tw funding relief

TRANSCRIPT

7/30/2019 TW Funding relief

http://slidepdf.com/reader/full/tw-funding-relief 1/8

The Implications of Funding Relief

What Does it Mean for Asset Allocation and

Liability-Driven Investing?

7/30/2019 TW Funding relief

http://slidepdf.com/reader/full/tw-funding-relief 2/8

Funding Relie and the Impact on Asset Allocation and towerswatson.com

While the goal o the legislation was to ree up cash

or employers to spend elsewhere and increase tax

revenue by reducing the amount o tax-deductiblecontributions, a secondary impact may be a sizable

shit in asset allocation away rom liability-hedging

assets. In addition, this law, the most signicant

among multiple recent installments o unding

relie, may set a precedent that leads to a potential

reevaluation o the importance o risk when setting

pension investment policies.

MAP-21 and the Case Against LDI

Liability-driven investing (LDI) trended this past

decade in the wake o the Pension Protection Act

o 2006 (PPA) and word o potential accountingreorm. The rules governing pension plans began

to incorporate more mark-to-market concepts and

emphasize valuing liabilities at current bond yields.

nvestors, oten tasked with managing their unded

status and not simply their asset level, realized the

detrimental impact o interest rate risk and the greater

stabilization benets xed income now oered. Both

the incentive and ability to manage unded status via

iability-matched investments were on the rise. This

strategy proved ruitul as rates dropped in recent

years, since liabilities discounted by those lower rates

ncreased in value, and those who implemented an LDI

strategy saw a commensurate increase in the value o their xed-income investments.

Four years later, the introduction o MAP-21 represents

a departure rom the spirit o PPA and perhaps rom

LDI as well. While the idea behind portions o PPA

was to make liabilities move with the current yield

environment, MAP-21 accomplishes the opposite.

