unaudited condensed consolidated interim financial ... 2014... · unaudited condensed consolidated...

TRANSCRIPT

1

Unaudited Condensed Consolidated Interim Financial Statements

As at and for the Three months Ended March 31, 2014

2

COUNSEL CORPORATION CONDENSED CONSOLIDATED INTERIM STATEMENTS OF FINANCIAL POSITION AS AT MARCH 31, 2014 AND DECEMBER 31, 2013 (In thousands of Canadian dollars)

The accompanying notes are an integral part of these condensed consolidated interim financial statements.

March 31, December 31,

2014 2013

Notes $ $

Assets

Current assets

Cash and cash equivalents 11(i) 11,880 17,580

Marketable securities 413 410

Mortgages, loans, accounts and deferred interest receivable 6 36,009 22,004

Prepaid expenses, deposits and deferred charges 7 4,875 4,655

Shares held for dividend-in-kind 21 15,749 -

Assets of discontinued operations 21 863 18,415

69,789 63,064

Non-current assets

Deferred interest and mortgages receivable 6 17,871 19,403

Deferred charges 7 36,753 35,508 Property, plant and equipment 8 3,659 3,079

Portfolio investments 10 65,006 53,220 Intangible assets 9(a) 5,471 5,594

Goodwill 9(b) 24,919 24,919

Other assets 49 49

Assets of discontinued operations 21 622 53,367

Total assets 224,139 258,203

Liabilities

Current liabilities

Accounts payable and accrued liabilities 11 31,279 29,458

Dividend payable 21 15,749 -

Income taxes payable 2 4

Current portion of mortgages and loans payable 12 9,003 14,025

Contingent consideration 5 4,027 4,027

Liabilities of discontinued operations 21 1,021 20,550

61,081 68,064

Non-current liabilities

Mortgages and loans payable 12 11,069 6,703

Contingent consideration 5 4,672 4,543

Deferred income tax l iabilities 20 10,746 9,349

Derivative l iability 12(ii) 3 9

Liabilities of discontinued operations 21 238 318

Total liabilities 87,809 88,986

Equity

Share capital 15 203,714 203,333

Share based compensation 12,315 12,202

Foreign currency translation 273 2,392

Contributed surplus 50,215 50,215

Accumulated other comprehensive income (loss) (498) -

Retained earnings (deficit) (174,210) (152,035)

Shareholders' equity 91,809 116,107

Non-controlling interest 44,521 53,110

Total equity 136,330 169,217

Total liabilities and equity 224,139 258,203

Commitments, contingencies and guarantees 14

3

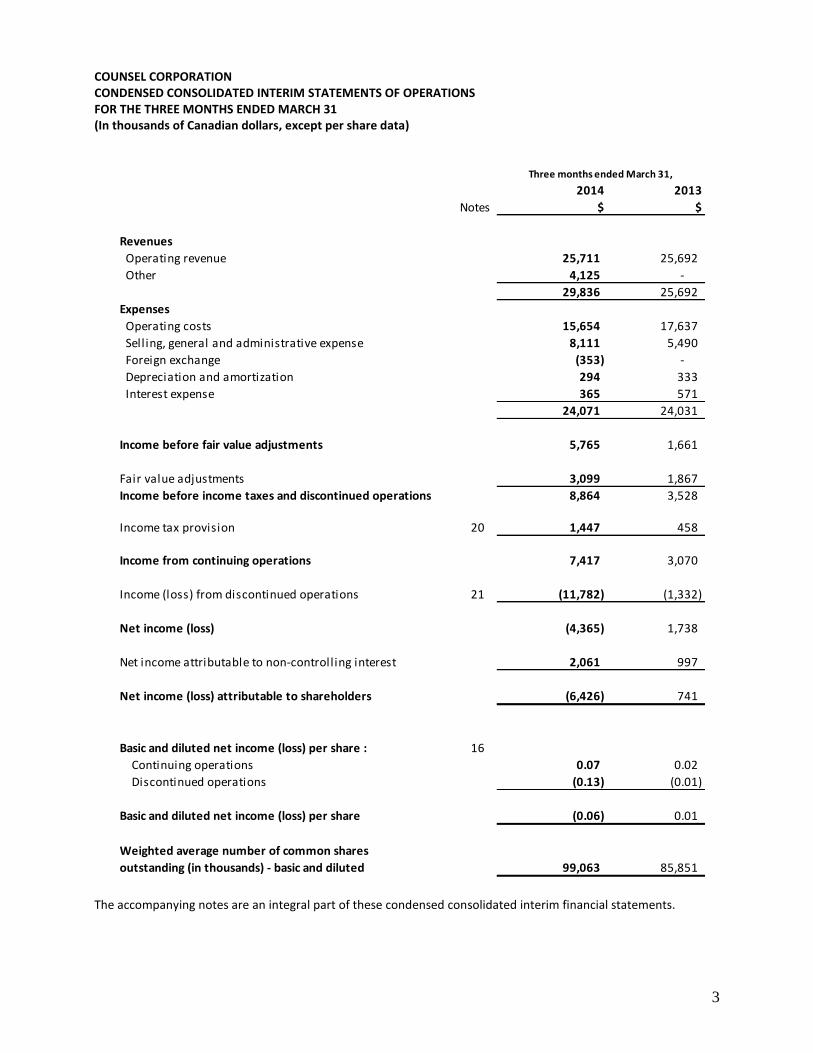

COUNSEL CORPORATION CONDENSED CONSOLIDATED INTERIM STATEMENTS OF OPERATIONS FOR THE THREE MONTHS ENDED MARCH 31 (In thousands of Canadian dollars, except per share data)

The accompanying notes are an integral part of these condensed consolidated interim financial statements.

2014 2013

Notes $ $

Revenues

Operating revenue 25,711 25,692

Other 4,125 -

29,836 25,692

Expenses

Operating costs 15,654 17,637

Selling, general and administrative expense 8,111 5,490

Foreign exchange (353) -

Depreciation and amortization 294 333

Interest expense 365 571

24,071 24,031

Income before fair value adjustments 5,765 1,661

Fair value adjustments 3,099 1,867

Income before income taxes and discontinued operations 8,864 3,528

Income tax provision 20 1,447 458

Income from continuing operations 7,417 3,070

Income (loss) from discontinued operations 21 (11,782) (1,332)

Net income (loss) (4,365) 1,738

Net income attributable to non-controlling interest 2,061 997

Net income (loss) attributable to shareholders (6,426) 741

Basic and diluted net income (loss) per share : 16

Continuing operations 0.07 0.02

Discontinued operations (0.13) (0.01)

Basic and diluted net income (loss) per share (0.06) 0.01

Weighted average number of common shares

outstanding (in thousands) - basic and diluted 99,063 85,851

Three months ended March 31,

4

COUNSEL CORPORATION CONDENSED CONSOLIDATED INTERIM STATEMENTS OF COMPREHENSIVE INCOME (LOSS) FOR THE THREE MONTHS ENDED MARCH 31 (In thousands of Canadian dollars)

The accompanying notes are an integral part of these condensed consolidated interim financial statements.

