under construction july 2016 construction & engineering ... bangkok came in second with 112...

TRANSCRIPT

UNDER CONSTRUCTION

Regional Thematic

UNDER CONSTRUCTION

Regional Sector Update

See important disclosures at the end of this report 1

Powered by the EFA Platform

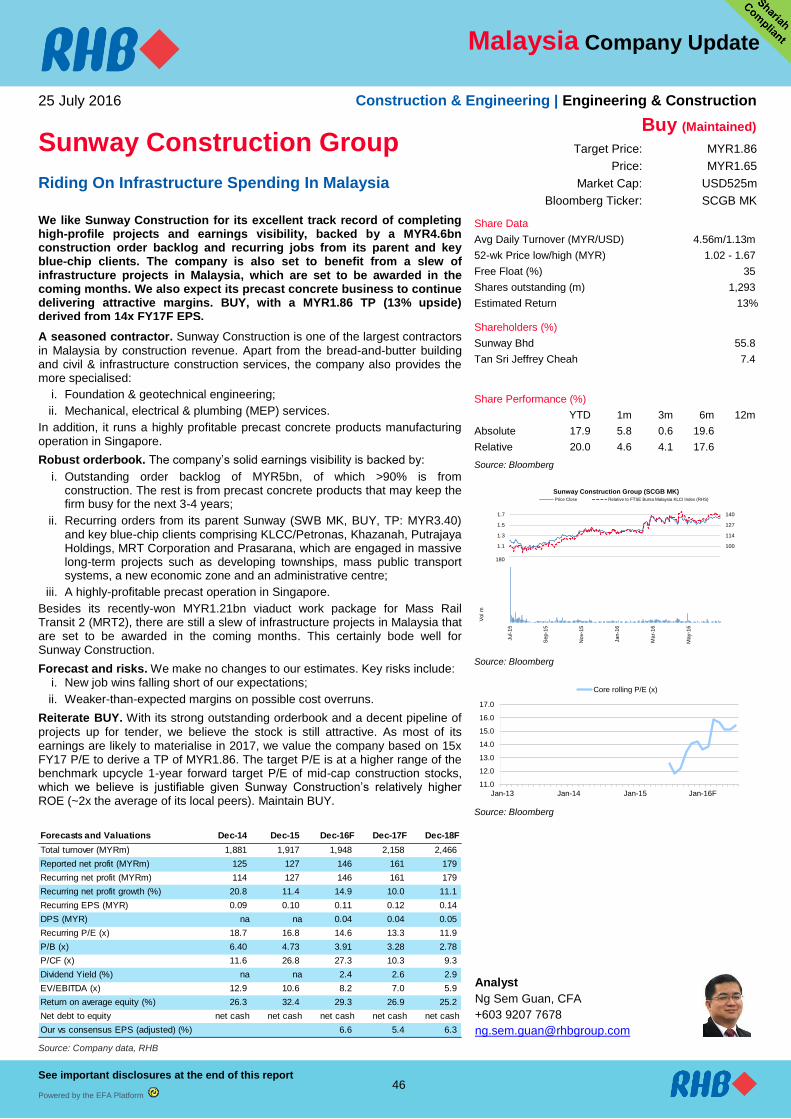

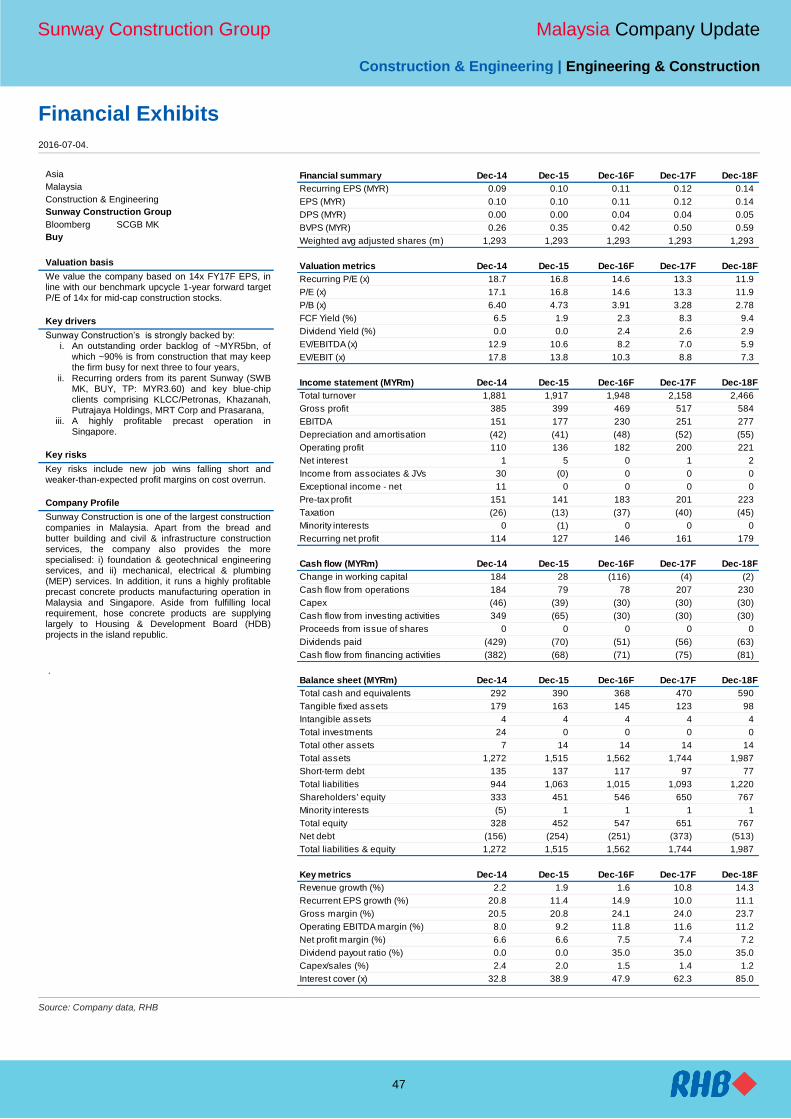

25 July 2016 Construction & Engineering | Construction

Construction Overweight

Stocks Covered: 10

As Many As Stars In The Sky Ratings (Buy/Neutral/Sell): 6 / 7 / 0

Last 12m Earnings Revision Trend: Negative Although four ASEAN countries – Indonesia, Malaysia, Singapore and Thailand – are facing the threat of an economic slowdown, each is relying on different engines to stimulate their economies. All four countries (based on our survey in each capital city) still report progress in terms of construction activities from both the private and public sectors. Our RHB construction analysts maintain their positive view on the sector with Top Picks as follows: 1. Indonesia: Adhi Karya Persero; 2. Malaysia: Sunway Construction and Gadang Holdings; 3. Thailand: Sino-Thai Engineering & Construction.

Top Picks Target Price

Adhi Karya Persero (ADHI IJ) – BUY IDR 3,400

Gadang Holdings (GADG MK) – BUY MYR 3.10

Sino-Thai Engineering & Construction (STEC TB) - BUY

THB29.00

Sunway Construction (SCGB MK) - BUY MYR 1.86

Crane count in four ASEAN countries

0

10

20

30

40

50

60

0

20

40

60

80

100

120

140

Indonesia Malaysia Singapore Thailand

No. of crane No. of project

No. of crane No. of project

Source: RHB

Table Of Contents

Why counting cranes? 2

Indonesia 3

Malaysia 8

Singapore 18

Thailand 28

Adhi Karya Persero (ADHI IJ) 37

Gadang Holdings (GADG MK) 40

Sino-Thai Engineering & Construction (STEC TB) 43

Sunway Construction (SCGB MK) 46

Different engines in different countries. In order to boost their economies and

prevent a slowdown, Singapore and Malaysia are focusing on export growth and domestic consumption respectively, while Thailand and Indonesia are relying on investments in public infrastructure projects. In spite of the different stimulus instruments, construction activities remain abundant within a 3km radius around the centre of each capital city – we counted many cranes working actively in our surveyed area. Kuala Lumpur ranks the top among the four, with 131 cranes. Bangkok came in second with 112 cranes. Jakarta and Singapore are almost equal, with about 66 and 52 cranes respectively.

What can be learnt from the crane survey?

Indonesia: Jakarta, with many infrastructure projects under construction, is set

to develop new projects. This is especially in terms of new skyscrapers aligned with mass rapid transit (MRT) routes. In the meantime, Indonesia’s residential property sector has been facing slow demand growth since FY15, which has led to delays of developers’ new project launches. Still, office and apartment projects under construction remain on track and are a dominant presence in Jakarta’s central business district (CBD).

Malaysia: The busiest construction activities in this country will not end soon, as

the Government has assured new infrastructure projects will be implemented as planned. However, there is a likely trend for developers to slow down their launches for residential and non-residential projects due to the weak property market. Our analyst believes infrastructure spending by the Government will boost new construction projects awarded to contractors in FY16-17.

Singapore: As the most developed and most congested country among the four

(with a construction cycle that is getting ahead of the others), Singapore is focusing on quality rather than quantity. There is a growing number of new mixed-use projects plus energy-efficient buildings. These are supported by planned construction of more transportation alternatives for a better access to the CBD area.

Thailand: Bangkok’s CBD is dominated by SET-listed companies’ condominium

projects for the mid- to high-end market. There are obvious trends in the CBD, including:

i. Facility expansion of long-term growth businesses such as hospitals and a university campus;

ii. The game of mixed-use projects played by Thai landlords; iii. Initial signs that the hotel sector will expand to a new location in the CBD.

P/E (x) P/B (x) Yield (%)

Dec-17F Dec-17F Dec-17F

Adhi Karya Persero IDR2,720 IDR3,400 11.2 1.5 3.4 BUY

Gadang Holdings MYR2.48 MYR3.10 6.7 1.0 2.9 BUY

Sino-Thai Engineering & Construction PCLTHB25.00 THB29.00 23.9 3.4 1.7 BUY

Sunw ay Construction Group MYR1.65 MYR1.86 13.3 3.3 2.6 BUY

Company Name Price Target Rating

Source: Company data, RHB

Analysts

Dony Gunawan

+6221 2970 7063

Ng Sem Guan, CFA

+603 9207 7678

Jarick Seet

+65 6232 3891

Chatree Srismaicharoen

+66 2862 9743

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 2

Why Counting Cranes? According to RHB’s estimate, the four ASEAN countries in our survey – Indonesia, Malaysia, Singapore, and Thailand – have the potential to see their GDPs increase gradually in FY16-17. Although all four economies have faced economic challenges due to internal and external threats, their governments are focusing on different engines to boost GDP growth to a higher level. Indonesia and Thailand remain focused on public investments in infrastructure projects, while Singapore and Malaysia are relying on the export sector and domestic consumption respectively. It is interesting to note, however, that the growth of construction activities in Indonesia, Malaysia and Thailand is estimated to be far above their respective GDP growth. Meanwhile, the construction sector in Singapore is significant to some degree.

Figure 1: RHB’s estimates on construction growth and as a percentage of GDP Indonesia Malaysia Singapore Thailand FY16F FY17F FY16F FY17F FY16F FY17F FY16F FY17F GDP Growth (%) 5.1 5.3 3.9 4.0 1.8 2.0 3.2 3.5

Construction % of GDP 10.5 10.5 4.5 4.5 13.2 13.3 8.7 9.0

Growth (%) 8.2 8.5 6.0 5.3 4.6 1.1 13.5 17.3

Public construction % of GDP NA NA NA NA 8.8 8.6 4.7 5.1

Growth (%) NA NA NA NA 8.4 9.1 18.6 23.6 Private construction

% of GDP NA NA NA NA 4.4 4.7 4.0 3.8 Growth (%) NA NA NA NA -3.0 -3.6 7.5 10.1

Source: RHB

Crane counting is the method we have adopted to measure the construction activities in each country, in terms of quality and quantity. In addition to collating the number of cranes counted in each CBD area (within a 3km radius of the centre of the capital city), we also detail out the current situation and circumstances as well as the future construction activity trends in each country.

Below is a summary of the results of our crane counting surveys. We counted a total of 361 cranes and 176 projects under construction for all four countries.

