understanding & drafting irrevocable trusts presented by: wealthcounsel, llc bill conway

TRANSCRIPT

Understanding & Drafting Irrevocable Trusts

Presented By:

WealthCounsel, LLC

Bill Conway www.wealthcounsel.com

Good Morning!

Introductions Name? From? Practice experience? Hobbies/Interests? Why EP 203?

Good Morning!

EP 203 significantly overhauled Overview

WealthDocx IRT Module Insurance-Related IRT Issues Sale Transactions with Defective IRTs Asset Protection & Self-Settled Trusts Split-Interest Trusts

WealthDocx IRT Module

Bill Conwaywww.wealthcounsel.com

WealthDocx IRT Module

Irrevocable Trusts Generally

Gifts are completed Trust assets are removed from estate Grantor trust?

Maybe Maybe not

Selecting the Type of IRT (Page 4)

Selecting the Type of IRT (Page 4)

2503(c) Trust FBO Minor Outright at 21 Included in estate Alternative to UGMA/UTMA

Asset Protection Self-Settled Trust Delaware Distribution advisor suggested

Selecting the Type of IRT (Page 5)

Family Bank Trust / BERT Trust Inter Vivos Bypass Trust

Gifting Trust Receptacle for lifetime gifts

HEET Trust Health and Education Exclusion Trust Appropriate where no GST exemption left

Intentionally Defective Grantor Trust Grantor trust set to yes Warning re: Crummey

Selecting the Type of IRT (Page 5)

Inheritor’s Trust Settled by non-beneficiary Only one beneficiary allowed

Life Insurance Trust (Single) Doesn’t ask if insurance is appropriate

investment Life Insurance (2nd to Die)

Crummey rights automatically included

Other IRTs in WealthDocx

Charitable Trusts CRTs, CLTs, Foundations

Split-Interest Trusts GRATs, QPRTs, QTIPs (Later)

Special Needs Trusts (3rd Party) Retirement Trusts

Grantor as Trustee (Page 6)

Maybe, but why?

Distribution Adviser/Trustee (Page 7)

Personal touch

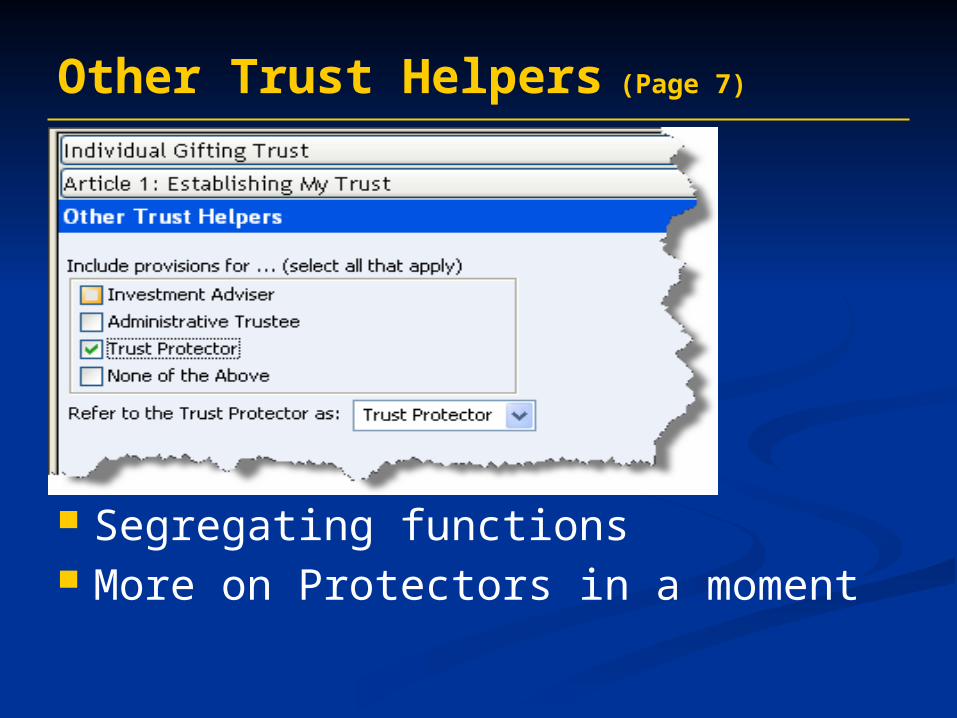

Other Trust Helpers (Page 7)

Segregating functions More on Protectors in a moment

UTC Provisions (Page 8)

Be familiar with your state law! Affects accountings, notice, etc.

Crummey Withdrawal Rights (Page 8)

Crummey Withdrawal Rights (Page 8)

Annual Gift Tax Exclusion Saves $5 million lifetime credit Future Interest Rule Crummey Solution

Gifting to Irrevocable Trust

Crummey Solution (Page 9)

No notice required or given Tax Court - withdrawal rights were illusory 9th Circuit reversed – present interest as long

as the withdrawal right is enforceable IRS acquiesced in Rev Rul 81-7; Reasonable

notice required

Crummey Issues

Minor Beneficiaries (Page 9)

Guardian may exercise Should not be donor/parent

Inconsistent positions by IRS WD precludes donor/parent from exercising

Non-guardian nominee??

Crummey Issues

Grantor’s Control Over Withdrawal Rights (Page 10)

WD defaults Withdrawal rights exist Pro rata among all benes

Invert defaults?