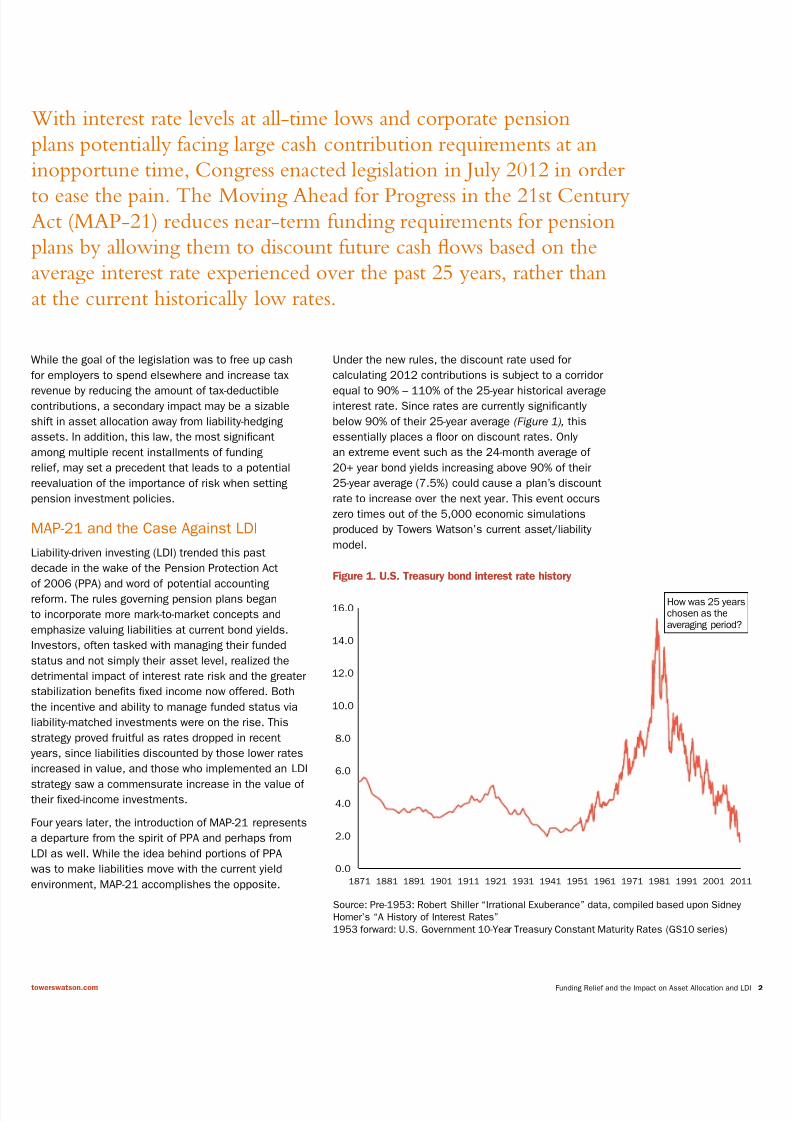

Under the new rules, the discount rate used or

calculating 2012 contributions is subject to a corridor

equal to 90% – 110% o the 25-year historical averageinterest rate. Since rates are currently signicantly

below 90% o their 25-year average (Figure 1), this

essentially places a foor on discount rates. Only

an extreme event such as the 24-month average o

20+ year bond yields increasing above 90% o their

25-year average (7.5%) could cause a plan’s discount

rate to increase over the next year. This event occurs

zero times out o the 5,000 economic simulations

produced by Towers Watson’s current asset/liability

model.

With interest rate levels at all-time lows and corporate pension

plans potentially acing large cash contribution requirements at an

inopportune time, Congress enacted legislation in July 2012 in order

to ease the pain. The Moving Ahead or Progress in the 21st CenturyAct (MAP-21) reduces near-term unding requirements or pension

plans by allowing them to discount uture cash ows based on the

average interest rate experienced over the past 25 years, rather than

at the current historically low rates.

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

1871 1881 1891 1901 1911 1921 1931 1941 1951 1961 1971 1981 1991 2001 201

Figure 1. U.S. Treasury bond interest rate history

How was 25 yearchosen as theaveraging period?

Source: Pre-1953: Robert Shiller “Irrational Exuberance” data, compiled based upon Sidney

Homer’s “A History of Interest Rates”

1953 forward: U.S. Government 10-Year Treasury Constant Maturity Rates (GS10 series)

7/30/2019 TW Funding relief

http://slidepdf.com/reader/full/tw-funding-relief 3/8

Funding Relie and the Impact on Asset Allocation and towerswatson.com

Further, a plan’s unding discount rate would actually

move in the opposite direction o interest rates over

the next ew years should uture rates unold in

accordance with Towers Watson Investment Ser vice’s

views.* The new law calls or the 90% – 110% corridor

to widen to 85% – 115% in 2013 (and then continue in

5% increments out to 70% – 130%). This means that

a plan’s discount rate will almost certainly decreaserom 2012 to 2013 even i interest rates rise. For

example, a 1% parallel increase in the yield curve rom

2012 to 2013 and then again rom 2013 to 2014

would still result in a plan’s unding discount rate

decreasing in both years. Not only will discount rates

over the next ew years likely be set independently

o the interest rate environment, there is actually

a strong likelihood that the two will move in

opposite directions. This disconnect is illustrated

in Figure 2, which utilizes Towers Watson’s capital

market assumptions to compare the rate used to

value a sample plan’s liability under MAP-21 versus

that under a market-value method. I the assumptionsmaterialize as demonstrated below, the decline in

the value o a plan’s long bond portolio due to rising

yields will no longer be oset by a decline in the value

o a plan’s liabilities as measured or unding.

