trusts and estates are not entities conduit theory of...

TRANSCRIPT

7/13/2015

1

MICKEY R. DAVISDAVIS & WILLMS, PLLC

HOUSTON, TEXASJULY 13, 2015

Trustsandestatesarenotentities◦ Taxlawstreatthemasthoughtheywere◦ RulesapplicabletoindividualsapplytotrustsandestatesexceptperSubchapterJ

Conduittheoryoftaxation:◦ Trustsandestatespaytaxonincometheyretain

◦ Theyreceive"distributiondeduction"fortaxableincomedistributedtobeneficiaries

◦ Beneficiariespaytaxondistributedincome◦ Characterremainsunchanged

© Davis & Willms, PLLC, 2015 2

7/13/2015

2

1. Simplevs.complextrusts,andestates2. Thecarry‐outof"distributablenetincome"3. Thecharitablededuction4. Thedeductibilityofinterestondeferredgifts5. Thetreatmentoftrustandestatenetlosses6. Recognitionofgainbyestatesandtrustswhen

appreciatedassetsaredistributed7. RecognitionofGainbybeneficiariesfrom

unauthorizednon‐proratadistributionsofassets8. “Incomeinrespectofadecedent"9. Thedeductibilityofadministrationexpensesfor

incomevs.estatetaxpurposes10. Thegrantortrustrules

© Davis & Willms, PLLC, 2015 3

Simpletrust:◦ Mustberequiredtodistributeall(fiduciaryaccounting)incomeatleastannually

◦ Nodistributionstocharities◦ Nocurrentdistributionsinexcessofincome

Truststhatarenotsimplearecomplex

Estatesaretaxedlikecomplextrusts

© Davis & Willms, PLLC, 2015 4

1

7/13/2015

3

Simpletrustsdeductamountsrequiredtobedistributed annually◦ Beneficiariesmustreportincomeinyearrequiredtobedistributed

◦ Characterofamountscarryouttobeneficiaries◦ Allowanceinlieuofpersonalexemption:$300

Estatesandcomplextrustdeductamountsrequiredorpermittedtobedistributed◦ Required(TierI)distributionscarryoutincomefirst◦ Permitted(TierII)distributionscarryoutanyremainingincometoextentofactualdistributions◦ Complextrustsallowance:$100;estates:$600

© Davis & Willms, PLLC, 2015 5

1

GeneralRule:Aninheritanceisincome‐taxfree Exception:Beneficiariespaytaxonreceiptof"DNI" "DNI"isafundamentalconceptinSubchapterJ Usedtoprovideroughadjustmenttoconformnotionsoftaxableandfiduciaryaccountingincome

DNI=Taxableincome(beforeanydistributiondeductionorallowanceinlieuofpersonalexemption)◦ Lessnetcapitalgains◦ Plusnetexemptincome

© Davis & Willms, PLLC, 2015 6

2

7/13/2015

4

DNImeasuresamountsandtypesoftrustorestateincome

DistributionsaregenerallytreatedascomingfirstfromDNI,thenfromcorpus

DistributionstomultiplebeneficiariesgenerallycarryoutDNIprorata

EstatesandtrustsgettodeductamountoftaxableDNIdistributed(orrequiredtobedistributed)

Beneficiariesreportcorrespondingamountinincome

Distributionsaretreatedasthoughmadeonthelastdayoftheentity'staxyear◦ Estatesandcomplextrustscanelecttoapply"65‐dayrule"

© Davis & Willms, PLLC, 2015 7

2

AandBarebeneficiariesof$1,000,000estate Executordistributes$200,000toA,$50,000toB Duringsameyear,estateearnsincomeof$100,000:◦ Amustreportincomeof$80,000 $100,000x($200,000/$250,000)◦ Bmustreportincomeof$20,000 $100,000x($50,000/$250,000)◦ Estategetsadistributiondeductionof$100,000

