understanding our climate- related risks and opportunities

TRANSCRIPT

UNDERSTANDING OUR CLIMATE- RELATED RISKS AND OPPORTUNITIESTASK FORCE ON CLIMATE-RELATED FINANCIAL DISCLOSURES

(TCFD) REPORT 2020

Kinnevik AB ∙ TCFD Report ∙ 2020

2

ong-term sustainable development is an integrated part of Kinnevik’s bu-siness model: from the sourcing and assessment of new business opportu-nities, to the ongoing development of our companies and the re-allocation of

capital into new opportunities. Our ambition is to develop our companies into

long-term sustainable businesses in line with the Paris Agreement, and to futureproof them for a new, low-carbon economy. To do this, we have set a sus-tainability strategy based on the UN 2030 Agenda for Sustainable Development, which balances the three dimensions of sustainability: environment, society and governance.

In the spring of 2020, Kinnevik adopted new climate targets for our own operations and our portfolio, in line with the carbon law and with the 1.5˚C ambition. You can read more about our cli-mate targets on page 9. As part of this effort, we are supporters of the TCFD and have implemented its recommendations, which enable us to better understand the actual and potential impact of climate-related risks and opportunities on our busi-ness, strategy and financial planning. By identifying and assessing the most material of these risks and

opportunities for Kinnevik and our portfolio, we can manage and mitigate the risks while seizing the opportunities, which creates resilience and enables long-term value creation. The result of our analysis is presented in this report, which covers the full year 2020.L

INTRODUCTION

The effects of climate change are clearly visible and will have an increasingly tangible impact on Kinnevik and our portfolio. Implementing the recommendations of the TCFD enables us to identify, assess and manage our most material climate-related risks and opportunities.

Our ambition is to develop our companies into long-term sustai-nable businesses in line with the Paris Agreement, and to future-proof them for a new low-carbon economy

OUR SUSTAINABILITY STRATEGYKinnevik’s sustainability strategy is a framework set up to focus our resources on the most relevant economic, social and environmental issues, drive performance and to engage internal and external stake-holders. Click here to read more.

MORE

Kinnevik AB ∙ TCFD Report ∙ 2020

3

GOVERNANCE

BOARD OVERSIGHTThe Board of Directors is responsible for Kinnevik’s overall strategy, including how we integrate sustainability aspects as part of our value creation. Further, the Board of Directors is specifically responsible for identifying risks and opportunities related to sustainability, including climate change, that may impact Kinnevik, and to define appropriate guidelines to go-vern Kinnevik’s conduct in society. This is embedded in the work and delegation procedures of the Board of Directors.

To assist the Board of Directors in fulfilling its responsibilities relating to sustainability and to oversee Kinnevik’s risk management process, the Board of Directors has appointed a Risk, Compli-ance & Sustainability (“RCS”) Committee. The RCS Committee specifically moni-tors the implementation of the Kinnevik Standards (read more on page 7) across our portfolio companies, including an-nual ratings and qualitative assessments, and regularly evaluates risks related to Kinnevik’s, and our portfolio companies’, operations. The Committee meets at least four times a year and reports to the Board of Directors on its activities, and makes relevant recommendations, at the subse-quent Board meeting.

During 2020, the Board of Directors approved a new climate strategy outli-ning Kinnevik’s ambitions which includes emission reduction targets for Kinnevik and our portfolio.

MANAGEMENT APPROACHTo drive the implementation of our sus-tainability strategy and assess potential risks and opportunities related to climate change, Kinnevik has a dedicated Sustai-nability Team. The Sustainability Team, together with the Investment Team, is re-sponsible for implementing our sustaina-bility standards across our portfolio com-panies and driving specific sustainability related projects, including our climate

strategy. In addition, to ensure that we deliver on our climate strategy, we have established a Climate Team, a sub-group within the Sustainability Team, which sup-ports our portfolio companies on climate-related topics. The Sustainability Team and the Climate Team regularly reports to the Kinnevik Management Team and the RCS Committee on the work done and progress made.

The overall responsibility for Kinnevik’s risk management process lies with Kinnevik’s CEO, who has delegated the responsibility to the CFO. Further, Kinne-vik has established a Risk Committee to oversee our risk management framework and support the CFO in this regard. The Risk Committee comprise all senior mana-gers of Kinnevik and meets at least three times a year to review key risks and deve-lopments since the previous meeting, the efficiency of any mitigating actions and our overall risk appetite. The work of the Risk Committee is presented at each RCS Committee meeting and at Audit Com-mittee meetings on a periodic basis. To manage the ongoing risk management work within Kinnevik and across our port-folio, the Risk Committee has appointed a Risk Team who is responsible for the ongoing risk assessment process. The Risk Team comprises the Sustainability Director, one Corporate Team member and one Investment Team member.

During 2020, the Management Team and the Climate Team held a workshop with the purpose of identifying an ac-tionable climate strategy, including re-levant reduction targets. The proposed climate strategy was later presented to, and approved by, the Kinnevik Board of Directors. The Sustainability Team and the Climate Team are responsible for implementing the climate strategy within Kinnevik’s operations and across the portfolio companies and regularly inform the Management Team and the RCS Committee on the execution of such.

Kinnevik have continued to intensify and further integrate climate-related to-pics into our existing governance pro-cesses during 2020. With climate being one of three dimensions of our Sustai-nability Framework and in light of our newly adopted climate strategy, we have increased our focus and efforts around climate-related issues and topics on all levels of our business.

In this section, in accordance with the TCFD recommendations, we aim to describe Kinnevik’s governance structure in relation to climate-related risks and opportunities.

“As active owners, it is Kinnevik’s responsibility to put sustainable business development at the top of the agenda at our inves-tee companies and to make sure that they seize the opportunities arising from this. Supporting the TCFD’s recommendations helps us to understand and act on our portfolio’s most important climate-related risks and oppor-tunities. We believe companies that operate in a responsible and sustainable manner will be able to remain the preferred choice for consumers, as well as to re-cruit the best employees, thereby outperforming their competitors in the long run.”

