understanding life insurance

DESCRIPTION

The purpose of life insurance is to help ensure that those who depend on you will still beable to maintain their standard of living if something should happen to you. Life insurancehelps secure your loved ones’ futures and potentially provide them with enough moneyto fulfill their obligations and pursue their dreams, even if you are no longer with them.TRANSCRIPT

Understanding Life Insurance

Products issued by

National Life Insurance Company® | Life Insurance Company of the Southwest™

National Life Group® is a trade name of National Life Insurance Company, Montpelier, VT, Life Insurance Company of the Southwest, Addison, TX and their affiliates. Each company of National Life Group is solely responsible for its own financial condition and contractual obligations. Life Insurance Company of the Southwest is not an authorized insurer in New York and does not conduct insurance business in New York.63784 MK3083(1212) TC70357(1212)10

%

2

“What does life insurance mean to you?” This question was posed to the agents and employees of National Life Insurance Company and Life Insurance Company of the Southwest. Included in this brochure are the photos they submitted to show who they protect with life insurance.

Cover Photos (clockwise from top left): Raymond & Jeannine; Expectant parents, Betsy & Dan; Family members, Palmer, Chapel, Emily, Charles, Adelaide & Katy; Malia.

Rosita & Antonio

Jett

3

Chris & Kristin

What are you doing to financially protect those you love?Chances are you have insurance coverage on your house or your car to help offset losses from unforeseen events. But have you done the same with your life?

The purpose of life insurance is to help ensure that those who depend on you will still be able to maintain their standard of living if something should happen to you. Life insurance helps secure your loved ones’ futures and potentially provide them with enough money to fulfill their obligations and pursue their dreams, even if you are no longer with them.

4

1 Riders are optional, may require additional premium and may not be available in all states.

2 Policy loans and withdrawals reduce the policy’s cash value and death benefit and may result in a taxable event. Surrender charges may reduce the policy’s cash value in early years.

Colby

Brother and sister, Christopher & Angela

What is life insurance?As uncomfortable as it is to think about, imagine what standard of living your family would have if you were no longer with them. Could they still pay the mortgage? Pay for education? Buy groceries? Life insurance protects your family against the loss of income when you die. It helps pay for funeral costs, cover household expenses and secure your family’s financial future.

Many life insurance policies have riders that can be added to provide you with benefits you may use throughout your lifetime, called living benefit riders.1

You may also be able to use your policy’s accumulated cash value to help fund your children’s education, assist with expenses if you become disabled, or supplement your retirement income.2

5

Cousins, Aiden & Rebecca

Siblings, Victoria, Kohl, Keisha, & Billy

How does life insurance work?All life insurance policies operate under the same general structure. You make payments, also known as “premiums,” to a life insurance company. In return, the company agrees to pay a specified amount to whomever you designate to receive the money from your policy when you pass away.

6Rossy & Antiono

Family members, Katy, Rebecca, Ingram & Emily

Who needs life insurance?Most people need life insurance in one form or another. If one or more of these scenarios apply to you, you may have a need for life insurance:

•Youhavedependentchildren

•Youhaveaspouseorolderfamilymember who depends on your wages

•Youareaworkingcouplewithdebt

•Youareplanningtostartafamily

•Youownahome

If you are in one or more of these stages of your life, you may want to meet with a licensed insurance professional to see if life insurance is right for you. It could prove to be one of the most valuable financial decisions you ever make.

7

Mother and son, Jane & Jason

Brother and sister, Ryan & Julie

What type of insurance should I purchase?Once you determine that you may have a need for insurance, there are three basic types of insurance that you can choose from: Term, Whole Life and Universal Life.

Term Insurance

With Term insurance, you are guaranteed coverage for a set period of time, or term, usually for a specific number of years or until a specified age, as long as premiums are paid. Term insurance policies are usually renewable once that time period has expired, although it is likely for premiums to then increase. Since Term provides a death benefit if the insured dies within a defined period of time and does not accumulate cash value, you can generally purchase a higher death benefit for your premium dollars. It is frequently the most affordable coverage.

8

Mother and daughter, Christine & Hayley

Thomas & Cynthia

Caira

1 Guarantees are dependent on the claims-paying ability of the issuing insurer.

Whole Life

Whole Life insurance offers guaranteed premiums that will not increase or decrease, a guaranteed death benefit plus the guarantee of building cash value within your life insurance policy.1 With Whole Life insurance, you do not have to pay current income taxes on the increase of the cash value within the policy and you may be able to potentially access these funds on a tax-advantaged basis.2

Whole Life is frequently referred to as “permanent” insurance because unlike Term policies, it remains in force for life, as long as the premiums are paid as scheduled. Also, unlike Term

policies, after owning a policy long enough to build cash value, you may take out a loan on the cash value to use however you wish. When you pass away, your beneficiaries will receive the amount of the death benefit, minus any outstanding loans and loan interest that may be due on your policy.