Crummey Issues

Contingent Beneficiaries (Page 12)

Cristofani (Tax Court)

2 children as current benes 5 grandchildren as contingent benes Tax Ct said no vested interest required

Crummey Issues

Contingent Beneficiaries (Page 12)

Cristofani (Tax Court)

Kholsaat (Tax Court)

16 contingent benes No withdrawal rights exercised IRS argued implicit understanding Tax Court said no evidence of an understanding

and none would be inferred

Crummey Issues

Contingent Beneficiaries (Page 13)

Cristofani (Tax Court)

Kholsaat (Tax Court)

Holland (Tax Court)

Family meeting to discuss not exercising IRS argued implicit understanding Tax Court said meeting evidenced knowledge of

rights and conscious decision not to exercise

Crummey Issues

Notice of Withdrawal Right (Page 13)

Oral vs. Written

Crummey Issues

Notice of Withdrawal Right (Page 14)

Oral vs. Written Frequency

“Current” notice Schedule of contributions sufficient WD requires notice upon each contribution

Crummey Issues

Notice of Withdrawal Right (Page 14)

Oral vs. Written Frequency Duration

Reasonable period of time Cristofani was 15 days 4 days has been approved; 3 days disapproved ETIP if spouse has withdrawal right

Crummey Issues

Notice of Withdrawal Right (Page 16)

Oral vs. Written Frequency Duration Accuracy Waiver

Crummey Issues

Maintaining Sufficient Assets (Page 16)

Satisfy from other trust assets Distribute fractional portion of policy (if

applicable) WD provides for grant of line of credit from

grantor

Crummey Issues

Estate Tax Treatment (Page 16)

Withdrawal Right = GPOA GPOA included in power holder’s estate

Gift-Over Problem (Page 17)

Lapse of Withdrawal Right IRC 2514 (vs. 2503) Lapse over 5/5 = Release Release = transfer to other beneficiaries (if

any) Transfer is of a future interest

Gift-Over Problem

Gift-Over Solutions (Page 18)

Limit withdrawal right to 5/5 Separate trusts Common trust with hanging powers Contribute assets so that 5/5 = $12,000 Loans in lieu of contributions

Gift-Over Problem

Gift-Over Solutions

Common Trust (Page 19)

Limits withdrawal right to 5/5 No lapse greater than 5/5 Donee has to aggregate gifts for 5/5

Gift-Over Solutions

Common Trust (Page 19)

Annual Premium:$5,000

Beneficiaries:2-Son & Daughter

Dad Mom$2,500 $2,500

$5,000

2514(e) lapse of $2,500 each

(no gift)

No Giftover Problem

Gift-Over Solutions

Common Trust (Page 19)

Beneficiaries:2-Son & Daughter

Dad Mom$26,000 $26,000

$52,000

2514(e) lapse of $5,000 each

(no gift)

Deemed gift of $21,000 from

each beneficiary to the other

Annual Premium:$52,000

Gift-Over Solutions

Separate Subtrusts (Page 19)

Allows for full utilization of annual exclusion Lapse in excess of 5/5 gifts over to no one Beneficiary becomes grantor for GST

purposes over released portion Separate accounts must be funded

Gift-Over Solutions

Separate Subtrusts (Page 19)

Annual Premium:$52,000

Beneficiaries:2-Son & Daughter

$26,000

$52,000

No Giftover because no other beneficiaries to

whom to gift over

Dad Mom$26,000

Lapse to Separate Trust for Son of

$26,000

Lapse to Separate Trust for Daughter of

$26,000

Gift-Over Solutions

Hanging Powers (Page 21)

Allows for full utilization of annual exclusion Amounts in excess of 5/5 continue to be

withdrawable Estate inclusion in event power holder

predeceases Best of both worlds

Gift-Over Solutions

Hanging Powers (Page 21)Annual Premium:

$52,000

Beneficiaries:2-Son & Daughter

Dad Mom$26,000 $26,000

$52,000

2514(e) lapse of $5,000 each

(no gift)

Remaining $42,000 continues to “hang,”

therefore no gift over

Gift-Over Solutions

Hanging Powers (Page 21)

Beneficiaries:2-Son & Daughter

$26,000

$260,000

Balance of $177,200 “hangs”

Year 5:Aggregate

Contributions of $260,000

Dad Mom$26,000

Year 1 $10,000 lapseYear 2 $10,400 lapseYear 3 $15,600 lapseYear 4 $20,800 lapseYear 5 $26,000 lapse

Incomplete Gifts (Page 23)

“dominion and control” retained But can’t get it back

Grantor Trust Provisions (Page 23)

Grantor Trust Provisions (Page 23)

Overview & History IRC 671-679 Created to eliminate income tax abuses

involving (then-lower) trusts brackets Grantor trust as to:

Income Principal Both

Grantor Trust Opportunities (Page 24)

Tax free sale of appreciated assets Tax burn as non-taxable contributions Removal of assets from estate Tax free distribution to trust beneficiaries Permissible transferee of life insurance

policy outside of transfer for value rules

Achieving Grantor Trust Status

672 Definitions (Page 24)

Adverse = beneficial interest that is substantial and whose interest is adversely affected by exercise or nonexercise

Nonadverse = Not adverse Related or Subordinate = Nonadverse +

parent/issue/sibling/employee/corp Spousal Attribution

Achieving Grantor Trust Status

672 Definitions (Page 24)

Adverse = beneficial interest that is substantial and whose interest is adversely affected by exercise or nonexercise