Ifdistributionswere$50,000toAand$25,000toB:◦ Awouldreportincomeof$50,000◦ Bwouldreportincomeof$25,000◦ Estatewouldreceive$75,000distributiondeduction◦ Estatewouldreportremaining$25,000asincomeontheestate'sincometaxreturn

© Davis & Willms, PLLC, 2015 8

2

7/13/2015

5

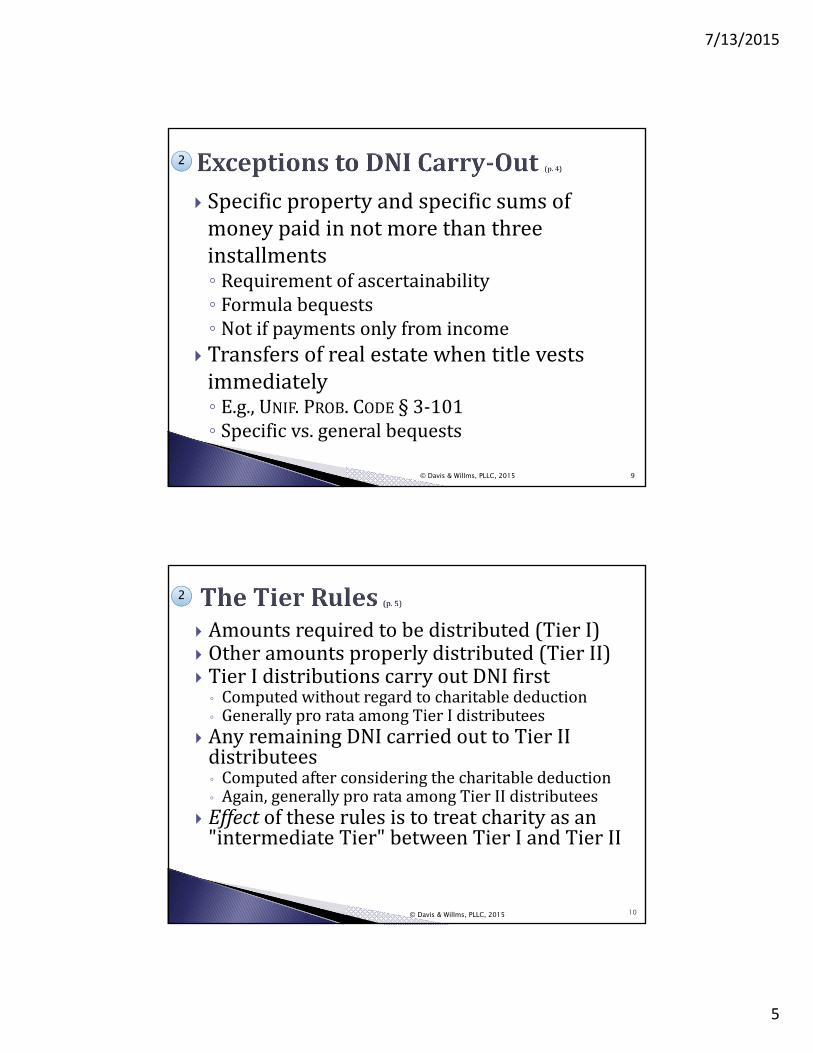

Specificpropertyandspecificsumsofmoneypaidinnotmorethanthreeinstallments◦ Requirementofascertainability◦ Formulabequests◦ Notifpaymentsonlyfromincome

Transfersofrealestatewhentitlevestsimmediately◦ E.g.,UNIF.PROB.CODE § 3‐101◦ Specificvs.generalbequests

© Davis & Willms, PLLC, 2015 9

2

Amountsrequiredtobedistributed(TierI) Otheramountsproperlydistributed(TierII) TierIdistributionscarryoutDNIfirst◦ Computedwithoutregardtocharitablededuction◦ GenerallyprorataamongTierIdistributees

AnyremainingDNIcarriedouttoTierIIdistributees◦ Computedafterconsideringthecharitablededuction◦ Again,generallyprorataamongTierIIdistributees