2014 2013

$ $

Net income (loss) (4,365) 1,738

Other comprehensive income (loss)

Reclassification of cumulative currency translation

adjustment - continuing operations to income (440) 170

Reclassification of cumulative currency translation

adjustment - discontinued operations to income (1,679) 396

Fair value adjustment of shares held for dividend-in-kind* (498) - (2,617) 566

Comprehensive income (loss) (6,982) 2,304

Comprehensive income (loss) attributable to:

Shareholders (9,097) 1,183

Non-controlling interest 2,115 1,121

(6,982) 2,304

*All items recorded in other comprehensive income will be relcassified in subsequent periods to net income

Three months ended March 31,

5

COUNSEL CORPORATION CONDENSED CONSOLIDATED INTERIM STATEMENTS OF CHANGES IN EQUITY FOR THE THREE MONTHS ENDED MARCH 31 (In thousands of Canadian dollars)

The accompanying notes are an integral part of these consolidated financial statements.

Accumulated

Share Foreign other Retained

capital Share based currency Contributed comprehensive earnings Non-controlling Total

(Note 15) compensation translation Surplus income (loss) (deficit) Total Interest equity

Notes $ $ $ $ $ $ $ $ $

Balance - December 31, 2012 188,349 8,627 498 49,579 75 (161,576) 85,552 61,449 147,001

Exercise of stock options 15 83 - - - - - 83 - 83

Net investment by non-controlling interest - - 124 - - - 124 (4,388) (4,264)

Share based compensation - (62) - - - - (62) - (62)

Foreign currency translation adjustment - - 442 - - - 442 124 566

Net income - - - - - 741 741 997 1,738

Balance - March 31, 2013 188,432 8,565 1,064 49,579 75 (160,835) 86,880 58,182 145,062

-

Exercise of stock options 15 2,509 - - - - - 2,509 - 2,509

Net investment by non-controlling interest - 275 - - - 275 (8,149) (7,874)

Conversion of convertible debentures 12,000 - - - - - 12,000 - 12,000

Employee share purchase loan repayment 392 - - 636 - - 1,028 - 1,028

Share based compensation - 3,637 - - - - 3,637 - 3,637

Foreign currency translation adjustment - - 1,053 - - - 1,053 275 1,328

Net income - - - - (75) 8,800 8,725 2,802 11,527

Balance - December 31, 2013 203,333 12,202 2,392 50,215 - (152,035) 116,107 53,110 169,217

Exercise of stock options 15 - - - - - - - - -

Net investment by non-controlling interest - - 54 - - - 54 (10,704) (10,650)

Conversion of convertible debentures - - - - - - - - -

Employee share purchase loan 381 - - - - - 381 - 381

Share based compensation - 113 - - - - 113 - 113

Foreign currency translation adjustment - - (2,173) - - - (2,173) 54 (2,119)

Dividends declared (in-kind) - - - - - (15,749) (15,749) - (15,749)

Change in fair value of available for sale investment - - - - (498) - (498) - (498)

Net income (loss) - - - - - (6,426) (6,426) 2,061 (4,365)

Balance - March 31, 2014 203,714 12,315 273 50,215 (498) (174,210) 91,809 44,521 136,330

Attributable to shareholders of the Company

6

COUNSEL CORPORATION CONDENSED CONSOLIDATED INTERIM STATEMENTS OF CASH FLOWS FOR THE THREE MONTHS ENDED MARCH 31 (In thousands of Canadian dollars)

The accompanying notes are an integral part of these consolidated financial statements.

2014 2013

$ $

Cash provided by (used in)

Operating activities

Income from continuing operations 7,417 3,070

Non-cash items

Deferred income taxes 1,447 458

Depreciation and amortization 294 333

Fair value adjustments for contingent consideration 129 181

Amortization of deferred financing and other costs 107 118

Fair value adjustments (3,170) (445)

Share based compensation 113 410

Deferred share unit plan expense - 290

Changes in non-cash working capital related to operations

(Increase) decrease in accounts receivable (9,973) (138)

(Increase) decrease in deferred charges (1,535) (2,098)

(Increase) decrease in other assets (303) 94

Increase (decrease) in accounts payable and accrued liabilities 1,821 (3,780)

Cash provided by continuing operations (3,653) (1,507)

Cash provided by (used in) discontinued operations 233 (514)

(3,420) (2,021)

Investing activities

Distributions from portfolio investments 378 5,648

Investment in portfolio investments - (38)

Discontinued operations (82) 592

296 6,202

Financing activities

Proceeds from mortgages and loans payable 100 1,051

Repayment of mortgages and loans payable 138 (866)

Exercise of stock options - 83

Non-controlling interest (2,743) (4,826)

Discontinued operations (24) (6,281)

(2,529) (10,839)

Increase (decrease) in cash and cash equivalents (5,653) (6,658)

Cash and cash equivalents - beginning of period 17,580 13,977

Cash and cash equivalents - end of period 11,927 7,319

Less: Cash - discontinued operations 47 1,781

Cash and cash equivalents - continuing operations 11,880 5,538

Represented by:

Cash and cash equivalents 1,799 5,538

Restricted cash represented by funds held in trust 10,081 -

Total - Cash and cash equivalents - continuing operations 11,880 5,538

Supplementary information

Cash paid (received) during the period

Interest received (87) (87)

Interest paid 536 529

Income taxes - 39

Effects of exchange rate changes on the

balance of cash held in foreign currencies 59 10

Non-cash investing and financing activities:

Dividend in kind of Heritage Global Inc. 15,749 -

Sale of real estate investment 1,000 -

Three monthss ended March 31

7

COUNSEL CORPORATION NOTES TO CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS March 31, 2014 (In thousands of Canadian dollars, except per share data) 1. General information

Counsel Corporation (“Counsel” or “the Company”), founded in 1979, is a financial services company. The address of its registered office is 1 Toronto Street, Suite 700, P.O. Box 3, Toronto, Ontario, M5C 2V6. Counsel currently operates principally as a mortgage lending business. Counsel carries on its mortgage lending business (“Mortgage Lending”) through its subsidiary, Street Capital Financial Corporation (“Street Capital”). Street Capital is a Canadian residential mortgage lender. Counsel acquired Street Capital on May 31, 2011. Counsel owns a private equity business (“Private Equity”) through a wholly-owned subsidiary, Knight’s Bridge Capital Partners Inc. (“Knight’s Bridge”). Knight’s Bridge is responsible for managing a private equity investment fund which it founded in 2008. In the first quarter of 2013, the Company decided to discontinue its non-core operating businesses, namely, its Asset Liquidation (through Heritage Global Inc.), Case Goods (through Fleetwood Fine Furniture LP) and Real Estate businesses.

