u.s. consumer spending outlook presented to: global insight spring outlook seminar chicago, illinois...

Post on 18-Dec-2015

216 views

TRANSCRIPT

U.S. Consumer Spending Outlook

Presented to:Global Insight Spring Outlook Seminar

Chicago, IllinoisMay 26, 2004

Presented by:Sara Johnson

Managing Director,Global Macroeconomics Group

Copyright © 2003 Global Insight, Inc.

Copyright © 2004 Global Insight, Inc. 2

U.S. Consumer Spending Keeps Growing!

• The recession that began in March 2001 was the first on record without a decline in real consumer spending.

• Low interest rates, tax cuts, and appreciating home values supported durable goods spending as unemployment rose.

• By mid-2002, job losses and depleted equity wealth caused households to restrain spending growth.

• More federal tax cuts and a stock market rally gave consumers a second wind in the summer of 2003.

• A solid rebound in employment and rising net worth will spark 4.0% growth in real consumer spending in 2004.

• But total spending will soon decelerate as tax cuts end and interest rates rise.

Copyright © 2004 Global Insight, Inc. 3

Retail Sales—A Great Start to 2004

Jan. Feb. March April %chya

Total Retail Sales 0.5 1.0 2.0 -0.5 8.0

Motor Vehicles -2.8 2.2 2.4 -1.8 3.6

Home Furnishings 1.2 0.6 1.4 0.7 9.8

Electronics & Appliances 0.0 0.9 1.0 0.8 12.4

Building Materials 0.6 0.4 11.0 -0.7 20.4

Health & Personal Care 0.6 -0.5 1.9 -0.1 6.8

Apparel 2.1 0.9 0.8 -2.0 8.2

General Merchandise 1.0 1.4 0.4 -0.8 7.2

Food & Beverage Stores 1.8 -0.5 0.7 0.5 4.2

Food Service Places 2.1 1.0 0.6 -0.1 10.9

(Percent change)

%chya = percent change from April 2003 to April 2004

Copyright © 2004 Global Insight, Inc. 4

Real Consumer Spending and Confidence

0

1

2

3

4

5

6

7

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

75

80

85

90

95

100

105

110

Real Consumption Growth Consumer Sentiment

(Annual percent change) (Michigan Index, 1966=100)

