urban renewal in denver - city and county of denver ... · dennis j. gallagher auditor office of...

TRANSCRIPT

Dennis J. Gallagher Auditor

Office of the Auditor

Audit Services Division

City and County of Denver

Urban Renewal in Denver Performance Audit

August 2014

The Auditor of the City and County of Denver is independently elected by the citizens of Denver.

He is responsible for examining and evaluating the operations of City agencies for the purpose

of ensuring the proper and efficient use of City resources and providing other audit services and

information to City Council, the Mayor and the public to improve all aspects of Denver’s

government. He also chairs the City’s Audit Committee.

The Audit Committee is chaired by the Auditor and consists of seven members. The Audit

Committee assists the Auditor in his oversight responsibilities of the integrity of the City’s finances

and operations, including the integrity of the City’s financial statements. The Audit Committee is

structured in a manner that ensures the independent oversight of City operations, thereby

enhancing citizen confidence and avoiding any appearance of a conflict of interest.

Audit Committee

Dennis Gallagher, Chair Robert Bishop

Maurice Goodgaine Jeffrey Hart

Leslie Mitchell Timothy O’Brien, Vice-Chair

Rudolfo Payan

Audit Staff

John Carlson, Deputy Director, JD, MBA, CIA, CRMA

Nancy Howe, Lead Internal Auditor, MPA, CRMA

Anthony Lewin, Senior Internal Auditor

Ronald F. Keller, Senior Internal Auditor, CIA, CFE

You can obtain copies of this report by contacting us at:

Office of the Auditor

201 West Colfax Avenue, Department 705 Denver CO, 80202

(720) 913-5000 Fax (720) 913-5247

Or download and view an electronic copy by visiting our website at:

www.denvergov.org/auditor

To promote open, accountable, efficient and effective government by performing impartial reviews and other audit services

that provide objective and useful information to improve decision making by management and the people.

We will monitor and report on recommendations and progress towards their implementation.

City and County of Denver 201 West Colfax Avenue, Department 705 Denver, Colorado 80202 720-913-5000

FAX 720-913-5247 www.denvergov.org/auditor

Dennis J. Gallagher

Auditor

August 15, 2014

Cary Kennedy, Deputy Mayor, Chief Financial Officer

Mayor’s Office

City and County of Denver

Dear Ms. Kennedy:

Attached is our audit of the City and County of Denver’s relationship with the Denver Urban

Renewal Authority (DURA). The purpose of the audit was to assess whether any enhancements

are needed in the City’s relationship with DURA regarding the use of tax increment financing

(TIF) and the monitoring of TIFs used for urban redevelopment.

We found that various City agencies and the public are involved in the TIF designation process.

However, after approving the use of TIFs, DURA’s statutory status as a separate legal entity limits

the City’s authority to oversee redevelopment activities. Despite limits on its administrative

authority, the City is connected to DURA through the Cooperation Agreements developed for

TIF Areas. Further, TIFs generate a great deal of tax revenue, which the City collects and

forwards to DURA. As a result, it makes sense that the City should help ensure visibility into the

amount of forgone property, sales, and lodger’s taxes it collects on behalf of DURA as well as

the redevelopment projects these tax revenues fund. Visibility into TIFs and TIF-funded projects is

critical to ensuring that the City is benefitting from these redevelopment projects and ensuring a

positive public perception of DURA activities.

We identified three types of information that would provide the City, the public, and other

stakeholders additional detail on TIF Areas and TIF funding of redevelopment projects.

Specifically, the City can create a consolidated repository of TIF Cooperation Agreements,

publish a list of active Denver Urban Renewal Plans and TIF Areas, and periodically report urban

renewal activity to the public.

If you have any questions, please call Kip Memmott, Director of Audit Services, at 720-913-5000.

Sincerely,

Dennis J. Gallagher

Auditor

DJG/nh

To promote open, accountable, efficient and effective government by performing impartial reviews and other audit services

that provide objective and useful information to improve decision making by management and the people.

We will monitor and report on recommendations and progress towards their implementation.

cc: Honorable Michael Hancock, Mayor

Honorable Members of City Council

Members of Audit Committee

Ms. Janice Sinden, Chief of Staff

Mr. David P. Edinger, Chief Performance Officer

Ms. Beth Machann, Controller

Mr. Scott Martinez, City Attorney

Ms. Janna Young, City Council Executive Staff Director

Mr. L. Michael Henry, Staff Director, Board of Ethics

To promote open, accountable, efficient and effective government by performing impartial reviews and other audit services

that provide objective and useful information to improve decision making by management and the people.

We will monitor and report on recommendations and progress towards their implementation.

City and County of Denver 201 West Colfax Avenue, Department 705 Denver, Colorado 80202 720-913-5000

FAX 720-913-5247 www.denvergov.org/auditor

Dennis J. Gallagher

Auditor

AUDITOR’S REPORT

We have completed an audit examining the City and County of Denver’s relationship with the

Denver Urban Renewal Authority (DURA). The purpose of the audit was to assess whether any

enhancements are needed in the City’s relationship with DURA regarding the use of tax

increment financing (TIF) and the monitoring of TIFs used for urban redevelopment purposes.

This performance audit is authorized pursuant to the City and County of Denver Charter, Article

V, Part 2, Section 1, General Powers and Duties of Auditor, and was conducted in accordance

with generally accepted government auditing standards. Those standards require that we plan

and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis

for our findings and conclusions based on our audit objectives. We believe that the evidence

obtained provides a reasonable basis for our findings and conclusions based on our audit

objectives.

We examined the relationship between the City and DURA and found that although various City

agencies and the public are involved in the TIF designation process, DURA’s statutory status as a

separate legal entity limits the City’s authority to oversee redevelopment activities after such

designation is approved. Despite limits on its administrative authority, it is important that the City

ensure visibility into TIFs and TIF-funded projects, first because of its connection to DURA and

second because of the large amount of tax revenue that is foregone to fund redevelopment

using TIFs.

We extend our appreciation to the Department of Finance and the personnel who assisted and

cooperated with us during the audit.

Audit Services Division

Kip Memmott, MA, CGAP, CRMA

Director of Audit Services

For a complete copy of this report, visit www.denvergov.org/auditor Or Contact the Auditor’s Office at 720.913.5000

Background The Colorado Urban Renewal Law

was enacted in 1958, and the Denver

Urban Renewal Authority (DURA)

was created shortly thereafter. DURA

was created to help eliminate slum

housing conditions. Over time,

DURA’s focus has widened to address

redevelopment.

DURA originally pursued federal

grants to fund its activities. Over

time, these funds dwindled and the

absence of urban infrastructure on

redevelopment sites required major

public investment to make

redevelopment possible. In order to

finance the needed infrastructure,

urban renewal areas were created,

which enables financing of the

infrastructure necessary for

redevelopment by utilizing the future

taxes generated by the sites

themselves.

Purpose The purpose of the audit was to

assess the City’s relationship with the

Denver Urban Renewal Authority

(DURA), including the process for

designating Tax Increment Finance

(TIF) Areas and of the use of TIF

funds generally.

City and County of Denver – Office of the Auditor Audit Services Division

REPORT HIGHLIGHTS

Urban Renewal in Denver August 2014

The objective of this audit was to determine if enhancements are needed in the City’s relationship with

DURA regarding the use and monitoring of tax increment financing for urban redevelopment.

.]

Highlights Our work indicated that several City agencies, as well as the public,

are involved when Tax Increment Finance (TIF) Plans, Areas, and

projects are established. Once established, the Denver Urban

Renewal Authority (DURA) is responsible for ensuring that the

blight identified is remediated by the redevelopment project.

DURA’s statutory status as a body corporate and politic makes it a

separate legal entity and therefore limits the City’s authority over

DURA activities. Despite limited oversight authority, the City has a

connection with DURA through the Cooperation Agreements

developed for TIF Areas. As a result, the City is in a logical position

to help ensure the propriety of the forgone property, sales, and

lodger’s taxes it collects on behalf of DURA and the redevelopment

projects these tax revenues fund. Visibility into TIFs and TIF-funded

projects is critical to help show City benefits from these

redevelopment projects and to ensure a positive public perception

of DURA activities.