Figure 2: Summary of cranes and projects in the four ASEAN countries surveyed Total No. of cranes No. of projects Residential No. of cranes No. of projects

Malaysia 131 48 Malaysia 33 20 Thailand 112 55 Thailand 43 33 Indonesia 66 19 Indonesia 9 3 Singapore 52 54 Singapore 25 25

Office No. of cranes No. of projects Hotel No. of cranes No. of projects Malaysia 21 3 Malaysia 18 4 Thailand 17 8 Thailand 6 2 Indonesia 30 10 Indonesia - - Singapore 16 10 Singapore 7 12

Mixed-use No. of cranes No. of projects Other No. of cranes No. of projects Malaysia 34 11 Malaysia 25 10 Thailand 29 4 Thailand 17 8 Indonesia 21 4 Indonesia 6 2 Singapore - - Singapore 4 7

Source: RHB

We will detail our findings from the crane survey in alphabetical order of the countries, ie Indonesia first, followed by Malaysia, Singapore, and Thailand. The analysts behind each survey are listed below:

Indonesia Dony Gunawan [email protected] Malaysia Ng Sem Guan [email protected] Singapore Jarick Seet [email protected] Thailand Chatree Srismaicharoen [email protected]

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 3

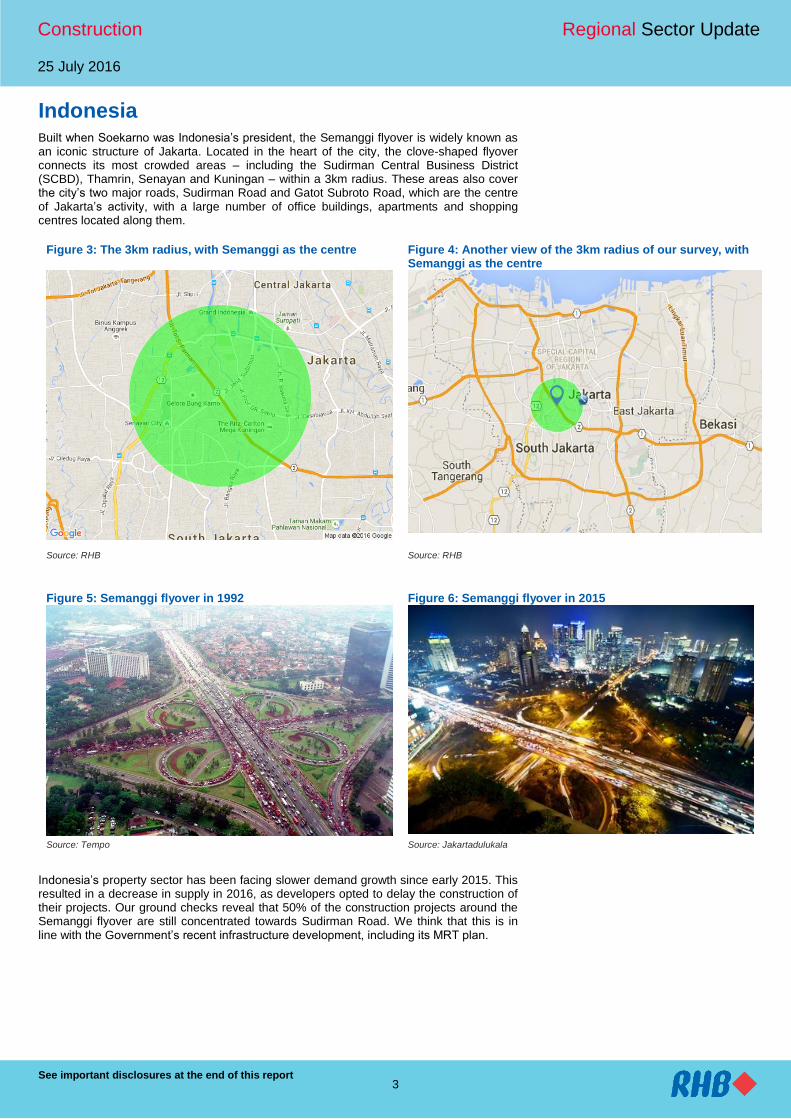

Indonesia Built when Soekarno was Indonesia’s president, the Semanggi flyover is widely known as an iconic structure of Jakarta. Located in the heart of the city, the clove-shaped flyover connects its most crowded areas – including the Sudirman Central Business District (SCBD), Thamrin, Senayan and Kuningan – within a 3km radius. These areas also cover the city’s two major roads, Sudirman Road and Gatot Subroto Road, which are the centre of Jakarta’s activity, with a large number of office buildings, apartments and shopping centres located along them.

Figure 3: The 3km radius, with Semanggi as the centre Figure 4: Another view of the 3km radius of our survey, with Semanggi as the centre

Source: RHB Source: RHB

Figure 5: Semanggi flyover in 1992 Figure 6: Semanggi flyover in 2015

Source: Tempo Source: Jakartadulukala

Indonesia’s property sector has been facing slower demand growth since early 2015. This resulted in a decrease in supply in 2016, as developers opted to delay the construction of their projects. Our ground checks reveal that 50% of the construction projects around the Semanggi flyover are still concentrated towards Sudirman Road. We think that this is in line with the Government’s recent infrastructure development, including its MRT plan.

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 4

Figure 7: Commercial property supply growth in the Jabodetabek area

Figure 8: Pipeline of apartments and office projects in Jakarta

Title:

Source:

Please fill in the values above to have them entered in your report

6.2

3.1

23.2

3.6

-5

0

5

10

15

20

25

30

35

40

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15

% YoY

Off ices Retails Apartments Hotels

Title:

Source:

Please fill in the values above to have them entered in your report

54

35

46

13

26

19

15

0

10

20

30

40

50

60

2016 2017 2018 2019

No of Buildings

Apartment Off ice

Source: Bank of Indonesia Source: Colliers International Indonesia

During our ground checks, we counted 19 different projects and 66 cranes within the 3km radius of Semanggi. Most of the construction works were for office buildings (14 projects were visible). According to Colliers, Jakarta’s CBD has recorded a total supply of 5.27m sqm (+7.7% YoY) in office space as at 1Q16. The data from Colliers also indicated that 75% of the 1m sqm projected office supply in 2019 will be located in Sudirman, Kuningan and Gatot Subroto.

The apartment segment came in second, with a total seven projects counted – some of them by well-known property developers including Ciputra Group [which consists of Ciputra Surya (CTRS IJ, BUY, TP: IDR5,000), Ciputra Development (CTRA IJ, BUY, TP: IDR1,530) and Ciputra Property (CTRP IJ, NR)], Astra Group (ASII IJ, BUY, TP: IDR7,350) and Lippo Group, ie Lippo Karawaci (LPKR IJ, NEUTRAL, TP: IDR1,460). We also note that there are not as many apartment projects near the CBD area, while the take-up rate for luxury apartments is low.

There are two infrastructure projects, including the MRT construction and Semanggi flyover extension. During our ground checks, we counted four cranes working on the infrastructure projects alone. The Semanggi flyover extension will provide an alternative two-way connection from Sudirman to Gatot Subroto. Works on the project began recently, and it is targeted to be ready on 1 Aug 2017. The Semanggi flyover contract was won by Wijaya Karya (WIKA IJ, NEUTRAL, TP: IDR2,665) with a contract value estimated at IDR563bn.

Figure 9: Current progress of Semanggi Flyover 2 Figure 10: Design of Semanggi Flyover 2

Source: RHB Source: Ahok

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 5

Langham and District 8

District 8 is located at the heart of Sudirman in the CBD, and tops the list with the largest number of tower cranes (10). The superblock project is located on 4.8ha of land and will provide the CBD area with additional apartments, office space, hotel and retail area.

The project, developed by Agung Sedayu Group, consists of two office towers, three apartments and two hospitality towers. The three apartments will provide additional 680 strata-title units of high-end apartments and 180 units of serviced apartments for the CBD. Moreover, the two towers of office buildings will provide an additional semi gross area (SGA) of more than 210,000 sqm.

District 8 project is located in SCBD, alongside two other projects, ie Sequis Tower and Grade A at Lot 10. These three projects alone contribute 22.7%, or 15 cranes, out of the total number of cranes in the 3km radius of Semanggi.

The contract for the construction of District 8 was won by Acset Indonesia (ACST IJ, BUY, TP: IDR4,550) and carries a total value of IDR800bn. The 1-stop-living project is expected to be finished in 2017.

Figure 11: Langham residence and District 8 Figure 12: Langham residence

Source: RHB Source: RHB

Anandamaya Residences and Astra Tower projects

The other side of Sudirman road features two Astra projects, Anandamaya Residences and Astra Tower. Anandamaya Residences comprises three apartment towers on 1.6ha of prime land. According to our observations, the three towers’ construction site has three tower cranes in total. The apartment is developed by Astra International and Hongkong Land Ltd and will have 500 luxurious apartment units. The apartment has a project value nearing USD150m and is set to begin operations in 2017.

On the other hand, Astra’s other project, Astra Tower, is located right next door to the luxury apartments. The office tower has a total of 47 floors and 80,000 sqm of SGA available for lease. Astra expects the leasing of the office space to begin in 1Q18. The total value of the office building is estimated to be around IDR3.5trn.

The Astra Tower construction is done by a joint-venture (JV) between Total Bangun Persada (TOTL IJ, NR) and Shimizu Corp (Shimizu). Total Bangun Persada owns 40% of the construction project, which is valued at IDR1.1trn. On the other hand, Anandamaya Residences’ construction contract was won by a local private contractor, Tata.

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 6

Figure 13: A view of construction works for Astra Tower Figure 14: Astra Tower and Anandamaya Residences projects

Source: Indopora Source: RHB

Figure 15: Artist impression of Anandamaya Residences and Astra Tower

Source: Company

MRT is the main catalyst

We think that the main catalyst for the development along the CBD area is still the construction of the MRT network. The first phase of the MRT will span 15.7km and connect Lebak Bulus (South Jakarta) and Bundaran HI (Thamrin, Central Jakarta). On Sudirman Road, we counted at least two mobile cranes and two crawler cranes on the site. Construction started back in 2013 and is expected to start operations by early 2019. YTD, construction of the first phase of the MRT system is 43% complete, and will be ready to serve 212,000-960,000 passengers per day when operations begin. The total construction value for the MRT project is USD1.29bn.

The construction project is divided into eight civil engineering projects and one for operations & maintenance (O&M) consulting. These civil projects include elevated civil works, underground works, railway systems and track works and rolling stock. Wijaya Karya is one of the many contractors for the first phase of the project. The company is responsible for Construction Package (CP) 101-102 for elevated works with Tokyu Corp (Tokyu), and CP 104-105 for underground works with Shimizu, Obayashi Corp (Obayashi) and Jaya Konstruksi.

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 7

Figure 16: A portion of the MRT Jakarta tunnel Figure 17: Building the elevated track for the MRT

Source: SkyscraperCity Source: SkyscraperCity

Outlook

Currently, we see that the CBD area within a 3km radius of Semanggi is already diversified and well developed with a mix of apartments, office buildings and retail spaces. Most of the available land plots are already included in the development plan for the next three years. Future developments within the CBD will mostly centralise around the revitalisation of old buildings. Therefore, we expect to see more skyscrapers in Jakarta’s CBD in the future.

On the other hand, we also note the Government’s plan to accelerate infrastructure and public transportation development, both in and out of the CBD area. This plan includes the development of the MRT and light rail transit (LRT) networks. Jakarta Propertindo (Jakpro) recently announced that it will continue the construction of the inner city LRT in September. The inner city LRT is set to connect North Jakarta and South Jakarta, as well as West Jakarta and East Jakarta. With the improvements in infrastructure and public transportation, we think the CBD area in Jakarta will not be as central as it is today, but will eventually widen to other areas. In the future, we expect to see skyscrapers projects in the outer CBD areas, including Kuningan and TB Simatupang.

Our outlook on the construction sector is still robust, supported by the many infrastructure projects across the nation. Therefore, state-owned contractors such as Adhi Karya (ADHI IJ, BUY, TP: IDR3,400), Waskita Karya (WSKT IJ, NR), Pembangunan Perumahan (PTPP IJ, BUY, TP: IDR4,200) and Wijaya Karya will be the biggest beneficiaries of this development. We also think infrastructure development will also boost the demand for properties, in the future – which will also benefit construction companies.