Copyright © 2004 Global Insight, Inc. 5

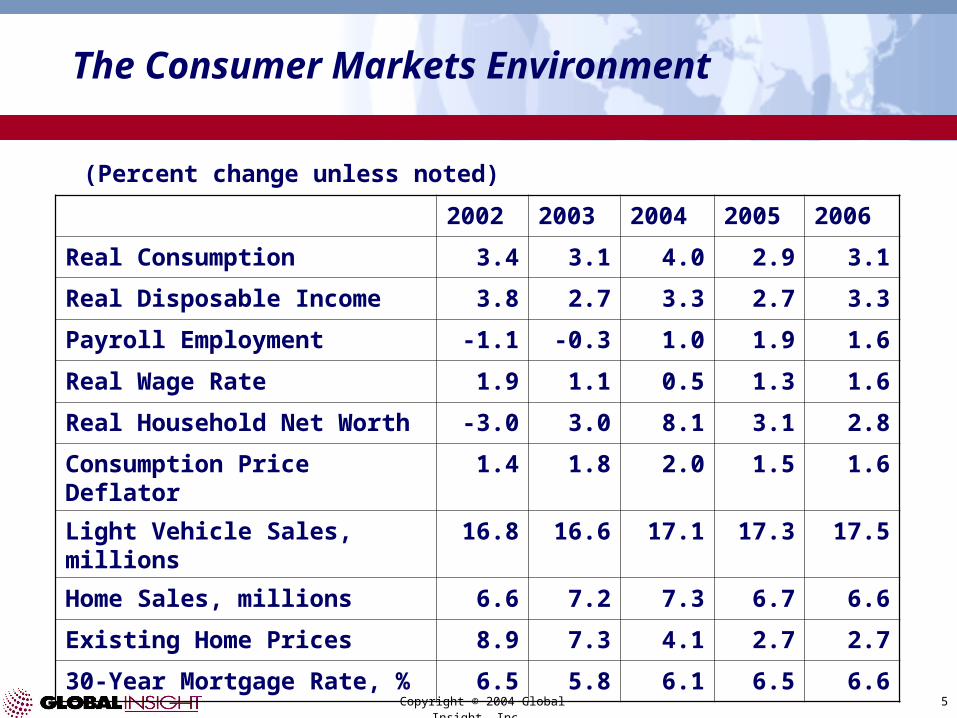

The Consumer Markets Environment

2002 2003 2004 2005 2006

Real Consumption 3.4 3.1 4.0 2.9 3.1

Real Disposable Income 3.8 2.7 3.3 2.7 3.3

Payroll Employment -1.1 -0.3 1.0 1.9 1.6

Real Wage Rate 1.9 1.1 0.5 1.3 1.6

Real Household Net Worth -3.0 3.0 8.1 3.1 2.8

Consumption Price Deflator 1.4 1.8 2.0 1.5 1.6

Light Vehicle Sales, millions 16.8 16.6 17.1 17.3 17.5

Home Sales, millions 6.6 7.2 7.3 6.7 6.6

Existing Home Prices 8.9 7.3 4.1 2.7 2.7

30-Year Mortgage Rate, % 6.5 5.8 6.1 6.5 6.6

(Percent change unless noted)

Copyright © 2004 Global Insight, Inc. 6

Disposable Income Supports Consumer Spending

-1

0

1

2

3

4

5

6

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Real Consumption Real Disposable Income

(Percent change)

Copyright © 2004 Global Insight, Inc. 7

When Will Employment Regain Its 2000-01 Peak?

2001-032004200520062007-09

Copyright © 2004 Global Insight, Inc. 8

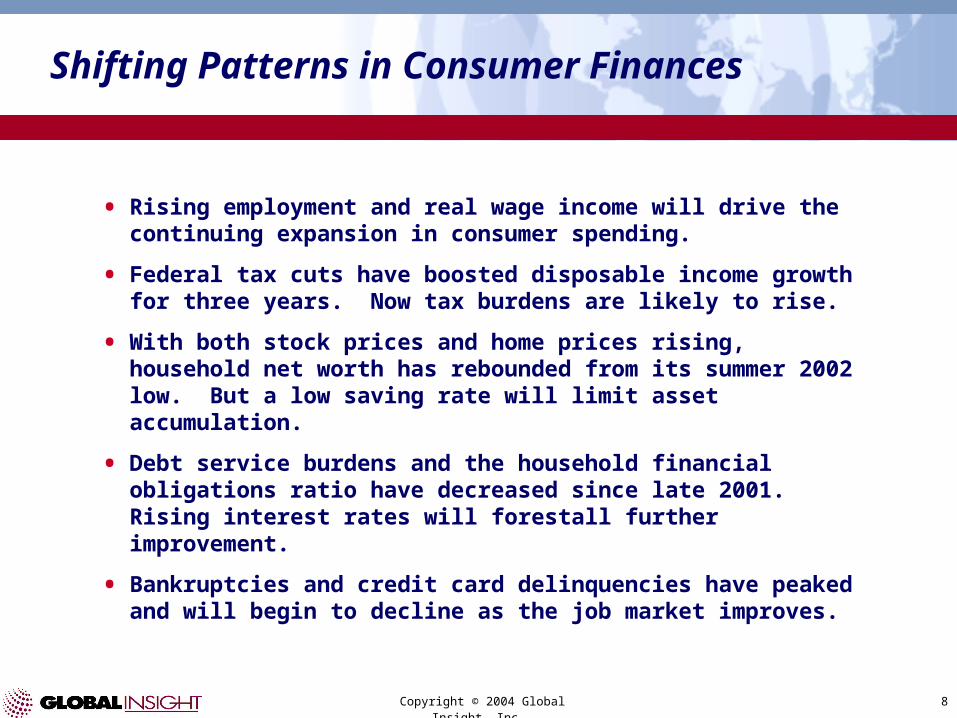

Shifting Patterns in Consumer Finances

• Rising employment and real wage income will drive the continuing expansion in consumer spending.

• Federal tax cuts have boosted disposable income growth for three years. Now tax burdens are likely to rise.

• With both stock prices and home prices rising, household net worth has rebounded from its summer 2002 low. But a low saving rate will limit asset accumulation.