Georgi Ganev Kinnevik’s CEO

Kinnevik AB ∙ TCFD Report ∙ 2020

4

Board of Directors

Management

Investment Team Sustainability Team

Climate Team

Risk Committee Sustainability Team

Risk Team

Investee Companies

Risk, Compliance & Sustainability Committee

Audit Committee

OUR CORPORATE GOVERNANCEThe basis for corporate governance within Kinnevik is Swedish legislation, the NASDAQ Stock-holm Rules for Issuers and Issuer Agents and the regulations and recommendations issued by relevant self-regulatory bodies. Click here to read more about corporate governance at Kinnevik.

MORE

Overview of Kinnevik’s Governance and Sustainability Organisation

Kinnevik AB ∙ TCFD Report ∙ 2020

5

STRATEGY

KINNEVIK’S BUSINESS AND STRATEGYKinnevik’s strategy is to be the leading growth investor by:

• Backing challenger businesses that use technology to address material, everyday consumer needs

• Being a bold and long-term business builder and partnering with talented entrepreneurs

• Focusing on Fashion & Food e-Com-merce, Online Marketplaces, Financial Services, Healthcare and TMT: large sectors in the process of significant technological disruption

• Investing in Europe, with a focus on the Nordics, the US, and selectively in other markets

• Leveraging our experience and ex-pertise to build leading, long-term sustainable businesses

We believe in the power of technology to make life better for people around the world. That is why we build digital businesses that make a positive difference to peoples’ lives. Whether it is consumer services, financial services, healthcare services or telecom, technology is making everything easier, speedier and more freely available.

CLIMATE-RELATED RISKS AND OPPORTUNITIES

Methodology and ProcessKinnevik’s portfolio consists of around 25 companies in four sectors: Consumer Services, Financial Services, Healthcare Services and TMT. Within Consumer Ser-vices, there are four sub-sectors: Online Fashion, Online Food, Travel and Other.

To identify our most material climate-

related risks and opportunities, Kinnevik’s CEO convened a workshop in May 2020 for Kinnevik’s Management Team and Climate Team. The workshop analysed the potential implications of climate change on Kinnevik’s business, strategy and financial planning. Each of Kinnevik’s sectors and sub-sectors were analysed individually, with emphasis on those with the highest climate-related risks and opp-ortunities, as well as those that are most material in terms of share of our portfolio value.

The analysis is done from Kinnevik’s per-spective as an owner, as opposed to the portfolio companies’, and focuses on the implications on our business, strategy and financial planning. As an investment company, we do not have the level of insight into all our portfolio companies that an operating company would per-haps have into its own operations, which creates an uncertainty factor. However, implementing the TCFD recommenda-tions provides us with an overview and a base from which to continue our active dialogue with our companies. The results of the workshop are summarised below.

Summary Implications on Our Business, Strategy and Financial PlanningIn our assessment of the potential implica-tions of climate change on Kinnevik’s bu-siness, strategy and financial planning in accordance with the TCFD framework, we have identified near-, mid- and long-term risks and opportunities across our four sectors. We believe transition risks related to market and reputation, i.e. changes in customer behaviour and preferences, are the most material climate-related risks. Increasing awareness about climate change will impact customer preferen-ces, leading to increased demand for products and services with a low climate impact. The risk of not being able to meet these demands by making the transition to a low-carbon economy may have a significant impact on our companies’ competitiveness.

Our Consumer Services and TMT companies are to a larger degree reli-ant on physical assets and facilities for their production and offices, and they have more complex supply chains. They would therefore be more affected by se-vere weather events such as heat waves, floods and forest fires - generally referred to as physical risks. The consequences could include reduced product availa-bility, increased repair costs of damaged buildings and inventory loss, which would have a negative impact on sales and lead to increased costs. Our Healthcare and Financial Services companies are gene-rally less exposed to climate risks, both transition and physical, given their highly digital business models.

All our companies are to some de-gree exposed to transition risks stemming from increased pricing of greenhouse gas emissions and increased emissions reporting obligations. Carbon pricing mechanisms (e.g. carbon taxes, tariffs and cap-and-trade schemes) could have future implications on costs, their ability to operate and return on investment. Simi-

This section aims to describe the actual and potential material impacts of climate-related risks and opportunities on Kinnevik’s business, strategy and financial planning.

Kinnevik’s portfolio composition per 31 December 2020

Consumer Services

57%TMT

19%

20%Healthcare Services

2%Emerging Markets

2% Financial Services

Kinnevik AB ∙ TCFD Report ∙ 2020

6

larly, overhead costs may rise as a result of more rigorous regulations related to emissions reporting.

Meanwhile, we see several opportuni-ties related to climate change, particularly as our strategy is to invest in technology enabled digital businesses. The main opportunity relates to being consumers’ preferred choice by leveraging new tech-

nology to take the lead in developing products and services with a low or po-sitive climate impact. Compared to more analogue business models, our compa-nies are in a good position to accelerate the pace of transformation to meet the increasing demands of their increasingly climate-conscious customer base.

For more details on the main climate-related risks and opportunities for each of our sectors and sub-sectors, refer to the appendix on page 11.

Timeline: Short term: <3 years Mid-term: 3-5 years Long term: 5-30 years

Classifications: Low: Monitor development to ensure risk exposure remains low Mid: Mitigate and monitor risks to maintain current level of risk exposure High: Implement mitigating actions to reduce exposure

Note: More information about the risk classifications is available on page 8.

RISKS OPPORTUNITIES

TRANSITION PHYSICAL

Policy &

Legal

Technolo

gy

Market

Rep

utation

Acute

Chro

nic

Reso

urce Efficiency

Energ

y source

Prod

ucts & Services

Markets

Resilience

Timeline Mid Mid Short Short Mid Long Short Short Short Short Mid

Classification Mid High High High Mid Low

Consumer Services

Fashion X X X X X X

Food X X X X X X X

Travel X X X X

Financial Services X X X X

Healthcare Services X X

TMT X X X X X X X

Overview of key risks and opportunities per Kinnevik sector

Kinnevik AB ∙ TCFD Report ∙ 2020

7

INFLUENCING THE TRANSITION TO A LOW-CARBON ECONOMYKinnevik systematically sources and as-sesses potential new investments. From a wide funnel of companies, a small se-lection is brought to Kinnevik’s Executive Investment Committee (“EIC”), where these companies are evaluated based on our eleven investment criteria, which includes sustainability related risks and opportunities. We also conduct thorough sustainability due diligence, where com-panies are evaluated based on their per-formance and structures in relation to environmental, social and governance aspects. During 2021, we will continue to develop our sourcing process, including the EIC procedures, to focus more closely on the companies’ risks and opportunities related to climate change.

