update on nafta negotiation

TRANSCRIPT

December 18, 2017

Update on NAFTA Negotiation

Despite the pessimism surrounding NAFTA talks, we still maintain that no country is likely to walk away from a deal because the economic and political costs of doing so are simply too high.

This report analyzes:

Main sectors up for negotiation

Possible changes to NAFTA

Why Trump will not attempt to withdraw from NAFTA

Why Canada and Mexico cannot afford to abandon negotiations

Main sectors up for negotiation

Rules of origin

The United States wants to significantly increase how much of a product must be fabricated within the NAFTA trade zone to qualify for tariff-free status. For example, it wants to raise the content threshold for automobiles to 85% from its current 62.5% level. The Trump administration also wants half of a vehicle’s components to be sourced from the United States. This would force manufacturers either to reduce the amount of materials they import from outside the NAFTA zone or to pay more tariffs.

Canada and Mexico have indicated they are open to increasing the content requirements but that any changes must apply equally to all three countries.

Agriculture

The United States wants to end Canada’s agriculture supply management system, which includes production quotas for milk, eggs and poultry and tariffs of up to 300% on imports. We feel Canada will ultimately agree to certain concessions. This is based on the fact it has made certain concessions in past trade negotiations, as the following examples illustrate:

Under the now collapsed Trans-Pacific Partnership, Canada had agreed to raise by 3.25% the amount of foreign dairy products entering Canada tariff-free. The plan was for dairy farmers to receive financial compensation for their losses.1

Canada has agreed to accept more European dairy products under the Comprehensive Economic and Trade Agreement. This means that tariff-free cheese imports will go from accounting for 5% of Canada's current cheese market to 9% over the next few years.2

Given that Canada’s trade relationship with the United States is considerably more important than its trade relationship with Europe, logic dictates that it will offer concessions to the United States as well. The European Union accounts for just under 10% of Canada’s trade compared to 76% for the United States.

Five-year sunset clause

The United States is pushing for a sunset clause that would allow NAFTA to expire at five-year intervals unless the three countries decide otherwise. A potential compromise would be to agree on holding regular reviews without the risk of the deal being cancelled in the event of a disagreement.

We feel that the U.S. push for a sunset clause is a ploy to get concessions in other areas.

1 “U.S. dairy takes aim at Canada’s supply management system in NAFTA talks,” The Globe and Mail, September 23, 2017 2 “Canada carves out more European cheese for retailers after EU concerns,” CBC, August 1, 2017

Geopolitical Briefing

2

Trade dispute mechanism

The United States wants to eliminate the binational trade dispute panel (Chapter 19), which is used when one country challenges the legality of another country’s trade barriers. Rulings by this panel cannot be appealed to domestic courts. The Trump administration maintains that the panel infringes on the country’s sovereignty and wants to revert to settling disputes in U.S. courts instead. Both Canada and Mexico are vehemently opposed to this.

While common ground on this issue will be difficult to attain, a compromise might entail allowing more U.S. arbiters on the panels. The United States could also agree to keep this dispute panel intact in exchange for concessions elsewhere.

Government procurement contracts

The Trump administration is seeking to limit Mexican and Canadian access to U.S. government procurement contracts to the dollar amount of Mexican and Canadian contracts open to U.S. companies. Given the much larger size of the U.S. economy, adopting this rule would drastically reduce Canada’s and Mexico’s access to U.S. procurement contracts. We feel the ultimate goal of this extreme position is for it be used as a bargaining chip to gain concessions elsewhere.

Wages

While Canada and the United States are at odds in many areas, they appear to be in tacit agreement that wages in Mexico are too low and thus constitute an unfair competitive advantage. For example, despite billions in FDI over the last decade, Mexico’s auto industry still pays wages that are 12% to 18% of those in the United States.3 Moreover, the minimum wage in Mexico is currently only 88 pesos ($4.74) a day.4 Look for Canada and the United States to push Mexico to raise wages and tighten labor standards.