2. Basis of preparation

The Company prepares its financial statements in accordance with Canadian generally accepted accounting principles as set out in the Handbook of the Chartered Professional Accountants (“CPA”) Canada Handbook (“CPA Handbook”). The interim condensed consolidated financial statements have been prepared in accordance with IAS 34 – interim financial Reporting under International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”) and using the accounting policies the Company applied in its consolidated financial statements as of and for the year ended December 31, 2013 except for the adoption of new standards and amendments effective January 1, 2014 described in Note 3. The accounting policies the Company applied in its annual consolidated financial statements as of and for the year ended December 31, 2013, are disclosed in Note 3 of such financial statements with which reference should be made in reading these interim condensed and consolidated financial statements. The condensed consolidated interim financial statements are presented in Canadian dollars, except when otherwise indicated.

3. Summary of accounting policies

Consolidation These consolidated financial statements include the accounts of the Company and its consolidated subsidiaries, which are entities over which the Company has control. Control exists when the Company has the power, directly or indirectly, to govern the financial and operating policies of an entity so as to obtain benefit from its activities. Furthermore, effective January 1, 2013, IFRS 10 requires the consolidation of an investee only if the investor possesses power over the investee, has exposure to variable returns from its investment with the investee and has the ability to use its power over the investee to affect its returns. Non-controlling interests in the equity and results of the Company’s subsidiaries are shown separately in the consolidated statement of changes in equity. Intercompany balances and transactions among the Company and its subsidiaries are eliminated on consolidation. The Company's principal subsidiaries comprising continuing and discontinued operations and its respective ownership interest in each subsidiary as at March 31, 2014 and December 31, 2013 are as follows:

8

(i) As of March 31, 2014, the Company disposed of its interests in both HGI and Fleetwood via a dividend-in-kind and sale of majority interest, respectively, (see Note 21 for further details on the dispositions).

Non-controlling interest Non-controlling interest represents equity interests in subsidiaries and controlled assets owned by outside parties. The share of net assets of subsidiaries attributable to non-controlling interest is presented as a separate component within equity. Their share of net income (loss) and comprehensive income (loss) is recognized directly in equity. Changes in the Company’s ownership interest in subsidiaries that do not result in a loss of control are accounted for as equity transactions.

Future accounting changes Financial Instruments – The IASB has issued a new standard, IFRS 9 “Financial Instruments”, which will ultimately replace IAS 39, “Financial Instruments: Recognition and Measurement”. The replacement of IAS 39 is a multi-phase project with the objective of improving and simplifying the reporting for financial instruments and the issuance of IFRS 9 is part of the first phase. In November 2013, the IASB removed the mandatory effective date of January 1, 2015 and has not proposed a future effective date. The Company has yet to assess the impact of the new standard on its results of operations, financial position and disclosures. Recently adopted accounting standards and amendments Financial instruments: Presentation -Amendment to IAS 32, Financial Instruments: Presentation on asset and liability offsetting clarifies some of the requirements for offsetting financial assets and financial liabilities on the statement of financial position. The amendment to this standard is effective for annual periods beginning on or after January 1, 2014. The adoption of this amendment did not have a significant impact on the Company’s results of operations, financial position and disclosures. Impairment of assets - Amendment to IAS 36, Impairment of Assets establishes the disclosure of information about the recoverable amount of impaired assets if that amount is based on fair value less cost of disposal. The amendment to this standard is effective for annual periods beginning on or after January 1, 2014. The adoption of this amendment did not have a significant impact on the Company’s results of operations, financial position and disclosures.

4. Critical accounting estimates, assumptions and judgments

The preparation of consolidated financial statements in accordance with IFRS requires the use of estimates, assumptions and judgments that in some cases relate to matters that are inherently uncertain, and which

March 31, December 31,

2014 2013

% %

Street Capital Financial Corporation 100.0 100.0

Knight's Bridge Capital Partners Inc. 100.0 100.0

Heritage Global Inc. ("HGI")* (i) - 73.3

Heritage Global LLC ("HG LLC")* - 100.0

Heritage Global Partners, Inc. ("HGP")* - 100.0

Fleetwood Fine Furniture LP ("Fleetwood")* (i) - 71.2

*Business units reclassified as discontinued operations in the first quarter of 2013

9

affect the amounts reported as assets, liabilities, revenue and expense in the consolidated financial statements and accompanying notes. Key areas of such estimation are: re-measurement at fair value of financial instruments, valuations of receivables (i.e. duration factors on deferred interest receivable) and inventories, impairment of property, plant and equipment, portfolio investments, intangibles and goodwill, provisions, accounting accruals, the useful life and residual value of certain assets, accounting for deferred income taxes, and allowance for credit losses. Allowance for credit losses represent management’s best estimate of losses incurred in our loan portfolio at the date of the statement of financial position and requires management’s judgment in making assumptions and estimations. The determination of the Company’s deferred tax asset or liability requires significant management judgment as the recognition is dependent on management’s projection of future taxable profits and tax rates expected to be in effect in the period in which the asset is realized or the liability settled. The classification, presentation and measurement of discontinued operations also involved significant estimates, assumptions and judgments. Changes to estimates and assumptions may affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenue and expense during the reporting period. Actual results could also differ from those estimates under different assumptions and conditions. Fair value of portfolio investments not quoted in an active market - The fair values of portfolio investments that are not quoted in an active market are determined by using valuation techniques, primarily earnings multiples, discounted cash flows and recent comparable transactions. The inputs in the earnings multiples models include observable data, such as earnings multiples of comparable companies to the relevant portfolio company, and unobservable data, such as forecast earnings for the portfolio company. In discounted cash flow models, unobservable inputs are the projected cash flows of the relevant portfolio company and the risk premium for liquidity and credit risk that are incorporated into the discount rate. Critical judgments include the determination of CGUs and the allocation of certain costs among the CGUs, and the determination of depreciation and amortization periods for property, plant and equipment and intangible assets.

5. Acquisitions

On May 31, 2011, Counsel completed the acquisition of Street Capital Financial Corporation (“Street Capital”). Street Capital is a Canadian prime residential mortgage lender. The purchase price was satisfied through a combination of the issuance of 6,616,664 common shares of Counsel and approximately $28,000 in cash. Counsel financed the purchase price through a $17,500 acquisition debt facility provided by a Canadian chartered bank and a private placement of convertible unsecured subordinated debentures for gross proceeds of $12,000. In support of the loan of $17,500, the Company provided a limited recourse guarantee of amounts outstanding under the loan. The Company directly and indirectly pledged the shares it owns in Street Capital and its subsidiaries as well as provided general security over the assets of, and a guarantee from, Street Capital and one of its subsidiaries.

