university of leipzig institute for economic policy of leipzig institute for economic policy ......

TRANSCRIPT

December 2014 1

University of Leipzig Institute for Economic Policy

Prof. Dr. Gunther Schnabl

Experiences with the Current EU Economic

Governance Framework

European Parliament Committee on Economic and Monetary Affairs

Brussels, 10. December 2014

Prof. Dr. Gunther Schnabl, Institute for Economic Policy

2

Table of Contents 1. The Global Context of Current Account Imbalances 2. Crisis Patterns 3. Origins of the European Debt Crisis 4. Effectiveness of the Macroeconomic Surveillance 5. Outlook Abad, José / Löffler, Axel / Schnabl, Gunther / Zemanek, Holger

2013: Fiscal Divergence and TARGET2 Imbalances in the EMU. Intereconomics 48, 1, 51-58

Duarte, Pablo / Schnabl, Gunther 2014: Macroeconomic Policy Making, Exchange Rate Adjustment and Current Accounts in Emerging Markets. CESifo Working Paper 5064.

Schnabl, Gunther / Wollmershäuser, Timo 2012: Fiscal Divergence and Current Account Imbalances in Europe. CESifo Working Paper 4801.

December 2014 Prof. Dr. Gunther Schnabl, Institute for Economic Policy

3

1. The Global Context of Current Account Imbalances

Structural Break in Global Imbalances • Global imbalances have substantially increased since the late 1990s. • Regional dimensions ($, €):

– US current account deficit (since early 1980s), – rising East Asian current account surpluses (since early 1980s), – rising current surpluses of oil-exporting countries (since 2001), – intra-European current account imbalances (2001-2014).

Determinants of Global Imbalances (Duarte and Schnabl 2014) • Benign global liquidity conditions (starting from 2001), • divergent monetary and fiscal policy stances, • only to a minor extent exchange rates /membership in a monetary

union matter.

December 2014 Prof. Dr. Gunther Schnabl, Institute for Economic Policy

4

Growing Global Imbalances

December 2014 Prof. Dr. Gunther Schnabl, Institute for Economic Policy

5

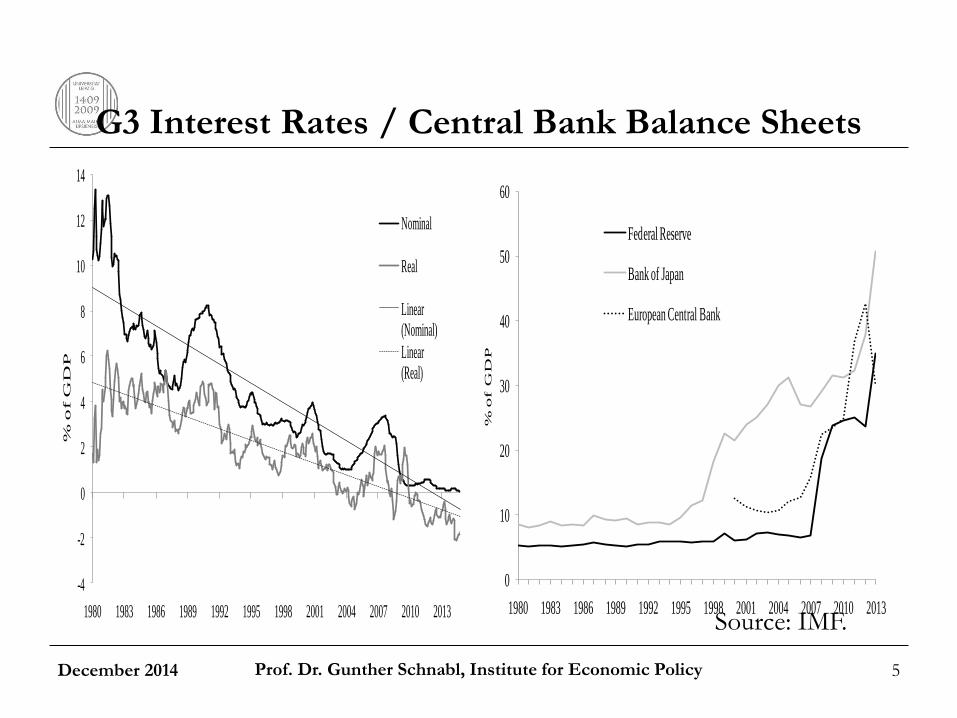

G3 Interest Rates / Central Bank Balance Sheets

December 2014 Prof. Dr. Gunther Schnabl, Institute for Economic Policy

-4

-2

0

2

4

6

8

10

12

14

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010 2013

Nominal

Real

Linear (Nominal)

Linear (Real)

% o

f G

DP

0

10

20

30

40

50

60

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010 2013

% o

f G

DP

Federal Reserve

Bank of Japan

European Central Bank

Source: IMF.

