road and wait until after dark to continue their transit.

Conclusion: It is simplistic in the extreme to equate an increase in the number of checkpoints or forest guards with improved forest law enforcement. The reality is that corruption, arrogance and mismanagement continue and are seriously undermining the rule of law, accountability of government and future of the forest sector.

6 “The 20%” In 2004, there was a lot of discussion about “the 20%” of timber licence fees that the communities were entitled to receive under the Forestry and Wildlife Law of 199917. The government had been criticised for delays in passing the necessary regulations to enable implementation, and for failure to reserve the funds for communities from the years before regulation was passed. In May 2005, Diploma Ministerial No. 93/05, establishing mechanisms to channel these revenues to communities in logging areas, was passed, and

17

Other community entitlements under the law included: subsistence level use of the resources;

participation in co-management; community consultation and approval prior to awarding licenses to

operators; development benefits derived from exploitation under a concession regime; and 50% of the

value of fines awarded to persons contributing to law enforcement.

28

SPFFBZ began implementation. With funding from various donors, they eventually appointed a local NGO, RADEZA (Network of Organisations for the Environment and Sustainable Community Development of Zambézia) to do most the work with the communities18, and dissemination of the law started in late 2005. By 2008, there had been three rounds of delivery of the 20% to communities. Table 6 summarises the progress. In 2005, most provinces had not been yet able to deliver the money, mostly because of the failure to establish required Village Management Committees (Comites de Gestao) and open bank accounts. In Zambézia, this amounted to 7,380,317 MTN (US$307,000), intended for 166 communities in 12 districts. The money went into general budget of districts instead, and it’s unclear what happened to it. Table 6: Progress on Distribution of the 20% to communities in Zambézia, 2005-2008 Year Districts Communities Committees Total MTN

2005 - - - 7,830,317

2006 5 ? 1,561.929

2007 ? 91 37 5,799,964

2008 8 168 40 ??

In 2006, a faltering start was made, with 1,561,929 MTN delivered to an unrecorded number of communities in 5 districts (Mocuba, Namarroi, Maganja da Costa, Mopeia and Ile). Momentum picked up in 2007, when 5,799,964 MTN from the 2006 campaign channelled to 91 communities in 37 committees.

In 2008, money from the 2007 campaign was being prepared for delivery to 168 communities in 8 districts. Of these, 98 communities are in simple licence areas and 70 in concessions. Individual communities are set to receive between 11,500 (US$540) and 450,000 MTN(US$18,750). This implementation does represent a vast improvement over the situation in 2004. However, there have been problems, policy disputes and irregularities in implementation which need to be resolved, and from which lessons can be learned for future implementation.

18

This involved: i) dissemination of the regulation and coordination with partners (NGO, private

sector and government offices); ii) calculation of the value of the 20% for 2005; iii) inventory of

beneficiary districts and communities; iv) opening Community Funds to receive the 20% ; v) instructing

the Agrarian Promotion Fund (Fundo de Fomento Agraria) to transfer the money; vi) support for the

formation of local committees to manage the funds and opening bank accounts; and vii) official opening

ceremonies for the first delivery of the 20%

29

6.1 Problems Identification of communities When implementation began, the chaotic state of the sector immediately became apparent. With simple licences, it should be easy to identify communities entitled to get 20% under the simple licence regime, because the licence covers a relatively small area (5000 ha). But the fact is that SPFFBZ licensing and supervision have been so irresponsible, that a licence is issued for one place, but cutting often, perhaps usually, takes place somewhere else. So, some communities get the 20% when none of their timber has been removed, and some communities see their forests logged, but get no share of the royalties (see Box 5). Concessions are much larger and more problematic. They often include numerous communities, and the only practical approach is to share equally amongst all of them, reducing the sums received by each even further. If concessionaires operated annual felling coupes, as they are supposed to, individual communities would be more easily defined. Receiving organisation for the 20% In Zambézia, the 20% funds have been delivered not to Village Management Committees, but to the administrative level higher up – the Administrative Post (Posto Administrativo– local government level below the district), and its Community Council (Conselho Comunitario). Furthermore, 11 of the 37 Administrative Posts have had their bank accounts opened in Quelimane, making them expensive and time consuming to access. These have caused a lot of complaints to the NGO implementing the community support programme, RADEZA. One community complained about the practice promoted by RADEZA of forming committees at the level of the Administrative Posts. There were lots of problems with transport to get to committee meetings, and with communication between the five communities involved, and with the Administrator. Each community was supposed to plan its activities. There was only one training from RADEZA, and no follow up until the centralised “evaluation”. The DDA helped them form their committee. RADEZA defend their approach, with the fallacious argument that banks do not like to open lots of little accounts for individual communities. They also argued that it would enable other communities in the area to benefit. After all why should 20% only go to the communities close to the forest, and not to the whole Administrative Post, especially, if loggers have cleaned out some local forests before the 20% was implemented? Director DNTF admitted that it had been “uma confusao” (“a confusion”) that the money had gone to Administrative Posts, rather than directly to the communities. He assured us that the law will be changed to clarify this.