In addition the Company agreed to pay earn-out payments if specified future events occur (the “contingent consideration”). Under the contingent consideration arrangement, the Company expected to pay certain members of management of Street Capital a total of approximately $10,900 in cash over the three fiscal years beginning in 2013 upon the achievement of specific earnings targets. The contingent consideration, valued at $10,353 on acquisition, has an estimated fair value of $8,699 at March 31, 2014 (December 31, 2013 - $8,570). During the second quarter of 2013, the first earn out payment of $4,026 was made. The remaining $8,570 of contingent consideration is allocated between current and long term liabilities of $4,027 and $4,672, respectively.

The members of management who are entitled to the contingent consideration also have the right to participate in the future value creation in Street Capital so long as they remain employed by the Company until at least December 31, 2018. However, if Street Capital achieves certain cumulative earnings targets, which

10

are significantly in excess of historic earnings at the date of acquisition, they will be entitled to earlier payouts during the three-year period 2017 to 2019. Due to risks and uncertainties arising from macro-economic changes affecting the Canadian real estate and mortgage lending sectors that could impact future earnings, qualification for and timing of regulatory approvals for Street Capital to become a Schedule I bank, fulfillment of minimum contractual terms of employment by Street Capital management, and achievement by Street Capital of earnings targets significantly in excess of historical earnings, management’s entitlement to early payment of their share of any future value creation is considered to be remote. In light of the aforementioned, the amount of such potential payment cannot be practicably estimated at this time.

The acquisition has been accounted for using the acquisition method in accordance with IFRS 3 “Business Combinations”. In determining the purchase price of the acquisition the Company included the estimated fair value of any contingent consideration. The Company recognized the acquisition date fair value of the contingent consideration as part of the consideration transferred in exchange for Street Capital. The acquisition date fair value of the contingent consideration is based on management’s assessment and may decrease or increase substantially depending upon the financial performance of Street Capital each year through and including the year ending December 31, 2018 or in the event of a sale of Street Capital. As of the acquisition date, the Company allocated the purchase price among the identifiable assets acquired and the liabilities assumed. Any excess purchase price was recognized as identified intangible assets and goodwill.

6. Mortgages, accounts and deferred interest receivable

Mortgages, accounts and deferred interest receivable consist of the following:

Accounts receivable include trade receivables, harmonized sales taxes and any other amounts receivable excluding mortgages and deferred interest receivable. Deferred interest receivable is the excess interest rate spread to be received over the remaining life of mortgages that have been placed with or sold to third parties. The balance represents the present value of this excess interest spread calculated based on the contractually agreed duration factor of the underlying mortgages sold. Mortgages receivable are carried at cost. Provisions are made for probable losses on mortgages based upon a number of factors, including previous loss experience, time value of money, current economic conditions and other related factors.

7. Prepaid expenses, deposits and deferred charges Deferred charges of $41,424 represent prepaid mortgage portfolio insurance premiums on mortgage pools, which are amortized over the average term of the underlying mortgages. The other prepaid expenses of

11

$204 are comprised of prepaid operating expenses which will be expensed within the next twelve months.

8. Property, plant and equipment

Property, plant and equipment consist of the following:

A reconciliation of the carrying amount of property, plant and equipment from the end of 2012 to the end of the current fiscal period is set out below:

9. Goodwill and intangible assets

(a) Intangible assets

Details of the Company’s intangible assets are as follows:

Furniture,

fixtures & Information Leasehold

Artwork office equipment systems improvements Vehicles Total

$ $ $ $ $ $

Balance at December 31, 2012 2,148 516 312 225 15 3,216

Additions - 144 716 - - 860

Depreciation - (126) (662) (53) - (841)

Transferred to discontinued operations - (84) (38) (19) (15) (156)

Balance at December 31, 2013 2,148 450 328 153 - 3,079

Additions - 616 133 - - 749

Depreciation - (61) (101) (7) - (169)

Balance at March 31, 2014 2,148 1,005 360 146 - 3,659

12

(i) Amortization expense for the mortgage renewal stream related to the acquisition of Street Capital

for the three months ended March 31, 2014 was $123 (2013 – $494). The amortization period of 15 years is based on historical renewal rates and industry benchmarks.

(b) Goodwill

Goodwill, arising from business acquisition transactions, is detailed as follows:

No impairment to goodwill from continuing operations was determined for the first three months of 2014 (2013 - $nil).

10. Portfolio investments The Company’s portfolio investments consist of:

The H Company Holdings, LLC (“Halston”) is a New York based company that designs, markets, distributes and licenses apparel, accessories and home products under the Halston brand. In the first quarter of 2007, Counsel acquired approximately 1.2% of Halston for US$375. In the first quarter of 2008, Counsel made an additional investment of US$100 in Halston. No fair value adjustments were recorded for the first three months of 2014 or in fiscal 2013.

Fleetwood Fine Furniture International LP (“Fleetwood”) is a private equity investment that was established to acquire the business of Fleetwood Fine Furniture LP in the first quarter of 2014. Fleetwood provides high quality customized case goods to large, upscale hotel chains. Established in 1972, Fleetwood serves a focused niche, being the upscale and upper upscale strata of the hospitality industry.

March 31, December

2014 2013

$ $

Street Capital 23,465 23,465

Knight's Bridge 1,454 1,454

24,919 24,919

March 31, December

2014 2013

$ $

The H Company Holdings, LLC 100 100

Fleetwood Fine Furniture International LP 9,000 -

Knight's Bridge Capital Partners Fund I investments 55,906 53,120

65,006 53,220

13

Knight’s Bridge Capital Partners Fund I (“KBCP Fund I”) is a private equity investment fund sponsored by

Knight’s Bridge, which seeks to invest in small to mid-market companies, primarily throughout North

America and in a variety of industries, which require between $1,000 and $10,000 in equity financing. KBCP Fund I closed on March 7, 2008 with capital commitments in excess of $62,000, including $10,000 of capital committed by Counsel and approximately $5,000 of capital committed by senior management. At March 31, 2014, Counsel has invested approximately $8,300 in KBCP Fund I.

Counsel has determined that it controls KBCP Fund I and therefore consolidates the fund. The factors that the Company considered in making this determination include that its wholly owned subsidiary is the General Partner of the Fund and it can appoint the persons who sit on the investment committee. The non-controlling interest in KBCP Fund I held by the other limited partners amounts to $47,196 at the end of Q1 2014 (2013 - $44,473). Counsel has the right to a 2% per annum management fee based on aggregate capital commitments for the first 5 years following the closing of KBCP Fund I, and thereafter, a 2% per annum management fee calculated based on capital invested by KBCP Fund I. Counsel also is entitled to a carried interest of 20% of the total profits realized by KBCP Fund I so long as investors have received the return of their contributed capital and a minimum 8% per annum preferred return on their invested capital. As of March 7, 2013, KBCP Fund I may no longer make capital calls for new acquisitions. It may however continue to call for funds from existing investors for further investments in existing portfolio companies and for management fees.