6

2. Crisis Patterns

1st and 3rd Generation of Balance of Payments Crisis Models • Capital inflows encourage domestic consumption, government

expenditure and current account deficits, which become unsustainable (Krugman 1979, Flood/Garber 1984).

• Capital inflows are paired with speculative investment and unsustainable international foreign currency-denominated debt positions (Krugman 1998, Corsetti/Pensenti/Roubini 1999). Overlending, overborrowing, moral hazard path the way into crisis.

Monetary Policy-Induced Boom and Bust • Ample low-cost liquidity causes boom and bust in financial markets

(Wicksell 1898, Hayek 1929, Schnabl and Hoffmann 2008, 2011). • Ample liquidity paired with negative domestic expectations triggers

capital outflows / current account surpluses, which encourage boom and bust abroad (Schnabl and Wollmershäuser 2013).

• Foreign crisis goes along with negative balance sheet shocks for domestic financial institutions (Japan and Asian crisis, US-subprime market and Germany) (Hoffmann and Schnabl 2014).

December 2014 Prof. Dr. Gunther Schnabl, Institute for Economic Policy

7

Pre-EMU • (Relative) expansionary fiscal policies in the south and west of Europe

were matched by relative expansionary monetary policies. • Current account deficits were constrained by limited foreign reserves,

limited credit mechanisms, exchange rate depreciation and risk premiums originating in macroeconomic instability.

• In the north tight monetary policy (led by the German central bank) put a limit on domestic inflation and private capital outflows.

Post-Euro Introduction • Monetary expansion after the bursting of the dotcom bubble from

2001. • Tight fiscal policy in Germany is triggered by consolidation efforts

after the end of the unification boom (Maastricht, Agenda 2010). • Capital inflows into southern, western and eastern European

countries (inside and outside the euro area) lead to fiscal expansion as well as bubbles in financial and real estate markets.

• Current account deficits (and surpluses?) became a key indicator for crisis (MIP).

3. Origins of the European Debt Crisis

December 2014 Prof. Dr. Gunther Schnabl, Institute for Economic Policy

8

EMU Monetary Policy Beyond Taylor-Target?

December 2014 Prof. Dr. Gunther Schnabl, Institute for Economic Policy

-6

-5

-4

-3

-2

-1

0

1

2

3

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Per

cen

t

GIIPS

Germany

Source: Abad et al. 2013.

9

Fiscal Policy Stances in the EMU

December 2014 Prof. Dr. Gunther Schnabl, Institute for Economic Policy

Source: Schnabl and Wollmershäuser 2013.

10

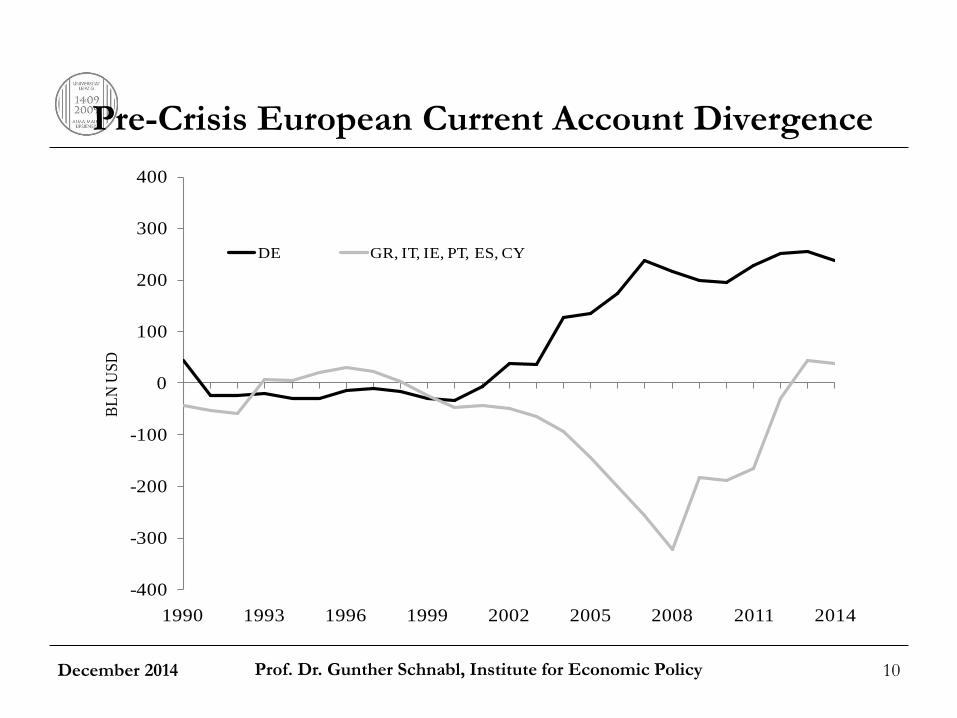

Pre-Crisis European Current Account Divergence

December 2014 Prof. Dr. Gunther Schnabl, Institute for Economic Policy

-400

-300

-200

-100

0

100

200

300

400

1990 1993 1996 1999 2002 2005 2008 2011 2014

BL

N U

SD

DE GR, IT, IE, PT, ES, CY

11

(Previous) Crisis Countries • Fiscal tightening (combined with monetary easing) has

contributed to the consolidation of government spending, real estate price dynamics and risks taken in the national financial sectors. (EIP, Adjustment Programs, etc.)

