understanding the sweeping changes to duty … nei...speakers 3 •david corn is a vice president...

TRANSCRIPT

Understanding the Sweeping

Changes to Duty Drawback

July 28, 2016

Presented by: Michael Cerny, David Corn, and Bobby Waid

Speakers

2

• Michael V. Cerny is Chief Executive Officer and General Counsel of Global Customs & Trade Specialists, Inc., a licensed Customs broker specializing in duty drawback services and duty refund programs. Mr. Cerny is also an attorney and managing principal of Cerny Associates, P.C., a law firm focused exclusively on customs and trade law.

• Mr. Cerny is the Chair of the Drawback Committee for the National Customs Brokers & Forwarders Association of America. He was selected by U.S. Customs & Border Protection to serve as a Trade Ambassador as part of the Trade Support Network (TSN), and he is also the Chair for the TSN Subcommittee on Drawback, Co-Chair of the TSN Legal Policy Committee, and a member of the TSN Entry Committee. Mr. Cerny is Co-Chair of the Drawback and Duty Deferral Committee of the American Association of Exporters & Importers, as well as a member of that organization’s Nominating Committee. Mr. Cerny is admitted to the United States Court of International Trade and is a member of the Customs & International Trade Bar Association, the American Bar Association Section of International Law & Practice, the New York State Bar Association, and the Association of the Bar of the City of New York.

• Mr. Cerny received a Bachelor of Arts degree from the University at Albany, where he also played varsity lacrosse for the Albany Great Danes. He received his J.D. degree from Albany Law School.

Speakers

3

• David Corn is a Vice President with Comstock & Theakston Inc., starting his drawback career in 2011. David was appointed to the co-chair position of AAEI's Drawback and Duty Deferral Committee in 2015 and is active on the NCBFAA Drawback Committee. He also serves on a working group for the Trade Support Network that is coordinating efforts with CBP to write the new drawback CATAIR to fulfill the user requirements for ACE. Mr. Corn has discussed drawback legislation with congressional representatives from NJ, NY, CT, the House Ways and Means Committee and the Senate Finance Committee.

• Mr. Corn has a Bachelor of Science degree from The Ohio State University in Consumer Affairs and is a Licensed Customs Broker.

Speakers

4

• C.R. "Bobby" Waid is Chief Executive Officer for Charter Brokerage LLC, a firm that provides 3PL services to improve trade flows and to recover costs for its clients. Charter's 3PL services include Customs Brokerage, Freight Forwarding, and Duty Drawback for a number of end-markets, including petroleum and petrochemicals.

• Mr. Waid is active with issues affecting these industries and participates within trade committees such as the American Petroleum Institute, American Association of Exporters and Importers, National Customs Brokers and Freight Forwarders Association, and the Trade Support Network.

• Mr. Waid received a B.B.A. in Accounting from the University of Houston and is a licensed customs broker.

The Purpose of Drawback

• Drawback is the last remaining export promotion program that is sanctioned by the World Trade Organization/GATT

• As stated by Congress, “[t]he rationale for drawback has always been to encourage American commerce or manufacturing, or both. It permits the American manufacturer to compete in foreign markets without the handicap of including in his costs, and consequently in his sales price, the duty paid on imported merchandise.” See the Legislative History Report of the Customs Mod Act from the House Ways and Means Committee, House Report 103-361, 103d Cong., 1st Sess. (1993)

• Customs states that “[t]he purpose of drawback is to enable a manufacturer to compete in foreign markets. To do so, however, the manufacturer must know, prior to making contractual commitments, that he will be entitled to drawback on his exports. The drawback procedure has been designed to give the manufacturer this assurance and protection.” http://www.customs.gov/xp/cgov/import/cargo_control/ftz/about_ftz.xml.

5

Why Change Drawback?

• One word – simplification • Streamline a process

• Move to 8-digits

• Make it user friendly and less complex

• Decrease the cost and administrative burden for both CBP and manufacturers/exporters

6

Taking Effect

• When does the new law take effect? • Subsection (q) of the new law states that the amendments made by Section

906 take effect • On the date of enactment, and

• “apply to drawback filed on or after the date that is 2 years after such date of enactment.”