All investments made through the fund are measured and reported at fair value. The fair value of portfolio investments is determined by using valuation techniques where third party valuations are not available. The Company uses a variety of methods and makes assumptions that are based on the portfolio investments’ performance, and market conditions existing at each reporting date. Valuation techniques used include the use of comparable recent arm’s length transactions, earnings multiple based valuation, discounted cash flow analysis, and other valuation techniques commonly used by market participants making the maximum use of available market inputs and relying as little as possible on entity-specific inputs. Changes in the methodologies, assumptions and judgment used to value portfolio investments could have a material impact on the reported fair value and consequently on the Company’s results of operations. The net income attributable to non-controlling interest for the period ended March 31, 2014 was $1,008 (2013 - $6,901).

A reconciliation of the carrying amount of portfolio investments from the end of 2012 through to March 31, 2014 is set out below:

$

Balance at December 31, 2012 53,454

Acquisitions and investments 4,594

Fair value adjustments 6,583

Foreign exchange adjustments 3,213

Distributions (14,124)

Reclassified as discontinued operations (500)

Balance at December 31, 2013 53,220

Acquisitions and investments 9,000

Fair value adjustments 1,141

Foreign exchange adjustments 2,023

Distributions (378)

Reclassified as discontinued operations -

Balance at March 31, 2014 65,006

14

11. Accounts payable and accrued liabilities

Details of accounts payable and accrued liabilities from continuing operations are as follows:

(i) Included in cash and cash equivalents is approximately $10,081 (2013 - $12,714) of restricted cash

representing funds held in trust by the Mortgage Lending business. Of these, $347 (2013 - $5,443) are held for purposes of funding third party mortgage loans and $9,734 (2013 - $7,271) represents mortgage loan repayments collected on behalf of a third party servicer.

12. Mortgages and loans payable

Details of mortgages and loans payable are as follows:

(i) The total financing costs netted in the mortgages and loans payable was $71 at March 31, 2014 ($178 at December 31, 2013).

(ii) On May 31, 2011, Counsel financed the purchase of Street Capital through a $17,500 term debt facility

provided by a Canadian chartered bank. The term debt bears interest at BA+4% and matures on May 31, 2014. The Company entered into a floating to fixed interest rate swap to mitigate the risk of movement in the BA curve. This derivative instrument is marked to market at the end of each reporting period

March 31, December

2014 2013

$ $

Accounts payable (i) 28,918 27,086

Accrued compensation 1,454 1,372

Accrued interest 110 276

Tenant allowances/reserves 399 409

Professional fees 184 203

Due to JV partners and clients - -

Dividends payable - -

Other 214 112

31,279 29,458

Classified as follows:

Current 31,279 29,458

Long-term - -

31,279 29,458

Maturity Interest Current Long- term Current Long- term

date rate Total portion portion Total portion portion

$ $ $ $ $ $

Street Capital - term debt (ii) May 31/14 BA+4% 9,875 - 9,875 10,671 10,671 -

Street Capital - credit facility (ii) prime +2.0% 1,194 - 1,194 1,154 1,154 -

Corporate debt (iii) Various 5%, 6% 9,003 9,003 - 8,903 2,200 6,703

Total debt - continuing operations 20,072 9,003 11,069 20,728 14,025 6,703

Other - reclassified as discontinued operations in Q1 2013 - - - 23,536 - -

Total debt 20,072 9,003 11,069 44,264 14,025 6,703

March 31, 2014 (i) December 31, 2013 (i)

15

with any resulting gains and losses recorded in fair value adjustments. During the first three months of 2014, a loss of $6 was recorded (2013 – loss of $18). The net effect of the floating interest rate on the term debt and fixed rate on the swap contract yields an interest rate of 5.43% on the term debt. This rate was reduced to 4.43 % in the third quarter of 2012 upon achievement of certain covenant requirements. The term debt has principal payments of $350 per quarter starting August 31, 2011 and increasing to $875 per quarter on August 31, 2012 for the remainder of the term, with a balance payable on maturity of $9,100. In addition Street Capital has a revolving credit facility of $2,500, which bears interest at prime plus 2%. The term debt and the revolving credit facility are subject to general security and covenant provisions. In March 2014, the Company extended this term debt and credit facility for an additional year, with a maturity date deemed to be the earlier of May 29, 2015 or when the Company or its subsidiaries obtain a license to carry on business as a bank. The payment terms will continue to require principal repayments of $875 per quarter for the remainder of the term, with a balance payable on maturity of $5,600.

(iii) Counsel currently has term loan facilities of $4,150 and US$2,400 bearing 6% interest per annum

maturing on January 15, 2015. In the second quarter of 2013, an on demand loan facility of $2,100 was arranged bearing interest at 6%. In the third quarter of 2013, an on demand loan facility of $250 was arranged bearing interest at 5%. Counsel repaid $150 of the $250 facility in the fourth quarter of 2013. The debt is not subject to security or covenant provisions.

13. Convertible debentures

Counsel partially financed the acquisition of Street Capital by a non-brokered private placement of convertible unsecured subordinated debentures (the “Debentures”) for gross proceeds of $12,000 on May 31, 2011. The Debentures were originally convertible at $1.25 per common share; however as a result of the payment of a special dividend in kind on January 1, 2013, the conversion rate has been reduced to $1.2264 per common share. The Debentures bear interest at 8% per annum, payable quarterly, in cash on the last day of March, June, September and December of each year, commencing September 30, 2011, and mature on May 31, 2014. The Company has the right to require conversion of the Debentures when the market price per common share is equal to or greater than $1.75 for 20 consecutive trading days. As at the end of the third quarter of 2013, $12,000 of the debentures had been converted to 9,784,735 common shares.

14. Contingencies

Litigation The Company, from time to time, is involved in various claims, legal proceedings and complaints arising in the ordinary course of business. The Company is not aware of any pending or threatened proceedings that would have a material adverse effect on the consolidated financial condition or future results of the Company.

16

Guarantees The Company had guaranteed a mortgage payable on a long-term care facility sold by the Company to a limited partnership in 1985. The mortgage on the facility was assumed by the limited partnership and was guaranteed by the Company. The Company received a fee for this guarantee. The Company has no equity interest in the limited partnership; however, it did receive an annual incentive fee from the partnership based on the limited partnership's financial performance, and was entitled to an incentive fee based on the proceeds of a sale or refinancing of the facility. The facility was sold in the fourth quarter of 2013 resulting in the elimination of the Company’s guarantee obligation. The Company earned an incentive fee of approximately $1,282 as a result of the sale in 2013.