5th − 25th percentile 25th − 50th 50th − 75th 75th − 95th

Figure 2. Effective interest rate: Market-value method

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Mean

5th − 25th percentile 25th − 50th 50th − 75th 75th − 95th

Effective interest rate: Post-MAP-21

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Mean

*Towers Watson Investment Services Global Markets Overview, July 2012

7/30/2019 TW Funding relief

http://slidepdf.com/reader/full/tw-funding-relief 4/8

Funding Relie and the Impact on Asset Allocation and towerswatson.com

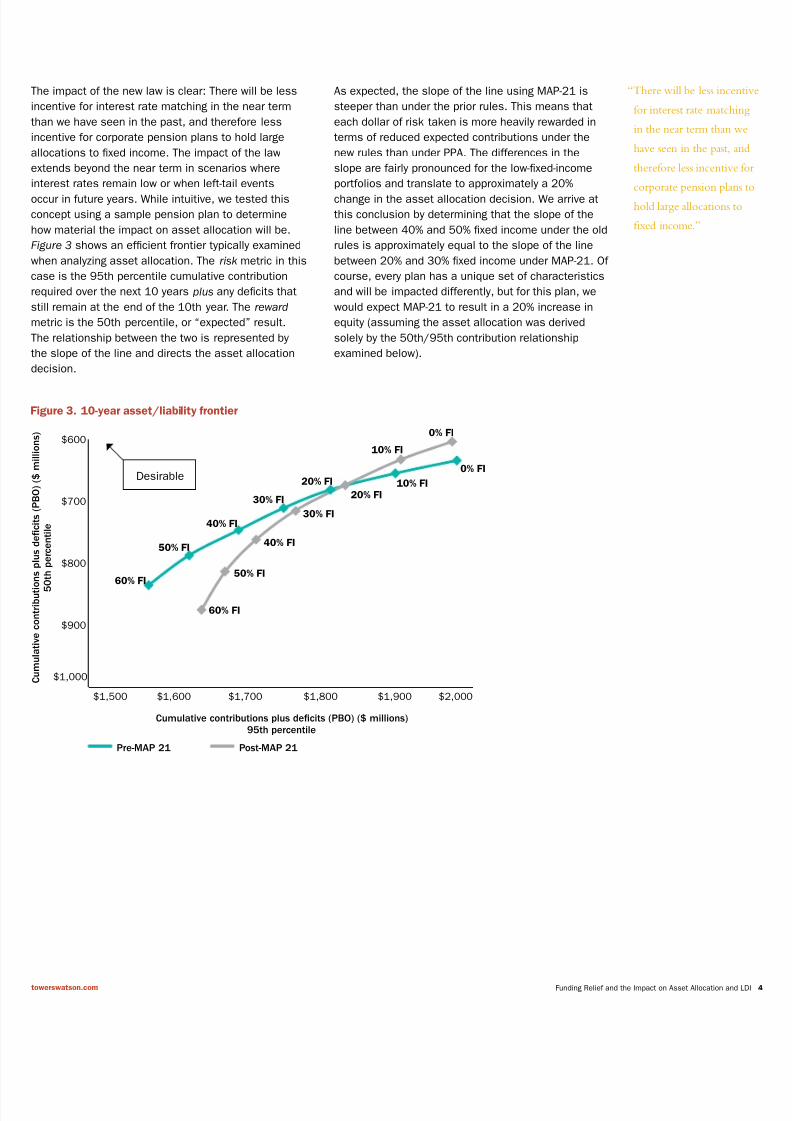

The impact o the new law is clear: There will be less

ncentive or interest rate matching in the near term

than we have seen in the past, and thereore less

ncentive or corporate pension plans to hold large

allocations to xed income. The impact o the law

extends beyond the near term in scenarios where

nterest rates remain low or when let-tail events

occur in uture years. While intuitive, we tested this

concept using a sample pension plan to determine

how material the impact on asset allocation will be.

Figure 3 shows an ecient rontier typically examined

when analyzing asset allocation. The risk metric in this

case is the 95th percentile cumulative contribution

required over the next 10 years plus any decits that

still remain at the end o the 10th year. The reward

metric is the 50th percentile, or “expected” result.

The relationship between the two is represented by

the slope o the line and directs the asset allocation

decision.

