tvm accelerator fund a new building block in the ... · pdf filea new building block in the...

TRANSCRIPT

TVM Accelerator Fund

A new building block in the innovation

landscape of Germany

Technology Innovation Summit, Munich, 23. March 2015

Confidential

TVM Capital’s track record

• Leading European investment firm. Offices in Munich,

Montreal and Dubai. Founded by Siemens AG,

Germany, in 1983.

–>260 deals in 25 years

–€1.4bn ($1.8bn) raised in seven fund generations

–Long-standing pan-European and transatlantic

experience

• Life sciences practice: AUM €824m ($1.1bn)

–120 Life sciences venture and growth investments

–90 total exits, 30 active portfolio companies

–45 IPOs on Nasdaq, London, Frankfurt, Zurich,

Vienna

TVM Capital - 25 year track record

TVM Capital’s business

2 Source: TVM Capital

Confidential

TVM Accelerator

Time (y)

Duration

of

phase

14 Y Clinical Stage Preclinical Stage

Hit

to

lead

Lead

Optim. Preclin PhI III II Market Science

Target

to

hit

S

Source: Paul et al. Nature Reviews 9: 203 3

Accelerator Accelerator

+ Syndicate

Focus on truly innovative early asset and their development in

Virtual Single Asset (“VSAD”)

TVM LS VII

Confidential

Life Science Venture Capital – Status

Difficult Fund Raising Environment especially in

Europe/Germany

Macroeconomic environment changed post

2008(Risk Adverse at LP Level)

Performance issues at VC level since 2000

High capital use

Long investment cycles

High risk of failure

In Europe limited exit channels via public

markets

4 Source: TVM Capital

Confidential

Whereas in the US VC financing remains solid contribution…

5 Source: Ernst & Young

Confidential

0

5

10

15

20

25

30

35

40

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

Amount raised Number of IPOs

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Am

ount ra

ised (

US

$b)

Num

ber

of

IPO

s

Solid Capital Influx into Life Science Sector since 2012

IPO window opened again

6 Source: Ernst & Young

Confidential

- 23%

+100%

Keine IPOs seit 2006

In Germany levels of capital for Biotech remains low

7 Source: Ernst & Young

Confidential

Venture Capital Investments driven by Family

Offices…

8 Source: Ernst & Young

Confidential

The opportunity: filling the gap in early stage drug discovery

Dramatic venture funding gap: constant high levels of medical

research output but insufficient venture capital funding to translate

discovery into clinical development

9

Target

Identific. Target

Valid. Assay

dev. Screen

Hit to

lead

Lead opt.