Effect oftheserulesistotreatcharityasan"intermediateTier"betweenTierIandTierII

2

© Davis & Willms, PLLC, 2015 10

7/13/2015

6

Generalrule:DNIgetscarriedouttomultiplebeneficiaries(withineachtier,ifany)prorata

Exception:SeparateSharetreatmentappliesWhen the governing instrument of the trust or estate (e.g., the trustagreement, the will, or applicable local law) creates separate economicinterests in one beneficiary or class of beneficiaries such that theeconomic interests of those beneficiaries (e.g., rights to income orgains from specific items of property) are not affected by economicinterests accruing to another separate beneficiary or class ofbeneficiaries

AppliessolelyforallocatingDNIDNIallocatedbaseduponbeneficiaries'respectiveeconomicshares

2

© Davis & Willms, PLLC, 2015 11

WillbequeathsIBMstocktoXandthebalanceoftheestatetoY

IBMstockpays$20,000ofpost‐deathdividendstowhichXisentitledunderlocallaw.Nootherincome

Executordistributes$20,000toXand$20,000toY Pre‐separatesharerule:DNIcarriedoutprorata(i.e.,$10,000toXand$10,000toY)

ButXhaseconomicinterestindividends;Ydoesnot SeparateShareRules:Distributionof$20,000toXcarriesoutalloftheDNItoX.NoDNIiscarriedouttoY

© Davis & Willms, PLLC, 2015 12

2

7/13/2015

7

Incomefrompropertyspecificallybequeathed◦ E.g.,Unif.Prin.&Inc.Act§ 201(1)◦ Beforeseparatesharerules,proratarulescausemismatchbetweeneconomicbenefitsandtaxrules

Interestonpecuniarybequests◦ E.g.,Unif.Prin.&Inc.Act§ 201(3) Interestpaymentsarenot"distributions"carryingoutDNI

Interestexpensetoestateortrust

Interestincometobeneficiary

2

© Davis & Willms, PLLC, 2015 13

Distributionstocharitiesdon'tcarryoutDNI◦ Charityas"intermediatetier"isafictiondescribingeffectoftierrules

Instead,trustsandestatesgetcharitabledeductions◦ Availableforamountsofgrossincomepaidtocharities

◦ Estates(andpre‐'69trusts)candeductamounts"setaside"forcharity

Mayelectone‐year"look‐back" Notlimitedtoapercentageof"AGI"likeindividuals

3

© Davis & Willms, PLLC, 2015 14

7/13/2015

8

Interestonpecuniarybequests◦ E.g.,Unif.Prin.&Inc.Act§ 201(3)◦ Interestpaymentsarenot"distributions"carryingoutDNI

◦ Interestincometobeneficiary◦ Interestexpensetoestateortrust

Taxableasinterestincometobeneficiary "Personalinterest"isnotdeductible "Investmentinterest"canbededucted◦ Investmentinterestargument◦ Cf.Treas.Reg.§ 1.663(c)‐5,Ex.7

4

© Davis & Willms, PLLC, 2015 15

Ifestateortrustdeductionsexceedincome:◦ Excessdeductionscan'tnormallybecarriedbackorforward◦ Exceptionfornetoperatinglosses NOLscanbecarriedback2yearsandforward20years◦ Exceptionfornetcapitallosses Non‐corporatetaxpayerscancarryforwardcapitallossesindefinitely

Specialruleinyearofestateortrusttermination◦ Excessdeductionscarriedouttobeneficiaries◦ Itemizeddeductionstobeneficiariesinyearentityterminates◦ Deductiblebybeneficiariesthatsufferloss

© Davis & Willms, PLLC, 2015 16

5

7/13/2015

9

DistributionsofassetscarryoutDNI(unlessageneralDNIexceptionapplies)

Amountdistributedislesserofasset'sfairmarketvalueorbasis(plusanygainrecognizedondistribution)

