union budget 2016-17 preview - web.angelbackoffice.com

TRANSCRIPT

Union Budget 2016-17 Preview

Index

Union Budget 2016-17 Preview 2

Sector-wise Summary 12

Sector-wise Expectations

Automobile 14

Banking 15

Capital Goods 19

Cement 22

Education 23

FMCG 24

Infrastructure 25

Information Technology 29

Media 30

Metals & Mining 31

Oil & Gas 32

Pharmaceutical 33

Power 34

Real Estate 35

Telecom 37

Tyre 38

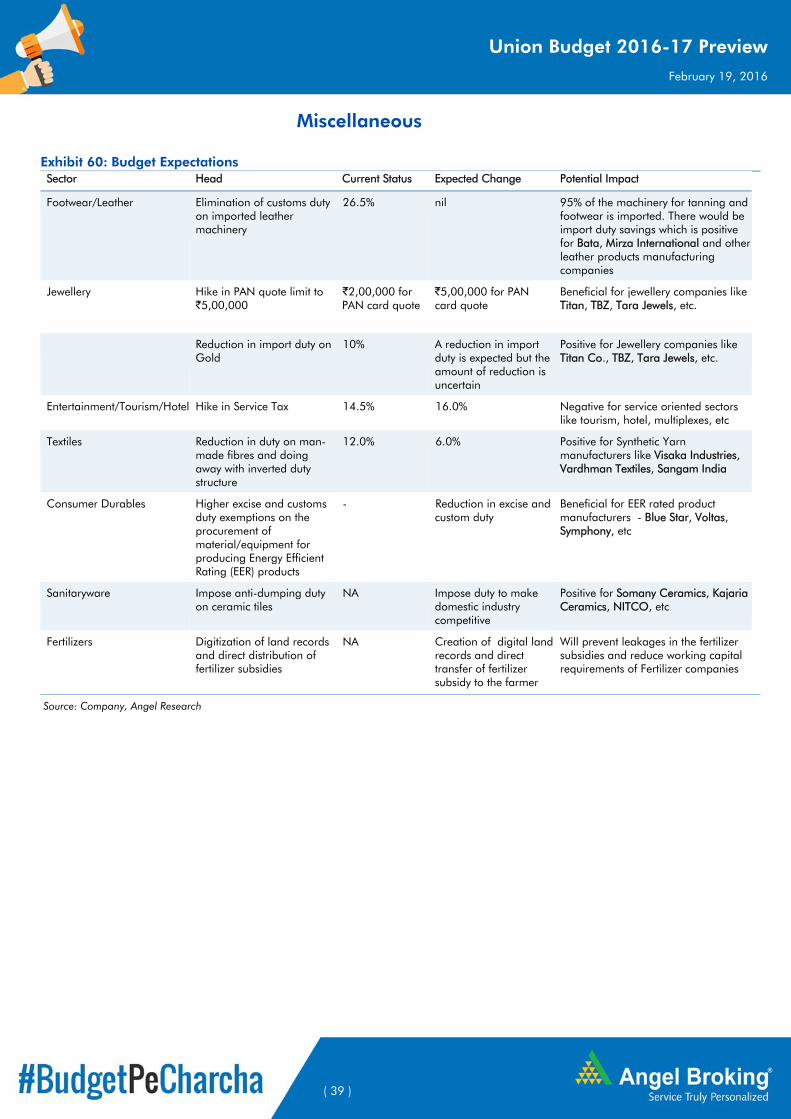

Miscellaneous 39

( 2 )

Union Budget 2016-17 Preview February 19, 2016

Will the FM strike the right balance?

The Finance Minister (FM) will present the Union Budget 2016-17 on February 29, 2016 which will be the third budget from the NDA-led government in its current term. All eyes are set on whether he will be able to increase investment spending, while adhering to the path of fiscal consolidation.

We cannot emphasize enough on the importance of both these objectives. The government realizes the importance of increasing investment spending to stimulate an economy already facing global headwinds. The budget needs to be growth oriented and the FM will have to push capital and infrastructure spending higher, if the investment cycle is to be revived.

Even so it’s critical for the government to rein in the fiscal deficit in a year when it has received a windfall gain from a drop in crude prices and macro indicators are looking at their strongest in recent years. The RBI governor has clearly outlined his views against relaxing the fiscal deficit. With a reined in fiscal deficit, the RBI would have enough headroom to cut rates further, which would be positive for the economy.

Our Take

We expect the FY2016 target set under the Fiscal Responsibility and Budget Management (FRBM) Act of restricting the fiscal deficit to under 3.9% of GDP to be attained; however, the FY2017 fiscal deficit target of 3.5% of GDP appears slightly challenging, although not impossible. We bake into our estimates strong preference towards increasing infrastructure spending, while achieving the FRBM targets partially in FY2017. This spending would be supported by savings from crude and an increase in the service tax rates. We also expect measures to unclog the financial sector by tackling the NPA menace and recapitalizing the PSU banks. Overall we expect a pragmatic budget focused on growth and one promoting India as an investment destination by eliminating tax distortions, while taking further measures to improve the ease of doing business.

7th Pay Commission + Rural Spending = Consumption Boost

We expect higher spending led by the implementation of the 7th Pay Commission recommendations and the One Rank, One Pension (OROP) scheme to boost consumption. Also with the rural economy reeling under the stress of two consecutive droughts and slower growth in minimum support prices, we expect a 10% increase in allocation towards rural schemes to contain the agrarian slowdown.

Budget conviction picks

In line with our view that investment spending will continue to remain high we see infrastructure, cement and capital goods companies as the direct beneficiaries of the budget. We prefer Sadbhav Engineering and KNR Constructions with their focus on road/highway, while BEL remains our best play on defense spending. We like Ultratech within the cement space. Increased allocation to rural schemes and higher salaries & pension bill will have a positive impact on consumption, benefitting two wheeler players such as TVS Motors. With housing expected to see some push, LIC Housing remain our best play on that sector.

Addressing rural distress whilemaintaining high infrastructurespending vital

Budget Picks – Infra & Cap Goods(Sadbhav Eng., KNR Construction, BEL),Cement (Ultratech), Consumption (TVS),Housing Finance (LIC Housing)

( 3 )

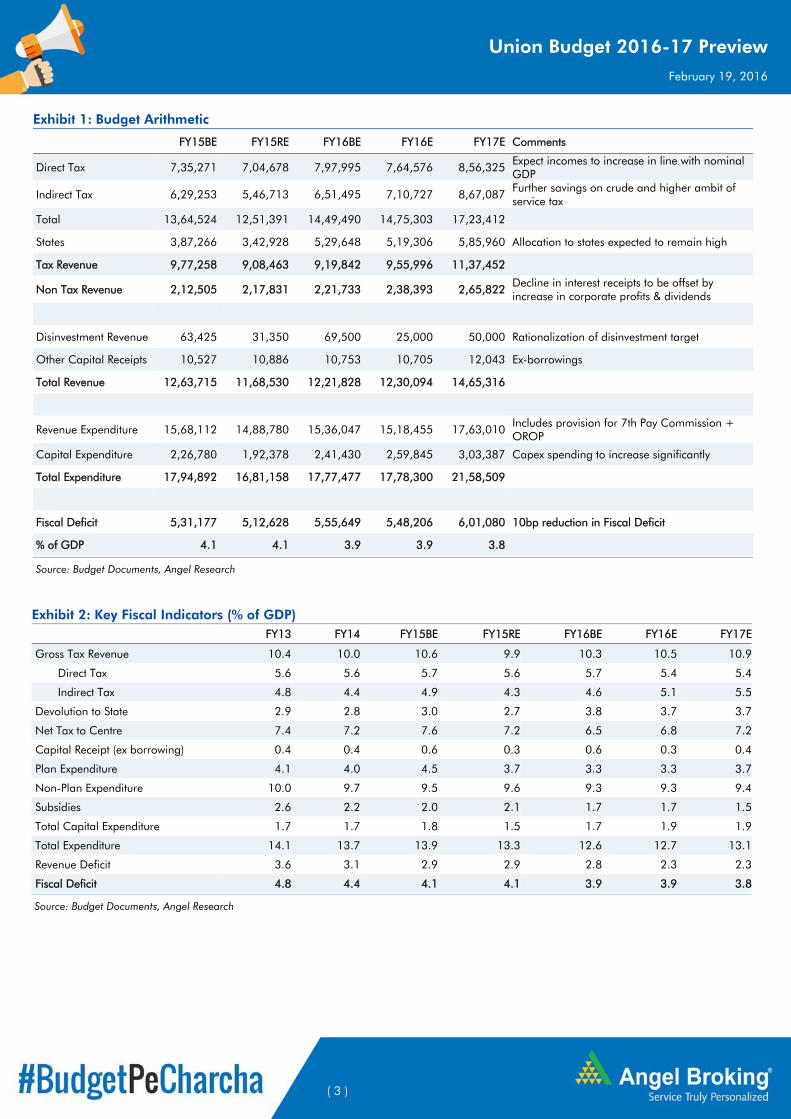

Union Budget 2016-17 Preview February 19, 2016

Exhibit 1: Budget Arithmetic

FY15BE FY15RE FY16BE FY16E FY17E Comments

Direct Tax 7,35,271 7,04,678 7,97,995 7,64,576 8,56,325Expect incomes to increase in line with nominal GDP

Indirect Tax 6,29,253 5,46,713 6,51,495 7,10,727 8,67,087Further savings on crude and higher ambit of service tax

Total 13,64,524 12,51,391 14,49,490 14,75,303 17,23,412

States 3,87,266 3,42,928 5,29,648 5,19,306 5,85,960 Allocation to states expected to remain high

Tax Revenue 9,77,258 9,08,463 9,19,842 9,55,996 11,37,452

Non Tax Revenue 2,12,505 2,17,831 2,21,733 2,38,393 2,65,822Decline in interest receipts to be offset by increase in corporate profits & dividends

Disinvestment Revenue 63,425 31,350 69,500 25,000 50,000 Rationalization of disinvestment target

Other Capital Receipts 10,527 10,886 10,753 10,705 12,043 Ex-borrowings

Total Revenue 12,63,715 11,68,530 12,21,828 12,30,094 14,65,316

Revenue Expenditure 15,68,112 14,88,780 15,36,047 15,18,455 17,63,010Includes provision for 7th Pay Commission + OROP

Capital Expenditure 2,26,780 1,92,378 2,41,430 2,59,845 3,03,387 Capex spending to increase significantly

Total Expenditure 17,94,892 16,81,158 17,77,477 17,78,300 21,58,509

Fiscal Deficit 5,31,177 5,12,628 5,55,649 5,48,206 6,01,080 10bp reduction in Fiscal Deficit

% of GDP 4.1 4.1 3.9 3.9 3.8

Source: Budget Documents, Angel Research

Exhibit 2: Key Fiscal Indicators (% of GDP)

FY13 FY14 FY15BE FY15RE FY16BE FY16E FY17E

Gross Tax Revenue 10.4 10.0 10.6 9.9 10.3 10.5 10.9

Direct Tax 5.6 5.6 5.7 5.6 5.7 5.4 5.4

Indirect Tax 4.8 4.4 4.9 4.3 4.6 5.1 5.5

Devolution to State 2.9 2.8 3.0 2.7 3.8 3.7 3.7

Net Tax to Centre 7.4 7.2 7.6 7.2 6.5 6.8 7.2

Capital Receipt (ex borrowing) 0.4 0.4 0.6 0.3 0.6 0.3 0.4

Plan Expenditure 4.1 4.0 4.5 3.7 3.3 3.3 3.7

Non-Plan Expenditure 10.0 9.7 9.5 9.6 9.3 9.3 9.4

Subsidies 2.6 2.2 2.0 2.1 1.7 1.7 1.5

Total Capital Expenditure 1.7 1.7 1.8 1.5 1.7 1.9 1.9

Total Expenditure 14.1 13.7 13.9 13.3 12.6 12.7 13.1

Revenue Deficit 3.6 3.1 2.9 2.9 2.8 2.3 2.3

Fiscal Deficit 4.8 4.4 4.1 4.1 3.9 3.9 3.8

Source: Budget Documents, Angel Research

( 4 )

Union Budget 2016-17 Preview February 19, 2016

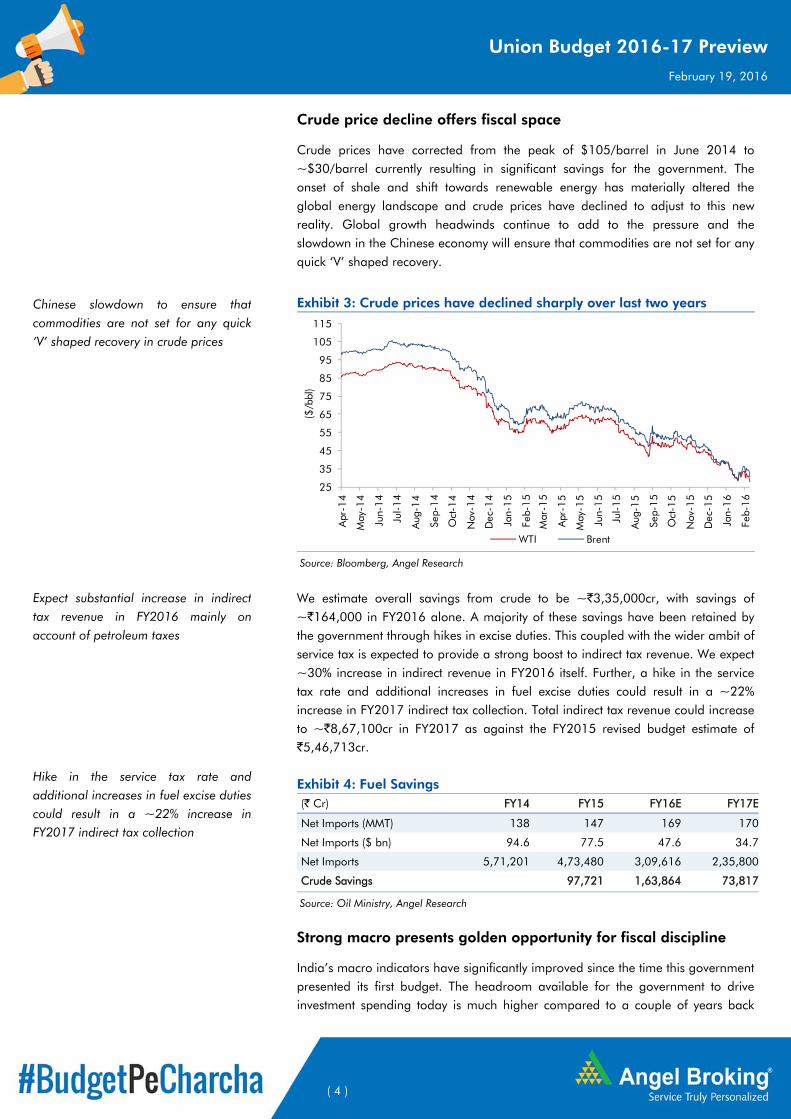

Crude price decline offers fiscal space

Crude prices have corrected from the peak of $105/barrel in June 2014 to ~$30/barrel currently resulting in significant savings for the government. The onset of shale and shift towards renewable energy has materially altered the global energy landscape and crude prices have declined to adjust to this new reality. Global growth headwinds continue to add to the pressure and the slowdown in the Chinese economy will ensure that commodities are not set for any quick ‘V’ shaped recovery.