15. Share capital

The authorized capital stock consists of an unlimited number of common and preferred shares. At December 31, 2011 there were 85,147,831 common shares outstanding. In the second quarter of 2012, stock options to purchase 635,000 common shares were exercised. In November 2012, stock options to purchase 50,000 common shares were exercised. In the first quarter of 2013, stock options to purchase 97,544 common shares were exercised. In the second quarter of 2013, stock options to purchase 1,715,000 common shares were exercised and convertible debentures were converted into 5,300,064 common shares. In the third quarter of 2013, stock options to purchase 724,000 common shares were exercised and convertible debentures were converted into 4,484,671 common shares. In the fourth quarter of 2013, stock options to purchase 909,000 common shares were exercised. At March 31, 2014 the Company had share purchase loans receivable of $2,417 (December 31, 2013 - $2,798). The share purchase loans were granted to certain key employees and former employees. The loans are collateralized by the shares purchased and personal guarantees. At March 31, 2014, the share purchase loans outstanding were for the purchase of 780,000 (December 31, 2013 – 937,500) common shares of the Company. These loans have various maturity dates through to January 19, 2016. All the loans are non-interest bearing. A loan which was written down to approximately $392 was repaid in full during the third quarter of 2013, resulting in a recovery of approximately $870 which has been included in contributed surplus. In the first quarter of 2014, a loan was written off resulting in a loss of $381.

On November 7, 2013, the Company’s board of directors amended its Deferred Share Unit Plan (“DSU Plan) for all directors who were not employees of the Company. The DSU Plan was instituted in March 2006 and

17

provided that eligible directors were granted annually that number of deferred share units equal to $20 divided by the closing price of the Company’s common stock on the Toronto Stock Exchange on the trading day immediately preceding the grant. When a DSU holder ceases to be a director, he/she is entitled to be paid for their units based on the closing price of the Company’s common stock on the Toronto Stock Exchange on the trading day immediately following the day they cease to be a director. In June 2011, the Company ceased granting DSUs pursuant to the DSU Plan, with all previously granted DSUs remaining outstanding and to be paid in accordance with the terms of the DSU Plan. The Company and the existing DSU holders have agreed to amend the DSU Plan to provide for payment in shares rather than cash. Consequently the existing DSUs totaling approximately 980,000 units will result in the issuance of the like amount of shares as and when directors retire or cease to be members of the board of directors. Counsel has accounted for the DSU Plan as a liability, marking it to market quarterly and including it in accounts payable and accrued liabilities. Any quarterly change in fair market value was reflected within selling, general and administration expense in the statement of operations. As a result of the amendment on November 7, 2013 there will be no further impact on the statements of operations or statements of financial position and the amount of the liability at that date has been transferred to share capital.

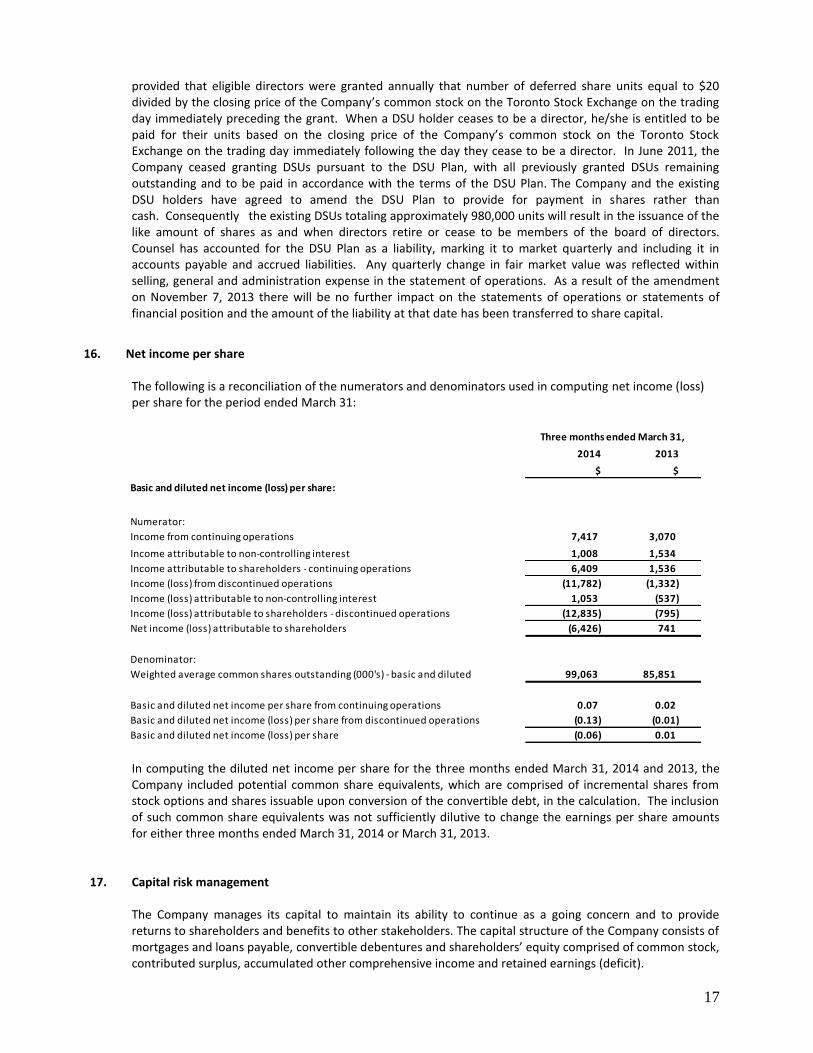

16. Net income per share

The following is a reconciliation of the numerators and denominators used in computing net income (loss) per share for the period ended March 31:

In computing the diluted net income per share for the three months ended March 31, 2014 and 2013, the Company included potential common share equivalents, which are comprised of incremental shares from stock options and shares issuable upon conversion of the convertible debt, in the calculation. The inclusion of such common share equivalents was not sufficiently dilutive to change the earnings per share amounts for either three months ended March 31, 2014 or March 31, 2013.

17. Capital risk management

The Company manages its capital to maintain its ability to continue as a going concern and to provide returns to shareholders and benefits to other stakeholders. The capital structure of the Company consists of mortgages and loans payable, convertible debentures and shareholders’ equity comprised of common stock, contributed surplus, accumulated other comprehensive income and retained earnings (deficit).

2014 2013

$ $

Basic and diluted net income (loss) per share:

Numerator:

Income from continuing operations 7,417 3,070

1,008 1,534

Income attributable to shareholders - continuing operations 6,409 1,536

Income (loss) from discontinued operations (11,782) (1,332)

Income (loss) attributable to non-controlling interest 1,053 (537)

Income (loss) attributable to shareholders - discontinued operations (12,835) (795)

Net income (loss) attributable to shareholders (6,426) 741

Denominator:

Weighted average common shares outstanding (000's) - basic and diluted 99,063 85,851

Basic and diluted net income per share from continuing operations 0.07 0.02

Basic and diluted net income (loss) per share from discontinued operations (0.13) (0.01)

Basic and diluted net income (loss) per share (0.06) 0.01

Income attributable to non-controlling interest

Three months ended March 31,

18

The Company makes adjustments to its capital structure in light of economic conditions. The Company will balance its overall capital structure through new share issues, share repurchases, the payment of dividends, the issue of debt or by undertaking other activities as deemed appropriate under specific circumstances. The Company’s overall strategy with respect to capital risk management remained unchanged during the current reporting period. The Company is compliant with all covenants related to its outstanding debt.