Distributionofappreciatedpropertysatisfyingbequestof"specificdollaramount"causesestateortrusttorecognizegains

"Specificdollaramount"notthesameas"specificsumofmoney"—mostformulabequestscauserecognition

© Davis & Willms, PLLC, 2015 17

6

Executormayelect torecognizegainsondistributions◦ All‐or‐nothingelection;IRC§ 643(e)

Reasonforelection‐‐Example:◦ Dateofdeath:estateworth$1.8million◦ Stocks:$1.1million;Bonds:$700,000◦ Dateofdistribution:estateworth$2.1million◦ Stocks:$1.4million;Bonds:$700,000◦ Estatedividedamongthreekids—allbondstoone

Lossesgenerallynotrecognizedduetorelatedpartyrules

Exception:estatesfundingpecuniarybequests

© Davis & Willms, PLLC, 2015 18

6

7/13/2015

10

Formulagiftrequiresexecutortodistribute$400,000worthofproperty

Executorproperlyfundsbequestwithassetsworth$400,000atdateofdistribution

Date‐of‐deathvalue(andthereforecostbasis)ofassetofonly$380,000

Estaterecognizesa$20,000gain

© Davis & Willms, PLLC, 2015 19

6

Generallynogainorlossrecognizedbybeneficiariesasaresultoftrustorestatedistributions

Exceptionforunauthorized non‐pro‐ratadistribution

Wheretofindauthority:◦ Statelaw◦ Languageinthegoverninginstrument

© Davis & Willms, PLLC, 2015 20

7

7/13/2015

11

EstatepassesequallytoAandB Twoassets:stock&farm,eachworth$120,000 Dateofdeathvalues(equalsbasis):◦ Stock:$100,000;Farm:$110,000

ExecutorgivesstocktoAandfarmtoB NeitherWillnorlocallawauthorizesnon‐proratadistributions

IRS: AandBeachreceivedone‐halfofeachasset◦ A"sold"herinterestinfarm(basisof$55,000)forstockworth$60,000:$5,000gaintoA.◦ B"sold"hisinterestinstock(basisof$50,000)foraone‐halfinterestinfarmworth$60,000:$10,000gaintoB

BothAandBare"disappointed"

© Davis & Willms, PLLC, 2015 21

7

GeneralRule:Aninheritanceisincome‐taxfree

Exception:IncomeinRespectofaDecedent◦ Income"earned"bythedecedentbutnotproperlyreportedbyhimorher

Decedententeredintolegallysignificanttransaction

Decedentperformedsubstantivetasksrequired

Noeconomicallysignificantcontingencies

Decedentwouldhavereceivedpropertybutfordeath

MajorsourcesofIRD:◦ Retirementaccounts

◦ Installmentgainobligations

© Davis & Willms, PLLC, 2015 22

8

7/13/2015

12

Generalrule:Gainrecognizedwhenpaymentisactuallyreceived

DistributionofrighttoreceiveIRDtypicallydoesnotacceleraterecognition◦ SpecificbequestofIRDasset◦ ResiduarydispositionofIRDasset

IRDrecognitionwillbeacceleratedifestateortrustdistributesassetinmannergenerallycausinggainrecognition(SeeRule6)◦ Distributionsinsatisfactionofpecuniarybequest◦ Executormakes§ 643(e)electiontorecognizegain

© Davis & Willms, PLLC, 2015 23

8

Xdieswith$8,430,000estateWillmakesformulamaritalgiftof$3,000,000tospouse,leavingtheresttoX'skids

IRDassetworth$3,000,000(butwithbasisof$0)isusedtofundmaritalgift

NOstep‐upinbasisforIRDassets Estaterecognizes$3,000,000gain Spousereceives$3,000,000worthofproperty Estate owesincometaxof$1,198,000 Kidsgetonly$4,232,000($8,430,000‐$3,000,000‐ $1,198,000)insteadof$5.43million