Pre-MAP 21 Post-MAP 21

Figure 3. 10-year asset/liability frontier

0% FI

10% FI20% FI

30% FI

40% FI

50% FI

60% FI

0% FI

10% FI

20% FI

30% FI

40% FI

50% FI

60% FI

$600

$700

$800

$900

$1,000

$1,500 $1,600 $1,700 $1,800 $1,900 $2,000

C u m u l a t i v e c o n t r i b u t i o n s p l u s d e c i t s ( P B O ) ( $ m i l l i o n s )

5

0 t h p e r c e n t i l e

Cumulative contributions plus decits (PBO) ($ millions)95th percentile

As expected, the slope o the line using MAP-21 is

steeper than under the prior rules. This means that

each dollar o risk taken is more heavily rewarded in

terms o reduced expected contributions under the

new rules than under PPA. The dierences in the

slope are airly pronounced or the low-xed-income

portolios and translate to approximately a 20%

change in the asset allocation decision. We arrive at

this conclusion by determining that the slope o the

line between 40% and 50% xed income under the old

rules is approximately equal to the slope o the line

between 20% and 30% xed income under MAP-21. O

course, every plan has a unique set o characteristics

and will be impacted dierently, but or this plan, we

would expect MAP-21 to result in a 20% increase in

equity (assuming the asset allocation was derived

solely by the 50th/95th contribution relationship

examined below).

“There will be less incen

or interest rate matchin

in the near term than w

have seen in the past, an

thereore less incentive

corporate pension plans

hold large allocations to

fxed income.”