• Debt service burdens and the household financial obligations ratio have decreased since late 2001. Rising interest rates will forestall further improvement.

• Bankruptcies and credit card delinquencies have peaked and will begin to decline as the job market improves.

Copyright © 2004 Global Insight, Inc. 9

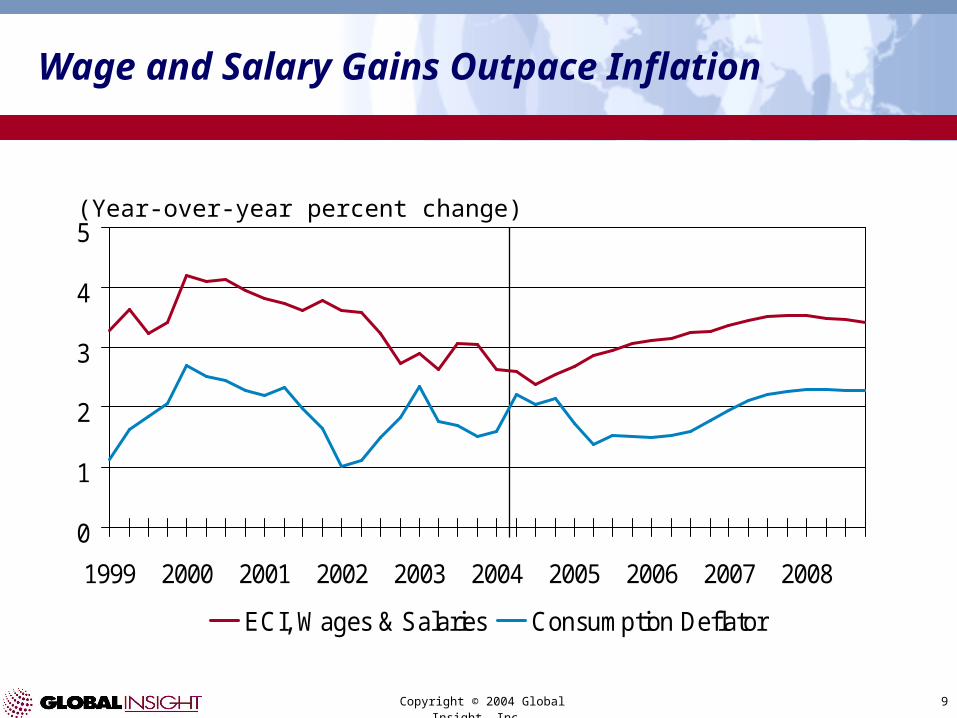

Wage and Salary Gains Outpace Inflation

(Year-over-year percent change)

0

1

2

3

4

5

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

ECI, Wages & Salaries Consumption Deflator

Copyright © 2004 Global Insight, Inc. 10

The Saving Rate Remains Low, Limiting the Recovery in Household Net Worth

0

2

4

6

8

10

12

1980 1984 1988 1992 1996 2000 2004 2008

3.5

4.0

4.5

5.0

5.5

6.0

6.5

Saving Rate Household Net Worth/Disposable Income

(Percent of disposable income) (Ratio to disposable income)