© Davis & Willms, PLLC, 2015 24

8

7/13/2015

13

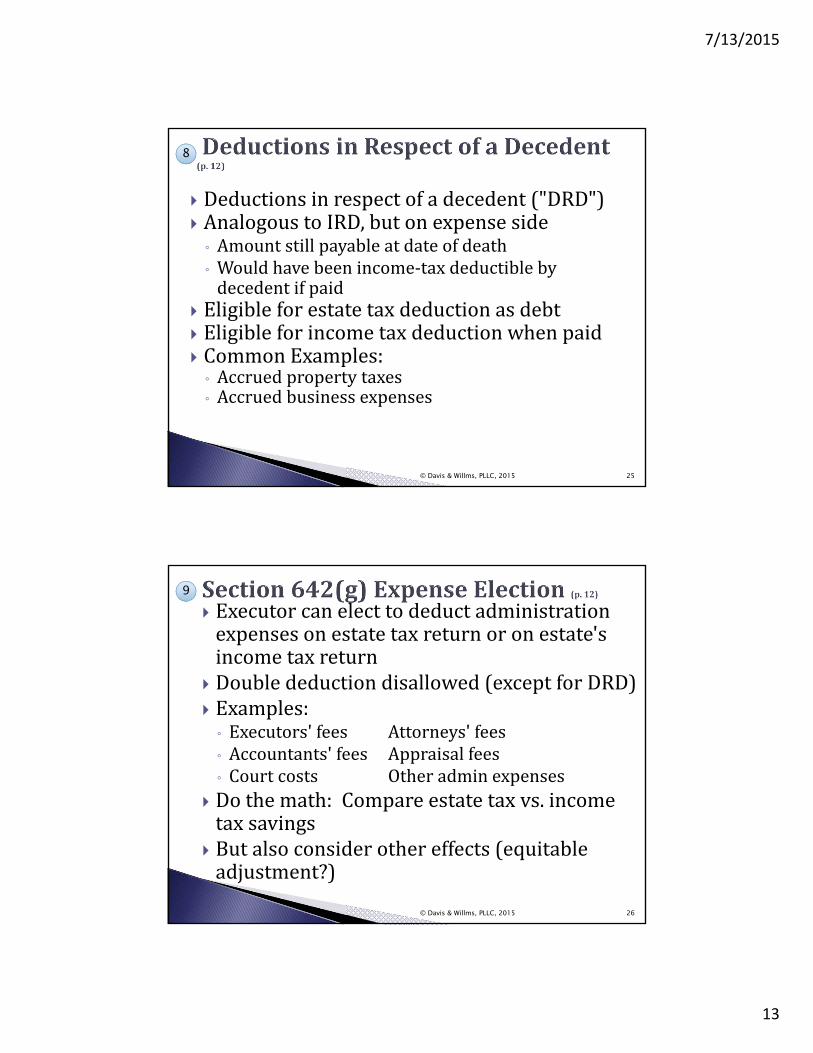

Deductionsinrespectofadecedent("DRD") AnalogoustoIRD,butonexpenseside◦ Amountstillpayableatdateofdeath◦ Wouldhavebeenincome‐taxdeductiblebydecedentifpaid

Eligibleforestatetaxdeductionasdebt Eligibleforincometaxdeductionwhenpaid CommonExamples:◦ Accruedpropertytaxes◦ Accruedbusinessexpenses

© Davis & Willms, PLLC, 2015 25

8

Executorcanelecttodeductadministrationexpensesonestatetaxreturnoronestate'sincometaxreturn

Doubledeductiondisallowed(exceptforDRD) Examples:◦ Executors'fees Attorneys'fees◦ Accountants'fees Appraisalfees◦ Courtcosts Otheradminexpenses

Dothemath:Compareestatetaxvs.incometaxsavings

Butalsoconsiderothereffects(equitableadjustment?)

