undergraduate research symposium - bitcoin price fluctuations & infamous reputation

TRANSCRIPT

1 Bitcoin and the Blockchain

Authors: Rhiannon Gladney & Marvin Norwood

Acknowledgements: Dr. Djeto Assane

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 2

Table of Contents:

COVER PAGE...............................................................................................................................................................1

TABLE OF CONTENTS ...........................................................................................................................................2

ABSTRACT ...................................................................................................................................................................3

INTRODUCTION .......................................................................................................................................................4

LITERATURE REVIEW..........................................................................................................................................6

THE MODEL .............................................................................................................................................................10

DESCRIPTIVE STATISTICS………………………………………………………………………………….13

EMPIRICAL RESULTS…………………………………………………………………………………………15

CONCLUSION……………………………………………………………………………………………………..25

REFERENCES……………………………………………………………………………………………………..26

APPENDIX (STATA RESULTS)……..…………………..………………………………………………….27

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 3

Abstract:

Bitcoin is both a digital asset and a payment system. In 2008, bitcoins were first published

and developed by the allusive Satoshi Nakamoto. This new system does not require a financial

intermediary; in other words, it is peer-to- peer. The transactions are verified by network nodes and

then recorded in a ledger, the blockchain. The blockchain uses bitcoins as its unit of account. This

system does not require a central repository or an administrator. With that being said, bitcoin is the

very first decentralized digital currency and is considered the first successful cryptocurrency.

Putting bank opposition, price fluctuation, and bitcoin’s ‘bad’ reputation aside, bitcoin is just

a currency; it is a currency with great potential. Paired with the blockchain system, bitcoins have to

the potential to create a new way to buy and purchase items securely and affordably. This report

attempts to answer the question: Has ‘fluctuating price’ and an infamous reputation prevented an

otherwise secure and affordable system for financial transactions, bitcoin and its blockchain, from

being widely implemented? Mainly, this report focuses on bitcoin’s fluctuating prices because they

are much more testable than bitcoin’s reputation.

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 4

I. Introduction: Bitcoin is both a digital asset and a payment system. In 2008, bitcoins were first published

and developed by the allusive Satoshi Nakamoto. This new system does not require a financial

intermediary; in other words, it is peer-to- peer. The transactions are verified by network nodes and

then recorded in a ledger, the blockchain. The blockchain uses bitcoins as its unit of account. This

system does require a central repository or an administrator. With that being said, bitcoin is the very

first decentralized digital currency and is considered the first successful cryptocurrency.

The inspiration for this proposal came from the increased development of the blockchain

technology by major banks that has been all over the news recently; major banks are attempting to

create a universal and highly secure ledger system by experimenting with blockchain technology;

some of these major banks include: BNP Paribas, Société Générale (SocGen), Citi Bank, UBS, Barclays,

Goldman Sachs, Banco Santander, and Standard Chartered.

The blockchain is not only exceedingly secure but it is also exceedingly transparent. The

blockchain publically displays all transactions without exposing secure private information of the

senders or of the recipients. It stands as proof of all the transactions on the network. Each time a

block gets completed, a new block is generated. For austerity, consider conventional banking as an

analogy, the blockchain is like a full history of banking transactions. bitcoin transactions are entered

chronologically in a blockchain just the way bank transactions are. Blocks, meanwhile, are like an

individual. These banks are all for the blockchain but they are not all for bitcoins. This is mostly due

to bitcoins being decentralized and unregulated.

In regards to bitcoins being ‘decentralized’, this means that there will only ever be 21

million bitcoins in existence, because of this no central bank will needed to manage bitcoin’s money

supply or manage bitcoin’s interest rate. In regards to bitcoins being ‘unregulated’, that does not

mean that there are no laws regarding bitcoin; actually, a wide variety of laws and regulations have

been applied to the use of bitcoin since its inception in 2009. Instead, it is more accurate to say that

bitcoin is never unregulated. bitcoin’s protocol is ultimately a set of rules that regulates the currency,

and the peer-to-peer network enforces these rules in its operation. At its core bitcoin is an attempt at

regulation through cryptography, rather than through human operated institutions.

When paying with bitcoin, neither the buyer or the seller has to provide any personal

information. This means they do not have to provide bank account information, or credit card

information. This prevents against identity Theft and Fraud (Including Chargebacks) The perks to

using a bitcoin Wallet is that are no overdraft fees , no ATM fees, no service fees, no maintenance fees,

etc. Many of these banks are creating their own versions of bitcoins; some examples include:

MUFGCoin, BK Coin, CITICoin, SETLCoin, and eCM. There is speculation that prophesizes that the

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 5

popularization of bitcoin and bitcoin wallets could lead to the end of bank accounts. Instead of bitcoin

being the universal cryptocurrency; every individual bank would have their own individual currency.

This provides the banks not only branding opportunities but also provides a way for the banks to

stay relevant.

Bank opposition aside, another bitcoin adversary is bitcoin’s notorious fluctuating prices.

The bitcoin exchange equivalent of $1 US Dollar has been at times upward of $1100.00 and at other

times lower than $10.00. That does not exactly make bitcoin seem like a steady resilient currency.

Although, since 2014, bitcoin’s price has been relatively stable. It has mostly remained in the realm of

1 bitcoin exchanging for $400.00 US Dollars. In May of 2016, 1 bitcoin was exchanging for roughly

$445.16. In June of 2016, bitcoin experienced its first major spike in two years. This was due to

speculation in regards to Brexit, the United Kingdom exiting the European Union. However, it is

worth noting that all of the major currencies experienced major price fluctuations due to

speculations regarding Brexit. bitcoin was not alone in this.

In order to quantitatively prove that bitcoin’s prices have remained relatively stable since

2014, I have actually attempted to run a time series regression that uses variables devised different

increments of time, such as: the average value prediction of bitcoins traded, in two day, five day,

seven day, ten day, twenty day, and fifity day intervals. There is also a variable that is a measure of

the likelihood that the price will be the same as the day before.

Putting price fluctuations aside, the other reason that bitcoin is not wildly popular with the

banks is due to its ‘bad reputation’. Illicit activities are heavily associated with bitcoin, including:

sales of illegal goods, sales of illegal drugs, sales of illegal weapons, assassins for hire, money

laundering services, unlawful gambling, etc. bitcoin’s ‘bad’ reputation came from its association with

the Deep Web. bitcoin and Tor together create the essential tool kit needed by Deep Web

lawbreakers. bitcoin is the currency used to purchase items on black markets found on the Deep

Web; Tor is the internet browser used to access these markets. However, at the end of the day,

bitcoin is just a currency; any currency can be used to purchase illicit items given the right

circumstance.