• However, there is a transition rule which says that for one year after the date that filings can be made under the new law, drawback claims can be filed under the new law (1313 as amended) or the old law (1313 prior to the amendments)

• Application of the new law is not subject to the operation of ACE

7

Current

• Same kind and quality

• Receipt and use requirements

• Rulings

• CDs and CMs required

Future

• 8-digit HTS number (aligns to new

ACE system, no need to trace

“other”)

• No tracking of receipt date and

broader time limit requirement on

use

• Reduced rulings

• Need to show business records for

transfer of merchandise (directly*

or indirectly* from importer)

* Definitions outlined in 1313(z)

8

Manufacturing Substitution Drawback

9

Current

• Bills of Material (BOM) not

required by statute to be

submitted with claim

• BOM calculation at unit level

Future

• BOM required to be submitted

with substitution manufacturing

claims

• BOM calculation at HTS level as

value of imported designated and

substituted merchandise (aligns

with ACE records that are

required)

Manufacturing Substitution Drawback

Manufacturing Drawback Calculations

• 1313(a) & 1313(b) calculations are now found in 1313(l) • For manufacturing direct identification, will be equal to 99% of duties, taxes,

and fees paid on the imported merchandise

• Need specific definitions in new regulations for average per unit on the entry summary line item

• Can collect taxes and fees

10

Manufacturing Substitution Drawback Lesser-of Calculation

• “The regulations required by subparagraph (A) for determining the calculation of amounts refunded as drawback under this section shall provide for a refund of equal to 99 percent of the duties, taxes, and fees paid on the imported merchandise incorporated into an article that is exported or destroyed….except that where there is substitution of the imported merchandise, then- • i. in the case of an article that is exported, the amount of the refund shall be equal to

99 percent of the lesser of- • (I) the amount of duties, taxes, and fees paid with respect to the imported merchandise; or • (II) the amount of duties, taxes, and fees that would apply to the substituted merchandise if

the substituted merchandise were imported;”

• AND • If destruction only, reduced by the value of the materials recovered during destruction