Would (or could) Trump actually withdraw from NAFTA? The President’s ability to terminate NAFTA has been the subject of intense debate. Some experts maintain that the President can unilaterally walk away from NAFTA with only six months’ notice, while others feel only Congress has the constitutional authority to kill trade deals. Regardless of who is right, we believe it is highly unlikely that President Trump would actually take steps to withdraw from NAFTA. Here’s why:

It would spark a rebellion in Congress. This would include attempting to delay NAFTA’s demise by holding countless hearings. Further, even if Trump succeeded in terminating NAFTA by presidential decree, legislative action would be required to implement new trade regulations. Congress could threaten not to pass any new trade legislation.

An attempt by Trump to unilaterally terminate NAFTA would trigger a wave of lawsuits challenging the legality of the move. The matter could be appealed all the way to the Supreme Court. All of this would create a long period of uncertainty, with businesses potentially holding back on investment until the legal fog cleared.

President Trump does not have to resort to the nuclear option of ripping up trade agreements in order to implement protectionist measures. He has the legal authority to impose tariffs or quotas on virtually any sector of the economy without the approval of Congress.

Withdrawing from NAFTA risks creating market turmoil and disrupting the activities of companies with supply chains spread across the trade zone. This could put at risk what Trump considers to be one of his main accomplishments: strong economic growth and record stock market valuations.

Many states, including those that voted for Trump, have deep trade ties with both Mexico and Canada. Mexico and Canada account for about 25% of U.S. trade and for almost 10% of its inward and outward stock of FDI.5

3 “Labor Wants to Make NAFTA Its Friend. Here’s the Problem.” New York Times, August 22, 2017 4 “The U.S.-Mexico Wage Gap Is Actually Widening Under Nafta,” Bloomberg, November 28, 2017 5 “What if NAFTA ended? The Imperative of a Successful Renegotiations,” Atlantic Council, October 2017

Geopolitical Briefing

3

Sources: “What if NAFTA ended? The Imperative of a Successful Renegotiations” Atlantic Council, October 2017, and American Enterprise Institute, 2017

Finally, leaving NAFTA would only further burden a Presidency already struggling with the collusion investigation, internal infighting, high disapproval ratings, a stalled legislative agenda and various foreign policy challenges, including North Korea.