Figure 18: Crane counts survey table Project name Project type Project owner Location No of cranes

Telkom Landmark Tower Office Building Telekomunikasi Indonesia Gatot Subroto 2 tower cranes

Grade A lot 10 Office Building Hongkong Land SCBD 2 tower cranes and 1 crawler crane

Sequis Tower Office Building Sequis SCBD/Sudirman 2 tower cranes

Langham & District 8 Office & Apartment Building Langham SCBD 10 tower cranes

Simpang Susun Semanggi 2 Road Government Sudirman 2 crawler cranes

Anandamaya & Astra Tower Office Building, Shopping Mall & Apartment Building

Astra & Hongkong Land Sudirman/Benhil 6 tower cranes

Benhil Central Apartment Building Kurnia Realty and Pasar Jaya Sudirman 4 mobile cranes

Lippo Thamrin Office Building Lippo Group Thamrin 1 tower crane

Plaza CIMB Office Building CIMB Sudirman 4 crawler cranes

MRT Jakarta MRT Government Sudirman 2 mobile and 2 crawler cranes

WTC 2 Office Building Pollux Sudirman 2 crawler cranes

Menara Pertiwi Tower Office Building Wiratara Prima Mega Kuningan 5 tower cranes

Chitaland Tower Office Building Sigmatech Satrio 3 crawler and 3 mobile cranes

Ciputra World 2 Office & Apartment Building Ciputra Group Satrio 2 tower cranes

Satrio Tower Office Building Mitra Pertala Perkasa Satrio 2 tower cranes

Mangkuluhur City Office & Apartment Building KG Global Gatot Subroto 3 tower cranes

South hills Apartment Building Tan Kian Group Setiabudi 2 mobile cranes

La Vie Apartment Apartment Building Wilsor Group Setiabudi 3 tower cranes

Icon Complex Office Building Duta Anggada Group Setiabudi 3 tower cranes

Source: RHB

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 8

Malaysia The Petronas Twin Towers, the most iconic building in Kuala Lumpur's Golden Triangle, was chosen as our reference point for our 3km radius crane survey. The 88-storey twin towers, which soar to a height of 451.9 metres, were once the tallest buildings in the world – and remain the tallest twin structures to date.

The 3km radius from the Petronas Twin Towers covers the entire Golden Triangle, which is known as Kuala Lumpur's commercial, shopping and entertainment hub. This is actually a large area that encompasses a number of major streets. Three major roads – Jalan Imbi, Jalan Sultan Ismail and Jalan Raja Chulan feature towering skyscrapers, shopping malls and world-class hotels. Aside from the Golden Triangle, we also sub-divided the remaining area into six districts – Titiwangsa, Datuk Keramat, Kampung Baru, Old City Centre, Ampang and Pudu/Loke Yew

Figure 19: 3km radius, with the Petronas Twin Towers as the centre

Figure 20: 3km radius map feature the Petronas Twin Towers as the centre

Source: RHB Source: RHB

Our survey showed that most of the major developments in Kuala Lumpur’s city centre are still very much concentrated within the Golden Triangle, with 19 major projects now in various stages of completion and 55 cranes (43 mobile and 12 tower cranes) currently deployed in this area. That said, the old city centre is not forgotten, as we found 12 projects currently ongoing with 32 cranes (20 mobile and 12 tower cranes) deployed at this district. The Pudu/Loke Yew area, which is situated next to the Golden Triangle and old city centre, is the third-busiest place in terms of construction, as there are seven ongoing major projects with 27 cranes (20 mobile and seven tower) deployed at this district at the moment. The rest of the four districts only have 2-3 mega projects that are currently in various stages of completion, with up to five cranes being deployed at each of these districts at the time of our survey.

Figure 21: Survey results for Kuala Lumpur Figure 22: Number of cranes by districts in Kuala Lumpur

Source: RHB Source: RHB

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 9

Figure 23: Types of cranes used

Source: RHB

Figure 24: Types of developments in Kuala Lumpur Figure 25: Types of developments in Kuala Lumpur

Source: RHB Source: RHB

Developments within the Kuala Lumpur city centre are currently concentrated on serviced apartments and condominiums, with 11 and nine such projects being built respectively. We also observed that mixed-use developments are currently trending, with 11 ongoing projects under construction. This type of development normally includes common areas and a cohesive design. The modern mixed-use development offers the feel of a small town in the middle of a major metropolis. Although we witnessed eight infrastructure-related projects currently under construction, five of these were related to the construction of the underground station for the MRT network. Some MRT track works for the areas that we surveyed may be in final stages of construction, but they were not visible, given that they are situated underground.

In the two days that we carried out our site survey, we also realised that there are still some pockets of prime vacant land. However, most may have been identified for various developments like residential, office or mixed-used high-rise projects. Although there was no physical work being carried out, we believe some of those may have already obtained approvals from the relevant government authorities. We believe those developers may prefer to wait for market sentiment to improve before announcing any official launches.

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 10

Figure 26: Vacant land fenced off along Jalan Conlay Figure 27: Vacant land fenced off along Jalan Kia Peng

Source: RHB Source: RHB

The biggest plot of land that may potentially be used for future development is situated in the Kampung Baru area (please note that this area is spelt in a variety of ways). The 115-year-old village, the city’s oldest Malay settlement, is located on land that was granted to the Malay community by the fourth Sultan of Selangor, Sultan Abdul Samad (1804-1898). Since the 1970s, the authorities have been trying to develop this Malay enclave, but the biggest stumbling block is the fact that the 121.9ha plot of land comprises 1,355 lots that are owned by more than 5,300 people.

In spite of this hurdle, the Kampong Bharu Development Corp (PKB) is in the process of studying the detailed Kampung Baru 2020 master plan. PKB plans to transform the rustic village into a new Malay cultural centre and the city’s new economic hub, with:

i. 1,900 hotel rooms;

ii. 30m sq ft of office space;

iii. 17,500 residential units;

iv. 12% green and water feature spaces.

One of the main projects identified is the Kampong Bharu City Centre (KBCC), which will become the focal point of the area. Projects under KBCC include a park called KBCC Central Park with pedestrian walkways, pocket parks and water features. This includes 12 iconic buildings with four signature towers that have a collective GDV in the billions of MYR. While there are various challenges to redevelop this piece of prime land, we are keeping a close eye on its progress.

Figure 28: An aerial view of Kampung Baru Figure 29: Artist impression of a redeveloped Kampung Baru

Source: The Star Source: RHB

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 11

We decided to feature five major projects within the survey area that are still in early stages of construction.

Merdeka PNB118 (PNB118)

Merdeka PNB118 is a 118-storey tower within a 19-acre, multi-phase development. Scheduled for completion in 2020, the tower will house Permodalan Nasional’s (PNB) group of companies over 60 floors. It will also comprise 23 floors of rentable commercial space and an 18-story luxury hotel with 236 rooms, as well as multiple sky lobbies and observation decks. The first phase of the project consists of a 118-storey iconic tower and shopping mall with a development cost of MYR5bn.

International consultancy firm Turner International is the project manager. The first contract for Merdeka PNB118, worth MYR74m, was won by Pintaras Jaya (PINT MK, NEUTRAL, TP: MYR3.47) for foundation and piling works back in Mar 2014. These works were completed in late 2015. Meanwhile, South Korea’s Samsung C&T Corp is partnering with local firm UEM Group to build a MYR3.4bn tower. We estimate that the construction of this project is approximately 15% completed.

Figure 30: Artist impression of Merdeka PNB118 Figure 31: Site progress of Merdeka PNB118

Source: KL118 Source: RHB

Tun Razak Exchange (TRX)

The TRX Master Plan includes a total of 25 buildings and over 21m sq ft of total building gross floor area (GFA) spread across office, residential, hotel, retail, food & beverage (F&B) and cultural offerings. The TRX has a development period of 15 years, and will be completed in phases. The initial Phase 1 is slated for completion in 2018. Strategically located at the southern gateway to Kuala Lumpur’s city centre, the TRX is flanked by main arterial roads. It is a natural extension to the Golden Triangle – the city’s commercial, entertainment and shopping belt. The development will offer an unrivalled connectivity to the existing city centre and the rest of the Greater Kuala Lumpur area, given its:

i. Excellent accessibility and connectivity via an integrated underground MRT interchange station;

ii. Direct connectivity to key roads and major highways.

In Oct 2015, WCT (WCTHG MK, BUY, TP: MYR1.84) won a major infrastructure package at the TRX, valued at MYR754.8m. The 2-year contract covers:

i. Underground road structures;

ii. Installation of direct buried utilities;

iii. At-grade and elevated roadway;

iv. Associated earthworks;

v. Mechanical and electrical works.

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 12

A leading Indonesian property developer, Mulia Group, will develop the TRX’s landmark Signature Tower building. TRX City SB, the master developer of TRX, is currently inviting contractors to participate in a pre-qualification exercise for the proposed traffic dispersion and improvement to a part of Jalan Tun Razak (JTR), as well as the construction of the TRX Ingress and Egress. The development is less than 5% complete and construction activities are likely to stretch over a period of 15 years.

Figure 32: TRX Master plan Figure 33: Site progress of TRX

Source: TRX Source: RHB

Bukit Bintang City Centre (BBCC)

The history of the redevelopment of the old Pudu Prison site, which is now called BBCC, can be traced back some 20 years when the 19.4-acre prime land first became vacant. In Feb 2015, the Urban Development Authority (UDA) decided to partner Eco World Development Group for the redevelopment under a JV partnership with the Employees Provident Fund (EPF) via a special-purpose vehicle (SPV) BBCC Development SB (BBCCD) on a 40:40:20 basis.

While construction works have yet to begin, the BBCC’s showroom, site office and car park are all ready for the first official launch of the office tower in 3Q16. BBCCD signed the head of terms agreements with Mitsui Fudosan (Asia) Pte Ltd (Mitsui Fudosan) for the development, ownership and operation of the 1.4m sq ft retail mall through the establishment of a JV company. Phase 1 of the project will consist of a 45-storey block of strata offices and two blocks of serviced residences, comprising 680 units.

Apart from that, BBCCD also signed an agreement with Zepp Hall Network Inc (Zepp Hall), which will see the development of a live concert hall in BBCC that can host an audience of more than 2,000 people. Official awards are expected to be dished out in various packages as at 2H16. The actual site progress is said to begin from 3Q16 or 4Q16, according to our sources.

Figure 34: Artist impression of BBCC Figure 35: BBCC site office and car park

Source: BBCC Development (BBCCD) Source: RHB

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 13

8 Conlay

Standing strategically in the heart of Kuala Lumpur’s bustling golden triangle, 8 Conlay is a mixed-use development project with an estimated GDV of MYR5.4bn. It is slated for completion by end-2020. The development comprises two branded residence towers (57- and 62-storeys high respectively) whose interior design is by design and development company YOO. These two blocks will be connected via two sky bridges at Levels 26 and 44.

The development is complemented by a 68-storey 5-star hotel, serviced suites and a lifestyle retail component. Europe’s oldest luxury hospitality group, Kempinski Hotels SA, will provide services for the branded residence towers as well as manage the hotel tower.

Econpile Holdings (Econpile) has been tasked to undertake foundation and substructure works for the project for a contract value of MYR128.9m. We understand that works are at an advanced stage of completion (the project is presently about 10% complete overall). After this, super structure works will follow.

Figure 36: Artist impression of 8 Conlay Figure 37: Site progress of 8 Conlay

Source: yoo8.8conlay.com Source: RHB

Klang Valley MRT (KVMRT)

The KVMRT project involves the construction of a rail-based public transport network comprising three lines. The MRT system, together with the existing urban rail network, will form the backbone of the public transport system in the Greater Kuala Lumpur/Klang Valley region. The estimated cost for the entire project is MYR80bn.

The first MRT line is the 51km Sungai Buloh-Kajang (SBK) Line. The line begins in Sungai Buloh, located to the north-west of Kuala Lumpur, and runs through the capital’s centre before ending in Kajang. The latter is a fast-developing town to the south-east of Kuala Lumpur. This line will cut through three districts within our survey area via the underground alignment. These areas are the:

i. Golden Triangle;

ii. Old city centre;

iii. Pudu/Loke Yew.