Desirable

7/30/2019 TW Funding relief

http://slidepdf.com/reader/full/tw-funding-relief 5/8

Funding Relie and the Impact on Asset Allocation and towerswatson.com

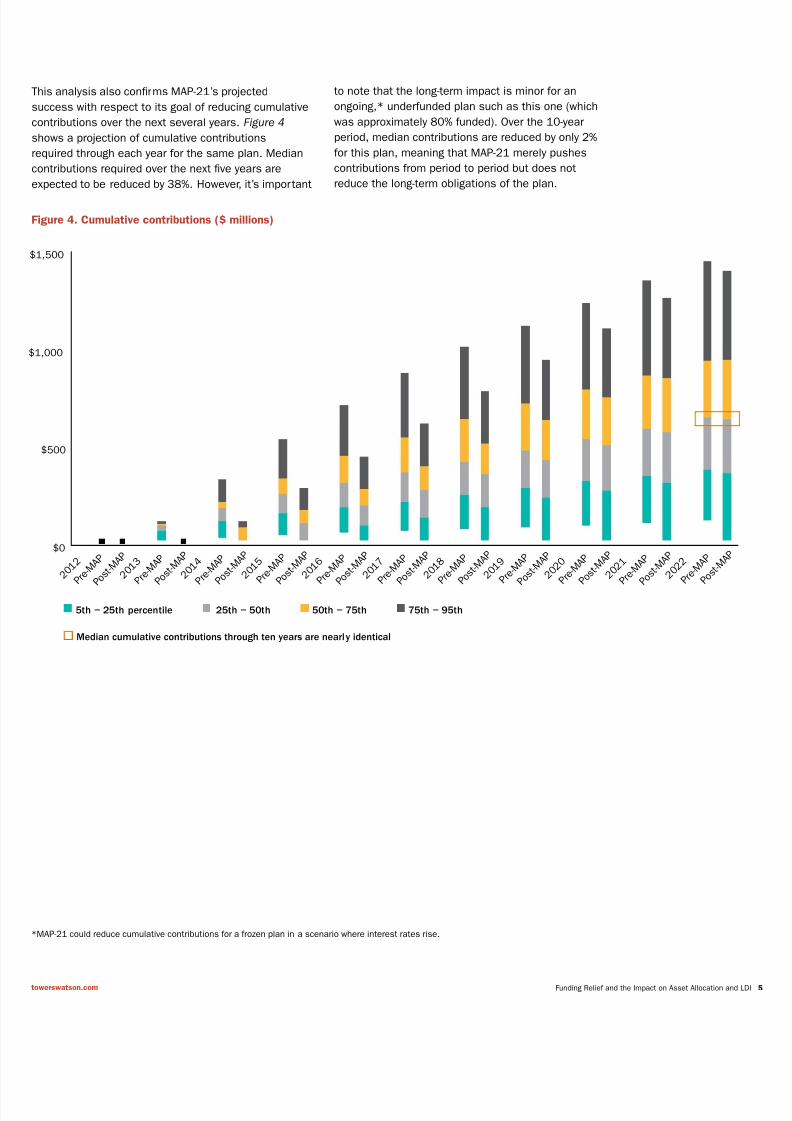

This analysis also conrms MAP-21’s projected

success with respect to its goal o reducing cumulative

contributions over the next several years. Figure 4

shows a projection o cumulative contributions

required through each year or the same plan. Median

contributions required over the next ve years are

expected to be reduced by 38%. However, it’s important

to note that the long-term impact is minor or an

ongoing,* underunded plan such as this one (which

was approximately 80% unded). Over the 10-year

period, median contributions are reduced by only 2%

or this plan, meaning that MAP-21 merely pushes

contributions rom period to period but does not

reduce the long-term obligations o the plan.

5th − 25th percentile 25th − 50th 50th − 75th 75th − 95th

Figure 4. Cumulative contributions ($ millions)

$0

$500

$1,000

$1,500

2 0 1 2

P r e - M

A P

P o s t - M A P

2 0 1 3

P r e - M

A P

P o s t - M A P

2 0 1 4

P r e - M

A P

P o s t - M A P

2 0 1 5

P r e - M

A P

P o s t - M A P

2 0 1 6

P r e - M

A P

P o s t - M A P

2 0 1 7

P r e - M

A P

P o s t - M A P

2 0 1 8

P r e - M

A P

P o s t - M A P

2 0 1 9

P r e - M

A P

P o s t - M A P

2 0 2 0

P r e - M

A P

P o s t - M A P

2 0 2 1

P r e - M

A P

P o s t - M A P

2 0 2 2

P r e - M

A P

P o s t - M A P

*MAP-21 could reduce cumulative contributions or a rozen plan in a scenario where interest rates rise.