Post investment, we develop a plan for each company, which varies according to each business’s characteristics and needs. We conduct bi-annual investment reviews during which our Investment Team discus-ses our companies’ developments across a number of parameters, including sustai-nability. In addition, Kinnevik’s Sustaina-bility Team conducts a yearly qualitative assessment of all portfolio companies and sets targets and priorities for the coming year. Companies are assessed according to the Kinnevik Standards (the “Standards”), which comprises of a structured framework of best practice standards across environmental, social and economic aspects. During 2020, we updated the Standards and raised our expectations of our companies in rela-tion to climate aspects, requiring yearly calculations of greenhouse gas (”GHG”) emissions, establishment of relevant cli-mate targets in line with the 1.5˚C am-

bition, and assessment of key risks and opportunities related to climate.

To enable our companies to measure their GHG emissions, we support them in implementing a GHG reporting tool. This allows Kinnevik to aggregate our total portfolio emissions and to track progress according to our emissions reduction target for the portfolio. The GHG emis-sions tool also allows us to influence our companies to analyse and report on their climate-related risks and opportunities, which will provide us with a better base for future TCFD reports. Read more about our climate targets on page 9.

Scenario AnalysisIn 2020, we conducted a scenario analysis to better understand the future impact on our business, strategy and financial planning of different scenarios of global warming.

We selected two Representative Con-centration Pathways, reflecting two very different climate outcomes; the Stringent Mitigation Scenario (RCP2.6) where emis-sions are halved by 2050 in line with the Paris Agreement, and the Very High Emis-sions Scenario (RCP8.5) where emissions continue to rise at current rates. These were considered in combination with two Shared Socioeconomic Pathways; in our description of RCP2.6 we included the SSP1 narrative, and for RCP8.5 we inclu-ded the SSP5 narrative.

We started with a top-down analysis of our three focus sectors Consumer Services, Healthcare Services and Fi-nancial Services. Based on a materiality analysis, we put particular emphasis on those sectors and sub-sectors with the highest impact from climate-related risks and opportunities, as well as those that

are most material to Kinnevik in terms of share of our portfolio value. Following the top-down analysis, we conducted a more in-depth analysis of each sector together with the respective responsible Investment Managers.

As our strategy is to invest in digital companies operating primarily a market-place model, with the exception of food, our portfolio generally has relatively low dependency on complex supply chains, physical assets and fossil fuels. Hence, our strategy shows relative resilience in a Very High Emissions Scenario. However, in this scenario the overall benefits of sus-tainability and low-emissions services are not recognized by consumers, impacting businesses trying to use sustainability as a competitive advantage.

As an investor in consumer-facing sectors, Kinnevik is exposed to a broad set of transition risks in the Stringent Mi-tigation Scenario, particularly related to market and reputation, i.e. shifting con-sumer behaviour as a result of increased climate consciousness and decrease in discretionary consumption. Meanwhile, this scenario also offers the largest cli-mate-related opportunities with regards to Kinnevik’s strategy to invest in digital companies disrupting legacy industries through innovation and new technology.

The results of the scenario analysis, was presented to the Risk Committee in February 2021, after which they were pre-sented to the RCS Committee in March 2021.

For more details on the conclusions of our scenario analysis, refer to the ap-pendix on page 7.

OUR BUSINESS MODEL AND VALUE CREATIONSustainability is an integrated part of our business model, from the sourcing and assessment of new business opportunities to the ongoing development of our companies and the re-allocation of capital into new opportunities. Click here to read more about our business model.

MORE

Kinnevik AB ∙ TCFD Report ∙ 2020

8

RISK MANAGEMENT

RISK ASSESSMENT PROCESSTo identify, assess and manage risks, including climate-related risks, for Kin-nevik on an ongoing basis, the Board of Directors has adopted a Risk Manage-ment Policy. To facilitate the implementa-tion of this risk management framework, Kinnevik has a detailed risk assessment process which is overseen by the Risk Committee and run by the Risk Team. As a diversified investment company, a material level of Kinnevik’s risk exposure sits within our portfolio, which is why the risk assessment process is performed at both the Kinnevik and portfolio levels. The Kinnevik Risk Register and Portfolio Risk Register are used to record the results of this assessment process.

Kinnevik’s risk exposure is not static and consequently therefore risk assess-ment process is performed and updated at least three times a year. The Risk Team meet with the relevant internal teams to identify Kinnevik and portfolio risks which are then documented in the Risk Registers. Kinnevik risks are categorised according to a non-exhaustive list of de-fined risk categories, and portfolio risks are categorised by company. Kinnevik’s risk categories are: existing portfolio, new investments, liquidity, compliance, talent, reputation, financial and reporting.

On a Kinnevik level, we expect climate-related risks to be categorised as both existing portfolio risks and reputatio-nal risks as our companies’ sectors are increasingly scrutinised from a climate change perspective. During 2020, Kin-nevik further integrated climate-related risks into its risk management framework and existing risk categories.

Based on a qualitative analysis, all risks are awarded a risk score based on likeli-

hood and impact, which in turn classifies the risk as either a “high”, “medium” or “low” risk. Based on this score, all risks are assigned a relevant risk response and/or mitigation actions.

The Classification of RisksLikelihood is calculated as:

Score Likelihood Description

1 < 5% Very Unlikely

2 5% - 10% Unlikely

3 10% - 20% Maybe

4 20% - 25% Possible

5 > 25% Likely

Impact is calculated as:

Score Impact (EURm) Description

1 < 25 Immaterial

2 25 – 50 Low

3 50 – 100 Medium

4 100 – 250 High

5 > 250 Critical

Based on the combined risk score (like-lihood x impact), risks are classified as:

Classifi-cation

Risk Score Suggested actions

Low < 7Monitor develop-ment to ensure expo-sure remains low

Medium

≥ 7

and

≤ 15

Mitigate and monitor risks to maintain current level of risk exposure

High > 15Implement miti-gating actions to reduce exposure

The updated Kinnevik and Portfolio Risk Registers are presented to the Risk Committee after which a final version is presented to the RCS Committee.