Putting bank opposition, price fluctuation, and bitcoin’s ‘bad’ reputation aside, bitcoin is

just a currency; it is a currency with great potential. Paired with the blockchain system, bitcoins have

to the potential to create a new way to buy and purchase items securely and affordably. This report

attempts to answer the question: Do bitcoin and the blockchain, together, provide a secure and

affordable system for financial transactions that is not being widely implemented because of bitcoin’s

‘fluctuating prices’, and because of bitcoin’s infamous reputation? Mainly, this report focuses on

bitcoin’s fluctuating prices because they are much more testable than bitcoin’s reputation.

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 6

II. Literature Review

Bitcoin and the blockchain ultimately should be considered an ideal pairing as a transaction

alternative. They were designed solely to make transactions easier, more efficient, more secure, and

more affordable. Please note that bitcoin was not designed to replace existing currencies or become a

national currency of any sort. Singh’s journal, Performance Comparison of Executing Fast Transactions

in Bitcoin Network Using Verifiable Code, studies the bitcoin blockchain network for electronic cash

transactions. It goes over how bitcoin transactions provide special precision of executing fast

transactions, with greater security and assurance, than the former method, Proof-Of- Work. This

study dives into the concepts of mutual trust and verifiable code execution between the payer and

the payee in the network. Most importantly, this study promotes the use of bitcoin blockchain

transactions in real life scenarios; where the transactions are especially quick.

Daniel Kraft’s, Difficulty Control for Blockchain-based Consensus Systems, highlights the true

potential of the blockchain and it will eventually become a notable and prevailing technology in the

years to come. He also makes note of how to improve the blockchain; how to make it even more

effective. He begins by examining the crucial ingredient of the bitcoin network, the “mining”, that was

designed by Nakamoto blockchain. This system is very quick and can derive predictions about block

times, for various hash-rate scenarios. Kraft proposes that the system be slowed down, just a little

bit, in order for it to be easier to control and monitor. This will ease the minds of many critics. Kraft’s

proposed system would also make expiration times more predictable, which would be more effective

at preventing potential accidental losses. This journal is tremendous because it highlights the

blockchain’s potential and its capability to improve.

M. Andrychowicz of University of Warsaw in his journal Secure Multiparty Computations on

Bitcoin, Andrychowicz writes in favor of bitcoin; he argues that bitcoin is an underrated currency. He

begins by stating bitcoin’s main features: it lacks a central authority that controls the transactions,

the list of its transactions is publicly available, its syntax allows more advanced transactions than

simply transferring the money, and properties of bitcoin can be used in the area of secure multiparty

computation protocols (MPCs). He continues by mentioning that bitcoins are an attractive way to

construct a version of timed commitments. This helps to obtain fairness in multiparty protocols. This

protocol “emulates the trusted third party”. The protocols are secure enough to handle multiparty

lotteries using the bitcoin currency, without relying on a trusted authority. Andrychowitz even

argues that bitcion would be great for online gambling sites. Gambling sites require a lot of security

so this quite a compliment towards bitcoin.

J. Bonneau’s journal, Research Perspectives and Challenges for Bitcoin Cryptocurrencies, also

advocates for bitcoin by addressing bitcoin’s successful rise to popularity, and their likely success in

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 7

being the preferred cryptocurrency. bitcoin gained billions of dollars of economic value despite the

cursory analysis of the system’s design. This is a truly amazing achievement, especially when

considering how much this success contradicts years of financial doctrine. Bonneau highlights a

magnitude of literature regarding important properties of bitcoin, especially properties regarding

bitcoin’s success compared to other financial transaction alternatives, including other

cryptocurrency coins. bitcoin has proven to be very successful at preventing fraud and theft; bitcoin

is even more successful at this prevention than its current notable rival the Altcoin. This report goes

into the exposition of Altcoins and how Altcoins compare to bitcoins; bitcoins come out favorably.

The consensus was devised by comparing the mechanisms used by the respective coins, the currency

allocation mechanisms used, and the key management tools used. This report is very useful,

especially when considering that major banks are making their own coin alternatives to bitcoin. This

report highlights that bitcoin alternatives might not be able to perform as well as Bitcoin.

George Hurlburt’s journal, Might the blockchain outlive Bitcoin, and Newstex’s journal, Banks

Using the Bitcoin Blockchain is like Putting a Bird in a Cage, thoroughly dive into the major Wall Street

banks, including: Citi Corp, Goldman Sachs, and Barclays, developing their own blockchain

technology and their own bitcoin alternatives. Hurburt’s journal mainly highlights how bitcoin’s

popularity and success lead the major banks to want to start developing coin and blockchain

technology. The banks began to take notice when: PayPal and Apple began accepting bitcoin back in

2015, the state of New York enacted legislation to open up the crypto-currency market for bitcoin

banking licensure, mining became a growth industry in China, Australia took action towards adopting

bitcoin as an actual regarded currency and when the U.S. federal government declared bitcoin as

taxable. The banks took notice and began their own development, but will their blockchain

technologies and alternative cryptocurrencies be effective alternatives to bitcoin? Newtex’s journal

entertains this question. Nextex boldly claims that these banks alternatives will not work. Onl y

bitcoin is the only coin that can be used in this fashion. Blockchains can only work properly when

using their native unit, bitcoin. If you remove the native unit, you then have a centralized system. A

centralized system would defeat the point. Major banks are not the only ones that took notice of

bitcoin and the blockchain, the major stock exchange, NASDAQ, took notice as well.

Hurlburt and Melin‘s journals regard the NASDAQ stock exchange developing outlets for

bitcoin and the blockchain technology. The respected stock exchange NASDAQ is adopting blockchain

technology for its stock trading. It is presumed to increase transaction efficiency. The blockchain

technology validates trades based on an algorithm that runs on third-party computers,

disintermediating the need for banks, clearing houses and intermediaries. Bitcoin provides level of

auditing that is purely based on mathematics and not based on trusting a third party. Bitcoin is not

only a currency, but also is more notably a technology that actually reduces transnational costs. Bob

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 8

Greifeld, NASDAQ’s CEO, said the blockchain technology would be used to modernize, streamline and

secure typically cumbersome administrative functions. NASDAQ plans to use the technology to first

tackle issuance and transfer of stocks on NASDAQ’s network. It truly is exceptional that NASDAQ is

taking on bitcoin and the blockchain technology considering the notoriety in regards to bitcoin’s

price fluctuations. The fact that major banks and NASDAQ are actually adopting the blockchain

technology really enforces that bitcoin and the blockchain really do have potential. However, Ittay

Eyal, Danny Bradbury, and Irena Bojanova disagree.