Copyright © 2004 Global Insight, Inc. 11

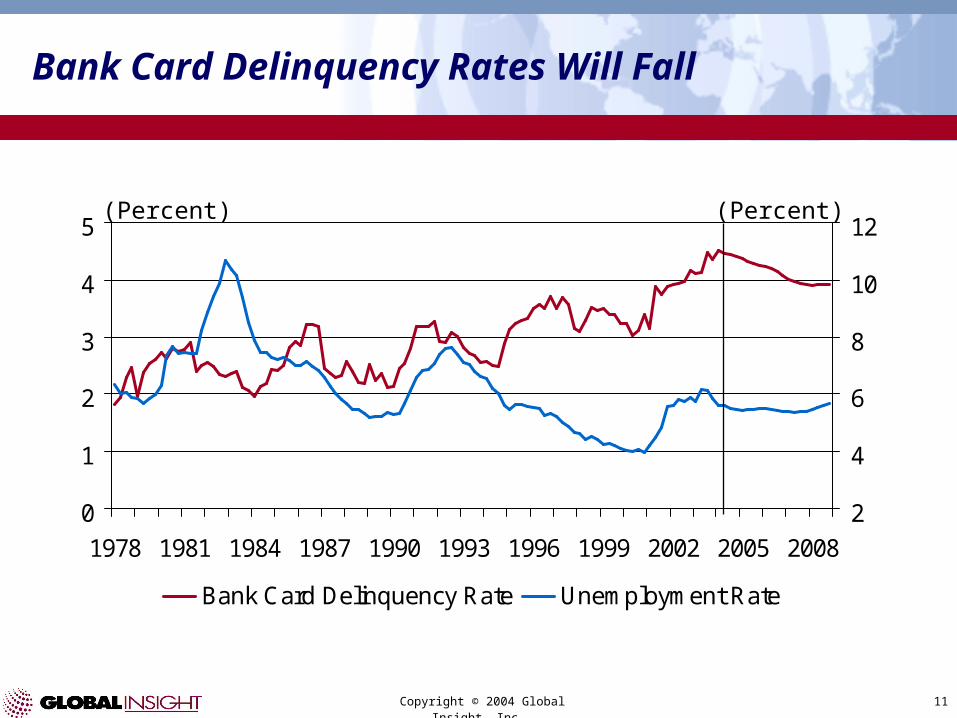

Bank Card Delinquency Rates Will Fall

0

1

2

3

4

5

1978 1981 1984 1987 1990 1993 1996 1999 2002 2005 2008

2

4

6

8

10

12

Bank Card Delinquency Rate Unemployment Rate

(Percent) (Percent)

Copyright © 2004 Global Insight, Inc. 12

Shifts in Consumer Spending on Essentials

0

5

10

15

20

25

30

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Food Energy Medical Housing Services

(Percent of total consumption)

Copyright © 2004 Global Insight, Inc. 13

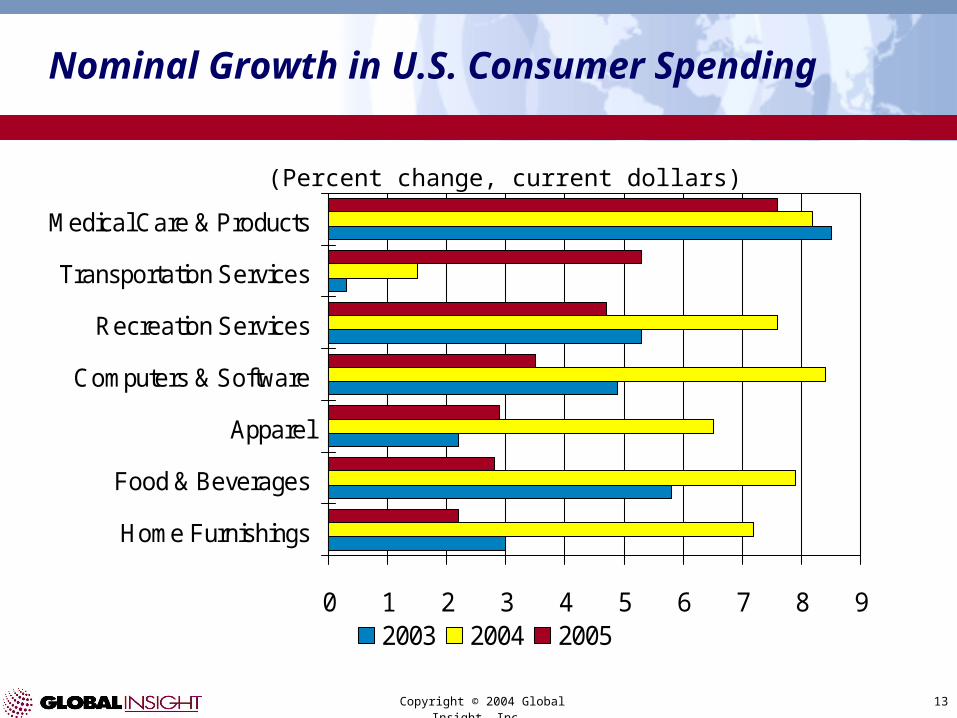

0 1 2 3 4 5 6 7 8 9

Home Furnishings

Food & Beverages

Apparel

Computers & Software

Recreation Services

Transportation Services

Medical Care & Products

2003 2004 2005

(Percent change, current dollars)