Exhibit 3: Crude prices have declined sharply over last two years

Source: Bloomberg, Angel Research

We estimate overall savings from crude to be ~`3,35,000cr, with savings of ~`164,000 in FY2016 alone. A majority of these savings have been retained by the government through hikes in excise duties. This coupled with the wider ambit of service tax is expected to provide a strong boost to indirect tax revenue. We expect ~30% increase in indirect revenue in FY2016 itself. Further, a hike in the service tax rate and additional increases in fuel excise duties could result in a ~22% increase in FY2017 indirect tax collection. Total indirect tax revenue could increase to ~`8,67,100cr in FY2017 as against the FY2015 revised budget estimate of `5,46,713cr.

Exhibit 4: Fuel Savings (` Cr) FY14 FY15 FY16E FY17E

Net Imports (MMT) 138 147 169 170

Net Imports ($ bn) 94.6 77.5 47.6 34.7

Net Imports 5,71,201 4,73,480 3,09,616 2,35,800

Crude Savings 97,721 1,63,864 73,817

Source: Oil Ministry, Angel Research

Strong macro presents golden opportunity for fiscal discipline

India’s macro indicators have significantly improved since the time this government presented its first budget. The headroom available for the government to drive investment spending today is much higher compared to a couple of years back

25

35

45

55

65

75

85

95

105

115

Apr

-14

May

-14

Jun-

14

Jul-

14

Aug

-14

Sep-

14

Oct

-14

Nov

-14

Dec

-14

Jan-

15

Feb-

15

Mar

-15

Apr

-15

May

-15

Jun-

15

Jul-

15

Aug

-15

Sep-

15

Oct

-15

Nov

-15

Dec

-15

Jan-

16

Feb-

16

($/b

bl)

WTI Brent

Chinese slowdown to ensure thatcommodities are not set for any quick‘V’ shaped recovery in crude prices

Expect substantial increase in indirecttax revenue in FY2016 mainly onaccount of petroleum taxes

Hike in the service tax rate andadditional increases in fuel excise dutiescould result in a ~22% increase inFY2017 indirect tax collection

( 5 )

Union Budget 2016-17 Preview February 19, 2016

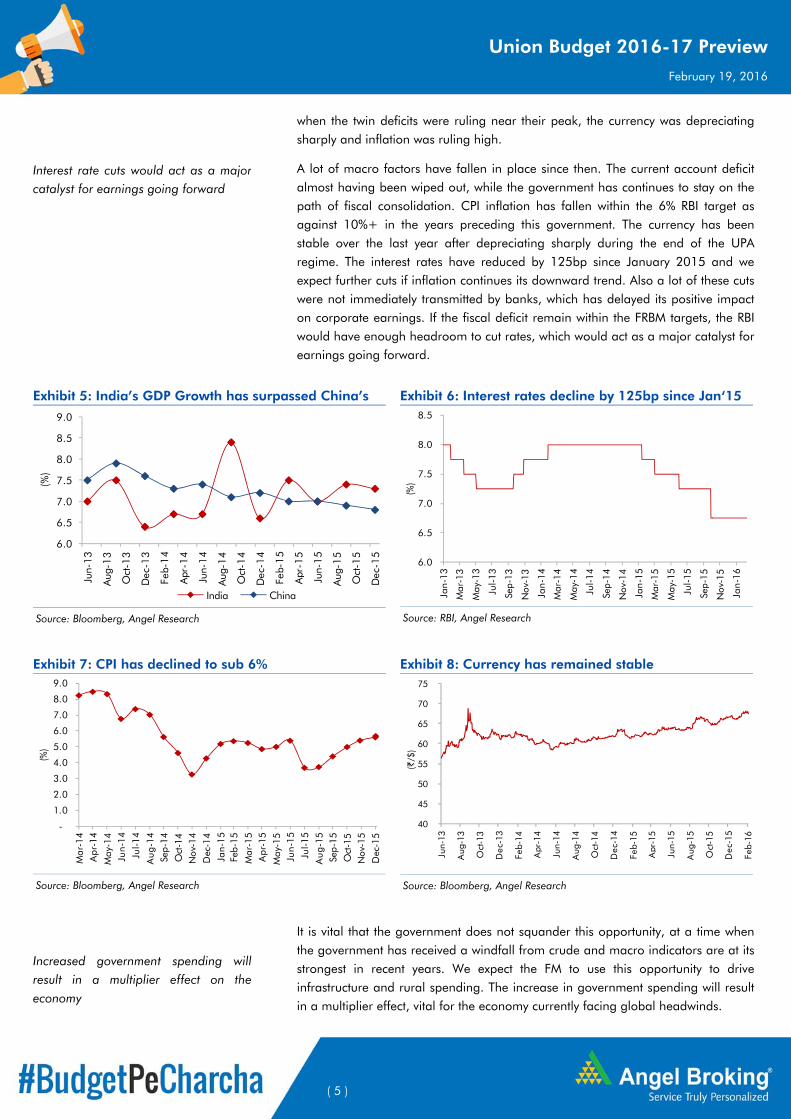

when the twin deficits were ruling near their peak, the currency was depreciating sharply and inflation was ruling high.

A lot of macro factors have fallen in place since then. The current account deficit almost having been wiped out, while the government has continues to stay on the path of fiscal consolidation. CPI inflation has fallen within the 6% RBI target as against 10%+ in the years preceding this government. The currency has been stable over the last year after depreciating sharply during the end of the UPA regime. The interest rates have reduced by 125bp since January 2015 and we expect further cuts if inflation continues its downward trend. Also a lot of these cuts were not immediately transmitted by banks, which has delayed its positive impact on corporate earnings. If the fiscal deficit remain within the FRBM targets, the RBI would have enough headroom to cut rates, which would act as a major catalyst for earnings going forward.

Exhibit 5: India’s GDP Growth has surpassed China’s

Source: Bloomberg, Angel Research

Exhibit 6: Interest rates decline by 125bp since Jan‘15

Source: RBI, Angel Research

Exhibit 7: CPI has declined to sub 6%

Source: Bloomberg, Angel Research

Exhibit 8: Currency has remained stable

Source: Bloomberg, Angel Research

It is vital that the government does not squander this opportunity, at a time when the government has received a windfall from crude and macro indicators are at its strongest in recent years. We expect the FM to use this opportunity to drive infrastructure and rural spending. The increase in government spending will result in a multiplier effect, vital for the economy currently facing global headwinds.

6.0

6.5

7.0

7.5

8.0

8.5

9.0

Jun-

13

Aug

-13

Oct

-13

Dec

-13

Feb-

14

Apr

-14

Jun-

14

Aug

-14

Oct

-14

Dec

-14

Feb-

15

Apr

-15

Jun-

15

Aug

-15

Oct

-15

Dec

-15

(%)

India China

6.0

6.5

7.0

7.5

8.0

8.5

Jan-

13

Mar

-13

May

-13

Jul-1

3

Sep-

13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-1

4

Sep-

14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-1

5

Sep-

15

Nov

-15

Jan-

16

(%)

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Mar

-14

Apr

-14

May

-14

Jun-

14

Jul-1

4

Aug

-14

Sep-

14

Oct

-14

Nov

-14

Dec

-14

Jan-

15Fe

b-15

Mar

-15

Apr

-15

May

-15

Jun-

15

Jul-1

5

Aug

-15

Sep-

15

Oct

-15

Nov

-15

Dec

-15

(%)

40

45

50

55

60

65

70

75

Jun-

13

Aug

-13

Oct

-13

Dec

-13

Feb-

14

Apr

-14

Jun-

14

Aug

-14

Oct

-14

Dec

-14

Feb-

15

Apr

-15

Jun-

15

Aug

-15

Oct

-15

Dec

-15

Feb-

16

(`/$

)

Interest rate cuts would act as a majorcatalyst for earnings going forward

Increased government spending willresult in a multiplier effect on theeconomy

( 6 )

Union Budget 2016-17 Preview February 19, 2016

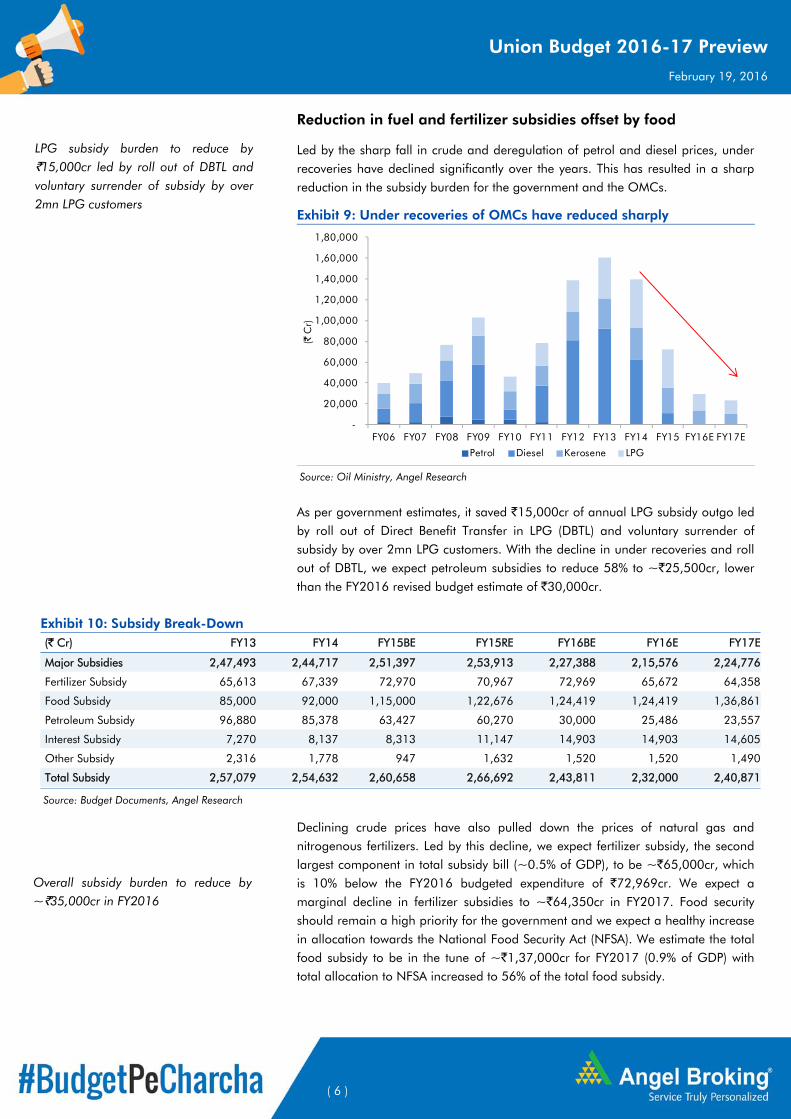

Reduction in fuel and fertilizer subsidies offset by food

Led by the sharp fall in crude and deregulation of petrol and diesel prices, under recoveries have declined significantly over the years. This has resulted in a sharp reduction in the subsidy burden for the government and the OMCs.

Exhibit 9: Under recoveries of OMCs have reduced sharply

Source: Oil Ministry, Angel Research

As per government estimates, it saved `15,000cr of annual LPG subsidy outgo led by roll out of Direct Benefit Transfer in LPG (DBTL) and voluntary surrender of subsidy by over 2mn LPG customers. With the decline in under recoveries and roll out of DBTL, we expect petroleum subsidies to reduce 58% to ~`25,500cr, lower than the FY2016 revised budget estimate of `30,000cr.

Exhibit 10: Subsidy Break-Down (` Cr) FY13 FY14 FY15BE FY15RE FY16BE FY16E FY17E

Major Subsidies 2,47,493 2,44,717 2,51,397 2,53,913 2,27,388 2,15,576 2,24,776

Fertilizer Subsidy 65,613 67,339 72,970 70,967 72,969 65,672 64,358

Food Subsidy 85,000 92,000 1,15,000 1,22,676 1,24,419 1,24,419 1,36,861

Petroleum Subsidy 96,880 85,378 63,427 60,270 30,000 25,486 23,557

Interest Subsidy 7,270 8,137 8,313 11,147 14,903 14,903 14,605

Other Subsidy 2,316 1,778 947 1,632 1,520 1,520 1,490

Total Subsidy 2,57,079 2,54,632 2,60,658 2,66,692 2,43,811 2,32,000 2,40,871

Source: Budget Documents, Angel Research

Declining crude prices have also pulled down the prices of natural gas and nitrogenous fertilizers. Led by this decline, we expect fertilizer subsidy, the second largest component in total subsidy bill (~0.5% of GDP), to be ~`65,000cr, which is 10% below the FY2016 budgeted expenditure of `72,969cr. We expect a marginal decline in fertilizer subsidies to ~`64,350cr in FY2017. Food security should remain a high priority for the government and we expect a healthy increase in allocation towards the National Food Security Act (NFSA). We estimate the total food subsidy to be in the tune of ~`1,37,000cr for FY2017 (0.9% of GDP) with total allocation to NFSA increased to 56% of the total food subsidy.

