u.s. court of international trade - u.s. customs …. court of international trade slip op. 16–51...

TRANSCRIPT

U.S. Court of International Trade◆

Slip Op. 16–51

TENSION STEEL INDUSTRIES CO., LTD., Plaintiff, v. UNITED STATES,Defendant.

PUBLIC VERSIONBefore: Leo M. Gordon, JudgeConsol. Court No. 14–00218

[Final determination of sales at less than fair value affirmed in part and remandedin part.]

Dated: May 16, 2016

Kelly A. Slater, Jay Y. Nee, and Edmund W. Sim, Appleton Luff Pte. Ltd of Wash-ington, DC for Plaintiff Tension Steel Industries Co., Ltd.

L. Misha Preheim, Senior Trial Attorney, Commercial Litigation Branch, CivilDivision, U.S. Department of Justice of Washington, DC for Defendant United States.On the brief with him were Benjamin C. Mizer, Principal Deputy Assistant AttorneyGeneral, Jeanne E. Davidson, Director, and Claudia Burke, Assistant Director. Ofcounsel on the brief was David P. Lyons, Attorney, Office of the Chief Counsel forEnforcement and Compliance, U.S. Department of Commerce of Washington, DC.

Robert E. DeFrancesco, III, Alan H. Price, and Adam Teslik, Wiley Rein, LLP ofWashington, DC for Defendant-Intervenor Maverick Tube Corporation.

Jeffrey D. Gerrish, Robert E. Lighthizer, and Jamieson L. Greer, Skadden, Arps,Slate, Meagher & Flom LLP for Defendant-Intervenor United States Steel Corpora-tion.

Roger B. Schagrin, John W. Bohn, and Paul W. Jameson, Schagrin Associates ofWashington, DC for Defendant-Intervenors Boomerang Tube LLC, Energex Tube (aDivision of JMC Steel Group), Tejas Tublar Products, TMK IPSCO, Vallourec Star, L.P.,and Welded Tube USA Inc.

OPINION AND ORDER

Gordon, Judge:

This action involves the U.S. Department of Commerce’s (“Com-merce”) final determination in the less than fair value investigation ofcertain oil country tubular goods (“OCTG”) from Taiwan. See Certain

Oil Country Tubular Goods from Taiwan, 79 Fed. Reg. 41,979 (Dep’tof Commerce July 18, 2014) (final LTFV determ.), as amended, 79Fed. Reg. 46,403 (Dep’t of Commerce Aug. 8, 2014) (“Final Determi-

123

nation”); see also Issues and Decision Memorandum for the FinalDetermination of the Antidumping Duty Investigation of Certain OilCountry Tubular Goods from Taiwan, A-583–850 (Dep’t of CommerceJuly 10, 2014), available at http://enforcement.trade.gov/frn/summary/taiwan/2014–16861–1.pdf (last visited this date) (“Decision

Memorandum”); Antidumping Duty Investigation of Certain OilCountry Tubular Goods from Taiwan: Proprietary Issues (Dep’t ofCommerce July 10, 2014), CD 388 (“Confidential Decision Memoran-

dum”).1

Before the court are the motions for judgment on the agency recordof Consolidated Plaintiffs Tension Steel Industries Co., Ltd. (“Ten-sion”) and Maverick Tube Corporation (“Maverick”). Mem. of Points &Authorities in Supp. of Pl. Tension Steel Industries Co., Ltd.’s R. 56.2Mot. for J. on the Agency R., ECF No. 42 (“Tension Br.”); Consol. Pl.Maverick Tube Corporation’s Mot. for J. on the Agency R., ECF No. 45(“Maverick Br.”); see also Def.’s Opp. to Pls.’ R. 56.2 Mots. for J. on theAgency R., ECF No. 61 (“Def.’s Resp.”); Intervenor-Def. MaverickTube Corporation’s Resp. to Tension’s Mem. in Supp. of its R.56.2 Mot.for J. on the Agency R., ECF No. 65; Resp. of Tension Steel IndustriesCo., Ltd. to Consol. Pls.’ Mots. for J. on the Agency R., ECF No. 66;Mem. in Opp. to Tension Steel Industries Co.’s Mot. for J. on theAgency R. Filed by Def.-Intervenor United States Steel Corporation,ECF No. 67; Reply Br. of Pl. Tension Steel Industries Co., Ltd., ECFNo. 72; Consol. Pl. Maverick Tube Corporation’s Reply Br., ECF No.74 (“Maverick Reply”). Consolidated Plaintiff United States SteelCorporation also moves for judgment on the agency record adoptingMaverick’s arguments by reference. Mot. of Pl. U.S. Steel Corp. for J.on the Agency R. under R. 56.2 1–2, ECF No. 43; see also Reply Br. inSupp. of Pl. United States Steel Corporation’s Mot. for J. on theAgency R. Under R. 56.2. The court has jurisdiction pursuant toSection 516A(a)(2)(B)(i) of the Tariff Act of 1930, as amended, 19U.S.C. § 1516a(a)(2)(B)(i) (2012),2 and 28 U.S.C. § 1581(c) (2012).

For the reasons that follow, the court remands the Final Determi-

nation on the rebate issue Tension raises in its motion, but sustainsthe Final Determination on each of the issues Maverick raises in itsmotion.

I. Standard of Review

The court sustains Commerce’s “determinations, findings, or con-clusions” unless they are “unsupported by substantial evidence on the

1 “CD” refers to a document contained in the confidential administrative record.2 Further citations to the Tariff Act of 1930, as amended, are to the relevant provisions ofTitle 19 of the U.S. Code, 2012 edition.

124 CUSTOMS BULLETIN AND DECISIONS, VOL. 50, NO. 23, JUNE 8, 2016

record, or otherwise not in accordance with law.” 19 U.S.C.§ 1516a(b)(1)(B)(i). More specifically, when reviewing agency deter-minations, findings, or conclusions for substantial evidence, the courtassesses whether the agency action is reasonable given the record asa whole. Nippon Steel Corp. v. United States, 458 F.3d 1345, 1350–51(Fed. Cir. 2006). Substantial evidence has been described as “suchrelevant evidence as a reasonable mind might accept as adequate tosupport a conclusion.” DuPont Teijin Films USA v. United States, 407F.3d 1211, 1215 (Fed. Cir. 2005) (quoting Consol. Edison Co. v. NLRB,305 U.S. 197, 229 (1938)). Substantial evidence has also been de-scribed as “something less than the weight of the evidence, and thepossibility of drawing two inconsistent conclusions from the evidencedoes not prevent an administrative agency’s finding from being sup-ported by substantial evidence.” Consolo v. Fed. Mar. Comm’n, 383U.S. 607, 620 (1966). Fundamentally, though, “substantial evidence”is best understood as a word formula connoting reasonableness re-view. 3 Charles H. Koch, Jr., Administrative Law and Practice

§ 9.24[1] (3d ed. 2016). Therefore, when addressing a substantialevidence issue raised by a party, the court analyzes whether thechallenged agency action “was reasonable given the circumstancespresented by the whole record.” 8–8A, West’s Fed. Forms, NationalCourts § 3.6 (5th ed. 2015).

Separately, the two-step framework provided in Chevron, U.S.A.,

Inc. v. Natural Res. Def. Council, Inc., 467 U.S. 837, 842–45 (1984),governs judicial review of Commerce’s interpretation of the anti-dumping statute. See United States v. Eurodif S.A., 555 U.S. 305, 316(2009) (Commerce’s “interpretation governs in the absence of unam-biguous statutory language to the contrary or unreasonable resolu-tion of language that is ambiguous.”). More specifically, when review-ing Commerce’s interpretation of its regulations, the court must givesubstantial deference to Commerce’s interpretation, Torrington Co. v.

United States, 156 F.3d 1361, 1363–64 (Fed. Cir. 1998), according it“‘controlling weight unless it is plainly erroneous or inconsistent withthe regulation.’” Thomas Jefferson Univ. v. Shalala, 512 U.S. 504,512, (1994) (citations omitted); accord Viraj Group v. United States,476 F.3d 1349, 1355 (Fed. Cir. 2007).

II. Discussion

A. Tension’s Rebate Issue

Tension challenges the lawfulness of Commerce’s refusal to acceptsome of Tension’s proposed rebate adjustments to certain home mar-ket sales. The statute directs Commerce to calculate normal valueusing “the price at which the foreign like product is first sold . . . for

125 CUSTOMS BULLETIN AND DECISIONS, VOL. 50, NO. 23, JUNE 8, 2016

consumption in the exporting country.” 19 U.S.C. § 1677b(a)(1)(B)(i).Commerce’s regulations explain that the price used for normal valuewill be “a price that is net of any price adjustment . . . that isreasonably attributable to the . . . foreign like product.” 19 C.F.R.§ 351.401(c) (2015). The regulations define a “price adjustment” as“any change in the price charged for subject merchandise or theforeign like product, such as discounts, rebates and post-sale priceadjustments, that are reflected in the purchaser’s net outlay.” 19C.F.R. § 351.102(b)(38) (emphasis added).