Nonadverse = Not adverse Related or Subordinate = Nonadverse +

parent/issue/sibling/employee/corp Spousal Attribution

Achieving Grantor Trust Status

Know your defect One vs. More than One

Certainty Ease of Toggling

Achieving Grantor Trust Status

674 Power to Affect Beneficial Enjoyment 674(c) – Power to Distribute Income or

Principal, or to add beneficiaries

Grantor holding power = inclusion

Achieving Grantor Trust Status

674 Power to Affect Beneficial Enjoyment 674(d) – Power to allocate income

Power granted to someone other than grantor or “spouse living with grantor” to distribute, apportion or accumulate income to or for beneficiaries if limited by reasonably definite external standard

Power creates grantor trust as to income only Possible to switch grantor trust status on and off

merely by spouse moving out and back in?

Achieving Grantor Trust Status

675 Administrative Powers (Page 28)

675(2) – Power given to nonadverse party to make loans to grantor without adequate interest or security

N/A if trustee has authority to make loans to anyone without regard to interest or security

Power alone will cause grantor trust status, even if no loan is made

Achieving Grantor Trust Status

675 Administrative Powers 675(3) – Actual borrowing of funds

Direct or indirect loan to grantor or grantor’s spouse which is unrepaid at the end of year

N/A to loans with adequate interest and security Creates grantor trust to extent amounts are

unrepaid at year end, but . . . IRS has apparently ignored requirement that loan

remain outstanding until year end

Achieving Grantor Trust Status

675 Administrative Powers (Page 30)

675(4) – General Right exercisable in a non-fiduciary capacity by

any person to reacquire trust corpus by substituting other property

Grantor can hold

Achieving Grantor Trust Status

675 Administrative Powers (Page 30)

675(4) – General Right exercisable in a non-fiduciary capacity by

any person to reacquire trust corpus by substituting other property

Service’s position is that power alone isn’t sufficient, and applies a facts and circumstances analysis

Defective as to both income and principal Grantor can release Protector can re-grant

Achieving Grantor Trust Status

677 Power to Use Income for Benefit of Grantor (Page 34)

Grantor treated as owner of any portion of trust, whether or not under §674, the income of which, without the approval or consent of adverse party is, or in discretion of grantor or nonadverse party may be, distributed to or for benefit of grantor or spouse

Or used to pay premiums on life insurance on the life of grantor or spouse

Achieving Grantor Trust Status

677 Power to Use Income for Benefit of Grantor (Page 35)

Achieving Grantor Trust Status

677 Power to Use Income for Benefit of Grantor Trust should disallow use of income to satisfy

obligation of support Discretionary power to pay income to grantor

may cause inclusion under state law Some states have changed their laws to not

cause inclusion (Alaska, Delaware, and others)

Achieving Grantor Trust Status

678 Persons other than Grantor Treated as Owner (Page 35)

ONLY Code section attributing ownership to someone other than the actual grantor

Power to vest corpus or income exercisable solely by that person

surviving spouse as sole trustee of bypass trust? limitation to ascertainable standard (HEMS)

prevents estate tax inclusion switch on/off grantor trust status by

appointing/firing co-trustee

Achieving Grantor Trust Status

678 Persons other than Grantor Treated as Owner (Page 36)

Power to distribute income or principal which is “partially released or otherwise modified” that would cause grantor trust status under 671-677 5/5 power holder, until released, modified, or allowed

to lapse, is treated as grantor over portion of trust subject to power

Upon lapse, power holder is treated as grantor of amount in excess of 5/5

Crummey

Achieving Grantor Trust Status

§ 678 vs. §§ 671-677 (Page 36)

§ 678 N/A with respect to power over “income” during any period actual grantor is treated as owner under §§671-677

Service has interpreted §678(b) as applying to principal as well as income

Income Tax Reimbursement (Page 37)

Silence = prohibition? Mandatory = inclusion Discretionary = ??

Prearrangement?

Terminating Grantor Trust Status

Maintain Flexibility Power to terminate grantor trust status

should not be in hands of grantor

Reporting for a Grantor Trust

To File or Not to File (Treas. Reg. 1.671-4)

Option 1: No EIN or 1041 Provide payors with Grantor/owner’s TIN Grantor provides W-9 to Trustee Trustee statement for Grantor/owner

Option 2: EIN and 1041 Provide payors with Trust’s TIN Trust files Forms 1099 Trustee statement for Grantor/owner

Page 134 – Letter to CPA

Removing & Replacing Trustees (Page 37)

Right to Remove and Replace RR 77-182: No inclusion if trustee resigned RR 79-353: Inclusion if grantor removed

without cause PLR 9303018: Facts and circumstances Wall: No inclusion where replacement was

corporate fiduciary

Removing & Replacing Trustees (Page 41)

Right to Remove and Replace (con’t)

Vak: 8th Circuit said power to change trustee did not prevent gift from being complete, contrary to Tax Court’s position

RR 95-58: 79-353 revoked, 77-182 modified; No inclusion if successor was not “related or subordinate” under §672(c)

Related or Subordinate – A Review

Not adverse AND Any one of

Spouse, if living with grantor Parent Issue Sibling Employee Corporation where grantor has significant

voting control

Related or Subordinate – A Review

Does not include issue of siblings (nieces and nephews, etc.)

