ubc faculty pension plan pension forum · mike leslie, executive director, investments may 25, 2016...

TRANSCRIPT

UBC FACULTY PENSION PLAN

PENSION FORUM M R . J OOS T B L OM , C HA I R , B OA R D OF T R US T E E S

M S . OR L A C OUS I NE A U, E X E C UT I V E D I R E C T OR , P E NS I ONS

M R . M I KE L E S L I E , E X E C UT I V E D I R E C T OR , I NV E S T M E NT S

M A Y 2 5 , 2 0 1 6

2

• Introduction Of Trustees

• Plan’s Financial And Membership Update

• 2016 Board Initiatives And Projects

• 2015 Operations Update & 2016

Operations Objectives

• Investment Review For 2015 And First

Quarter 2016

• Questions 2

Agenda

3

3

Mr. Joost Blom, Chair

Professor, Faculty of Law

Dr. Ken Carty

Professor Emeritus, Department

of Political Science

Dr. Robert Heinkel, Vice-

Chair

Professor, Sauder School of

Business

Dr. Joanne Emerman

Professor Emerita, Department of

Cellular and Physiological

Sciences

Dr. Joy Begley

Associate Professor, Sauder

School of Business

Dr. Lorenzo Garlappi

Associate Professor, Sauder

School of Business

Dr. Joyce Boon

Associate Professor Emerita,

Barber Arts & Sciences, UBCO

Mr. Vijay Verma

Researcher Emeritus, TRIUMF

Board of Trustees

4

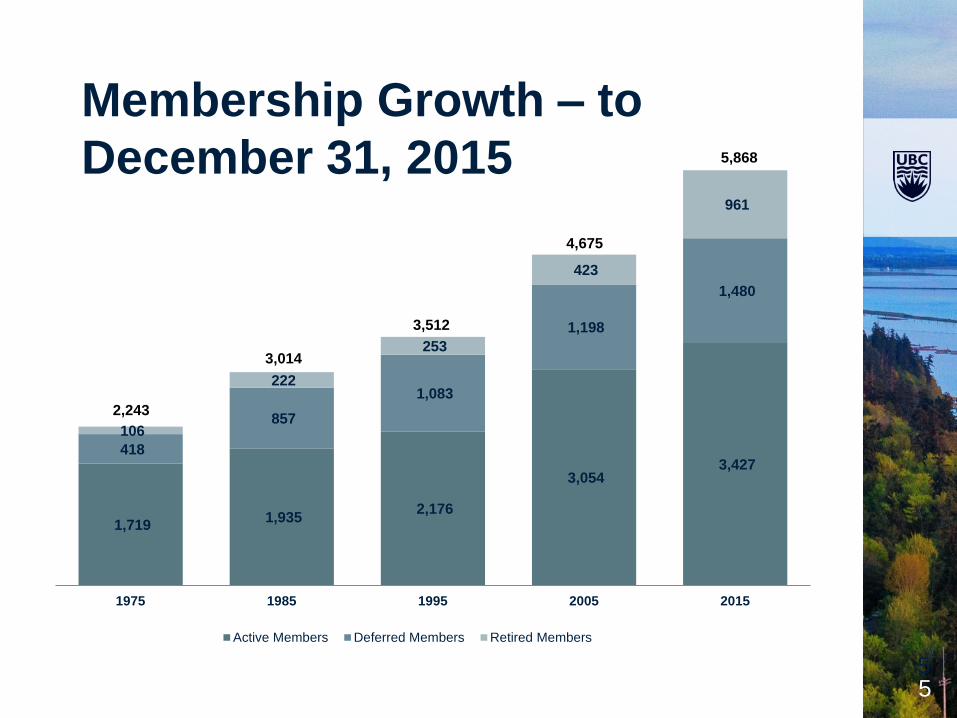

Plan Statistics December 31,2015

4

Active Deferred Retired Total

Members 3,427 1,480 961 5,868

59% 25% 16% 100%

Assets

(millions)