Commerce has developed a practice of rejecting claimed rebateadjustments when a respondent’s customers lacked knowledge of theterms and conditions of the rebates at or before the time of sale. See,

e.g., Issues and Decision Memorandum for the Antidumping DutyAdministrative Reviews of Ball Bearings and Parts Thereof fromFrance, Germany, Italy, Japan and the United Kingdom 63–64 (Dep’tof Commerce July 14, 2006), available at http://enforcement.trade.gov/ frn / summary / multiple / E6–111231.pdf (last visited this date) (“Itis [Commerce]’s practice to adjust normal value to account for rebateswhen the terms and conditions of the rebate are known to the cus-tomer prior to the sale and the claimed rebates are customer-specific.”); Issues and Decision Memorandum for the Final Results ofthe Administrative Review of the Antidumping Duty Order onCanned Pineapple Fruit from Thailand 3–5 (Dep’t of Commerce Dec.7, 2006), available at http://enforcement.trade.gov / frn / summary /thailand/ E6–20779–1.pdf (last visited this date) (“[W]here a priceadjustment made after the fact lowers a respondent’s dumping mar-gin, [Commerce] will closely examine the circumstances surroundingthe adjustment to determine whether it was a bona fide adjustmentmade in the ordinary course of business.”).

Citing this practice, Commerce rejected adjustments for rebatepayments Tension made pursuant to sales contracts that did notspecifically include a rebate clause. Decision Memorandum at 11.According to Commerce the only “legitimate rebates” Tension prof-fered were those that customers knew about at or before the time ofthe sale. Id.

Tension argues that Commerce’s practice of rejecting rebate adjust-ments when it is not satisfied that customers were aware of the termsand conditions of the rebate at the time of the sale violates a recentdecision of the court, Papierfabrik August Koehler AG v. United

States, 38 CIT ___, 971 F. Supp. 2d 1246 (2014), in which the courtheld that such a practice contravenes the plain language of Com-merce’s regulations. Tension Br. at 1–18. The court agrees. In Papier-

fabrik, the court explained that the plain language of Commerce’s

126 CUSTOMS BULLETIN AND DECISIONS, VOL. 50, NO. 23, JUNE 8, 2016

regulations require it to calculate normal value “net of any priceadjustment . . . that is reasonably attributable to the . . . foreign likeproduct” that “are reflected in the purchaser’s net outlay.” Id. at ___,971 F. Supp. 2d at 1252–53 (quoting 19 C.F.R. §§ 351.102(b)(38),351.401(c)) (emphasis in original). Consequently, Commerce’s prac-tice of rejecting rebates even though they are “reasonably attribut-able to the . . . foreign like product” and “are reflected in the purchas-er’s net outlay” violates the regulation. Id. at ___, 971 F. Supp. 2d at1252–53; see 19 C.F.R. §§ 351.102(b)(38), 351.401(c).

Commerce noted that Papierfabrik “is not final.” Decision Memo-

randum at 10. Defendant, for its part, also urges that court disregardPapierfabrik, and argues that Commerce’s rebate practice is consis-tent with the regulation. See Def.’s Resp. at 24–32. Papierfabrik isnow final, and rather than appeal, Commerce chose to amend theregulation instead. Modification of Regulations Regarding Price Ad-

justments in Antidumping Duty Proceedings, 79 Fed. Reg. 78,742(Dep’t of Commerce Dec. 31, 2014) (proposed rule and request forcomment).

As Papierfabrik noted, “[t]he regulatory provisions unambiguouslyrequire that rebates and other post-sale downward adjustments inthe price charged for the foreign like product that are reflected in thepurchaser’s net outlay be reflected in the starting price Commerceuses for determining normal value.” Papierfabrik, 38 CIT at ___, 971F. Supp. 2d at 1257. The court therefore remands this issue to Com-merce to accept Tension’s rebate adjustments. Id.

B. Maverick Issues

1. VAT

In the final determination Commerce rejected Maverick’s argumentthat Commerce should deny respondent Chung Hung Steel Corp.(“CHS”) a value added tax (“VAT”) adjustment:

We disagree with the petitioners’ argument that [Commerce]should include in the reported costs the amount of any VAT thatwas not refunded. Section 773(e) of the Act provides that, forpurposes of calculating constructed value, “the cost of materialsshall be determined without regard to any internal tax in theexporting country imposed on such materials or their dispositionwhich are remitted or refunded upon exportation of the subjectmerchandise produced from such materials.” The purpose of thisprovision is to ensure an appropriate comparison between ex-port sales of subject merchandise, upon which no VAT taxes arecharged, and the constructed value of that merchandise, when

127 CUSTOMS BULLETIN AND DECISIONS, VOL. 50, NO. 23, JUNE 8, 2016

any VAT costs incurred in purchasing the inputs are remitted orrefunded upon exportation. CHS reported that a VAT of 5 per-cent is levied on purchases of inputs and home market sales offinished goods, while export sales are not subject to VAT. CHSfurther stated that during the [period of investigation], the in-put VAT paid on purchased inputs was largely offset by theoutput VAT collected from home market sales of finished goods.CHS stated that the balance is completely refunded by the taxauthority.

CHS pays VAT on purchases of goods and services and collectsVAT on sales to its customers. While CHS does not collect VATon export sales, it is granted a credit to offset the appropriateVAT. In OCTG Mexico, [Commerce] explained that, “[e]ven if theamount ‘not exacted’ in a given month were to be less than theamount paid as VAT to suppliers in that month, the amountsassociated with VAT paid on inputs to exported merchandise arestill ‘pardoned.’” [Commerce] only requires that a respondentdemonstrate that it is entitled to a VAT refund on exports andcan offset VAT paid on domestic market sales because there aretiming differences between the purchases of raw materials andthe subsequent collection of VAT from the customer. Moreover,CHS does not have a domestic market for OCTG and we arerelying on Canadian sales for NV, which would also be subject tothe export refund.

Decision Memorandum at 18–19 (footnotes omitted) (quoting Issuesand Decision Memorandum for the 1998–1999 Administrative Re-view of Oil Country Tubular Goods from Mexico, at Hysla cmt. 2(Dep’t of Commerce Mar. 21, 2001), available at http://enforcement.trade.gov/frn/summary/mexico/01–6913–1.txt (last vis-ited this date) (“OCTG Mexico”). In its opening brief, Maverick ac-knowledges Commerce’s existing VAT practice pursuant to which it“requires only that a respondent demonstrate that it (1) is entitled toa VAT refund on exports, and (2) can offset VAT paid on domesticmarket sales because there are timing differences between the pur-chases of raw materials and the subsequent collection of VAT from thecustomer.” Maverick Br. at 25–26 (citing Decision Memorandum at19).

So to be clear, “to account for the timing differences between rawmaterial purchases and subsequent VAT recoupment, Commerce re-quires only that a respondent demonstrate entitlement to a VATrefund on exports. Commerce does not require that a respondent

128 CUSTOMS BULLETIN AND DECISIONS, VOL. 50, NO. 23, JUNE 8, 2016

document that every VAT payment was refunded during the period ofinvestigation or outside the period of investigation.” Def.’s Resp. at21–22 (citing OCTG Mexico at Hysla cmt. 2) (emphasis in original).

Maverick highlights a difference between the amount of VAT paidon inputs during the period of investigation (“POI”) and the amountof VAT collected on sales and refunded on exports. Maverick Br. at 25(citing CHS’s Supplemental Section D Questionnaire Response at Ex.3SD-8 (Dep’t of Commerce Jan. 15, 2014), CD 206–07). As explainedabove, however, under Commerce’s VAT practice such a difference isunremarkable and to be expected because of timing differences be-tween raw material purchases and the subsequent collection of VATfrom customers. Decision Memorandum at 18–19. For Maverickthough, “CHS’s historical treatment of VAT appears incongruent withCommerce’s allocation of it for the final determination,” leading Mav-erick to conclude that Commerce’s handling of VAT “was unsupportedby substantial evidence and otherwise not in accordance with thelaw.” Maverick Br. at 26.