There are six underground MRT stations, ie Pasar Seni, Merdeka, Bukit Bintang, TRX, Cochrane and Maluri situated within our survey perimeter. Construction of the SBK Line began on 8 Jul 2011 and is now approximately 80% complete. Operations are scheduled to begin by Jul 2017.

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 14

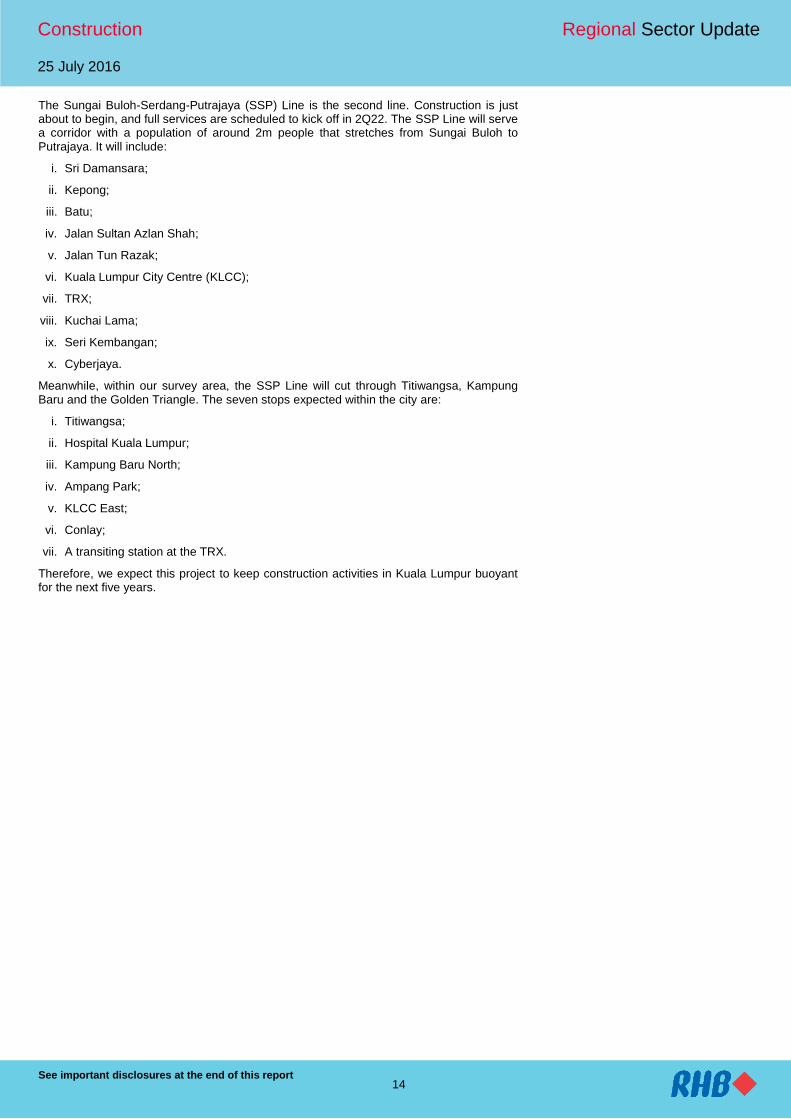

The Sungai Buloh-Serdang-Putrajaya (SSP) Line is the second line. Construction is just about to begin, and full services are scheduled to kick off in 2Q22. The SSP Line will serve a corridor with a population of around 2m people that stretches from Sungai Buloh to Putrajaya. It will include:

i. Sri Damansara;

ii. Kepong;

iii. Batu;

iv. Jalan Sultan Azlan Shah;

v. Jalan Tun Razak;

vi. Kuala Lumpur City Centre (KLCC);

vii. TRX;

viii. Kuchai Lama;

ix. Seri Kembangan;

x. Cyberjaya.

Meanwhile, within our survey area, the SSP Line will cut through Titiwangsa, Kampung Baru and the Golden Triangle. The seven stops expected within the city are:

i. Titiwangsa;

ii. Hospital Kuala Lumpur;

iii. Kampung Baru North;

iv. Ampang Park;

v. KLCC East;

vi. Conlay;

vii. A transiting station at the TRX.

Therefore, we expect this project to keep construction activities in Kuala Lumpur buoyant for the next five years.

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 15

Conclusion

The construction sector emerged relatively unscathed from the recalibrated Budget 2016 tabled by Prime Minister Dato’ Sri Najib Razak in January. The focus remains on projects and programmes that are rakyat-centric, and have a high multiplier effect and low import

content. Physical projects that will be prioritised include the construction of affordable houses, hospitals, schools and roads, as well as public transport and security.

Dato’ Sri Najib reaffirmed the implementation of the following projects:

i. Mass Rapid Transit Line 2 (MRT2);

ii. Light Rail Transit 3 (LRT3);

iii. The Refinery and Petrochemical Integrated Development (RAPID) project;

iv. The Pan Borneo Highway;

v. The Malaysian Vision Valley;

vi. Cyber City Centre;

vii. High-Speed Rail (HSR).

These projects, according to the Prime Minister, are to be carried out as planned. Therefore, the infrastructure boom may keep local contractors busy, at least for the short to medium term, in our opinion.

Meanwhile, we believe the value of projects awarded to contractors domestically in 2016 and 2017 may likely surpass that of 2015’s. This will be thanks to the Government’s spending on infrastructure. That said, we are unsure if it can exceed the record set in 2014 of MYR171.6bn. This is as developers are likely to slow down their launches for residential and non-residential projects on the back of a weak property market.

Figure 38: Value of projects awarded to contractors in Malaysia

Source: CIDB Malaysia

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 16

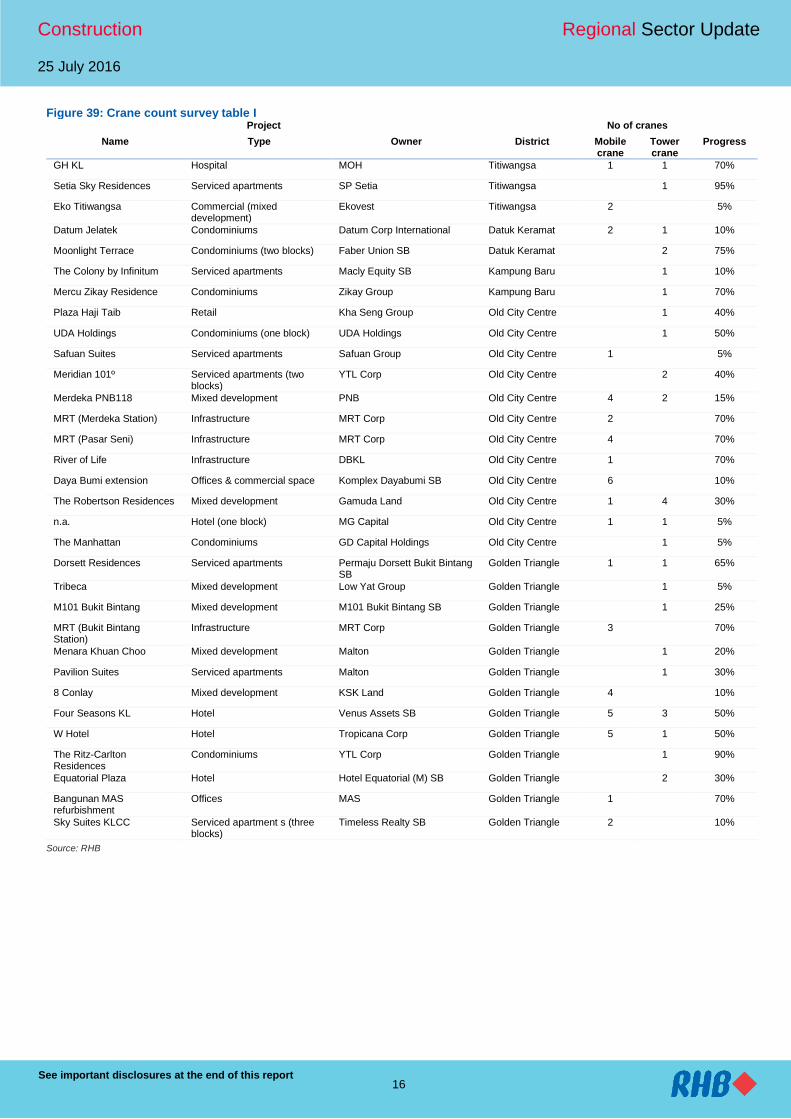

Figure 39: Crane count survey table I Project No of cranes

Name Type Owner District Mobile crane

Tower crane

Progress

GH KL Hospital MOH Titiwangsa 1 1 70%

Setia Sky Residences Serviced apartments SP Setia Titiwangsa 1 95%

Eko Titiwangsa Commercial (mixed development)

Ekovest Titiwangsa 2 5%

Datum Jelatek Condominiums Datum Corp International Datuk Keramat 2 1 10%

Moonlight Terrace Condominiums (two blocks) Faber Union SB Datuk Keramat 2 75%

The Colony by Infinitum Serviced apartments Macly Equity SB Kampung Baru 1 10%

Mercu Zikay Residence Condominiums Zikay Group Kampung Baru 1 70%

Plaza Haji Taib Retail Kha Seng Group Old City Centre 1 40%

UDA Holdings Condominiums (one block) UDA Holdings Old City Centre 1 50%

Safuan Suites Serviced apartments Safuan Group Old City Centre 1 5%

Meridian 101º Serviced apartments (two blocks)

YTL Corp Old City Centre 2 40%

Merdeka PNB118 Mixed development PNB Old City Centre 4 2 15%

MRT (Merdeka Station) Infrastructure MRT Corp Old City Centre 2 70%

MRT (Pasar Seni) Infrastructure MRT Corp Old City Centre 4 70%

River of Life Infrastructure DBKL Old City Centre 1 70%

Daya Bumi extension Offices & commercial space Komplex Dayabumi SB Old City Centre 6 10%

The Robertson Residences Mixed development Gamuda Land Old City Centre 1 4 30%

n.a. Hotel (one block) MG Capital Old City Centre 1 1 5%

The Manhattan Condominiums GD Capital Holdings Old City Centre 1 5%

Dorsett Residences Serviced apartments Permaju Dorsett Bukit Bintang SB

Golden Triangle 1 1 65%

Tribeca Mixed development Low Yat Group Golden Triangle 1 5%

M101 Bukit Bintang Mixed development M101 Bukit Bintang SB Golden Triangle 1 25%

MRT (Bukit Bintang Station)

Infrastructure MRT Corp Golden Triangle 3 70%

Menara Khuan Choo Mixed development Malton Golden Triangle 1 20%

Pavilion Suites Serviced apartments Malton Golden Triangle 1 30%

8 Conlay Mixed development KSK Land Golden Triangle 4 10%

Four Seasons KL Hotel Venus Assets SB Golden Triangle 5 3 50%

W Hotel Hotel Tropicana Corp Golden Triangle 5 1 50%

The Ritz-Carlton Residences

Condominiums YTL Corp Golden Triangle 1 90%

Equatorial Plaza Hotel Hotel Equatorial (M) SB Golden Triangle 2 30%

Bangunan MAS refurbishment

Offices MAS Golden Triangle 1 70%

Sky Suites KLCC Serviced apartment s (three blocks)

Timeless Realty SB Golden Triangle 2 10%

Source: RHB

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 17

Figure 40: Crane count survey table II Project No of cranes

Name Type Owner District Mobile crane

Tower crane

Progress

n.a. Serviced apartments (two blocks)

TA Dev / TA Global Golden Triangle 2 10%

n.a. Condominiums (one block) En. Leong Seong Cheong Golden Triangle 1 5%

Aria Residence Serviced apartments (two block)

Hap Seng Consolidated Golden Triangle 1 5%

Tun Razak Exchange Commercial IMDB & Others Golden Triangle 14 5%

n.a. Serviced apartments n.a. Golden Triangle 1 10%

n.a. Serviced apartments n.a. Golden Triangle 3 5%

Damai Residences Condominiums (one block) Tan & Tan Ampang 1 60%

Road Widening (Jalan Jelatek)

Infrastructure n.a. Ampang 1 10%

Picasso Residences Condominiums (two blocks) Premier De Muara Sdn Bhd Ampang 3 10%

Bukit Bintang City Central Mixed development Eco World & UDA Holdings & EPF

Pudu/Loke Yew 2 1%

MRT (Maluri Station) Infrastructure MRT Corp Pudu/Loke Yew 4 65%

MRT (Cochrane Station) Infrastructure MRT Corp Pudu Loke Yew 4 70%

Tun Razak Traffic Dispersal Infra MOW Pudu/Loke Yew 3 25%

MyTown Shopping Centre Mixed development Boustead Holdings & Ikano Pudu/Loke Yew 3 3 70%

Sunway Velocity Mixed development Sunway Pudu/Loke Yew 4 3 70%

ICC Pudu Mixed development Kuala Lumpur City Hall (DBKL)

Pudu/Loke Yew 1 80%

92 39 37%

Source: RHB

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 18

Singapore We surveyed the CBD region of Singapore and we believe that there is long-term growth potential for the construction sector. The following are our key findings during our crane-counting exercise:

i. A total of 52 cranes within the CBD region – construction progress is on track;

ii. Office developments constitute the main component and are mostly within Singapore’s downtown core region;

iii. Other classes of developments are well spread across the CBD region.