© Davis & Willms, PLLC, 2015 26

9

7/13/2015

14

Deductionofexpensespaidfrommaritalorcharitablebequest onincometaxreturnmayreducethosedeductionsforestatetaxpurposes

Maydeductestate"managementexpenses"withnolossofestatetaxdeduction◦ Investmentfees Stockbrokeragecommissions◦ Custodialfees Interest

Cannotdeductestate"transmissionexpenses"withoutcorrespondinglossofestatetaxdeduction◦ Executors'fees Mostattorneyfees◦ Probatefees Courtcosts

Summaryofdeductibleexpenses—pages14‐15

© Davis & Willms, PLLC, 2015 27

9

Notalltrustsaresubjecttothe"normal"rulesofSubchapterJ

Congressionalsetof"string"statutesresultinincometaxationoftrustincometograntoroftrust(orsomeonetreatedasgrantor)

Statutetreatsgrantorasownerofthatportionoftrustpropertyoverwhichspecifiedpowerisheld

Similar,butnotidentical,listof"string"statutesresultinestatetaxinclusionoftrustpropertyingrantor'sfederaltaxableestate

Statutorylistofincometax"strings"isexhaustive

© Davis & Willms, PLLC, 2015 28

10

7/13/2015

15

RightofReversion—§ 673 PowertoControlBeneficialEnjoyment—§ 674 CertainAdministrativePowers—§ 675 PowertoRevoke—§ 676 RetainedRighttoIncome—§ 677 RightinBeneficiarytoVestTrustinSelf —§ 678 TransferstoForeignTrusts —§ 679

© Davis & Willms, PLLC, 2015 29

10

RightofReversion—§ 673 Trustthatultimatelyrevertstograntoristreatedasownedbygrantorunlessitoccursafter"safeperiod"

Pre‐1986,"safeperiod"was10years Current"safeperiod"ifactuarialvalueofreversionattimeoftrustcreationislessthan5%◦ Withverylowinterestrates,virtuallyallreversionsflunkthistest

◦ At2.2%7520rate,reversionafter60years=27%;reversionvaluedat<5%onlyafter138+years!

Reversionafterdeathofdescendant/beneficiarywhodiesbeforeage21isalsopermitted

© Davis & Willms, PLLC, 2015 30

10

7/13/2015

16

PowertoRevoke—§ 676 Sortoflikediscretionaryreversionandsame"safeperiod"applies

Alsoappliestopowerheldbynon‐adverseparty Manygrantorsrecreaterevocabletrustsfornon‐taxreason;theyareignoredfortaxpurposes

Defaultruleinmoststates:Trustisirrevocableunlesstrustinstrumentsaysotherwise

Notuniversallytrue,andtrustscanchangejurisdictions

Bestpractice:Explicitlystatewhethertrustisrevocableorirrevocable

© Davis & Willms, PLLC, 2015 31

10

RetainedRighttoIncome—§ 677 Appliestotruststhatcanpayincometograntororspouse

Alsoappliesifincomecanbeaccumulatedforlaterdistributiontograntororspouse

Evenappliestoindirectuseoftrustincome:◦ Paymentsthatdischargelegalorcontractualobligations◦ Paymentofpremiumsofinsuranceonlifeofgrantororgrantor'sspouse

Paymentforsupportormaintenanceofsomeonegrantorlegallyobligatedtosupport?◦ Righttohavetrustsouseddoesn'tcauseautomaticgrantortrusttreatment