It is difficult to identify merit in a substantial evidence challenge toCommerce’s factual findings on the VAT issue (e.g., the existence ofthe Taiwan VAT regime, how CHS accounted for VAT within its booksand records). It is also difficult to identify merit in a substantialevidence challenge to Commerce’s application of its VAT practice tothose findings (the reasonableness of Commerce’s application of itsVAT practice to the facts of this administrative record). CHS reportedthat Taiwan levies a five percent VAT on input purchases but exemptsexport sales from VAT. Decision Memorandum at 18. Maverick doesnot appear to challenge the Taiwan VAT regime. Maverick, for ex-ample, did not proffer to Commerce any affidavits, declarations, orother information from Taiwanese tax experts analyzing the TaiwanVAT regime. Commerce found that under that regime CHS was en-titled to a credit to offset any VAT applied on input purchases used toproduce subject merchandise that was exported. Id. at 18–19. Mav-erick did not proffer any information from Taiwanese tax experts thatCHS was somehow not entitled to such a credit. CHS explained, andCommerce accepted, that during the POI, the VAT on input purchasesfor export sales was “largely offset” by the output VAT collected fromhome market sales of finished goods. Id. at 18. The remainder, CHSreported, and Commerce accepted, “is completely refunded by the taxauthority.” Id. Maverick believes this is unlikely, but again, Maverickdid not proffer, for example, an opinion letter from a Taiwanese taxexpert that confirmed Maverick’s suspicions. Defendant explains thatCommerce, consistent with its practice and in recognition of timingdifferences between purchases of raw materials and the subsequent

129 CUSTOMS BULLETIN AND DECISIONS, VOL. 50, NO. 23, JUNE 8, 2016

collection of VAT from customers, did not limit CHS’s VAT refunds tothose offsets that occurred during the POI as Maverick would havepreferred. Def.’s Resp. at 21–23. In other words, Commerce did notrequire anything more than evidence that CHS was entitled underTaiwanese law to VAT refunds for export sales. Id. As a result,Commerce used CHS’s books and records, which excluded VAT thathappened not to have been refunded during the POI. Decision Memo-

randum at 18–19. The court cannot fault this determination as un-reasonable (unsupported by substantial evidence).

Beyond substantial evidence issues, Maverick also vaguely sug-gests that Commerce’s VAT adjustment is “otherwise contrary to law.”Maverick Br. at 25–26. Maverick, however, does not frame that “legal”argument against an applicable standard of review. For example,Maverick chose not to analyze the legality of Commerce’s VAT prac-tice within the Chevron framework. The court therefore declines toentertain Maverick’s asserted but unanalyzed “legal” challenge toCommerce’s VAT practice. See Carducci v. Regan, 714 F.2d 171, 177(D.C. Cir. 1983) (“The premise of our adversarial system is thatappellate courts do not sit as self-directed boards of legal inquiry andresearch, but essentially as arbiters of legal questions presented andargued by the parties before them.”).

2. Date of Sale

Commerce used the date of shipment as the date of sale for CHS.Decision Memorandum at 13–14; Confidential Decision Memoran-

dum at 12. Maverick challenges this determination, arguing thatCommerce misapplied its date of sale regulation, 19 C.F.R.§ 351.401(i). Maverick Br. at 26–27; Maverick Reply at 12–14.

Pursuant to its regulation, Commerce has a rebuttable presump-tion in favor of invoice date for the date of sale. 19 C.F.R. § 351.401(i).Commerce “may,” however, “use a date other than the date of invoiceif [Commerce] is satisfied that a different date better reflects the dateon which the exporter or producer establishes the material terms ofsale.” Id. ; see generally Yieh Phui Enter. Co. v. United States , 35 CIT___, ___, 791 F. Supp. 2d 1319, 1322–24 (2011) (describing in detailCommerce’s date of sale regulation).

Commerce found that CHS has the following sales process for itsUnited States and comparison market sales:

• First, CHS and its customers entered into sales contracts pre-liminarily specifying the terms of sale—price, quantity, paymentterms, and delivery terms. The material terms of sale could bealtered during the period of time following these sales contracts.

130 CUSTOMS BULLETIN AND DECISIONS, VOL. 50, NO. 23, JUNE 8, 2016

CHS documented one example of the material terms changingbetween the preliminary sales contract and the date of ship-ment.

• Second, CHS would ship to its customers. Commerce verifiedthat changes could be made to the material terms of sale up tothe date of shipment.

• Third, at some time after date of shipment, CHS would issue aninvoice.

Decision Memorandum at 13–14 (citing record sources). Commercedetermined that the material terms of sale were not fixed when CHSconcluded sales contracts with its customers. Id. at 13. Rather, Com-merce found that the material terms of sale could change—and in atleast one instance did change—during the period between the con-tract date and the date of shipment. Id. CHS issued invoices to itscustomers only after the date of shipment. Id. at 13–14. Commercetherefore determined that the material terms of sale were establishedon the date of shipment, not the subsequent date of invoice. See id. at13–14; see also Confidential Decision Memorandum at 12.

This determination followed Commerce’s practice for cases in whichthe date of shipment precedes the date of invoice. Decision Memoran-

dum at 14 (citing Certain Polyester Stable Fiber from Korea, 74 Fed.Reg. 27,281, 27,283 (Dep’t of Commerce June 9, 2009) (prelim. re-sults) unchanged in 74 Fed. Reg. 65,517 (Dep’t of Commerce Dec. 10,2009) (final results)); but see U.S. Steel Corp. v. United States, 37 CIT___, ___, 953 F. Supp. 2d 1332, 1340 (2013) (noting in dicta thatrelying on administrative practice alone—of using shipment datewhen it precedes invoice date—“would seem not to be enough tosatisfy the standard that the regulation, written by Commerce, pro-vides”).

Commerce explained that the record evidence here demonstratedthat the material terms of CHS’s sales were subject to change untilthe date of shipment, which preceded the date of invoice. Decision

Memorandum at 13–14. There is, of course, a baked in practical logicto this practice. When a party ships its product to a customer, it isreasonable to assume that the material terms of the sale have beenestablished. See, e.g., Certain Hot-Rolled Flat-Rolled Carbon-Quality

Steel Products from Brazil, 64 Fed. Reg. 38,756, 38,768 (Dep’t ofCommerce July 19, 1999) (final determ.) ([“Commerce”] does notconsider dates subsequent to the date of shipment from the factory asappropriate for date of sale.”); Issues and Decisions Memorandum forthe Administrative Review of Stainless Steel Bar from Japan, cmt. 1

131 CUSTOMS BULLETIN AND DECISIONS, VOL. 50, NO. 23, JUNE 8, 2016

(Dep’t of Commerce Mar. 14, 2000), available at http://enforcement.trade.gov / frn / summary / japan / 00–6264–1.txt (lastvisited this date) (“In keeping with [Commerce’s] practice, the date ofsale cannot occur after the date of shipment.”). Here, once the mer-chandise is shipped, the terms are set, and there are no changes inthose terms when CHS subsequently issues the invoice. And indeed,Maverick has not identified any such changes on this record. Thecourt therefore sustains as reasonable Commerce’s use of shipmentdate as the date of sale for CHS.

3. Treatment of Non-Prime Pipe

In the final determination Commerce valued CHS’s non-prime pipeat the net recovery price rather than the full cost incurred to producethe product. Maverick argues that Commerce should have rejectedthis offset because the non-prime pipe is a by-product of OCTG, andCHS’s reported costs already account for scrap sales at standard cost.Maverick Br. at 23–25.

The statute directs Commerce to use the normal books and recordsof the exporter or producer if such records are kept in accordance withGenerally Accepted Accounting Principles (“GAAP”) and reasonablyreflect the costs associated with the production and sale of subjectmerchandise. 19 U.S.C. § 1677b(f)(1)(A). When Commerce encountersdowngraded pipe, it evaluates the extent to which the downgradedproduct differs from subject merchandise. Decision Memorandum at16. A downgraded product so different that “it no longer belongs to thesame group and cannot be used for the same applications” typicallyindicates the diminishment of market value “to a point where itsproduction costs cannot be recovered.” Id.; see also Issues and Deci-sion Memorandum for the Antidumping Administrative Review ofCircular Welded Carbon Steel Pipes and Tubes from Thailand,A-549–502, at 16–18 (Dep’t of Commerce Oct. 3, 2012), available at

http://enforcement.trade.gov / frn / summary / thailand /2012–25040–1.pdf (last visited this date). Commerce’s stated practiceis to determine whether downgraded products may fulfill the sameapplications as subject merchandise rather than attempt to parse therelative values and qualities between grades. Decision Memorandum

at 16. If the downgraded products cannot fulfill the same applicationsas the subject merchandise, Commerce will grant an offset to reflectthe market value of the downgraded merchandise.

