union budget : 2016 -17 pre–budget...

TRANSCRIPT

UNION BUDGET : 2016 - 17PRE–BUDGET MEMORANDUM

Issues, Concerns & Submissions of

Indian Tyre Industry

1

Indian Tyre Industry

Submitted to:

Ministry of Finance, Government of India

Note by;

AUTOMOTIVE TYRE MANUFACTURERS’ ASSOCIATION (ATMA)PHD House, 4th Floor, Opp. Asian Games Village, New Delhi–110016

Tel: 011- 2685 1187 / 2656 4291, Fax: 011- 26864799E-Mail: [email protected], [email protected], Website: www.atmaindia.org

ContentsContents

• Indian Tyre Industry - A Profile

• Industry Environment & Outlook

- Auto Sector

- Tyre Industry (Including Capacity & Investment by Tyre Industry)

Key Issues / Major Concerns of the Indian Tyre IndustryKey Issues / Major Concerns of the Indian Tyre Industry

- Natural Rubber : Inverted Duty Structure

- Major Raw Materials of Tyre Industry

- Demand Supply Gap

- Duty Structure – Existing &Proposed

- Customs Duty on Tyres

• ATMA Submissions 2

Indian Tyre Industry 2015Indian Tyre Industry 2015--16 16 –– A ProfileA Profile

• No. of Tyre Companies - 39

• No. of Tyre Plants - 60

• Turnover + - Rs. 53,000 crores

• Export in value + - Rs. 10500 crores

• Production - 1461 Lakh / Nos• Production - 1461 Lakh / Nos

• Exports - 86.80 Lakh/Nos

• Imports - 96 Lakh/Nos

• Product Profile - From Moped Tyres (weighing 1.5 kg) to Giant Earthmover Tyres (weighing over 1.5

Tons), Steel Belted Radial Truck Tyres, High Performance Tubeless Passenger Car Tyres and Tyres for Fighter Aircraft of Indian Air Force

3

ATMA Member Companies ATMA Member Companies

11 Large Co's (comprising of)

- Global MNCs

- Indian Tyre Co's (having presence overseas)

- Leading Indian Players

• (accounting for) 90%+ of Industry (in Value/Tonnage)