Figure 41: 52 cranes surveyed in the CBD region in total

Source: RHB

We observed that the construction progress of the development projects within the CBD is on track for completion. In this region, we counted a total of 52 cranes. We also note that residential projects are the highest in terms of numbers, but office developments are the largest in terms of project scale.

Figure 42: Zooming into the CBD region Figure 43: Developments are mostly office space

Office Retail Hotel Residential Total

Number of projects

under development10 7 12 25 54

Number of cranes 16 4 7 25 52

GFA/ units 5,251,880 514,647 3,657 4,302 5,774,486

Source: RHB Source: RHB

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 19

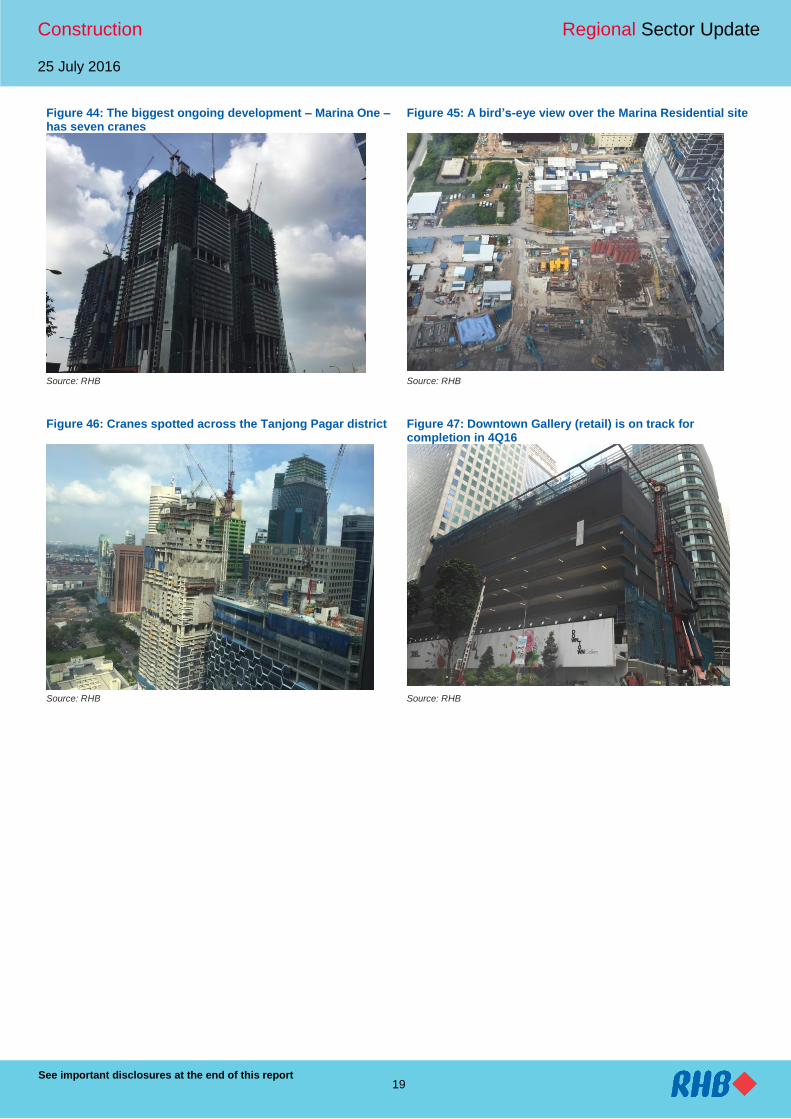

Figure 44: The biggest ongoing development – Marina One – has seven cranes

Figure 45: A bird’s-eye view over the Marina Residential site

Source: RHB Source: RHB

Figure 46: Cranes spotted across the Tanjong Pagar district Figure 47: Downtown Gallery (retail) is on track for completion in 4Q16

Source: RHB Source: RHB

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 20

Figure 48: Guoco Tower will be the tallest building in Singapore

Figure 49: Frasers Tower will be the only CBD office supply in 2018

Source: RHB Source: RHB

The future of Singapore’s CBD

The CBD region is the bloodline of Singapore’s future economy. Since the late 1980s, the Government has pushed initiatives to develop and maintain the sustainability of this region.

The crucial task now is how to maintain the sustainability of the CBD, in order to keep Singapore’s economic status intact. To this end, three mega trends (strongly backed by the Government) will emerge in the CBD region:

i. An increase in the number of mixed developments;

ii. Development of better transport accessibility;

iii. An increase in the number of energy-efficient buildings.

Figure 50: Huge transformation of Marina Bay since the late 1980s

Source: Ministry of National Development (MND)

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 21

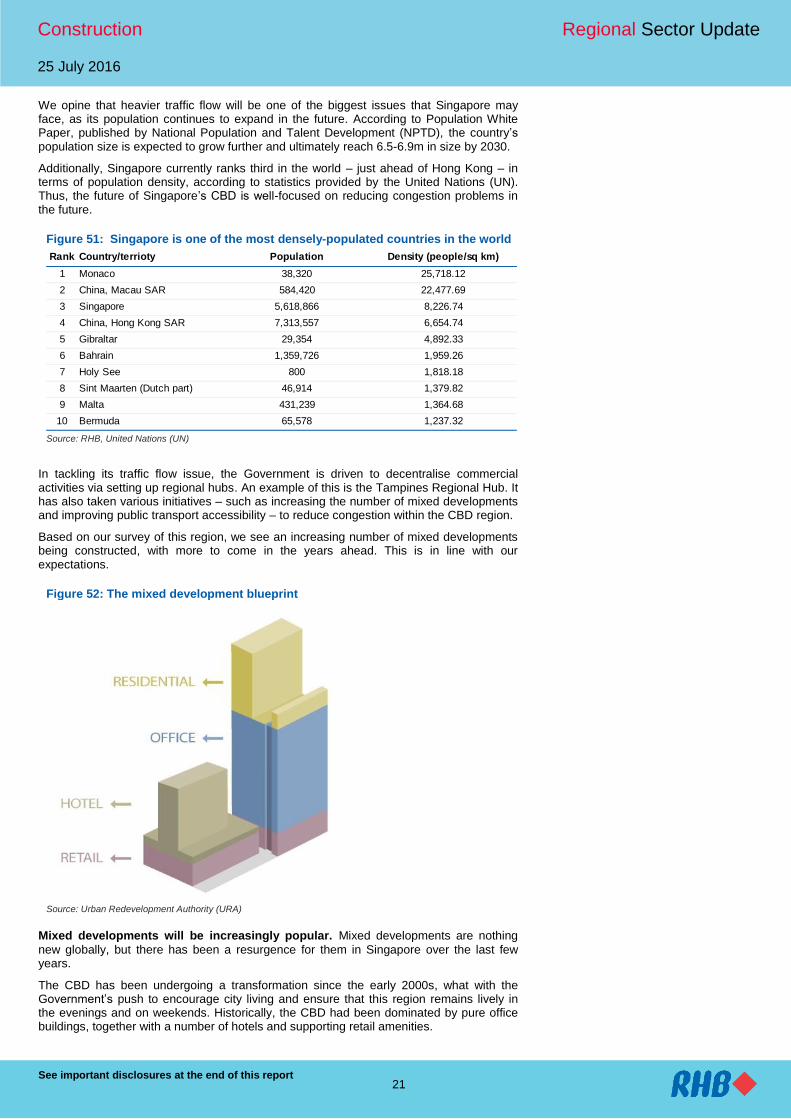

We opine that heavier traffic flow will be one of the biggest issues that Singapore may face, as its population continues to expand in the future. According to Population White Paper, published by National Population and Talent Development (NPTD), the country’s population size is expected to grow further and ultimately reach 6.5-6.9m in size by 2030.

Additionally, Singapore currently ranks third in the world – just ahead of Hong Kong – in terms of population density, according to statistics provided by the United Nations (UN). Thus, the future of Singapore’s CBD is well-focused on reducing congestion problems in the future.

Figure 51: Singapore is one of the most densely-populated countries in the world

Rank Country/terrioty Population Density (people/sq km)

1 Monaco 38,320 25,718.12

2 China, Macau SAR 584,420 22,477.69

3 Singapore 5,618,866 8,226.74

4 China, Hong Kong SAR 7,313,557 6,654.74

5 Gibraltar 29,354 4,892.33

6 Bahrain 1,359,726 1,959.26

7 Holy See 800 1,818.18

8 Sint Maarten (Dutch part) 46,914 1,379.82

9 Malta 431,239 1,364.68

10 Bermuda 65,578 1,237.32

Source: RHB, United Nations (UN)

In tackling its traffic flow issue, the Government is driven to decentralise commercial activities via setting up regional hubs. An example of this is the Tampines Regional Hub. It has also taken various initiatives – such as increasing the number of mixed developments and improving public transport accessibility – to reduce congestion within the CBD region.

Based on our survey of this region, we see an increasing number of mixed developments being constructed, with more to come in the years ahead. This is in line with our expectations.

Figure 52: The mixed development blueprint

Source: Urban Redevelopment Authority (URA)

Mixed developments will be increasingly popular. Mixed developments are nothing

new globally, but there has been a resurgence for them in Singapore over the last few years.

The CBD has been undergoing a transformation since the early 2000s, what with the Government’s push to encourage city living and ensure that this region remains lively in the evenings and on weekends. Historically, the CBD had been dominated by pure office buildings, together with a number of hotels and supporting retail amenities.