In accordance with GAAP, Commerce values by-products at theirmarket price to avoid overstating inventory accounts on the balancesheet. Id. Indeed, pursuant to the “lower cost or market—LCM”practice, GAAP prohibits companies from valuing products held in

132 CUSTOMS BULLETIN AND DECISIONS, VOL. 50, NO. 23, JUNE 8, 2016

inventory at an amount that exceeds their market price. Id. The courthas affirmed Commerce’s valuation of by-products at the net recoveryprice. E.I. DuPont De Nemours & Co. v. United States, 20 CIT 373,377–78, 932 F. Supp. 296, 300–01 (1996) (recognizing that “assigning[recycled] pellets the cost of virgin chips would overstate the actualcosts of PET film production”).

Commerce preliminarily disallowed CHS’s adjustment for non-prime pipe and thus did not account for the field “Adjustment due toNon-Prime Pipes” in CHS’s reported costs. See Decision Memoran-

dum at 14. However, in light of further development of the record andon-site verification of CHS, Commerce realized that it had not givenCHS “credit for the value of the non-prime pipes as they are treatedin their normal records.” CHS Cost Verification Report at 3 (Dep’t ofCommerce Apr. 23, 2014), CD 380. In its normal books and records,CHS valued this non-prime pipe using its market price. Decision

Memorandum at 16. Non-prime pipe may be sold for structural ap-plication, such as in construction and highway gantry, but is not soldas OCTG. Id. (citing CHS Section D Response at D-5 (Dep’t of Com-merce Oct. 28, 2013), CD 49–50 (“CHS Sec. D. Resp.”)). Given thesefacts and its practice with regard to non-prime by-products, Com-merce valued the down-graded pipe at net recovery price rather thanthe full cost incurred to produce the product. Id. at 15–17. Commerceexplained that setting the cost of downgraded pipe at the net recoveryprice of the product is consistent with GAAP, which, to avoid theoverstatement of inventory accounts on the balance sheet, does notallow companies to value products held in inventory at an amountgreater than their market price. Id. Thus, Commerce found that CHSis not permitted under GAAP to value the non-prime pipe at the costof prime OCTG. Id.

Here, CHS’s non-prime pipe is properly classified as a by-product ofthe production of OCTG. In pipe making, there is no simultaneousproduction process up to a split point, so there are no co-products. See

Decision Memorandum at 15. Pipes are made sequentially on a pro-duction line, and costs and production activities are generally iden-tifiable to individual products. Id. At the end of the production line,the pipes are evaluated for quality to determine if they are fit for useas OCTG or are non-prime. Id. Commerce determined that the non-prime pipe is a by-product of OCTG production, a finding Maverickdoes not challenge in its brief.

Valuing the cost of non-prime pipe at the net recovery price of theproduct is consistent with GAAP. Decision Memorandum at 16. Asnoted above, to avoid the overstatement of inventory accounts on a

133 CUSTOMS BULLETIN AND DECISIONS, VOL. 50, NO. 23, JUNE 8, 2016

company’s balance sheet, GAAP does not allow companies to valueproducts held in inventory at an amount greater than their marketprice. See id. Thus, CHS is not allowed under GAAP to value thenon-prime pipe at the cost of prime OCTG, and CHS in its normalrecords does not do so. See id. Rather, CHS assigns a cost to non-prime pipe equal to the net market price. See id. Commerce found inthe final determination that assigning costs “based on market valueis a well-established practice in cost accounting and accepted underGAAP.” Id. at 17. The practice of assigning costs based on marketvalue has also been upheld by the U.S. Court of Appeals for theFederal Circuit. See PSC VSMPO-Avisma Corp. v. United States, 688F.3d 751, 764–65 (Fed. Cir. 2012). Commerce thus reasonably usedthe net recovery price to value the non-prime pipe and granted CHSan offset to its reported costs in that amount to account for theby-product.

Maverick argues that Commerce’s practice “supports a finding thatCHS’s non-prime pipe is a by-product.” Maverick Br. at 23. Specifi-cally, Maverick cites two cases in which Commerce treated lower-grade products generated in producing the subject merchandise asby-products rather than “joint products” (that is, co-products). Mav-erick Br. at 22–23 (citing Issues and Decision Memorandum for theFinal Results and Rescission, in Part, of the Antidumping Duty Ad-ministrative Review of Fresh Garlic from the People’s Republic ofChina, A-570–831, at 30–32 (Dep’t of Commerce June 10, 2013),available at http:// enforcement.trade.gov / frn / summary / prc/2013–14329–1.pdf (last visited this date); Issues and Decision Memo-randum for the Antidumping Duty Investigation of Certain OrangeJuice from Brazil, A-351–840, at 34–42 (Dep’t of Commerce Jan. 13,2006), available at http://enforcement.trade.gov/frn/summary/brazil/E6–333–1.pdf (last visited this date) (“Orange Juice from Brazil”)).Maverick’s argument is confusing because it advocates the very de-termination Commerce reached—that CHS’s non-prime pipe is a by-product—but leaves unexplained how this relates to the offset fornon-prime pipe. See Maverick Br. at 22–24. See also Decision Memo-

randum at 16 (explaining that “[i]n its normal books and records,CHS treats non-prime pipe as by-products” and then uses the value inthose books and records to value the non-prime pipe). Neither casecited by Maverick conflicts with Commerce’s practice of valuing down-graded product at the net recovery price. And in Orange Juice from

Brazil Commerce allowed the respondents’ by-product revenue offsetfor orange juice by-products. Orange Juice from Brazil at 39–42.

Maverick argues that Commerce’s non-prime pipe offset is improperbecause CHS’s cost database, without the “Adjustment Due to Non-

134 CUSTOMS BULLETIN AND DECISIONS, VOL. 50, NO. 23, JUNE 8, 2016

Prime Pipes” field, represents CHS’s cost of manufacturing in itsnormal records and already includes the offset for scrap and non-prime pipes. See Maverick Br. at 24. Defendant notes that “[t]hefactual record refutes Maverick’s assertion,” Def.’s Resp. at 20, andthe court agrees. Commerce found that “CHS did not include in thecost buildups the normal offset for non-prime pipe, thus withoutadjusting for this offset, costs would be overstated.” Decision Memo-

randum at 17; see CHS Sec. D. Resp. at D-42. CHS’s Section DResponse states that the cost of manufacturing that it reported toCommerce uses “only the production quality of prime quality to ab-sorb and share the aggregate costs.” CHS Sec. D. Resp. at D-43. CHSthen explained that the adjustment reflected in Field 7.2 is necessarybecause non-prime products should be included in the pool of produc-tion volume to share and absorb part of the aggregated costs. Id.

Commerce found in the final determination that CHS’s reported costsexcluding the adjustment for non-prime pipe did not account for theoffset for non-prime pipe normally recorded in their books and re-cords. See Decision Memorandum at 17.

More broadly, Maverick argues that Commerce’s “shift in decision”between its preliminary and final determinations fails “to provide arational connection to the conclusion drawn.” Maverick Br. at 24.Commerce fully explained its determination to value downgradednon-prime pipe at the net recovery cost. See Decision Memorandum at15–16. As described above, this determination followed Commerce’spractice with regard to downgraded product that is not suitable forthe same applications as subject merchandise. Accordingly, it is areasonable determination that the court must sustain.

4. Rebates

Maverick argues that Commerce unreasonably declined to rejectevery one of Tension’s claimed rebate adjustments. Maverick claimsthat the “Price Rebate Statements” Tension offered in support of itsproposed offsets were created on a confidential date well after thedate Tension claimed it began offering rebates to its customers. Mav-erick Br. at 20–21. To Maverick, this discrepancy indicates that Ten-sion provided inadequate supporting documentation and that Ten-sion’s price rebate statements did not connect to Tension’s sales. See

Maverick Br. at 19–21.The court is not persuaded. In considering Tension’s requested

rebate adjustments, Commerce identified certain Tension sales con-tracts with rebate clauses stipulating that Tension would pay a re-bate conditioned upon Tension itself receiving a rebate. Confidential

Decision Memorandum at 10–11. Commerce requested, and Tension

135 CUSTOMS BULLETIN AND DECISIONS, VOL. 50, NO. 23, JUNE 8, 2016

provided, copies of every Price Rebate Statement applicable to OCTGfor the POI, which specify the particular sales contracts for whichTension granted rebates. Commerce verified those rebate amountsduring its on-site verification. Id. Commerce found that Tension’srequested rebates were attributable to certain sales made during thePOI. Id. at 10–11; see Decision Memorandum at 11–12.