4

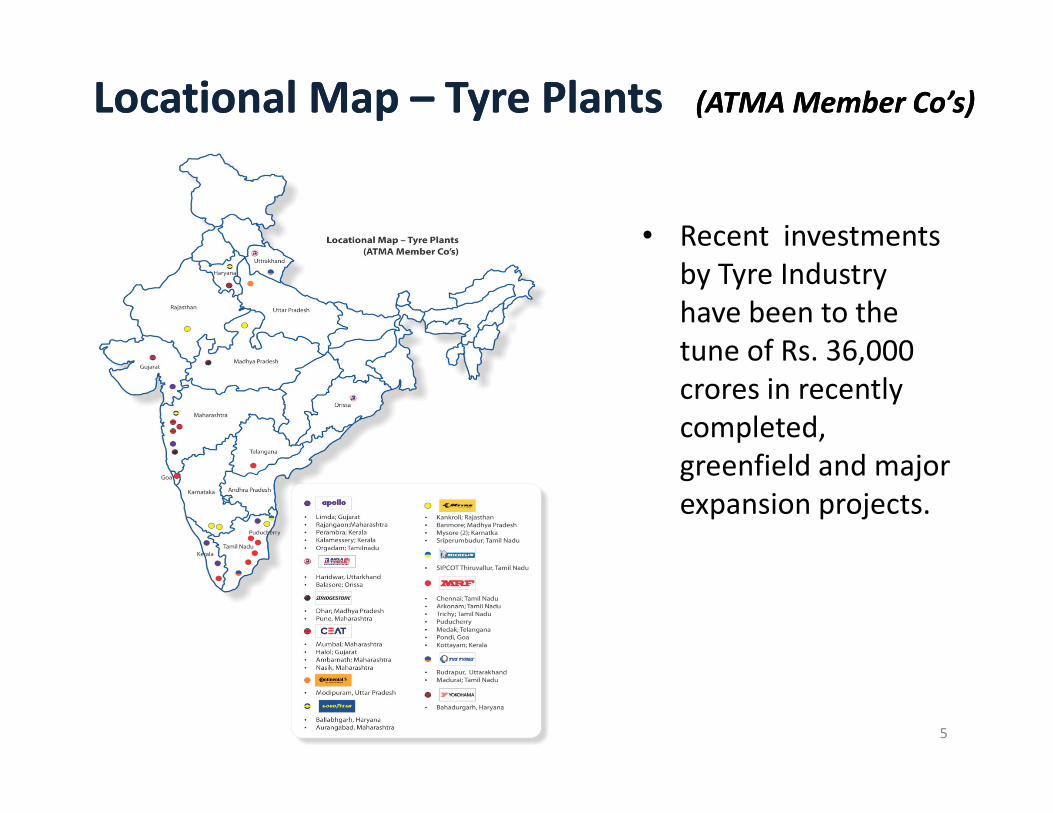

LocationalLocational Map Map –– Tyre Plants Tyre Plants (ATMA Member Co’s)(ATMA Member Co’s)

• Recent investments

by Tyre Industry

have been to the

tune of Rs. 36,000

crores in recently

completed,

crores in recently

completed,

greenfield and major

expansion projects.

5

Industry, Environment & OutlookIndustry, Environment & OutlookCurrent Economic & Sectoral Environment

Auto Sector

The prevailing economic turndown has adversely affected the India’s

Automobile Industry. As per Society of Indian Automobile manufacturers

(SIAM), Commercial Vehicle segment, in particular, has witnessed a continuing

spell of negative growth for the last several years.

Table 1 : Automobile Production – Avg. per Month (APM) (Lakh/Nos)

Passenger Vehicles incl. Passenger Cars, Utility Vehicles & Vans ; Commercial Vehicles incl.

M&HCV & LCV.

Category 2010-11 2011-12 2012-13 2013-14 2014-15 2015-

16(H1)

Commercial

Vehicles0.63 0.76 0.69 0.58 0.58 0.61

Passenger

Vehicles2.49 2.60 2.69 2.57 2.68 2.83

Automobile Production Automobile Production -- % Change % Change S.No Category FY12-13

(Over 11-12)

FY13-14

(Over 12-13)

FY14-15

(Over 13-14)

FY15-16H1

(Over 14-15H1)

1 M&HCV (-)28% (-)21% 21% 31%

2 LCV 2% (-)14% (-)10% (-)4%

3 P. Vehicles 3% (-)5% 4% 7%

3.1 P. Car (-)4% (-)5% 4% 8%

3.2 UVs/SUVs 52% (-)1% 11% 8%

3.3 Vans 1% (-)18% (-)12% 0.5%

4 2/3 Wheeler 1% 7% 10% (-)0.2%4 2/3 Wheeler 1% 7% 10% (-)0.2%

4.1 Motorcycle (-)1% 5% 4% (-)3%

4.2 Scooter(2W) 14% 21% 28% 10%

4.3 Scooter(3W) (-)4% (-)1% 14% 3%

4.4 Moped 1% (-)8% 3% (-)4%

5 Tractor (-)10% 22% (-)13% (-)11%

• Commercial Vehicles, has witnessed an increase in FY 14-15 after continuous

YoY decline in FY12-13 and FY 13-14. Passenger Vehicles also seen an increase

in FY 14-15 after slowed down in FY 12-13 and FY 13-14.

7

Tyre Sector

Indian Tyre industry’s performance is directly linked to that of the Automotive

Sector. The percentage share of tyre supplies to OEMs (Original Equipment

Manufacturers), has been increasing consistently for all major tyre categories i.e.

CV, Passenger Car, 2/3 Wheeler, Tractor etc. With the ongoing slowdown of the

Automotive sector, the Tyre Industry too faces a slow growth.