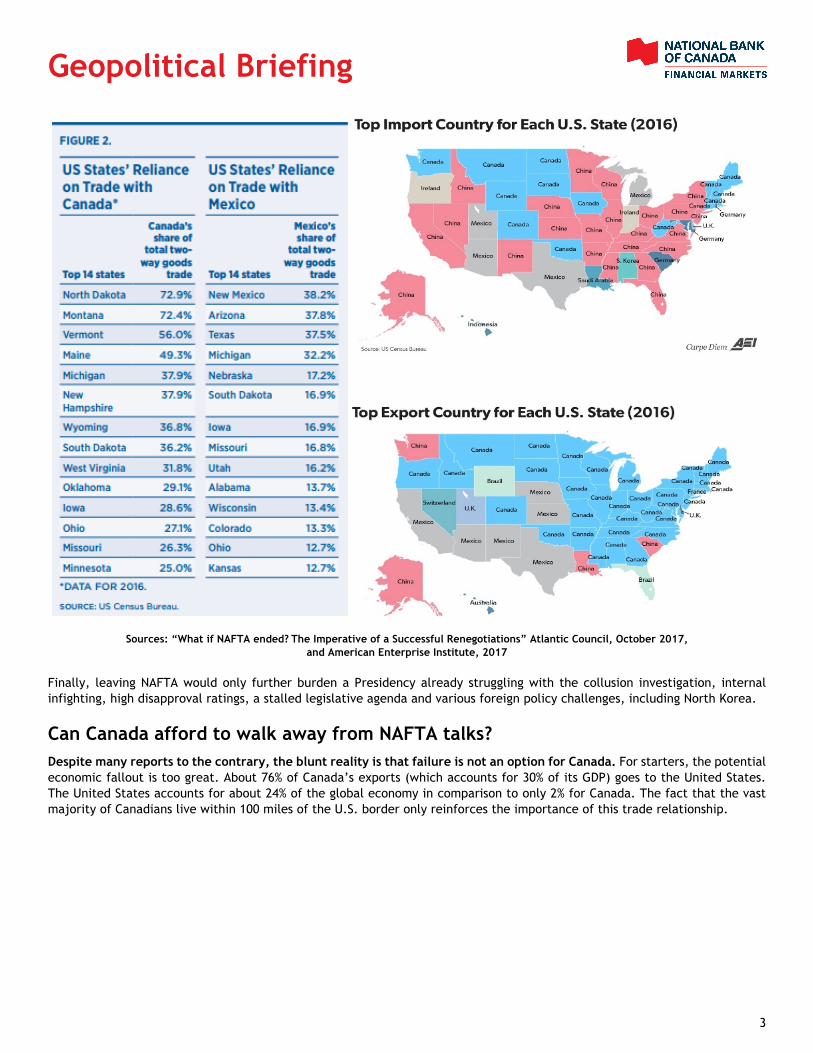

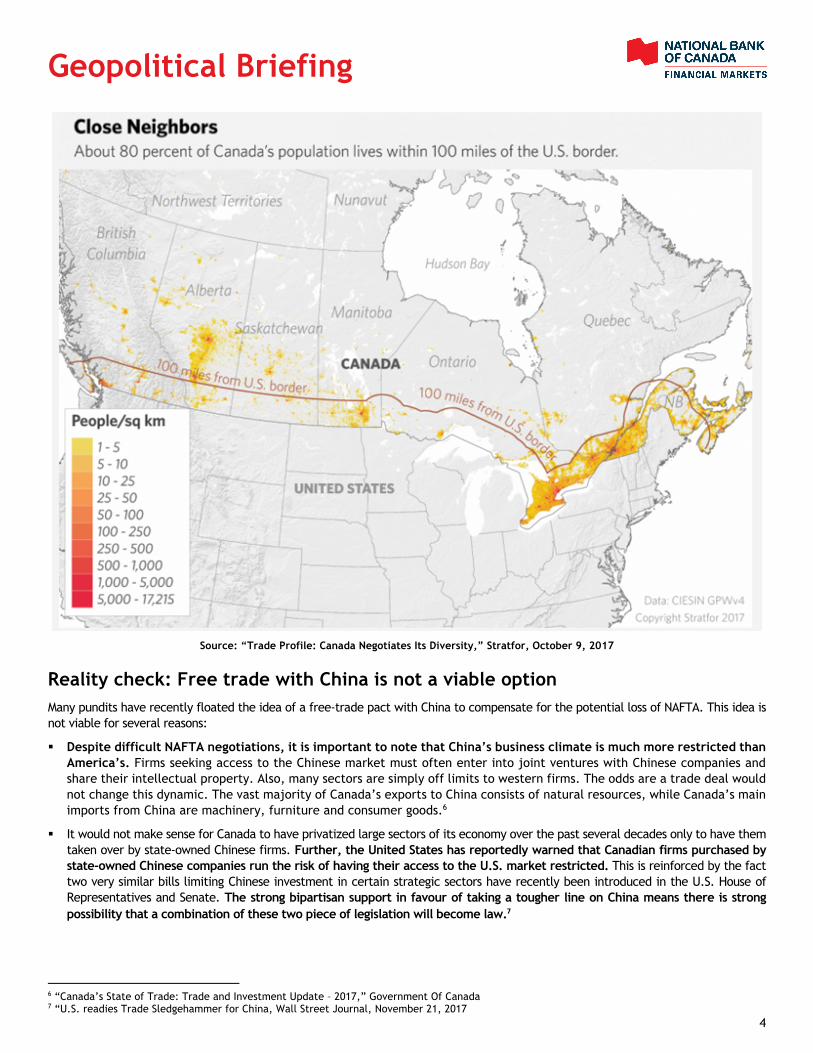

Can Canada afford to walk away from NAFTA talks? Despite many reports to the contrary, the blunt reality is that failure is not an option for Canada. For starters, the potential economic fallout is too great. About 76% of Canada’s exports (which accounts for 30% of its GDP) goes to the United States. The United States accounts for about 24% of the global economy in comparison to only 2% for Canada. The fact that the vast majority of Canadians live within 100 miles of the U.S. border only reinforces the importance of this trade relationship.