$1,150 $255 $595 $2,000

58% 13% 29% 100%

5 5

1,719 1,935

2,176

3,054 3,427

418

857

1,083

1,198

1,480

106

222

253

423

961

1975 1985 1995 2005 2015

Active Members Deferred Members Retired Members

5,868

4,675

3,512

3,014

2,243

Membership Growth – to

December 31, 2015

6

Composition of Funds – March 31, 2016

6

Total Plan Assets $2.0 Billion

7 7

2016 Board Initiatives and Projects

• Governance Review

• Investment Structure Review – Foreign Equity

Managers

• Variable Payout Life Annuity Review

• Continuing oversight of the Plan’s investment

manager’s reporting on how they

consider/implement environmental, social and

governance factors (ESG) in their investment

process

8 8

2015 Operations Update

• Successful transition to Sun Life as

recordkeeper and custodian

• Smooth transition to new senior leadership

team for the UBC Pension Administration

Office

• Changes to the Plan documents and forms to

comply with the new BC pension legislation

9

2016 Operations Objectives

• Redesign FPP website

• Member education and communication – Role of Board, UBC Pension Administration

office and Sun Life

– Increase awareness and usage of tools

available through Sun Life

• Change to bi-weekly remittance of

contributions effective January 1, 2017

10

10

Investment Review of 2015

11

11

Agenda

• Plan – Fund Weightings & Asset Mix

• Fund Returns

• Investment Market Update

• Question Period

12

Investment Changes in 2015

1. Moved investment funds to Sun Life recordkeeping

platform

• No changes to investment funds

• No changes to investment managers

2. Hedge Fund: Removed

• Terminated in January 2015 due to continued weakness

• Funds reallocated to two Global Equity managers

• Affected Balanced and Foreign Equity Funds

3. Short Term Investment Fund (“STIF”)

• Changed managers to MFS/Sun Life from bcIMC

12

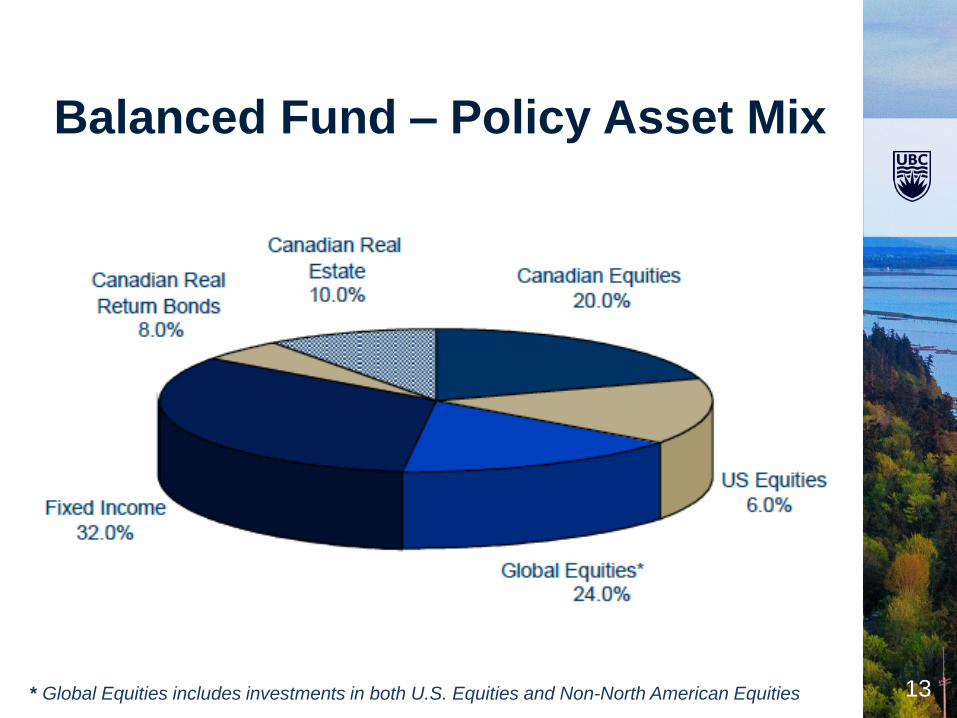

13 * Global Equities includes investments in both U.S. Equities and Non-North American Equities

Balanced Fund – Policy Asset Mix

13

14

2015 Fund Returns / Peer Rankings

Fund Returns (%)

Return Ranking (percentile)*

Risk** Ranking

(percentile)*

1 Yr 5 Yr 10 Yr 1 Year 5 Years 4 Years

Balanced 6.6 9.0 6.9 10th 8th 84th

Bond 3.5 4.8 5.3 33rd 73rd 4th

Canadian

Equity -6.8 5.0 6.1 63rd 43rd 62nd

Foreign Equity 19.