Industry, Environment & OutlookIndustry, Environment & OutlookCurrent Economic & Sectoral Environment

Table 2 : Tyre Production – Avg. per Month (APM)(Lakh/Nos)

Category 2011-12 2012-13 2013-14 2014-15 2015-16

(Apr - June)

Truck &

Bus Tyres13.40 13.78 13.73 14.26 14.05

Passenger

Car Tyres23.95 26.73 26.39 29.79 29.43

8

Project(s) TBR (Units)PCR + LT

(Units) 2W/3W (Units)Speciality & OTR

(MT)Others

(MT)Recently

Commissioned 466,000 1,826,000 450,000 - 8,667

Greenfield 102,500 1,252,000 1,129,200 82,200 -

Brownfield 264,000 822,000 300,000 6,310 66,750

Total 832,500 3,900,000 1,879,200 88,510 75,417

Summary Statement of Capacity Summary Statement of Capacity Creation & Creation &

Investments Investments in Tyre Industry in Indiain Tyre Industry in India

Project(s)Total Investment (Rs

crore)

Recently completed � 12,479

Greenfield � 10,160

Brownfield � 13,033

Total � 35,672

• Inline with the capacity creation in the auto sector, the tyre sector has also

added/expanded capacity pan India.

• This kind of investment by the tyre industry in India is unprecedented in

history.

As of Sep/Oct’15

Source: Smithers / ERJ

Cumulative Cumulative

Investment Investment

(approx.) (approx.)

Rs. 36, 000 CroreRs. 36, 000 Crore

Key Issues / Concerns of the Key Issues / Concerns of the

Indian Indian TyreTyre Industry Industry

10

Key issues & Concerns of Indian Tyre Industry Key issues & Concerns of Indian Tyre Industry

• Related to Raw Materials (RMs)– Tyre industry is RM intensive

– Raw materials accounts for 72% of Production cost

– Natural Rubber (NR) , the principal raw material, accounts for approx. 41% of RM cost

• Tyre Industry consumes over 66% of Total NR consumption in India.

• Key Tyre related issues relate to:– Trade Agreements

– Tyre Imports

11

Domestic NR Demand – Supply ImbalanceApr-Oct'15 (vs Apr-Oct'14) - YTD Comparison

387000

329000

300000

400000

500000

Production

(-)15%

593565584935

500000

700000

Consumption(-)1%

279265252587

200000

300000

400000

Import

(-) 10%

(Fig in MT)

12

Apr'14-Oct.'14

Apr'15-Oct.'15

200000

2014-15 2015-16300000

2014-15 2015-16

100000

2014-15 2015-16

200

222

100

150

200

250

2014-15 2015-16

Export11%

89.62

120.71

103.31

70

90

110

130

SMR-20 RSS-4 RSS-3

NR Price Comparison Avg. Mthly.(Apr'15-Oct'15)

₹/Kg

Natural Rubber Imports Imperative Natural Rubber Imports Imperative ––

Yet ‘Inverted Duty Structure’ continuesYet ‘Inverted Duty Structure’ continuesNR Imports are necessary:

• To bridge the demand/supply gap

• For quality specific requirement of new technology driven Radial Truck & Bus (TBR)

Tyres

• To maintain international competitiveness in Tyre Exports

• For reasons cited above, Tyre Industry seeks regular supply and competitive

domestic & international pricing/sourcing of its critical raw-material.

• Customs duty on Tyres has been reduced over the last few years under FTAs with• Customs duty on Tyres has been reduced over the last few years under FTAs with

no corresponding reduction in basic rate of customs duty on Natural Rubber.

Period Rate of Duty

Advalorem Specific

Upto 31st Mar'11 20% N.A.

w.e.f. 01.04.2011 20% Rs. 20/kg*

w.e.f. 20.12.2013 20% Rs.30 kg*

w.e.f 30.4.2015 25% Rs. 30 kg*

*whichever is lower ;

NR Duty in India : Recent Changes

13

NR Duty Structure : India NR Duty Structure : India vsvs other major NR other major NR

Producing / Consuming Countries Producing / Consuming Countries

Major NR Producing Countries

S.*

No

Name of

the

Countries

Customs Duty(%)

1 Thailand 0%

2 Malaysia 0%

Major NR Consuming Countries

S*.

No

Name of the

Countries

Customs

Duty(%)

1China

20% or 1200

Yuan/MT

• India’s effective NR duty is the highest amongst all countries.