Geopolitical Briefing

4

Source: “Trade Profile: Canada Negotiates Its Diversity,” Stratfor, October 9, 2017

Reality check: Free trade with China is not a viable option Many pundits have recently floated the idea of a free-trade pact with China to compensate for the potential loss of NAFTA. This idea is not viable for several reasons:

Despite difficult NAFTA negotiations, it is important to note that China’s business climate is much more restricted than America’s. Firms seeking access to the Chinese market must often enter into joint ventures with Chinese companies and share their intellectual property. Also, many sectors are simply off limits to western firms. The odds are a trade deal would not change this dynamic. The vast majority of Canada’s exports to China consists of natural resources, while Canada’s main imports from China are machinery, furniture and consumer goods.6

It would not make sense for Canada to have privatized large sectors of its economy over the past several decades only to have them taken over by state-owned Chinese firms. Further, the United States has reportedly warned that Canadian firms purchased by state-owned Chinese companies run the risk of having their access to the U.S. market restricted. This is reinforced by the fact two very similar bills limiting Chinese investment in certain strategic sectors have recently been introduced in the U.S. House of Representatives and Senate. The strong bipartisan support in favour of taking a tougher line on China means there is strong possibility that a combination of these two piece of legislation will become law.7

6 “Canada’s State of Trade: Trade and Investment Update – 2017,” Government Of Canada 7 “U.S. readies Trade Sledgehammer for China, Wall Street Journal, November 21, 2017

Geopolitical Briefing

5

The U.S. government would react negatively to China gaining increased access to the North American market via Canada at the same time that it is pushing for higher local content rules.

While China’s trade with Canada has increased significantly over the past decade, it still accounts for only about 4% of Canada’s total exports.8

Will the Canada-U.S. Free Trade Agreement come to the rescue? Should NAFTA talks fail reverting back to the original Canada-U.S. Free Trade Agreement (CFTA) is easier said than done. To begin with, many experts feel reviving the deal would require the issuance of a presidential proclamation.9 It is also highly likely that President Trump would push for additional concessions before agreeing to bring the CFTA back into force. All of this reinforces our view that Canada has little choice but to continue with the NAFTA negotiations and eventually offer certain concessions in order to strike a deal.

The Mexican government stands to lose the most from a collapse of NAFTA talks Mexico is even more economically reliant on the United States than Canada is. Over 80% of its exports go to the United States. Trade accounts for 38% of Mexico’s GDP versus only 12% of U.S. GDP.

That said, Mexico’s vulnerability constitutes its great negotiating advantage.

There is a significant risk of seeing Mexico fall into a recession if NAFTA is scrapped. Given that Mexico is the United States’ third-largest trading partner (value of two-way trade is $586 billion), this could negatively impact the United States’ economic performance.

The collapse of NAFTA could also reduce Mexico's willingness to cooperate on drug-smuggling and illegal immigration. Mexican Foreign Minister Luis Videgaray recently said: “It’s good for Mexico that we cooperate with the U.S. on security and also on migration and many other issues, but it’s a fact of life and there is a political reality that a bad outcome on NAFTA will have some impact on that.”10 Over 90% of the heroin in the United States is either produced in or shipped through Mexico. It is also an important transit point for the deadly opioid fentanyl entering the United States.11

Meanwhile, a political consequence of rejecting NAFTA could be increased support for Andrés Manuel Lόpez Obrador, the far-left candidate in the upcoming presidential election (July 2018) who is currently leading in the polls. Support for him has already been bolstered by Trump’s sometimes incendiary rhetoric against Mexico. Obrador has positioned himself as a major critic of NAFTA and has demanded that renegotiations be delayed until after the election. Recently, in an effort to appear more moderate, he stated that NAFTA had provided some benefits but could still use major improvements. Obrador has already run for the presidency twice, and lost narrowly both times.

Mexico’s increasingly fragmented political landscape and the fact that there is no second-round vote means someone could win the presidency with as little as 30% of the popular vote. Growing anti-American sentiment, a spike in the murder rate owing to increased cartel violence, and the recent spate of government corruption scandals only adds to the political uncertainty.