Nominal Growth in U.S. Consumer Spending

Copyright © 2004 Global Insight, Inc. 14

-4 -2 0 2 4 6 8 10

Motor Vehicles

Home Furnishings

Food & Beverages

Apparel

Recreation Services

Transportation Services

Medical Care & Products

2003 2004 2005

(Percent change, 2000 dollars)

Real Growth in U.S. Consumer Spending

Computers and Software: 28% in 2003, 24% in 2004, 20% in 2004

Copyright © 2004 Global Insight, Inc. 15

Real Spending on Home Furnishings Follows Housing Investment

-20

-15

-10

-5

0

5

10

15

20

1986 1989 1992 1995 1998 2001 2004 2007

Consumption of Home Furnishings Residential Investment

(Year-over-year percent change, 2000 dollars)

Copyright © 2004 Global Insight, Inc. 16

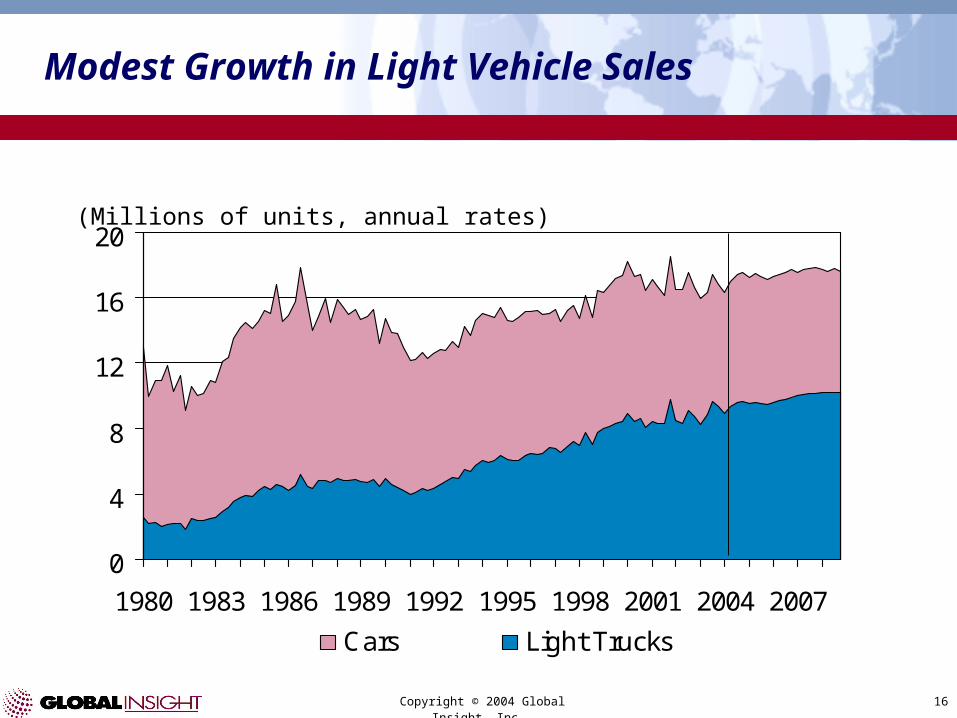

Modest Growth in Light Vehicle Sales

(Millions of units, annual rates)

0

4

8

12

16

20

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007

Cars Light Trucks

Copyright © 2004 Global Insight, Inc. 17

Light Vehicle Sales Are Sensitive to Oil Prices

15.5

16.0

16.5

17.0

17.5

18.0

18.5

1999 2000 2001 2002 2003 2004 2005 2006 2007

Baseline $40 Oil Scenario

(Millions of units, annual rates)

Copyright © 2004 Global Insight, Inc. 18

Global Insight’s Global Consumer Markets Service provides:

• Comprehensive view of worldwide consumer market activity

• 10-year forecasts on consumer spending by 22 product categories in 95 countries, updated in Q2 and Q4

• Forecasts and insights into demographic, socio-economic, and household income trends by country

• Microsoft Excel™ workbook format with tools for screening and selection

• Strategic insights to identify and compare business opportunities and market risks