3 Vietnam 3%

4 Indonesia 5%

5 Combodia 7%

6 Sri Lanka 15%

7 India25% or Rs. 30/kg

whichever is lower

2 USA 0%

3 Russia 0%

4 Japan 0%

5 Mexico 0%

6 India

25% or Rs. 30/kg

whichever is

lower

14

Basic & Concessional Customs Duty on NR in India Basic & Concessional Customs Duty on NR in India

–– No relief to Consumer Sector No relief to Consumer Sector

20

%

20%

25

% o

r R

s. 3

0/k

g,

wh

ich

ev

er

Although tyres (finished product) can be imported into India at preferential / concessional duties

under various RTAs, the corresponding concessional duties for NR do not exist for all practical

purposes.

NR falls in the negative list across most FTA except for Asia Pacific. However, in both Asia Pacific

and SAFTA, the concessional duties apply mainly for NR imports from Sri Lanka (which are

insignificant and hence of no practical significance).N

eg

ati

ve

Lis

t

20

%

Ne

ga

tiv

e L

ist

Ne

ga

tiv

e L

ist

Ne

ga

tiv

e L

ist

0%

4%

8%

12%

16%

Basic Customs

Duty

ASEAN FTA Asia Pacific Trade

Agreement

Indo Sri Lanka SAFTA* India Singapore India - Malaysia

No Duty

Concession No Duty

Concession

No Duty

Concession

No Duty

Concession

In India

SAFTA

25

% o

r R

s. 3

0/k

g,

wh

ich

ev

er

is l

ow

er

Ne

ga

tiv

e L

ist

No Duty

Concession

+ India’s NR Import from APTA Countries (South Korea, Bangladesh, China, Lao PDR, Sri Lanka) is negligible

+

• During FY 2014-15, the gap between domestic NR Production and

Consumption was 3.76 Lakh MT. In 2015-16, the actual gap till Oct. is

over 2.56 Lac MT. The estimated gap in 2015-16 is expected to be

3.06 MT.

Submission

Correct Inverted Duty by way reduction of Customs Duty of Natural

Rubber.

Or alternativelyOr alternatively

Increase in Customs Duty of Tyres (finished product) from 10%

at present to 30%, as the principal RM of Tyre Industry i.e.

Natural Rubber attracts a duty of 25%.

Allow import of Natural Rubber under ASEAN FTA in line with

concessional tariff on finished products (Tyres)

16

Customs Duty on Tyres under Trade AgreementsCustoms Duty on Tyres under Trade Agreements

• While basic customs duty on tyres is 10%, under various Trade Agreements

the duty (on tyres) is actually much lower than the basic rate of customs

duty (on its principal RM (i.e. Natural Rubber):

Item

Normal

/Basic Rate of Duty

in India ASEAN FTA

Asia Pacific

Trade

Agreement

(Bangkok

Agreement)

Indo Sri

Lanka SAFTA

India

Singapore

India

Malaysia

Nil 6%

Tyre 10% 6% 8.60% Nil 5% / Nil*

Nil

(Bias Tyre)

6%

(Radial Tyre)

NR 20% OR Rs.30/kg

whichever is lower

Negative List

(No Duty

Concession) 20%

Negative List

(No Duty

Concession)

Negative List

(No Duty

Concession

Negative

List

(No Duty

Concession)

Negative List

(No Duty

Concession)

* Under SAFTA 5% concessional duty for Tyre when imports from Pakistan & Sri Lanka ,imports from other SAFTA countries Nil Duty.

Tyre is perhaps the only finished product (vis-a-vis its basic RM) on which

‘duty inversion’ not only continues but has actually aggravated in recent

years. This needs to be addressed and corrected on priority.17

Duty inversion has favoured large Tyre Imports (esp. from China)

Source: DGCI & S ; Figs. in brackets ( ) indicate the percentage of China of Total Truck/Bus tyre Imports.

◊ Cumulative increase since 2002-03 to 2014-15 is 1087% in Total Truck & Bus Tyre Imports.