11

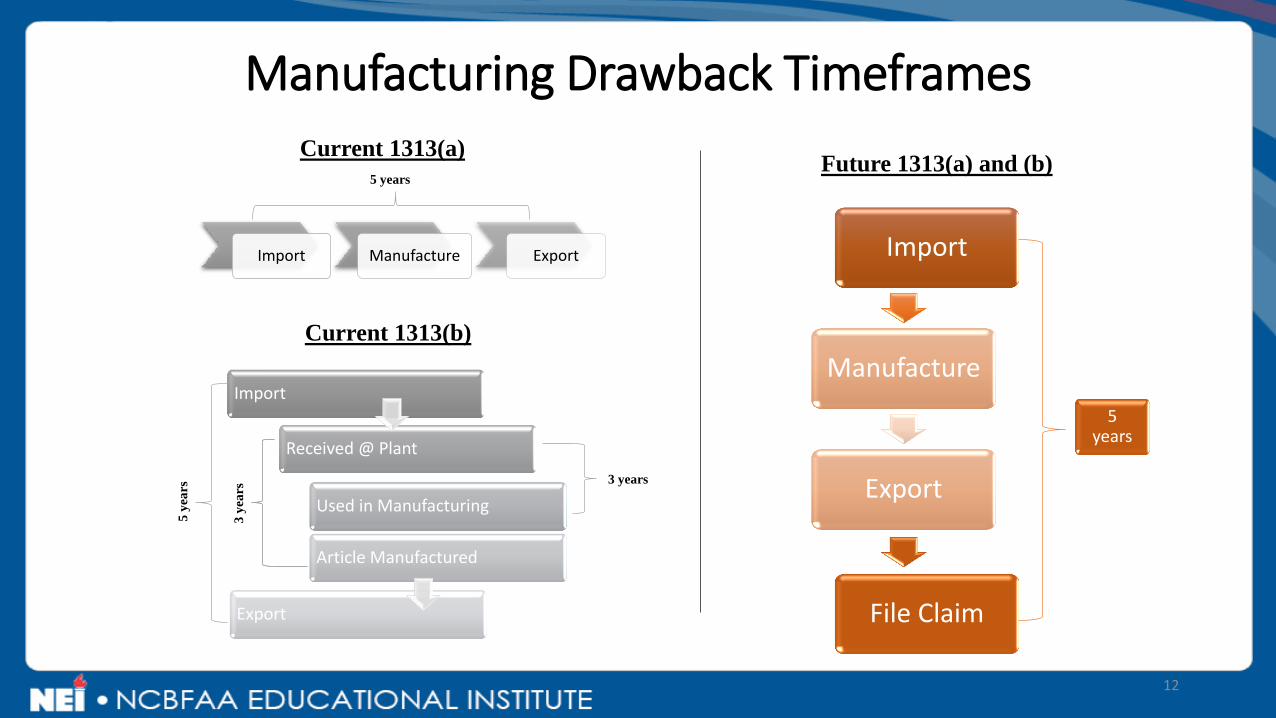

Import

Manufacture

Export

File Claim

5 years

Future 1313(a) and (b)

Import Manufacture Export

Current 1313(a)

Current 1313(b)

Import

Received @ Plant

Used in Manufacturing

Article Manufactured

Export

5 years

3 years

5 y

ears

3 y

ears

12

Manufacturing Drawback Timeframes

Manufacturing Substitution Drawback Sought Chemical Elements

• Statute has special provision to protect sought chemical elements within 8-digit substitution (tied to calculation subsection (l))

• Sought elements in today’s world with apportioned quantity

13

Import and designate titanium sponge (99kg pure)

• Or substitute scrap (99kg pure titanium)

Use any combination of sponge and scrap

Export article containing 99kg pure

titanium

Apportion duty paid on 100kg of sponge with

99% duty to pure titanium content

Manufacturing Substitution Drawback Sought Chemical Elements

• Lesser-of provision was added late

• Intent was to leave the apportionment to be based on the value of the metal is the substituted material, not based on duty alone

• Regulations should clarify based on value

14

Substitution Unused Merchandise Drawback 1313(j)(2)

• Standard for substitution is 8-digit HTS, not commercial interchangeability

• Limitations if your 8-digit HTS starts with “other”

• 5 years import to claim

• No more Certificates of Delivery

• New rules for calculating drawback amount

• Consider value of exported/destroyed items

• Drawback for recovered materials

15

1313(j)(2) Drawback What does 8-digit substitution mean?

• It means just that, same 8-digit HTS in and out

• Schedule B can be used at export, and it could be broader- “without regard to whether the Schedule B number corresponds to more than one 8-digit HTS subheading”

• Your Entry Summary could have an incorrect HTS, but still qualify for drawback (PEAs, Protests, Disclosures, Rulings, Court Cases)