The only issue Maverick identifies with Tension’s Price RebateStatements to substantiate its claim is the apparent timing discrep-ancy. Maverick Br. at 17–22. As explained, however, Tension’s PriceRebate Statements detail the link between particular sales contractsand rebates Tension paid in accordance with those contracts. Confi-

dential Decision Memorandum at 10–11. When Commerce asked Ten-sion about the apparent timing discrepancy, Tension explained thatthe Price Rebate Statements may include rebates paid on sales madein prior years. See id. at 11; Tension Sales Verification Report at12–13 (Dep’t of Commerce Apr. 4, 2013), CD 378 (“Tension Verifica-tion”). Maverick may doubt the reliability of Tension’s explanationand documentation, but Commerce was able to verify all of Tension’sproposed rebate amounts while on-site in Taiwan. Confidential Deci-

sion Memorandum at 10–11. The court therefore sustains Com-merce’s reasonable decision to grant Tension’s proposed rebate ad-justments.

5. Affiliation

Maverick challenges Commerce’s conclusion that Tension and itssupplier, Company A, were not affiliated by virtue of a close supplierrelationship.

The statute defines “affiliated persons” in relevant part as “[a]nyperson who controls any other person and such other person.” 19U.S.C. § 1677(33)(G). Affiliation requires a finding of “control,” whichthe statute defines as “legally or operationally in a position to exerciserestraint or direction over the other person.” 19 U.S.C. § 1677(33).Commerce’s regulations specify that “control” means a “relationship[that] has the potential to impact decisions concerning the produc-tion, pricing, or cost of the subject merchandise.” 19 C.F.R.§ 351.102(b)(3).

In determining whether control exists, Commerce considers, amongother factors, “close supplier relationships.” Id.; see also Statement ofAdministrative Action, H.R. Doc. No. 103–316, vol. 1 at 838 (1994)(control sufficient to establish affiliation may be demonstrated “forexample, through . . . close supplier relationships”) (“SAA”). A closesupplier relationship is a control relationship when “the supplier or

136 CUSTOMS BULLETIN AND DECISIONS, VOL. 50, NO. 23, JUNE 8, 2016

buyer becomes reliant upon the other.” SAA at 838 (emphasis added).Commerce has a two-part analysis to determine whether a closesupplier relationship is a control relationship. Commerce first con-siders whether a party has demonstrated that “the relationship issignificant and could not be easily replaced”—that the buyer or sup-plier has become reliant on the other. TIJID, Inc. v. United States, 29CIT 307, 321, 366 F. Supp. 2d 1286, 1299 (2005) (affirming Com-merce’s determination that supplier’s sale of 100 percent of itscandles to TIJID did not itself establish a close supplier relationship).“Only if Commerce determines that there is reliance does it evaluatewhether the relationship of reliance has the potential to impact de-cisions relating to subject merchandise.” Id.

Maverick argues that Commerce erred in failing to find that Ten-sion is not reliant on its supplier—Company A—and therefore notaffiliated through a “close supplier” relationship. Maverick Br. at 4–5.This issue was briefed and argued extensively below. See Decision

Memorandum at 3–6; Confidential Decision Memorandum at 2–8.Maverick attempted without success to persuade Commerce as afactual matter that Company A controlled Tension because Tensionsourced a large proportion of its hot-rolled coil during the POI fromCompany A, and Tension used a factoring arrangement involving debtfinancing for a small fraction of its purchases from Company A.Maverick also tried to argue that the facts of this case were “nearlyidentical” to Stainless Steel Wire Rod from Korea, 63 Fed. Reg. 40,404,40,410 (Dep’t Commerce July 29, 1998) (final results) (“SSWR from

Korea”) in which Commerce collapsed entities based on a close sup-plier relationship.

Maverick repeats these same arguments here. Maverick Br. at5–13. As for the factoring arrangement, Commerce determined it wasinconsequential, Confidential Decision Memorandum at 8, a reason-able finding that the court cannot upend.3 Commerce also distin-guished the facts of SSWR from Korea, explaining that “in SSWR

from Korea, we found that ‘Dongbang has not obtained suitable blackcoil from alternative sources but continues to exclusively rely uponPOSCO/Changwon for this input,’” whereas “in this investigation,Tension did find and bought suitable hot-rolled steel coil from alter-native suppliers.” Decision Memorandum at 5. Commerce thereforereasonably concluded that the facts of SSWR from Korea were not“nearly identical” to the facts of this case.

3 Commerce explained that the program accounted for just [[ ]] of the POI and only [[ ]] ofthe [[ ]] line items for short-term New Taiwan Dollar borrowings in the general ledger [[

]]. Confidential Decision Memorandum at 8. Commerce determined that the [[ ]] ofthe arrangement did not evince control of Tension by Company A. Id.

137 CUSTOMS BULLETIN AND DECISIONS, VOL. 50, NO. 23, JUNE 8, 2016

Maverick also claimed that Tension’s sales contracts barred Tensionfrom sourcing from other suppliers. Confidential Decision Memoran-

dum at 3, 7. Maverick repeats this argument again before the court.Maverick Br. at 8. Commerce rejected the argument, explaining thatCommerce found nothing on the record or during its on-site verifica-tions in Taiwan to indicate that the agreements precluded Tensionfrom sourcing from other suppliers outside of the People’s Republic ofChina. Confidential Decision Memorandum at 7; see also TensionVerification at 3. Maverick does not address Commerce’s analysis onthis point. See Maverick Br. at 8; Maverick Reply at 2–8.

On the specific issue of Company A supplying Tension’s inputs,Commerce found that Company A did not control Tension through aclose supplier relationship. Decision Memorandum at 5–6; Confiden-

tial Decision Memorandumat 7–8. Commerce acknowledged that Ten-sion purchased a large share of its coil from Company A during thePOI, but Commerce found that “Tension could, and did, look to otherunaffiliated suppliers of the input.” Decision Memorandum at 5 (cit-ing Tension Supplemental Response, exs. 1–2 (Dep’t of CommerceDec. 6, 2013), CD 130–31). Commerce reasoned that Tension’s pur-chases from Company A resulted not from compulsion, but soundbusiness choices. Confidential Decision Memorandum at 7. Specifi-cally, (1) Company A could deliver in a more timely fashion thanforeign suppliers and (2) Tension observed that “the quality of the coilis good.” Tension Verification at 3. Commerce determined that, al-though these advantages led Tension to purchase a large share of itscoil during the POI from Company A, they did not establish theabsence of commercially viable alternative suppliers or that Tensionwould fail if forced to look to other suppliers. Confidential Decision

Memorandum at 7.Maverick emphasizes that Company A has a strong position in the

market as a supplier of inputs for OCTG. Maverick argues that “it issimply not possible to quickly replace this supplier.” Maverick Replyat 3. Perhaps. The administrative record does not reveal with cer-tainty what would happen if Company A decided to terminate thesupply of inputs to Tension. Maybe Tension would fail immediately;maybe Tension would pivot quickly, and do what was necessary tosurvive. Maverick infers the former. Commerce inferred the latter.This administrative record does not mandate one and only one infer-ence. It may not be optimal in the short term for Tension to replaceCompany A, but Commerce’s inference that Tension’s replacement ofCompany A would not result in its failure is not unreasonable.

The court agrees with Defendant that “consistent with its regula-tions and past practice, Commerce determined that the record

138 CUSTOMS BULLETIN AND DECISIONS, VOL. 50, NO. 23, JUNE 8, 2016

evidence—in particular, Company A’s role as Tension’s predominatecoil supplier and a seldom-used factoring arrangement— did notsuffice to affiliate Tension and Company A.” Def.’s Resp. at 10. Thecourt therefore sustains Commerce’s determination not to treat Ten-sion and Company A as affiliated.

6. Collapsing

Maverick argues that Commerce should have collapsed Tensionwith Company A’s parent, Company B. The collapsing result advo-cated by Maverick depended upon a finding of affiliation betweenTension and Company A. See Maverick Br. at 13. Commerce, however,determined that Tension and Company A were not affiliated, a resultthe court has sustained above. Defendant explains that if Tension isnot affiliated with Company A, Commerce could not collapse Tensionwith Company A’s parent, Company B. Def.’s Resp. at 10–12. Defen-dant also notes that “Maverick does not argue that its collapsingargument could survive without affiliation between Tension and Com-pany A.” Id. at 12 (citing Maverick Br. at 13–17). The court agreeswith Defendant and therefore sustains Commerce’s decision to notcollapse Tension with Company A’s parent, Company B.