6

16.7 7.3 35th 11th 43rd

Short Term Invt. 1.0 1.2 1.9 20th 17th 4th

Gross returns to Dec. 31/15

* 1st percentile – highest ranking best performance, 100th percentile – lowest ranking

** Risk - as measured by annual standard deviation of returns

- a lower ranking number (say 80th percentile) means less risky

14

15

Review of 2015

Q1 Q2 Q3 Q4 1 Year

Canadian Equities 2.6% -1.6% -7.9% -1.4% -8.3%

U.S. Equities (C$) 10.4% -1.4% 0.5% 10.6% 21.0%

International Equities

(C$) 14.7% -1.0% -3.6% 8.2% 18.3%

Bonds 4.2% -1.7% 0.2% 1.0% 3.5%

16

• Further Collapse in Energy Prices

• WTI – December 31, 2014 $53.27

• WTI – December 31, 2015 $36.60

• Slowdown in Emerging Markets

• China, Brazil, Russia

• Decline in Commodity Prices

• Central banks influence

Key Themes in 2015

17

50

60

70

80

90

100

110

120

130

De

c 2

01

4

Ja

n 2

01

5

Feb

201

5

Ma

r 2

01

5

Ap

r 2

01

5

Ma

y 2

01

5

Ju

n 2

01

5

Ju

l 2

01

5

Au

g 2

01

5

Se

p 2

01

5

Oct 2

01

5

No

v 2

01

5

De

c 2

01

5

WTI Oil Natural Gas Copper Gold Silver

Commodities down

24% on average in 2015

Commodities Prices Have Fallen

Across the Board

18

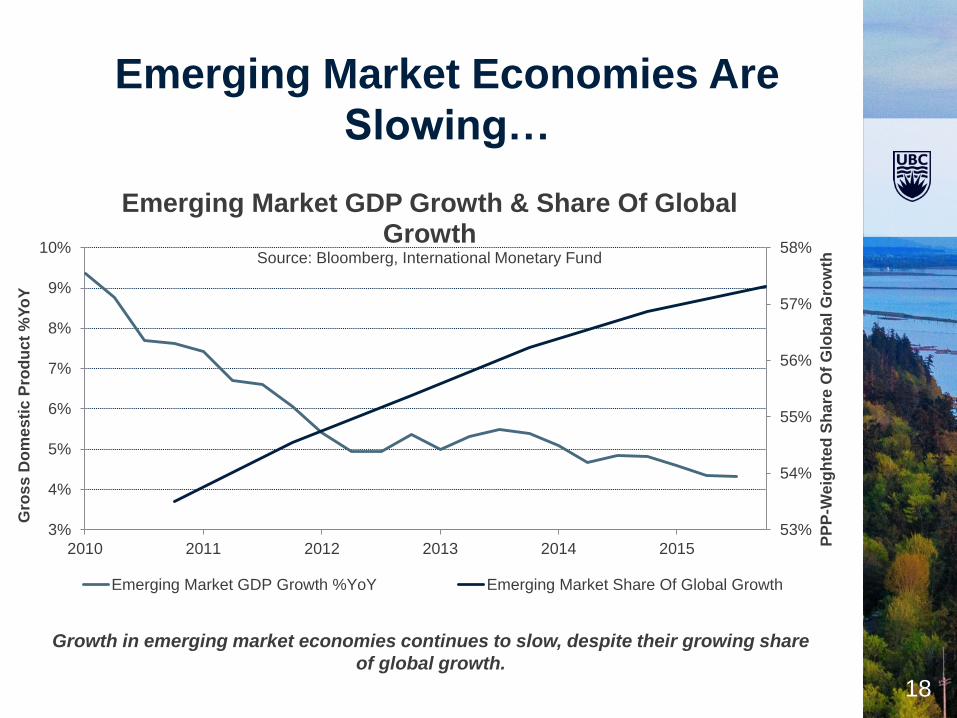

Growth in emerging market economies continues to slow, despite their growing share

of global growth.