We identified three types of information the City could request

from DURA that would provide it and other stakeholders with

additional detail on TIF Areas and TIF funding of redevelopment

projects. Specifically, the City can create a consolidated repository

of TIF Cooperation Agreements, publish a list of active Urban

Renewal Plans and TIF Areas, and regularly publish information

about urban renewal activity.

TABLE OF CONTENTS

INTRODUCTION & BACKGROUND 1

Urban Renewal History 1

Overview of the Colorado Urban Renewal Law 2

Denver Urban Renewal Authority 4

Urban Renewal Plan Process 5

Colorado Urban Renewal Law and Blighted Areas 6

How Do TIFs Work? 10

Process for Creating a TIF Area 12

Potential Issues with TIFs 14

SCOPE 15

OBJECTIVE 15

METHODOLOGY 15

FINDING 16

Additional Tax Increment Financing Information Can Be Made

Available to Stakeholders 16

Substantive Stakeholder Involvement in the TIF Designation Process 16

No Centralized List for TIF Areas and Cooperation Agreements 16

Opportunities to Enhance Urban Renewal Public Reporting 18

TIF Reporting Best Practice 20

Colorado Municipal League URA Reporting 20

Transparent Denver 21

RECOMMENDATIONS 22

APPENDIX A 23

Cross Functional Process Map of Denver’s TIF Process 23

TABLE OF CONTENTS (continued)

APPENDIX B 24

Active TIF Areas in the City and County of Denver 24

APPENDIX C 25

Colorado Municipal League URA Annual Report Template 25

AGENCY RESPONSE 26

P a g e 1

OOffffiiccee ooff tthhee AAuuddiittoorr Office of the Auditor

INTRODUCTION & BACKGROUND

Urban Renewal History

Congress enacted the federal urban redevelopment program in Title I of the Housing Act

of 1949, and over the next twenty years, planners, mayors, journalists, and the public

implemented plans to revitalize the nation’s cities. “Artists’ renderings of slick glass and

steel skyscrapers set in sunny plazas appeared in metropolitan newspapers and city

planning reports, and nurtured hopes of a golden future. With the aid of Uncle Sam, cities

were supposedly to be cleansed of their ugly past and re-clothed in the latest modern

attire.”1 By the 1960s, skeptics were questioning the merits of a federally subsidized urban

renewal program, and 10 years later the program was losing favor. The federal urban

renewal program would cease in 1974.2

Title I Projects - Early Title I projects focused on moderate-income housing. Philadelphia’s

first Title I project, the East Poplar scheme, provided housing for low and middle-income

residents.3 As a greater amount of federal dollars could be allocated to commercial

redevelopment residential projects diminished. Unfortunately, affordable housing did not

become the stimulus for the urban renaissance contemplated by proponents of the Title I

federal program.4

Community Development Block Grants - In 1974, Congress created the Community

Development Block Grant (CDBG) program. The CDBG scheme sought to give localities

more options when using federal funds. Recipient cities had broad discretion in how they

used federal grants, but the chief beneficiaries were supposed to be low and moderate-

income residents.5 Like the previous urban renewal program, cities could allocate the

money for mitigation of slum and blighted areas, but the grants could also fund a range

of programs and facilities including neighborhood centers, nonprofit economic

development schemes, building code enforcement, energy conservation, and varied

public works projects and public services.6

1 Urban Renewal and Its Aftermath, Jon C. Teaford, Housing Policy Debate, Volume 11, Issue 2, Fannie Mae Foundation 2000,

page 443. In Denver, developer William Zeckendorf embarked during the mid-1950s on the development of the Mile High Center office building, followed by the Courthouse Square project, comprising a department store, hotel, and office annex. Local observers hailed this private renewal effort as the spark that reignited Denver’s core (Abbott 1981; Adde 1969). Ibid. 2 Ibid.

3 Ibid.

4 Ibid.

5 Ibid.

6 Ibid.

P a g e 2

City and County of Denver

Urban Renewal Authorities

Responding to a desired need for a program to eradicate slums in urban areas, urban

renewal authorities began to appear in the 1950s to address these issues. The goal of

urban renewal efforts at the time was to revitalize decaying city areas. Urban renewal

authorities (URAs) are created by municipalities to redevelop areas within their jurisdiction

that are found to contain blight or slum conditions and require public participation to

attract redevelopment. Typically, an urban renewal project is considered a

public/private partnership. The majority of the funding comes from the private sector;

public investment comes from tax increment financing (TIF).7 A TIF is a financing tool

where the increased amount of property tax or municipal sales tax revenue collected

within the URA after the project begins is used to pay off the obligations that help finance

project costs. This new revenue is generated by the increased property values that result

from the project.8

Overview of the Colorado Urban Renewal Law

The Colorado Urban Renewal Law was enacted in 1958, when urban renewal and slum

clearance were a nationwide priority. Following the 1949 Federal Housing Act, the Urban

Renewal Statute was originally intended to enable Colorado to receive federal funds

designated for slum clearance and housing construction.9 Title I of the Federal Housing

Act provided funds for slum clearance and urban redevelopment, primarily targeted at

the provision of housing. Under the Federal Housing Act, the federal government would

provide funds for up to two-thirds of the cost of slum clearance and urban

redevelopment projects; local governments were to provide the remainder.10 According

to the Colorado Department of Local Affairs there are currently fifty-one urban renewal

authorities located across the state.11

1958 Statute Provisions

The provisions of the original Urban Renewal Law have not changed significantly since

inception. Pursuant to the 1958 statute, a municipality could form an urban renewal

7 Urban Renewal and Its Aftermath, Jon C. Teaford. The negative image of urban renewal, together with growing budget

deficits, dampened any enthusiasm for marked increases in federal funding to the central cities. Beginning in the late 1970s, the portion of city revenues derived from the federal government declined, especially during the Reagan administration. States and localities increasingly had to rely on their own ingenuity and resources to finance revitalization. One of the most widespread approaches was use of the TIF. Under a TIF, a portion of the additional property tax revenue generated by development in a renewal area was used to pay off the bonds issued to finance such project costs as site and infrastructure improvements. In other words, a city borrowed against its expected increase in income and used the enhanced tax revenues in a designated TIF district to reimburse the cost of the public investment in the renewal project. By the late 1990s, 44 states had authorized municipalities to establish TIF districts, with 780 such project areas in California. Ibid. California has since repealed the use of TIFs due to its fiscal crisis. Viewpoint: As California’s TIF goes, so might Colorado’s, Denver Business Journal, January 13, 2012. 8 Colorado Municipal League, Urban Renewal Background, https://www.cml.org.

9 See 63 Stat. 413. Enacted July 15, 1949, the Federal Housing Act established a national housing objective to provide Federal

aid to assist slum-clearance, community development, and redevelopment programs. See also Government and Administrative Law News: A Brief Overview of Recent Changes in Colorado's Urban Renewal, Colorado Lawyer, Vol. 33, No. 9, September 2004, page 99. 10

A Brief Overview of Recent Changes in Colorado's Urban Renewal, Colorado Lawyer, Vol. 33, No. 9. 11

Colorado Department of Local Affairs, https://dola.colorado.gov.