◦ Butgrantoristaxedtoextendincomeisactuallysoused

© Davis & Willms, PLLC, 2015 32

10

7/13/2015

17

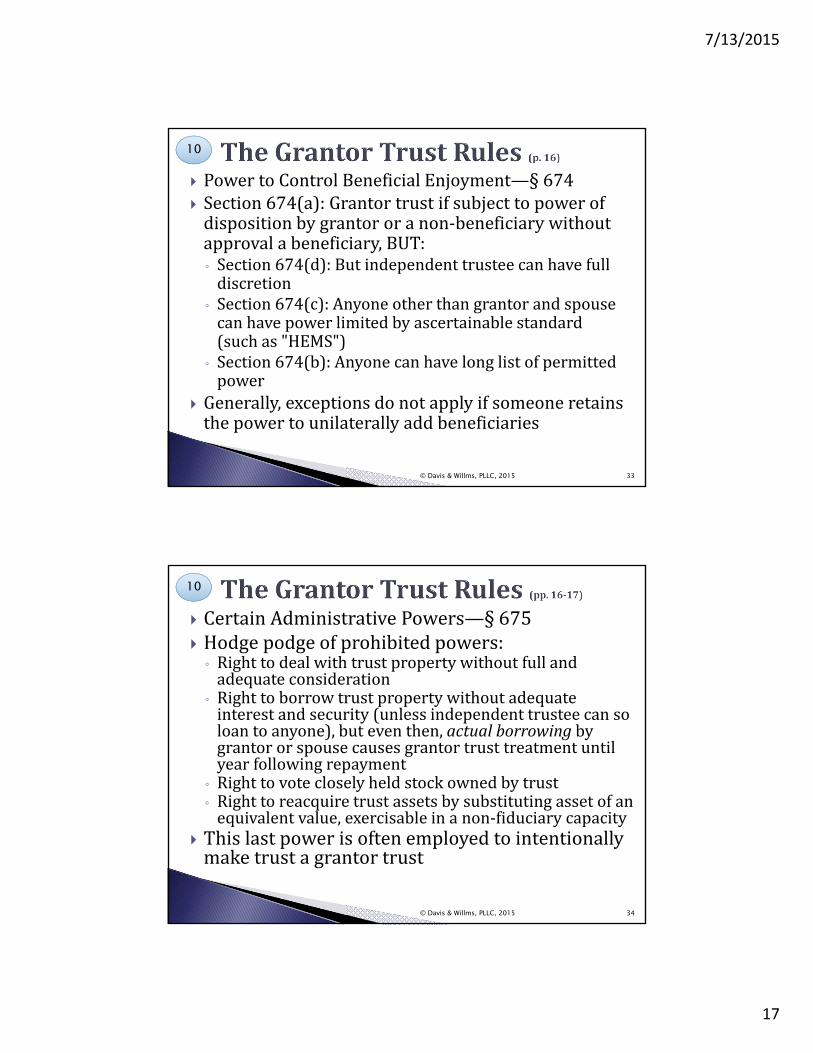

PowertoControlBeneficialEnjoyment—§ 674 Section674(a):Grantortrustifsubjecttopowerofdispositionbygrantororanon‐beneficiarywithoutapprovalabeneficiary,BUT:◦ Section674(d):Butindependenttrusteecanhavefulldiscretion

◦ Section674(c):Anyoneotherthangrantorandspousecanhavepowerlimitedbyascertainablestandard(suchas"HEMS")

◦ Section674(b):Anyonecanhavelonglistofpermittedpower

Generally,exceptionsdonotapplyifsomeoneretainsthepowertounilaterallyaddbeneficiaries

© Davis & Willms, PLLC, 2015 33

10

CertainAdministrativePowers—§ 675 Hodgepodgeofprohibitedpowers:◦ Righttodealwithtrustpropertywithoutfullandadequateconsideration

◦ Righttoborrowtrustpropertywithoutadequateinterestandsecurity(unlessindependenttrusteecansoloantoanyone),buteventhen,actualborrowingbygrantororspousecausesgrantortrusttreatmentuntilyearfollowingrepayment

◦ Righttovotecloselyheldstockownedbytrust◦ Righttoreacquiretrustassetsbysubstitutingassetofanequivalentvalue,exercisableinanon‐fiduciarycapacity