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 22

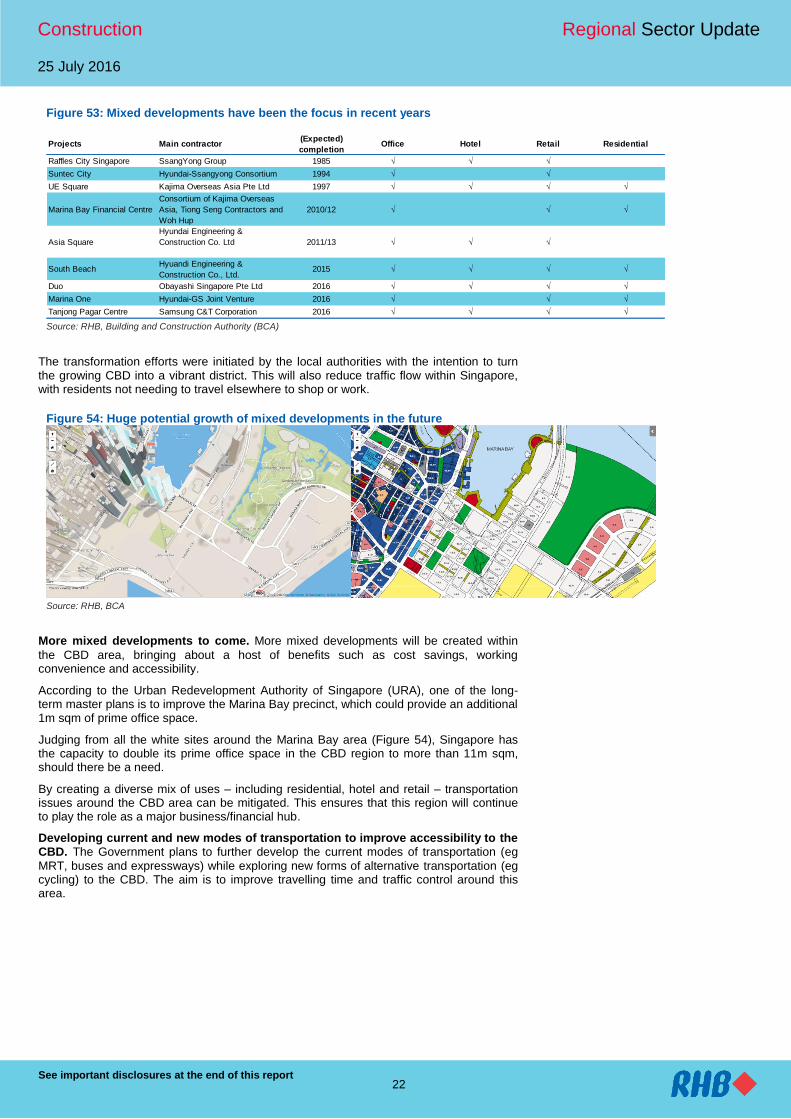

Figure 53: Mixed developments have been the focus in recent years

Projects Main contractor(Expected)

completionOffice Hotel Retail Residential

Raffles City Singapore SsangYong Group 1985 √ √ √

Suntec City Hyundai-Ssangyong Consortium 1994 √ √

UE Square Kajima Overseas Asia Pte Ltd 1997 √ √ √ √

Marina Bay Financial Centre

Consortium of Kajima Overseas

Asia, Tiong Seng Contractors and

Woh Hup

2010/12 √ √ √

Asia Square

Hyundai Engineering &

Construction Co. Ltd 2011/13 √ √ √

South BeachHyuandi Engineering &

Construction Co., Ltd.2015 √ √ √ √

Duo Obayashi Singapore Pte Ltd 2016 √ √ √ √

Marina One Hyundai-GS Joint Venture 2016 √ √ √

Tanjong Pagar Centre Samsung C&T Corporation 2016 √ √ √ √ Source: RHB, Building and Construction Authority (BCA)

The transformation efforts were initiated by the local authorities with the intention to turn the growing CBD into a vibrant district. This will also reduce traffic flow within Singapore, with residents not needing to travel elsewhere to shop or work.

Figure 54: Huge potential growth of mixed developments in the future

Source: RHB, BCA

More mixed developments to come. More mixed developments will be created within

the CBD area, bringing about a host of benefits such as cost savings, working convenience and accessibility.

According to the Urban Redevelopment Authority of Singapore (URA), one of the long-term master plans is to improve the Marina Bay precinct, which could provide an additional 1m sqm of prime office space.

Judging from all the white sites around the Marina Bay area (Figure 54), Singapore has the capacity to double its prime office space in the CBD region to more than 11m sqm, should there be a need.

By creating a diverse mix of uses – including residential, hotel and retail – transportation issues around the CBD area can be mitigated. This ensures that this region will continue to play the role as a major business/financial hub.

Developing current and new modes of transportation to improve accessibility to the CBD. The Government plans to further develop the current modes of transportation (eg

MRT, buses and expressways) while exploring new forms of alternative transportation (eg cycling) to the CBD. The aim is to improve travelling time and traffic control around this area.

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 23

Figure 55: One of the main MRT developments is to develop the Thomson East Coast Line (TEL)

Source: RHB, Land Transport Authority (LTA)

Key MRT developments within the CBD region are:

i. The Thomson East Coast Line (TEL) is expected to open in 2019. It will bring about greater accessibility to the CBD area by connecting the Eastern Region Line with the Thomson Line;

ii. The Downtown Line is also expected to have all stations up and ready by 2017, making it easier for more commuters to access CBD areas;

iii. Circle Line Stage 6 (CCL6) is slated to be ready by 2025, which will allow commuters staying in the west of the republic to have better access to the CBD area.

Other than the completion of new MRT lines, the Singapore Land Transport Authority (LTA) aims to have more than 90% of all buildings in CBD to be within 400m of the nearest MRT station by 2025. The walking routes will also be sheltered to facilitate travelling within the CBD area.

Bus services towards the CBD. The Bus Service Enhancement Programme (BSEP)

aims to create more bus services in the CBD area. Commuters now enjoy direct journeys to the CBD following the implementation of five new City Direct Services (CDS) in February-March, bringing the total number of CDS to 20.

Expressways. The completion of the North-South Expressway (NSE) by 2020 will link

areas like Bishan, Toa Payoh and Novena to the CBD. Commuters in the north-south region should see a significant 30% improvement in their travelling times. For example, with the new NSE expressway, it will take only 20-30 minutes to travel from Yishun to the CBD vs 30-35 minutes currently.

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 24

Figure 56: Cycling route to the CBD

Source: URA

Cycling infrastructure. The URA plans to shift focus towards cycling as a form of

alternative transport, especially towards the CBD area. One option that it is considering is redesigning Kallang Park Connector to be a north-south commuter cycling route from the central to the CBD areas. Cyclists will take an average of 30-45 minutes to travel from one end to the other.

Green is the new black. Adopting cleaner energy will be a major trend within Singapore’s

infrastructure sector. As a low-lying, densely-populated island in the tropics, the country is vulnerable to the impact of climate change.

In view of this, it is essential for Singapore to move towards becoming a nation with “greener buildings”, which will reduce its energy intensity. As such, the Government targets to:

i. Increase greenery in high-rise buildings to 50ha by 2030;

ii. To have 80% of the current existing buildings achieve the Building & Construction Authority’s (BCA) Green Mark certification, at the very least.

The BCA’s Green Mark scheme is a green building rating system that evaluates a building for its environmental impact and performance. The assessment criteria for the certification cover:

i. Energy efficiency;

ii. Water efficiency;

iii. Environmental protection;

iv. Indoor environment quality;

v. Other green features and innovations.

Therefore, we expect energy-saving infrastructure to increase, not only within the CBD region, but across Singapore as well.

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 25

Figure 57: Funds have been set up to achieve a greener nation

Source: BCA

Initiative well backed by the Government. As shown in Figure 57, multiple funds have

been set up by the authorities to build a more sustainable Singapore. The largest initiative is the SGD52m Green Buildings Innovation Cluster (GBIC), an integrated building energy efficiency research, development & demonstration (RD&D) hub that aims to help bolster the link between research and how it translates into public policy.

Green buildings since 2000. Capital Tower (along Robinson Road) became Singapore’s

first intelligent building when it was completed in 2000. It has set the trend for green buildings on the island.

Figure 58: High growth of green buildings in Singapore

Title:

Source:

Please fill in the values above to have them entered in your report

17 33127

239427

732

1,171

1,557

2,0032,155

2,524

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

0

500

1,000

1,500

2,000

2,500

3,000

Sep

-05

Sep

-06

Sep

-07

Sep

-08

Sep

-09

Sep

-10

Sep

-11

Sep

-12

Sep

-13

Sep

-14

Sep

-15

[LHS] Number of green buildings [RHS] GFA (m sq f t)

Source: RHB, BCA

Since the BCA’s Green Mark scheme kicked off in 2005, the number of green buildings in Singapore has surged to more than 2,500 today from 17 originally. This translates into over 70m sqm of GFA, or c.29% of total GFA in the country.

Interestingly, green building tenants tend to be multi-national corporations (MNCs) and large locally-listed organisations. This is because they have carbon commitments and climate policies to adhere to, according to a 19 Oct 2015 report by the Business Times.

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 26

Figure 59: Projects under construction I

Project Name Project type Project Owner District # of cranesConstruction

progress (%)

Marina One Office M+S Pte Ltd Marina Bay 7 83%

SBF Centre (strata titled) Office FEO Shenton Way 1 83%

EON Shenton (strata titled) Office 70 Shenton Pte Ltd Shenton Way 0 83%

GSH Plaza (strata titled) Office Plaza Venture Pte Ltd Raffles Place 1 83%

Duo Office M+S Pte Ltd Beach Rd/ City Hall 1 89%

Guoco Tower Office GuocoLand Tanjong Pagar 1 97%

Redevelopment of International Factors

Building and Robinson TowersOffice Tuan Sing Robinson Road 1 50%

5 Shenton Way Office UIC Land Shenton Way 1 75%

Oxley Tower (strata titled) Office Oxley Holdings Robinson Road 1 73%

Frasers Tower Office Frasers Centrepoint Shenton Way 2 31%

Havelock II RetailHorizon Value Investments SP3 Pte Ltd

(Gutherie GTS Limited)Havelock Road 0 97%

Hotel Development at Middle Road

(Former Midlink Plaza)Retail 122 Middle Investment Pte Ltd 122 Middle Road 0 97%

Duo Galleria Retail Ophir-Rochor Commercial Pte Ltd Fraser Street 0 83%

Refurbishment of Gallery Hotel Retail RB Corp Pte Ltd Nanson Road 1 83%

Downtown Gallery Retail OUE Shenton Way 1 75%

City Gate Retail Bayfront Ventures Pte Ltd Beach Road 1 22%

Office/shopping development (Former

Tower Fifteen, Sky Tower)Retail Fragrance Grandeur Pte Ltd Hoe Chiang Road 1 0%

Mercure Singapore Middle Road Hotel Accor Middle Road 0 97%

M Social Hotel Millennium Hotels Robertson Quay 0 97%

Premier Inn Singapore HotelMaster Contract Services Pte Ltd/ Fine

Grain Property ConsortiumBeach Road 0 97%

InterContinental Singapore Robertson

Quay (formerly Gallery Hotel)Hotel Frasers Hospitality Trust Havelock Road 0 83%

Swissôtel Merchant Court Hotel Accor Merchant Road 0 83%

Novotel Singapore on Stevens Hotel Oxley Gem Pte Ltd Stevens Road 1 33%

Somerset Grand Cairnhill Singapore

RedevelopmentHotel CapitaLand Cairnhill Road 1 33%

Murray House Hotel China Classic Pte Ltd Maxwell Road 1 33%

Ibis Singapore on Stevens Hotel Oxley Gem Pte Ltd Stevens Road 1 33%

YOTEL Orchard Road Hotel Yat Yuen Hong Co Orchard Road 1 33%

The Biltmore Hotel Granmil Holdings Pte Ltd Cuscaden Road 1 0%

Frasers @ China Street Hotel Frasers Centrepoint China Street 1 0% Source: RHB

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 27

Figure 60: Projects under construction II

Project Name Project type Project Owner District # of cranes Construction

progress (%)

3 Orchard By-The-Park Residential YTL Westwood Properties Pte Ltd Orchard Boulevard 1 58%

Cairnhill Nine Residential CH Commercial Pte Ltd/CH Residential

Pte Ltd

Cairnhill Road 1 58%

DUO Residences Residential Ophir-Rochor Commercial Pte Ltd/Ophir-

Rochor Hotel Pte Ltd/Ophir-Rochor

Fraser Street 1 50%

Eon Shenton Residential 70 Shenton Pte Ltd Shenton Way 1 13%

Ferra Residential Far East Lighthouse Pte Ltd/Orchard

Landmark Pte Ltd

Leonie Hill 1 17%

Goodwood Grand Residential Feature (Balmoral) Pte Ltd Balmoral Road 1 17%

Gramercy Park Residential Aston Properties Pte Ltd Grange Road 1 83%

Liv On Sophia Residential RH Mount Sophia Pte Ltd Adis Road 1 0%

Liv on Wilkie Residential RH Rochor Pte Ltd Wilkie Terrace 1 0%

Lloyd Sixtyfive Residential TG (2010) Pte Ltd Lloyd Road 1 83%

New Futura Residential City Sunshine Holdings Pte Ltd Leonie Hill Road 1 0%

One Balmoral Residential Hong Leong Holdings Ltd Balmoral Road 1 58%

Oxley Edge Residential Oxley Mosaic Pte Ltd River Valley Road 1 83%

Residential apartments Residential Yow Cheong Pte Ltd Balmoral Road 1 58%

Residential apartments Residential Celestial Fortune Pte Ltd Draycott Park 1 58%

Robinson Suites Residential 50 Robinson Pte Ltd Robinson Road 1 83%

Service apartments in OUE Downtown 1 Residential Alkas Realty Pte Ltd Shenton Way 1 83%