Emerging Market Economies Are

Slowing…

53%

54%

55%

56%

57%

58%

3%

4%

5%

6%

7%

8%

9%

10%

2010 2011 2012 2013 2014 2015 PP

P-W

eig

hte

d S

hare

Of

Glo

ba

l G

row

th

Gro

ss

Do

mes

tic P

rod

uct

%Y

oY

Emerging Market GDP Growth & Share Of Global Growth

Source: Bloomberg, International Monetary Fund

Emerging Market GDP Growth %YoY Emerging Market Share Of Global Growth

19

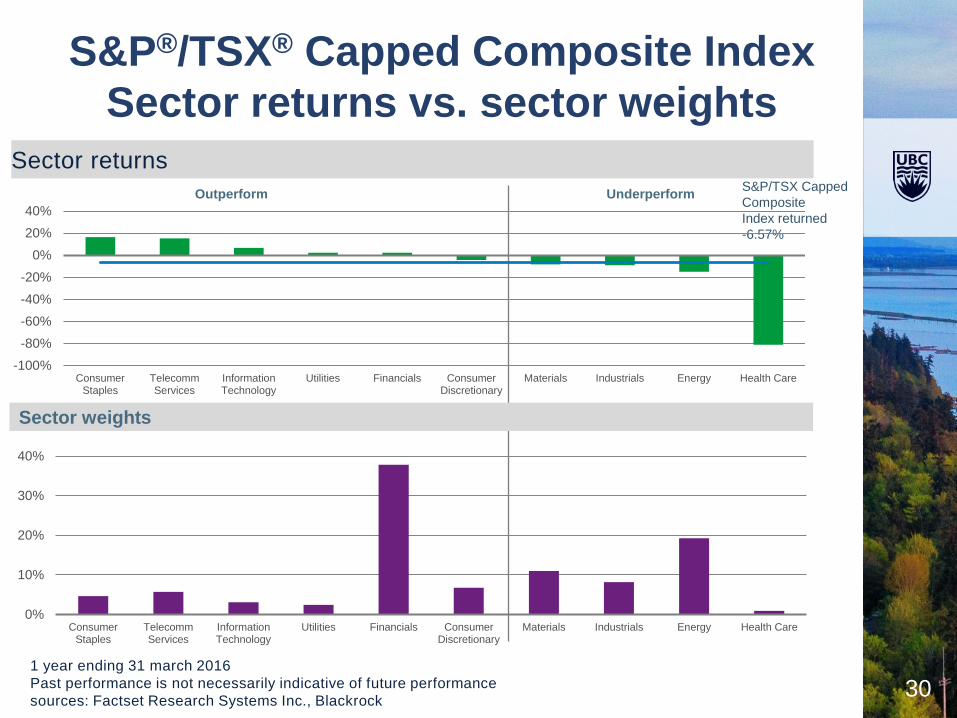

S&P®/TSX® Capped Composite

Index Sector returns vs. sector weights

S&P/TSX Capped

Composite

Index returned

-8.32%

Sector weights

-40%

-20%

0%

20%

InformationTechnology

ConsumerStaples

TelecommServices

ConsumerDiscretionary

Financials Utilities Industrials Health Care Materials Energy

Outperform Underperform

0%

10%

20%

30%

40%

InformationTechnology

ConsumerStaples

TelecommServices

ConsumerDiscretionary

Financials Utilities Industrials Health Care Materials Energy

1 year ending 31 December 2015

Past performance is not necessarily indicative of future performance

Sources: FactSet Research Systems Inc., BlackRock

20

0.7

0.72

0.74

0.76

0.78

0.8

0.82

0.84

0.86

0.88

Dec-1

4

Jan-15

Feb-15

Mar-1

5

Apr-1

5

May-1

5

Jun-15

Jul-1

5

Aug-1

5

Sep-15

Oct-15

Nov-1

5

Dec-1

5The Canadian Dollar

Currency Added Over 19% to the Canadian Dollar S&P 500 Return in 2015.

21

2015 Global Market Performance

Stock Market (YTD) Local

Currency

Canadian

Dollars

Japan 9.9% 30.7%

Europe (Ex. U.K.) 8.3% 18.5%

United States 0.7% 20.1%

United Kingdom -2.2% 10.3%

Canada -9.0% -9.0%

Pacific (Ex. Japan) -1.0% 9.2%

MSCI World 2.1% 18.3%

Emerging Markets -5.8% 1.5%

* Source: MSCI Developed & Emerging Market Indices

22

It Was A Challenging Year For Canadian

Equities

-70.0%

-50.0%

-30.0%

-10.0%

10.0%

30.0%

50.0%

De

nm

ark

Ire

land

Be

lgiu

m

Au

str

ia

Ita

ly

Fin

land

Ne

the

rla

nd

s

Po

rtu

ga

l

Fra

nce

Ja

pa

n

Germ

any

Ne

w Z

ea

land

Sw

ede

n

Un

ite

d S

tate

s

Sw

itze

rlan

d

No

rway

Au

str

alia

Ho

ng

Ko

ng

United K

ingdom

Sp

ain

Canada

Sin

ga

po

re

Gre

ece

MSCI Country Performance (in LocalCurrency)

Canada was among the worst performing countries in the developed world.