Bojanova’s journal, Bitcoin: Benefit or Curse?, questions bitcoin’s security. Their journal

highlights that Mt. Gox, a notable bitcoin exchange in Japan, was hit by a “transaction malleability”

attack. This attack exploited software, which allowed double payouts from the exchange; this

resulted in an estimated $500M loss. Also, the Canadian bitcoin exchange, Flexcoin, also lost $600k in

a similar attack. However, it should be noted that these bitcoin exchanges most likely had weak

software security independent of bitcoin or the blockchain. Exchanging bitcoin does not

automatically mean that there will be software vulnerabilities. There are plenty of other bitcoin

Exchanges that have effectively thwarted attacks such as these.

In Eyal’s article, Majority is not Enough: Bitcoin Mining is Vulnerable , he also argues that

bitcoin does not have the security that it claims to have. Bitcoin cryptocurrency transactions are

public. Its security rests critically on the distributed protocol that maintains the blockchain, run by

participants called miners. Conventional wisdom asserts that the protocol is not incentive-

compatible and is not secure against colluding minority groups. Colluding miners could obtain

revenue larger than their fair share. Collusion can have significant consequences for bitcoin.

Colluding group will increase in size until it becomes a majority. At this point, the bitcoin system

ceases to be a decentralized currency. Selfish mining is feasible for any group size of colluding

miners. There should be a practical modification to the bitcoin protocol that protects against selfish

mining pools. Eyal was effective in highlighting a vulnerability, however, this vulnerability is highly

unlikely and has not been taken advantage of yet, so it remains just a hypothetical. The current

system could be updated before this vulnerability is taken advantage of. On that same note, Bradbury

in his journal, the Problem with Bitcoin, argues that bitcoin’s history has proved it to be anything but

secure. He mentions that the developer’s real name is still unknown. This developer used to interact

with people on developer forums but has since disappeared. Bradbury considers this to be alarming.

He also notes that bitcoin has been affected by previous attacks. All in all, Bradbury argues that

bitcoin still has to evolve more before it will be truly secure. However, the founder does not need to

participate in the system in order for it to be effective; and again, the previous attacks most likely

were related to security issues independent of bitcoin and the blockchain. Considering all of that,

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 9

security isn’t even the main reason that bitcoin is facing so much scrutiny; bitcoin’s major obstacles

are its association with the deep web and its notorious price fluctuations.

Bojanova’s journal, Bitcoin: Benefit or Curse?, and Möser’s journal, An Inquiry into Money

Laundering Tools in the Bitcoin Ecosystem, address the criminal illicit activities associated with

Bitcoin. Bojanova’s journal highlights that bitcoins are used for the sales of illegal goods including:

drugs, weapons, assassinations, money laundering, illegal mining, unlawful gambling, etc. However, it

is important to not that bitcoin is merely a currency. Any currency can be used to purchase such

items so it is ultimately unfair to scorn bitcoin for this. Möser’s journal starts with explaining why

bitcoin attracts criminal activity. While this claim does not stand up to scrutiny, several services

offering increased transaction anonymization have emerged within the bitcoin ecosystem. There are

services that utilize the functionality of Blockchain.info to launder money. This study proceeds to

engineer the process of money laundering via bitcoin to further demonstrate that it can be done.

Although this study proves that money laundering is possible via bitcoin, I would like to highlight

that money laundering is possible via the current system as well. It should be noted that money

laundering is much less common and feasible via bitcoin than it is with the current transaction

alternatives. Möser’s journal also includes information about bitcoin’s notorious price fluctuations.

Again, putting price fluctuation, and bitcoin’s ‘bad’ reputation aside, bitcoin is just a

currency; it is a currency with great potential. Paired with the blockchain system, bitcoins have to the

potential to create a new way to buy and purchase items securely and affordably. This proposal

attempts to answer the question: Do bitcoin and the blockchain, together, provide a secure and

affordable system for financial transactions that is not being widely implemented because of bitcoin’s

‘fluctuating prices’, and because of bitcoin’s infamous reputation?

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 10

III. The Model

Overview: Testing for Price Fluctuations:

bitcoin’s price fluctuations are notorious The bitcoin exchange equivalent of $1 US Dollar has

been at times upward of $1100.00 and at other times lower than $10.00. That does not exactly make

bitcoin seem like a steady resilient currency. However, since 2014, bitcoin’s price has been relatively

stable. It has mostly remained in the realm of 1 Bitcoin exchanging for $400.00. As of today, May 2nd

2016, 1 bitcoin is exchanging for $445.16. I attempted to design a model that quantitatively proves

that bitcoin’s prices have remained relatively stable since 2014.

The model should be interpreted as such: the Independent variable is an observed response

and includes columns for contemporaneous values of observable predictors; the partial regression

coefficients represent the marginal contributions of individual predictors to the variation, when all of

the other predictors are held fixed; and the error term is a catch-all for differences between

predicted and observed values.

The data used for this report was data collected directly from the blockchain public ledger;

the data’s date range is 2014 – Current; 2014 is when bitcoin’s price began to stabilize. This model is

barely not considered perfect collinear. The time series nature of this data makes analysis especially

difficult. If further research were approved, this model would have to be adjusted; different variables

would need to be considered. Maybe ‘Price Volatility’ rather than ‘Price Fluctuations’ would make for

better analysis.

The Model:

• Price = β0 + β1Same + β2TwoDay + β3FiveDay + β4SevenDay + β5TenDay + β6TwentyDay + β7FiftyDay + ϵ

• Data retrieved from: SARL, L. (n.d.). Blockchain.info. Retrieved April 13, 2016.

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 11

Table 1: Definitions of the Variables in the Model

Values are expected to be positive in the short term and negative in the long term. However,

the expected signs are not especially relevant in this model. The amount of change is what is

important; it doesn’t really matter if that change is negative or positive.

Variables: Price: Price is the dependent variable of this model. It represents the average value of bitcoins

traded for the day. The expected sign of this variable is not applicable because it is the dependent

variable.

Same: Same is an independent variable in this model. It represents that prediction that the average

value of bitcoins will be the same as the day before. Its expected sign is positive however this is not

especially relevant; the amount of change is what is important; it doesn’t really matter if that change

is negative or positive.

TwoDay: TwoDay is an independent variable in this model. TwoDay is the average value prediction

of bitcoins traded, in two day intervals. Its expected sign is positive however this is not especially

relevant; the amount of change is what is important; it doesn’t really matter if that change is negative

or positive.

FiveDay: FiveDay is an independent variable in this model. FiveDay is the average value prediction of

bitcoins traded, in five day intervals. Its expected sign is positive however this is not especially

relevant; the amount of change is what is important; it doesn’t really matter if that change is negative

or positive.