Sophia Hills Residential Hoi Hup Sunway Mount Sophia Pte Ltd Mount Sophia 1 28%

Strata housing development Residential Far East Land And Housing

Development Co Pte Ltd

Peirce Road 1 28%

The Met @ 18 Residential Newfort Realty Pte Ltd Mount Elizabeth 1 28%

The Rise @ Oxley - Residences Residential Oxley Rise Pte Ltd Oxley Rise 1 13%

The Scotts Tower Residential Far East Success Development Pte

Ltd/Whitewater Properties Pte Ltd

Scotts Road 1 33%

The Siena Residential Far East SOHO Pte Ltd Tan Kim Cheng Road 1 50%

Valley House Residential Kwan Im Thong Hood Cho Temple River Valley Road 1 50%

Wallich Residence at Tanjong Pagar Centre Residential Belmeth Pte Ltd/Guston Pte Ltd/Perfect

Eagle Pte Ltd

Wallich Street 1 83%

Source: RHB

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 28

Thailand For Bangkok, which is also known as the City of Angels, we made the 304m tall Baiyoke Tower II the centre of our survey area. This is because this 85-storey building has been the tallest structure in the city since 1997. However, there are two new skyscrapers in the pipeline that will be taller than this building:

i. The MahaNakhon project, located next to RHB Securities’ (Thailand) head office, will be 10m higher than Baiyoke Tower II and is expected to be fully completed within 4Q16. However, Baiyoke Tower II’s location – at the centre of the CBD – seems more superior and the radius around the building covers many types of construction projects, ie residential, commercial, government centres, etc;

ii. The 615m-high Super Tower will be almost double the height of the MahaNakhon. The project, which has not begun construction yet, is set to be the tallest structure in Bangkok by FY19 at the earliest. However, the Super Tower will be located outside of the CBD.

We choose Baiyoke Tower II as the centre of our survey area, due to the following factors:

i. It is located in Bangkok’s CBD and is the tallest structure within a 3km radius. The survey area covers two districts fully and eight districts partially (out of a total of 50 districts in Bangkok). Note that these 10 districts are significant to the city in terms of economic contributions, ie more than 50% of Bangkok’s tax revenue comes from these areas;

ii. With its location, we are able to cover diversified economic activities that are found in different areas. There are several well-known commercial projects towards the south, such as Siam Paragon, Central World and Silom Road. Towards the north lie a hub of government agencies and a military base. Eastwards, there are new-generation residential projects that are popular, especially mid- to high-end condominiums, in Asoke, Ploenchit, Nana, Rama IX and Ratchadapisek amongst others. Meanwhile, towards the west, communities in the old part of Central Bangkok have been living there for a long time.

Figure 61: Baiyoke Tower II is the centre of our survey area Figure 62: Condominium projects dominate the CBD area

Source: RHB Source: RHB

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 29

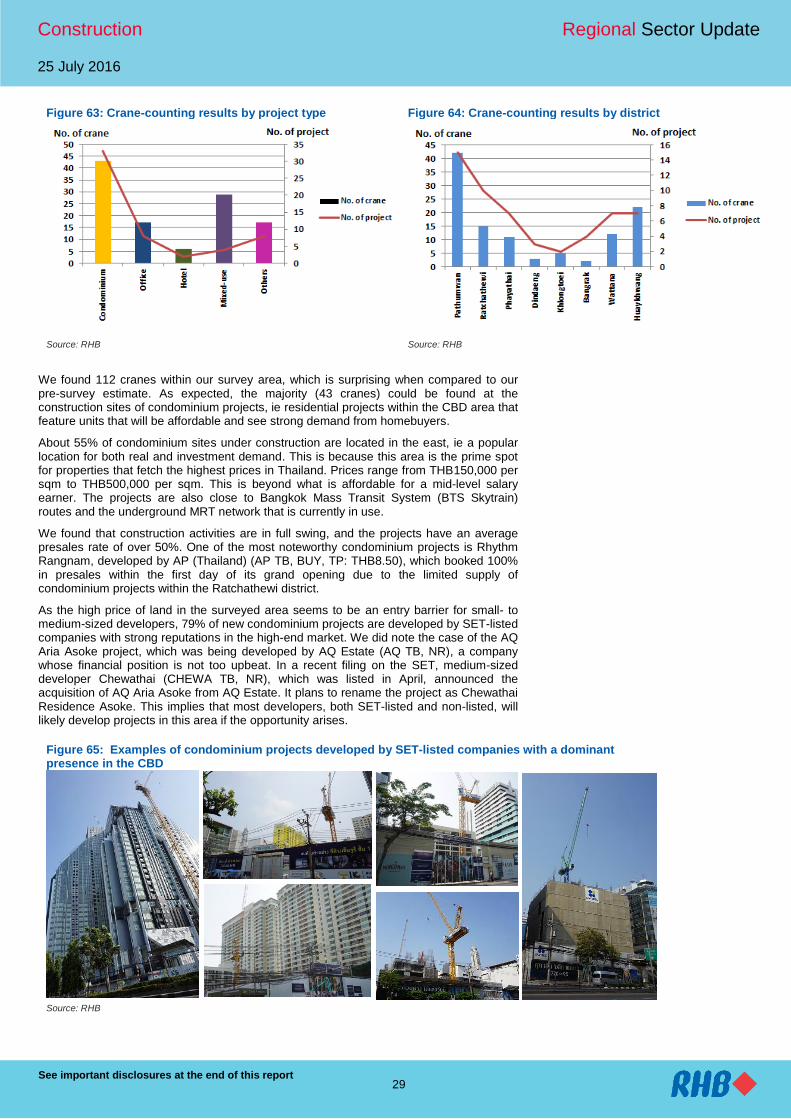

Figure 63: Crane-counting results by project type Figure 64: Crane-counting results by district

Source: RHB Source: RHB

We found 112 cranes within our survey area, which is surprising when compared to our pre-survey estimate. As expected, the majority (43 cranes) could be found at the construction sites of condominium projects, ie residential projects within the CBD area that feature units that will be affordable and see strong demand from homebuyers.

About 55% of condominium sites under construction are located in the east, ie a popular location for both real and investment demand. This is because this area is the prime spot for properties that fetch the highest prices in Thailand. Prices range from THB150,000 per sqm to THB500,000 per sqm. This is beyond what is affordable for a mid-level salary earner. The projects are also close to Bangkok Mass Transit System (BTS Skytrain) routes and the underground MRT network that is currently in use.

We found that construction activities are in full swing, and the projects have an average presales rate of over 50%. One of the most noteworthy condominium projects is Rhythm Rangnam, developed by AP (Thailand) (AP TB, BUY, TP: THB8.50), which booked 100% in presales within the first day of its grand opening due to the limited supply of condominium projects within the Ratchathewi district.

As the high price of land in the surveyed area seems to be an entry barrier for small- to medium-sized developers, 79% of new condominium projects are developed by SET-listed companies with strong reputations in the high-end market. We did note the case of the AQ Aria Asoke project, which was being developed by AQ Estate (AQ TB, NR), a company whose financial position is not too upbeat. In a recent filing on the SET, medium-sized developer Chewathai (CHEWA TB, NR), which was listed in April, announced the acquisition of AQ Aria Asoke from AQ Estate. It plans to rename the project as Chewathai Residence Asoke. This implies that most developers, both SET-listed and non-listed, will likely develop projects in this area if the opportunity arises.

Figure 65: Examples of condominium projects developed by SET-listed companies with a dominant presence in the CBD

Source: RHB

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 30

Figure 66: There are only a few condominium projects developed by non-listed companies in the CBD, due to the high prices of land, which are a barrier to entry

Source: RHB

In addition to the actual number of cranes exceeding our expectation, we were also surprised to find some industries in expansion mode. These include:

i. Healthcare sector. There are nine cranes (or 8% of the total crane count) actively

involved in works for companies within this sector. Many are public and private hospitals that have strong reputations locally. We found three leading public healthcare institutions – Rajavithi Hospital, Phramongkutklao Hospital and the Thai Red Cross College of Nursing – under the process of new construction activities. The highlight development in this sector is the new 25-storey medical centre under Rajavithi Hospital. The latter has been providing medical services for 65 years now and its new building is designed to provide medical services. This is essential as Bangkok’s low-income segment is dependent on public hospitals, which normally recruit highly-experienced doctors but charge much lower rates vis-à-vis private hospitals. Currently, low-income patients spend half a day on average while waiting to see a doctor. The factors behind the expansion of public hospitals (as well as private hospitals) in Bangkok and nationwide are:

a. The rising proportion of the aging population in Thailand is anticipated to constitute 20% of the total population in FY25;

b. The low number of doctors to the total population should be rising to be on par with other ASEAN member states;

c. The urbanisation trend.

Figure 67: Proportion of aging population to reach 20% within FY25

Year Total population

(million) % of total population

Age: 0-14 years Age: 15-59 years Age: 60 years and above 2010 67.0 21.2 67.1 11.7 2015 69.1 20.2 66.0 13.8

2020F 70.8 19.0 64.2 16.8 2025F 72.3 18.0 62.0 20.0

Source: Office of The National Economic and Social Development Board

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 31

Figure 68: Rajavithi Hospital is constructing a new – and its largest building – in the healthcare sector

Source: RHB

Figure 69: New research centre being built for Phramongkutklao Hospital

Figure 70: Thai Red Cross College is constructing a new building to expand its capacity to educate new nursing students

Source: RHB Source: RHB

ii. Education sector. Although the crane count for projections under construction for

the education sector stood at four only (or 3.5% of the total crane count), this indicated that schools are keen to capture the strong demand for higher-level education. Such education will be needed for Thailand’s “Generation Z”, ie those born in 1997 and thereafter will complete Bachelor degree from university in the next few years. Education is a long-term business, as a more educated Generation Y enters parenthood. We think this generation will tend to have a bigger budget to spare for the education of their children and siblings. We discovered three construction sites for university campuses. Two of these are new faculty buildings, while the third is a car park facility for Master of Business Administration (MBA) students.

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 32

Figure 71: Construction works for the educational centre for environmental studies under Chulalongkorn University’s faculty of architecture

Figure 72: Construction site of the operations centre for Chulalongkorn University’s health science department

Source: RHB Source: RHB

Figure 73: New car parking building for students at the University of the Thai Chamber of Commerce (UTCC) campus

Source: RHB

iii. Hotel sector to expand to new locations. Normally, 4-5 star hotels in Bangkok are

concentrated in the central area of the CBD. However, we found one mixed-use project in the northern part of this district, which currently has offices and condominiums only. This 34-floor project combines a 180-room hotel with office spaces. The hotel opens up a new option for hospitality facilities to be located with easy access to the BTS Skytrain network – especially since land prices in the CBD have surged in the past few years. This may give hotel developers ideas on alternative locations to expand new projects.

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 33

Figure 74: Ari Hill, a mixed-use building comprising offices and a hotel

Figure 75: Ari Hill project’s progress

Source: Urban Capital Source: RHB

The game of landlords

Within the 28.3 sq km surveyed area, we also discovered what seems to be a classic game of Monopoly being played by the city’s landlords. Currently, there are three big land plots in Bangkok’s CBD with high potential for large-scale projects – and each plot is owned by a different entity. Chulalongkorn University owns the first plot, which is located close to its campus and near Siam Square. The latter is a trendy shopping area for Thai teenagers.

The second plot is owned under a leasehold concession by the Sirivadhanabhakdi family, which owns Chang Beer and the TCC Group. It is located in a prime area, at the Wireless Road intersection near the Japanese embassy and the beginning of Sathorn Road. However, these two entities are historically slow movers by nature and we expect no significant construction activities at this moment.

Construction is active at the third plot of land called Langsuan Village. Spanning 56 rai (or about 9ha), it is owned by Siam Sindhorn Co Ltd, which, in turn, is under the auspices of the Crown Property Bureau. Langsuan Village is located in a peaceful and green part of the CBD. It offers a view of Lumpini Park, the most popular recreational area for employees after working hours. Our ground checks show that Langsuan Village currently has 17 cranes (15% of the total crane count). This is the highest number of cranes in our surveyed areas. Construction is at an early stage, with foundation works done by SEAFCO Pcl (SEAFCO TB, NR). As the plot of land is large, the project is a mixed-use development comprising:

i. Four leasehold condominium buildings;

ii. Three serviced apartment blocks;

iii. A hotel;

iv. A health centre;

v. An art museum.