Thislastpowerisoftenemployedtointentionallymaketrustagrantortrust

© Davis & Willms, PLLC, 2015 34

10

7/13/2015

18

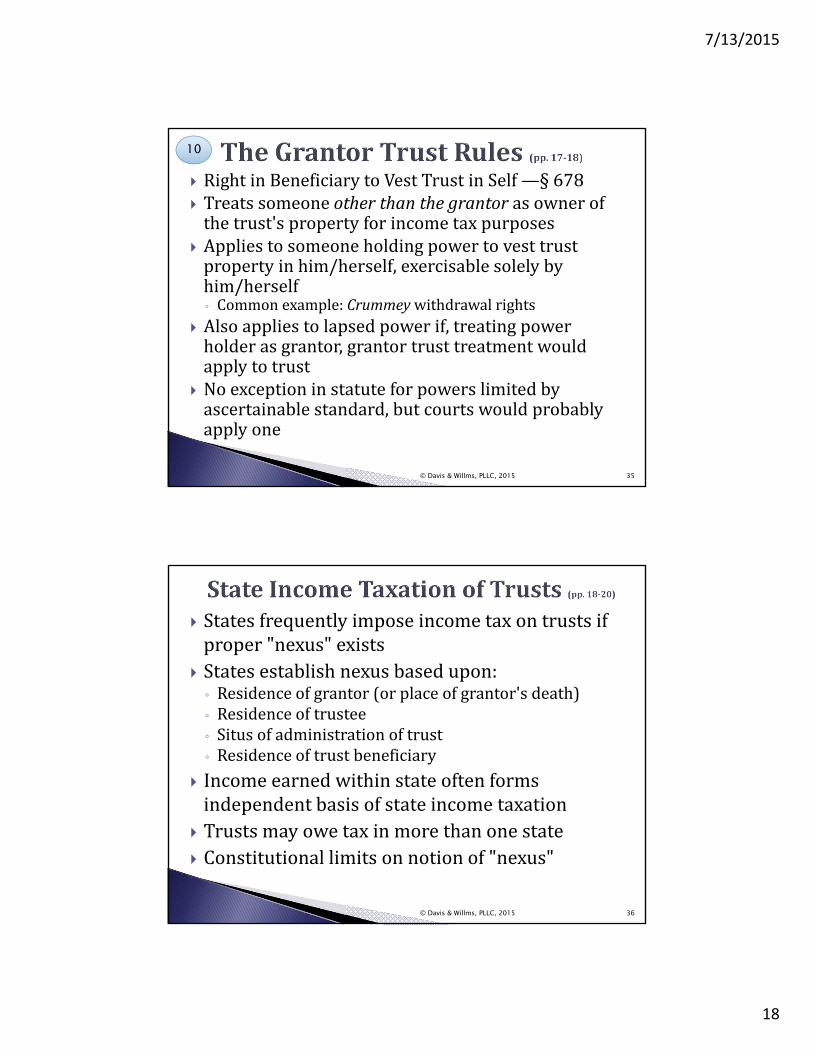

RightinBeneficiarytoVestTrustinSelf —§ 678 Treatssomeoneotherthanthegrantor asownerofthetrust'spropertyforincometaxpurposes

Appliestosomeoneholdingpowertovesttrustpropertyinhim/herself,exercisablesolelybyhim/herself◦ Commonexample:Crummeywithdrawalrights

Alsoappliestolapsedpowerif,treatingpowerholderasgrantor,grantortrusttreatmentwouldapplytotrust

Noexceptioninstatuteforpowerslimitedbyascertainablestandard,butcourtswouldprobablyapplyone

© Davis & Willms, PLLC, 2015 35

10

Statesfrequentlyimposeincometaxontrustsifproper"nexus"exists

Statesestablishnexusbasedupon:◦ Residenceofgrantor(orplaceofgrantor'sdeath)◦ Residenceoftrustee◦ Situsofadministrationoftrust◦ Residenceoftrustbeneficiary

Incomeearnedwithinstateoftenformsindependentbasisofstateincometaxation

Trustsmayowetaxinmorethanonestate

Constitutionallimitsonnotionof"nexus"

© Davis & Willms, PLLC, 2015 36