30

Meanwhile, the NGO ORAM Zambézia has an alternative vision: the 20% should be used as an incentive for rational use, so it needs to be delivered as close to forest as possible – ie to the communities. They argue that committees at the level of the administrative posts will only required if the community level committees want to form one. Banks are in the business of opening accounts so there should be no problem with multiple accounts19. ORAM’s work in supporting 3 communities to manage their 20% is described below. 6.2 Irregularities Transparency The manner in which the 20% entitlement is determined is not transparent. SPFFBZ has simply announced who gets what, without showing how the figures were reached. At the beginning of the logging campaign, SPFFBZ know which operators have been licensed for what species and volumes. All this information and the final calculation should be told to the communities before cutting begins. Communities are beginning to realise that illegal logging deprives them of their 20%, and so knowledge about licensing can be an effective tool for empowering communities to monitor timber extraction in their area. ORAM has been doing community training on timber identification and measurement, so the communities can control operations. Some communities said by SPFFB to have received the 20% never receiving anything: need for greater transparency and accountability. One community was told their 20% was coming in the form of a maize mill. They never saw an invoice showing the value, and the thing came in pieces – never was assembled properly. Use of the 20% Communities receive very little support in deciding how to use their 20% and manage the funds and projects. Apparently, most communities buy maize processing mills or rehabilitate small infrastructure – bridges, etc. In some places, however, communities are being encouraged to propose building schools and health posts, and this has caused some disagreement. The government has introduced a local investment fund (Orcamento de Initiativos de Investimento Local (OIIL)) through which 7 million MTN is given annually to every district in the country, to build schools, roads, etc. The use of the 20% in this way is said to cover up the mismanagement and political abuse of the fund. Conclusion: While delivery of the 20% is definitely an improvement over 2004, there is still a long way to go with its implementation and the use of the funds by communities. There is an excellent opportunity to use the 20% to leverage better forest governance, and better community development, as ORAM is promoting. SPFFBZ must now improve its licensing and supervision. It must ensure the areas licensed actually have sufficient forest resources, that the

19

In Manica and Sofala (perhaps everywhere) a bigger problem is the charges the banks make on

community accounts. Concessional rates need to be negotiated.

31

person licensed does the logging, that logging is done in the correct place, the correct volumes are taken, and that communities get the full value of their 20%. The 20% is in danger of becoming more of a distraction than a benefit! Its value is actually quite low (less than 5% of the total value of the timber) but it has consumed nearly 100% of the forestry debate, to the neglect of many other important issues notably communities’ land and other rights, and the continued chaos in the forest sector. Attention should also focus on using the 20% to leverage better forest governance.

Box 5: A Community’s experience of logging and the 20%: Bive/Makwia Five different loggers have been operating here over the last 6 years. An operator called Pinto was in here late last year cutting pau preto. Only the loggers Dominga and Nelson consulted with our community. They brought us food, some beer, and gave 300 MTN to the regulo (chief). We didn’t ask for anything – we didn’t realise we could. Most labourers were brought in from outside. Only 3 or 4 people from here got jobs. Nelson gave us a maize mill in 2007, because he’d been working here for 4 years. We’ve never heard about the 20% and certainly haven’t received it. We have heard about the Local Initiative Investment Fund, and a meeting was called by the chief to form an association to receive and manage the funds. We have a committee of 10 men and women. We opened a bank account. We were asked if we wanted money or goats. But nothing has happened. We also cut timber. In 2005-07 maybe we cut 120 logs a year. A team of 8 men cut around 6 trees a day, using hand saws. We should get 100 MTN ($4)/tree, but sometimes we didn’t get paid. The furtivos (illegal loggers) said the Chinese hadn’t paid them. Some of our people also work loading trucks. A team of twelve used to get paid 25 MTN per person per truck load. Now its 50 MTN. Often, we cut trees and look for the market afterwards. Concessions are no guarantee of fair employment for locals. One concessionaire gave part of his concession to another operator, who cuts one month in a place and then moves on, without paying anyone.

7 In-country processing, industrial capacity and employment In 2004, despite the 1999 legislation to the contrary, nearly all Zambézia’s timber was being exported as logs. This was justified, on the grounds that Zambézia lacked industrial capacity, particularly to process hard tropical timbers. We argued strongly Zambézia does have the necessary capacity, and called for full implementation of the laws requiring prior in-country processing, as an essential step towards fulfilling government policy to harness the forest sector and the skills and energies of the people to promote inward industrialisation and create jobs. At that time, regulations were being manipulated to avoid fully implementing the law and to allow the export of logs (and effectively jobs) to the Chinese market to continue. Because the law permits the export of logs of species classified as