23

Interest Rates Moved

Down Last Year

Canada Bond Yields 2012 2013 2014 2015

Overnight Lending Rate 1.00% 1.00% 1.00% 0.50%

5 Year 1.38% 1.94% 1.41% 0.73%

10 Year 1.80% 2.75% 1.87% 1.39%

30 Year 2.36% 3.23% 2.35% 2.15%

24

1 year ending 31 December 2015

Past performance is not necessarily indicative of future performance

Sources: BlackRock; FTSE TMX Global Debt Capital Markets Inc.

Sector & term returns

Canadian bond market

Sector returns vs. sector weights

FTSE TMX Canada

Universe Bond

Index returned

3.52%

Sector & term weights

0%

1%

2%

3%

4%

5%

6%

Provincials Municipals Federal Corporates Short Mid Long

0%

10%

20%

30%

40%

50%

Provincials Municipals Federal Corporates Short Mid Long

Sector Term

25

2.1%

2.8%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

0 5 10 15 20 25 30

Tenor

Spot 1Yr

2Yr 3Yr

4Yr 5Yr

Low yields could be persistent Market pricing less than 1% move over the next 5 years

The markets are saying "lower for longer"

Source: Bloomberg as of 30 September 2015.

26

Long Term Market Returns Investment Results

Growth of $100 from December 1949 to December 2015

U.S. Stocks in $C: $135,661 (11.6%)

Canadian Stocks: $43,194 (9.6%)

Bonds (Long): $11,759 (7.5%)

T-Bills: $3,180 (5.4%)

Inflation: $1,038 (3.6%)

$100

$1,000

$10,000

$100,000

1949 1955 1961 1967 1973 1979 1985 1991 1997 2003 2009 2015

27

Benefits of a Diversified Portfolio

Last 5

Years 2010 2000 1990 1980

TSX Composite 2.3% 4.2% 10.6% 3.7% 9.1%

S&P 500 (C$) 20.3% -4.5% 17.9% 9.0% 5.6%

MSCI EAFE (C$) 10.7% -3.0% 9.4% 13.9% 11.1%

10 Year Annualized Returns As of December 31

Best Performer

28

Summary of 2015

28

• Good results for 2015. Balanced Fund up 6.6%

over 1 year and 6.9% over 10 years.