New Global Consumer Markets Service

Copyright © 2004 Global Insight, Inc. 19

Country Coverage

North America

Canada

United States

Mexico

Latin America & Caribbean

Argentina

Belize

Bolivia

Brazil

Chile

Colombia

Costa Rica

Cuba

Ecuador

El Salvador

Guatemala

Honduras

Nicaragua

Panama

Paraguay

Peru

Puerto Rico

Uruguay

Venezuela

Western Europe

Austria

Belgium

Cyprus

Denmark

Finland

France

Germany

Greece

Iceland

Ireland

Italy

Luxembourg

Malta

Netherlands

Norway

Portugal

Spain

Sweden

Switzerland

United Kingdom

Eastern Europe

Azerbaijan

Belarus

Bulgaria

Croatia

Czech Republic

Estonia

Hungary

Kazakhstan

Latvia

Lithuania

Poland

Romania

Russia

Slovakia

Slovenia

Turkmenistan

Ukraine

Uzbekistan

Middle East & North Africa

Algeria

Egypt

Israel

Jordan

Kuwait

Morocco

Saudi Arabia

Tunisia

Turkey

United Arab Emirates

Sub-Saharan Africa

Côte D'Ivoire

Ghana

Nigeria

South Africa

Kenya

Tanzania

Uganda

Asia

Bangladesh

China

Hong Kong

India

Indonesia

Iran

Japan

South Korea

Malaysia

Pakistan

Philippines

Singapore

Sri Lanka

Taiwan

Thailand

Viet Nam

Oceania

Australia

New Zealand

Copyright © 2004 Global Insight, Inc. 20

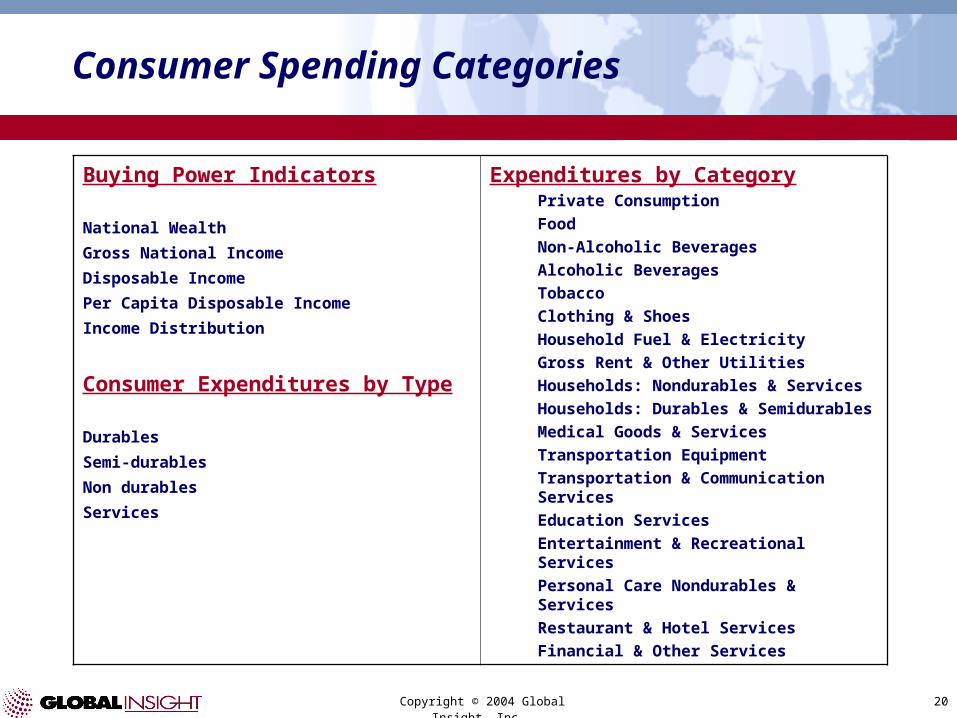

Consumer Spending Categories

Buying Power Indicators

National Wealth