• Previous CIDs and CI rulings are irrelevant

• No need for CIDs- obtain a classification ruling

16

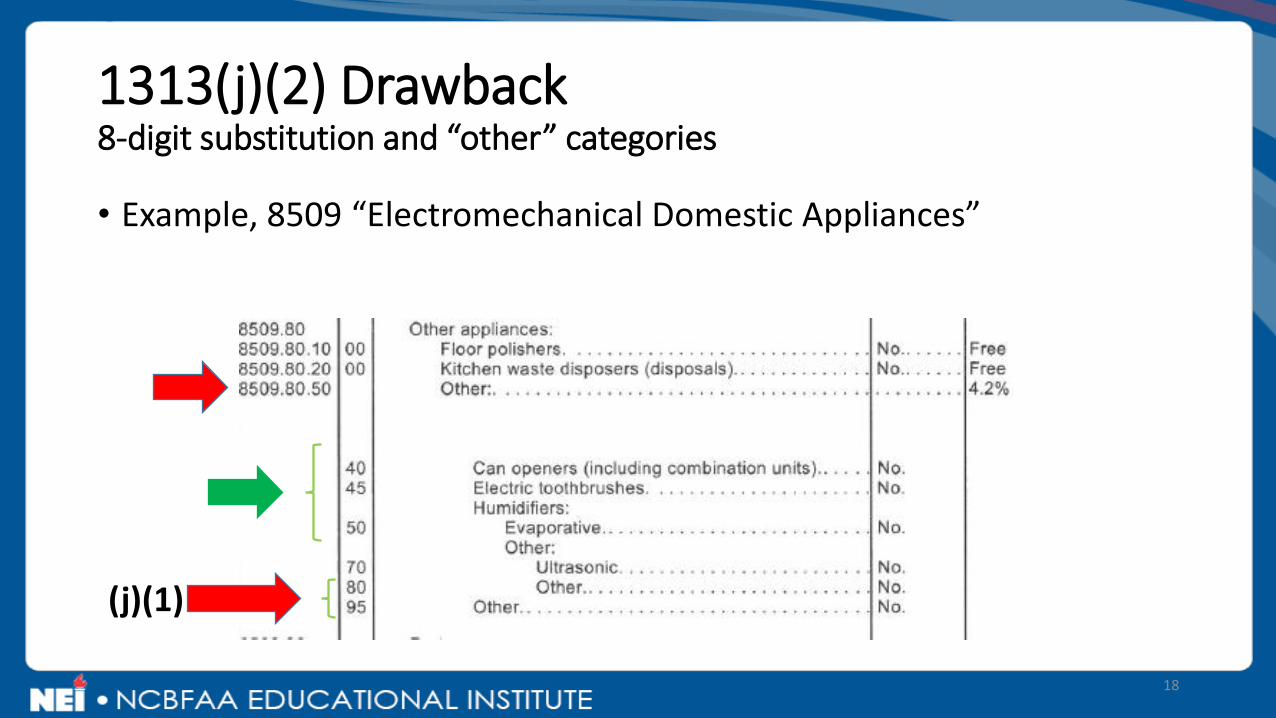

1313(j)(2) Drawback 8-digit substitution and “other” categories

• What is this about? Basket Provisions

• You may not be able to use j2 if your 8-digit HTS starts with the word “other”

• However, you can use j2 if your 8-digit HTS has 10 digit breakouts and you product’s breakout doesn’t start with the word “other.”

• If your 10 digit HTS begins with “other,” then you can only claim drawback under 1313(j) using j1.

17

• Example, 8509 “Electromechanical Domestic Appliances”

18

(j)(1)

1313(j)(2) Drawback 8-digit substitution and “other” categories

1313(j)(2) Drawback New Statutory Time Requirements

• Current Law:

• New Law:

19

Date of Import Date of Export

3 Years

Date of Claim

3 Years

Date of Import Date of Export

5 Years

Date of Claim

1313(j)(2) Drawback Certificates of Delivery Eliminated

• “Transfers of merchandise may be evidenced by business records kept in the normal course of business and no additional certificates of transfer shall be required.”

20

1313(j)(2) Drawback What does this mean?

• You do not need CDs under the new law

• Transfers need only be evidenced by business records kept in the normal course of business, such as invoice and shipping records (what, by whom, to whom, when)

• Must be received “directly” or “indirectly” (intermediate transfers) from the importer

• With joint and several liability, some importers may feel more comfortable with agreements and some type of transfer records (a private CD?)

21

1313(j)(2) Drawback Calculating Drawback – 1313(l)

• Every drawback provision now points to (l) for the drawback calculation.

• 1313(l)(2)(A): • “Not later than the date that is 2 years after the date of the enactment of the

Trade Facilitation and Trade Enforcement Act of 2015 (or, if later, the effective date provided for in section 606(q)(2)(B) of that Act), the Secretary shall prescribe regulations for determining the calculation of amounts refunded as drawback under this section.”

22

1313(j)(2) Drawback Calculating Drawback – 1313(l)

• The regulations required by subparagraph (A) for determining the calculation of amounts refunded as drawback under this section shall provide for a refund of equal to 99 percent of the duties, taxes, and fees paid on the imported merchandise, which were imposed under Federal law upon entry or importation of the imported merchandise, and may require the claim to be based upon the average per unit duties, taxes, and fees as reported on the entry summary line item, or if not reported on the entry summary line item, as otherwise allocated by U.S. Customs and Border Protection

23

1313(j)(2) Drawback This means:

• Customs must write regulations to explain calculation of drawback

• They must provide for an amount equal to 99% of the duties, taxes, and fees paid

• Customs can choose to issue regulations providing for calculation of duties, taxes and fees based upon the average line item amount

24

1313(j)(2) Drawback

• You are limited to no more than drawback of 99% of the duties, taxes, and fees that would apply to the exported or destroyed merchandise.