SevenDay: SevenDay is an independent variable in this model. SevenDay is the average value

prediction of bitcoins traded, in seven day intervals. Its expected sign is positive however this is not

especially relevant; the amount of change is what is important; it doesn’t really matter if that change

is negative or positive.

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 12

TenDay: TenDay is an independent variable in this model. TenDay is the average value prediction of

bitcoins traded, in ten day intervals. Its expected sign is negative however this is not especially

relevant; the amount of change is what is important; it doesn’t really matter if that change is negative

or positive.

TwentyDay: TwentyDay is an independent variable in this model. TwentyDay is the average value

prediction of bitcoins traded, in twenty day intervals. Its expected sign is negative however this is not

especially relevant; the amount of change is what is important; it doesn’t really matter if that change

is negative or positive.

FiftyDay: FiftyDay is an independent variable in this model. FiftyDay is the average value prediction

of bitcoins traded, in fifty day intervals. Its expected sign is negative however this is not especially

relevant; the amount of change is what is important; it doesn’t really matter if that change is negative

or positive.

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 13

IV. Descriptive Statistics

Table 2: Descriptive Statistics of the Model

All values are in the same ballpark. It does not matter if you are measuring changes in two

day intervals or if measuring in changes in fifty day intervals, the change is pretty consistent. Prices

are not fluctuating very much.

Variables: Price: Price is the dependent variable of this model. It represents the average value of bitcoins

traded for the day. Its mean is 379.4471, its standard deviation is 198.0156, its minimum is 69.05

and its maximum is 1132.26.

Same: Same is an independent variable in this model. It represents that prediction that the average

value of bitcoins will be the same as the day before. Its mean is 379.1147, its standard deviation is

198.1887 its minimum is 69.05 and its maximum is 1132.26.

TwoDay: TwoDay is an independent variable in this model. TwoDay is the average value prediction

of bitcoins traded, in two day intervals. Its mean is 379.4512, its standard deviation is 201.0037, its

minimum is 63.74 and its maximum is 1191.69.

FiveDay: FiveDay is an independent variable in this model. FiveDay is the average value prediction of

bitcoins traded, in five day intervals. Its mean is 379.4185 its standard deviation is 199.8558, its

minimum is 62.703 and its maximum is 1213.178.

SevenDay: SevenDay is an independent variable in this model. SevenDay is the average value

prediction of bitcoins traded, in seven day intervals. Its mean is 379.4032, its standard deviation is

200.055, its minimum is 63.07714 and its maximum is 1200.221.

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 14

TenDay: TenDay is an independent variable in this model. TenDay is the average value prediction of

bitcoins traded, in ten day intervals Its mean is 379.3849, its standard deviation is 200.824, its

minimum is 64.52133 and its maximum is 1170.293.

TwentyDay: TwentyDay is an independent variable in this model. TwentyDay is the average value

prediction of bitcoins traded, in twenty day intervals. Its mean is 379.3221, its standard deviation is

203.9141, its minimum is 67.29632 and its maximum is 1207.714.

FiftyDay: FiftyDay is an independent variable in this model. FiftyDay is the average value prediction

of bitcoins traded, in fifty day intervals. Its mean is 379.3022, its standard deviation is 209.0119, its

minimum is 75.55033 and its maximum is 1123.617.

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 15

V. Empirical Results: Table 3: Regression Results of the Model

The partial regression coefficients represent small marginal contributions of individual

predictions of variation. There is not much change in variation over time, even when measuring with

different time intervals. TwoDay and FiftyDay are the variables that are most significant. The number

of observations used in this model could be higher in order to get more accurate results. The R-

squared is also alarmingly high. Issues aside, the results of this model conclude that prices have

remained relatively stable since 2014.

Variables: Price: Price is the dependent variable of this model. It represents the average value of bitcoins

traded for the day. Its coefficient is 4.115187, its standard error is 1.658349, its P-Value is 0.00, and

its sign is not applicable. This is a significant variable.

Same: Same is an independent variable in this model. It represents that prediction that the average

value of bitcoins will be the same as the day before. Its coefficient is 0.7820214, its standard error is

0.1161428, its P-Value is 0.572, and its sign is positive. This is not a significant variable.

TwoDay: TwoDay is an independent variable in this model. TwoDay is the average value prediction

of bitcoins traded, in two day intervals. Its coefficient is 0.0343532, its standard error is 0.0608178,

its P-Value is 0.015, and its sign is positive. This is a significant variable.

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 16

FiveDay: FiveDay is an independent variable in this model. FiveDay is the average value prediction of

bitcoins traded, in five day intervals. Its coefficient is -0.1807502, its standard error is 0.0740712, its

P-Value is 0.00, and its sign is negative. This is a significant variable.

SevenDay: SevenDay is an independent variable in this model. SevenDay is the average value

prediction of bitcoins traded, in seven day intervals. Its coefficient is 0.4413013, its standard error is

0.0785681, its P-Value is 0.012 and its sign is positive. This is a significant variable.

TenDay: TenDay is an independent variable in this model. TenDay is the average value prediction of

bitcoins traded, in ten day intervals. Its coefficient is -0.1634128, its standard error is 0.0646604, its

P-Value is 0.022, and its sign is negative. This is a significant variable.

TwentyDay: TwentyDay is an independent variable in this model. TwentyDay is the average value

prediction of bitcoins traded, in twenty day intervals. Its coefficient is 0.0766486, its standard error

is 0.0333536, its P-Value is 0.987, and its sign is positive. This is not a significant variable.

FiftyDay: FiftyDay is an independent variable in this model. FiftyDay is the average value prediction

of bitcoins traded, in fifty day intervals. Its coefficient is -0.0002836, its standard error is 0.0169855,

its P-Value is -0.013, and its sign is negative. This is a significant variable.

Table 4: Regression Results of the Model (in Log Form)

The log transformations of variables can be used to make skewed distributions less skewed.

This is valuable because it makes patterns in the data more interpretable and it helps to meet the

assumptions of inferential statistics. In this case, the distributions did become less skewed. Most

notably: Same is not significant, however, LSame is significant. FiveDay is significant, however,

LFiveDay is not significant. Both TwentyDay and LTwentyDay are not significant.

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 17

Variables (in Log Form): LPrice: Price is the dependent variable of this model. It represents the average value of bitcoins

traded for the day. Its log coefficient is 0.0241, its standard error is 0.0136, its P-Value is 0.078, and

its sign is not applicable. This is a significant variable.