Gross National Income

Disposable Income

Per Capita Disposable Income

Income Distribution

Consumer Expenditures by Type

Durables

Semi-durables

Non durables

Services

Expenditures by CategoryPrivate Consumption

Food

Non-Alcoholic Beverages

Alcoholic Beverages

Tobacco

Clothing & Shoes

Household Fuel & Electricity

Gross Rent & Other Utilities

Households: Nondurables & Services

Households: Durables & Semidurables

Medical Goods & Services

Transportation Equipment

Transportation & Communication Services

Education Services

Entertainment & Recreational Services

Personal Care Nondurables & Services

Restaurant & Hotel Services

Financial & Other Services

Copyright © 2004 Global Insight, Inc. 21

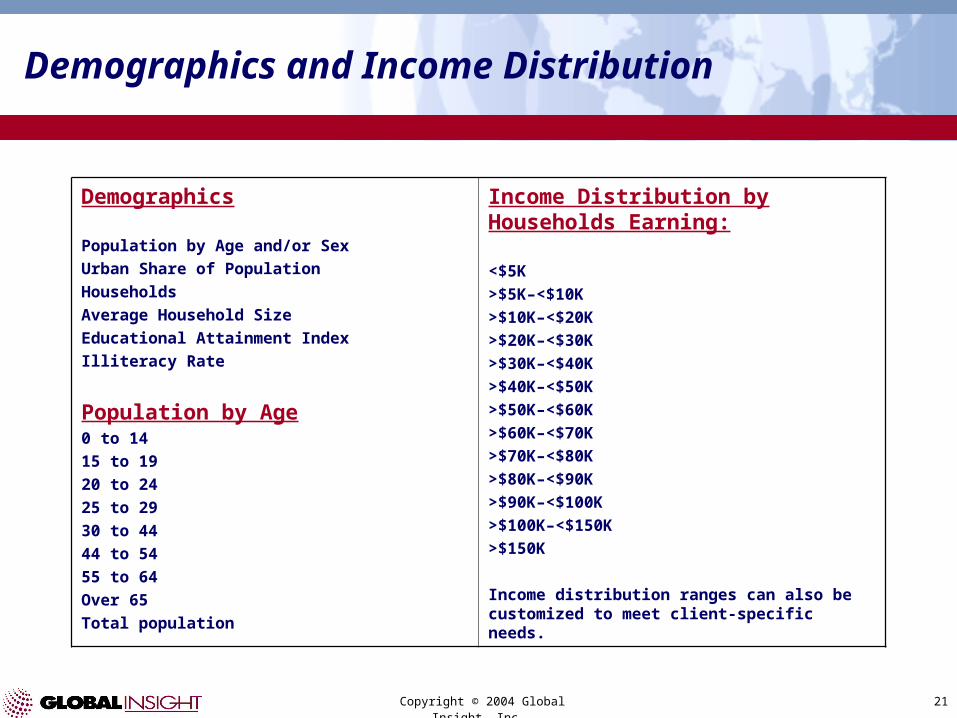

Demographics and Income Distribution

Demographics

Population by Age and/or Sex

Urban Share of Population

Households

Average Household Size

Educational Attainment Index

Illiteracy Rate

Population by Age0 to 14

15 to 19

20 to 24

25 to 29

30 to 44

44 to 54

55 to 64

Over 65

Total population

Income Distribution by Households Earning:

<$5K

>$5K–<$10K

>$10K–<$20K

>$20K–<$30K

>$30K–<$40K

>$40K–<$50K

>$50K–<$60K

>$60K–<$70K

>$70K–<$80K

>$80K–<$90K

>$90K–<$100K

>$100K–<$150K

>$150K

Income distribution ranges can also be customized to meet client-specific needs.