Some construction works in the project will be completed from FY19 onwards, and this project is set to transform the area from being a quiet place during the weekends to a busy area every day.

However, the slow movement of two land plots mentioned above can be seen as a positive factor that will not lead to an oversupplied situation within the area. This is because the three areas are located within a 10 minute drive from each another. Therefore, there is a pipeline of mix-used projects and construction in this prime CBD area, which will continue to be active for the next five years.

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 34

Figure 76: The master plan of the Langsuan Village project

Source: www.langsuanvillage.com

The fourth large land plot, which housed the former quarters of the Japanese Embassy, is currently owned by Singha Estate (S TB, NR). The latter is majority-owned by the family that owns Singha Beer. The Singha Complex project spans 8.8 rai (1.4ha) and is currently under construction, ie at the early stage of foundation works. It is planned as a mixed-use project comprising 50,000 sqm of office space and 6,000 sqm of retail space in the Asoke area. This project will not affect the three land plots that we mentioned earlier, as it is not close to them. Moreover, the project owner will also relocate its headquarters to this project and lease 20% of its total office space. However, this project should be another landmark for this specific location that will attract other developers to launch more new projects – especially condominiums – in the vicinity.

Figure 77: Master plan of the Singha Complex project Figure 78: Singha Complex project’s progress

Source: Singha Estate Source: RHB

Conclusion

Based on the availability of the expressway network, and BTS Skytrain and MRT underground routes within Bangkok’s CBD, SET-listed companies’ condominium projects for mid- to high-end customers dominate the market. There are obvious trends, however:

i. The expansion of the facilities of long-term growth businesses such as hospitals and university campuses;

ii. The game of mixed-use projects being played by Thai landlords;

iii. Fresh signs that the hospitality sector may expand to a new location in the CBD.

According to the Government’s infrastructure investment plan for FY15-22, all projects will be focused in non-CBD areas. However, some projects to be launched for bidding in the near future - including the Orange Line, Yellow Line and Pink Line MRT works – are aimed at transporting people into two key route networks in the CBD area. Therefore, the trend of new projects (especially for the services sector) is inevitable. This should keep the construction of high-rise projects in the CBD active for at least the next five years.

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 35

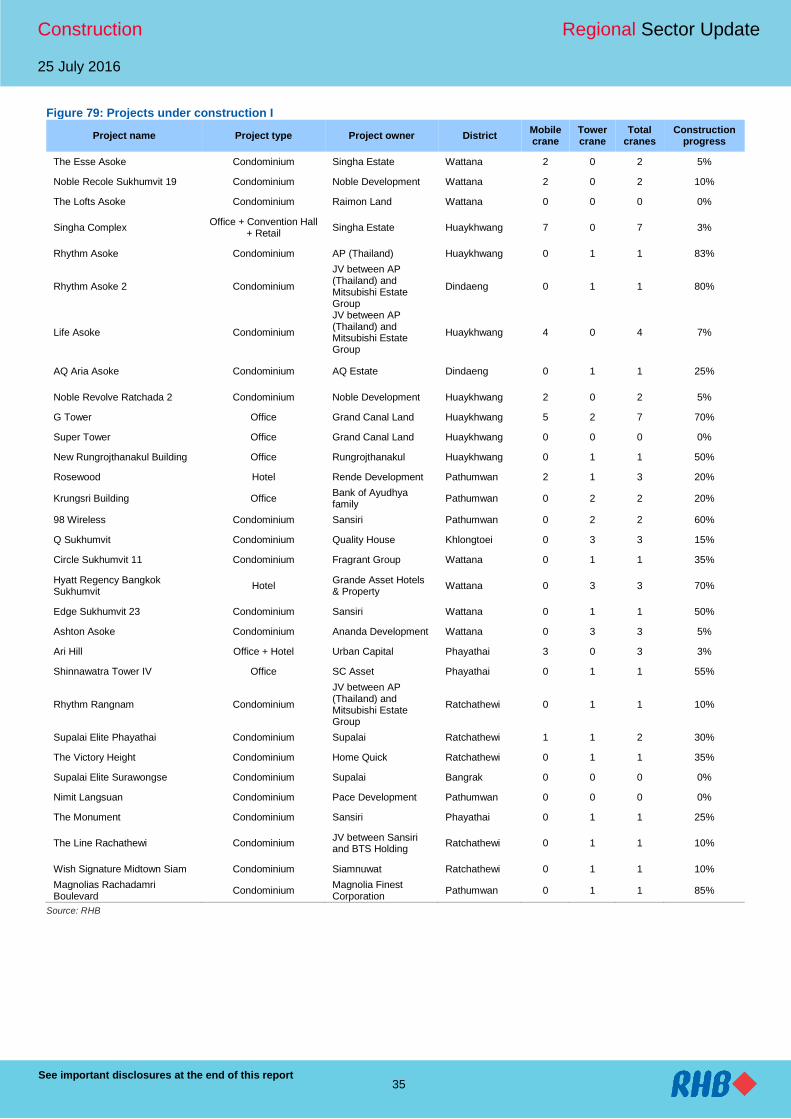

Figure 79: Projects under construction I

Project name Project type Project owner District Mobile crane

Tower crane

Total cranes

Construction progress

The Esse Asoke Condominium Singha Estate Wattana 2 0 2 5%

Noble Recole Sukhumvit 19 Condominium Noble Development Wattana 2 0 2 10%

The Lofts Asoke Condominium Raimon Land Wattana 0 0 0 0%

Singha Complex Office + Convention Hall

+ Retail Singha Estate Huaykhwang 7 0 7 3%

Rhythm Asoke Condominium AP (Thailand) Huaykhwang 0 1 1 83%

Rhythm Asoke 2 Condominium

JV between AP (Thailand) and Mitsubishi Estate Group

Dindaeng 0 1 1 80%

Life Asoke Condominium

JV between AP (Thailand) and Mitsubishi Estate Group

Huaykhwang 4 0 4 7%

AQ Aria Asoke Condominium AQ Estate Dindaeng 0 1 1 25%

Noble Revolve Ratchada 2 Condominium Noble Development Huaykhwang 2 0 2 5%

G Tower Office Grand Canal Land Huaykhwang 5 2 7 70%

Super Tower Office Grand Canal Land Huaykhwang 0 0 0 0%

New Rungrojthanakul Building Office Rungrojthanakul Huaykhwang 0 1 1 50%

Rosewood Hotel Rende Development Pathumwan 2 1 3 20%

Krungsri Building Office Bank of Ayudhya family

Pathumwan 0 2 2 20%

98 Wireless Condominium Sansiri Pathumwan 0 2 2 60%

Q Sukhumvit Condominium Quality House Khlongtoei 0 3 3 15%

Circle Sukhumvit 11 Condominium Fragrant Group Wattana 0 1 1 35%

Hyatt Regency Bangkok Sukhumvit

Hotel Grande Asset Hotels & Property

Wattana 0 3 3 70%

Edge Sukhumvit 23 Condominium Sansiri Wattana 0 1 1 50%

Ashton Asoke Condominium Ananda Development Wattana 0 3 3 5%

Ari Hill Office + Hotel Urban Capital Phayathai 3 0 3 3%

Shinnawatra Tower IV Office SC Asset Phayathai 0 1 1 55%

Rhythm Rangnam Condominium

JV between AP (Thailand) and Mitsubishi Estate Group

Ratchathewi 0 1 1 10%

Supalai Elite Phayathai Condominium Supalai Ratchathewi 1 1 2 30%

The Victory Height Condominium Home Quick Ratchathewi 0 1 1 35%

Supalai Elite Surawongse Condominium Supalai Bangrak 0 0 0 0%

Nimit Langsuan Condominium Pace Development Pathumwan 0 0 0 0%

The Monument Condominium Sansiri Phayathai 0 1 1 25%

The Line Rachathewi Condominium JV between Sansiri and BTS Holding

Ratchathewi 0 1 1 10%

Wish Signature Midtown Siam Condominium Siamnuwat Ratchathewi 0 1 1 10%

Magnolias Rachadamri Boulevard

Condominium Magnolia Finest Corporation

Pathumwan 0 1 1 85%

Source: RHB

Construction Regional Sector Update

25 July 2016

See important disclosures at the end of this report 36

Figure 80: Projects under construction II

Project name Project type Project owner District Mobile crane

Tower crane

Total cranes

Construction progress

Saladaeng One Condominium SC Asset Bangrak 1 0 1 5%

Ideo Q Siam-Ratchathewi Condominium Ananda Development Ratchathewi 0 2 2 10%

Ideo Q Chula-Samyan Condominium Ananda Development Bangrak 0 1 1 98%

Ashton Chula-Silom Condominium Ananda Development Bangrak 0 0 0 0%

Q Chidlom Condominium Ananda Development Pathumwan 1 1 2 3%

Maestro 14 Condominium Major Development Ratchathewi 0 0 0 0%

Metro Luxe Condominium Property Perfect Phayathai 0 0 0 0%

Pearl Bangkok Office TCT (owned by Thongma Vijitphongpun)

Phayathai 0 3 3 65%

Car Parking building Car Parking building University of the Thai Chamber of Commerce

Dindaeng 0 1 1 25%

Metro Luxe Phahol-Suthisarn Condominium Property Perfect Phayathai 0 1 1 70%

New Medical Center Building Hospital Rajavithi Hospital Ratchathewi 0 2 2 75%

New Research Center Building Hospital Phramongkutklao Hospital

Ratchathewi 0 3 3 20%

Operation Center for Health Science Department

Multi-purpose Building Chulalongkorn University

Pathumwan 0 2 2 70%

Educational Center for Environment

Multi-purpose Building Chulalongkorn University

Pathumwan 0 1 1 10%

Smile Square Shopping Center +

Office + Retail + Condominium + Hotel

Asia Thaiyuan Construction & Development

Ratchathewi 0 2 2 20%

Thavorn Tractor Building Office Thavorn Tractor Engineering

Pathumwan 0 1 1 20%

Sync Nature @ Siam Condominium Saichol Patana Pathumwan 0 1 1 60%

Gaysorn Office Tower Office Gaysorn Property Pathumwan 0 2 2 35%

Budget Bureau (New building) Government Office Ministry of Finance Phayathai 1 1 2 15%

Thai Red Cross College of Nursing (New building)

Hospital Chulalongkorn Hospital

Pathumwan 4 0 4 3%

New Khlongtoei branch office State Agency Office Metropolitan Electricity Authority

Khlongtoei 2 0 2 5%

Sindhorn Midtown Condominium Siam Sindhorn Pathumwan 3 0 3 3%

Sindhorn Residence Condominium Siam Sindhorn Pathumwan 0 1 1 75%

Langsuan Village Mixed-use Siam Sindhorn Pathumwan 17 0 17 5%

Source: RHB

Indonesia Company Update

See important disclosures at the end of this report 37

Powered by the EFA Platform

25 July 2016 Construction & Engineering | Construction

Adhi Karya Persero Buy (Maintained)

Target Price: IDR3,400

Price: IDR2,720

Ready To Run Market Cap: USD739m

Bloomberg Ticker: ADHI IJ We continue to like Adhi Karya given its position as the cheapest state-owned contractor in the market and its strong earnings visibility, backed by the Greater Jakarta LRT project. We expect the company to book a strong new contract collection of IDR41.5trn (including the LRT project) in FY16, up 197.1% YoY. The Government’s continued focus on infrastructure spending should benefit the company directly. Maintain BUY with an unchanged IDR3,400 TP (25% upside), which implies 18x FY16F P/E.

Share Data

Avg Daily Turnover (IDR/USD) 49,161m/3.70m

52-wk Price low/high (IDR) 1,464 - 2,870

Free Float (%) 49

Shares outstanding (m) 3,561

Estimated Return 25%

Shareholders (%)

Republic of Indonesia 76.8

Dimensional Fund Advisors LP 1.9

Schroder Investment Management 1.2

Share Performance (%)

YTD 1m 3m 6m 12m

Absolute 27.1 (3.6) (4.7) 11.2 17.4