LSame: Log of Same is an independent variable in this model. It represents that prediction that the

average value of bitcoins will be the same as the day before. Its coefficient is 1.39, its standard error

is 0.19, its P-Value is 0.00, and its sign is positive. This is a significant variable.

LTwoDay: Log of TwoDay is an independent variable in this model. TwoDay is the average value

prediction of bitcoins traded, in two day intervals. Its coefficient is -0.96, its standard error is 0.052,

its P-Value is 0.065, and its sign is negative. This is a significant variable.

LFiveDay: Log of FiveDay is an independent variable in this model. FiveDay is the average value

prediction of bitcoins traded, in five day intervals. Its coefficient is -0.02633, its standard error is

0.1129, its P-Value is 0.818, and its sign is negative. This is a not significant variable.

LSevenDay: Log of SevenDay is an independent variable in this model. SevenDay is the average value

prediction of bitcoins traded, in seven day intervals. Its coefficient is 0.1967, its standard error is

0.0855, its P-Value is 0.684 and its sign is positive. This is a significant variable.

LTenDay: Log of TenDay is an independent variable in this model. TenDay is the average value

prediction of bitcoins traded, in ten day intervals. Its coefficient is -0.1845, its standard error is

0.0618, its P-Value is 0.003, and its sign is negative. This is a significant variable.

LTwentyDay: Log of TwentyDay is an independent variable in this model. TwentyDay is the average

value prediction of bitcoins traded, in twenty day intervals. Its coefficient is -0.0317, its standard

error is 0.0337, its P-Value is 0.684, and its sign is negative. This is not a significant variable.

LFiftyDay: Log of FiftyDay is an independent variable in this model. FiftyDay is the average value

prediction of bitcoins traded, in fifty day intervals. Its coefficient is -0.0547, its standard error is

0.0201, its P-Value is -0.007, and its sign is negative. This is a significant variable.

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 18

Figure 1: Bitcoin Price Volatility Time Series

‘

This is a price volatility time series line graph. It visually displays how bitcoin’s prices in the

beginning, in 2009, were very unstable. In 2014, bitcoin’s price began to stabilize,

Figure 2: Bitcoin to US Dollar Exchange Rate in May 2016

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 19

The Bitcoin to US Dollar exchange rate was 1 Bitcoin roughly $458.50 US Dollars in May of

2016; this represents the price value of a Bitcoin as of May 2nd 2016. Until June of 2016, Bitcoin has

been in the $400 to $1 US dollar range until since 2014.

Figure 3: Bitcoin to US Dollar Exchange Rate in June 2016 (Includes Brexit Break)

In June of 2016, Bitcoin experienced its first major spike in two years due to speculation

regarding Brexit, the United Kingdom leaving the European Union. Considering, all of the major

currencies had major shifts de to Brexit, it is still fair to say that bitcoin’s price is stable.

Figure 4: US Dollar to Euro Exchange Rate in June 2016 (Includes Brexit Break)

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 20

Figure 5: Euro to US Dollar Exchange Rate in June 2016 (Includes Brexit Break)

Figure 6: British Pound to US Dollar Exchange Rate in June 2016 (Includes Brexit Break)

Upon first glance, the bitcoin price fluctuation graph looks more unstable than the US, Dollar,

the Euro, and the British Pound price fluctuation graphs. However, volume needs to be accounted for.

There are simply a lot more US dollars out there than there are bitcoins. Even at the peak of the most

recent bubble, the total value of bitcoins was less than $3 billion. Whereas the US dollar supply is

nearly $10 trillion. Considering bitcoin’s low volume, it has proved to be as stable as any of the other

major currencies. It is not wild to say that bitcoin has the possibility of becoming even more stable

than the US dollar, the global currency. If this becomes the case, it is safe to say that there will be an

increase in demand for bitcoin investments.

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 21

Unit Root Tests: Augmented Dickey Fuller & Phillips-Perron

Cointegration has become a valuable property in modern time series analysis. Time series

often have trends; trends that are either deterministic or stochastic. To account for this, unit root

tests must be performed. In this report, the Dickey-Fuller Test and the Phillips-Perron Test will be

used.

Table 5: Augmented Dickey-Fuller Results:

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 22

*These results are in levels

The Dickey-Fuller test tests if the null hypothesis of a unit root can be rejected. In other

words, it tests to see if the model is stationary. In this case, the variables prove to be stationary. The

residuals are negative and relatively close to zero.

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 23

Table 6: Phillips-Perron Results:

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 24

The Phillips-Perron test is used in time series analysis to test if the null hypothesis is

integrated of order 1. It adds to the Dickey-Fuller test by testing if the process for generating the data

might have had a higher order of autocorrelation. To account for autocorrelation, the Phillips-Perron

test makes a non-parametric correction to the test statistic. In this case, there were very minimal

adjustments.

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 25

VI. Conclusion: Bitcoin is both a digital asset and a payment system. In 2008, bitcoins were first published

and developed by the allusive Satoshi Nakamoto. This new system does not require a financial

intermediary; in other words, it is peer-to- peer. The transactions are verified by network nodes and

then recorded in a ledger, the blockchain. The blockchain uses bitcoins as its unit of account. This

system does require a central repository or an administrator. With that being said, bitcoin is the very

first decentralized digital currency and is considered the first successful cryptocurrency.

Putting bank opposition, price fluctuations, and bitcoin’s ‘bad’ reputation aside, Bitcoin is

just a currency; it is a currency with great potential. Paired with the blockchain system, bitcoins have

to the potential to create a new way to buy and purchase items securely and affordably. This report

attempted to answer the question: Do bitcoin and the Blockchain, together, provide a secure and

affordable system for financial transactions that is not being widely implemented because of bitcoin’s

‘fluctuating prices’, and because of bitcoin’s infamous reputation? Mainly, this report focused on

bitcoin’s fluctuating prices because they are much more testable than bitcoin’s reputation.

Putting the potential issues with the model used aside, the descriptive statistics and

empirical results of the model conclude that bitcoin’s prices have stabilized since 2014.

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 26

VII. References

• Andrychowicz, M. "Secure Multiparty Computations on Bitcoin." University of

Warsaw, May 2014. Web. Apr. 2016.

• Bojanova, Irena. "Bitcoin: Benefit or Curse?" IEEE Xplore. IEEE Computer

Society, May-June 2014. Web. Apr. 2016.

• Bonneau, J. "Research Perspectives and Challenges for Bitcoin

Cryptocurrencies." N.p., May 2015. Web. Apr. 2016.

• Bradbury, Danny. "The Problem with Bitcoin." N.p., n.d. Web. Apr. 2016.

• CARL, L. Blockchain.info. Retrieved April 13, 2016.