8 “Nafta Tensions Simmer, Canada Pursues Trade With Asia,” Wall Street Journal, December 1, 2017 9 “The North American Free Trade Agreement (NAFTA),” Congressional Research Service, May 2017 10 “Bad Nafta Outcome Could Hit Cooperation on Security, Mexico Says,” Bloomberg, November 11, 2017 11 “Nafta’s Renegotiation Risks National Security,” New York Times, October 20, 2017

Geopolitical Briefing

6

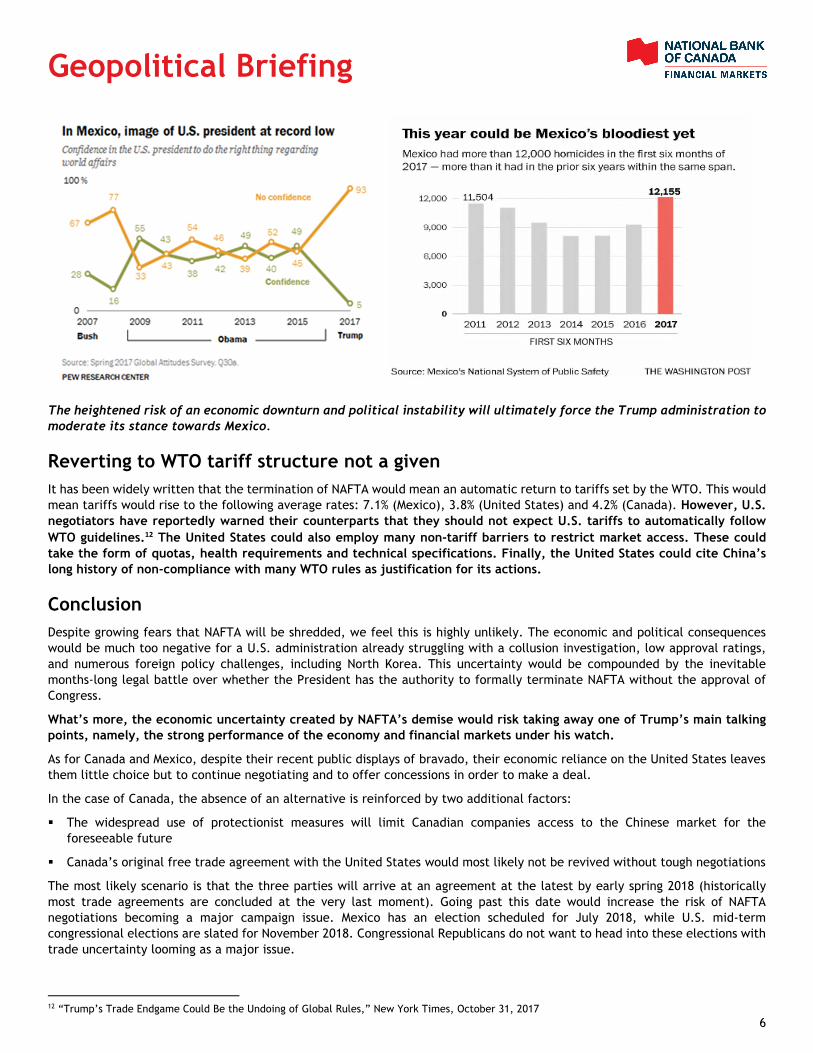

The heightened risk of an economic downturn and political instability will ultimately force the Trump administration to moderate its stance towards Mexico.

Reverting to WTO tariff structure not a given It has been widely written that the termination of NAFTA would mean an automatic return to tariffs set by the WTO. This would mean tariffs would rise to the following average rates: 7.1% (Mexico), 3.8% (United States) and 4.2% (Canada). However, U.S. negotiators have reportedly warned their counterparts that they should not expect U.S. tariffs to automatically follow WTO guidelines.12 The United States could also employ many non-tariff barriers to restrict market access. These could take the form of quotas, health requirements and technical specifications. Finally, the United States could cite China’s long history of non-compliance with many WTO rules as justification for its actions.