Spousal attribution Typically related or subordinate Literally adverse but not technically due to

spousal attribution

Removing & Replacing Trustees (Page 42)

Power to remove and replace retained by the grantor?

Yes

No

Is person being removed acting in a fiduciary capacity?

No

Yes

No 2036(a)(2) or 2038(a)(1) concern.

Must replacement be not related or subordinate to grantor with IRC

672?

2036(a)(2)/2038(a)(1) concern. Beyond Wall

logic.

No2036(a)(2)/2038(a)(1) concern. Beyond Rev.

Rul. 95-58.

Yes

Within Rev. Rul. 95-58

Removal of Trustee by Bene (Page 43)

For cause = Court; good or bad?

Corp Fiduciary Requirements (Page 44)

Be careful! Exclude expressly named institutions?

Lifetime LPOA (Page 44)

Ejection button Trustee vs. Protector

“Amending” an IRT (Page 44)

Lifetime LPOA Sell assets to new IRT Non-judicial modification per UTC Judicial modification Decanting (later) Trust Protector Other?

Trust Protectors (Page 46)

Common in offshore jurisdictions Little guidance in American law Role is different from trustee

Perspective of trusted family friend or advisor Counter-balance to impersonal institutional

trustee Enhanced flexibility without adverse tax

consequences

Trust Protectors (Page 47)

Who should serve? Gift tax consequences Income tax consequences

Trust Protectors (Page 49)

Removal and Replacement?

Power to remove and replace retained by the grantor?

Yes

No

Is person being removed acting in a fiduciary capacity?

No

Yes

No 2036(a)(2) or 2038(a)(1) concern.

Must replacement be not related or subordinate to grantor with IRC

672?

2036(a)(2)/2038(a)(1) concern. Beyond Wall

logic.

No2036(a)(2)/2038(a)(1) concern. Beyond Rev.

Rul. 95-58.

Yes

Within Rev. Rul. 95-58

Trust Protectors (Page 49)

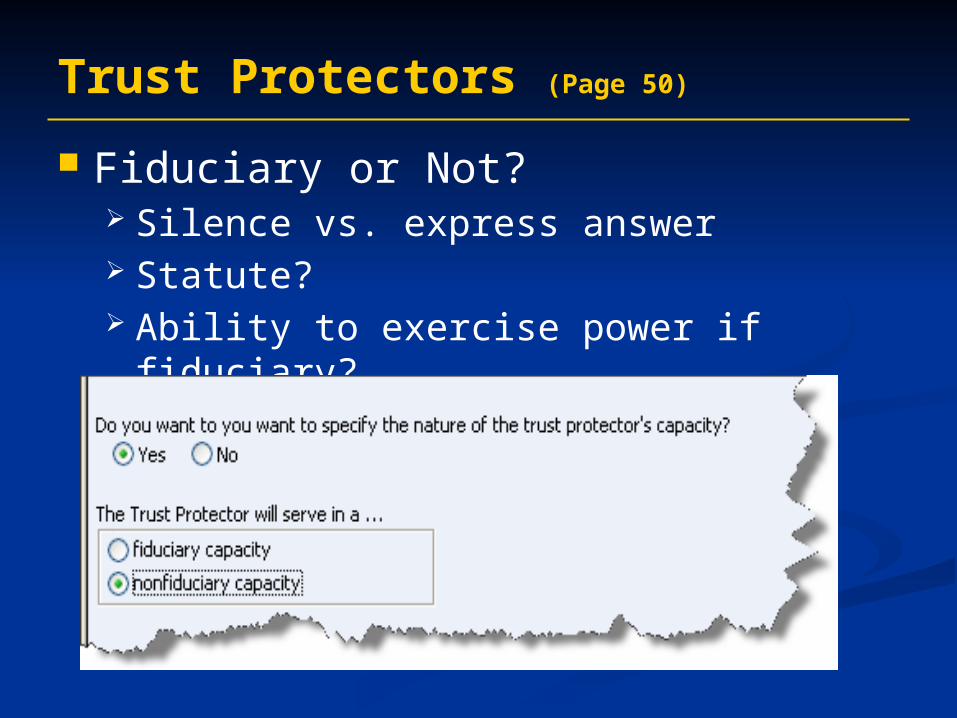

Trust Protectors (Page 50)

Fiduciary or Not? Silence vs. express answer Statute? Ability to exercise power if fiduciary?

Trust Protectors (Page 51)

Distribution of Estate Tax Includable Property (Page 53)

Marital deduction issues

Bypass(-type) Trust Issues (Page 54)

Mandatory vs. Discretionary Income Trust income tax rates better?

5/5 Powers

Administration of Remaining Trust (Page 55)

Guidelines for discretionary distributions Silences = required?