• Eyal, Ittay. "Majority Is Not Enough: Bitcoin Mining Is Vulnerable." N.p., Nov.

2013. Web. Apr. 2016.

• Hurlburt, George. "Might the Blockchain Outlive Bitcoin?" IEEE Xplore. IEEE

Computer Society, Mar.-Apr. 2016. Web. Apr. 2016.

• Kraft, D. Difficulty control for blockchain-based consensus systems. April 15,

2015.Retrieved April 13, 2016.

• Melin, Mark. "Nasdaq Adopts Bitcoin Blockchain Technology." Newstex

Global Business, May 2015. Web. Apr. 2016.

• Möser, M. "An Inquiry into Money Laundering Tools in the Bitcoin

Ecosystem." Univ. of Munster, n.d. Web. Apr. 2016.

• Newstex. "Banks Using the Bitcoin Blockchain Is like Putting a Bird in a

Cage." Newstex Finance and Accounting, Oct. 2014. Web. Apr. 2016.

• Singh, P. Performance Comparison of Executing Fast Transactions in Bitcoin

Network Using Verifiable Code Execution. 2013. Retrieved April 13, 2016

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 27

VIII. Appendix

delta: 1 day

time variable: date, 4/22/2013 to 3/3/2016, but with gaps

. tsset date, daily

lin50 1,032 379.3022 209.0119 75.55033 1123.617

lin20 1,032 379.3221 203.9141 67.29632 1207.714

lin10 1,032 379.3849 200.824 64.52133 1170.293

lin7 1,032 379.4032 200.055 63.07714 1200.221

lin5 1,032 379.4185 199.8558 62.703 1213.178

lin2 1,032 379.4512 201.0037 63.74 1191.69

same 1,032 379.1147 198.1887 69.05 1132.26

actual 1,032 379.4471 198.0156 69.05 1132.26

Variable Obs Mean Std. Dev. Min Max

. sum actual same lin2 lin5 lin7 lin10 lin20 lin50

_cons 4.115187 1.658349 2.48 0.013 .8610355 7.369338

lin50 -.0002863 .0169855 -0.02 0.987 -.0336167 .0330441

lin20 .0766486 .0333536 2.30 0.022 .0111993 .1420979

lin10 -.1634128 .0646604 -2.53 0.012 -.2902948 -.0365308

lin7 .4413013 .0785681 5.62 0.000 .2871284 .5954741

lin5 -.1807502 .0740712 -2.44 0.015 -.3260989 -.0354015

lin2 .0343532 .0608178 0.56 0.572 -.0849886 .153695

same .7820214 .1661428 4.71 0.000 .4560021 1.108041

actual Coef. Std. Err. t P>|t| [95% Conf. Interval]

Total 40425682.7 1,031 39210.1675 Root MSE = 23.987

Adj R-squared = 0.9853

Residual 589193.579 1,024 575.384354 R-squared = 0.9854

Model 39836489.1 7 5690927.01 Prob > F = 0.0000

F(7, 1024) = 9890.65

Source SS df MS Number of obs = 1,032

. regress actual same lin2 lin5 lin7 lin10 lin20 lin50

lin50 0.9431 1.0000

actual 1.0000

actual lin50

(obs=1,032)

. corr actual lin50

same 0.9924 1.0000

actual 1.0000

actual same

(obs=1,032)

. corr actual same

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 28

55. 6/15/2013 100.79 100.24

54. 6/14/2013 100.24 101.33

53. 6/13/2013 101.33 101.46

52. 6/12/2013 101.46 104.48

51. 6/11/2013 104.48 100.15

50. 6/10/2013 100.15 97.5

49. 6/9/2013 97.5 96.84

48. 6/8/2013 96.84 92.72

47. 6/7/2013 92.72 93.13

46. 6/6/2013 93.13 93.4

45. 6/5/2013 93.4 91.07

44. 6/4/2013 91.07 90.9

43. 6/3/2013 90.9 88.33

42. 6/2/2013 88.33 87.78

41. 6/1/2013 87.78 89.09

40. 5/31/2013 89.09 89.65

39. 5/30/2013 89.65 88.31

38. 5/29/2013 88.31 95.32

37. 5/28/2013 95.32 95.2

36. 5/27/2013 95.2 96.51

35. 5/26/2013 96.51 93.97

34. 5/25/2013 93.97 91.8

33. 5/24/2013 91.8 95.07

32. 5/23/2013 95.07 86.41

31. 5/22/2013 86.41 81.09

30. 5/21/2013 81.09 74.49

29. 5/20/2013 74.49 76

28. 5/19/2013 76 70.26

27. 5/18/2013 70.26 69.05

26. 5/17/2013 69.05 70.82

25. 5/16/2013 70.82 77.9

24. 5/15/2013 77.9 82.75

23. 5/14/2013 82.75 88.13

22. 5/13/2013 88.13 89.03

21. 5/12/2013 89.03 94.26

20. 5/11/2013 94.26 95.08

19. 5/10/2013 95.08 95.06

18. 5/9/2013 95.06 100.59

17. 5/8/2013 100.59 102.27

16. 5/7/2013 102.27 103.65

15. 5/6/2013 103.65 101.35

14. 5/5/2013 101.35 104.93

13. 5/4/2013 104.93 105.02

12. 5/3/2013 105.02 108.13

11. 5/2/2013 108.13 110.04

10. 5/1/2013 110.04 106.95

9. 4/30/2013 106.95 106.87

8. 4/29/2013 106.87 100.72

7. 4/28/2013 100.72 99.92

6. 4/27/2013 99.92 100.38

5. 4/26/2013 100.38 100.54

4. 4/25/2013 100.54 105.08

3. 4/24/2013 105.08 108.85

2. 4/23/2013 108.85 106.83

1. 4/22/2013 106.83 104.68

date actual same

. list date actual same

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 29

name: <unnamed>

log: d:\bitcoin.log

log type: text

opened on: 17 Jul 2016, 09:39:58

. insheet using d:\bitcoin.txt

(11 vars, 1032 obs)

. save d:\bitcoin, replace

file d:\bitcoin.dta saved

.

. gen daily=date(day, "MDY")

. sum actual same lin2 lin3 lin4 lin5 lin7 lin10 lin20 lin50

Variable | Obs Mean Std. Dev. Min Max

-------------+--------------------------------------------------------

actual | 1032 379.4471 198.0156 69.05 1132.26

same | 1032 379.1147 198.1887 69.05 1132.26

lin2 | 1032 379.4512 201.0037 63.74 1191.69

lin3 | 1032 379.44 200.1871 63.74 1214.95

lin4 | 1032 379.4295 199.9485 63.085 1211.7

-------------+--------------------------------------------------------

lin5 | 1032 379.4185 199.8558 62.703 1213.178

lin7 | 1032 379.4032 200.055 63.07714 1200.221

lin10 | 1032 379.3849 200.824 64.52133 1170.293

lin20 | 1032 379.3221 203.9141 67.29632 1207.714

lin50 | 1032 379.3022 209.0119 75.55033 1123.617

.