P a g e 3

OOffffiiccee ooff tthhee AAuuddiittoorr Office of the Auditor

authority if it found that one or more slums or blighted areas existed within the

municipality and that the rehabilitation of such areas was necessary to preserve the

public's health, safety, morals, or welfare. In such areas, the Authority could adopt an

urban renewal plan and undertake an urban renewal project, including the acquisition

of property by eminent domain.12 The original statute used the terms slum area and

blighted area, and defined each generally. The 1958 Urban Renewal Law also required a

public hearing concerning the finding that an area was a slum or blighted area and the

adoption of the urban renewal plan.13 In 1958, the Denver City Council passed a

resolution creating an urban renewal authority pursuant to the Urban Renewal Law.14

1999 Amendments

The Urban Renewal Law was amended in 1999. In 1999, the General Assembly replaced

the general definition of blighted area with a list of eleven factors. It added the

requirement that four of those eleven factors must be present to justify a finding of

blight.15 The 1999 amendments contained a provision that, if the owners consented to

the inclusion of their property in an urban renewal area, only one factor need be present

for it to be considered a blighted area. A new requirement specified that the boundaries

of an urban renewal area be drawn as narrowly as possible to accomplish the planning

and development objectives of the urban renewal area.16

2004 Amendments

Before 2004, the Urban Renewal Law defined blight as evidence that four out of eleven

factors were present. The existence of blight was the prerequisite to the adoption of an

urban renewal plan and the undertaking of an urban renewal project. After 2004, if a

governing body is going to acquire property by eminent domain and transfer it to a

private entity, the governing body must determine that the property is located in a

blighted area or that the property itself is blighted. For purposes of this determination,

and to be able to use the power of eminent domain, blighted now means that five out

of the eleven factors must be present. There were also some slight changes made to the

eleven blight factors listed in the Urban Renewal Law.17

12

Eminent domain or condemnation is a governmental power that permits a government authority or, in limited circumstances, a private party to acquire or take property rights for certain specified purposes. The enabling authority of condemnation in Colorado comes from two provisions of the Colorado Constitution: Article II, §§ 14 and 15. 13

A Brief Overview of Recent Changes in Colorado's Urban Renewal, Colorado Lawyer, Vol. 33, No. 9, September 2004. 14

See CC Res. No. 6-1958. 15

A Brief Overview of Recent Changes in Colorado's Urban Renewal, Colorado Lawyer, Vol. 33, No. 9, September 2004. 16

Ibid. See also C.R.S. Section 31-25-107(c)(1) which provides that the boundaries of an area that the governing body determines to be a blighted area shall be drawn as narrowly as the governing body determines feasible to accomplish the planning and development objectives of the proposed urban renewal area. The governing body shall not approve an urban renewal plan until a general plan for the municipality has been prepared. An authority shall not acquire real property for an urban renewal project unless the local governing body has approved the urban renewal plan. 17

A Brief Overview of Recent Changes in Colorado's Urban Renewal, Colorado Lawyer, Vol. 33, No. 9, September 2004.

P a g e 4

City and County of Denver

Denver Urban Renewal Authority

The Denver Urban Renewal Authority (DURA) was created in 1958 with an initial mission to

help eliminate post World War II slum housing conditions. DURA was organized pursuant

to the state Urban Renewal Law, and was statutorily defined as a "body corporate and

politic" established to carry out urban renewal projects for a municipality.18 Since that

time, issues facing the City have changed with the times and DURA has partnered with

the public and private sectors to help address redevelopment issues. After the Great

Depression and Second World War, the United States in the late 1940s experienced a

widespread housing crisis. Two decades of focusing financial resources on the war effort

left the nation’s urban housing inventory inadequate, including in Denver.19

By 1950, the Rocky Mountain News reported that 24 percent of Denver’s housing units

were substandard and overcrowded, often lacking electricity or running water. Residents

with the resources to escape these conditions headed to the suburbs, exacerbating the

situation and leaving Denver with a declining tax base and a growing demand for social

services, which consumed almost 50 percent of the City’s annual budget. City leaders

passed a series of measures that included an overhaul of Denver’s zoning and building

codes, among other initiatives. One of those measures was the creation of DURA. DURA is

an independent agency with the power to acquire blighted property through

condemnation proceedings, approved by City Council.20

Leading up to DURA’s creation in 1958, the City identified four neighborhoods where slum

conditions were most serious and applied for federal grants and loans to assist in their

eradication. Federal monies in hand, Denver’s City Council approved a local

contribution to be repaid when the acquired properties were sold for redevelopment.

The first four projects undertaken by DURA were Avondale, Blake Street, Jerome Park,

and Whittier.21

A Focus on Downtown

When DURA’s initial work to eliminate central Denver’s slums was underway, the City

began to address another important issue—the modernization of downtown. After

suffering from many years of neglect and facing competition from more affordable

suburban land, America’s downtowns were in need of revitalization.22 In Denver’s case,

there were two downtowns. The area above “Champa Street was thriving with major

department stores, restaurants and hotels, while the area below Champa Street was

known as Denver’s skid row.”23

18

See C.R.S. Section 31-25-104(1)(b). When the organizing certificate has been filed with the Colorado Department of Local Affairs, the commissioners and their successors are constituted an urban renewal authority, which shall be a body corporate and politic. The boundaries of such authority shall be coterminous with those of the municipality. Ibid. 19

Denver Urban Renewal Authority 50 Years of Revitalizing Denver, May 21, 2008. 20

Ibid. 21

Ibid. 22

Ibid. 23

Ibid.

P a g e 5

OOffffiiccee ooff tthhee AAuuddiittoorr Office of the Auditor

By the 1950s, the area was a fiscal drain on the City as a whole. Civic leaders and area

newspapers were calling for action. At the time, the federal government was

aggressively supporting downtown revitalization through urban renewal grants, but in

Denver use of these funds was the subject of much debate. It would take the “flood of

the century” in 1965 to coalesce public support for the effort and, two years later, a

referendum in support of the Skyline Project passed with more than 70 percent

approval.24

In 1966, voters approved a referred ordinance adopting a large scale urban renewal

endeavor, known as the Skyline Project. In 1969, DURA presided over the first stages of

the project, which demolished nearly thirty blocks of Denver's urban core. The Skyline

project was accomplished quickly, and with little concern for the historic structures that it

leveled.25

From 1968 to 1984, DURA and Denver undertook urban renewal on a large scale,

acquiring property, relocating existing residents and businesses, remediating

contaminated areas, and selling the cleared sites to private developers to enable a

wide variety of redevelopment efforts aimed at modernizing downtown Denver. The

most significant projects of this era were the creation of the Auraria Higher Education

Campus and the Skyline Project.

Creating New Neighborhoods

With the closures of the Lowry Air Force Base and Stapleton International Airport in the

early 1990s, Denver faced large challenges. Working with citizens and civic leaders, the

City developed a vision for reincorporating these massive sites back into the surrounding

communities and then crafted plans for implementing those visions. While the private

development community was set to undertake development, the absence of urban

infrastructure on these sites required major public investment to make redevelopment

possible. In order to finance the needed infrastructure, DURA worked with the City,

Denver Public Schools, and the redevelopment entities to create urban renewal areas.

The utilization of urban renewal allowed the City and DURA to finance the roads, sewers,

schools, parks, fire stations, and police stations necessary for redevelopment by utilizing

the future taxes generated by the sites themselves. As with the revitalization of downtown

in prior years, the combination of planning and creative financing resulted in the

communities we know today as Lowry and Stapleton.26

Urban Renewal Plan Process

The process of urban redevelopment starts with an idea followed by an Urban Renewal

Plan. Many times the idea comes from a developer who approaches DURA for

assistance with redeveloping a blighted property. The ideas can also come from the City

community. With the idea in hand, DURA begins the processes of documenting an urban

24

Ibid. 25

The Skyline Project: Urban Renewal and the Demolition of Old Denver - Historical Perspectives, Colorado Lawyer, Vol. 34, No. 8, August 2005. 26

Denver Urban Renewal Authority 50 Years of Revitalizing Denver, May 21, 2008.

P a g e 6

City and County of Denver

renewal project. The steps involved in beginning an urban renewal project follow. These

steps often happen concurrently.