5/5 Powers Providing for children-in-law

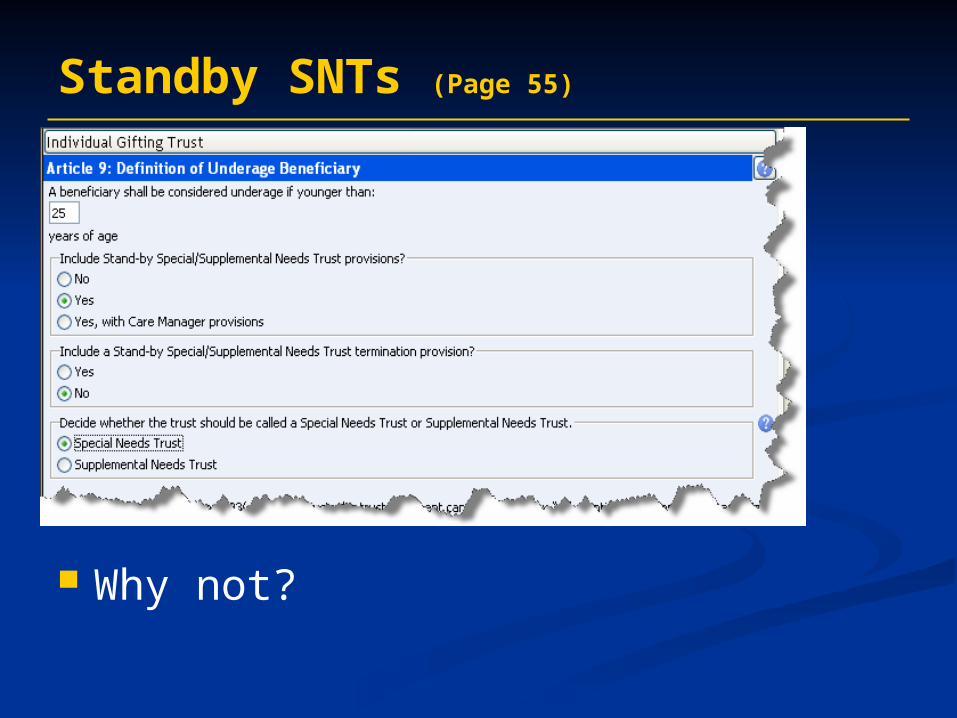

Standby SNTs (Page 55)

Why not?

Decanting Powers (Page 56)

Broad powers Discuss with client Tutorial

GST Exempt & Non-Exempt (Page 57)

Again, why not?

Generation Skipping (Page 57)

Annual GST Exclusion Only for direct-skip gifts (outright or in trust) If in trust:

Only one beneficiary; and Trust assets fully included in donee’s estate

Generation Skipping (Page 57)

Annual GST Exclusion Qualifying Trusts include:

2503(c) Trusts Separate Trusts for skip persons

Non-Qualifying Trusts include: Dynasty trusts Common trusts

Generation Skipping (Page 59)

GST Exemption $5.0M in 2011-2012 $??M in 2013 Can only be allocated by the transferor

Crummey Powers

Generation Skipping (Page 61)

Allocating the GST Exemption Allocation is irrevocable Automatic allocation to:

Lifetime direct skips At death, of any remaining GST exemption to

trusts from which there could be a generation skip Lifetime indirect skips to a “Generation-Skipping

Transfer Trust” Opt Out of Automatic Allocation on 709

IRS Form 709

If you aren’t preparing them …. Part 1 – personal information Schedule A

Part 1 – Gifts Subject Only to Gift Tax Gifts to children

Part 2 – Direct Skips Gifts to grandchildren

Part 3 – Indirect Skips Gifts to trust for children and grandchildren

IRS Form 709

Part 4 Line 1 – total gifts Line 2 – annual exclusions Line 3 – net of the two

Schedule B – Prior returns Schedule C – Computing GST

Part 2 – Allocating Remember to allocate to entire gift, not just taxable

portion!! Use formula allocation just in case

Divorce Provision (Page 63)

Need to discuss to avoid appearance of conflict

Gift Splitting (Page 63)

A legal fiction Only to third parties (not to spouses) All or nothing annually Consent must be made on Form 709 Gift

Tax Return

Drafting for Lifetime Benefits (Page 64)

Loans to grantor Trustee borrows against policy and re-loans If adequately documented and secured,

should be no incident of ownership No taxable income – trust is grantor trust

under IRC 675(3) Interest accrued is debt against estate (“Tax

Burning”)

Drafting for Lifetime Benefits (Page 65)

Inter-vivos Bypass Trust Spouse has access Danger is spouse’s death

Self-Settled Trust Jurisdictions

Reciprocal Trust Doctrine (Page 65)

Estate of Grace (US Sup Ct.)

Applicable where trusts are interrelated and grantors are left in the same economic position as if no trusts had been created

Reciprocal Trust Doctrine (Page 65)

Estate of Grace (US Sup Ct.)

Estate of Bischoff (Tax Court)

Applied doctrine to trusts established by grandparents for the benefit of grandchildren and naming grandparents as trustees.

Reciprocal Trust Doctrine (Page 65)

Estate of Grace (US Sup Ct.)

Estate of Bischoff (Tax Court)

Estate of Green (2nd Cir)

Refused to follow Bischoff stating that Grace court required benefit to be retained by grantors before doctrine was applicable.