III. Conclusion

In accordance with the foregoing, it is herebyORDERED that Maverick’s and United States Steel Corporation’s

respective Motions for Judgment on the Agency Record are denied; itis further

ORDERED that the Final Determination is sustained as to Com-merce’s treatment of VAT, date of sale, non-prime pipe, affiliation,collapsing, and Commerce’s decision to accept certain Tension rebateadjustments; it is further

ORDERED that Tension’s Motion for Judgment on the AgencyRecord is granted; it is further

ORDERED that this action is remanded to Commerce to grantTension’s remaining proposed rebate adjustments; it is further

ORDERED that Commerce shall file its remand results on orbefore July 15, 2016; and it is further

ORDERED that, if applicable, the parties shall file a proposedscheduling order with page/word limits for comments on the remandresults no later than seven days after Commerce files its remandresults with the court.Dated: May 16, 2016

New York, New York/s/ Leo M. Gordon

JUDGE LEO M. GORDON

139 CUSTOMS BULLETIN AND DECISIONS, VOL. 50, NO. 23, JUNE 8, 2016

Slip Op. 16–52

CHEMTALL, INC., Plaintiff, v. UNITED STATES, Defendant.

Before: Leo M. Gordon, JudgeCourt No. 12–00079

[Summary judgment denied for Plaintiff; summary judgment granted for Defen-dant.]

Dated: May 25, 2016

Robert L. LaFrankie, Hughes Hubbard & Reed LLP of Washington, DC for PlaintiffChemtall, Inc.

Eric E. Laufgraben, Trial Attorney, Commercial Litigation Branch, Civil Division,U.S. Department of Justice of Washington, DC for Defendant United States. On thebrief with him were Joyce R. Branda, Acting Assistant Attorney General, Jeanne E.

Davidson, Director, Claudia Burke, Assistant Director. Of counsel on the brief wasPaula S. Smith Attorney, Office of Assistant Chief Counsel for International TradeLitigation, U.S. Customs and Border Protection of New York, NY.

OPINION

Gordon, Judge:

Before the court are cross-motions for summary judgment. See Pl.’sMot. for Summ. J. and Pl.’s Statement of Material Facts Not inDispute, ECF No. 32 (“Pl.’s Br.”); Def.’s Mot. for Summ. J., ECF No. 34(“Def.’s Br.”); see also Pl.’s Resp. to Def.’s Mot. for Summ. J., ECF No.36 (“Pl.’s Resp.”); Def.’s Resp. and Objections to Pl.’s Statement ofMaterial Facts, ECF No. 37 (“Def.’s Resp.”); Def.’s Reply in Supp. ofMot. for Summ. J., ECF No. 40 (Def.’s Reply). Plaintiff Chemtall, Inc.challenges the decision of Defendant U.S. Customs and Border Pro-tection (“Customs”) denying Chemtall’s protests of Customs’ classifi-cation of the imported “acrylamide tertiary butyl sulfonic acid”(“ATBS”) within the Harmonized Tariff Schedule of the United States(“HTSUS”). Customs classified the merchandise as “Carboxyamide-function compounds; amide-function compounds of carbonic acid: Acy-clic amides (including acyclic carbamates) and their derivatives; saltsthereof: Other: Other” under HTSUS subheading 2924.19.80, whichcarries a 6.5% duty rate. Plaintiff claims that the merchandise isproperly classified as “Carboxyamide-function compounds; amide-function compounds of carbonic acid: Acyclic amides (including acycliccarbamates) and their derivatives; salts thereof: Other: Amides: Acry-lamide” under HTSUS subheading 2924.19.11, which carries a 3.7%duty rate. The court has jurisdiction pursuant to 28 U.S.C. § 1581(a)(2012). For the reasons set forth below, Defendant’s motion for sum-mary judgment is granted, and Plaintiff’s motion is denied.

140 CUSTOMS BULLETIN AND DECISIONS, VOL. 50, NO. 23, JUNE 8, 2016

I. Undisputed Facts

The following facts are not in dispute. Plaintiff is the importer ofrecord of the subject merchandise. Compl. ¶ 2; Ans. ¶ 2. The mer-chandise at issue is acrylamido tertiary butyl sulfonic acid (“ATBS”).Compl. ¶ 4; Ans. ¶ 4; Pl.’s Br. Ex. 3 at 26. The chemical structure forATBS is as follows:

Pl.’s Br. Ex. 3 at 27.

Plaintiff classified its ATBS entries under HTSUS subheading2924.19.11, Compl. ¶ 7; Ans. ¶ 7, which covers “Carboxyamide-function compounds; amide-function compounds of carbonic acid: Acy-clic amides (including acyclic carbamates) and their derivatives; saltsthereof: Other: Amides: Acrylamide.” HTSUS subheading 2924.19.11.Customs rejected this classification, opting instead for the “other:other” category for acyclic amides under HTSUS subheading2924.19.80. Compl. ¶ 8; Ans. ¶ 8.

II. Standard of Review

The court reviews Customs’ protest decisions de novo. 28 U.S.C.§ 2640(a)(1). USCIT Rule 56 permits summary judgment when “thereis no genuine issue as to any material fact.” USCIT R. 56(c); see also

Anderson v. Liberty Lobby, Inc., 477 U.S. 242, 247 (1986). In consid-ering whether material facts are in dispute, the evidence must beconsidered in the light most favorable to the non-moving party, draw-ing all reasonable inferences in its favor. See Adickes v. S.H. Kress &

Co., 398 U.S. 144, 157 (1970); Anderson, 477 U.S. at 261 n.2.A classification decision involves two steps. The first step addresses

the proper meaning of the relevant tariff provisions, which is a ques-tion of law. See Faus Group, Inc. v. United States, 581 F.3d 1369,1371–72 (Fed. Cir. 2009) (citing Orlando Food Corp. v. United States,140 F.3d 1437, 1439 (Fed. Cir. 1998)). The second step involves de-termining whether the merchandise at issue falls within a particulartariff provision as construed, which, when disputed, is a question offact. Id.

141 CUSTOMS BULLETIN AND DECISIONS, VOL. 50, NO. 23, JUNE 8, 2016

When there is no factual dispute regarding the merchandise, theresolution of the classification issue turns on the first step, determin-ing the proper meaning and scope of the relevant tariff provisions. See

Carl Zeiss, Inc. v. United States, 195 F.3d 1375, 1378 (Fed. Cir. 1999);Bausch & Lomb, Inc. v. United States, 148 F.3d 1363, 1365–66 (Fed.Cir. 1998). This is such a case, and summary judgment is appropriate.See Bausch & Lomb, 148 F.3d at 1365–66.

While the court accords deference to Customs classification rulingsrelative to their “power to persuade,” United States v. Mead Corp.,533 U.S. 218, 235 (2001) (citing Skidmore v. Swift & Co., 323 U.S.134, 140 (1944)), the court has “an independent responsibility todecide the legal issue of the proper meaning and scope of HTSUSterms.” Warner-Lambert Co. v. United States, 407 F.3d 1207, 1209(Fed. Cir. 2005) (citing Rocknel Fastener, Inc. v. United States, 267F.3d 1354, 1358 (Fed. Cir. 2001)).

III. Discussion

Classification disputes under the HTSUS are resolved by referenceto the General Rules of Interpretation (“GRIs”) and the AdditionalU.S. Rules of Interpretation. See Carl Zeiss, 195 F.3d at 1379. TheGRIs are applied in numerical order. Id. Interpretation of the HTSUSbegins with the language of the tariff headings, subheadings, theirsection and chapter notes, and may also be aided by the ExplanatoryNotes (“ENs”) published by the World Customs Organization. Id.

“GRI 1 is paramount. . . . The HTSUS is designed so that mostclassification questions can be answered by GRI 1 . . . .” Telebrands

Corp. v. United States, 36 CIT ___, ___, 865 F. Supp. 2d 1277, 1280(2012).

Under GRI 1, merchandise that is described “in whole by a singleclassification heading or subheading” is classifiable under that head-ing or subheading. CamelBak Prods. LLC v. United States, 649 F.3d1361, 1364 (Fed. Cir. 2011). If that single classification applies, thesucceeding GRIs are inoperative. Mita Copystar Am. v. United States,160 F.3d 710, 712 (Fed. Cir. 1998). Here, GRI 1 resolves the classifi-cation of ATBS.

The court construes tariff terms according to their common andcommercial meanings, and may rely on both its own understanding ofthe term as well as upon lexicographic and scientific authorities. See

Len-Ron Mfg. Co. v. United States, 334 F.3d 1304, 1309 (Fed. Cir.2003). The court may also refer to the Explanatory Notes “accompa-nying a tariff subheading, which—although not controlling—provideinterpretive guidance.” E.T. Horn Co. v. United States, 367 F.3d 1326,1329 (Fed. Cir. 2004) (citing Len-Ron, 334 F.3d at 1309).