COMPANY ENGAGEMENTThe Investment, Sustainability and Cli-mate Teams engage with Kinnevik’s portfolio companies on a regular basis, including through the annual sustaina-bility assessment of our portfolio com-panies. The assessment focuses on the progress made in relation to the Kinnevik Standards. The Standards mirror our sus-tainability strategy and targets and were created to define best practice for our companies, measure performance and set priorities across the three dimensions of sustainability: environment, society and governance. In addition, in 2020 Kinnevik drove the implementation of a GHG emis-sions reporting tool in our companies (read more on page 9).

Kinnevik’s ”Our Group Platform” is a network of companies and people, and a forum for knowledge sharing and networ-king. Kinnevik uses this forum, and events and conferences organised in connection with it, to raise awareness and discuss our sustainability ambitions. During 2020, the Climate Team used this platform to strengthen our ongoing dialogue on climate-related disclosures and targets with our portfolio companies.

In this section we describe how Kinnevik identifies, assesses, and manages climate-related risks, in accordance with the TCFD reccomendations.

Identification Classification Mitigation Reporting

Kinnevik’s risk assessment process

Kinnevik AB ∙ TCFD Report ∙ 2020

9

METRICS & TARGETS

OUR CLIMATE TARGETSKinnevik is in a unique position to in-fluence our companies to identify and mitigate climate risk, seize opportunities related to climate change and make the transition into a low-carbon economy. In May 2020, Kinnevik announced climate targets in line with the Paris Agreement and the 1.5˚C ambition for Kinnevik and our portfolio. These are:

1. Net zero GHG emissions from Kinnevik’s own operations and bu-siness travel by 2020 and onward

2. 50% reduction in GHG emission intensity in Kinnevik’s portfolio by 2030 compared to 2020

Kinnevik’s GHG inventory is prepared in accordance with the GHG Protocol Corporate Accounting and Reporting Standard. The GHG Protocol classifies a company’s GHG emissions into three “scopes”. You can read more about the scopes on the next page.

Kinnevik’s scope 1 consists primarily of company owned/leased vehicles and scope 2 consists of district heating and electricity for our offices in Stockholm and London. Business travel (which consists almost entirely of air travel) accounted for [99]% of Kinnevik’s scope 3 and [95]% of our total emissions in 2020, and the pattern is similar throughout the last few years.

To achieve our first climate target, we will implement a more stringent travel policy for employees and an internal pricing structure on air travel reflecting the associated cost of offsetting GHG emissions. We will also move to electric or hybrid employee cars and implement a car policy with the aim of minimizing car travel. Unavoidable emissions will be offset to achieve net zero emissions. The offsetting will be done through a perma-nent carbon dioxide removal programme,

leveraging technology which enables capturing carbon dioxide from the air and storing it underground.

To achieve our second climate target, Kinnevik is driving the implementation of a GHG emission reporting tool across our portfolio in 2020. The reporting tool ena-bles us to report on the metrics recom-mended by TCFD such as total carbon emissions, carbon intensity and weighted average carbon intensity. Due to the high-growth nature of our portfolio, Kinnevik’s aggregated emissions reduction from the portfolio will be measured in relation to relevant intensity metrics (economic or physical, e.g. per unit of revenue or per product) across our portfolio companies. We will report the emission intensity in our portfolio split by sector in relation to number of companies and in relation to value of our portfolio. As 2020 will be the first year of measuring, progress can be assessed after the 2021 reporting cycle. In addition, during 2021 we will assist our companies in identifying relevant emis-sions reduction targets and we will drive transformation programmes in selected companies.

Part of the compensation of Kinnevik’s employees is linked to the portfolio com-panies’ overall sustainability performance.

CLIMATE-RELATED OPPORTUNITIESOur portfolio company Zalando set Sci-ence Based Targets in June 2020 and Tele2 has announced it is in the process of setting the same. These two companies accounted for 65% of our portfolio value as at 31 December 2020. We also expect that many of our other portfolio compa-nies will set relevant climate targets in line with the 1.5˚C ambition during 2021.

While climate change poses huge risks and challenges, we are convinced that it also poses a significant opportunity for Kinnevik and our portfolio companies to remain the preferred choice of their

increasingly climate conscious consumer base. Kinnevik believes that our compa-nies are well positioned with respect to the transition to a low-carbon economy. With our active support, our companies are increasingly taking action to reduce their environmental impact and impro-ve climate-related disclosures. During 2021, Kinnevik will continue to engage with our portfolio companies to support, encourage and influence them on their transformational journey towards making sustainability part of their core business models.

This section aims to disclose the metrics and targets Kinnevik use to assess and manage relevant climate-related risks and opportunities.

OUR CLIMATE IMPACTKinnevik conducts a yearly green-house gas emissions estimate which quantifies the total direct and indirect greenhouse gas emissions produced by our ope-rations. The estimate provides us with a tool to monitor and reduce our climate impact. Click here to read more about our emissions report for 2020.

MORE

Kinnevik AB ∙ TCFD Report ∙ 2020

10

Overview of Kinnevik’s greenhouse gas emissions 2016-2020

The GHG Protocol classifies a company’s GHG emissions into three “scopes”. Scope 1 emissions are direct emissions from owned or controlled sources. Scope 2 emissions are indirect emissions from the generation of purchased energy. Scope 3 emissions are all indirect emissions (not included in scope 2) that occur in the value chain of the reporting company, including both upstream. Kinnevik’s emissions inventory for 2016-2020 does not include our portfolio companies’ emissions, and therefore scope 3 emissions consists mainly of business travel.

591 602645

511

91

SCOPE 1

SCOPE 2

SCOPE 3

Kinnevik’s GHG emissions (tonnes CO2e) 2016 2017 2018 2019* 2020

Scope 1 37 11 17 17 12

Scope 2 7 15 9 7 5

Scope 3 547 577 619 487 74

Total 591 602 645 511 91

Per full time equivalent employee 14.8 16.1 17.6 12.8 2.3

Per square metre office space 0.766 0.78 0.835 0.662 0.118

* 2019 data restated due to updated emissions factors and methodology to better align with the GHG Protocol.