• Foreign equities had strongest returns, depreciating

dollar helped

• Low oil prices and commodity prices hurt Canadian

returns

• Bond returns were low, reflecting low interest rates

• Central Bank policies continue to have a big impact

on markets throughout the world

29 29

Results to March 31, 2016

30

Sector returns

1 year ending 31 march 2016

Past performance is not necessarily indicative of future performance

sources: Factset Research Systems Inc., Blackrock

S&P®/TSX® Capped Composite Index

Sector returns vs. sector weights

S&P/TSX Capped

Composite

Index returned

-6.57%

Sector weights

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

ConsumerStaples

TelecommServices

InformationTechnology

Utilities Financials ConsumerDiscretionary

Materials Industrials Energy Health Care

Outperform Underperform

0%

10%

20%

30%

40%

ConsumerStaples

TelecommServices

InformationTechnology

Utilities Financials ConsumerDiscretionary

Materials Industrials Energy Health Care

31

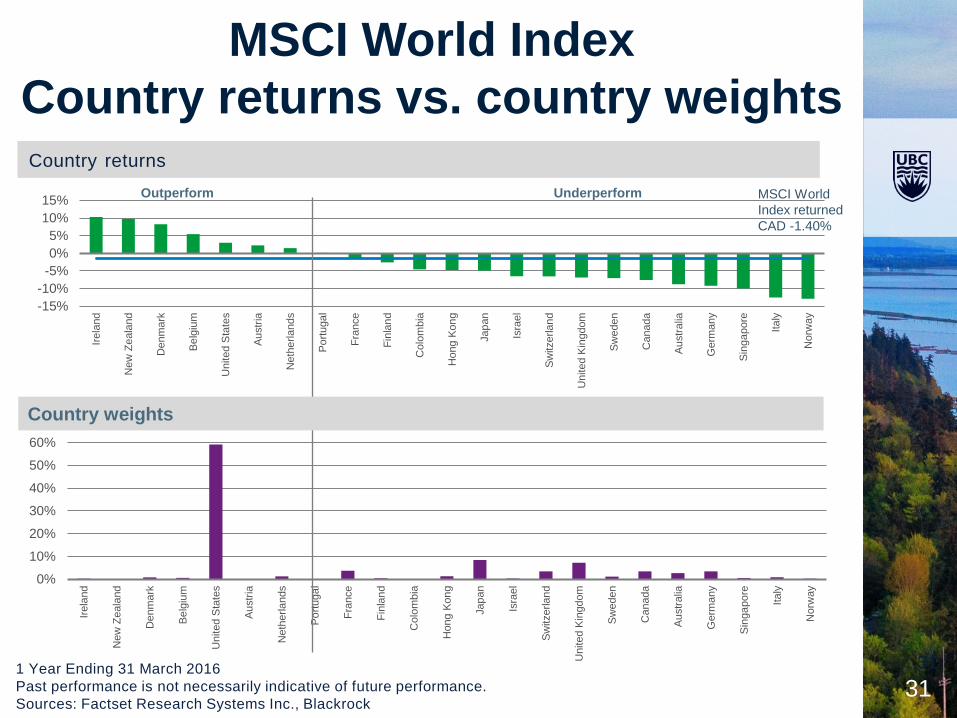

Country returns

1 Year Ending 31 March 2016

Past performance is not necessarily indicative of future performance.

Sources: Factset Research Systems Inc., Blackrock

MSCI World Index

Country returns vs. country weights

31

MSCI World

Index returned

CAD -1.40%

0%

10%

20%

30%

40%

50%

60%

Irela

nd

New

Ze

ala

nd

Denm

ark

Be

lgiu

m

United S

tate

s

Au

str

ia

Neth

erla

nds

Po

rtuga

l

Fra

nce

Fin

lan

d

Colo

mb

ia

Hong K

on

g

Jap

an

Isra

el

Sw

itzerlan

d

United K

ingdom

Sw

eden

Canada

Au

str

alia

Germ

any

Sin

ga

pore

Italy

Norw

ay

Outperform Underperform

-15%

-10%

-5%

0%

5%

10%

15%

Irela

nd

New

Ze

ala

nd

Denm

ark

Be

lgiu

m

United S

tate

s

Au

str

ia

Neth

erla

nds

Po

rtuga

l

Fra

nce

Fin

lan

d

Colo

mb

ia

Hong K

on

g

Jap

an

Isra

el

Sw

itzerlan

d

United K

ingdom

Sw

eden

Canada

Au

str

alia

Germ

any

Sin

ga

pore

Italy

Norw

ay

Country weights

32

32

Fund Rates of Return*

(to March 31, 2016)

* Before investment manager fees

Fund Q1/2016 1 Yr. 5 Yrs. 10 Yrs.

Balanced Fund -0.66% -0.2% 8.33% 6.37%

Bond Fund 1.59% 0.43% 5.10% 5.49%

Canadian Equity Fund 4.23% -5.3% 4.72% 5.71%

Foreign Equity Fund -6.25% 0.06% 14.71% 5.94%

Short Term Investment Fund 0.17% 0.76% 1.19% 1.80%

33

Change in Equity Leadership

Source: Thomson Reuters Datastream

-20%

-15%

-10%

-5%

0%

5%

10%

Energy Materials Canada EM

Select Global Relative Equity Index Returns

Jan 1, 2015 to Feb 11, 2016

Feb 11, 2016 to Mar 31, 2016

34

• Returns have been more muted recently

and volatility remains quite high

• Our large plan size ($2 billion) allows for

lower fees and broader diversification by

asset classes and managers

• The move to Sun Life did not have an

impact on the investment options

currently provided

Conclusions

34

35

35

Thank You!

Questions?

36 36 36

Administrative Staff

Orla Cousineau Executive Director, Pensions

Mike Leslie Executive Director – Investments

Debbie Wilson Associate Director

GV Fragante Systems Analyst

Helena Huynh Systems Analyst

Diana Iampietro Faculty Pension Plan Manager

Lorraine Heseltine Member Services Specialist

Lily Lee Member Services Associate

Louise Mah Pension Clerk

Maricres De Leon Pension Plan Accountant

Kathy Pang Communications Manager

Chelsey Maher Communications Assistant

Shirley Lim Project Coordinator

Claudia Chan Office Administrator

37

37

Plan Considerations

• Lower risk through broad diversification

- 12 Managers, 13 Mandates

• Provide flexibility regarding contribution,

investment, retirement and withdrawal options

• Low cost

• High level of member service

• One part of member’s overall retirement plan