142 CUSTOMS BULLETIN AND DECISIONS, VOL. 50, NO. 23, JUNE 8, 2016

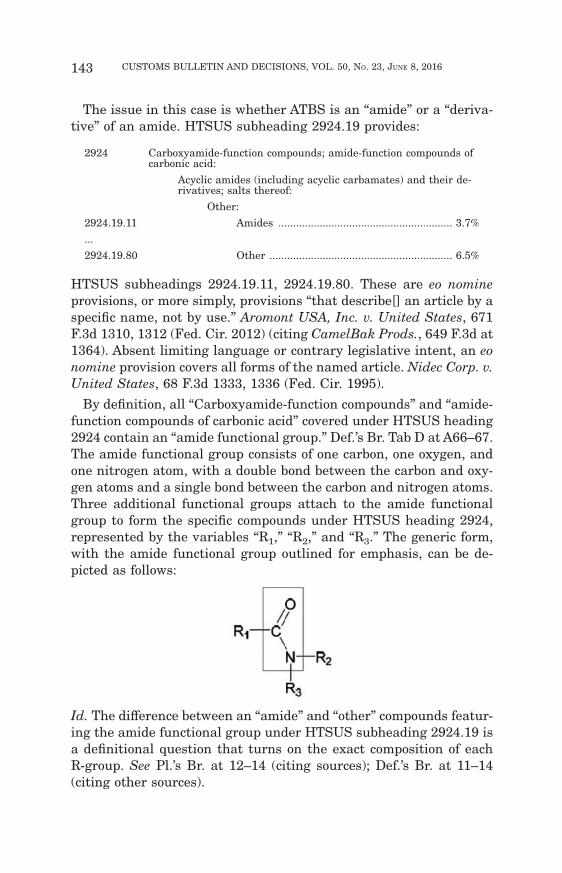

The issue in this case is whether ATBS is an “amide” or a “deriva-tive” of an amide. HTSUS subheading 2924.19 provides:

2924 Carboxyamide-function compounds; amide-function compounds ofcarbonic acid:

Acyclic amides (including acyclic carbamates) and their de-rivatives; salts thereof:

Other:

2924.19.11 Amides ........................................................... 3.7%

...

2924.19.80 Other .............................................................. 6.5%

HTSUS subheadings 2924.19.11, 2924.19.80. These are eo nomine

provisions, or more simply, provisions “that describe[] an article by aspecific name, not by use.” Aromont USA, Inc. v. United States, 671F.3d 1310, 1312 (Fed. Cir. 2012) (citing CamelBak Prods., 649 F.3d at1364). Absent limiting language or contrary legislative intent, an eo

nomine provision covers all forms of the named article. Nidec Corp. v.

United States, 68 F.3d 1333, 1336 (Fed. Cir. 1995).

By definition, all “Carboxyamide-function compounds” and “amide-function compounds of carbonic acid” covered under HTSUS heading2924 contain an “amide functional group.” Def.’s Br. Tab D at A66–67.The amide functional group consists of one carbon, one oxygen, andone nitrogen atom, with a double bond between the carbon and oxy-gen atoms and a single bond between the carbon and nitrogen atoms.Three additional functional groups attach to the amide functionalgroup to form the specific compounds under HTSUS heading 2924,represented by the variables “R1,” “R2,” and “R3.” The generic form,with the amide functional group outlined for emphasis, can be de-picted as follows:

Id. The difference between an “amide” and “other” compounds featur-ing the amide functional group under HTSUS subheading 2924.19 isa definitional question that turns on the exact composition of eachR-group. See Pl.’s Br. at 12–14 (citing sources); Def.’s Br. at 11–14(citing other sources).

143 CUSTOMS BULLETIN AND DECISIONS, VOL. 50, NO. 23, JUNE 8, 2016

There is no factual dispute as to ATBS’s chemical structure. ATBScontains an amide functional group with three R-groups attached.The R1 and R2 groups in ATBS are a hydrocarbon group and ahydrogen atom, respectively. The R3 group consists of a compounddominated by hydrogen and carbon, but also including sulfur andoxygen. ATBS compares to the generic amide as follows:

Pl.’s Br. ¶ 21; Def.’s Resp. ¶ 21.

Plaintiff contends that ATBS is an “amide” under HTSUS subhead-ing 2924.19.11. Pl.’s Br. at 10. According to Plaintiff, the only specificlimitation for the R1, R2, and R3 groups are that they must be “inde-pendently hydrogen, hydrocarbyl, or substituted hydrocarbyl.” Pl.’sBr. at 12–13 (quoting Pl.’s Br. Ex. 4 ¶ 11 (“Storey Aff.”)). Plaintiff’ssource for this definition is Dr. Robson F. Storey, the Bennett Distin-guished Professor of Polymer Science at the University of SouthernMississippi. See id. (citing Storey Aff. ¶ 11); Pl.’s Resp. at 4–5 (citingPl.’s Resp. Ex. 1 ¶¶ 10–12 (“Second Storey Aff.”)); see also Def.’s Br.Tab O at A169–219 (“Storey Dep.”). Plaintiff explains that Dr. Storey’sdefinition is consistent with “textbook examples of universally recog-nized ‘amides.’” Pl.’s Br. at 13–14.

Defendant counters that ATBS is only a “derivative” of an amide,not an “amide.” Def.’s Br. at 13–14. Defendant explains that lexico-graphical sources limit the R1, R2, and R3 groups to hydrogen orhydrocarbons. Id. Defendant challenges Dr. Storey’s definition as“inconsistent with the tariff schedule, the Explanatory Notes, diction-ary definitions, and organic chemistry textbooks,” and insists that Dr.Storey’s definition is also internally inconsistent. Def.’s Reply at 2.Specifically, Defendant contends that “substituted hydrocarbon” doesnot appear in dictionary or textbook definitions of “amide.”

In the court’s view, ATBS is not classifiable as an “amide” underHTSUS subheading 2924.19.11. The HTSUS does not define “amide.”See HTSUS Chapter 29. The EN to heading 2924, however, providesa clear definition. According to the ENs:

144 CUSTOMS BULLETIN AND DECISIONS, VOL. 50, NO. 23, JUNE 8, 2016

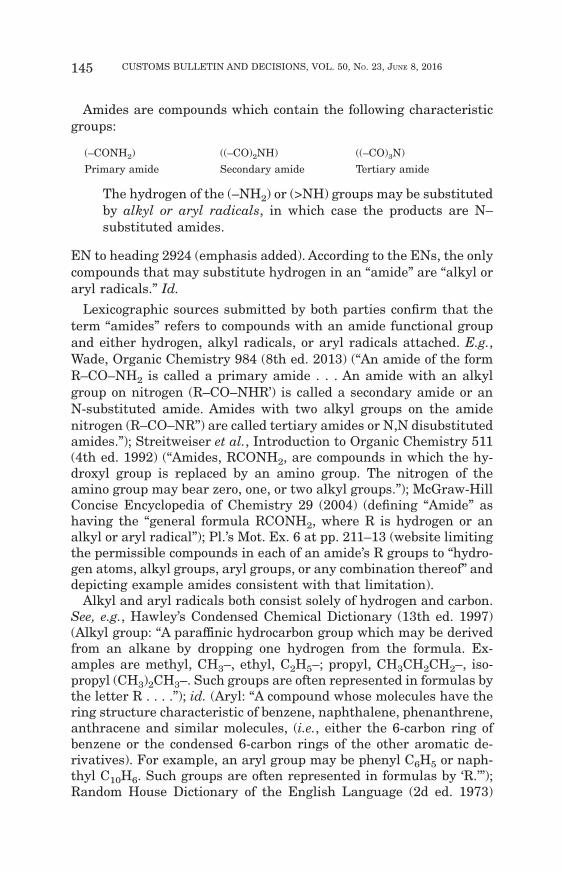

Amides are compounds which contain the following characteristicgroups:

(–CONH2) ((–CO)2NH) ((–CO)3N)

Primary amide Secondary amide Tertiary amide

The hydrogen of the (–NH2) or (>NH) groups may be substitutedby alkyl or aryl radicals, in which case the products are N–substituted amides.

EN to heading 2924 (emphasis added). According to the ENs, the onlycompounds that may substitute hydrogen in an “amide” are “alkyl oraryl radicals.” Id.

Lexicographic sources submitted by both parties confirm that theterm “amides” refers to compounds with an amide functional groupand either hydrogen, alkyl radicals, or aryl radicals attached. E.g.,Wade, Organic Chemistry 984 (8th ed. 2013) (“An amide of the formR–CO–NH2 is called a primary amide . . . An amide with an alkylgroup on nitrogen (R–CO–NHR’) is called a secondary amide or anN-substituted amide. Amides with two alkyl groups on the amidenitrogen (R–CO–NR’’) are called tertiary amides or N,N disubstitutedamides.”); Streitweiser et al., Introduction to Organic Chemistry 511(4th ed. 1992) (“Amides, RCONH2, are compounds in which the hy-droxyl group is replaced by an amino group. The nitrogen of theamino group may bear zero, one, or two alkyl groups.”); McGraw-HillConcise Encyclopedia of Chemistry 29 (2004) (defining “Amide” ashaving the “general formula RCONH2, where R is hydrogen or analkyl or aryl radical”); Pl.’s Mot. Ex. 6 at pp. 211–13 (website limitingthe permissible compounds in each of an amide’s R groups to “hydro-gen atoms, alkyl groups, aryl groups, or any combination thereof” anddepicting example amides consistent with that limitation).