-

20,000

40,000

60,000

80,000

1,00,000

1,20,000

1,40,000

1,60,000

1,80,000

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16E FY17E

(`C

r)

Petrol Diesel Kerosene LPG

LPG subsidy burden to reduce by`15,000cr led by roll out of DBTL andvoluntary surrender of subsidy by over2mn LPG customers

Overall subsidy burden to reduce by~`35,000cr in FY2016

( 7 )

Union Budget 2016-17 Preview February 19, 2016

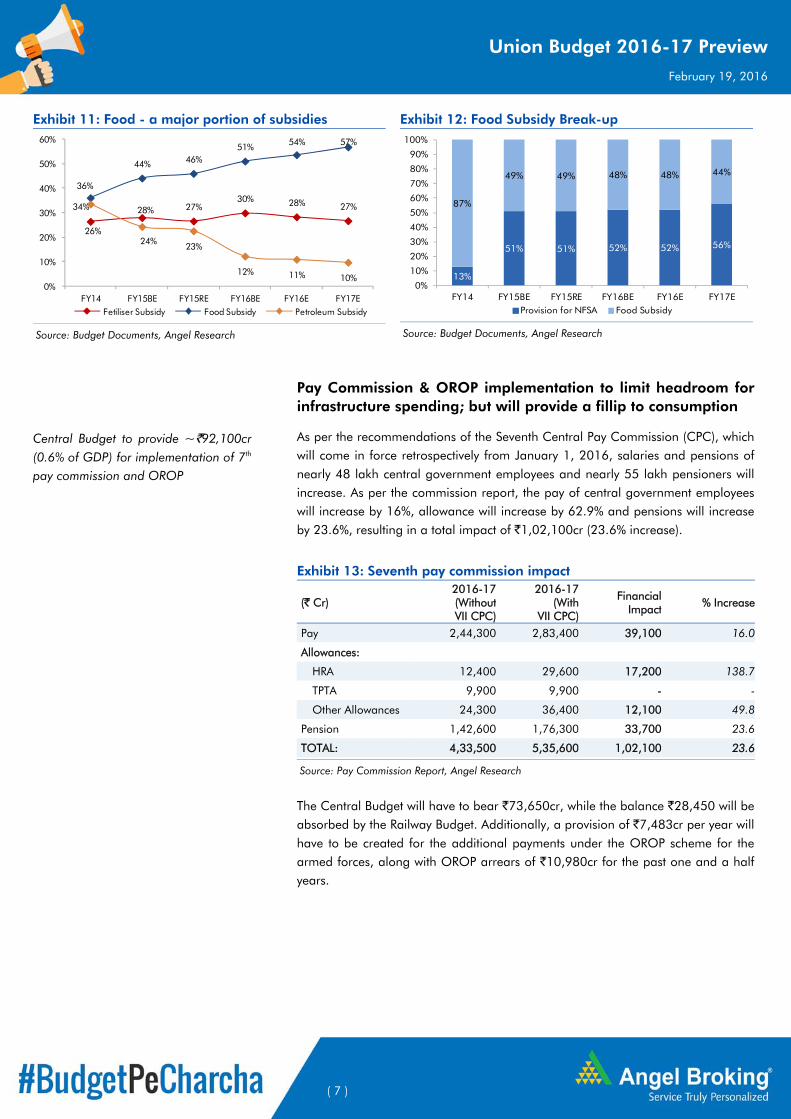

Exhibit 11: Food - a major portion of subsidies

Source: Budget Documents, Angel Research

Exhibit 12: Food Subsidy Break-up

Source: Budget Documents, Angel Research

Pay Commission & OROP implementation to limit headroom for infrastructure spending; but will provide a fillip to consumption

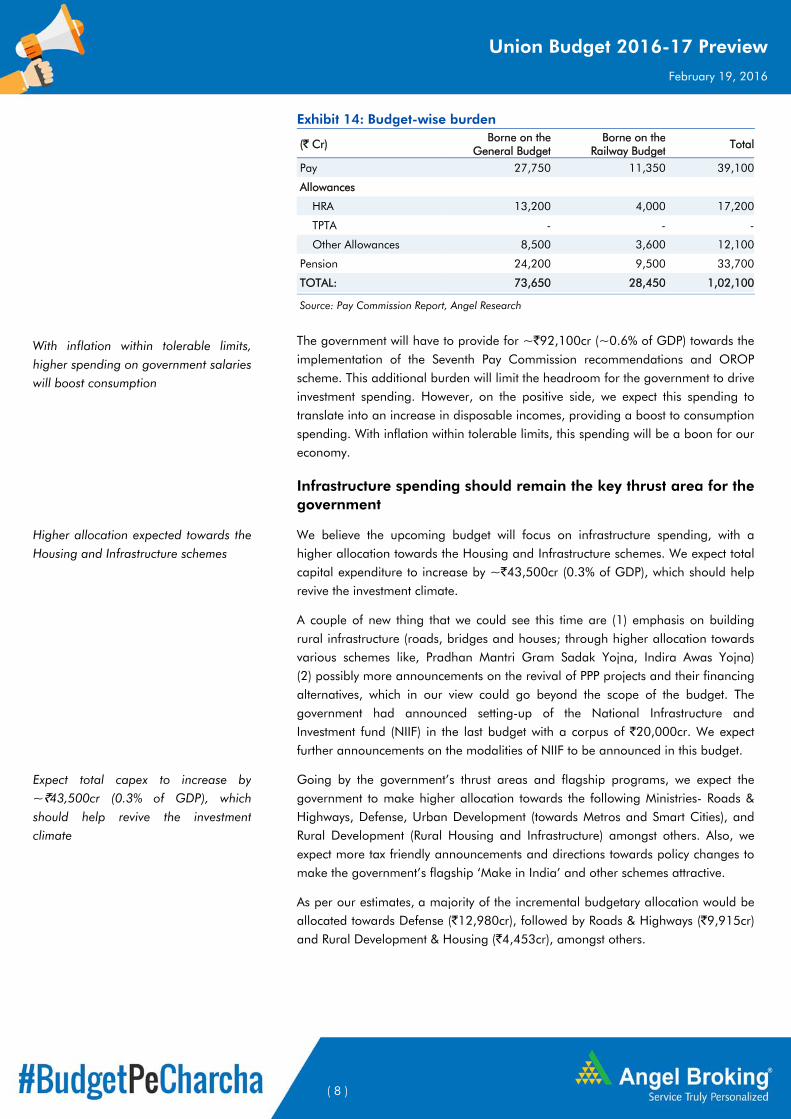

As per the recommendations of the Seventh Central Pay Commission (CPC), which will come in force retrospectively from January 1, 2016, salaries and pensions of nearly 48 lakh central government employees and nearly 55 lakh pensioners will increase. As per the commission report, the pay of central government employees will increase by 16%, allowance will increase by 62.9% and pensions will increase by 23.6%, resulting in a total impact of `1,02,100cr (23.6% increase).

Exhibit 13: Seventh pay commission impact

(` Cr) 2016-17(WithoutVII CPC)

2016-17(With

VII CPC)

FinancialImpact

% Increase

Pay 2,44,300 2,83,400 39,100 16.0

Allowances:

HRA 12,400 29,600 17,200 138.7

TPTA 9,900 9,900 - -

Other Allowances 24,300 36,400 12,100 49.8

Pension 1,42,600 1,76,300 33,700 23.6

TOTAL: 4,33,500 5,35,600 1,02,100 23.6

Source: Pay Commission Report, Angel Research

The Central Budget will have to bear `73,650cr, while the balance `28,450 will be absorbed by the Railway Budget. Additionally, a provision of `7,483cr per year will have to be created for the additional payments under the OROP scheme for the armed forces, along with OROP arrears of `10,980cr for the past one and a half years.

26%

28% 27%30% 28% 27%

36%

44% 46%51% 54% 57%

34%

24%23%

12% 11% 10%0%

10%

20%

30%

40%

50%

60%

FY14 FY15BE FY15RE FY16BE FY16E FY17EFetiliser Subsidy Food Subsidy Petroleum Subsidy

13%

51% 51% 52% 52% 56%

87%

49% 49% 48% 48% 44%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY14 FY15BE FY15RE FY16BE FY16E FY17EProvision for NFSA Food Subsidy

Central Budget to provide ~`92,100cr(0.6% of GDP) for implementation of 7th

pay commission and OROP

( 8 )

Union Budget 2016-17 Preview February 19, 2016

Exhibit 14: Budget-wise burden

(` Cr) Borne on the

General BudgetBorne on the

Railway BudgetTotal

Pay 27,750 11,350 39,100

Allowances

HRA 13,200 4,000 17,200

TPTA - - -

Other Allowances 8,500 3,600 12,100

Pension 24,200 9,500 33,700

TOTAL: 73,650 28,450 1,02,100

Source: Pay Commission Report, Angel Research

The government will have to provide for ~`92,100cr (~0.6% of GDP) towards the implementation of the Seventh Pay Commission recommendations and OROP scheme. This additional burden will limit the headroom for the government to drive investment spending. However, on the positive side, we expect this spending to translate into an increase in disposable incomes, providing a boost to consumption spending. With inflation within tolerable limits, this spending will be a boon for our economy.

Infrastructure spending should remain the key thrust area for the government

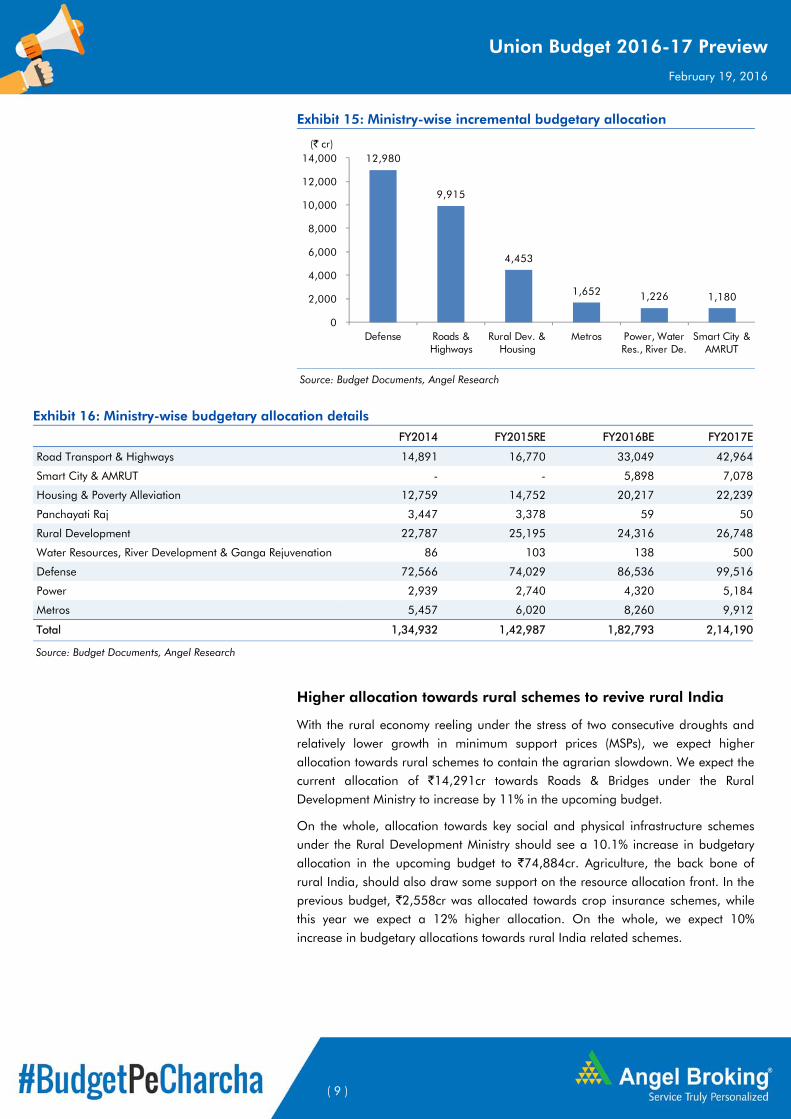

We believe the upcoming budget will focus on infrastructure spending, with a higher allocation towards the Housing and Infrastructure schemes. We expect total capital expenditure to increase by ~`43,500cr (0.3% of GDP), which should help revive the investment climate.

A couple of new thing that we could see this time are (1) emphasis on building rural infrastructure (roads, bridges and houses; through higher allocation towards various schemes like, Pradhan Mantri Gram Sadak Yojna, Indira Awas Yojna) (2) possibly more announcements on the revival of PPP projects and their financing alternatives, which in our view could go beyond the scope of the budget. The government had announced setting-up of the National Infrastructure and Investment fund (NIIF) in the last budget with a corpus of `20,000cr. We expect further announcements on the modalities of NIIF to be announced in this budget.

Going by the government’s thrust areas and flagship programs, we expect the government to make higher allocation towards the following Ministries- Roads & Highways, Defense, Urban Development (towards Metros and Smart Cities), and Rural Development (Rural Housing and Infrastructure) amongst others. Also, we expect more tax friendly announcements and directions towards policy changes to make the government’s flagship ‘Make in India’ and other schemes attractive.

As per our estimates, a majority of the incremental budgetary allocation would be allocated towards Defense (`12,980cr), followed by Roads & Highways (`9,915cr) and Rural Development & Housing (`4,453cr), amongst others.

With inflation within tolerable limits,higher spending on government salarieswill boost consumption

Higher allocation expected towards theHousing and Infrastructure schemes

Expect total capex to increase by~`43,500cr (0.3% of GDP), whichshould help revive the investmentclimate

( 9 )

Union Budget 2016-17 Preview February 19, 2016

Exhibit 15: Ministry-wise incremental budgetary allocation

Source: Budget Documents, Angel Research

Exhibit 16: Ministry-wise budgetary allocation details

FY2014 FY2015RE FY2016BE FY2017E

Road Transport & Highways 14,891 16,770 33,049 42,964

Smart City & AMRUT - - 5,898 7,078

Housing & Poverty Alleviation 12,759 14,752 20,217 22,239

Panchayati Raj 3,447 3,378 59 50

Rural Development 22,787 25,195 24,316 26,748

Water Resources, River Development & Ganga Rejuvenation 86 103 138 500

Defense 72,566 74,029 86,536 99,516

Power 2,939 2,740 4,320 5,184

Metros 5,457 6,020 8,260 9,912

Total 1,34,932 1,42,987 1,82,793 2,14,190

Source: Budget Documents, Angel Research

Higher allocation towards rural schemes to revive rural India

With the rural economy reeling under the stress of two consecutive droughts and relatively lower growth in minimum support prices (MSPs), we expect higher allocation towards rural schemes to contain the agrarian slowdown. We expect the current allocation of `14,291cr towards Roads & Bridges under the Rural Development Ministry to increase by 11% in the upcoming budget.

On the whole, allocation towards key social and physical infrastructure schemes under the Rural Development Ministry should see a 10.1% increase in budgetary allocation in the upcoming budget to `74,884cr. Agriculture, the back bone of rural India, should also draw some support on the resource allocation front. In the previous budget, `2,558cr was allocated towards crop insurance schemes, while this year we expect a 12% higher allocation. On the whole, we expect 10% increase in budgetary allocations towards rural India related schemes.

12,980

9,915

4,453

1,652 1,226 1,180

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Defense Roads & Highways

Rural Dev. & Housing

Metros Power, Water Res., River De.