PLR 200426008

Insurance-Related IRT Issues(ILITs)

Bill Conwaywww.wealthcounsel.com

ILIT Benefits (Page 67)

Remove death benefits from taxable estate

Control disposition of death proceeds Utilize annual gift tax exclusion for gifts to

the trust Asset Protection

ILIT Objections

Cost to set up Administrative hassle Perceived loss of access to cash value

build-up within policy

ILIT Alternatives (Page 67)

Continued individual ownership Ownership by adult children Family Insurance Partnership

Estate Taxation of Insurance (Page 68)

Insurance is included if: Insured possessed incidents of ownership (IRC

2042)

Proceeds are payable to or for the benefit of the estate (IRC 2042)

Policy (or incidents of ownership) are transferred within 3 years of death (IRC 2035)

Estate Taxation of Insurance (Page 68)

IRC 2042 Incidents of ownership

Power to change beneficiary Power to surrender or cancel the policy Power to assign the policy Power to revoke an assignment Power to pledge the policy A reversionary interest in the policy

Payable to or for the benefit of the estate

Valuation of Insurance (Page 69)

Generally: Interpolated terminal reserve

+ Unused premiums

+ Accumulated dividends

- Policy Loans Single premium policies valued by

replacement Group term has no value but continued

payment of premiums are on-going gifts from the employee

Income Taxation of Insurance (Page 69)

General Rule: Excluded from income (IRC 101(a)(1))

Exception: Transfer for Value (IRC 101(a)(2))

Exception to the Exception: Transferee determines basis from transferor’s

basis, i.e., carry-over basis (IRC 101(a)(2)(A))

Transferee is insured, partner of the insured, partnership in which insured is a partner, or corporation in which insured is shareholder or officer. (IRC 101(a)(2)(B))

Avoiding 3 Year Rule of 2035 (Page 70)

Never possess incidents of ownership Purchase new policy Sell policy to grantor trust Sell policy to partner of the insured Sell policy to partnership in which insured

is a partner

Avoiding 3 Year Rule of 2035 (Page 70)

Sell policy to grantor trust

RevocableLivingTrust

RevocableLivingTrust

ILITILIT

$150,000 + other assets

$150,000

Policy

Avoiding 3 Year Rule of 2035 (Page 71)

Sell policy to partner of the insured

RevocableLivingTrust

RevocableLivingTrust

ILITILIT

Limited Partnership (or LLC)Limited Partnership (or LLC)

$150,000 + other assets

Otherassets

L.P.Int.

Assets

G.P. & L.P. Int.

$150,000

Policy

Drafting to Provide Liquidity (Page 71)

Trustee is authorized to lend to the estate Trustee is authorized to purchase assets

from estate WD provides these options

Community Property Issues (Page 71)

Non-insured spouse cannot contribute to trust of which he or she is beneficiary

Solution is Partition Agreement

ILITs for Survivorship Policies (Page 72)

Neither spouse/insured can be trustee Incidents of ownership exist even in

fiduciary capacity Co-trustee may solve Joint trust can hold individual policies

Trustee Liability for Policy Performance (Page 72)

Recent lawsuits Trend to statutorily reduce liability Audits

Sale Transactions to Grantor Trusts

Bill Conway www.wealthcounsel.com

Introduction (Page 74)

Chapter 14 Lack of certainty with GRAT Grantor trust rules remain Less frequency with $5 million gift

exemption

Sequence

Grantor establishes defective IRT Grantor contributes assets, allocates GST

exemption Grantor engages in sale (or part-gift/part-

sale) with IRT

Initial Funding (Page 74)

Seeding the trust 10% “Rule” Guarantees as alternative

Types of Consideration (Page 76)

Case Not typically

Installment Note Interest-only vs. Self-amortizing Refinancing Income tax concerns at death

IRD? Step-up in basis?

Types of Consideration (Page 74)

Self-Canceling Note Term > life expectancy = Private Annuity Even for the young and healthy

Private Annuity Even for the young and healthy Exhaustion test

2036 Recharacterization (Page 82)

LaFarge & Lazarus (9th Cir.) Weigl Key is cash flow!

Defined Value Formulas (Page 82)

Procter, King, Ward McCord

Tax Court Lots of politics Full Tax Court Decision See Judge Laro’s dissent (Page 86)

5th Circuit

Defined Value Formulas (Page 82)

Christiansen Formula disclaimer of 75% to near-zero CLAT

and 25% to Foundation Disclaimant was CLAT remainderman 8th Circuit slams IRS – see page 88

Petter UPS stock LLC with three classes Sale for promissory notes three days after gift Defined value amount; excess to charity

Reporting a Sale to Grantor Trust (Page 90)

New Question 12(e) on 706 Better to report now or later?

Asset Protection Trusts (APTs) and Self-Settled Trusts

Bill Conwaywww.wealthcounsel.com

Asset Protection & Estate Taxation (Page 91)

Creditor may reach beneficiaries’ interest based on: Enforceability of spendthrift provision; Beneficiary’s control over trust; and Whether beneficiary has property interest

4 Exceptions to Spendthrift (Page 92)

Self-Settled Trusts 3 Exceptions under Restatement (Second)

of Trusts Tort creditor Misc. case law exceptions

Enforceability of Spendthrift Provision (Page 92)

Self-Settled Trust Exception to Spendthrift No protection except in twelve states and

twenty offshore jurisdictions More states are changing laws Common self-settled trusts:

Revocable “Living” Trusts Charitable Remainder Trusts Grantor Retained Annuity Trusts

Enforceability of Spendthrift Provision (Page 93)

Self-Settled Trust Exception Restatement of Trusts Exceptions

Alimony or child support; Necessary services or supplies rendered to

beneficiary (such as medical services) Claim by US or State (such as tax liens)

Enforceability of Spendthrift Provision (Page 94)

Self-Settled Trust Exception Restatement of Trusts Exceptions Tort Public Policy Exceptions

MS court vs. MS legislature

Enforceability of Spendthrift Provision (Page 94)

Self-Settled Trust Exception Restatement of Trusts Exceptions Tort Public Policy Exceptions Case Law Exceptions

ERISA protects assets until paid out NY statute exposing principal “unnecessary

for reasonable requirements of judgment debtor”

Income paid is exposed

Beneficiary’s Control (Page 95)

Non Self-Settled Trusts Bene/Sole Trustee can’t protect from own

improvidence therefore no protection – FL AR expressly states otherwise Check your state law!