18. Financial instruments

The Company utilizes financial instruments to finance its operations in the normal course of business. The Company has classified its financial instruments as follows:

For mortgages, accounts and interest receivable (net of allowance for doubtful accounts) and accounts payable and accrued liabilities, the carrying amounts approximate fair value because of the short maturity of these instruments. Convertible debentures, contingent consideration and mortgages and loans payable are carried at amortized cost. The carrying values of financial liabilities equal or approximate their fair values. Short-term investments, marketable securities and portfolio investments are carried at fair value through profit and loss. The Company uses the following hierarchy for determining the fair value of financial instruments:

Level 1 – inputs to the valuation methodology are quoted prices (unadjusted) for identical assets or liabilities in active markets.

Level 2 – inputs to the valuation methodology include quoted prices for similar assets and liabilities in active markets, and inputs that are observable for the asset or liability, either directly or indirectly, for substantially the full term of the financial instruments.

Level 3 – valuation methodology in which one or more significant inputs are unobservable.

The following tables present the financial instruments measured at fair value at March 31, 2014 and

Carrying value Fair value Carrying value Fair value

$ $ $ $

Financial assets

Cash and cash equivalents (ii) 11,880 11,880 17,580 17,580

Marketable securities (i) 413 413 410 410

Mortgages, accounts and deferred interest receivable (ii) 53,880 53,880 41,407 41,407

Portfolio investments (i) 65,006 65,006 53,220 53,220

131,179 131,179 112,617 112,617

Financial liabilities

Accounts payable and accrued liabilities (iii) 31,279 31,279 29,458 29,458

Mortgages and loans payable (iii) 20,072 20,072 20,728 20,728

Contingent consideration (iii) 8,699 8,699 8,570 8,570

60,050 60,050 58,756 58,756

(i) Fair value through profit or loss

(ii) Loans and receivables at amortized cost

(iii) Financial liabilities at amortized cost

March 31, 2014 December 31, 2013

19

December 31, 2013 as classified by the fair value hierarchy set out above:

The continuity table for level 3 assets, comprised of portfolio investments, is presented in Note 10. Financial instruments disclosures regarding discontinued operations are presented in Note 21.

19. Financial risk management

The Company has exposure to credit risk, foreign exchange risk, interest rate risk, liquidity risk and market value risk. The Company has established policies and procedures to manage these risks, with the objective of minimizing any adverse effects that changes in these variables could have on the Company. Credit risk The Company extends credit to customers in the Mortgage Lending, Asset Liquidation, Real Estate and Case Goods businesses. The Company’s credit risk on liquid funds and derivative financial instruments is limited because the counterparties are banks with high credit ratings assigned by international credit-rating agencies. The Company manages credit risk on accounts receivable by requiring customer deposits and/or credit checks for new customers, and by issuing notices and evictions. All the mortgage receivables except for a few, which are recorded at a fair value of $683, are insured or insurable with the Canada Mortgage and Housing Corporation or other private insurers. The Company does not hold any collateral or other credit enhancements to cover its credit risks associated with its financial assets. The Company has no allowance for doubtful accounts on continuing operations at March 31, 2014 (December 31, 2013 - $Nil) on outstanding accounts receivable. The Company historically has not experienced any major collection issues. Foreign exchange risk Foreign exchange risk arises from assets and liabilities invested in U.S. dollars, operations derived from those U.S. dollar investments, and transactions in the U.S. with U.S. customers and foreign suppliers. The Company had the following U.S. dollar denominated monetary assets and liabilities at March 31, 2014 and December 31, 2013, respectively: Cash US$791 and US$1,366; Accounts receivable US$267 and US$127; Loans receivable US$3,057 and US$ nil; Portfolio investments US$49,379 and US$48,625; Accounts payable US$379 and US$956; and Mortgages and loans payable of US$2,400 and US$2,400. A one cent increase in

20

the value of the U.S. dollar relative to the Canadian dollar would result in a $507 net increase in net income related to U.S. dollar denominated monetary assets and liabilities (2013 - $477). Interest rate risk Interest rate risk arises due to exposure to the effects of future changes in the level of interest rates. The Company is exposed to interest rate risk arising from fluctuations in interest rates primarily on its mortgages and loans payable, depending on prevailing rates at renewal. With respect to the mortgage receivables, the Company is not exposed to a significant amount of interest rate risk as the purchase price for mortgages placed with financial institutions is based on the customer commitment rate and not the ultimate funded rate. In order to manage funding needs or capital structure goals, the Company enters into debt agreements that are subject to fixed market interest rates set at the time of issue or floating rates determined by on-going market conditions. Debt subject to variable interest rates exposes the Company to variability in interest expense, while debt subject to fixed interest rates exposes the Company to variability in the fair value of the debt. To manage interest rate exposure, the Company accesses diverse sources of financing and manages borrowings in line with a targeted range of capital structure, liquidity needs, maturity schedule, and currency and interest rate profiles. At March 31, 2014, a 100 basis point change in interest rates would result in a $201 change in annual interest expense (December 31, 2013 - $207). Liquidity risk Liquidity risk is the risk the Company will not be able to meet its financial obligations as they fall due. The Company’s approach to managing liquidity risk is to ensure, as far as possible, that it will always have sufficient liquidity to meet its liabilities when due, under both normal and stressed conditions, without incurring unacceptable losses or risking damage to the Company’s reputation. Market value risk The Company has investments in marketable securities. At March 31, 2014, a 10% change in the S&P/TSX composite index would result in a $41 change in net income (December 31, 2013 - $40). The Company has portfolio investments which are subject to market value risk. The Company records its portfolio investments at fair value through profit or loss.

20. Income taxes

In the first quarter of 2014, the Company recognized a deferred income tax expense from continuing operations of $1,447 (2013: $458). The deferred income tax expense in 2014 and 2013 is primarily due to profits generated from the Company’s residential mortgage lending business which will be taxable in the future, and which will reduce available tax loss carry forwards. In addition, the expense incurred in the first quarter of 2014 related to gains realized on the disposition of the Company’s Case Goods business. The $10,746 deferred income tax liability balance as at March 31, 2014 reflects primarily the estimated tax liability from prior and current period profits that are expected to be taxable in the future, net of available tax loss carry forwards the utilization of which is considered probable. As at March 31, 2014 the Company had approximately $242,813 in non-capital loss carry-forwards in Canada and approximately US$5,800 in non-capital loss carry-forwards in the United States which may be used to reduce future years’ taxable income until 2024. In addition, the Company and its subsidiaries have approximately $73,453 of capital loss carry-forwards in Canada, and nil capital loss carry-forwards in the United States. Canadian capital losses may be carried forward indefinitely. Substantially all of the Company’s capital losses are unlikely to be utilized and accordingly these capital losses have not been recognized at the end of the period.