Smart City & AMRUT

(` cr)

( 10 )

Union Budget 2016-17 Preview February 19, 2016

Exhibit 17: Allocation to Major Schemes (Under Ministry of Rural Development)

Scheme FY2014 FY2015BE FY2015RE FY2016E FY2017E

Mahatma Gandhi National Rural Employment Guarantee Scheme 32,993 34,000 33,000 34,699 37,822

Housing for all (Rural) Indira Awas Yojana 12,982 16,000 11,000 10,025 11,028

Pradhan Mantri Gram Sadak Yojana (PMGSY) 3,978 6,738 6,547 6,638 7,368

Central Road Fund (CRF) 5,827 7,653 7,653 7,654 8,495

National Social Assistance Programme (NSAP) - 10,635 7,241 9,082 10,172

Source: Budget Documents, Angel Research

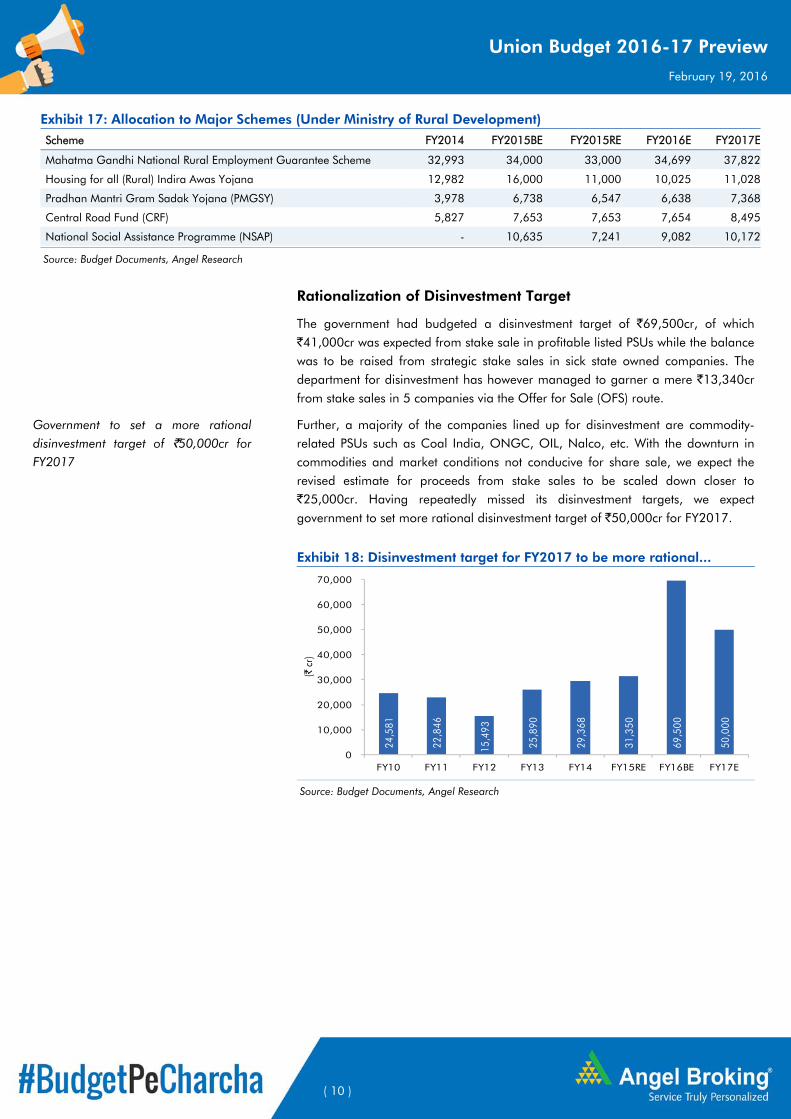

Rationalization of Disinvestment Target

The government had budgeted a disinvestment target of `69,500cr, of which `41,000cr was expected from stake sale in profitable listed PSUs while the balance was to be raised from strategic stake sales in sick state owned companies. The department for disinvestment has however managed to garner a mere `13,340cr from stake sales in 5 companies via the Offer for Sale (OFS) route.

Further, a majority of the companies lined up for disinvestment are commodity-related PSUs such as Coal India, ONGC, OIL, Nalco, etc. With the downturn in commodities and market conditions not conducive for share sale, we expect the revised estimate for proceeds from stake sales to be scaled down closer to `25,000cr. Having repeatedly missed its disinvestment targets, we expect government to set more rational disinvestment target of `50,000cr for FY2017.

Exhibit 18: Disinvestment target for FY2017 to be more rational...

Source: Budget Documents, Angel Research

24,5

81

22,8

46

15,4

93

25,8

90

29,3

68

31,3

50

69,5

00

50,0

00

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

FY10 FY11 FY12 FY13 FY14 FY15RE FY16BE FY17E

(` c

r)

Government to set a more rationaldisinvestment target of `50,000cr forFY2017

( 11 )

Union Budget 2016-17 Preview February 19, 2016

Expect a balanced budget focused on growth, while moving towards the FRBM targets

The government has so far focused on bringing about structural changes, especially in areas of foreign direct investments (FDI), thereby improving India’s image as a business destination. It has been trying to improve the ease of doing business in the country, clear issues surrounding taxation & environment approvals and better manage natural resources. The easing of FDI rules across 15 sectors showed the government’s strong resolve towards foreign investment. The government has also been specifically working on removing the legal and regulatory bottlenecks that were affecting fresh investments, such as retrospective taxation, double taxation, lack of a single window clearance, etc. India’s ranking on the ease of doing business improved four places to 130th in the world and the government is targeting to bring India in the top 50.

Some of the reforms related to the allocation of natural resources have delivered excellent results. The efforts towards streamlining fuel supply related issues have resulted in a huge reduction in coal imports. The auction of mines and telecom spectrum in a transparent fashion has been an important and indicative move, highlighting the government’s outlook towards future allocation of natural resources. We expect the government to announce more measures to further improve the ease of doing business, especially for start-ups, in the upcoming budget.

Markets are looking towards the budget for a more directional view on spending and fiscal prudence, rather than specific measures. We believe this budget will be a continuation of the government’s policy of moving gradually on the path of fiscal consolidation, while keeping infrastructure spending high. The government is laying the foundation for a structural growth map where earnings growth may be gradual, but more sustainable. The market is going through a phase where it is adjusting to this reality and realigning expectations.

Government laying the foundation for astructural growth map where earningsgrowth may be gradual, but moresustainable

( 12 )

Union Budget 2016-17 Preview February 19, 2016

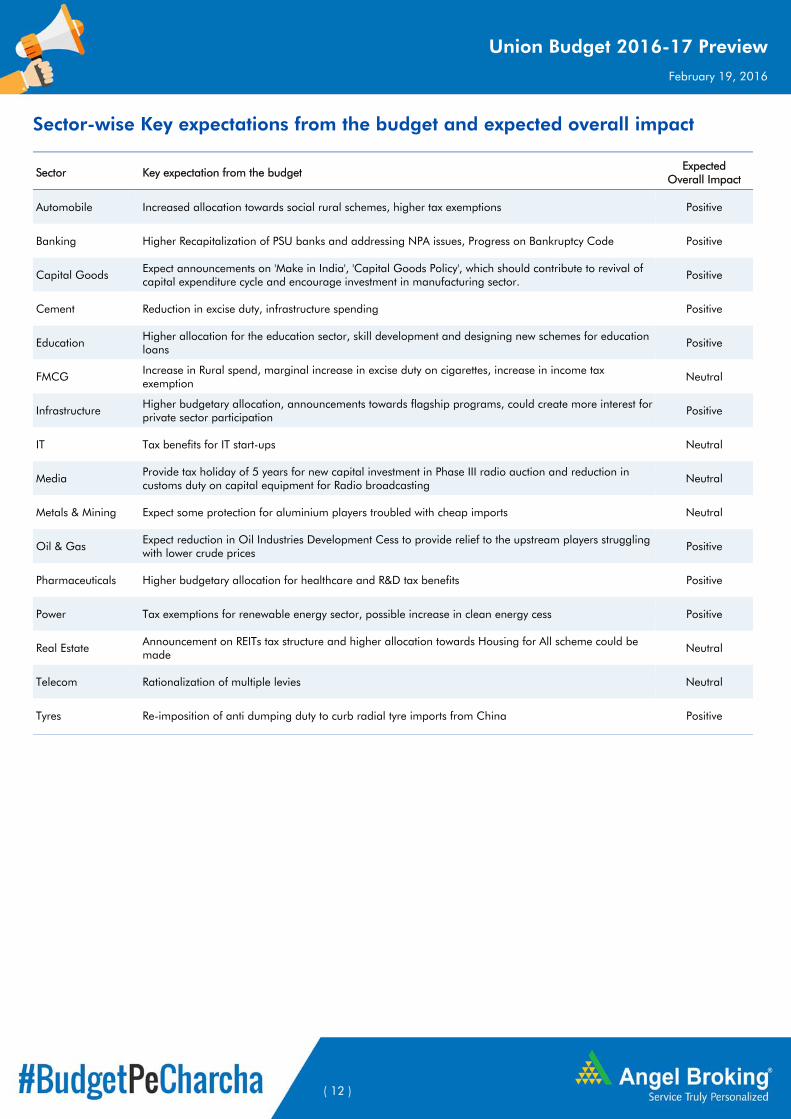

Sector-wise Key expectations from the budget and expected overall impact

Sector Key expectation from the budget Expected

Overall Impact

Automobile Increased allocation towards social rural schemes, higher tax exemptions Positive

Banking Higher Recapitalization of PSU banks and addressing NPA issues, Progress on Bankruptcy Code Positive

Capital Goods Expect announcements on 'Make in India', 'Capital Goods Policy', which should contribute to revival of capital expenditure cycle and encourage investment in manufacturing sector.

Positive

Cement Reduction in excise duty, infrastructure spending Positive

Education Higher allocation for the education sector, skill development and designing new schemes for education loans

Positive

FMCG Increase in Rural spend, marginal increase in excise duty on cigarettes, increase in income tax exemption

Neutral

Infrastructure Higher budgetary allocation, announcements towards flagship programs, could create more interest for private sector participation

Positive

IT Tax benefits for IT start-ups Neutral

Media Provide tax holiday of 5 years for new capital investment in Phase III radio auction and reduction in customs duty on capital equipment for Radio broadcasting

Neutral

Metals & Mining Expect some protection for aluminium players troubled with cheap imports Neutral

Oil & Gas Expect reduction in Oil Industries Development Cess to provide relief to the upstream players struggling with lower crude prices

Positive

Pharmaceuticals Higher budgetary allocation for healthcare and R&D tax benefits Positive

Power Tax exemptions for renewable energy sector, possible increase in clean energy cess Positive

Real Estate Announcement on REITs tax structure and higher allocation towards Housing for All scheme could be made

Neutral

Telecom Rationalization of multiple levies Neutral

Tyres Re-imposition of anti dumping duty to curb radial tyre imports from China Positive

( 13 )

Union Budget 2016-17 Preview February 19, 2016

Sector-wise Expectations

( 14 )

Union Budget 2016-17 Preview February 19, 2016

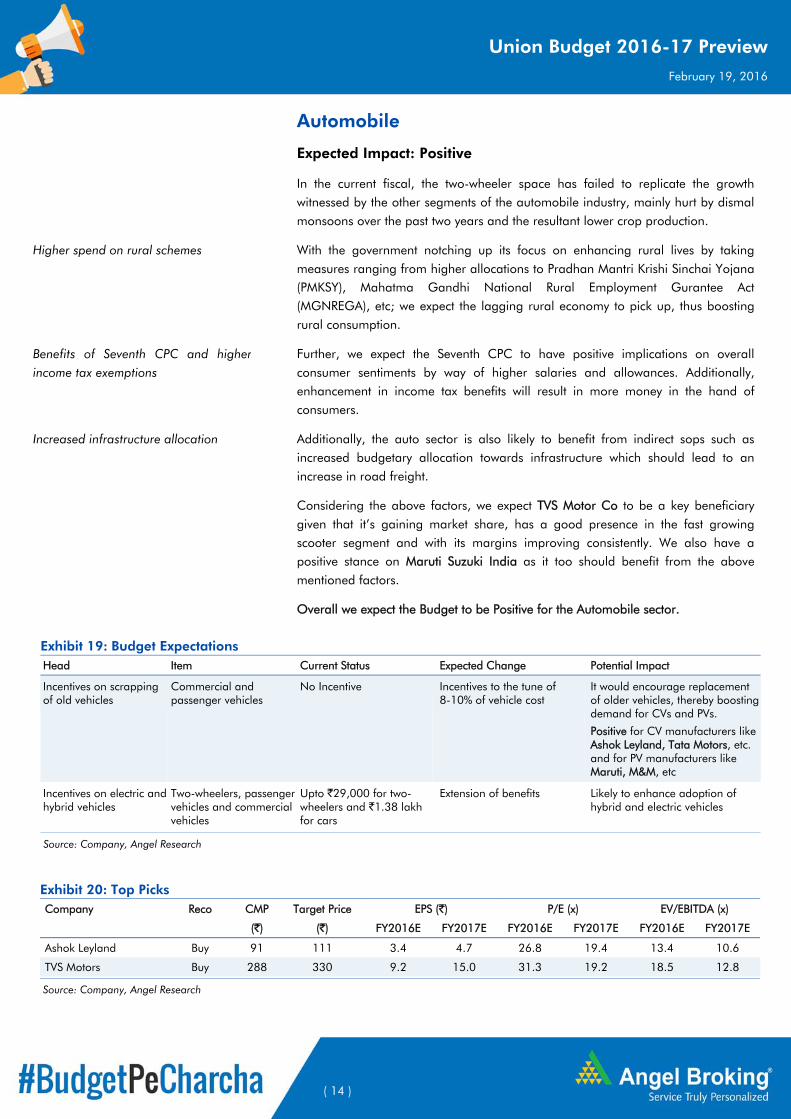

Automobile

Expected Impact: Positive

In the current fiscal, the two-wheeler space has failed to replicate the growth witnessed by the other segments of the automobile industry, mainly hurt by dismal monsoons over the past two years and the resultant lower crop production.

With the government notching up its focus on enhancing rural lives by taking measures ranging from higher allocations to Pradhan Mantri Krishi Sinchai Yojana

(PMKSY), Mahatma Gandhi National Rural Employment Gurantee Act (MGNREGA), etc; we expect the lagging rural economy to pick up, thus boosting rural consumption.

Further, we expect the Seventh CPC to have positive implications on overall consumer sentiments by way of higher salaries and allowances. Additionally, enhancement in income tax benefits will result in more money in the hand of consumers.

Additionally, the auto sector is also likely to benefit from indirect sops such as increased budgetary allocation towards infrastructure which should lead to an increase in road freight.

Considering the above factors, we expect TVS Motor Co to be a key beneficiary given that it’s gaining market share, has a good presence in the fast growing scooter segment and with its margins improving consistently. We also have a positive stance on Maruti Suzuki India as it too should benefit from the above mentioned factors.

Overall we expect the Budget to be Positive for the Automobile sector.

Exhibit 19: Budget Expectations Head Item Current Status Expected Change Potential Impact

Incentives on scrapping of old vehicles

Commercial and passenger vehicles

No Incentive Incentives to the tune of 8-10% of vehicle cost

It would encourage replacement of older vehicles, thereby boosting demand for CVs and PVs.