32

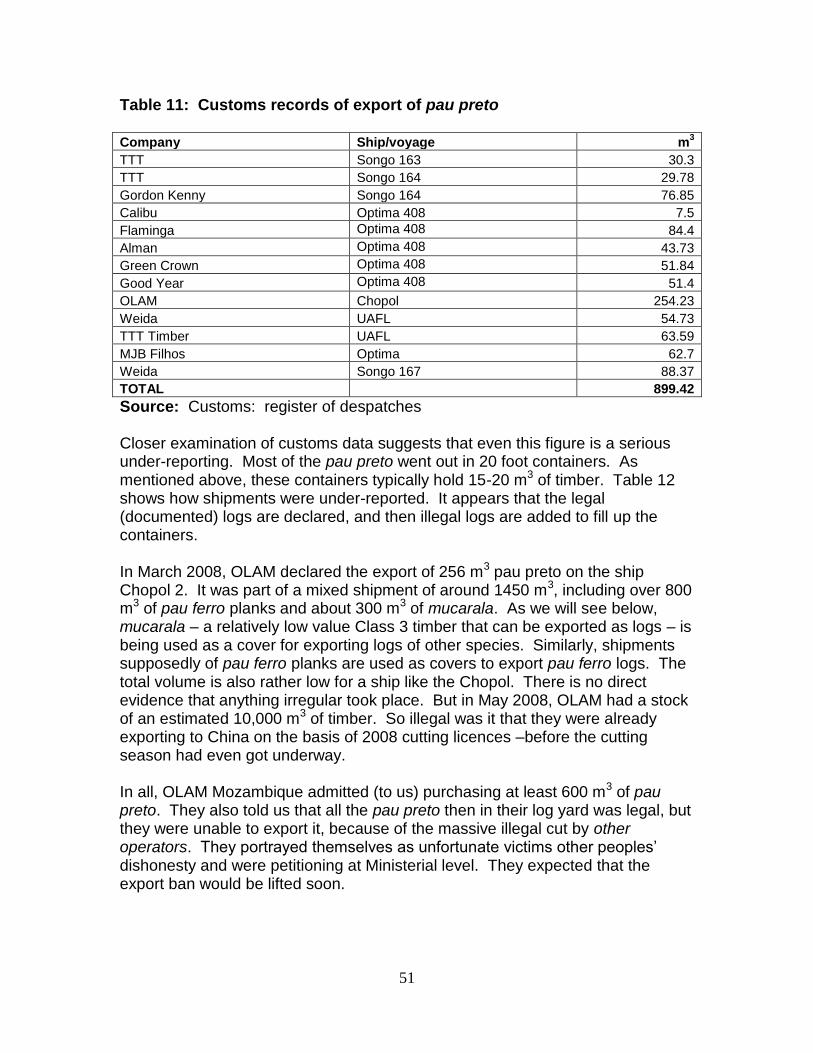

“precious”, the Ministry issued various decrees reclassifying most of the main commercial species as such. In 2005, the regulation enabling the export of logs of umbila, jambire and chanfuta expired, and from April that year in-country processing was supposed to be enforced. However, manipulation of the regulations began again. First, export of logs continued to be allowed on the grounds that they had been felled under licences from 2003 and 2004. Sawing began in July 2005, but operators did not respect the industrial norms for thickness and proper squaring up (“4x4 finishing”) so, processing standards had to be officially established through Ministerial Diploma (185/2005), to prevent the export of rough sawn timber. The export of these species then fell substantially, but has continued. In January 2007 a Ministerial Diploma, reversed the 2003 reclassification of the two most sought-after species, pau ferro and mondzo, into precious class, which had enabled their export as logs, and these species were returned to Class 120. This resulted in a 75% reduction in their royalties, but required that they be processed before export. However, SPFFBZ allowed export to continue until 31 March, as before, on the basis that these were logs from 2006. And then they extended deadline until 31 May and then extended it again to 31 June. The influential firms, OLAM and Green Crown, continued to export logs in August, September and October 2007, amounting to an officially declared volume of over 3,000 m3. When asked, DPA claimed these were old logs and authorised their export, but when Green Crown’s shipment was inspected, a lot of fresh logs were found mixed in with relatively few old ones. Since Green Crown is well-connected, political pressure was applied through Bonifacio Grueveta, and it was allowed out. Then, because the Chinese market supposedly would not accept fully processed timber, (and certain operators’ sawmills were not capable of sawing to specification), the Asian lobby put pressure on the government in Maputo and in September 2007, got another Diploma published, which changed the sawing requirements to permit the export of slabs of rough cut timber, known as “pranchas” (rough sawn planks) (see Photo 4), instead of fully squared (4x4 finished) . In 2007, 1980 m3 (28%) of total exports were in the form of such planks, 780 m3 (11% of all exports) of this pau ferro.

20

In the same regulation, muaga and chanato, previously Class 3 and 4 respectively, were elevated

to Class 1, raising their royalties and also introducing the processing requirement.

33

Photo 4: “Sawn timber” of pau ferro en route to Quelimane port

From mid-June 2007, most exporters were obliged to export sawn timber. Figure 1 provides customs data for the four quarters of 2007, demonstrating the impact of this. In anticipation of the crack-down, a record 40,000 m3 of logs left Quelimane in the first half of the year. In the second half of the year, almost none were exported. Many exporters, rather than sawing and exporting, simply stored their logs in their log-yards, figuring that the government would soon be persuaded to allow log exports to start again. Log-yards of companies like Madeiras Alman and OLAM filled to overflowing.

34

Figure 1: Export of logs and sawn timber from Quelimane in four quarters of 2007