Conclusion Despite growing fears that NAFTA will be shredded, we feel this is highly unlikely. The economic and political consequences would be much too negative for a U.S. administration already struggling with a collusion investigation, low approval ratings, and numerous foreign policy challenges, including North Korea. This uncertainty would be compounded by the inevitable months-long legal battle over whether the President has the authority to formally terminate NAFTA without the approval of Congress.

What’s more, the economic uncertainty created by NAFTA’s demise would risk taking away one of Trump’s main talking points, namely, the strong performance of the economy and financial markets under his watch.

As for Canada and Mexico, despite their recent public displays of bravado, their economic reliance on the United States leaves them little choice but to continue negotiating and to offer concessions in order to make a deal.

In the case of Canada, the absence of an alternative is reinforced by two additional factors:

The widespread use of protectionist measures will limit Canadian companies access to the Chinese market for the foreseeable future

Canada’s original free trade agreement with the United States would most likely not be revived without tough negotiations

The most likely scenario is that the three parties will arrive at an agreement at the latest by early spring 2018 (historically most trade agreements are concluded at the very last moment). Going past this date would increase the risk of NAFTA negotiations becoming a major campaign issue. Mexico has an election scheduled for July 2018, while U.S. mid-term congressional elections are slated for November 2018. Congressional Republicans do not want to head into these elections with trade uncertainty looming as a major issue.

12 “Trump’s Trade Endgame Could Be the Undoing of Global Rules,” New York Times, October 31, 2017

Geopolitical Briefing

7

The negative scenario

However, should an agreement not be reached by early spring 2018, the odds of a successful outcome would decline significantly. Under this scenario, there is a major risk that Trump would trigger the six-month notice period required to terminate NAFTA. Then, as the inevitable legal challenges and waiting periods play out, Trump could use his extensive executive powers to impose greater trade restrictions in a bid to force the other two countries back to the bargaining table. This in turn would provoke a political backlash in both Canada and Mexico, and consequently make it even more difficult to make a deal.

Angelo Katsoras

Geopolitical Briefing

Economics and Strategy

Montreal Office Toronto Office

514-879-2529 416-869-8598

Stéfane Marion Marc Pinsonneault Kyle Dahms Warren Lovely Chief Economist and Strategist Senior Economist Economist MD, Public Sector Research and Strategy [email protected] [email protected] [email protected] [email protected]

Paul-André Pinsonnault Matthieu Arseneau Jocelyn Paquet Senior Fixed Income Economist Senior Economist Economist [email protected] [email protected] [email protected]

Krishen Rangasamy Angelo Katsoras Senior Economist Geopolitical Analyst [email protected] [email protected]

General – National Bank Financial (NBF) is an indirect wholly owned subsidiary of National Bank of Canada. National Bank of Canada is a public company listed on Canadian stock exchanges.

The particulars contained herein were obtained from sources which we believe to be reliable but are not guaranteed by us and may be incomplete. The opinions expressed are based upon our analysis and interpretation of these particulars and are not to be construed as a solicitation or offer to buy or sell the securities mentioned herein.

Research Analysts – The Research Analyst(s) who prepare these reports certify that their respective report accurately reflects his or her personal opinion and that no part of his/her compensation was, is, or will be directly or indirectly related to the specific recommendations or views as to the securities or companies.

NBF compensates its Research Analysts from a variety of sources. The Research Department is a cost centre and is funded by the business activities of NBF including, Institutional Equity Sales and Trading, Retail Sales, the correspondent clearing business, and Corporate and Investment Banking. Since the revenues from these businesses vary, the funds for research compensation vary. No one business line has a greater influence than any other for Research Analyst compensation.

Canadian Residents – In respect of the distribution of this report in Canada, NBF accepts responsibility for its contents. To make further inquiry related to this report, Canadian residents should contact their NBF professional representative. To effect any transaction, Canadian residents should contact their NBF Investment advisor.

U.S. Residents – With respect to the distribution of this report in the United States, National Bank of Canada Financial Inc. (NBCFI) is regulated by the Financial Industry Regulatory Authority (FINRA) and a member of the Securities Investor Protection Corporation (SIPC). This report has been prepared in whole or in part by, research analysts employed by non-US affiliates of NBCFI that are not registered as broker/dealers in the US. These non-US research analysts are not registered as associated persons of NBCFI and are not licensed or qualified as research analysts with FINRA or any other US regulatory authority and, accordingly, may not be subject (among other things) to FINRA restrictions regarding communications by a research analyst with the subject company, public appearances by research analysts and trading securities held a research analyst account.