Median cumulative contributions through ten years are nearly identical

7/30/2019 TW Funding relief

http://slidepdf.com/reader/full/tw-funding-relief 6/8

Funding Relie and the Impact on Asset Allocation and towerswatson.com

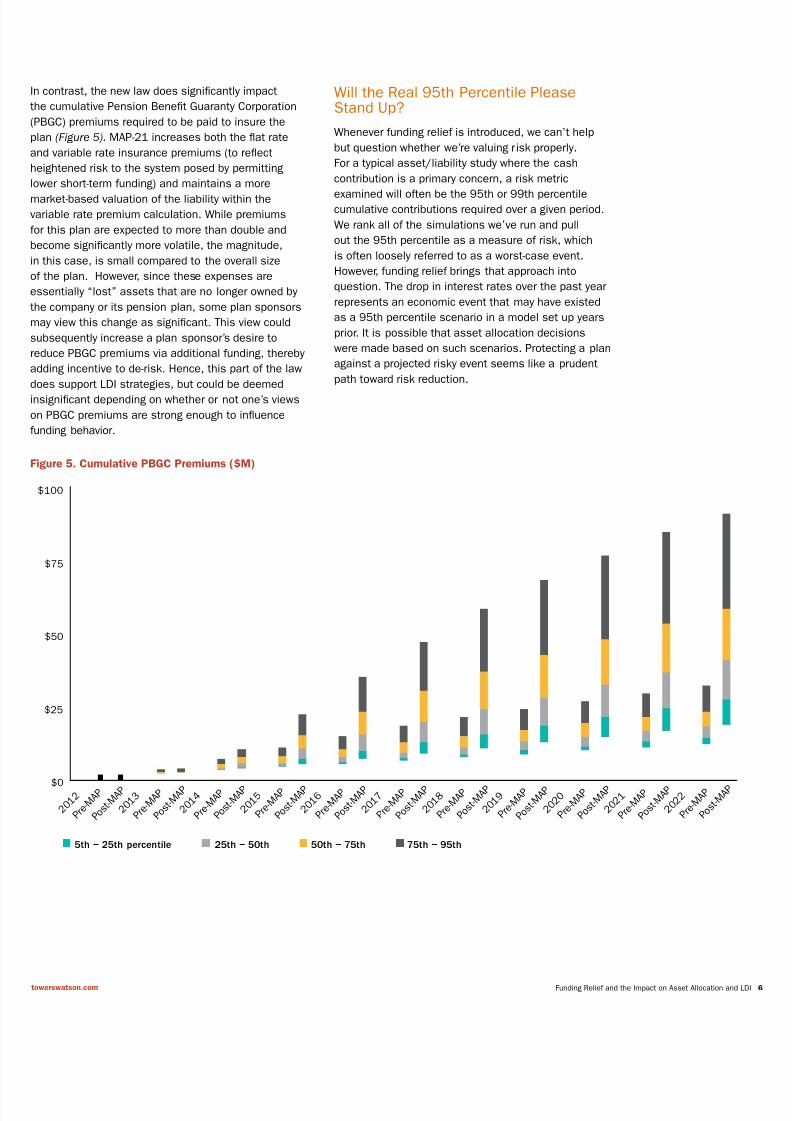

n contrast, the new law does signicantly impact

the cumulative Pension Benet Guaranty Corporation

PBGC) premiums required to be paid to insure the

plan (Figure 5). MAP-21 increases both the fat rate

and variable rate insurance premiums (to refect

heightened risk to the system posed by permitting

ower short-term unding) and maintains a more

market-based valuation o the liability within the

variable rate premium calculation. While premiums

or this plan are expected to more than double and

become signicantly more volatile, the magnitude,

n this case, is small compared to the overall size

o the plan. However, since these expenses are

essentially “lost” assets that are no longer owned by

the company or its pension plan, some plan sponsors

may view this change as signicant. This view could

subsequently increase a plan sponsor’s desire to

reduce PBGC premiums via additional unding, thereby

adding incentive to de-risk. Hence, this part o the law

does support LDI strategies, but could be deemed

nsignicant depending on whether or not one’s views

on PBGC premiums are strong enough to infuence

unding behavior.

Will the Real 95th Percentile PleaseStand Up?

Whenever unding relie is introduced, we can’t help

but question whether we’re valuing risk properly.

For a typical asset/liability study where the cash

contribution is a primary concern, a risk metric

examined will oten be the 95th or 99th percentilecumulative contributions required over a given period.

We rank all o the simulations we’ve run and pull

out the 95th percentile as a measure o risk, which

is oten loosely reerred to as a worst-case event.

However, unding relie brings that approach into

question. The drop in interest rates over the past year

represents an economic event that may have existed

as a 95th percentile scenario in a model set up years

prior. It is possible that asset allocation decisions

were made based on such scenarios. Protecting a plan

against a projected risky event seems like a prudent

path toward risk reduction.

5th − 25th percentile 25th − 50th 50th − 75th 75th − 95th

Figure 5. Cumulative PBGC Premiums ($M)

2 0 1 2

P r e - M

A P

P o s t - M A P

2 0 1 3

P r e - M

A P

P o s t - M A P

2 0 1 4

P r e - M

A P

P o s t - M A P

2 0 1 5

P r e - M

A P

P o s t - M A P

2 0 1 6

P r e - M

A P

P o s t - M A P

2 0 1 7

P r e - M

A P

P o s t - M A P

2 0 1 8

P r e - M

A P

P o s t - M A P

2 0 1 9

P r e - M

A P

P o s t - M A P

2 0 2 0

P r e - M

A P

P o s t - M A P

2 0 2 1

P r e - M

A P

P o s t - M A P

2 0 2 2

P r e - M

A P

P o s t - M A P$0

$25

$50

$75

$100

7/30/2019 TW Funding relief

http://slidepdf.com/reader/full/tw-funding-relief 7/8

Funding Relie and the Impact on Asset Allocation and towerswatson.com

But when the actual economic environment that

transpired in 2011 matched one o these worst-case

scenarios, legislation was enacted to prevent the pain

rom being as severe as indicated by our models.