Positive for CV manufacturers like Ashok Leyland, Tata Motors, etc. and for PV manufacturers like Maruti, M&M, etc

Incentives on electric and hybrid vehicles

Two-wheelers, passengervehicles and commercial vehicles

Upto `29,000 for two-wheelers and `1.38 lakh for cars

Extension of benefits Likely to enhance adoption of hybrid and electric vehicles

Source: Company, Angel Research

Exhibit 20: Top Picks Company Reco CMP Target Price EPS (`) P/E (x) EV/EBITDA (x)

(`) (`) FY2016E FY2017E FY2016E FY2017E FY2016E FY2017E

Ashok Leyland Buy 91 111 3.4 4.7 26.8 19.4 13.4 10.6

TVS Motors Buy 288 330 9.2 15.0 31.3 19.2 18.5 12.8

Source: Company, Angel Research

Higher spend on rural schemes

Benefits of Seventh CPC and higherincome tax exemptions

Increased infrastructure allocation

( 15 )

Union Budget 2016-17 Preview February 19, 2016

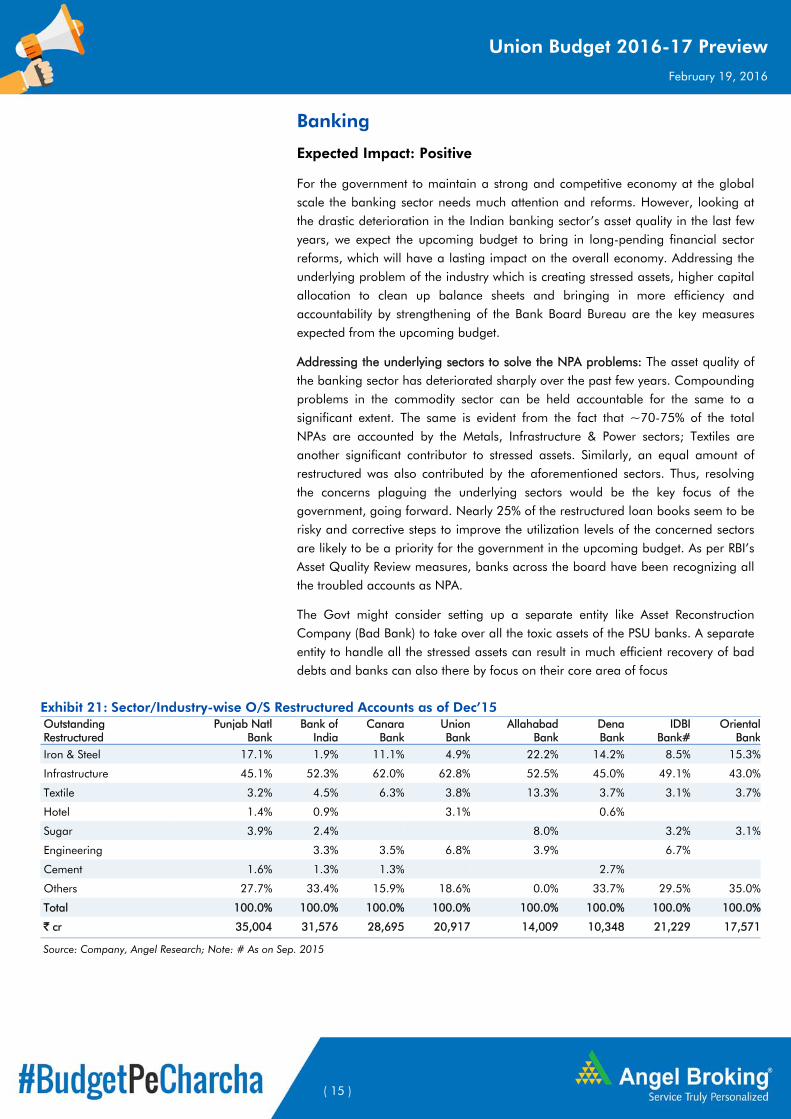

Banking

Expected Impact: Positive

For the government to maintain a strong and competitive economy at the global scale the banking sector needs much attention and reforms. However, looking at the drastic deterioration in the Indian banking sector’s asset quality in the last few years, we expect the upcoming budget to bring in long-pending financial sector reforms, which will have a lasting impact on the overall economy. Addressing the underlying problem of the industry which is creating stressed assets, higher capital allocation to clean up balance sheets and bringing in more efficiency and accountability by strengthening of the Bank Board Bureau are the key measures expected from the upcoming budget.

Addressing the underlying sectors to solve the NPA problems: The asset quality of the banking sector has deteriorated sharply over the past few years. Compounding problems in the commodity sector can be held accountable for the same to a significant extent. The same is evident from the fact that ~70-75% of the total NPAs are accounted by the Metals, Infrastructure & Power sectors; Textiles are another significant contributor to stressed assets. Similarly, an equal amount of restructured was also contributed by the aforementioned sectors. Thus, resolving the concerns plaguing the underlying sectors would be the key focus of the government, going forward. Nearly 25% of the restructured loan books seem to be risky and corrective steps to improve the utilization levels of the concerned sectors are likely to be a priority for the government in the upcoming budget. As per RBI’s Asset Quality Review measures, banks across the board have been recognizing all the troubled accounts as NPA.

The Govt might consider setting up a separate entity like Asset Reconstruction Company (Bad Bank) to take over all the toxic assets of the PSU banks. A separate entity to handle all the stressed assets can result in much efficient recovery of bad debts and banks can also there by focus on their core area of focus

Exhibit 21: Sector/Industry-wise O/S Restructured Accounts as of Dec’15 Outstanding Restructured

Punjab Natl Bank

Bank of India

Canara Bank

Union Bank

Allahabad Bank

Dena Bank

IDBI Bank#

Oriental Bank

Iron & Steel 17.1% 1.9% 11.1% 4.9% 22.2% 14.2% 8.5% 15.3%

Infrastructure 45.1% 52.3% 62.0% 62.8% 52.5% 45.0% 49.1% 43.0%

Textile 3.2% 4.5% 6.3% 3.8% 13.3% 3.7% 3.1% 3.7%

Hotel 1.4% 0.9%

3.1% 0.6%

Sugar 3.9% 2.4%

8.0%

3.2% 3.1%

Engineering 3.3% 3.5% 6.8% 3.9%

6.7%

Cement 1.6% 1.3% 1.3% 2.7%

Others 27.7% 33.4% 15.9% 18.6% 0.0% 33.7% 29.5% 35.0%

Total 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

` cr 35,004 31,576 28,695 20,917 14,009 10,348 21,229 17,571

Source: Company, Angel Research; Note: # As on Sep. 2015

( 16 )

Union Budget 2016-17 Preview February 19, 2016

Higher capital allocation to clean up balance sheets: We expect the government to address the sector’s distress by providing additional funds to PSU banks. The government had earlier planned to infuse `25,000cr each in FY2016 and FY2017 into PSU banks. We believe given the current capital adequacy of the PSU banks the government will have to set aside a much higher capital.

Exhibit 22: Tier-I Capital and Provision Coverage of various PSU banks

Name of the Bank CET I (%) CET (` cr) PCR %TTM PAT

(` cr)Net NPA

(` cr)

Indian Bank 10.37 12,673 60.8 1,090 3,881

BOB 9.84 40,540 52.7 (1,567) 21,806

SBI 9.60 130,032 65.2 12,429 40,249

PNB 8.49 36,422 53.9 1,699 22,983

Canara Bank 8.03 27,685 54.0 1,706 12,940

IDBI Bank 7.84 23,031 62.9 1,129 9,613

OBC 7.56 12,911 56.3 651 7,359

Union Bank 7.45 19,370 55.0 1,699 10,322

Vijaya Bank 7.29 5,919 58.1 407 2,633

Allahabad Bank 7.27 11,685 55.4 40 6,308

Dena Bank 7.05 6,060 49.0 (553) 5,176

BOI 7.00 24,580 54.5 (2,558) 19,979

Source: Company, Angel Research

New avenues for lending: Despite a 125bp cut in the interest rate by the RBI since January 2015, credit demand has still been weak in FY2016. According to RBI data, bank credit growth has been 8.5% for YTDFY2016 (as of January 22, 2016) compared to 6.2% for the same period of the previous year. Deposit growth for the commensurate period has also been moderate at 8.6% as compared to 8.2% in the corresponding period of the previous year.

Lack of demand for credit from capital intensive industries has impacted income growth of the banking sector on one hand while on the flip side stressed asset creation has choked funds for certain productive sectors and projects as well. We expect the government to announce corrective measures to ensure that credit flow to the needy sectors is facilitated in an efficient way. This might help in incremental credit demand for the banking sector in FY2017.

Further progress on implementation of Bankruptcy Code: The implementation of the Bankruptcy Code which has been much delayed is expected to be pushed by the government during the upcoming budget session. Currently, bankruptcy proceedings in India remain complicated with multilayered bodies and laws being involved like the Companies Act, SARFAESI Act, and the Sick Industrial Companies Act. As a result, the process of winding up companies ends up being lengthy as the courts, debt recovery tribunals and the BIFR, all having a role to play. The implementation of the Bankruptcy code will allow faster resolution of the problems and enhance the recovery process. This can prove to be an effective tool for banking and non-banking financial companies in dealing with the bad assets problem.

New avenues for lending to increasecredit demand

Progress on implementation ofBankruptcy code will enable higherrecovery of bad assets

( 17 )

Union Budget 2016-17 Preview February 19, 2016

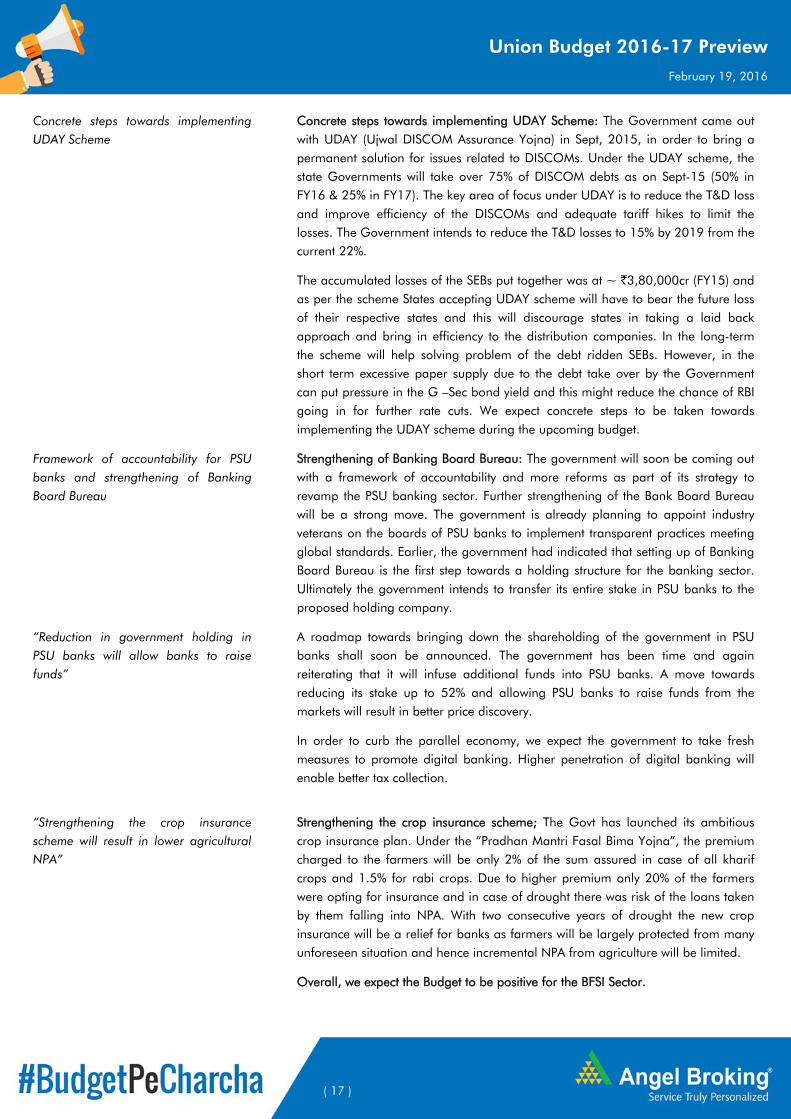

Concrete steps towards implementing UDAY Scheme: The Government came out with UDAY (Ujwal DISCOM Assurance Yojna) in Sept, 2015, in order to bring a permanent solution for issues related to DISCOMs. Under the UDAY scheme, the state Governments will take over 75% of DISCOM debts as on Sept-15 (50% in FY16 & 25% in FY17). The key area of focus under UDAY is to reduce the T&D loss and improve efficiency of the DISCOMs and adequate tariff hikes to limit the losses. The Government intends to reduce the T&D losses to 15% by 2019 from the current 22%.

The accumulated losses of the SEBs put together was at ~ `3,80,000cr (FY15) and as per the scheme States accepting UDAY scheme will have to bear the future loss of their respective states and this will discourage states in taking a laid back approach and bring in efficiency to the distribution companies. In the long-term the scheme will help solving problem of the debt ridden SEBs. However, in the short term excessive paper supply due to the debt take over by the Government can put pressure in the G –Sec bond yield and this might reduce the chance of RBI going in for further rate cuts. We expect concrete steps to be taken towards implementing the UDAY scheme during the upcoming budget.

Strengthening of Banking Board Bureau: The government will soon be coming out with a framework of accountability and more reforms as part of its strategy to revamp the PSU banking sector. Further strengthening of the Bank Board Bureau will be a strong move. The government is already planning to appoint industry veterans on the boards of PSU banks to implement transparent practices meeting global standards. Earlier, the government had indicated that setting up of Banking Board Bureau is the first step towards a holding structure for the banking sector. Ultimately the government intends to transfer its entire stake in PSU banks to the proposed holding company.

A roadmap towards bringing down the shareholding of the government in PSU banks shall soon be announced. The government has been time and again reiterating that it will infuse additional funds into PSU banks. A move towards reducing its stake up to 52% and allowing PSU banks to raise funds from the markets will result in better price discovery.

In order to curb the parallel economy, we expect the government to take fresh measures to promote digital banking. Higher penetration of digital banking will enable better tax collection.

Strengthening the crop insurance scheme; The Govt has launched its ambitious crop insurance plan. Under the “Pradhan Mantri Fasal Bima Yojna”, the premium charged to the farmers will be only 2% of the sum assured in case of all kharif crops and 1.5% for rabi crops. Due to higher premium only 20% of the farmers were opting for insurance and in case of drought there was risk of the loans taken by them falling into NPA. With two consecutive years of drought the new crop insurance will be a relief for banks as farmers will be largely protected from many unforeseen situation and hence incremental NPA from agriculture will be limited.

Overall, we expect the Budget to be positive for the BFSI Sector.