1. Determine survey area boundaries

2. Verify presence and location of blighting factors

3. Prepare conditions survey

4. Present conditions survey findings to DURA and City Council for acceptance

5. Identify market opportunities within area and quantify timing

6. Together with stakeholders, define future role of area in community

7. Prepare Urban Renewal Plan

8. Complete financial analysis (Tax Increment Finance – TIF)

9. Complete impact analysis and share with impacted taxing bodies

10. Present Urban Renewal Plan to DURA and City Council for adoption

11. Issue Request for Projects

12. Implement Urban Renewal Plan

The first step in determining whether or not a proposed redevelopment project is eligible

for assistance from DURA is assessing whether or not the area is blighted. Blight is a term

defined in the Colorado Urban Renewal Law. Any planned redevelopment should

eliminate the blighted conditions that have been identified. Moreover, the planned

redevelopment must be consistent with the vision and goals laid out for the area by the

City’s Comprehensive Plan. As part of the process, DURA will hold at least one

community meeting to review the proposed redevelopment plan and every

redevelopment project undertaken by DURA is reviewed by the Denver Planning Board

to determine whether it conforms to the City’s Comprehensive Plan.27 Once a

redevelopment plan has the Planning Board’s approval, it moves to City Council where it

receives two hearings – preliminary Council action and then a public hearing followed

by final Council action.

Colorado Urban Renewal Law and Blighted Areas

In the Colorado Urban Renewal Law, the legislature has declared that an area of blight

"constitute a serious and growing menace, injurious to the public health, safety, morals,

and welfare of the residents of the state in general and of the municipalities thereof; that

the existence of such areas contributes substantially to the spread of disease and crime,

constitutes an economic and social liability. . .”28 Further, blight impairs the growth of

municipalities, “retards the provision of housing accommodations, aggravates traffic

problems and impairs or arrests the elimination of traffic hazards and the improvement of

traffic facilities”29 The prevention of blight is a matter of public policy and statewide

27

The Denver Planning Board advises the Mayor and Denver City Council on land use matters including planning and zoning. 28

See C.R.S. § 31-25-101 et seq. 29

Ibid.

P a g e 7

OOffffiiccee ooff tthhee AAuuddiittoorr Office of the Auditor

concern in order to mitigate risk, and to save resources spent on extra services required

for police, fire, accident, hospitalization, and public protection. Pursuant to the Urban

Renewal Law, the term blighted area describes an area with an array of urban problems,

including health and social deficiencies, and physical deterioration.30 Before remedial

action can be taken, however, the Urban Renewal Law requires a finding by the

appropriate governing body that the study area constitutes a blighted area.31

Conditions Study

The blight finding is a legislative determination by the municipality's governing body that,

as a result of the presence of factors enumerated in the definition of blighted area, the

area is a detriment to the health and vitality of the community, requiring the use of the

municipality's urban renewal powers to correct those conditions or prevent their spread.

In some cases, the factors enumerated in the definition are symptoms of decay, and in

some instances, these factors are the cause of the problems. The definition requires the

governing body to examine the factors and determine whether these factors indicate a

deterioration that threatens the community as a whole. This determination is facilitated

by the Conditions Study. A Conditions Study is a necessary step if urban renewal, as

defined and authorized by Colorado Urban Renewal Law, is to be used as a tool by

DURA to remedy and prevent conditions of blight. The findings and conclusions

presented in such a report are intended to assist the City Council in making a final

determination as to whether the study area qualifies as blighted. The feasibility and

appropriateness of using urban renewal as a reinvestment tool is also discussed in a

Conditions Study. Based upon the conditions identified in the study area, the Conditions

Study makes a recommendation as to whether the study area qualifies as a blighted

area. In Denver, the ultimate determination of blight is the responsibility of the City

Council.

30

See C.R.S. § 31-25-103(2). "Blighted area" means an area that, in its present condition and use and, by reason of the presence of at least four of the following factors, substantially impairs or arrests the sound growth of the municipality, retards the provision of housing accommodations, or constitutes an economic or social liability, and is a menace to the public health, safety, morals, or welfare: (a) Slum, deteriorated, or deteriorating structures; (b) Predominance of defective or inadequate street layout; (c) Faulty lot layout in relation to size, adequacy, accessibility, or usefulness; (d) Unsanitary or unsafe conditions; (e) Deterioration of site or other improvements; (f) Unusual topography or inadequate public improvements or utilities; (g) Defective or unusual conditions of title rendering the title nonmarketable; (h) The existence of conditions that endanger life or property by fire or other causes; (i) Buildings that are unsafe or unhealthy for persons to live or work in because of building code violations, dilapidation, deterioration, defective design, physical construction, or faulty or inadequate facilities; (j) Environmental contamination of buildings or property; (k) (Deleted by amendment, L. 2004, p. 1745, § 3, effective June 4, 2004.) (k.5) The existence of health, safety, or welfare factors requiring high levels of municipal services or substantial physical underutilization or vacancy of sites, buildings, or other improvements. Ibid. 31

See C.R.S. § 31-25-107(1).

P a g e 8

City and County of Denver

Blight Factors

The Colorado Urban Renewal Law provides a list of eleven factors that, through their

presence, may allow an area to be declared as blighted. Using these criteria, the statute

requires, depending on the circumstances, that a minimum of either one, four, or five

blight factors be present for an area to be considered a blighted area. Colorado courts

have developed a guide toward the determination of whether an area constitutes a

blighted area under the Urban Renewal Law.32 First, the absence of widespread violation

of building and health codes do not preclude a finding of blight. The courts have held,

"the definition of blighted area is broad and encompasses not only those areas

containing properties so dilapidated as to justify condemnation as nuisances, but also

envisions the prevention of deterioration.”33 Courts have also reasoned that the presence

of one well-maintained building does not defeat a determination that an area

constitutes a blighted area. Normally, a determination of blight is based upon an area

taken as a whole and not on a building-by-building, parcel-by-parcel, or block-by-block

basis.34

Four Factor Blight Test

The definition of a blighted area is articulated in the Colorado Urban Renewal statute.

This definition is used when a Conditions Study is performed. Blighted area means an

area that, in its present condition and use and, by reason of the presence of at least four

of the following factors, substantially impairs or arrests the sound growth of the

municipality, retards the provision of housing accommodations, or constitutes an

economic or social liability, and is a menace to the public health safety, morals, or

welfare.35

a. Slum, deteriorated, or deteriorating structures36

b. Predominance of defective or inadequate street layout37

c. Faulty lot layout in relation to size, adequacy, accessibility, or usefulness

d. Unsanitary or unsafe conditions

e. Deterioration of site or other improvements

f. Unusual topography or inadequate public improvements or utilities

32

Urban blight is matter of both statewide and local concern. Denver Urban Renewal Auth. v. Byrne, 618 P.2d 1374 (Colo. 1980). Both the Colorado general assembly and local government can act to alleviate problem or urban blight provided the state and the local law do not conflict. Denver Urban Renewal Auth. v. Byrne, 618 P.2d 1374 (Colo. 1980). 33

Welton Corridor Conditions Study, City and County of Denver, March 2012, Matrix Design Group, page 5. 34

Ibid. 35

See C.R.S. § 31-25-103(2). 36

Examples of exterior elements observed for signs of deterioration include: Primary elements (exterior walls, visible foundation, roof), Secondary elements (fascia/soffits, gutters/downspouts, windows/doors, facade finishes, loading docks) Ancillary structures (detached garages, storage buildings). Welton Corridor Conditions Study, page 7. 37

Conditions may include: inadequate street or alley widths, cross-sections, or geometries; poor provisions or unsafe conditions for the flow of vehicular traffic; poor provisions or unsafe conditions for the flow of pedestrians; insufficient roadway capacity leading to unusual congestion of traffic; inadequate emergency vehicle access, poor vehicular/pedestrian access to buildings. Ibid.