Kinnevik AB ∙ TCFD Report ∙ 2020

11

APPENDIX CLIMATE RISKS AND OPPORTUNITIES

CONSUMER SERVICESFor online fashion and groceries, we be-lieve the opportunities of a more climate conscious customer base are imminent and clear. The companies that do not ma-nage to integrate climate opportunities into their core business models will risk being outpaced by competitors.

For our online fashion companies there is a growing business opportunity in offering customers new ways of enjoy-ing fashion which also result in reduced climate impact and increased customer loyalty. This includes local production, rental, second-hand products, clothing care and repairs to extend the life of the garments. By using advanced analytics and artificial intelligence to develop more precise purchasing practices, the offe-ring can be made even more relevant to customers. Supply and demand can be more precisely aligned, helping to avoid overproduction and unnecessary transportation, thereby reducing climate impact. On the other hand, acute physical risks, such as severe weather events or di-sease, could lead to disruption in produc-tion and distribution. Extreme weather could affect major transport nodes in the supply chain. The consequences could include reduced product availability for customers and therefore have a negative impact on sales. However, our online fa-shion companies operate a marketplace business model, which means they have very little own production. No material supply chain of their own means less di-rect exposure to physical risks.

For our online food companies, in-creasing awareness of the climate crisis is shifting customer preferences towards providers with transparency around car-bon footprint and that operate with a low climate impact, both up- and downstream. Acute physical risks can affect agricultural production, production of semi-finished goods, increase costs of maintenance and repair of damaged buildings, delay or

hinder deliveries to end-consumers and cause inventory loss from damage and spoiled food during power outages or extreme heat. Chronic physical risks such as temperature rise could affect energy costs by requiring air conditioning and refrigeration systems to work harder or longer – using more energy to maintain appropriate temperatures in facilities.

For our travel companies, the main climate risk, apart from policy and legal risks, relates to the stigmatisation of air travel. Increasing local charges and emis-sions trading schemes, such as carbon emissions-based passenger taxes, will likely decrease demand for air travel. Pro-viding detailed information on carbon footprint for various flight options is a key opportunity. As is, when possible, the provision of easily accessible and trans-parent information on carbon footprint for other modes of transports such as buses, trains and ferries.

FINANCIAL SERVICESFor our financial services companies ope-rating in investments and savings, a key climate risk is a decrease in demand for products and funds that are not environ-mentally friendly. There is also a potential stigmatisation of products with a high climate impact, such as oil and gas, which could have an impact on assets under management and revenues. Offering products and funds with a low climate impact to meet the increased demand is a key opportunity. Demand for potentially climate controversial products is likely to persist to some degree however, which requires striking a balance.

HEALTHCARE SERVICESFour our healthcare companies, we main-ly see climate-related opportunities. With the increase in demand for low emission services, digital models are well-placed to meet shifting consumer and government preferences.

TMTFor our communications company, a key climate risk is the possibility of unsuccess-ful investments in new technologies to facilitate the transition into a low carbon business and thereby not meeting the emissions requirements and demand from consumers. Another risk is increased production costs due to increased energy costs. Increased awareness and pressure around climate impact will potentially result in reduced employee attraction and retention and capital availability unless companies are able to position them-selves as sustainability leaders. Acute and chronic physical risks is an issue for business continuity. It may also lead to increased costs due to for example in-creased cooling needs at facilities and office locations.

Climate change will most likely only increase the need and importance of connectivity resulting in increased re-venue if companies can also make the transition to climate focused products and services needed with in the TMT in-dustry. Other opportunities include use of more efficient production processes and lower-emission sources of energy. This may reduce operating costs as a transition into more efficient processes enables lower product prices.

This section contains detailed information on climate risks and opportunities for each of Kinnevik’s sectors and sub-sectors. This is a continuation of the strategy section starting on page 5.

Kinnevik AB ∙ TCFD Report ∙ 2020

12

APPENDIX SCENARIO ANALYSIS

In accordance with the TCFD recommen-dations, we have used scenario analysis as a method to better understand the potential effects of climate change on our business, strategy and financial planning under different potential future climate scenarios. It allows us to test the robust-ness and resilience of our strategy, to properly identify climate-related risks and opportunities and it provides gui-dance for capital allocation decisions. In addition, scenario analysis improves our external reporting and transparency and enables investors to make more informed decisions.

CLIMATE SCENARIOSThe Intergovernmental Panel on Climate Change (IPCC) explores different pat-hways of GHG concentration and, effec-tively, the amount of warming that could occur by the end of the century. These Representative Concentration Pathways (“RCPs”) are used for climate modelling and describes different climate futures depending on the volume of greenhouse gases (GHG) emitted in the years to come.

The RCPs should be considered in combination with the Shared Socioeco-nomic Pathways (SSPs), modelling how socioeconomic factors may change over the next century. These include for ex-ample population, economic growth, education, urbanisation and the rate of technological development. The SSPs look at five different ways in which the world might evolve in the absence of climate policy and how different levels of climate change mitigation could be achieved when the mitigation targets of the RCPs are combined with the SSPs.

We have selected two RCPs for our scenario analysis to reflect two very dif-ferent climate outcomes; the Stringent Mitigation Scenario (RCP2.6) where emis-sions are halved by 2050 in line with the Paris Agreement, and the Very High Emis-sions Scenario (RCP8.5) where emissions continue to rise at current rates. Climate researchers have found that RCP 2.6 is possible to achieve under three of the

SSPs (SSP1 Sustainability, SSP2 Middle of the Road and SSP4 Inequality), while the very high level of emissions associa-ted with RCP8.5 can only be achieved under one SSP (SSP5 Fossil-fuelled De-velopment). 1

In our description of RCP2.6 we have included the SSP1 narrative, and for RCP8.5 we have included the SSP5 nar-rative. Both climate scenarios stretch to the end of the century, however our sce-nario analysis extends to year 2050. While this is well beyond our strategic planning timeframe, it provides insights into broa-der trends that could have implications for our near- and mid-term decision making. Each of these plausible pathways are de-signed to stretch our strategic thinking about potential rates of new technology adoption, policy development and con-sumer behaviour.