All of the views expressed in this research report accurately reflect the research analysts’ personal views regarding any and all of the subject securities or issuers. No part of the analysts’ compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed in this research report. The analyst responsible for the production of this report certifies that the views expressed herein reflect his or her accurate personal and technical judgment at the moment of publication. Because the views of analysts may differ, members of the National Bank Financial Group may have or may in the future issue reports that are inconsistent with this report, or that reach conclusions different from those in this report. To make further inquiry related to this report, United States residents should contact their NBCFI registered representative.

UK Residents – In respect of the distribution of this report to UK residents, National Bank Financial Inc. has approved the contents (including, where necessary, for the purposes of Section 21(1) of the Financial Services and Markets Act 2000). National Bank Financial Inc. and/or its parent and/or any companies within or affiliates of the National Bank of Canada group and/or any of their directors, officers and employees may have or may have had interests or long or short positions in, and may at any time make purchases and/or sales as principal or agent, or may act or may have acted as market maker in the relevant investments or related investments discussed in this report, or may act or have acted as investment and/or commercial banker with respect thereto. The value of investments can go down as well as up. Past performance will not necessarily be repeated in the future. The investments contained in this report are not available to retail customers. This report does not constitute or form part of any offer for sale or subscription of or solicitation of any offer to buy or subscribe for the securities described herein nor shall it or any part of it form the basis of or be relied on in connection with any contract or commitment whatsoever.

This information is only for distribution to Eligible Counterparties and Professional Clients in the United Kingdom within the meaning of the rules of the Financial Conduct Authority. National Bank Financial Inc. is authorised and regulated by the Financial Conduct Authority and has its registered office at 71 Fenchurch Street, London, EC3M 4HD.

National Bank Financial Inc. is not authorised by the Prudential Regulation Authority and the Financial Conduct Authority to accept deposits in the United Kingdom.

HK Residents – With respect to the distribution of this report in Hong Kong by NBC Financial Markets Asia Limited (“NBCFMA”)which is licensed by the Securities and Futures Commission (“SFC”) to conduct Type 1 (dealing in securities) regulated activity, the contents of this report are solely for informational purposes. It has not been approved by, reviewed by, verified by or filed with any regulator in Hong Kong. Nothing herein is a recommendation, advice, offer or solicitation to buy or sell a product or service, nor an official confirmation of any transaction. None of the products issuers, NBCFMA or its affiliates or other persons or entities named herein are obliged to notify you of changes to any information and none of the foregoing assume any loss suffered by you in reliance of such information.

The content of this report may contain information about investment products which are not authorized by SFC for offering to the public in Hong Kong and such information will only be available to, those persons who are Professional Investors (as defined in the Securities and Futures Ordinance of Hong Kong (“SFO”)). If you are in any doubt as to your status you should consult a financial adviser or contact us. This material is not meant to be marketing materials and is not intended for public distribution. Please note that neither this material nor the product referred to is authorized for sale by SFC. Please refer to product prospectus for full details.

There may be conflicts of interest relating to NBCFMA or its affiliates’ businesses. These activities and interests include potential multiple advisory, transactional and financial and other interests in securities and instruments that may be purchased or sold by NBCFMA or its affiliates, or in other investment vehicles which are managed by NBCFMA or its affiliates that may purchase or sell such securities and instruments.

No other entity within the National Bank of Canada group, including NBF, is licensed or registered with the SFC. Accordingly, such entities and their employees are not permitted and do not intend to: (i) carry on a business in any regulated activity in Hong Kong; (ii) hold themselves out as carrying on a business in any regulated activity in Hong Kong; or (iii) actively market their services to the Hong Kong public.

Copyright – This report may not be reproduced in whole or in part, or further distributed or published or referred to in any manner whatsoever, nor may the information, opinions or conclusions contained in it be referred to without in each case the prior express written consent of National Bank Financial.