The real worst-case event in this scenario wasn’t the

95th percentile result, but rather a change in law

ensuring that results did not all below, let’s say, the

75th percentile. This is not the rst example o the

government stepping in to alleviate the downside.

Following the credit crisis in 2008, PPA was amended

with the Worker, Retiree, and Employer Recovery Act

o 2008, which lowered the short-term unding target.

Further relie was oered in 2010 via the Preservation

o Access to Care or Medicare Beneciaries and

Pension Relie Act, which allowed pension plans to

extend the amortization period or ununded liabilities.

While MAP-21 is dierent rom these rounds o relie

because it is permanent and could eventually impact

the upside as well as the downside, this third post-

credit-crisis amendment to PPA raises a question:Should we be ignoring the governmental saety net that

has consistently been implemented in tough times?

the answer is no, this would again point pension

plan investors toward taking more risk. I the upside

o equity risk is always attainable but the downside is

potentially avoidable due to legislative intervention, the

ncentive or xed income is not as strong as indicated

n our models. I there is an unspoken foor at the 75th

percentile, it is possible that risk/reward trade-os

are not currently being analyzed properly. The more

prevalent unding relie becomes, the more likely it

could be viewed as a risk management alternative to

xed income.

Economic Liability and the Case AgainstRDI

Despite these two anti-LDI arguments, we eel the

role o xed income in pension plans should never

change when considering the true economic liability

o a plan. The discussion above ocuses solely on

the contribution rules dictated by the IRS (“rules-

driven investing”). I, instead, we consider that a

plan’s undamental responsibility is to ully pay or

ts obligations regardless o the rules governing its

unding, a change in law would not impact assetallocation behavior.

A duciary is responsible or the series o payments

promised. In determining the total amount needed in

today’s dollars that would und those promises, the

conservative (and responsible, in our view) method

inorming pension asset allocation would be to

discount the payments at a rate we were airly certain

to earn (i.e., current bond yields). Investors relying on

these principles would always value LDI regardless o

the rules surrounding cash contributions.

Conclusion

Liability-matching strategies are valuable when takingan economic approach to liability valuation. However,

investors who allow contribution risk to drive their

decisions may be apt to take on more return-seeking

assets with the recent passing o MAP-21. The new

law lessens the current eectiveness o LDI strategies

with respect to contributions and also brings into

question the importance o risk reduction in a system

where relie laws requently bail us out in hard times.

Further inormation

I you would like to discuss any o the areas covered in

more detail, please contact your local Towers Watsonconsultant or:

Adam Levine

+1 212 309 3813

“Despite these two anti-LDI arguments, we

eel the role o fxed income in pension plans

should never change when considering the

true economic liability o a plan.”

7/30/2019 TW Funding relief

http://slidepdf.com/reader/full/tw-funding-relief 8/8

Copyright © 2012 Towers Watson. All rights reserved.

TW-NA-2012-27708

towerswatson.com

About Towers WatsonTowers Watson is a leading global proessional services

company that helps organizations improve perormance through

eective people, risk and nancial management. With 14,000

associates around the world, we oer solutions in the areas

o employee benets, talent management, rewards, and risk and

capital management.

Please note: This document was prepared or

general inormation purposes only and should not be

considered a substitute or specifc proessional advice.

n particular, its contents are not intended by Towers

Watson to be construed as the provision o investment,

egal, accounting, tax or other proessional advice or

recommendations o any kind, or to orm the basis o

any decision to do or to rerain rom doing anything.

As such, this document should not be relied upon or

nvestment or other fnancial decisions, and no such

decisions should be made on the basis o its contents

without seeking specifc advice. This document is

based on inormation available to Towers Watson at

the date o issue, and takes no account o subsequent

developments ater that date.

In addition, past perormance is not indicative o uture

results. This document may not be reproduced or

distributed to any other party, whether in whole or in

part, without Towers Watson’s prior written permission,

except as may be required by law. In the absence o

its express written permission to the contrary, Towers

Watson and its afliates and their respective directors,

ofcers and employees accept no responsibility and will

not be liable or any consequences howsoever arising

rom any use o or reliance on the contents o this

document including any opinions expressed herein.