RCP2.6 – The Stringent Mitigation ScenarioThis scenario implies a global tempe-rature rise of 0.9-2.3˚C relative to pre-industrial levels and is the scenario closest aligned with the Paris Agreement. In this scenario, businesses would be more im-pacted by policy changes and transition risks, rather than physical risks. RCP2.6 is characterised by:• Higher use of renewable energy sources

and lower energy consumption overall• Higher use of bioenergy and Carbon

Capture and Storage, resulting in ne-gative emissions

• Constant use of grasslands and in-creased use of croplands, but largely as a result of bioenergy production

• Greenhouse gas emissions culminate in year 2020, reach net zero by 2050 and are negative by 2100

• Significantly increased investments and fast-paced adoption of technolo-gies to combat climate change

• Highly stringent climate policiesImplications from this scenario includes significantly increased demand for ener-gy-efficient and lower-carbon products and services, an ever-evolving patchwork

of policy and legal requirements on inter-national and national level, and growing expectations for responsible conduct from stakeholders including investors, lenders and consumers.

SSP1 Sustainability: The world shifts gradually, but pervasively, toward a more sustainable path, emphasizing more inclu-sive development that respects perceived environmental boundaries. Management of the global commons slowly improves, educational and health investments ac-celerate the demographic transition, and the emphasis on economic growth shifts toward a broader emphasis on human well-being. Driven by an increasing com-mitment to achieving development goals, inequality is reduced both across and within countries. Consumption is oriented toward low material growth and lower resource and energy intensity.

RCP8.5 – The Very High Emissions ScenarioThis scenario implies a global tempera-ture rise of 3.2-5.4˚C relative to pre-indu-strial levels. In this scenario, human-driven climate change will be more evident, and businesses will be more impacted by physical climate risks. RCP8.5 is cha-racterised by :• Global population of 12 billion• High dependency on fossil fuels and

overall high energy consumption as a result of high population growth and lower rate of technology development

• Increase use of cropland and grass-lands, mostly driven by an increasing global population

• Greenhouse gas emissions are three times today’s levels

• Development of new technology will have progressed but at a slower rate

• All today’s announced policy intentio-nal are realised, but with no additional policies

Implications from this scenario include more extreme weather events such as heatwaves, flooding and wildfires, chan-ges in rainfall patterns and monsoon sys-tems, more acid oceans melting of arctic

This section contains detailed information on Kinnevik’s scenario analys . This is a continuation of the strategy section starting on page 7.

Kinnevik AB ∙ TCFD Report ∙ 2020

13

APPENDIX SCENARIO ANALYSIS

sea ice and sea level rises by a half to one meter. Like the Stringent Mitigation Sce-nario, demand for lower-carbon products and services, as well as expectations from stakeholders, are likely to increase from today’s levels, but not to the same extent.

SSP5 Fossil-fuelled Development: This world places increasing faith in competitive markets, innovation and participatory societies to produce rapid technological progress and development of human capital as the path to sustai-nable development. Global markets are increasingly integrated. There are also strong investments in health, education, and institutions to enhance human and social capital. At the same time, the push for economic and social development is coupled with the exploitation of abundant fossil fuel resources and the adoption of resource and energy intensive lifestyles around the world. All these factors lead to rapid growth of the global economy, while global population peaks and de-clines in the 21st century. Local environ-mental problems like air pollution are successfully managed. There is faith in the ability to effectively manage social and ecological systems, including by geo-engineering if necessary.

Methodology, Materiality and ProcessOur scenario analysis was conducted with the aim of testing our strategy and how it would likely perform under the two dif-ferent climate scenarios. Read more about our business strategy on page 5.

We started with a top-down analysis of our three focus sectors Consumer Ser-vices, Healthcare Services and Financial Services. Within Consumer Services, we focused on three sub-sectors; Food, Tra-vel and Last mile logistics. We modelled and analysed potential implications for the three sectors and sub-sectors under each of the two climate scenarios. Based on a materiality analysis, we have put par-ticular emphasis on those sectors and sub-sectors with the highest impact from climate-related risks and opportunities, as well as those that are most material to Kinnevik in terms of share of our portfolio value.

The analysis is predominantly qualita-tive or “directional” in nature, and is done

from Kinnevik’s perspective as an owner, as opposed to the portfolio companies’, and focuses on the implications on our business, strategy and financial planning. As an investment company, we do not have the level of insight into all our portfo-lio companies that an operating company would perhaps have into its own opera-tions, which creates an uncertainty factor.We have focused primarily on market, reputation and technology risks as those are the most pressing for our portfolio of digital companies. We have also looked at some physical risks for the businesses in our portfolio with more complex and international supply chains.

Following the top-down analysis, we conducted a more in-depth analysis of each sector together with the respective responsible Investment Manager. For this report, we have focused on the findings in two specific sectors, Food and Health-care. These face some of the most evident impacts in each of the climate scenarios – Food faces both climate-related risks and opportunities in both scenarios while Healthcare see primarily climate-related opportunities in the Stringent Mitigation Scenario. These sectors also form a core part of our strategy and capital alloca-tion plan.

As per 31 December 2020, the fair value of Kinnevik’s food companies was SEK 2.8bn, corresponding to 2.6% of our total portfolio value. The fair value of Kinnevik’s healthcare companies was SEK 21.3bn, corresponding to 2% of our total portfolio value.

To present and challenge the results of the scenario analysis, a workshop with the Risk Committee was held in February 2021, after which they were presented to the RCS Committee in March 2021.

ROBUSTNESS AND RESILIENCE OF OUR STRATEGY IN EACH SCENARIOThe scenario analysis provides us with important input on our business, strategy and financial planning. Our strategy is to invest in digital companies operating pri-marily a marketplace model, and as such, with the exception of food, our portfolio generally has relatively low dependency on complex supply chains, physical as-

sets and fossil fuels. As such, our strategy shows relative resilience in the face of a Very High Emissions Scenario. However, in a Very High Emissions Scenario the overall benefits of sustainability and low-emissions services will not be recognized by a majority of consumers which means that sustainability will not be considered a competitive advantage.