P a g e 9

OOffffiiccee ooff tthhee AAuuddiittoorr Office of the Auditor

g. Defective or unusual conditions of title rendering the title non-marketable

h. The existence of conditions that endanger life or property by fire or other

causes

i. Buildings that are unsafe or unhealthy for persons to live or work in because of

building code violations, dilapidation, deterioration, defective design,

physical construction, or faulty or inadequate facilities

j. Environmental contamination of buildings or property

k.5. The existence of health, safety, or welfare factors requiring high levels of

municipal services or substantial physical underutilization or vacancy of sites,

buildings, or other improvements

One Factor Blight Test – No Objections of Property Owners

The Urban Renewal Law also provides that if there is no objection by any property owners

or tenants to the inclusion of property within the urban renewal area, the area will meet

the definition of blighted area if there is the presence of any one of the eleven factors.38

Five Factor Blight Test – Eminent Domain

The statute also states a separate requirement for the number of blight factors that must

be present if private property is to be acquired by eminent domain. Blighted area shall

have the same meaning as set forth in section 31-25-103 (2), C.R.S., except that blighted

area means an area that, in its present condition and use and, by reason of the

presence of at least five of the factors.39 DURA has no eminent domain authority unless

the City Council grants it to the Authority. City Council has complete control to

determine if eminent domain is merited.40

Tax Increment Financing in Colorado

In Colorado, urban renewal projects may be financed in whole or in part by a URA

pursuant to the TIF provisions of the Urban Renewal Law, or by any other available source

of financing authorized to be undertaken by the Authority under C.R.S. § 31-25-105 of the

Urban Renewal Law.41 The impetus to use TIF in the 1970s was related to the declining

availability of federal funds for urban renewal projects. This situation coupled with a

38

See C.R.S. § 31-25-103(2). 39

C.R.S. § 31-25-105.5.(5)(a) Acquisition of private property by eminent domain by authority for subsequent transfer to private party - restrictions - exceptions - right of civil action - damages – definitions. Paragraph (5)(a) provides that a “blighted area" shall have the same meaning as set forth in section 31-25-103 (2); except that, for purposes of this section only, "blighted area" means an area that, in its present condition and use and, by reason of the presence of at least five of the factors specified in section 31-25-103 (2) (a) to (2) (l), substantially impairs or arrests the sound growth of the municipality, retards the provision of housing accommodations, or constitutes an economic or social liability, and is a menace to the public health, safety, morals, or welfare . 40

David Broadwell, Esq. testimony provided during the Welton Corridor Redevelopment Plan, Public Hearing, September 10, 2012. See generally C.R.S § 31-25-105.5. Acquisition of private property by eminent domain by authority for subsequent transfer to private party - restrictions - exceptions - right of civil action - damages – definitions and C.R.S § 31-25-107. Approval of urban renewal plans by local governing body. 41

Colorado Legislative Council Staff, Memorandum, Property Tax Accruing to Tax Increment Financing Districts, January 8, 2008.

P a g e 10

City and County of Denver

national recession in 1974 and 1975 made the use of TIF more prevalent. “TIF was used as

a financing mechanism to offset the reduced level of federal funding and allow cities

and other jurisdictions to work with the private sector to stimulate economic growth and

employment through urban redevelopment projects.”42 Colorado enacted the TIF

portion of its urban renewal law in 1975. The initial Colorado TIF was used by the Boulder

Urban Renewal Authority for the development of the Crossroads Urban Renewal Project

in 1979. In 1980, the Colorado legislature expanded the ability of TIF to municipal sales

tax.43

How Do TIFs Work?

TIF is a mechanism for funding redevelopment projects. The concept of TIF has been

around since the early 1940s. TIF was used as a financing mechanism to offset the

reduced level of federal funding and allow cities to work with the private sector to

stimulate economic growth through urban redevelopment projects. California was the

first state to adopt a TIF law in 1952.

TIF is a mechanism to capture the net new or incremental taxes that are created when a

blighted property is redeveloped and use those incremental revenues to help finance

the project. The Colorado Urban Renewal Law authorizes an urban redevelopment

authority such as DURA to issue tax increment revenue bonds to fund redevelopment

costs including eligible developer project expenses.

Since tax increment revenues will be generated and collected over the life of the

project, which could be up to twenty-five years, there generally are no revenues at the

inception of a project when development costs are being incurred. Consequently

money must be borrowed or invested up front and be repaid over time. DURA

accomplishes this by agreeing to reimburse the developer or by issuing TIF bonds, or

both.

When DURA agrees to reimburse the developer, the developer must borrow or invest to

pay the eligible project costs. If the developer borrows funds, TIF revenues can be used

as collateral and a source of repayment for the banks or the investors. The developer’s

project costs can include capital costs for demolishing improvements, excavating,

grading, landscaping, and constructing improvements within the areas covered by the

Urban Renewal Plan.

42

Ibid. 43

Ibid. See also, C.R.S. Section 31-25-807(3)(a).

P a g e 11

OOffffiiccee ooff tthhee AAuuddiittoorr Office of the Auditor

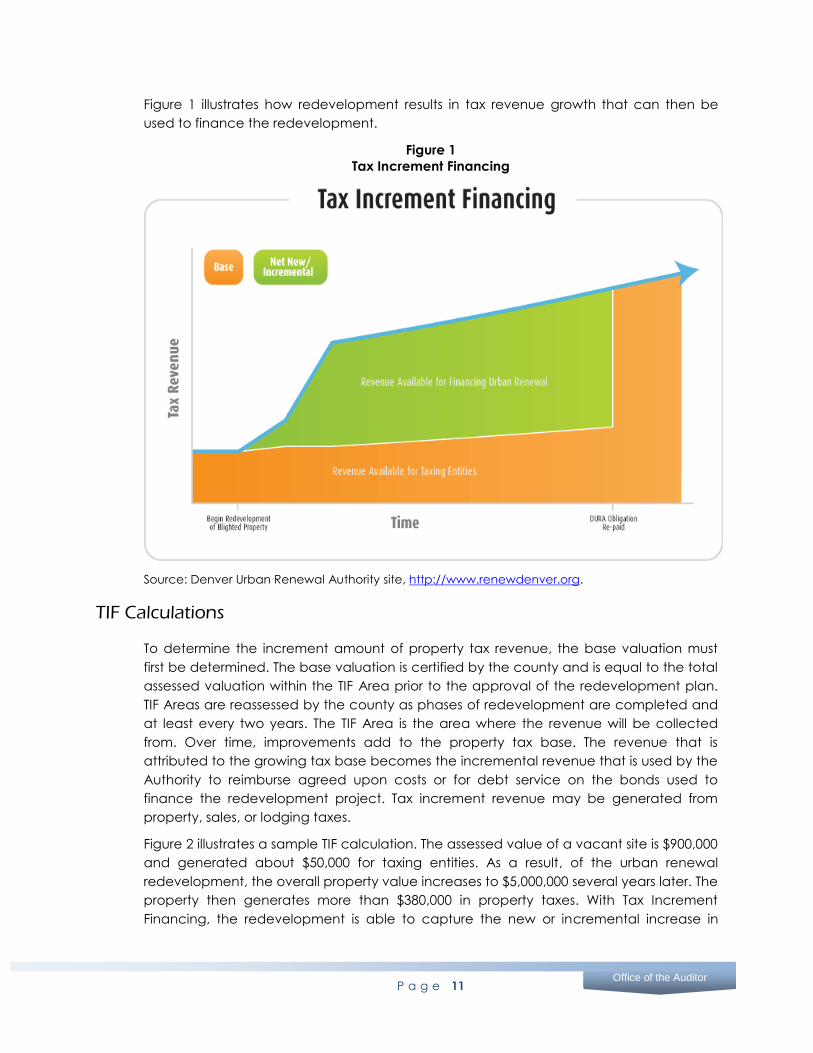

Figure 1 illustrates how redevelopment results in tax revenue growth that can then be

used to finance the redevelopment.

Figure 1

Tax Increment Financing

Source: Denver Urban Renewal Authority site, http://www.renewdenver.org.

TIF Calculations

To determine the increment amount of property tax revenue, the base valuation must

first be determined. The base valuation is certified by the county and is equal to the total

assessed valuation within the TIF Area prior to the approval of the redevelopment plan.