9

Uncle and nephew, Ron & Connor

Universal Life

Considered the most flexible of the three types of life insurance, Universal Life allows you to adjust the amount of your policy, also called the face amount, and the premiums you pay. You also have the potential to build cash value in your policy based on a guaranteed minimum interest rate.1 Like Whole Life, you can build cash value in your policy without paying current income taxes on the increases and you can potentially access the funds on a tax-advantaged basis.2

Universal Life’s flexibility allows you to stop paying premiums if there is enough accumulated value in your policy to cover the cost of insurance each month. If you desire, you can then pay additional premiums to build back up accumulated cash value. You may also be able to increase or decrease your death benefit depending on your life insurance needs. An increase may require additional underwriting.

Two of the most popular types of Universal Life insurance are Fixed Universal Life and Indexed Universal Life. One of the main differences between them is in how the policy’s interest is credited. With a Traditional Fixed Universal Life policy there is an interest rate declared by the company that is credited to the policy’s cash value. Indexed Universal Life credits the interest based on the changes in value of a major market index. Both offer you varying degrees of guarantees and returns, based on your appetite for risk.

2 Policy loans and withdrawals reduce the policy’s cash value and death benefit and may result in a taxable event. Policy loans in excess of premiums paid will not be considered taxable income unless the policy lapses. Values withdrawn exceeding the premiums paid into the contract will be treated as taxable income.

10

Cousins, M.J. & Trace

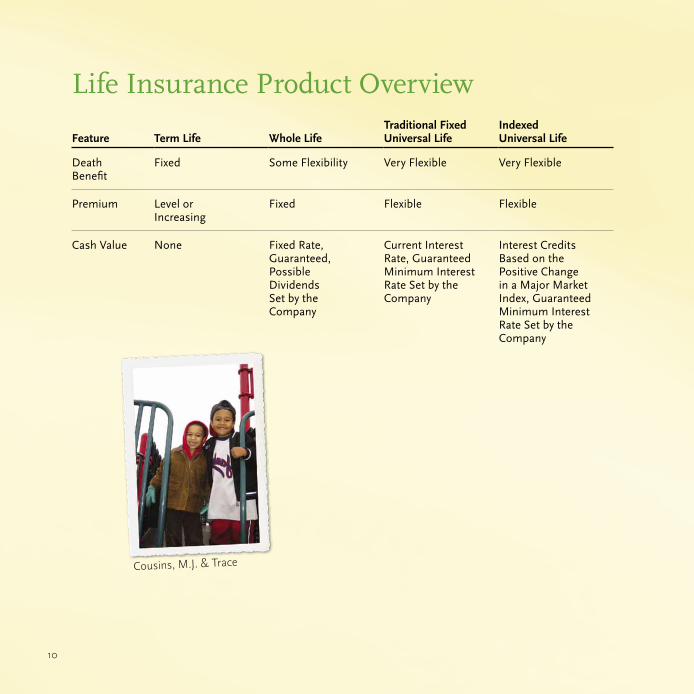

Life Insurance Product Overview

Feature Term Life Whole LifeTraditional Fixed Universal Life

Indexed Universal Life

Death Benefit

Fixed Some Flexibility Very Flexible Very Flexible

Premium Level or Increasing

Fixed Flexible Flexible

Cash Value None Fixed Rate, Guaranteed, Possible Dividends Set by the Company

Current Interest Rate, Guaranteed Minimum Interest Rate Set by the Company

Interest Credits Based on the Positive Change in a Major Market Index, Guaranteed Minimum Interest Rate Set by the Company

11Siblings, Julie, Aimee & Ryan

A licensed National Life Insurance Company or Life Insurance Company of the Southwest agent can help you decide what type of coverage and premium payment is right for you. Although there are many choices available, the most important thing is to find a policy and combination of riders that best fits you and your family’s needs.

Life insurance is a unique financial tool that can be structured to accomplish many objectives, and it can be customized to fit very specific needs. If you are committed to protecting the people that are important to you, find out how life insurance can provide you with the security, protection and opportunities that can help you make what may be today’s dreams, tomorrow’s reality.

800-732-8939 | www.NationalLifeGroup.com Centralized Mailing Address: One National Life Drive, Montpelier, VT 05604