Copyright © 2004 Global Insight, Inc. 22

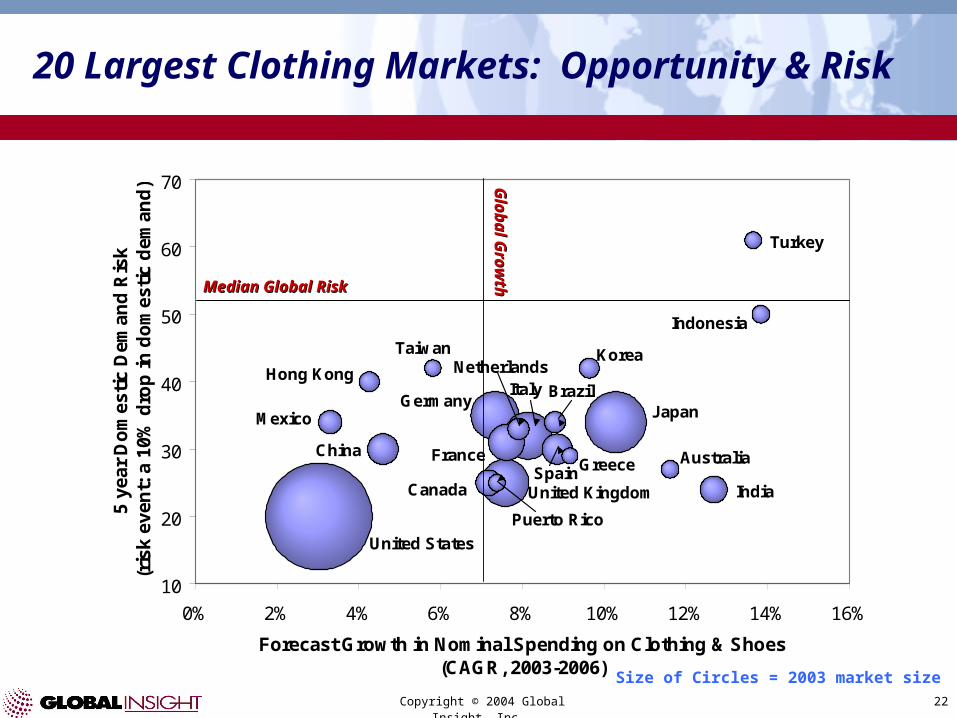

20 Largest Clothing Markets: Opportunity & Risk

Size of Circles = 2003 market size

Greece

Taiwan

Turkey

Puerto Rico

Australia

Indonesia

Hong KongKorea

Brazil

Netherlands

Mexico

Canada IndiaSpain

China France

United Kingdom

ItalyGermany

Japan

United States

10

20

30

40

50

60

70

0% 2% 4% 6% 8% 10% 12% 14% 16%

Forecast Growth in Nominal Spending on Clothing & Shoes(CAGR, 2003-2006)

5 ye

ar D

om

esti

c D

eman

d R

isk

(ris

k ev

ent:

a 1

0% d

rop

in d

om

esti

c d

eman

d)

Median Global RiskMedian Global Risk

Global G

rowth

Global G

rowth

Copyright © 2004 Global Insight, Inc. 23

500

505

510

515

520

525

530

535

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009

The Number of Young Children Peaked in 1996

(Millions of children under 5 years old)

Top Declining Markets

2003 to 2010 absolute increase (millions)

China -7.71India -3.12Russia -0.77Korea -0.46Ukraine -0.41

Top Growing Markets

2003 to 2010 absolute increase (millions)

Pakistan 2.94Nigeria 2.36Uganda 1.28Egypt 0.92United States 0.59

Copyright © 2004 Global Insight, Inc. 24

The World’s Growing Middle Class

0

200

400

600

800

1994 1997 2000 2003 2006 2009 2012 2015 2018

25

30

35

40

45

Number of Middle Class Households Percent of Total Households

Note: “World” is the aggregate of 95 countries covered in Global Insight’s Global Consumer Model

(Percent of total)(Millions of households)

Copyright © 2004 Global Insight, Inc. 25

0

25

50

75

100

125

2003 2010

The 15 Largest Markets in 2010: Households Earning $10,000 or More

(Millions of households with income > $10,000 (1997$))

Source: Global Insight’s Global Consumer Model (incorporating U.N. and World Bank data)

Copyright © 2004 Global Insight, Inc. 26

Ranking of Markets by Number of Households Earning $10,000 or More

Number of households with income >US $10,000 ( 1997$)

1993 2003 2010 2020

U.S. U.S. U.S. U.S.

Japan Japan Japan China

Germany Germany China Japan

France China Germany Germany

U.K. France France Brazil

Italy U.K. U.K. France

Brazil Italy Brazil U.K.

Russia Brazil Italy Russia

Spain S. Korea Mexico Mexico

S. Korea Mexico Russia ItalySource: Global Insight’s Global Consumer Model (incorporating U.N. and World Bank data)