21

21. Discontinued operations

In the first quarter of 2013, Counsel’s Board of Directors approved of a plan to dispose of the Company’s non-core operating business segments. The decision reflects the Company’s strategy, undertaken in recent years, to focus on financial services. The Company’s discontinued operations are in the Asset Liquidation, Case Goods and Real Estate segments. Discontinued operations have been presented on a segmented basis to enhance the reader’s understanding of the financial information presented. A summary of the carrying value of the assets and liabilities for discontinued operations is as follows:

The composition of earnings (loss) from discontinued operations for the period ended March 31 is as follows:

December 31, 2013

Asset Case Real

Liquidation Goods Estate Total Total

$ $ $ $ $

Assets:

Current

Cash and cash equivalents - - 47 47 3,472

Amounts receivable - - 814 814 3,327

Inventory - - - - 7,080

Properties under development - - - - 3,429

Prepaid expenses and deposits - - 2 2 1,107

Total current assets - - 863 863 18,415

Non-current

Deferred charges - - 14 14 14

Promissory note - - 608 608 597

Property plant and equipment - - - - 166

Intangible assets - - - - 5,584

Goodwill - - - - 19,282

Interest in joint ventures - - - - 1,468

Equity accounted investments - - - - 20

Future income tax - - - - 26,236

Total Assets - - 1,485 1,485 71,782

Liabilities:

Current

Accounts payable and accrued liabilities - - 1,021 1,021 9,560

Customer deposits - - - - 1,544

Mortgages and loans payable - - - - 9,446

Total current liabilities - - 1,021 1,021 20,550

Non-current

Long term liabilites on closing - - 238 238 318

Total Liabilities - - 1,259 1,259 20,868

March 31, 2014

22

Asset Case Real

Liquidation Goods Estate Total

$ $ $ $

Revenues 1,591 3,026 126 4,743

Operating costs 231 1,417 - 1,648

Selling, general and administrative expense 2,141 576 251 2,968

Foreign exchange (gain) loss (1,147) (521) - (1,668)

Interest expense 70 - - 70

Other 114 30 381 525

182 1,524 (506) 1,200

Fair value adjustments (13,032) - - (13,032)

(12,850) 1,524 (506) (11,832)

Income tax provision (recovery) (50) - - (50)

(12,800) 1,524 (506) (11,782)

(273) 1,326 - 1,053

Net income (loss) (12,527) 198 (506) (12,835)

March 31, 2014

Expenses and other (income) losses

Income (loss) before fair value adjustments and income taxes

Income (loss) before income taxes

Income (loss) before non-controlling interest

Net income (loss) attributable to non-controlling interest

Asset Case Real

Liquidation Goods Estate Total

$ $ $ $

Revenues 2,430 1,322 113 3,865

Operating costs 590 1,176 47 1,813

Selling, general and administrative expense 2,835 628 52 3,515

Interest expense 95 172 60 327

Other (1) - (27) (28)

(1,089) (654) (19) (1,762)

Income tax provision (recovery) (425) - (5) (430)

(664) (654) (14) (1,332)

(188) (352) 3 (537)

Net income (loss) (476) (302) (17) (795)

Net income (loss) attributable to non-controlling interest

March 31, 2013

Expenses and other (income) losses

Income (loss) before income taxes

Income (loss) before non-controlling interest

23

The Asset Liquidation business is carried on through HGP Global LLC (“HG LLC”) (formerly known as CRB LLC) and HGP Global Partners Inc. (“HGP”). These entities, collectively, are referred to as “HGI”. HG LLC specializes primarily in the acquisition and disposition of distressed and surplus assets throughout the United States and Canada, including industrial machinery and equipment, real estate, inventories, accounts receivables and distressed debt. It also includes the corporate overheads of HGI and the costs associated with maintaining the intellectual property of HGI. The Case Goods business is carried on through Fleetwood. Fleetwood provides high quality customized case goods for large, upscale hotel chains, primarily in North America. Fleetwood serves a focused niche, being the “upscale” and “upper upscale” strata of the hospitality industry. Real Estate encompasses the ownership and development of properties as well as the provision of real estate property and asset management services to third parties. All three segments have been discontinued as at March 31, 2013. In the first quarter of 2014, the Case Goods business was sold to third parties, resulting in a gain of approximately $1,500. In addition, the Company extinguished a debt related to the Case Goods business, resulting in a gain of $4,125. The Asset Liquidation business is being distributed to Counsel shareholders as a dividend-in-kind, which was declared on March 20, 2014 with a payment date of April 30, 2014. Upon the declaration of the dividend-in-kind, the Company’s investment in HGI was reclassified from discontinued operations to shares “available for sale”. This required the shares to be recorded at fair value, resulting in a fair value adjustment of ($13,032) at the declaration date. The disposal or all three segments was part of a plan of disposal approved by the board of directors.

22. Related party transactions

The Company’s Asset Liquidation subsidiary, beginning in 2009, leased office space in White Plains, NY and Los Angeles, CA as part of the operations of HG LLC. Both premises were owned by entities that are controlled by former Co-CEOs of HG LLC (see below). In connection with the departure of the Co-CEOs, these lease agreements were terminated, without penalty, effective June 30, 2013. Additionally, office space in Foster City, CA is also under lease. The premises are owned by an entity that is jointly controlled by the former owners of HGP. During the first quarter of 2014 and 2013, total rent of US$57 and US$96 respectively, was paid to the entities for the lease of the three premises. On July 26, 2013, HGI and its Co-CEOs entered into agreements by which the Co-CEOs terminated their employment with HGI. Under the agreements, effective July 1, 2013, the Co-CEOs of HGI have departed the company along with the personnel in the New York and Los Angeles offices of HGI. Both Co-CEOs retained their initial equity position of 1,621,000 common shares of HGI. However, they have each returned the 400,000 common shares of HGI that they acquired in August 2012 in return for intellectual property licensing agreements. The licensing agreements have been cancelled. Upon the return and cancellation of the 800,000 shares in the third quarter of 2013, Counsel’s ownership increased to 73.3%. The return of the shares in exchange for the cancellation of the licensing agreement resulted in a gain on disposition of HGI’s intellectual property of approximately US$624 in 2013.

23. Subsequent Events

The Company has evaluated events subsequent to March 31, 2014 through to the date of approval of the financial statements by the board of directors for disclosure. There were no material subsequent events requiring disclosure aside from those noted in Note 21.

24

24. Approval of financial statements

The financial statements were approved by the board of directors and authorized for issue on May 8, 2014.