TIF Areas are reassessed by the county as phases of redevelopment are completed and

at least every two years. The TIF Area is the area where the revenue will be collected

from. Over time, improvements add to the property tax base. The revenue that is

attributed to the growing tax base becomes the incremental revenue that is used by the

Authority to reimburse agreed upon costs or for debt service on the bonds used to

finance the redevelopment project. Tax increment revenue may be generated from

property, sales, or lodging taxes.

Figure 2 illustrates a sample TIF calculation. The assessed value of a vacant site is $900,000

and generated about $50,000 for taxing entities. As a result, of the urban renewal

redevelopment, the overall property value increases to $5,000,000 several years later. The

property then generates more than $380,000 in property taxes. With Tax Increment

Financing, the redevelopment is able to capture the new or incremental increase in

P a g e 12

City and County of Denver

property tax revenue. The original tax entities continue to receive appreciation-adjusted

revenue as if the site were still a vacant site.

Figure 2

Sample TIF Calculation

Source: Denver Urban Renewal Authority website, http://www.renewdenver.org.

All property taxes attributable to the base valuation are paid to each taxing entity in the

TIF Area. When DURA has repaid the TIF obligation it incurred to finance the project within

the urban renewal area, the incremental revenues will be available to the original taxing

entities from that point forward.

Process for Creating a TIF Area

The City and County of Denver has multiple touch points with a TIF project before it is

created. Appendix A illustrates the process for creating a TIF project using a cross-

functional process map, which shows a step-by-step pictorial sequence of the process.

This type of process map is a tool that highlights inputs, outputs, and cycle time. It also

includes who is involved in the process and what the “who” is doing for the process.

The urban redevelopment review and approval process includes the establishment of

the Urban Redevelopment Area Plan; the Cooperation Agreement among the Area,

DURA, and the City and County of Denver; and the TIF Area. All these are approved by

City ordinance. Generally, City Council considers all three items at the same time.

However, there may be occasions when the TIF Area is considered later.

P a g e 13

OOffffiiccee ooff tthhee AAuuddiittoorr Office of the Auditor

For a project to be approved by the City Council, it must first meet the following City

criteria before a TIF Area can be created:

Fit within City plan

Meet blighted conditions

Approve final viability study

Once the City Council approves the Urban Renewal Plan and Urban Renewal Area, it

enters into the Cooperation Agreement with DURA which establishes the TIF Area. Once

all these steps are met, the base tax amount is set and the increment can go to DURA to

reimburse the developer.

The City’s primary authority related to DURA resides with the Mayor and City Council in

their authority to approve the appointment of Board members. In addition, several City

agencies are involved in the process for creating a TIF Area. Specifically, the Department

of Community Planning and Development and the City’s Planning Board are involved to

ensure that the Urban Redevelopment Plan aligns with various City plans such as its

Comprehensive Plan, Blueprint Denver, and/or any relevant small area or corridor plans.

The Assessor’s Office establishes the base property tax amount and the Controller’s

Office establishes the base sales tax amount. In addition, the process for establishing a TIF

Area involves public hearings, which enable the public to provide input. Figure 3

provides a high-level summary of the urban renewal process in Denver. See Appendix A

for a more detailed cross-functional process map of the process for creating a TIF Area.

Figure 3

The Urban Renewal Process

Source: Denver Urban Renewal Authority website, http://www.renewdenver.org.

P a g e 14

City and County of Denver

Potential Issues with TIFs

TIFs may fail to bring new investment. In order to be a productive use of taxpayer

resources, a city must judge that a development would not happen but for the issuance

of a subsidy. In practice, this can be difficult to prove one way or the other.44

TIFs may serve narrow interests without a broader public benefit. A TIF can be lucrative to

private developers seeking locations in which to build. However, from the public’s

perspective, TIFs are meant to benefit broader public goals. A recent study suggests that

there be a clear evaluation of a TIF project’s benefits to the public; however, such an

evaluation can often become lost in public officials’ rush to deliver new economic

development.45

TIFs may draw investment from areas that need it most. TIFs were originally designed to

act as a catalyst for new investment in blighted neighborhoods that suffer from chronic

underinvestment. These neighborhoods can suffer from vicious cycles of economic

decline for many reasons. TIFs are an effective public policy tool when used as part of a

development strategy that delivers public benefits and unlocks economic potential in

areas of need.46

TIF may impose local governments with additional costs if growth is less than anticipated.

If a municipality issues bonds on future TIF revenue and the developments fail to

generate sufficient additional growth, local government may be forced to use its

general tax revenue on an expensive bailout.47

The TIF process may lack transparency. TIF district spending is typically far harder for

residents to follow and monitor than ordinary spending. Ordinary budget transparency

requirements generally do not apply to TIF districts. TIF districts may be overseen by

relatively obscure agencies with little public disclosure.48

44

Tax-Increment Financing: The Need for Increased Transparency and Accountability in Local Economic Development Subsidies, U.S. PIRG Education Fund Fall 2011. 45

Ibid. 46

Ibid. 47

Ibid. 48

Ibid.

P a g e 15

OOffffiiccee ooff tthhee AAuuddiittoorr Office of the Auditor

SCOPE

Our audit assessed the City’s relationship with the Denver Urban Renewal Authority

(DURA), including the process for designating Tax Increment Financing (TIF) Areas and of

the use of TIF funds generally. We focused on information and practices between the

City and DURA. Our conclusions are based on our review of two areas. First, we reviewed

the City Council process for authorizing an Urban Redevelopment Area (URA) and a TIF

Area. Second, we reviewed the City’s and DURA’s progress reporting regarding DURA

activity.

OBJECTIVE

The objective of our audit was to determine if any enhancements are needed in the

City’s relationship with DURA regarding the use of tax increment financing (TIF) and the

monitoring of TIFs used for urban redevelopment purposes.

METHODOLOGY

We utilized the following methodologies to achieve our audit objective:

Reviewing the Colorado Urban Renewal Law to determine the City’s roles and

responsibilities related to oversight of the designation of TIF Areas and the

expenditure of TIF funds

Assessing the process for establishing TIF Areas

Interviewing personnel from the Denver Urban Renewal Authority, the

Department of Finance, the Denver City Attorney’s Office, and the Department

of Community Planning and Development to understand roles and practices

Locating the Cooperation Agreements between the City and DURA for TIF Areas

Reviewing and assessing ten Cooperation Agreements between DURA and the

City for audit and reporting requirements

Reviewing City Council meetings and briefing documents for comment during

the process for approving selected TIF Areas

Conducting benchmarking work to assess reporting and other practices adopted

by other Urban Renewal Authorities across the nation

P a g e 16

City and County of Denver

FINDING

Additional Tax Increment Financing Information Can Be Made Available to Stakeholders

Based on a limited review of the process for approving urban redevelopment in the City

and County of Denver through tax increment financing (TIF), we found that various City

entities and the public are involved. However, after a TIF Area is approved, we found

limited information about TIF Areas and TIF-funded projects. We identified three types of

information that could provide the City, the public, and other stakeholders additional

detail on TIF Areas and TIF funding of redevelopment projects. Specifically, the City can

create a repository of TIF Cooperation Agreements, publish a list of active Denver Urban

Renewal Plans and TIF Areas, and include urban renewal reporting on the Transparent

Denver webpage to periodically report comprehensive urban renewal activity.

Substantive Stakeholder Involvement in the TIF Designation Process

Audit work included a limited review of the process for approving TIF-funded urban

redevelopment. This review revealed that various City entities and the public are

involved in the process. The Denver Planning Board plays an important role in ensuring

the Urban Renewal Plan is in keeping with the City’s Comprehensive Plan, Blueprint

Denver, and any other relevant smaller area plans.49 Further, Denver’s School District is

permitted to participate in an advisory capacity concerning any TIF that may be in the

Urban Renewal Plan. In addition, several opportunities exist for citizen review during the

process for approving TIF-funded redevelopment. For example, a formal hearing is

required when the ordinance is presented to City Council for approval of the Urban

Renewal Plan, Cooperation Agreement, and the TIF Area. The involvement of City

agencies and the public enhances transparency into the process for approving TIF and

the redevelopment plans they are used to finance.