As an investor in consumer-facing sectors, Kinnevik is exposed to a broad set of transition risks associated with the Stringent Mitigation Scenario, particular-ly related to market and reputation, i.e. shifting consumer behaviour as a result of increased climate consciousness and overall decrease in discretionary con-sumption. Meanwhile, this scenario also offers the largest climate-related oppor-tunities with regards to Kinnevik’s strategy to invest in digital companies disrupting legacy industries through innovation and new technology.

Kinnevik AB ∙ TCFD Report ∙ 2020

14

APPENDIX SCENARIO ANALYSIS

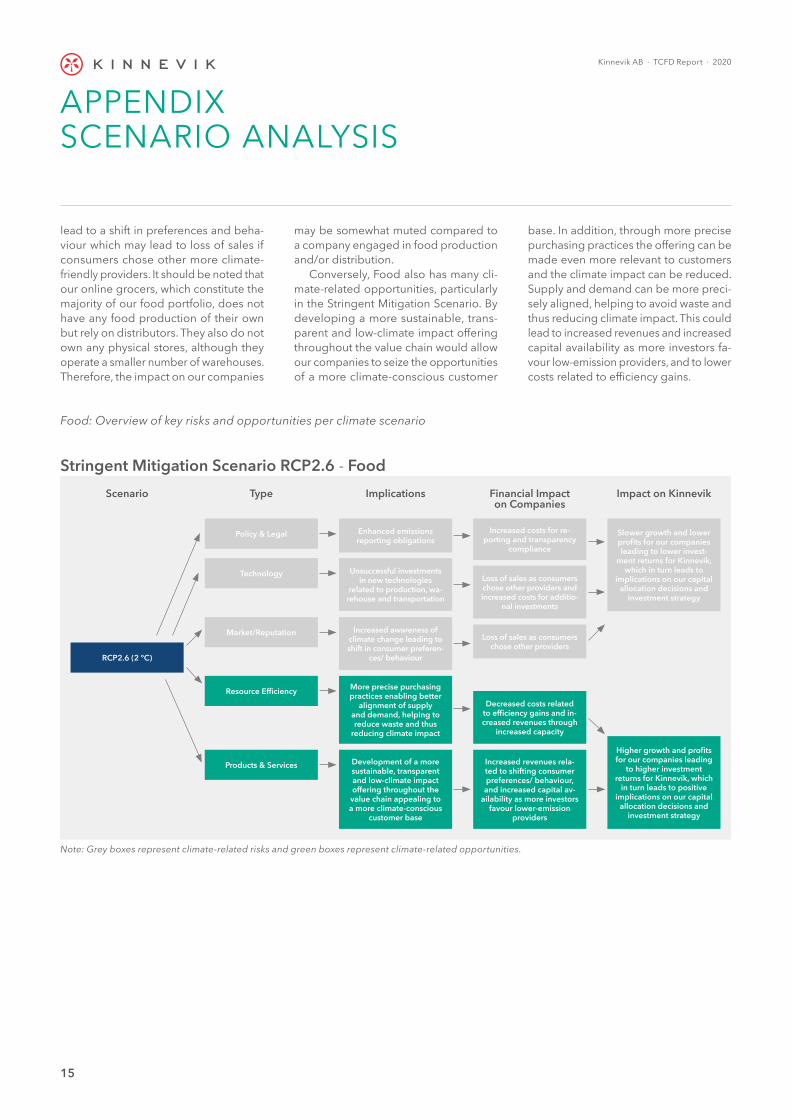

FoodThe production and transportation of food is one of the major climate chal-lenges accounting for 25% of emissions in developed countries. It is a sector which will need to transition fast and which will play a material role in our ability to ac-hieve the EU’s net zero emissions goal by 2050.

The food sector stands out in the scenario analysis as, in the Very High Emissions Scenario, increased severity of extreme weather events can lead to disruptions in production, transportation

and distribution. Increasing temperatures may affect cultivation possibilities and increases energy need. This could lead to a loss of sales due to lack of product availability and/or increased consumer prices, increased costs for repairing damaged facilities, inventory loss and increased insurance premiums. It could also lead to increased costs for energy (cooling and air conditioning) and pro-duct procurement. Further, in a Very High Emissions Scenario, sustainability is not recognized by consumers as expected, which will impact food businesses that

currently have a clear sustainability profile and/or strategy.

In the Stringent Mitigation Scenario, enhanced reporting obligations may lead to increased costs for reporting and transparency compliance. Unsuccessful investments in production, warehouse and transportation technologies could lead to loss of sales as consumers may chose other providers, and to increased costs for additional investments to align with a low-carbon economy. And perhaps most importantly, increased awareness of climate change among consumers may

Food: Overview of key risks and opportunities per climate scenario

Slower growth and lower profits for our companies leading to lower invest-

ment returns for Kinnevik, which in turn leads to

implications on our capital allocation decisions and

investment strategy

Increased costs for energy (cooling and air conditio-ning) and increased costs for product procurement

Loss of sales due to lack of product availabi-

lity/ increased consumer prices, increased costs for repairing damaged facilities, inventory loss

and increased insurance premiums

Increasing temperatures affecting cultivation pos-

sibilities and increases energy need

Increased severity of extreme weather events leading to disruptions in production, transporta-

tion and distribution

Scenario Type Implications Financial Impact on Companies

Impact on Kinnevik

Very High Emissions Scenario RCP8.5 - Food

Chronic

Acute

RCP8.5 (4 °C)

Note: Grey boxes represent climate-related risks and green boxes represent climate-related opportunities.

Kinnevik AB ∙ TCFD Report ∙ 2020

15

lead to a shift in preferences and beha-viour which may lead to loss of sales if consumers chose other more climate-friendly providers. It should be noted that our online grocers, which constitute the majority of our food portfolio, does not have any food production of their own but rely on distributors. They also do not own any physical stores, although they operate a smaller number of warehouses. Therefore, the impact on our companies

may be somewhat muted compared to a company engaged in food production and/or distribution.

Conversely, Food also has many cli-mate-related opportunities, particularly in the Stringent Mitigation Scenario. By developing a more sustainable, trans-parent and low-climate impact offering throughout the value chain would allow our companies to seize the opportunities of a more climate-conscious customer

base. In addition, through more precise purchasing practices the offering can be made even more relevant to customers and the climate impact can be reduced. Supply and demand can be more preci-sely aligned, helping to avoid waste and thus reducing climate impact. This could lead to increased revenues and increased capital availability as more investors fa-vour low-emission providers, and to lower costs related to efficiency gains.