. gen lactual=ln(actual)

. gen lsame=ln(same)

. gen llin2=ln(lin2)

. gen llin3=ln(lin3)

. gen llin4=ln(lin4)

. gen llin5=ln(lin5)

. gen llin7=ln(lin7)

. gen llin10=ln(lin10)

. gen llin20=ln(lin20)

. gen llin50=ln(lin50)

.

. tsset daily

time variable: daily, 19470 to 20516, but with gaps

delta: 1 unit

. ** Here I am ussing the Augmented Dickey-Fuller unit root test; the variable

. ** are in levels

. dfuller lactual

Dickey-Fuller test for unit root Number of obs = 1017

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 30

Statistic Value Value Value

------------------------------------------------------------------------------

Z(t) -1.690 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.4363

. dfuller lsame

Dickey-Fuller test for unit root Number of obs = 1017

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(t) -1.800 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.3806

. dfuller llin2

Dickey-Fuller test for unit root Number of obs = 1017

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(t) -3.084 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.0277

. dfuller llin3

Dickey-Fuller test for unit root Number of obs = 1017

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(t) -2.331 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.1621

. dfuller llin4

Dickey-Fuller test for unit root Number of obs = 1017

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(t) -2.120 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.2367

. dfuller llin5

Dickey-Fuller test for unit root Number of obs = 1017

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(t) -1.989 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.2915

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 31

. dfuller llin7

Dickey-Fuller test for unit root Number of obs = 1017

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(t) -1.931 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.3177

. dfuller llin10

Dickey-Fuller test for unit root Number of obs = 1017

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(t) -1.808 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.3765

. dfuller llin20

Dickey-Fuller test for unit root Number of obs = 1017

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(t) -1.887 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.3382

. dfuller llin50

Dickey-Fuller test for unit root Number of obs = 1017

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(t) -2.119 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.2369

.

. ** Here I am ussing the Augmented Dickey-Fuller unit root test; the variable

. ** are in first difference form

.

. dfuller d.lactual

Dickey-Fuller test for unit root Number of obs = 1004

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(t) -30.739 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.0000

. dfuller d.lsame

Dickey-Fuller test for unit root Number of obs = 1004

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 32

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(t) -32.944 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.0000

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 33

. dfuller d.llin2

Dickey-Fuller test for unit root Number of obs = 1004

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(t) -49.819 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.0000

. dfuller d.llin3

Dickey-Fuller test for unit root Number of obs = 1004

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(t) -30.847 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.0000

. dfuller d.llin4

Dickey-Fuller test for unit root Number of obs = 1004

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(t) -23.967 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.0000

. dfuller d.llin5

Dickey-Fuller test for unit root Number of obs = 1004

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(t) -20.377 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.0000

. dfuller d.llin7

Dickey-Fuller test for unit root Number of obs = 1004

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(t) -16.368 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.0000

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 34

. dfuller d.llin10

Dickey-Fuller test for unit root Number of obs = 1004

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(t) -13.541 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.0000

. dfuller d.llin20

Dickey-Fuller test for unit root Number of obs = 1004

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(t) -9.092 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.0000

. dfuller d.llin50

Dickey-Fuller test for unit root Number of obs = 1004

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(t) -5.100 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.0000

.

. ** Here I am ussing the Phillips-Perron unit root test; the variable

. ** are in levels

. pperron lactual

Phillips-Perron test for unit root Number of obs = 1017

Newey-West lags = 6

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(rho) -4.292 -20.700 -14.100 -11.300

Z(t) -1.734 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.4138

. pperron lsame

Phillips-Perron test for unit root Number of obs = 1017

Newey-West lags = 6

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(rho) -4.501 -20.700 -14.100 -11.300

Z(t) -1.824 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.3684

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 35

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 36

. pperron llin2

Phillips-Perron test for unit root Number of obs = 1017

Newey-West lags = 6

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(rho) -6.891 -20.700 -14.100 -11.300

Z(t) -1.994 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.2894

. pperron llin3

Phillips-Perron test for unit root Number of obs = 1017

Newey-West lags = 6

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(rho) -6.210 -20.700 -14.100 -11.300

Z(t) -2.064 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.2592

. pperron llin4

Phillips-Perron test for unit root Number of obs = 1017

Newey-West lags = 6

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(rho) -6.177 -20.700 -14.100 -11.300

Z(t) -2.112 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.2399

. pperron llin5

Phillips-Perron test for unit root Number of obs = 1017

Newey-West lags = 6

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(rho) -6.039 -20.700 -14.100 -11.300

Z(t) -2.094 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.2471

. pperron llin7

Phillips-Perron test for unit root Number of obs = 1017

Newey-West lags = 6

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(rho) -6.103 -20.700 -14.100 -11.300

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 37

Z(t) -2.096 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.2463

. pperron llin10

Phillips-Perron test for unit root Number of obs = 1017

Newey-West lags = 6

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(rho) -5.893 -20.700 -14.100 -11.300

Z(t) -2.014 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.2805

. pperron llin20

Phillips-Perron test for unit root Number of obs = 1017

Newey-West lags = 6

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(rho) -4.765 -20.700 -14.100 -11.300

Z(t) -1.862 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.3502

. pperron llin50

Phillips-Perron test for unit root Number of obs = 1017

Newey-West lags = 6

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(rho) -3.147 -20.700 -14.100 -11.300

Z(t) -1.648 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.4582

.