• Current account deficits have become widely consolidated. The Risk of Growing Current Account Surpluses • Expansionary E(M)U monetary policy becomes increasingly

paired with relatively tight EU fiscal policies. • Current account surpluses have become redirected towards third

countries, in particular UK and US, but also France. • Depending on the type of risk taken in international capital

markets, new crisis potential may emerge for the EU-current account surplus countries and the EU as a whole.

4. Effectiveness of Macroeconomic Surveillance

December 2014 Prof. Dr. Gunther Schnabl, Institute for Economic Policy

12

The Consolidation of European Current Accounts

December 2014 Prof. Dr. Gunther Schnabl, Institute for Economic Policy

Source: IMF.

-400

-300

-200

-100

0

100

200

300

400

500

1990 1993 1996 1999 2002 2005 2008 2011 2014

BL

N U

SD

FR, GB

SI, SK, RO, MT, LT, LV, HR, CZ, GB, EE, PL

DE, AT, DK, SE, FI, NL, BE, LU

GR, ES, PT, IT, IE, CY

13

The Redirection of German Capital Outflows (Proxy)

December 2014 Prof. Dr. Gunther Schnabl, Institute for Economic Policy

-300

-250

-200

-150

-100

-50

0

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014*

BL

N U

SD

GR, IT, IE, PT, ES

FR, GB, US

World

Source: IMF DOTS *estimation from first two quaters

14

5. Outlook

• Monetary expansion and divergent fiscal policies have been at the root of diverging current account positions in Europe since 2001.

• Since the European debt crisis intra-EU expenditure patterns have tended to converge linked to the macroeconomic imbalance procedure.

• This has contributed to a consolidation of the intra-European current account imbalances.

• At the same time the E(M)U current account surplus is growing. • Depending on the risks taken in foreign capital markets a new

crisis for European surplus countries may emerge. • The policy implication is a tighter monetary policy stance, more

expansionary fiscal policies in the surplus countries or tighter control mechanisms for surplus countries (possibly capital-outflow controls?).

• For the (former) crisis countries, Japan-type structural growth rigidities and real wage repression may emerge, which are outside the macroeconomic imbalance procedures (Schnabl 2013).

December 2014 Prof. Dr. Gunther Schnabl, Institute for Economic Policy

Thank your very much for your attention!

December 2014 Prof. Dr. Gunther Schnabl, Institute for Economic Policy

16

References

• Corsetti, Giancarlo / Pesenti, Paolo / Roubini, Nouriel 1999: Paper Tigers? A model of the Asian Crisis. European Economic Review 43, 1211-1236.

• Flood, Robert / Garber, Peter 1984: Collapsing Exchange-Rate Regimes. Some Linear Examples. Journal of International Economics 17, 1-13.

• Hayek, Friedrich 1929: Geldtheorie und Konjunkturtheorie, Salzburg, Philosophia Verlag (Reprint).

• Hoffmann, Andreas / Schnabl, Gunther 2011: A Vicious Cycle of Manias, Bursting Bubbles and Asymmetric Policy Responses – An Overinvestment View. The World Economy 34, 3, 382-403.

• Hoffmann, Andreas / Schnabl, Gunther 2014: Monetary Policy in Large Industrialized Countries, Emerging Market Credit Cycles, and Feedback Effects. CESifo Working Paper 4723.

December 2014 Prof. Dr. Gunther Schnabl, Institute for Economic Policy

17

References (Cont.)

• Krugman, Paul 1979: A Model of Balance-of-Payments Crises. Journal of Money, Credit, and Banking 11, 3, 311-325.

• Krugman, Paul 1998: What Happened to Asia?, http://web.mit.edu/krugman/www/DISINTER.html.

• Schnabl, Gunther (2013): The Macroeconomic Challenges of Balance Sheet Recession: Lessons from Japan for Europe. CESifo Working Paper 4249.

• Schnabl, Gunther / Hoffmann, Andreas 2008: Monetary Policy, Vagabonding Liquidity and Bursting Bubbles in New and Emerging Markets – An Overinvestment View. The World Economy 31, 9, 1226-1252.

• Schnabl, Gunther / Wollmershäuser, Timo 2013: Fiscal Divergence and Current Account Imbalances in Europe. CESifo Working Paper 4108.

• Wicksell, Knut (1898): Geldzins und Güterpreise, FinanzBuch Verlag, München (Reprint).

December 2014 Prof. Dr. Gunther Schnabl, Institute for Economic Policy