No Centralized List for TIF Areas and Cooperation Agreements

Our review included examining the Cooperation Agreements between Denver Urban

Renewal Authority (DURA) and the City. We encountered great difficulty in obtaining

these Agreements because the City lacks a centralized repository where interested

parties can access all Agreements. Therefore, we recommend the Chief Financial Officer

create a consolidated repository of TIF Cooperation Agreements.

The terms of the agreement between DURA and the City regarding each TIF Area is

captured in a Cooperation Agreement. The Colorado Urban Renewal Law and the

Colorado Constitution authorize the City and DURA to enter into cooperative

agreements. Typically, a Cooperation Agreement between the City and DURA

acknowledges, ratifies, and confirms the understanding and agreement between the

49

Blueprint Denver is a land use and transportation plan outlining a multi-modal transportation system with land use that accommodates future growth, and open space throughout the city. The plan was adopted in 2002 as a supplement to the Denver Comprehensive Plan 2000.

P a g e 17

OOffffiiccee ooff tthhee AAuuddiittoorr Office of the Auditor

City and DURA relating to any costs incurred by the City in connection with the

acquisition and construction of an urban renewal project and the provision of services to

the Urban Renewal Area. Further, Cooperation Agreements can be amended. While we

were able to locate some amended Agreements, we were unable to determine when

an Agreement was amended or whether an amended Agreement we located was the

final one. For example, we obtained the fourth amendment to the Downtown Denver TIF

Area Agreement. This indicates that we could search for Amendments one through

three, but we do not know if the Agreement was amended a fifth time.

We searched several sources for the Cooperation Agreements, and all yielded a

different number of TIF Areas. Table 1 summarizes these sources and the numbers of TIF

Areas identified by each source.

Table 1

Source and Number of TIF Areas

Source Number

of TIF

Areas

1 List of “TIF Districts” from the Department of Finance 30

2

Alfresco - using a list of contracts from the Clerk &

Recorder (16) and searching using the term “Denver

Urban Renewal Authority” (4)

20

3 Map of State Legislative Districts created by the

Department of Finance 32

4 Map of Denver TIF Areas from the Department of

Finance 37

5 Maps on DURA website 31

6 List developed in a meeting with Department of

Finance staff 38

7 Department of Finance’s internal shared drive 43

Source: Audit team compilation of sources.

The City’s Office of the Clerk and Recorder is the official repository of City records.

However, our search for Cooperation Agreements revealed limitations in using the Clerk

and Recorder for this purpose. The Clerk and Recorder’s system can be searched in

various ways. One is to search for a specific document using the City Clerk’s Filing

Number. However, this method cannot be used if the Filing Number is unknown. Another

is to search for contracts between the City and another party using the Second Party

Name field, then obtain a copy of the contract using Alfresco, the City’s automated

contract management system. DURA is the second party for the Cooperation

Agreements. However, while every contract is assigned a contract number, this field is

not consistently populated in the Clerk and Recorder’s system. As a result, this method

cannot be utilized to identify all Cooperation Agreements.

P a g e 18

City and County of Denver

Further, we found that the Alfresco system can be unreliable in performing this type of

search. For example, we searched for a specific contract number associated with DURA,

and found that the number was associated with a different contract in which DURA was

not the second party. As a result, we had to obtain the Cooperation Agreements from

various sources, and still did not have a way to ensure we had obtained all the

Agreements.

Working with DURA, we defined thirty-two TIF Areas.50 We recognize that urban

redevelopment is an ongoing activity, making it difficult to maintain up-to-date

information. However, the lack of a master list or method of accessing information

regarding active TIF Areas or projects inhibits transparency into TIF-funded urban

redevelopment activity in the City. We therefore recommend that the Chief Financial

Officer publish a list of active Denver Urban Renewal Plans and TIF Areas.

Opportunities to Enhance Urban Renewal Public Reporting

An annual report is a formal assessment of the previous year's operations. It also discusses

the goals of the upcoming year and the performance of current projects. Annual reports

are intended to give interested parties information about the organization's activities and

financial performance. While DURA publishes its annual audited financial statements on

its website, which are also included in the City’s Comprehensive Annual Financial Report,

it does not provide a formal annual report of project activities to the City and has not

published an annual report on its website since 2006.51

We reviewed several Urban Renewal Authorities’ (URAs) annual reports from across the

nation. We found the annual reports from Lakewood, Colorado, and Kansas City,

Missouri, had comprehensive information about their respective URA activities. We noted

that these reports included information about the organization as a whole, including

goals for the upcoming year and financial information from the previous year. In

addition, the Lakewood and Kansas City URA annual reports provide the following

information pertaining to specific projects:

A breakdown of increment spending

Total project costs allocated to the developer, the city, and the URA

The original estimate of time to pay off bonds and any debt

The most recent estimate of time to pay off bonds and any debt

The number of parcels obtained through the use of eminent domain, if

applicable

The number of residences and businesses relocated as a result of a Plan or Project

Any special agreements with affected taxing districts within the TIF Area during

the report period

The boundaries of the TIF Plan, and an attached boundary map from the Plan

50

See Appendix B for a list of the TIF Areas. 51

Although not an annual report, in 2008 DURA developed a publication for its 50th

anniversary called 50 Years of Revitalizing Denver.

P a g e 19

OOffffiiccee ooff tthhee AAuuddiittoorr Office of the Auditor

A summary of business activity in the TIF Area

A summary of increasing property values within the TIF Area

A chart showing assessed values over time (see Table 2 for an example)

Table 2

Lakewood, Colorado, URA Annual Report – Example of a Summary of Property Values

Year Assessed Value

2000 $11,534,200

2001 $9,025,170

2002 $4,341,940

2003 $6,293,460

2004 $12,624,800

2005 $34,185,530

2006 $40,170,040

2007 $45,978,720

2008 $52,596,400

2009 $54,889,920

2010 $53,692,620

2011 $48,297,907

Source: Lakewood Reinvestment Authority, Annual Report 2011, Phase

II Belmar Redevelopment Area. We did not audit these numbers. We

included them to provide an example of what a summary of property

values may look like.

Our review of six other URAs revealed that they all publish an annual report of URA

activities, while DURA does not consistently provide comprehensive annual reporting to

the City.52 Regular reporting enhances transparency and would allow stakeholders a

more comprehensive vision of DURA’s activities and redevelopment projects funded

through TIF.

52

The six URAs benchmarked included Lakewood Reinvestment Authority, Lakewood, Colorado; Pueblo Urban Renewal Authority, Pueblo, Colorado; Colorado Springs Urban Renewal Authority, Colorado Springs, Colorado; Community Development Commission, Chicago, Illinois; Invest Atlanta, Atlanta, Georgia; and Economic Development Corporation, Kansas City, Missouri. The City Assessor's Office webpage does provide links to the Denver Abstract and District Levies, which include a list of TIF Areas and their respective levies, the amount of assessed value increment of each TIF Area, and taxes distributed to DURA; however, this information relates only to property taxes. TIF Areas can also be funded by municipal sales and lodger’s taxes.

P a g e 20

City and County of Denver

TIF Reporting Best Practice

A recent study suggests that TIF information be comprehensive, one-stop, and one-click.

Comprehensive–including all the various ways governments spend money, including the

provision of subsidies to private actors. One-stop–aggregating all information on

government spending into a single website. One-click–providing searchable,

downloadable information that can be accessed by citizens without requiring a pre-

existing knowledge of budgetary nomenclature or bureaucratic structure.53

Governments should provide information regarding TIFs in an easy to understand format,

located in a central location.

1. Budget information about all TIF districts in a city, and about each individual TIF

district, accessible online.

2. Information on each TIF district should include:

a. The overall goals of the TIF district

b. The value of the TIF

c. The specific benefits (in terms of jobs or other measures) that it is

expected to produce

d. The most current information on what benefits have been produced to

date

e. The identities of all recipients of TIF funds

f. Regular reports on the progress of the project

3. Funds raised through TIF districts should be covered by at least the same

transparency requirements that apply to ordinary municipal spending.