80

88

22

1 50

6

87

3

13

28

11

07 13

62

24

64

13

37

17

59

12

82

94

9.5

0

60

3.0

7

19

(24

%)

67

(7

6%

)

19

2(8

7%

)

34

5(6

8%

)

75

0 (

86

%)

11

92

(9

0%

)

90

8(8

2%

)

95

8 (

70

%)

19

11

(7

8%

)

68

7(5

1%

)

85

8(4

9%

)

70

5(5

5%

)

65

4.3

0(6

9%

)

51

5.5

1(8

5%

)

0

500

1000

1500

2000

2500

3000

2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16(Apr-

Aug)

('000 nos) TRUCK / BUS TYRE IMPORTS - TOTAL & FROM CHINA

Total China

18

◊ Cumulative increase since 2002-03 to 2014-15 is 1087% in Total Truck & Bus Tyre Imports.

Source : DGCI & S ; Figs. in brackets ( ) indicate percentage share of China & South Korea in Total P. Car Tyre imports

◊ Cumulative increase since 2002-03 to 2014-15 is 2598% in Total Passenger Car Tyre Imports.

19

4 44

6 77

9

69

2

15

02

16

27

27

78

29

94

48

64

52

84

53

74

51

19

52

34

.62

21

34

.09

65

(33

%)

23

2(5

2%

)

45

9(5

9%

)

46

3 (

67

%)

88

4(5

9%

)

99

4 (

61

%)

19

82

(71

%)

20

33

(6

8%

)

28

96

(6

0%

)

26

37

(50

%)

27

60

(51

%)

27

37

(53

%)

26

30

.48

(50

%)

11

17

.38

(52

%)

0

1000

2000

3000

4000

5000

6000

2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16(Apr-

Aug)

PASSENGER CAR TYRE IMPORTS - TOTAL & FROM (CHINA & SOUTH KOREA)

Total China & S. Korea

('000/Nos)

Tyre Imports into India favoured by FTAs

• Low import tariffs in India have encouraged large &growing volume of tyre imports, despite adequatedomestic capacity already in place & investmentsmade in new capacity creation.

• Hence, based on compelling need andcircumstances, the Government of India can increasethe customs duty on tyres from existing rate of 10%(to a higher rate of duty say 30%) without anycorresponding action / explanation to the worldbody (WTO).

19

Major RMs of Tyre Industry

Raw Material(s) Domestic

Production

(est.)

Domestic

Consumpt

ion (est.)

Shortfall

/ Deficit

Shortfall as a %

to consumption

MT / Year

Nylon Tyre Cord Fabric 68000 126000 58000 46%

Rubber Chemicals 40000 56000 16000 27%

Steel Tyre Cord 20000 50000 30000 60%

Polyester Tyre Cord 5000 20000 15000 76%

(Gap between Domestic Demand and Supply / Capacity)

RMs with Domestic Demand : Supply Gap – Case for Reduction in Customs Duty

Polyester Tyre Cord 5000 20000 15000 76%

Polybutadine Rubber (PBR) 105000 171000* 65160 38%

Styrene Butadiene Rubber

(SBR)

35730 217400* 181670 84%

Butyl Rubber NIL 95000* 100% 100%

EPDM Nil 4000 100% 100%

RMs of Tyre Industry having no Domestic Production – Case for Exemption

from Customs Duty

20

* Consumption includes tyre & non-tyre sectors

Proposal for Reduction of Customs Duty on Raw-Materials having gap

(shortfall) in domestic Capacity : Consumption &

Waiver of Customs Duty on Raw - Materials of Tyre Industry

NOT manufactured domesticallyRaw Material Existing Duty Suggested /

Proposed Duty

Natural Rubber 25% or Rs.30/kg + Correct Inverted

Duty (Tyre vs NR)

Nylon Tyre Cord Fabric (NTCF) 10% 5%

Poly Butadiene Rubber (PBR) 10% 5%Poly Butadiene Rubber (PBR) 10% 5%

Rubber Chemicals 7.5% 2.5%

Polyester Tyre Cord 5% 2.5%

Steel Tyre Cord 10% 5%

Butyl Rubber* 5% Waive off

EPDM* 10% Waive off

* No Domestic Production

+ whichever is lower

21

Key Submission(s) 1/2

• There is an urgent need to correct the existing (and

continuing) anomaly of ‘inverted duty’ structure as it

prevails for the domestic Tyre Industry by way of the

following

Or alternatively

• Increase in Customs Duty of Tyres (finished product)

from 10% at present to 30%, as the principal RM offrom 10% at present to 30%, as the principal RM of

Tyre Industry i.e. Natural Rubber attracts a duty of

25%.