Concrete steps towards implementingUDAY Scheme

Framework of accountability for PSUbanks and strengthening of BankingBoard Bureau

“Reduction in government holding inPSU banks will allow banks to raisefunds”

“Strengthening the crop insurancescheme will result in lower agriculturalNPA”

( 18 )

Union Budget 2016-17 Preview February 19, 2016

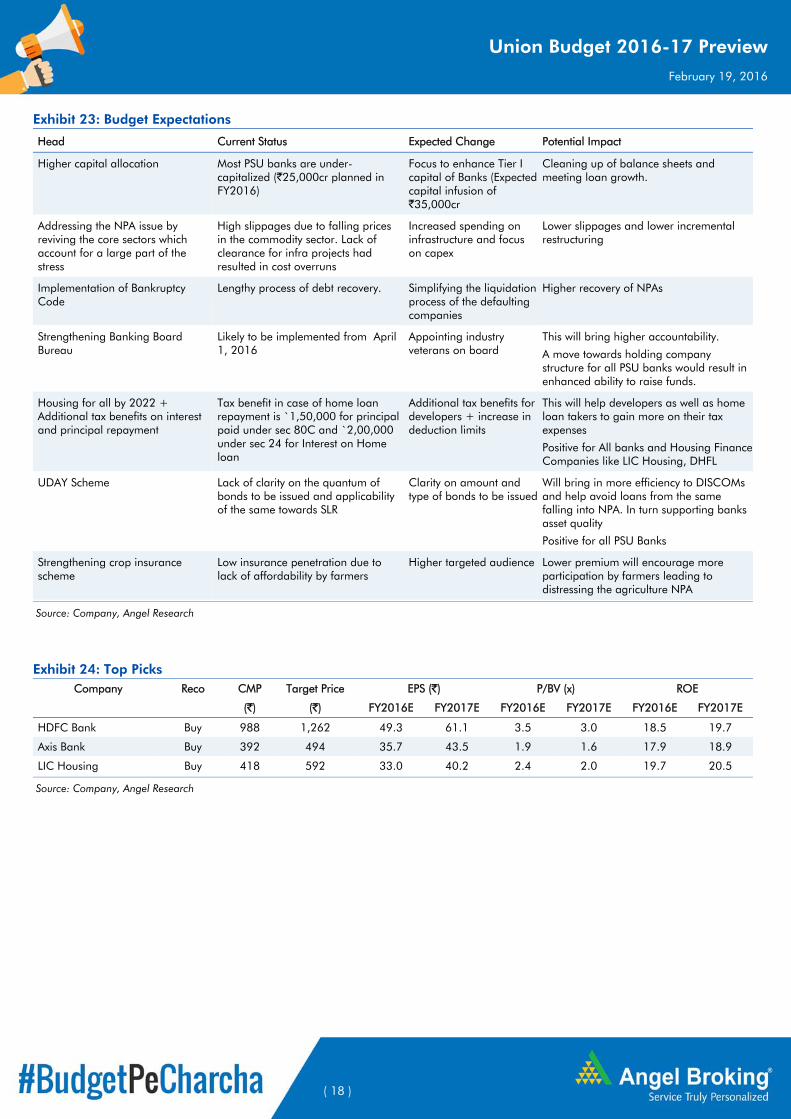

Exhibit 23: Budget Expectations

Head Current Status Expected Change Potential Impact

Higher capital allocation Most PSU banks are under-capitalized (`25,000cr planned in FY2016)

Focus to enhance Tier I capital of Banks (Expected capital infusion of `35,000cr

Cleaning up of balance sheets and meeting loan growth.

Addressing the NPA issue by reviving the core sectors which account for a large part of the stress

High slippages due to falling prices in the commodity sector. Lack of clearance for infra projects had resulted in cost overruns

Increased spending on infrastructure and focus on capex

Lower slippages and lower incremental restructuring

Implementation of Bankruptcy Code

Lengthy process of debt recovery. Simplifying the liquidation process of the defaulting companies

Higher recovery of NPAs

Strengthening Banking Board Bureau

Likely to be implemented from April 1, 2016

Appointing industry veterans on board

This will bring higher accountability.

A move towards holding company structure for all PSU banks would result in enhanced ability to raise funds.

Housing for all by 2022 + Additional tax benefits on interest and principal repayment

Tax benefit in case of home loan repayment is `1,50,000 for principal paid under sec 80C and `2,00,000 under sec 24 for Interest on Home loan

Additional tax benefits for developers + increase in deduction limits

This will help developers as well as home loan takers to gain more on their tax expenses

Positive for All banks and Housing Finance Companies like LIC Housing, DHFL

UDAY Scheme Lack of clarity on the quantum of bonds to be issued and applicability of the same towards SLR

Clarity on amount and type of bonds to be issued

Will bring in more efficiency to DISCOMs and help avoid loans from the same falling into NPA. In turn supporting banks asset quality

Positive for all PSU Banks

Strengthening crop insurance scheme

Low insurance penetration due to lack of affordability by farmers

Higher targeted audience Lower premium will encourage more participation by farmers leading to distressing the agriculture NPA

Source: Company, Angel Research

Exhibit 24: Top Picks Company Reco CMP Target Price EPS (`) P/BV (x) ROE

(`) (`) FY2016E FY2017E FY2016E FY2017E FY2016E FY2017E

HDFC Bank Buy 988 1,262 49.3 61.1 3.5 3.0 18.5 19.7

Axis Bank Buy 392 494 35.7 43.5 1.9 1.6 17.9 18.9

LIC Housing Buy 418 592 33.0 40.2 2.4 2.0 19.7 20.5

Source: Company, Angel Research

( 19 )

Union Budget 2016-17 Preview February 19, 2016

Capital Goods

Expected Impact: Positive

The government has taken several measures to revive the economy since having come to power ~2 years back and has already picked up low hanging fruits to spur economic growth. Still, the domestic economy has not witnessed any major signs of private sector capex recovery. The government has initiated strong awarding across Roads & Highways, Metros and Defense sectors, which we expect to continue going forward also. Considering the government’s thrust on infrastructure, we expect awarding to proliferate into other sectors like, housing, Smart Cities and water treatment.

FDI in Railways (select areas) has been opened up to 100% (in areas like suburban corridors, dedicated freight corridors, high speed train projects, rolling stock, and passenger terminals); while in Defense, it has been increased to 49%.

The government also announced “Make in India” scheme and “National Capital Goods Policy” intending to promote manufacturing within the country. In order to promote these schemes/policies, we won’t be surprised if the government announces (1) tax incentives for the manufacturing sector and (2) streamlines FDI policy for certain sectors. These announcements could revive the already ailing private sector capex cycle.

Indian Railways - riding on lots of hopes

Government renewed its thrust towards Indian Railways by allocating a 52.8% increase in budgetary spend to `100,011cr. A major chunk of the incremental budgetary spend was towards Dedicated Freight Corridor Corp. (DFCC), construction of new lines, doubling of lines, and towards rolling stock (including engines, coaches, wagons). Currently, Indian Railways has floated ~110 tenders worth over `3,000cr. Further, if we look at the YTD tendering as well as awarding activity, then Railways has shown signs of uptick. Also, Railways is exploring the PPP route across a few areas which should reduce its financing burden and at the same time help in raising funds to enable it to incur developmental capex.

Defense sector – a key part of the ‘Make in India’ campaign

After years of lull, the government announced a 16.9% yoy increase in core defense capital outlay to `86,536cr. Exhibiting its intent to expedite the defense sector procurement process, the Defense Acquisition Council (DAC) after being dormant for the last few years, has now become active and approved projects worth over `3 lakh cr in the last 21 months. Also, the defense sector should get a boost owing to the government’s ‘Make in India’ campaign, which emphasizes on manufacturing indigenization. Further high expectations are built on the soon to be released Defence Procurement Procedures (DPP). On a whole, we expect 15% increase in budgetary allocation.

Expect over 10% increase in allocationtowards the Railways Ministry

Allocation towards Defense sector tosee ~15% increase

( 20 )

Union Budget 2016-17 Preview February 19, 2016

Exhibit 25: Allocation towards Defense Ministry

(` in cr) Actual

FY2013-14 Rev. Budgeted

FY2014-15 Budgeted

FY2015-16 Angel Exp. FY2016-17

Ministry of Defense (core capital allocation)

72,566 74,029 86,536 99,516

Source: Angel Research, Budget Docs

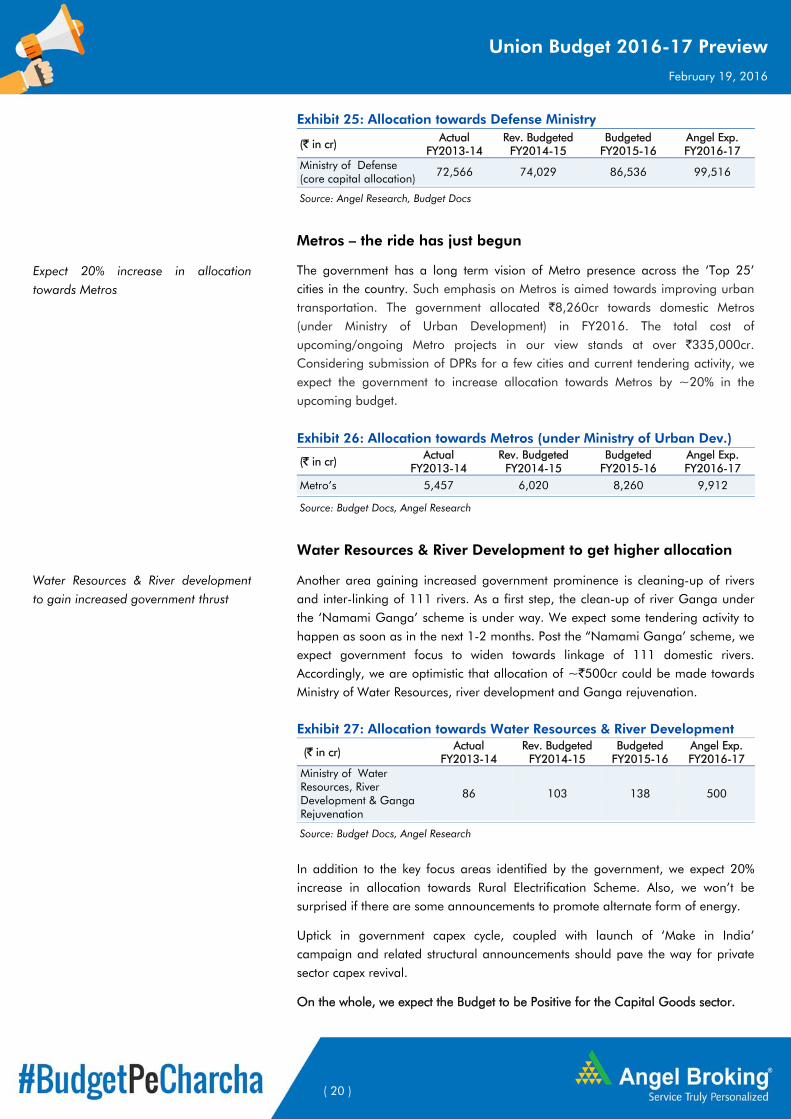

Metros – the ride has just begun

The government has a long term vision of Metro presence across the ‘Top 25’ cities in the country. Such emphasis on Metros is aimed towards improving urban transportation. The government allocated `8,260cr towards domestic Metros (under Ministry of Urban Development) in FY2016. The total cost of upcoming/ongoing Metro projects in our view stands at over `335,000cr. Considering submission of DPRs for a few cities and current tendering activity, we expect the government to increase allocation towards Metros by ~20% in the upcoming budget.

Exhibit 26: Allocation towards Metros (under Ministry of Urban Dev.)

(` in cr) Actual

FY2013-14 Rev. Budgeted

FY2014-15 Budgeted

FY2015-16 Angel Exp. FY2016-17

Metro’s 5,457 6,020 8,260 9,912

Source: Budget Docs, Angel Research

Water Resources & River Development to get higher allocation

Another area gaining increased government prominence is cleaning-up of rivers and inter-linking of 111 rivers. As a first step, the clean-up of river Ganga under the ‘Namami Ganga’ scheme is under way. We expect some tendering activity to happen as soon as in the next 1-2 months. Post the “Namami Ganga’ scheme, we expect government focus to widen towards linkage of 111 domestic rivers. Accordingly, we are optimistic that allocation of ~`500cr could be made towards Ministry of Water Resources, river development and Ganga rejuvenation.

Exhibit 27: Allocation towards Water Resources & River Development

(` in cr) Actual

FY2013-14 Rev. Budgeted

FY2014-15 Budgeted

FY2015-16 Angel Exp. FY2016-17

Ministry of Water Resources, River Development & Ganga Rejuvenation

86 103 138 500

Source: Budget Docs, Angel Research

In addition to the key focus areas identified by the government, we expect 20% increase in allocation towards Rural Electrification Scheme. Also, we won’t be surprised if there are some announcements to promote alternate form of energy.

Uptick in government capex cycle, coupled with launch of ‘Make in India’ campaign and related structural announcements should pave the way for private sector capex revival.

On the whole, we expect the Budget to be Positive for the Capital Goods sector.

Expect 20% increase in allocationtowards Metros

Water Resources & River developmentto gain increased government thrust

( 21 )

Union Budget 2016-17 Preview February 19, 2016

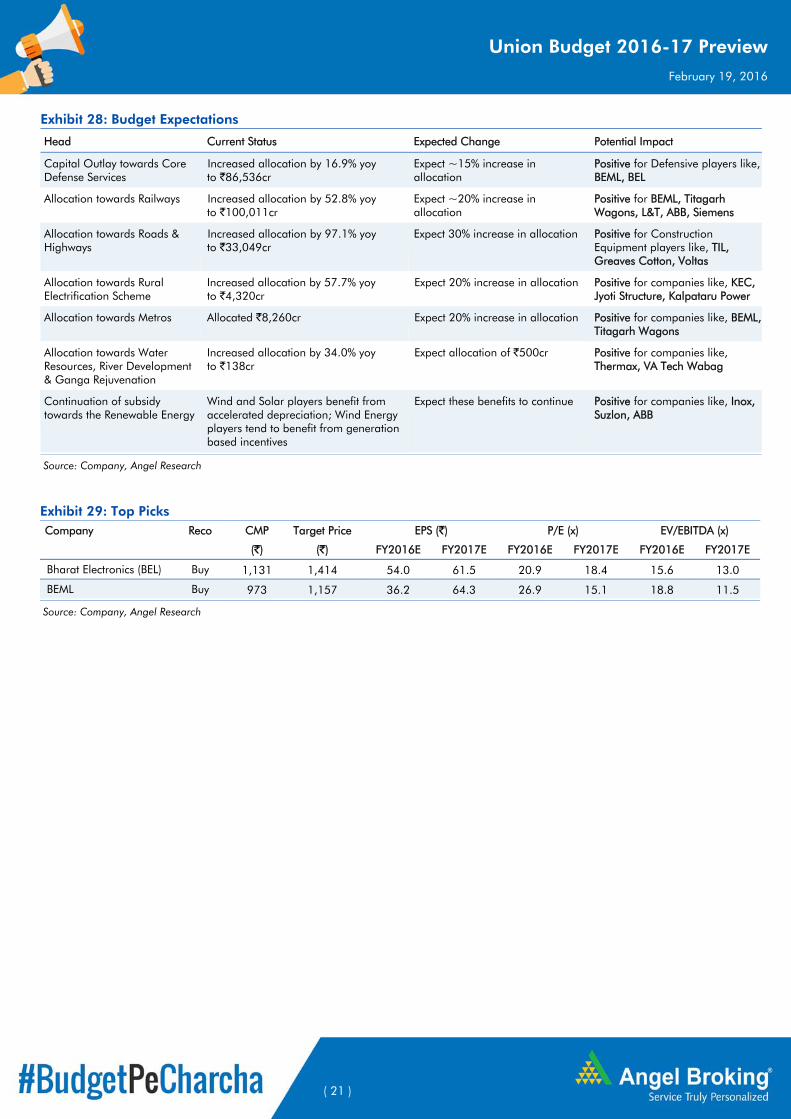

Exhibit 28: Budget Expectations

Head Current Status Expected Change Potential Impact

Capital Outlay towards Core Defense Services

Increased allocation by 16.9% yoy to `86,536cr

Expect ~15% increase in allocation

Positive for Defensive players like, BEML, BEL

Allocation towards Railways Increased allocation by 52.8% yoy to `100,011cr

Expect ~20% increase in allocation

Positive for BEML, Titagarh Wagons, L&T, ABB, Siemens

Allocation towards Roads & Highways

Increased allocation by 97.1% yoy to `33,049cr

Expect 30% increase in allocation Positive for Construction Equipment players like, TIL, Greaves Cotton, Voltas