Animal POC GLP tox IND

ACADEMIA Screening

centers Industry +

Specialized VC funds Funding gap

Source: TVM Capital

Confidential

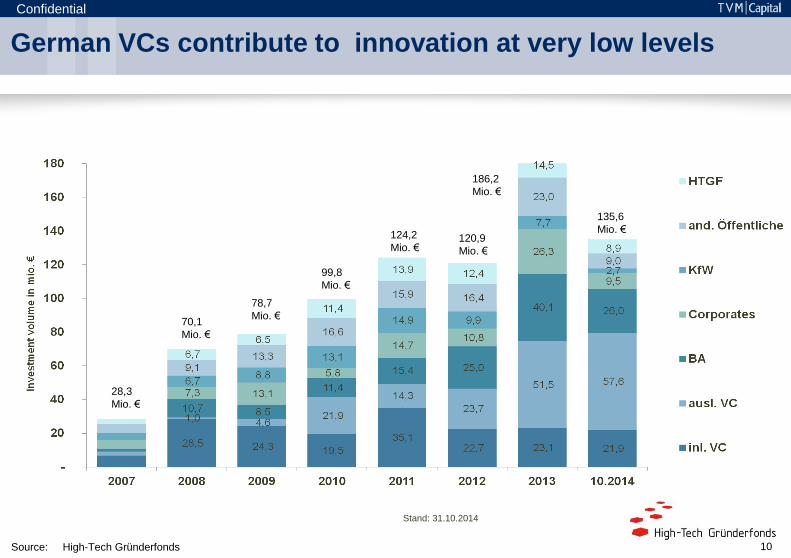

Stand: 31.10.2014

28,3

Mio. €

78,7

Mio. € 70,1

Mio. €

99,8

Mio. €

124,2

Mio. € 120,9

Mio. €

186,2

Mio. €

135,6

Mio. €

German VCs contribute to innovation at very low levels

Source: High-Tech Gründerfonds 10

Confidential

But there is light at the end of the tunnel …

• Demand for innovations across the health sector remains high

– Unmet medical need

– E-health

– Demographic Development

– Emerging markets

• Pharma recognized innovation gap and tackles it by various strategies.

Incubators, investment in early projects, alliances etc.

• Academic research delivers constant stream of innovations. CRISPR etc

.

• But note that 80 % of innovations from academia can’t be replicated in

other laboratories

• Cambridge MA and San Francisco provide role models for translation of

academic inventions into biotech/pharma

11 Source: TVM Capital

Confidential

Early-stage deals on the rise

12 Source: BIO Industry Analysis, Elsevier Database, October 2013

Confidential

The opportunity: filling the gap in early stage drug discovery

• Dramatic venture funding gap: constant high levels of medical research output

but insufficient venture capital funding to translate discovery into clinical

development

• Pull from Pharma: need for in-licensing and M&A to dampen patent cliff losses

and high in-house development attrition

Trend: increasing competition for early stage deals!

• Innovation sells: Increasing pricing and reimbursement pressure and regulatory

hurdles generally favor innovative development projects in high unmet need

indications.

13

Target

Identific. Target

Valid. Assay

dev. Screen

Hit to

lead

Lead opt.

Animal POC GLP tox IND

ACADEMIA Screening

centers Industry +

Specialized VC funds Funding gap

Source: TVM Capital

Confidential

Key ingredients for success

• Innovation: novel, biology validated targets with early leads addressing high unmet

need disease areas

• Intelligent deal sourcing strategy: preferred access to and proactive collaboration

with several prestigious research institutions, biotech and pharma companies

• Virtual development approach: investment into “virtual single asset development

companies” (“VSADs”) centered around one single molecule from entry to exit point

• Capital efficiency: each VSAD will be financed according to stringent go/no-go

decisions (early kill). Successful projects require €3-5m and about 3-5 years. We

expect up to 25% of projects to be successful. Average project costs are expected

to be €2-3m

• Partnerships with Max Planck / LDC ;Ascenion,PROvendis : unique deal

sourcing, preferred service partners, excellent understanding of buyer’s universe

14 Source: TVM Capital

Confidential

Innovation

Engine

TVM Accelerator Building Blocks

15 Source: TVM Capital

Innovation: Max-Planck-Innovation,

Ascenion, PROvendis and others

Translation: Small highly focused

teams and extended outsourcing

Venture Capital: TVM

Confidential

Invest in areas where customers have interest and are invested

Therapeutic areas

(ICD-10 nomenclature)

Focus Out of focus Partner interest *

Circulatory system atherosclerosis, CHF, slect. arrhythmias, RR lowering only,

lipid lowering

High

Endocrine, metab. Dis. T2D: Glc plus strategy, hormonal disorders,

diab sequela

T2D („Glc lowering

only“)

High

Infectious disease Gram neg, C. diff. MRSA High

Neoplasms Solid tumors, metastasis,

New MOAs

Liquid tumors High

Nervous system Pain, migraine prophylaxis Alzheimer’s disease High

Eye and ear Dry AMD, hearing loss, tinnitus Wet AMD

Digestive system ? yes Med

Female health, Endometriosis, hormonal replacement Birth control Med

Genitourinary system benign prostate hyperplasia (BPH) ? Med

Respiratory severe chronic obstructive pulmonary

disease (COPD), bronchiectasis

Mild /mod.Asthma Med.

Skin, muscosceletal Fibrotic disease Atop. dermititis Low

Pan – therapeutic area

approaches

Fibrosis, orphan diseases, mitochondrial

diseases,

Inflammation -

* Acc. to: Nat Biotechnol. 2013 Apr;31(4):284-7.