Co-trustee provides protection Fiduciary duties prevail if other benes

Beneficiary’s Control (Page 96)

Self-Settled Trusts in AP Jurisdictions Statutory specificity Classic jurisdictions:

Isle of Man Jersey Guernsey

Conflicts of Laws issues Contempt Orders

Affordable Media

Property Interest (Page 97)

Creditors may recover against debtor’s property interests

A discretionary interest in a trust is not a property interest

A property interest is one that can be sold or exchanged

Property Interest (Page 97)

Spendthrift precludes Mandatory distributions – “shall”

QTIPs GRTs & CRTs

Ascertainable Standards – “shall” for HEMS Beneficiary can sue under state law Creditor stands in beneficiary’s shoes

Special Needs Trusts

Property Interest (Page 99)

Conflicting Provisions Discretionary language + ascertainable

standards “may” for HEMS Have to consult state law to determine how

provision is interpreted

Discretionary Trusts (Page 101)

Beneficiary may not sue trustee Erosion of protection for:

Necessities of beneficiary Tax liens Alimony

Contingent Remainder vs. Dynasty Trust (Page 102)

Trend to treat contingent remainder as property interest CO – child bene has property interest in

bypass trust during life of surviving spouse CO – property interest in inter vivos trust even

during life of grantor Logic doesn’t apply to Dynasty Trust

Offshore or Domestic APT (Page 103)

Self-settled trusts Questionable protection in other than APT

jurisdiction Split-interest trusts

Non-Self Settled has fewer concerns Divorce – equitable division Cost/Benefit

Domestic Self-Settled Trust (Page 104)

More states changing laws Having it and not having it

Ownership vs. Exclusion Interplay between asset protection and

estate tax exclusion State law and creditor’s ability to reach

trust assets Prearrangement

Domestic Self-Settled Trust (Page 105)

Alaska Delaware Nevada Rhode Island Utah South Dakota Oklahoma Missouri?

Tennessee New Hampshire Wyoming Colorado Hawaii

Domestic Self-Settled Trusts (Page 106)

The evolution of the case law Herzog

Augustus Hand NY trust; completed gift

Holtz External standard for distributions = incomplete

Outwin MS trust; incomplete gift

Domestic Self-Settled Trusts (Page 107)

The evolution of the case law Irving Trust

Augustus Hand again NY trust; assets excluded

Uhl IN trust; assets included

Rev. Rul. 77-378 Retained “Right” is the problem Alaska’s Logical Next Step

Split-Interest Trusts

Bill Conwaywww.wealthcounsel.com

Techniques for leveraging gifts Distinct economic interests

Division of time of ownership Division of the type of interest

That which is not given away is retained

Split-Interest Trusts (Page 78)

Grantor

Gifted Asset

Retained Benefit

Remainder

Split-Interest Trusts (Page 111)

Common Split-Interest Trusts CRTs CLTs GRTs QPRTs

We’re going to focus on the taxable gift trusts, i.e., non-charitable split-interest trusts

Split-Interest Trusts & Ch. 14 (Page 112)

Chapter 14 Designed to reduce intra-family

undervaluations of split-interest transfers Valuation provisions 2702- Fixed annuity or unitrust amount

Benefit of Split-Interest Trusts (Page 112)

Assumes: Property will produce income equal to 120%

of Federal Mid-Term Rate (§7520 rate) Principal value neither increases or decreases

General Rules (Page 113)

Who Can Serve as Trustee During income interest, may be grantor After income interest, other than grantor

General Rules (Page 113)

Problems with Gift-Splitting If spouses gift-split and one dies, only one-

half of the applicable credit is restored All or nothing in any given year

General Rules (Page 113)

Estate Tax Inclusion Period & GST 2642(f)(3) values transfer of asset at end of

period “during which the value of the property involved would be included in the gross estate of the transferor under chapter 11 if he died immediately upon making such transfer.”

Not appropriate for split-interest trusts Cannot allocate GST until after ETIP period Grant GPOA if trust provides for skip persons

Practical Matters to Consider (Page 114)

Effect of Interest Rate Higher rate = higher retention = lower gift

Term Longer term = more retained = lower gift Mortality risk increases over longer term Hedge mortality risk with insurance

Appraisal – Get them! EIN

Grantor trust during initial term May or may not be grantor trust after initial

term

GRITS (Page 116)

Income to Grantor for term Remainder paid to remainder beneficiary Significant benefit with

Non-income producing property Low income producing property

2702 eliminates use with family members Specific exception for personal residence -

QPRT

GRITS (Page 117)

Still useful for Business situations Gift to nieces and nephews Non-family settings

QPRTs (Page 117)

Gift to family members with retained right to live in the residence for term of years QPRTs generally overvalue use QPRTs assume no appreciation

QPRTs (Page 118)

Income Tax Consequences Grantor trust during term Mortgage interest deduction passes through

to grantor IRC 121 exclusion still available

QPRTs (Page 118)

Gift Tax Consequences Ch. 14 doesn’t apply

QPRTs (Page 118)

PRTs Residence can’t be sold May not hold cash No contemplation of destruction of home

QPRT Residence may be sold

Reinvest within 2 years May hold cash Residences must be “personal residence”

Principal residence One other residence of grantor

Attributes of QPRTs (Page 119)

Attributes Prohibitions Requirements

QPRTs (Page 121)

Sale or disuse of residence disqualifies Upon disqualification, may

Distribute outright to grantor Convert to GRAT

Payment based on original 7520 rate Begins on date of sale, disuse, destruction, etc.