• Allow import of NR under ASEAN FTA in line with

concessional tariff of finished products (Tyres)

22

For other key RMs of Tyre Industry, the duty inversion / anomalies continue and

need to be corrected by way of:

Waiver of customs duty on raw materials NOT manufactured domestically,

• Butyl Rubber (HS Code 4002 31 00) – present rate of customs duty : 5%

• EPDM (HSN 4002 7000) - present rate of Customs Duty : 10%

Reduction in Customs Duty on key raw materials of Tyres for which the domestic

capacity / production is insufficient to meet domestic demand, i.e.

Key Submission(s) 2/2

capacity / production is insufficient to meet domestic demand, i.e.

• Nylon Tyre Cord (HSN 5902 1010) – Reduction sought from 10% to 5%;

• Poly Butadiene Rubber (HSN4002 2000) – Reduction sought from 10% to 5%;

• Steel Tyre Cord (HSN 7312 9000) – Reduction sought from 10% to 5%;

• Rubber Chemicals (HSN 38121000/30 10) – Reduction sought from 7.5% to 2.5%

• Polyester Tyre Cord (HSN 5902 20 00) – Reduction sought from 5% to 2.5%

• Styrene Butadiene Rubber (HSN 400219001) Reduction sought from 10% to 5%

23

Operational & Procedural Issues –

Tyre Industry Concern

Issue:

• Transfer of accumulated Cenvat credit of

Special Additional Duty (SAD) to another plant

of same company.of same company.

Proposal: To issue suitable clarification

amendment to transfer the credits to another

plant of the same company.

24

Excise Duty on sale of Tyre, Tube & Flap (TTF)

& MRP on Packed Commodity.

Tyre Tube & Flap (TTF) which are sold by TyreCompany as a set. These TTF are normallytied together with a plastic/jute material stripswith an objective that during thetransportation of the product, the tyre, tube &transportation of the product, the tyre, tube &flap are not separated. The TTF are sold insets, tubes are put inside the tyre and flap isinserted. Hence TTF which are tied withplastic strip cannot be called as a “PackedCommodity”.

25

The issue has been raised in the past by the

Central Excise Department at the various

locations and after thorough investigations

they upheld the contention of the Tyrethey upheld the contention of the Tyre

Industry and did not issue the show cause /

demand notice to all.

26

Proposal:

• Guidelines are issued by the Department to

clarify the position that through TTF may be

tied with plastic strips, these do not fall withintied with plastic strips, these do not fall within

the category of Packed Commodity, and

accordingly, not liable for Excise Duty on MRP

Basis.

27

Safeguard Duty on Carbon Black import-

Advance Authorization Scheme

• Under Para 4.1.4 of Foreign Trade Policy, Government has granted exemptionfrom payment of all kind of duties under Advance License Authorizationimports.

• Safeguard Duty was imposed on imports of Carbon Black vide NotificationNo.4/2012-Customs (SG) DATED 5th Oct. 2012.

• Customs Authorities at various ports have been demanding Safeguard Duty onimports of Carbon Black against Advance License Authorization.

• Finance Ministry clarified vide Circular No.11/2014-Customs dt. 14.11.14 thatSafeguard Duty will be leviable under Section 8C against AdvanceSafeguard Duty will be leviable under Section 8C against AdvanceAuthorization. Incase where SGD is negative, the same will be treated as Nil.

Submission:

As per Industry Submission & requests made, although Finance Ministry didissue the Circular giving clarification on the issue, the same fails to provide thedesired relief as :

i) the circular is not applicable with retrospective effect.

ii) exemption of duties under Section 8C on Advance Authorization import notaccorded.

28

Issue:

• Insoluble Sulphur, one of the raw materials of tyreindustry, classaification as Rubber Vulcanizing agentsinstead of Sulphur resulting duty as 7.5% instead of 5%

Proposal:

• Department may issue clarification that the material is• Department may issue clarification that the material isSulphur instead of Rubber Vulcanising agent.

***

29