16 Source: TVM Capital

Confidential

TVM Accelerator Checkpoints

Checkpoints for TVM team to rapidly evaluate offered assets for an investment:

• Is asset/technology innovative and addresses true medical need

.

• Innovator aproachable, supportive of valorization effort. Trustworthy.

• Team with expertise and right social skills.

• Differentian to standard of care.

• Preferably orphan or niche indication/subgroup of patients can be identified for

initial PoC

• Exit. Does pharma interest exist in this indication/technology. Or is another round

of financing most likely needed?

17 Source: TVM Capital

Confidential

Our strategic partnership with Max Planck / LDC

18

Lead Discovery Center

• The Lead Discovery Center (LDC) was established in 2008 by the technology transfer organization Max

Planck Innovation (MI), as a novel approach to capitalize on the potential of excellent basic research for

the discovery of new therapies for diseases with high medical need. The LDC seeks to advance promising

research projects into the development of novel medicines in a professional manner.

• Proven track record:

– Nominated leads

The LDC has already concluded five projects successfully with the generation of lead series that

demonstrate initial proof of concept in animal models and meet all required lead criteria.

– First LDC lead licensed to Bayer

– 2nd LDC lead licensed to Qurient

– Drug discovery alliances with AstraZeneca and Daiichi Sankyo

– Strategic partnership with Merck Serono

– Joint track record with TVM: Direvo, Develogen, Evotec, GPC Biotech, Probiodrug, Morphosys

Strategic partnership – key points of the agreement

• Partnership with the most prestigious academic research institution in Germany

• Access to relevant assets:

• Pre-negotiated term sheet to transfer assets into VSAD structure

• Access to services and people of the LDC and the Max Planck institutes

Source: TVM Capital

Confidential

TVM +

Originator

Virtual Single Asset Company

CROs

Pharma

Exit through

M&A or

licensing

eLeads + IP + tranched

investment

Project management

Go / Nogo decision

Corp. Governance Preclinical candidate/IND readyness

Exit proceeds

The Virtual Single Asset Development (“VSAD”) Concept

19 Source: TVM Capital

Confidential

Simple math: 1 in 4 PoS and killing early will create value

20

Step 1

Step 2 Step 3

Step 1

Step 2 Step 3

Step 1

Step 2 Step 3

Step 1

Step 2 Step 3

Cost Return

1.2m 0

2.4m 0

5.0m

3.6m

20-30m*

0

Total

investment

cost: 12,2m

Overall return

multiple: ~2x

*based on industry comparables; combination of upfront and NPV of milestones

Source: Life Science Accelerator

Confidential

The VSAD approach has many benefits

VSAD Approach Traditional Approach

Business Model One Asset to preclin POC (focused) Multiple Assets (diversified)

Management Semi-virtual/Low headcount High headcount

Capital Needs to Exit € 3-5m, low fixed costs €100m+, high fixed cost

Capital Source Accelerator (+/- one other Inv.) Many/Syndicate

Time to Exit 3-5 years 8-10+ years

Exit Route Trade Sale IPO, M&A, Licensing

Share Class for Originators Common Shares –

as TVM

Common Shares –

behind many classes of preferred

shares

Dilution for Originators None High

Comparison VSAD Versus Traditional Approach

21 Source: TVM Capital

Confidential

Summary

The current status of VC investment in Life Science in Germany ist still

unsatisfactory

• Number of VCs with local focus and long investment perspectives not sufficient

– Positive is, that problem has been recognized and could be transported to a

wider public. Remedies are discussed, but not yet implemented ( Alliance for

Venture Capital of BVK)

• No local access to capital market similar to Euronext or Nasdaq

– Thus local biotech will preferable exit vs. Asset sale. Only minority is able to

access public markets abroad.

• VCs adapted to situation in Germany by either shifting their focus of investment

abroad and/or focus on single asset/platform based companies.

Last but not least: Limited access to Venture Capital is hampering innovation

in German Life Science. The science, the teams, the assets are available in

Germany

22 Source: TVM Capital

Confidential

Our Hope

23 Source: TVM Capital

Thanks for your attention