Allocation towards Rural Electrification Scheme

Increased allocation by 57.7% yoy to `4,320cr

Expect 20% increase in allocation Positive for companies like, KEC, Jyoti Structure, Kalpataru Power

Allocation towards Metros Allocated `8,260cr Expect 20% increase in allocation Positive for companies like, BEML, Titagarh Wagons

Allocation towards Water Resources, River Development & Ganga Rejuvenation

Increased allocation by 34.0% yoy to `138cr

Expect allocation of `500cr Positive for companies like, Thermax, VA Tech Wabag

Continuation of subsidy towards the Renewable Energy

Wind and Solar players benefit from accelerated depreciation; Wind Energy players tend to benefit from generation based incentives

Expect these benefits to continue Positive for companies like, Inox, Suzlon, ABB

Source: Company, Angel Research

Exhibit 29: Top Picks Company Reco CMP Target Price EPS (`) P/E (x) EV/EBITDA (x)

(`) (`) FY2016E FY2017E FY2016E FY2017E FY2016E FY2017E

Bharat Electronics (BEL) Buy 1,131 1,414 54.0 61.5 20.9 18.4 15.6 13.0

BEML Buy 973 1,157 36.2 64.3 26.9 15.1 18.8 11.5

Source: Company, Angel Research

( 22 )

Union Budget 2016-17 Preview February 19, 2016

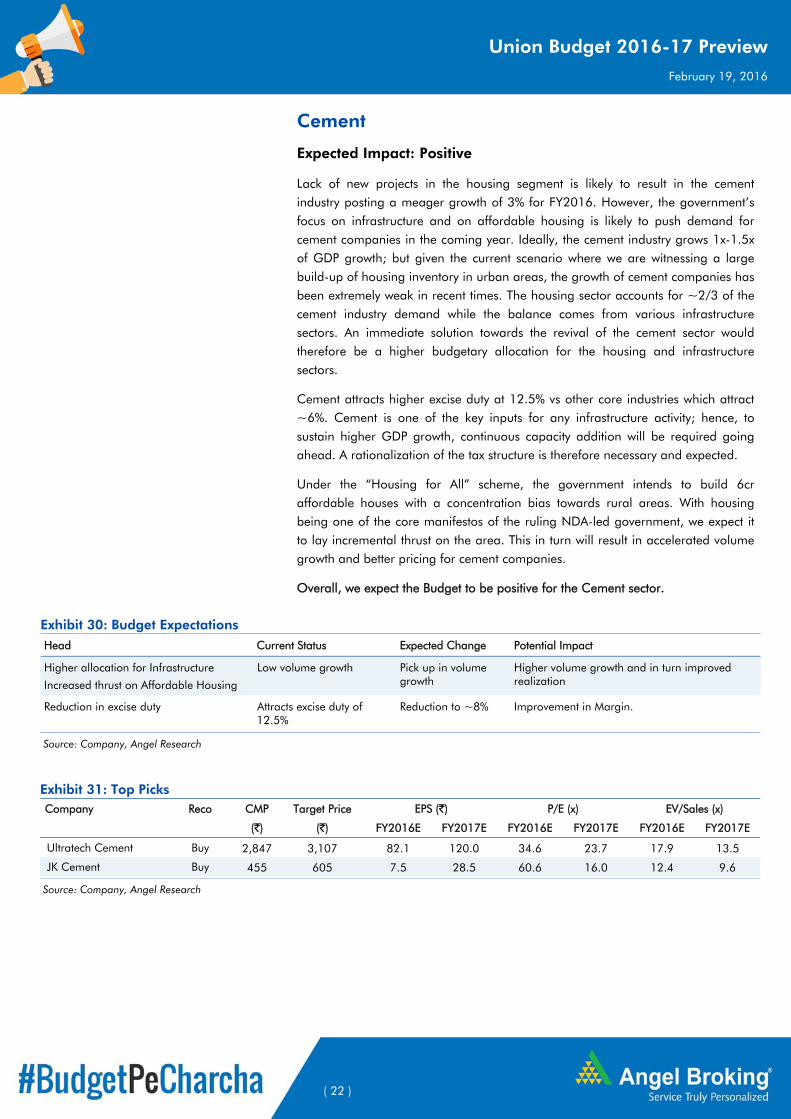

Cement

Expected Impact: Positive

Lack of new projects in the housing segment is likely to result in the cement industry posting a meager growth of 3% for FY2016. However, the government’s focus on infrastructure and on affordable housing is likely to push demand for cement companies in the coming year. Ideally, the cement industry grows 1x-1.5x of GDP growth; but given the current scenario where we are witnessing a large build-up of housing inventory in urban areas, the growth of cement companies has been extremely weak in recent times. The housing sector accounts for ~2/3 of the cement industry demand while the balance comes from various infrastructure sectors. An immediate solution towards the revival of the cement sector would therefore be a higher budgetary allocation for the housing and infrastructure sectors.

Cement attracts higher excise duty at 12.5% vs other core industries which attract ~6%. Cement is one of the key inputs for any infrastructure activity; hence, to sustain higher GDP growth, continuous capacity addition will be required going ahead. A rationalization of the tax structure is therefore necessary and expected.

Under the “Housing for All” scheme, the government intends to build 6cr affordable houses with a concentration bias towards rural areas. With housing being one of the core manifestos of the ruling NDA-led government, we expect it to lay incremental thrust on the area. This in turn will result in accelerated volume growth and better pricing for cement companies.

Overall, we expect the Budget to be positive for the Cement sector.

Exhibit 30: Budget Expectations Head Current Status Expected Change Potential Impact

Higher allocation for Infrastructure

Increased thrust on Affordable Housing

Low volume growth Pick up in volume growth

Higher volume growth and in turn improved realization

Reduction in excise duty Attracts excise duty of 12.5%

Reduction to ~8% Improvement in Margin.

Source: Company, Angel Research

Exhibit 31: Top Picks Company Reco CMP Target Price EPS (`) P/E (x) EV/Sales (x)

(`) (`) FY2016E FY2017E FY2016E FY2017E FY2016E FY2017E

Ultratech Cement Buy 2,847 3,107 82.1 120.0 34.6 23.7 17.9 13.5

JK Cement Buy 455 605 7.5 28.5 60.6 16.0 12.4 9.6

Source: Company, Angel Research

( 23 )

Union Budget 2016-17 Preview February 19, 2016

Education

Expected Impact: Positive

Education is one of the most important sectors of growing economies, including India. India is the youngest among large nations in the world with close to 54% of its population below the age of 25 years. Education and skill development are therefore crucial for the country in order to reap demographic dividends.

Considering the importance of education and skill development, we expect the government to make a higher allocation for the education sector in the upcoming budget. The funds would be spent on teacher training and development, life-skills, vocational education, digitization, technology adoption for K-12 segment in tier 2 cities and sub-urban towns (through providing institutional subsidy on education technology products) etc. Further, we expect the government to also emphasize on designing a new scheme for educational loans with low interest rates and long payment periods, which would promote higher education. We believe a skilled workforce would help the government in better executing its various development programs like ‘Make in India’ to name one.

The companies to benefit out of government thrust on the education sector in the budget would be MT Educare and NIIT which have exposure to government initiatives like teacher training and development, and also Zee Learn which has presence in the K-12 segment.

Exhibit 32: Allocation towards Education sector

(` in cr) Actual

FY2013-14 Rev. Budgeted

FY2014-15 Budgeted

FY2015-16 Angel Exp. FY2016-17

Ministry of human resource development School Education and Literacy 46,856 46,805 42,220 Department of Higher Education 24,465 23,700 26,855 Expect significantly higher allocation

Mnistry of Skill Development and Entrepreneurship - - 1,543

Source: Company, Angel Research

Overall, we expect the Budget to be Positive for the Education sector.

Exhibit 33: Budget Expectations Head Current Status Expected Change Potential Impact

Entrepreneur and Skill Development Program

`1,543cr allocated in FY16 Allocation expected to increase in FY17

Positive for companies providing skill and entrepreneurship training like MT Educare, NIIT, Zee Learn etc.

Source: Company, Angel Research

Considering India’s young demography, education is crucial for economic development of the country

Higher fund allocation expected onteacher training and development, life-skills, vocational studies, digitization,improvised scheme of educational loansetc

( 24 )

Union Budget 2016-17 Preview February 19, 2016

FMCG

Expected Impact: Neutral

The FMCG industry has been underperforming on the volume front owing to sub-normal monsoons for two consecutive years that has hurt the rural economy. However the industry has been able to sustain itself on the profitability front, mainly helped by softness in prices of crude based raw materials.

With slowing inflation and expected announcement of measures along the lines of increased allocation to rural employment schemes, increase in income tax exemptions, etc would put more money in the hands of consumers and provide a boost to the industry. A positive outcome on GST implementation will provide further respite to the industry. Additionally, FMCG is also likely to gain from the implementation of the Seventh CPC.

Governments have been invariably increasing excise duties on cigarettes by a significant proportion in budgets over the past few years which has resulted in continues decline in cigarette sales volumes. In the upcoming budget, the industry is expecting just a marginal hike in excise duty on cigarettes, which would provide some respite to the industry. On such anticipation, we are positive on ITC. Further, considering that the stock price of ITC has corrected significantly in the past one year period, the stock now poses as a good buying opportunity at the current levels.

Overall, we expect the Budget to be broadly Neutral for the FMCG sector.

Exhibit 34: Budget Expectations Head Current Status Expected Change Potential Impact

Increase in rural spending

Relatively lower allocation in last budget

Increase in allocation to marquee programs such as the Pradhan Mantri Krishi Sinchai Yojana, Rashtriya Krishi Vikas Yojana, Pradhan Mantri Gram Sadak Yojana etc.

Will provide a boost to the overall rural economy.

Positive for the entire FMCG sector which has significant rural exposure

Marginal increase in Excise duty on cigarettes

Duty varies as per the length of the cigarette stick

Marginal hike in excise duty on cigarettes

Correction in the declining trend of cigarette sales volumes.

Positive for companies like ITC, Godfrey Phillips, VST Industries etc.

End excise exemption on some items to realign with GST (food related items - green tea, dairy spreads, yoghurt, cheese, etc)

0-6% 12.0% Will have a Negative impact in the short run till the implementation of GST. Companies like Britannia, Dabur, Nestle, etc would be impacted

Increase in income tax exemption slabs

Age below 60 year – exemption is up to `2,50,000

Increase up to `4,00,000 It will leave more money in the hands of consumers which would boost demand for FMCG companies

Source: Company, Angel Research

Exhibit 35: Top Picks Company Reco CMP Target Price EPS (`) P/E (x) EV/EBITDA (x)

(`) (`) FY2016E FY2017E FY2016E FY2017E FY2016E FY2017E

ITC Buy 304 359 12.2 12.9 24.9 23.6 15.5 14.4

Source: Company, Angel Research

Underperformance on volume frontowing to sub-normal monsoons

Higher allocations towards ruralemployment, increase in Income Taxexemptions, etc to boost rural spending

( 25 )

Union Budget 2016-17 Preview February 19, 2016

Infrastructure

Expected Impact: Positive

Myriad regulations and complicated government machinery led to slowdown in the infrastructure sector, although the sector now seems to be on an early path to recovery. The NDA-led government currently in power is striving towards easing the regulatory environment and the same is highlighted by the fact that the number of stalled road projects has come down to ~14-15 from ~384 two years back. Also, some large infra projects have got fresh clearances. This reflects the Prime Minister’s Office (PMO) and Cabinet Committee’s (CC) proactive solution driven approach in clearing projects. On similar lines, after being dormant for quite a while, both, Environment and Forest department machineries have become more active in giving clearances than in the recent past. With the central government having set the wheel rolling and bureaucratic functioning improving gradually, some state governments too have become active in announcing reform measures in recent times. As a result, a favorable environment for increased private sector participation in respective states has been created.

The central government has also initiated key flagship programs such as ‘Make in India’, ‘Housing for All’, ‘Smart City’, ‘AMRUT’ and ‘Inland Waterways’ in the last 1-year period. It is in the process of laying down the ground rules and defining the execution framework for these programs. Some sectors (like Roads & Highways and Defense) where the government has been laying particular thrust and are already witnessing uptick in tendering / awarding activity is recent times, should see higher budgetary allocation.

Roads & Highways - Awarding momentum to catch-up..

In the previous budget, the government had set an ambitious target of awarding `75,000cr of road projects vs `21,000cr in the year prior to it. For 9MFY2016, NHAI has already awarded projects worth `33,900cr while another `70,500cr of NHAI road projects are at various stages of tendering and awarding.

Exhibit 36: MoRTH Funding mix (` in cr) FY2015 FY2016

NHAI+MoRTH 21,000 75,000

Borrowings 4,230 42,000

Budget Allocation 16,770 33,000

Source: Angel Research, Budget Docs

Exhibit 37: NHAI awarding details

kms Value

YTD (Dec-2015) 2,757 33,900

- EPC 1,923 21,200

- BOT 803 10,800

- Hybrid 31 1,900

Source: NHAI, Angel Research

Exhibit 38: NHAI tendering details

kms Value

YTD (Dec-2015) 4,700 70,564

- EPC 1,766 26,648

- BOT 2,245 30,290

- Hybrid 689 13,626

Source: NHAI, Angel Research

Faster clearance, uptick in awarding iscreating a favorable environment forincreased private sector participation

Budget to provide for higher allocationtowards flagship programs

Allocation towards Roads & Highwaysto increase by ~30%

( 26 )

Union Budget 2016-17 Preview February 19, 2016

Assuming that NHAI would set an awarding target of 15,000kms in FY2017 and given the current tendering pipeline, we are expecting a 30% increase in budgetary allocation towards the Roads & Highways Ministry.