4. Tracking of city spending in TIF districts should include not only direct outlays,

but also any subsidies provided.

Colorado Municipal League URA Reporting

Founded in 1923, the Colorado Municipal League (CML) is a nonprofit, nonpartisan

organization providing services and resources to assist municipal officials in managing

their governments and serving the cities and towns of Colorado.54

Currently, the CML website houses annual reporting from twenty-nine different URAs

located within Colorado.55 CML provides a template for a URA annual report, as shown in

Appendix C. CML reporting is completely voluntary on the part of a URA, with 56 percent

of the URAs in Colorado participating.56 DURA has not participated in CML’s voluntary

reporting. According to CML, this is due to the fact that DURA has a large number of

projects, thus creating a considerable amount of work to put together the report.

53

Tax-Increment Financing: The Need for Increased Transparency and Accountability in Local Economic Development Subsidies, U.S. PIRG Education Fund Fall 2011. 54

Colorado Municipal League, https://www.cml.org/about/. 55

Colorado Municipal League, Urban Renewal, https://www.cml.org/issues.aspx?taxid=11125. 56

Colorado Municipal League is currently evaluating whether it will continue to collect this information.

P a g e 21

OOffffiiccee ooff tthhee AAuuddiittoorr Office of the Auditor

However, the information URAs report to CML provides another example of the type of

data that DURA could provide to enhance the transparency of TIF projects and TIF

spending. While we are not suggesting that DURA participate in the CML program, we

do think the program provides an example of how other URAs report and that the City

and DURA should consider how more urban renewal information can be presented to

the public.

Transparent Denver

In July 2013, the City launched a program called Transparent Denver, making access to

certain City financial records more transparent and providing a centralized online

location to do so. The Transparent Denver webpage on the City’s website provides

information in eight component areas: checkbook, budget, financial reports, revenue,

investments and debt, contracts, business tax, and property. The City launched the

Transparent Denver webpage as a result of the Mayor’s commitment to promote

transparency and accountability.57 As a component unit of the City and County of

Denver, DURA should consider taking part in this initiative. As revealed through

benchmarking of other URAs, transparency is fostered by publishing annual reports. We

believe that the City can enhance its transparency by providing periodic urban renewal

activity reports to the City Council as well as displaying them publicly online or

encouraging DURA to do so itself.

Therefore, we recommend that the Department of Finance, specifically the Chief

Financial Officer, include urban renewal reporting on the Transparent Denver webpage

to periodically report comprehensive urban renewal activity to the City and other

stakeholders.

57

Transparent Denver, http://www.denvergov.org/transparency.

P a g e 22

City and County of Denver

RECOMMENDATIONS

We offer three recommendations to help the City enhance access to information regarding

urban renewal activity in Denver:

1.1 Cooperation Agreements – The Chief Financial Officer should create a

consolidated repository of TIF cooperation agreements.

1.2 Current Denver Urban Renewal Inventory – The Chief Financial Officer should

publish a list of active Denver Urban Renewal Plans and TIF Areas.

1.3 Regular DURA Reporting – The Chief Financial Officer should include urban

renewal reporting on the Transparent Denver webpage to periodically report

comprehensive urban renewal activity to the City and other stakeholders.

P a g e 23

Office of the Auditor

APPENDIX A

Cross Functional Process Map of Denver’s TIF Process

D enver T IF Process

De

ve

lop

er

Co

mm

un

ity

Pla

nn

ing

an

d

De

ve

lop

me

nt

Cit

y C

ou

nc

ilC

ity

of

De

nv

er

DU

RA

De

pa

rtm

en

t o

f

Fin

an

ce

As

se

ss

or

In itiates Idea

B lighted?

Process Ended

N o

Viable Project

R eview

C ontractors

F inancials

“Lessor of Three”

Process End

N o

Prelim inary

V iability (M eet w ith

C ity officals )

-F it in C ity V ision ?

-Possible B light?

Yes

F it w ith the city

p lan?Process End N o

Initiate B light

S tudy

Yes

F inal V iabilityYesD raft the U rban

R enew al P lan

F inal Evaluation of

V iability

F inal Evaluation of

V iability

D raft the Legal

D ocum ents

Prepare

presentation for

C ity C ouncil

Approve urban

renew al

project?

Process End N o

D eterm ine Base

Property Tax

Am ount

Yes

Is Sales Tax

U sed?

Increm ental

R evenues Begin

F low ing to D U R A

N o

C alculate Sales

Tax Am ountYes

Begin construction

F inalize

-U R Area

-U R P lan

-C ooperation

Agreem ent

F inal Evaluation of

V iability

P a g e 24

City and County of Denver

APPENDIX B

Active TIF Areas in the City and County of Denver

Funding Sources

Property

Tax

Sales

Tax

Lodger’s

Tax

1 9th & Colorado X

2 414 14th Street X

3 Adams Mark/Sheraton X X

4 Alameda Square X X

5 American National X X

6 Boston Lofts X

7 California Street Parking Garage X

8 Cherokee X X

9 City Park South X

10 Colorado National Bank Building X X X

11 Denver Dry X

12 Denver Pavilions X

13 Downtown Denver X

14 Executive Tower Hotel X X X

15 Globeville Commercial X X

16 Guaranty Bank X X

17 Highlands Garden Village X X

18 Lowenstein Theater X X

19 Lowry X

20 Marycrest X X

21 Mercantile Square X X

22 Northeast Park Hill X

23 Pepsi Center X

24 Point Urban X X

25 Rio Grande X

26 Saint Anthony X

27 South Broadway X X

28 Stapleton X X

29 Tamarac South X

30 Ironworks Foundry X X

31 Westwood X X

32 York Street X

Source: Developed by audit team from Department of Finance and DURA information.

P a g e 25

OOffffiiccee ooff tthhee AAuuddiittoorr Office of the Auditor

APPENDIX C

Colorado Municipal League URA Annual Report Template

(ura name) Contact:

(ura street address) (name)

(ura city, zip) (telephone)

(website) (email)

Project #1 Project #2 All Projects

REVENUES

Property tax increment $ $ $ -

Sales tax increment $ $ $ -

Other increment $ $ $ -

Subtotal Tax Increment Revenue $ - $ - $ -

Interest earnings $ $ $ -

Project fees $ $ $ -

User fees $ $ $ -

Grants and gifts $ $ $ -

Other $ $ $ -

Subtotal Other Revenue $ - $ - $ -

Total Revenue $ - $ - $ -

EXPENDITURES

Program administration $ $ $ -

URA capital improvement projects $ $ $ -

Debt service $ $ $ -

Restricted funds $ $ $ -

Agreements with other taxing bodies:

Total Expenditures $ - $ - $ -

DEBT COSTS

Current tax increment obligations $ $ $ -

Total 2011 debt service payments $ $ $ -

BASE PROPERTY TAX REVENUE TO OTHER TAXING ENTITIES

Current property tax base amount $ $ $ -

Percent of increase in base amount

FINANCIAL AUDIT

View the most recent financial audit on-line at:

BLIGHT FACTOR REMEDIATION

Urban Renewal Area "A" Blight Factors Description of Remediation Activity:

Urban Renewal Area "B" Blight Factors Description of Remediation Activity:

Urban Renewal Area "C" Blight Factors Description of Remediation Activity:

PUBLIC/PRIVATE INVESTMENT

Project:

Developer cost $ - $ - $ -

URA participation $ - $ - $ -

Total project cost $ - $ - $ -

Project description:

Anticipated completion date:

For more information

For more information on urban renewal projects from prior years please visit prior annual reports at

Source: Colorado Municipal League.

P a g e 26

City and County of Denver

AGENCY RESPONSE

P a g e 27

OOffffiiccee ooff tthhee AAuuddiittoorr Office of the Auditor

P a g e 28

City and County of Denver