Slower growth and lower profits for our companies leading to lower invest-

ment returns for Kinnevik, which in turn leads to

implications on our capital allocation decisions and

investment strategy

Higher growth and profits for our companies leading

to higher investment returns for Kinnevik, which

in turn leads to positive implications on our capital

allocation decisions and investment strategy

Increased costs for re-porting and transparency

compliance

Enhanced emissions reporting obligations

Unsuccessful investments in new technologies

related to production, wa-rehouse and transportation

Loss of sales as consumers chose other providers and increased costs for additio-

nal investments

Increased awareness of climate change leading to shift in consumer preferen-

ces/ behaviour

Loss of sales as consumers chose other providers

More precise purchasing practices enabling better

alignment of supply and demand, helping to reduce waste and thus

reducing climate impact

Decreased costs related to efficiency gains and in-creased revenues through

increased capacity

Development of a more sustainable, transparent and low-climate impact offering throughout the value chain appealing to a more climate-conscious

customer base

Increased revenues rela-ted to shifting consumer preferences/ behaviour, and increased capital av-

ailability as more investors favour lower-emission

providers

Scenario Type Implications Financial Impact on Companies

Impact on Kinnevik

Stringent Mitigation Scenario RCP2.6 - Food

Resource Efficiency

Products & Services

Policy & Legal

Technology

Market/Reputation

RCP2.6 (2 °C)

Food: Overview of key risks and opportunities per climate scenario

Note: Grey boxes represent climate-related risks and green boxes represent climate-related opportunities.

APPENDIX SCENARIO ANALYSIS

Kinnevik AB ∙ TCFD Report ∙ 2020

16

APPENDIX SCENARIO ANALYSIS

HealthcareHealthcare accounts for 5% of emissions in developed countries, however digital models have an inherently lower depen-dency on fossil fuels compared to tradi-tional players. The increased adoption of digital and value-based healthcare can play a significant role in making health-care more efficient and decreasing emis-sions from the healthcare sector.

In the Very High Emissions Scenario, increased severity of extreme weather events may lead to disruptions in supply chain for medical equipment and medici-ne, which could result in loss of sales from

decreased capacity for our value-based care providers. Increasing temperature and rising sea levels may affect the ability to treat and offer services for new and unknown conditions. This may particularly impact our value-based care provides as they enter into risk-sharing contracts with providers, meaning they take full risk on a patient’s health. This may cause increased operating costs and have a negative effect on profits. This risk will to a large extent depend on how quickly governments and insurance providers are able adapt to new and unknown conditions and a potential shift in the overall health spend.

However, in the Stringent Mitigation Scenario, there are some clear climate-related opportunities. Digital providers generally have a smaller footprint com-pared to traditional incumbents. Further-more, our value-based care providers aim to make healthcare more efficient and preventative, as opposed to relying too heavily on acute care which is more costly and has a higher climate impact. Increased consumer demand for lower emission healthcare services, as well as use of new technologies and supportive policy incentives, may lead to increased revenues.

Healthcare: Overview of key risks and opportunities per climate scenario

Chronic

AcuteSlower growth and lower profits for our companies leading to lower invest-

ment returns for Kinnevik, which in turn leads to

implications on our capital allocation decisions and

investment strategy

Reduced revenue from decreased production

capacity, and increased costs

Increased severity of extreme weather events leading to disruptions in supply chain for medical equipment and medicine

Increasing temperature and rising sea levels af-

fecting ability to treat and offer services for new and

unknown conditions

RCP8.5 (4 °C)

Scenario Type Implications Financial Impact on Companies

Impact on Kinnevik

Very High Emissions Scenario RCP8.5 - Healthcare

Note: Grey boxes represent climate-related risks and green boxes represent climate-related opportunities.

Stringent Mitigation Scenario RCP2.6 - Healthcare

Slower growth and lower profits for our companies leading to lower invest-

ment returns for Kinnevik, which in turn leads to

implications on our capital allocation decisions and

investment strategy

Higher growth and profits for our companies leading

to higher investment returns for Kinnevik, which

in turn leads to positive implications on our capital

allocation decisions and investment strategy

Increased operating costs

Increased revenues rela-ted to shifting consumer preferences/ behaviour, and increased capital av-

ailability as more investors favour lower-emissions

providers

Inability to adapt to shifting government

structures

Use of new technologies and supportive policy

incentives

Increased demand for more efficient and lower

emission healthcare services

Scenario Type Implications Financial Impact on Companies

Impact on Kinnevik

Products & Services

Energy Source

RCP2.6 (2 °C)

Kinnevik AB ∙ TCFD Report ∙ 2020

17

CONCLUSIONBased on our scenario analysis, the sce-nario with the largest potential negative impact on Kinnevik’s business, strategy and financial planning is the Very High Emissions Scenario. The most favourable scenario is conversely the Stringent Mi-tigation Scenario, as the climate-related opportunities facing our portfolio in this potential future would likely outweigh the climate-related risks.

Potential Impact and Effects on Our StrategyThe climate-related risks identified in both scenarios for the food sector, and

primarily in the Very High Emissions Sce-nario for the healthcare sector, may lead to slower growth and lower profits for our companies leading to lower investment returns for Kinnevik, which in turn may lead to implications on our investment strategy and capital allocation decisions.

The key climate-related risks and opp-ortunities for Kinnevik under the Stringent Mitigation Scenario is related to more climate-conscious consumers and more stringent climate policies. In this scenario, our strategy may be affected as we may put increasing emphasis on climate as-pects in capital allocation decisions, and increasingly look to invest in companies

that will thrive in a low-carbon economy. The key climate-related risks in the Very High Emissions Scenario relate to physical risks i.e. adverse effects on businesses with complex supply chains, such as in the Food sector. In this scenario, our strategy may be affected as we may decrease our exposure to these types of assets.

APPENDIX SCENARIO ANALYSIS

For an in-depth description of Kinnevik including our strategy,team and investee companies, please refer to www.kinnevik.com