25

However, for substitution, the calculation is limited by

the value of the exported/destroyed item

1313(j)(2) Drawback What does this do?

• You can’t import an expensive race car and then export an economy car and get the full duty, taxes and fees on the race car. You are limited by the value of the economy car.

• Another example: Montblanc for BIC pen

26

1313(j) Drawback 1313(x) Recovered Materials – now applies to (j)

• For purposes of subsections (a), (b), (c), and (j), the term ‘destruction’ includes a process by which materials are recovered from imported merchandise or from an article manufactured from imported merchandise. In determining the amount of duties to be refunded as drawback to a claimant under this subsection, the value of recovered materials (including the value of any tax benefit or royalty payment) that accrues to the drawback claimant shall be deducted from the value of the imported merchandise that is destroyed, or from the value of the merchandise used, or designated as used, in the manufacture of the article.

27

Direct Identification, 1313(j)(1) Drawback What has changed?

• Same 5-year time frame

• Likely same drawback calculation under (l) (same condition?)

• CDs are eliminated

• Will be claimed by only (1) those with 8-digit HTS numbers that fail the “other” rule, (2) those who otherwise can’t use substitution (3) those with same condition under NAFTA and US-Chile, and (4) those folks who want to punish themselves.

28

1313(c) Merchandise Not Conforming to Sample or Specification • Amendments to synchronize with new concepts

• Eliminating certificates of delivery

• Changing timeframe from 3 years to 5 years

• Changing “the Customs Service” to “U.S. Customs and Border Protection”

• Refund amount will be determined by calculation language in 1313(l)

• Evidence of Transfers by ordinary business records

29

1313(p) Substitution of Petroleum Products

• Amendments to synchronize with new concepts • Changing “Harmonized Tariff Schedule of the United States” to “HTS”

• Eliminating certificates of delivery

• Evidence of Transfers by ordinary business records

30

Proof of Exportation

• Amendments to 1313(i) • Proof of exportation shall establish fully the date and fact of exportation and

the identity of the exporter

• Records to meet the above can be:

• (1) Records kept in normal course of business; or

• (2) Electronic export system of the U.S. as determined by U.S. Customs and Border Protection

31

Liability for Drawback Claims

• Amendments to 1313(k) • Any person making a claim for drawback shall be liable for the full amount

claimed

• Liability for Importers will be lesser of • (1) amount claimed with respect to the imported merchandise; or

• (2) amount that the importer authorized other person to claim with respect to the imported merchandise

• Joint and Several Liability

32

Recordkeeping Time Frame What has changed?

• The current law is three years from date of payment.

• Today, many claims are paid accelerated and can take more than 3 years to liquidate. A desk review can actually be made AFTER the recordkeeping time frame has expired.

• Under new law, it is 3 years from the date of liquidation of the claim.

• This could be a period of time than is required now, but it will also ensure that records are kept through liquidation.

33

What About Regulations?

• The new Subsection (l)(2) of Section 313 requires CBP to prescribe regulations: • Within 2 years after the date of enactment - February 24, 2018, and

• That determine the calculation of amounts to be refunded as drawback under the new law.

• The new law is a statutory change, and CBP must prescribe regulations to implement the new law • Expect an NPRM

• The need for CBP and the Trade to work together in drafting

• Congressional oversight will be part of the process

34

Yet Another Government Report…

• Subsection (p): Government Accountability Office Report to be completed one year after issuance of the regulations • Assessment of modernization of drawback and refunds under the new law

• Description of permissible claims before and after the effective date and identification of the affected industries

• Description of drawback claims not permissible before the effective date that are now permissible and the affected industries

• Study to be submitted to Ways & Means and Finance Committees

• Why a GAO study?

35

36

Questions and Contact Information

• Michael Cerny Global Customs & Trade Specialists, Inc.

24 Smith Street

Building 2, Suite 101

Pawling, NY 12564

(845) 855-4200 x8901

• David Corn Comstock & Theakston, Inc.

466 Kinderkamack Road

Oradell, NJ 07649

(201) 967-1220 x103

• Bobby Waid Charter Brokerage

22762 Westheimer Parkway

Suite 530

Katy, TX 77450

(281) 599-1252 x203