Exhibit 39: Allocation towards MoRTH

(` in cr) Actual

FY2013-14 Rev. Budgeted

FY2014-15 Budgeted

FY2015-16 Angel Exp. FY2016-17

Ministry of Road Transport & Highways (MoRTH)

14,891 16,770 33,049 42,964

Source: Budget Docs, Angel Research

‘Smart City’ & ‘AMRUT’ draw government focus

Another thrust area for the government are the ‘Smart City’, ‘AMRUT’, and ‘Housing for All’ schemes. Of the identified 100 Smart Cities, early stage work has commenced across the first 20 cities, with awarding momentum expected to catch-up from 2HFY2017 onwards. We sense that very little of the allocated ~`2,000cr has been utilized towards the ‘Smart City’ scheme. However, with awarding for 20 Smart Cities nearing project life cycles, allocation towards Smart Cities would increase by 20%. Also, more clarity on the broader funding mechanism of Smart Cities will emerge soon.

~`500cr of the `3,899cr allocated towards AMRUT scheme has been released towards project execution to respective state level authorities.

On the whole, we expect ~20% increase in allocation towards these 2 schemes.

Exhibit 40: Allocation towards Smart City & AMRUT

(` in cr) Actual FY2013-14

Rev. Budgeted FY2014-15

Budgeted FY2015-16

Angel Exp. FY2016-17

Smart City & AMRUT 0 0 5,898 7,078

Source: Budget Docs, Angel Research

‘Housing for All, 2022’ & Rural Infra- Higher allocation expected

The first phase (Apr-2015 to Mar-2017) of the `2 lakh cr ’Housing for All, 2022’ scheme covering 305 cities and towns is under way. A delay in submitting DPRs and disengagement of experts from local cities is however causing implementation delays. Given the government’s increased thrust, when coupled with clubbing of all the earlier government housing schemes under ’Housing for All’ scheme, we are optimistic that this scheme would get a 10% increase in the budgetary allocation.

Allocation towards ‘Smart Cities’,‘AMRUT’ to increase by ~20%

Allocation to ‘Housing for All’ schemeto increase by ~10%

( 27 )

Union Budget 2016-17 Preview February 19, 2016

Exhibit 41: Allocation towards ‘Housing for All’ (under various Ministries)

(` in cr) Actual

FY2013-14 Rev. Budgeted

FY2014-15 Budgeted

FY2015-16 Angel Exp. FY2016-17

Housing & Poverty Alleviation 12,759 14,752 20,217 22,239

Rural Development 22,787 25,195 24,316 26,748 Allocation to Rural Infra and ‘Housing for All’ 35,546 39,947 44,533 48,986

Source: Company

After getting neglected in previous budget, we expect ~10% increase in allocation towards rural infrastructure (include roads and bridges) schemes.

In addition to the allocation details shared, we have high conviction that announcements on following fronts would be made:

(1) More details on `20,000cr National Investment and Infrastructure Fund (NIIF).

(2) Removal of Dividend Distribution Tax (DDT) on dividend payouts by SPVs to Infrastructure Investment Trusts (InvITs).

(3) Roadmap on how the PPP space could be revived.

(4) Commentary on faster execution of the Dedicated Freight Corridors and Industrial Corridors.

We also expect some announcements towards the Ports sector, although the probability of the same is low. These could include, announcement of setting-up 3 greenfield ports, scrapping-up of Tariff Authority for Major Ports (TAMP; applicable on government backed major ports).

Positive announcements in the budget should give further direction towards the growth prospects of the aforementioned schemes and initiatives, despite them having had a slow start. On the whole, announcement on the above lines could lead to uptick in awarding cycle from the government’s side, which would be favorable for the sector. All in all, we expect the upcoming Budget to be Positive for the Infrastructure sector.

( 28 )

Union Budget 2016-17 Preview February 19, 2016

Exhibit 42: Budget Expectations

Head Current Status Expected Change Potential Impact

Capital Outlay on Roads & Highways Increased allocation by 97.1% yoy to `33,049cr

Expect ~30% increase in allocation

Positive for Road sector focused EPC players like, KNR, MBL

Budgetary Allocation by Ministry of Housing & Poverty Alleviation

Increased allocation by 37.0% yoy to `20,217cr

Expect 10% increase in allocation Positive for smaller EPC players

Allocation towards Ministry of Rural Development (schemes focused on rural housing, roads and bridges)

Lowered allocation by 3.5% yoy to `24,316cr

Expect 10% increase in allocation Positive for unlisted EPC players

Allocation towards Urban Development Ministry (covers Smart City & AMRUT scheme)

Allocated `5,898cr towards these 2 flagship programs

Expect ~20% increase in allocation towards these schemes

Positive for Infra players like, NBCC, L&T

Dividend Distribution Tax (DDT) for InvITs

Current DDT makes the yield on InvITs unattractive

To make the yields attractive, DDT on dividend payouts by SPVs to the InvITs could be removed

Positive for players like, MEP Infra, IRB Infra

De-Regulation of major ports Currently governed by TAMP Expect scrapping of TAMP Neutral, as private port players would be less affected

Source: Company, Angel Research

Exhibit 43: Top Picks

Company Reco CMP Target Price EPS (`) P/E (x) EV/EBITDA (x)

(`) (`) FY2016E FY2017E FY2016E FY2017E FY2016E FY2017E

KNR Construction Buy 452 603 44.2 38.6 10.2 11.7 9.9 6.6

Sadbhav Engineering Buy 231 289 8.2 11.7 28.0 19.8 13.2 10.8

NBCC Buy 858 1,089 29.6 39.8 29.0 21.6 21.4 14.7

L&T Buy 1,151 1,310 42.0 53.0 27.2 21.7 24.6 17.9

Source: Company, Angel Research

( 29 )

Union Budget 2016-17 Preview February 19, 2016

Information Technology

Expected Impact: Neutral

According to a recent report released by Nasscom, Indian IT’s (US$132bn) share in the country’s total service exports is estimated at over 45% and the industry’s contribution relative to India’s GDP is over 9.3%. Overall, the industry is estimated to employ nearly 3.7mn people going forward, implying an addition of ~200,000 people from the current numbers. Its share in the global sourcing arena was ~56% in 2015. In 2015, a turbulent economic environment, volatility in currency, and technological shifts impacted global IT spend, which grew by a meager 0.4% to US$1.2trn. Unlike global spending, global sourcing continued its growth journey, posting an 8.5% growth in 2015 to an estimated US$162-166bn.

Following are the projections from Nasscom for FY2016:

India’s IT-BPM industry is projected to grow 8.5% in FY2016 to US$143bn from US$132bn in FY2015.

Exports in FY2016 are estimated at US$108bn, a 10.3% annual growth.

In FY2016, the domestic market is set to grow by around 10% in INR terms.

India’s IT-BPM sector’s total revenue is projected to reach US$350bn by 2025, a CAGR of 10.5%.

In terms of the budget, the industry is unlikely to get any major incentives, barring a few like tax benefits for start-ups. Any tax benefits on MAT will be a bonus. Overall, we expect the Budget to be broadly Neutral for the sector.

Exhibit 44: Budget Expectations Head Item Current Status Expected Change Potential Impact

MAT Exempt start-ups from direct and indirect taxes including MAT to reduce compliance burden and better cash flows.

Also allow carry forward of losses even if there is change in ownership structure to facilitate capital infusion in these entities. This will create a conducive environment for developing innovative products.

MAT Rate-18.5% (excluding surcharges)

To be made nil Will benefit all the companies, as IT companies invest in start-ups.

Source: Company, Angel Research

Exhibit 45: Top Picks Company Reco CMP Target Price EPS (`) P/E (x) EV/EBITDA (x)

(`) (`) FY2016E FY2017E FY2016E FY2017E FY2016E FY2017E

HCL Tech Buy 850 1,038 51.1 57.7 16.6 14.7 11.1 8.8

Infosys Buy 1,124 1,347 59.4 65.4 18.9 17.1 12.7 10.7

Source: Company, Angel Research

Outlook on industry robust; budgetshould be a non-event

( 30 )

Union Budget 2016-17 Preview February 19, 2016

Media

Expected Impact: Neutral

As per FICCI, the media and entertainment industry is expected to post a CAGR of 13.9% over CY2015-19 to `1,96,400cr on the back of growth in regional markets, digitization push, strength in the film sector, and fast growing new media businesses.

In the radio segment, if the e-auction of the first batch of private FM Radio Phase III channels gets completed, then we can expect favourable announcements towards successful auctions of further batches. The benefits of the same could include reduction in import duty on radio broadcasting equipment, tax holidays for new capital investment etc. Overall, we expect the Budget to be Neutral for the Media sector.

Exhibit 46: Budget Expectations Head Current Status Expected Change Potential Impact

Phase III of Digitization - Provide tax holiday of 5 years for new capital investment in Phase III

Would be Positive for ENIL, HT Media, DB Corp etc.

Custom Duty: Reduce capital

customs duty on equipment for radio broadcasting

- Expected to reduce to 4% Would be Positive for all radio broadcasting companies like ENIL, HT Media, DB Corp etc which have radio subsidiaries.

Source: Company, Angel Research

Exhibit 47: Top Picks Company Reco CMP Target Price EPS (`) P/E (x) EV/EBITDA (x)

(`) (`) FY2016E FY2017E FY2016E FY2017E FY2016E FY2017E

Jagran Prakashan Buy 152 189 8.9 9.9 17.1 15.3 8.0 7.7

Source: Company, Angel Research

Industry expected to post a CAGR of13.9% over next four years

Announcements favouring successfulauctioning of Phase III Radio licensing

( 31 )

Union Budget 2016-17 Preview February 19, 2016

Metals & Mining

Expected Impact: Neutral

The government has already taken steps to protect the domestic steel industry from the pressure of cheap imports. An anti-dumping duty of up to $316/tonne was levied on certain variety of hot-rolled flat products of stainless steel from three countries, including China, to protect domestic producers from below-cost inbound shipments. The government raised the import tax on certain steel products to 12.5% in August 2015 from 10% earlier. In September, a 20% safeguard duty was levied for 200 days on certain flat steel products, including hot-rolled coils.

Finally, a minimum import price was announced earlier this month on 173 steel products ranging between $341-$752/tonne, which would remain in place for six months. We believe a lot of measures have already been taken pre budget and we do not expect the government to make any major announcement for the metals sector. We however expect some protection to be extended to the aluminium sector, which remains troubled from import pressures as well.

We believe the government’s thrust on the infrastructure sector and steps to revive the investment cycle would in general be positive for the metals/mining sector.

Overall, we expect the Budget to be broadly Neutral for the Metals and Mining sector.

Exhibit 48: Budget Expectations Head Item Current Status Expected Change Potential Impact

Duties Import Duty on Steel 12.5% on flat products

10% on long products

Increase to 15-25% Positive for domestic steel players such as JSW Steel, Tata Steel, Sail

Duties Customs Duty on Coking Coal

Increased to 2.5% in last budget Reduce to Nil Positive for domestic steel players

Duties Basic Customs Duty on Metallurgical Coke

Increased from 2.5% to 5% in last budget

Reduce to Nil Positive for domestic steel players such as JSW Steel, Tata Steel, Sail

Duties Basic Customs Duty on Aluminium Products

5% currently Increase to 10% Positive for Hindalco, Nalco, Vedanta

Source: Company, Angel Research

Exhibit 49: Top Picks Company Reco CMP Target Price EPS (`) P/E (x) EV/EBITDA (x)

(`) (`) FY2016E FY2017E FY2016E FY2017E FY2016E FY2017E

Coal India Buy 313 380 22.4 25.8 13.9 12.1 8.2 7.0

Source: Company, Angel Research

With the safeguard duty and Minimumimport price, we do not expect anysignificant measures for steel players

We may see some protection extendedto the aluminium sector, which remainstroubled from import pressures

( 32 )

Union Budget 2016-17 Preview February 19, 2016

Oil & Gas

Expected Impact: Positive

Crude prices have fallen significantly this fiscal, resulting in lower under-recoveries and subsidy burden for the OMCs as well as upstream players. However, it has affected the profitability of upstream companies such as ONGC and OIL.

We expect the government to provide some relief to the upstream players with the removal of the Oil Industry Development (OID) cess levied on crude oil produced from nomination blocks and pre-NELP exploratory blocks. OID cess was last revised in March 2012 when crude was trading above $100/barrel. The existing rate of `4,500/tonne works out to ~$10/barrel at current exchange rates, with crude trading at ~$30/barrel. At these levels, a $10/barrel cess is clearly unviable and we expect the government to move to a mechanism of levying cess on an ad-valorem basis.

Overall, we expect the Budget to be Positive for the Oil & Gas sector.

Exhibit 50: Budget Expectations Head Item Current Status Expected Change Potential Impact

Cess Oil Industries Development cess

Currently `4,500/MT Levy on ad-valorem basis at 8%-10%/barrel

Positive for upstream players such as ONGC, OIL

Duties Customs Duty on LNG

LNG imports attract a customs duty of 5%

Reduce to 2.5% Positive for Petronet LNG

Source: Company, Angel Research

Exhibit 51: Top Picks Company Reco CMP Target Price EPS (`) P/E (x) EV/EBITDA (x)

(`) (`) FY2016E FY2017E FY2016E FY2017E FY2016E FY2017E

Reliance Industries Buy 945 1,150 91.3 102.6 10.4 9.2 9.5 8.4

Source: Company, Angel Research

Upstream companies bearing the bruntof lower crude prices may see somebenefits

( 33 )

Union Budget 2016-17 Preview February 19, 2016

Pharmaceutical

Expected Impact: Positive

FY2016 has been challenging for the pharma sector so far with respect to the USFDA surveillances, with a majority of plants across companies under the scanner. While many companies are taking corrective actions and are expected to come out clean in some time, others like the erstwhile Ranbaxy Labs and Wockhardt, to name a few, have been struggling for years. Also, while some companies like Sun Pharma and Dr Reddy’s Labs have taken third party sourcing as a way to mitigate the risk, others like IPCA Labs are opting to continue with their current facilities and resume US operations once they get the necessary clearances. With increased vigilance of the USFDA, the investment risk associated with pharma companies has increased much more than earlier with the US now accounting for ~20-50% of exports of most companies. Bigger pharma companies have an even higher exposure to the region. Apart from this, the domestic formulation growth has been robust, growing at 13-14% yoy, driven primarily by volumes and prices.

Thus, while FY2016 has been lackluster, FY2017 will likely witness a gradual improvement. The sector is unlikely to benefit from the budget, unless there are announcements with regards tax benefits either on R&D expenses or on the corporate front. Other benefits in the form of indirect sops such as increased budgetary allocation for healthcare will provide some boost to the sector.

Overall, we expect the Budget to be broadly Positive for the Pharmaceuticals sector.