. ** Here I am ussing the Phillips-Perron unit root test; the variable

. ** are in difference form

. pperron d.lactual

Phillips-Perron test for unit root Number of obs = 1004

Newey-West lags = 6

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(rho) -1014.997 -20.700 -14.100 -11.300

Z(t) -30.800 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.0000

. pperron d.lsame

Phillips-Perron test for unit root Number of obs = 1004

Newey-West lags = 6

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 38

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

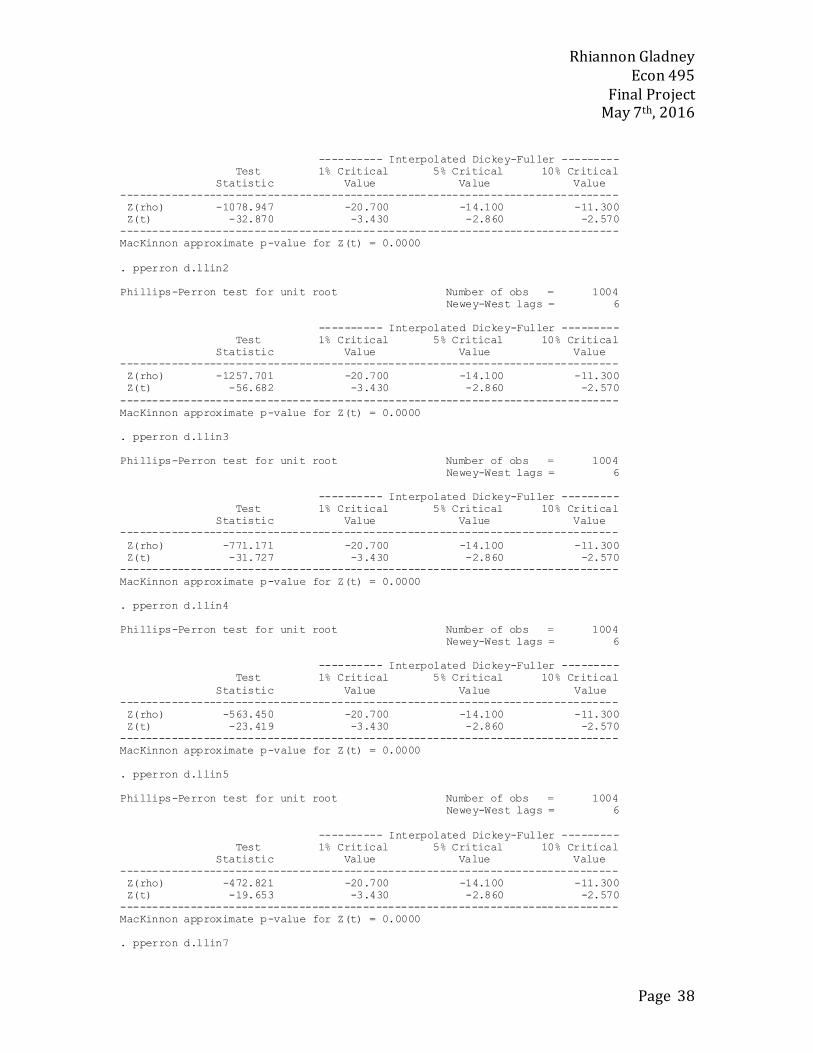

Z(rho) -1078.947 -20.700 -14.100 -11.300

Z(t) -32.870 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.0000

. pperron d.llin2

Phillips-Perron test for unit root Number of obs = 1004

Newey-West lags = 6

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(rho) -1257.701 -20.700 -14.100 -11.300

Z(t) -56.682 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.0000

. pperron d.llin3

Phillips-Perron test for unit root Number of obs = 1004

Newey-West lags = 6

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(rho) -771.171 -20.700 -14.100 -11.300

Z(t) -31.727 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.0000

. pperron d.llin4

Phillips-Perron test for unit root Number of obs = 1004

Newey-West lags = 6

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(rho) -563.450 -20.700 -14.100 -11.300

Z(t) -23.419 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.0000

. pperron d.llin5

Phillips-Perron test for unit root Number of obs = 1004

Newey-West lags = 6

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(rho) -472.821 -20.700 -14.100 -11.300

Z(t) -19.653 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.0000

. pperron d.llin7

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 39

Phillips-Perron test for unit root Number of obs = 1004

Newey-West lags = 6

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(rho) -369.324 -20.700 -14.100 -11.300

Z(t) -16.074 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.0000

. pperron d.llin10

Phillips-Perron test for unit root Number of obs = 1004

Newey-West lags = 6

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(rho) -312.008 -20.700 -14.100 -11.300

Z(t) -14.189 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.0000

. pperron d.llin20

Phillips-Perron test for unit root Number of obs = 1004

Newey-West lags = 6

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(rho) -154.082 -20.700 -14.100 -11.300

Z(t) -9.671 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.0000

. pperron d.llin50

Phillips-Perron test for unit root Number of obs = 1004

Newey-West lags = 6

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(rho) -44.183 -20.700 -14.100 -11.300

Z(t) -5.089 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.0000

.

. *** Here, I am estimating the log model

. reg lactual lsame llin2 llin3 llin4 llin5 llin7 llin10 llin20 llin50

Source | SS df MS Number of obs = 1032

-------------+------------------------------ F( 9, 1022) =20488.62

Model | 326.400119 9 36.2666798 Prob > F = 0.0000

Residual | 1.80903092 1022 .001770089 R-squared = 0.9945

-------------+------------------------------ Adj R-squared = 0.9944

Total | 328.209149 1031 .318340591 Root MSE = .04207

------------------------------------------------------------------------------

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 40

lactual | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

lsame | 1.398184 .1901512 7.35 0.000 1.025052 1.771315

llin2 | -.0960467 .0520253 -1.85 0.065 -.1981353 .0060419

llin3 | -.0416818 .0776889 -0.54 0.592 -.1941298 .1107661

llin4 | -.1820073 .1129358 -1.61 0.107 -.4036198 .0396051

llin5 | -.0263324 .1112416 -0.24 0.813 -.2446204 .1919556

llin7 | .1967558 .0855109 2.30 0.022 .0289589 .3645528

llin10 | -.1845026 .0618545 -2.98 0.003 -.305879 -.0631262

llin20 | -.0137035 .0337125 -0.41 0.684 -.0798571 .0524501

llin50 | -.0547127 .0201055 -2.72 0.007 -.0941654 -.0152599

_cons | .0241007 .0136436 1.77 0.078 -.0026719 .0508733

------------------------------------------------------------------------------

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 41

.

. *** The step below helps us testing for cointegration test using the Engel test

. predict e, resid

. dfuller e

Dickey-Fuller test for unit root Number of obs = 1017

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(t) -31.766 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.0000

. pperron e

Phillips-Perron test for unit root Number of obs = 1017

Newey-West lags = 6

---------- Interpolated Dickey-Fuller ---------

Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value

------------------------------------------------------------------------------

Z(rho) -1054.850 -20.700 -14.100 -11.300

Z(t) -31.791 -3.430 -2.860 -2.570

------------------------------------------------------------------------------

MacKinnon approximate p-value for Z(t) = 0.0000

.

. ***Rhiannon mentioned a recent schock in Bitcoin value. We could test that

. *** by introducing Breaks in the analysis

.

. log close

name: <unnamed>

log: d:\bitcoin.log

log type: text

closed on: 17 Jul 2016, 09:39:58

Rhiannon Gladney Econ 495

Final Project May 7th, 2016

Page 42