Alkyl and aryl radicals both consist solely of hydrogen and carbon.See, e.g., Hawley’s Condensed Chemical Dictionary (13th ed. 1997)(Alkyl group: “A paraffinic hydrocarbon group which may be derivedfrom an alkane by dropping one hydrogen from the formula. Ex-amples are methyl, CH3–, ethyl, C2H5–; propyl, CH3CH2CH2–, iso-propyl (CH3)2CH3–. Such groups are often represented in formulas bythe letter R . . . .”); id. (Aryl: “A compound whose molecules have thering structure characteristic of benzene, naphthalene, phenanthrene,anthracene and similar molecules, (i.e., either the 6-carbon ring ofbenzene or the condensed 6-carbon rings of the other aromatic de-rivatives). For example, an aryl group may be phenyl C6H5 or naph-thyl C10H6. Such groups are often represented in formulas by ‘R.’”);Random House Dictionary of the English Language (2d ed. 1973)

145 CUSTOMS BULLETIN AND DECISIONS, VOL. 50, NO. 23, JUNE 8, 2016

(Alkyl Group: “any of a series of univalent groups of the generalformula CnH2n+1, derived from aliphatic hydrocarbons, as the methylgroup, CH3–, or ethyl group, C2H5–”). The compound in ATBS’s R3

position contains sulfur and oxygen in addition to hydrogen andcarbon, meaning it cannot be an “alkyl or aryl radical.” Pl.’s Br. ¶ 21;Def.’s Resp. ¶ 21. Because the compound in ATBS is not an “alkyl oraryl radical[],” ATBS does not meet the definition of “amide” set forthin the ENs. EN to heading 2924.

Plaintiff’s main argument is that many lexicographic sources do notexplicitly limit the definition of “amide” to those compounds withamide functional groups containing only hydrogen and alkyl or arylradicals in each of its R positions. Pl.’s Br. at 18–21; see, e.g., Wade,supra at 983–85 (listing only hydrocarbons as examples of N– sub-stitutes, but not stating that hydrocarbons are in fact the only ac-ceptable N– substitutes). Plaintiff relies on an interpretation of theHTSUS from Dr. Storey, who proposes that “substituted hydrocarb-yls” may appear in the R3 position, and that the compound in ATBS’sR3 position is one such “substituted hydrocarbyl.” Storey Aff. ¶ 13. Dr.Storey refers to several U.S. Patents to support his interpretation. Id.

¶ 22 (citing U.S. Patent No. 8,383,760; U.S. Patent No. 5,811,580;U.S. Patent No. 6,482,983).

The court is not persuaded. The ENs define “amide” by reference tohydrogen, aryl radicals, and alkyl radicals only. EN to heading 2924.Plaintiff urges the court to read “substituted hydrocarbyls” into thislist, a phrase which appears in neither heading 2924 nor the accom-panying EN. Pl.’s Br. at 18–21. Although Dr. Storey is a potential“scientific authority” that the court may consider to discern the com-mon and commercial meaning of all tariff terms, see Mead Corp. v.

United States, 283 F.3d 1342, 1346 (Fed. Cir. 2002) (citing C.J. Tower

& Sons of Buffalo, Inc. v. United States, 673 F.2d 1268, 1271 (Cust. &Pat. App. 1982)), neither Dr. Storey nor Plaintiff has identified onedictionary, treatise, textbook, or other information source stating that“substituted hydrocarbyls” can appear in “amides” in addition to alkylor aryl radicals. Instead, these lexicographic sources uniformly defineor depict “amides” as consisting of an amide functional group witheither hydrogen, aryl radicals, or alkyl radicals attached. Conse-quently, because the compound in ATBS’s R3 position is not hydrogen,an alkyl radical, or aryl radical, the court concludes that ATBS doesnot meet the definition of “Amide” under HTSUS subheading2924.19.11. See EN to heading 2924.

This leaves HTSUS subheading 2924.19.80 as the only other viableoption. Plaintiff argues that ATBS cannot be classified under HTSUSsubheading 2924.19.80 because ATBS is not a “derivative” of an

146 CUSTOMS BULLETIN AND DECISIONS, VOL. 50, NO. 23, JUNE 8, 2016

amide. Pl.’s Br. at 22–30 (arguing that “derivative” refers to a com-pound actually derived from another through a chemical process, andthat there is no known process to derive ATBS from an amide). Thecourt does not agree. The ENs define “sulfonated derivative[s]” ofcompounds covered under HTSUS Chapter 29 as compounds “formedby substitution of one or more hydrogen atoms in the parent com-pound by one or more . . . sulpho (–SO3H) groups. . . . Any functionalgroup (e.g., aldehyde, carboxylic acid, amine) taken into considerationfor classification should remain intact in such derivatives.” EN toChapter 29, Chapter Note 4. With respect to ATBS, one sulpho(–SO3H) group substitutes one hydrogen atom on the parent com-pound, and the amide functional group remains intact. Plaintiff ar-gues that ATBS has not undergone “sulfonation,” Pl.’s Resp. at 13–15,but there is no reference in the EN’s definition of “sulfonated deriva-tive” to any chemical process or method of manufacture. See EN toChapter 29, Chapter Note 4. According to the ENs, therefore, ATBS isin fact a “sulfonated derivative” of an amide. See id.

More generally, for purposes of classifying chemicals under theHTSUS the term “derivative” refers to a compound structurally re-

lated to another compound, not solely a compound chemically pro-duced from another compound. E.g., Horn, 367 F.3d at 133133 (ex-plaining that “derivative” refers to chemical structure not method ofmanufacture, and that when Congress intends to “limit the classifi-cation of chemicals by source” it uses “more instructive phrases suchas ‘derived from,’ ‘produced from,’ or ‘manufactured from’”); see also

Wesbter’s New Int’l Dictionary of the English Language (2d ed. 1941)(Derivative: “2. Chem. A substance so related to another substance bymodification or partial substitution as to be regarded as theoreticallyderived from it, even when not obtainable from it in practice; thusamino compounds are derivatives of ammonia” (emphasis added)).Here, ATBS is a derivative of acrylamide because they share the samechemical structure except for the compounds located in the R3 posi-tion.

Finally, Plaintiff contends that even if the court accepts that ATBSis a “derivative” of an “amide,” classification under HTSUS subhead-ing 2924.19.80 would still be improper because, in Plaintiff’s view,ATBS is simultaneously an “amide” and a “derivative” of an amide,and because the ten-digit statistical suffixes under HTSUS subhead-ing 2924.19.11 are more specific to derivatives of “Acrylamide.” Pl.’sBr. at 3745; see also HTSUS subheading 2924.19.11.10 to .50 (statis-tical subheadings under “Amides” covering “Acrylamide,” “Dimethyl-formamide,” “Methacrylamide,” and “other”). The court again doesnot agree. Both arguments presuppose that ATBS meets the defini-

147 CUSTOMS BULLETIN AND DECISIONS, VOL. 50, NO. 23, JUNE 8, 2016

tion of “amide” under HTSUS subheading 2924.19.11. See Pillowtex

Corp. v. United States, 171 F.3d 1370, 1374 (Fed. Cir. 1990) (“[C]las-sification of merchandise should not be based upon the wording ofstatistical suffixes, because statistical annotations, including statis-tical suffixes, are not part of the legal text of the HTSUS.”). Asexplained above, ATBS does not meet the EN definition of “amide,”which means it is not classifiable under HTSUS subheading2924.19.11 (or any of its statistical suffixes).

The court therefore concludes that ATBS is properly classified un-der HTSUS subheading 2924.19.80 as a derivative of an amide.

IV. Conclusion

In accordance with the foregoing, the court concludes that ATBS isproperly classified under HTSUS subheading 2924.19.80. The courtwill therefore enter judgment granting Defendant’s cross-motion forsummary judgment and denying Plaintiff’s motion for summary judg-ment.Dated: May 25, 2016

New York, New York/s/ Leo M. Gordon

JUDGE LEO M. GORDON

148 CUSTOMS BULLETIN AND DECISIONS, VOL. 50, NO. 23, JUNE 8, 2016