QPRTs (Page 122)

Effect of transferring property subject to mortgage If non-recourse, gift is FMV – debt; Continued

payment on debt are recurring gifts If recourse, gift is FMV; Continued payments

on debt are not additional gifts

QPRTs (Page 123)

Joint Property Each spouse can contribute one-half interest

to separate QRPTs Beware Reciprocal Trust Doctrine!

QPRTs (Page 123)

Options at End of Term Lease Life-estate in non-grantor spouse

QPRTs (Page 124)

Capital Gain Tax on Sale Prohibition of Repurchase by Grantor Grantor Trust Beyond Term where

Administrative Powers Retained

QPRTs (Page 125)

Asset Protection After term, asset is removed During term, income interest is likely

reachable by creditors Regs require trustee to dispose of residence if

not used by grantor Conversion to GRAT may help

Remainder is protected Annuities are exempt in many states

GRUTs (Page 125)

Why They Do NOT Work Payout is unitrust amount As trust increases, payout increases Effect is that corpus remains about same as if

property had been gifted Direct gift has no reversion possibility

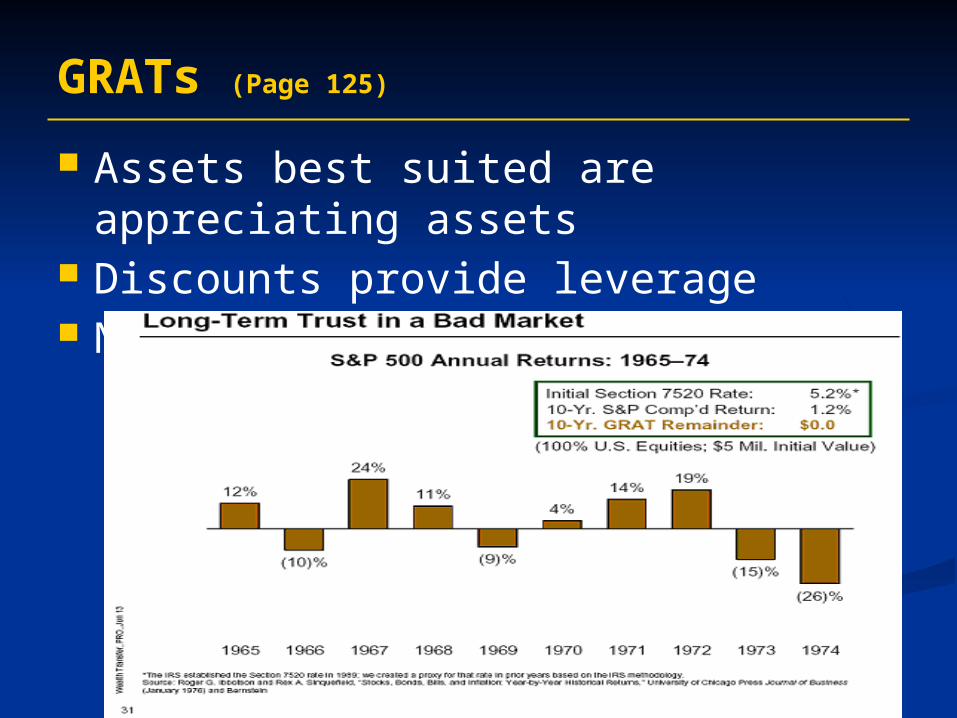

GRATs (Page 125)

Assets best suited are appreciating assets Discounts provide leverage No-Lose Propositions

GRATs (Page 127)

Rules for GRATs Can Increase Payouts (up to 120%) Gift Tax Valuation Estate Taxes

If grantor fails to survive term, inclusion of all property

Income Taxes GRAT is a grantor trust

Spousal Annuity Interest

GRATs (Page 129)

Zero’ed Out GRATs- Walton Case

GRATs (Page 130)

“Amoeba” or Rolling GRATs

GRATs (Page 131)

Effects of Rolling GRATs

Lifetime QTIPs (Page 132)

Trust created by one (“propertied”) spouse for another (“non-propertied”) spouse

Equalize estates without propertied spouse giving up control

Requires all income be paid at least annually to donee spouse

Can create secondary life estate for donor spouse

Lifetime QTIPs (Page 133)

Asset Protection During life of donee spouse – spendthrift trust After death of donee spouse

Lifetime QTIPs (Page 133)

Elements Only permissible beneficiary is donee spouse All income paid at least annually No person has power to appoint property

during life of donee spouse QTIP election is timely made on 709

No cure if you miss this!!! See PLR 201109012

Lifetime QTIPs (Page 134)

Estate Tax Effects Death of donee before donor renders donee

transferor for future trusts Can Allocate GST Exemption

Thank You!

Please fill out reviews!!

Bill Conway www.wealthcounsel.com