us equity market correlation to yields/funding currencies · pulled the opposite ... in how the...

TRANSCRIPT

Page 1 of 8

For Personal Use Only—Do Not Forward

BespokePremium.com © Copyright 2015, Bespoke Investment Group, LLC. Bespoke Investment Group, LLC believes all information contained in this report to be accurate, but we do not guarantee its accuracy. None of the information in this report or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities.

Recent market price action has

started to depart noticeably from

the pattern we’ve been accus-

tomed to recently. For instance,

despite the recent “funding cur-

rency” behavior for risk assets

that has seen the EURUSD cross

sell off on rallies in global equity

indices, today EURUSD declined

sharply in tandem with equities,

as shown in the chart at right.

We’ve also seen bonds go from

positively correlated to equities

throughout August and early

September to a resumption of

their more familiar trend of in-

verse correlation to stocks, again

charted.

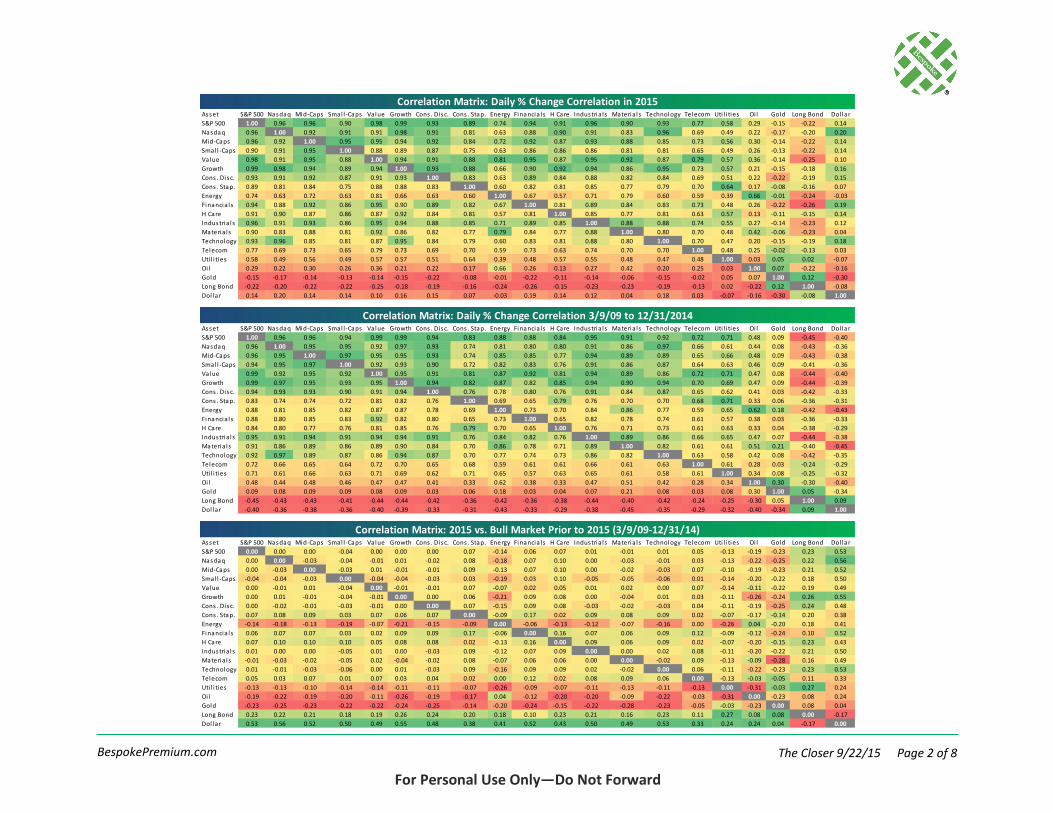

To get a handle on how some of

these different correlation chang-

es are playing out in the grander

scheme of things, on the follow-

ing page we’ve created three

matrices. The first two matrices

measure the daily price correla-

tion of 20 different assets and indices with each other. The first matrix shows the correlations between

each since the start of 2015. The second shows these correlations from the start of the bull market

through the end of 2014. Finally, in the third matrix we show the difference between the two, to high-

light where correlations are shifting. In the third matrix, lower readings indicate drops in correlation in

2015 versus the bull market, while higher readings indicate increases in correlation.

For most of the bull market, the USD was negatively correlated with stock indices of various types.

Since then, though, it has shifted to become positively correlated with the market. Commodities have

pulled the opposite move: after being relatively correlated with stocks for most of the bull run, they

are now sharply negatively correlated. Energy as a sector has broadly followed this move given its beta

to oil. We also think it’s interesting that bonds are becoming less and less negatively correlated to eq-

uities.

Overall, these matrices and the recent shift in how the equity market tracks EURUSD or the long bond

are a very good lesson that correlations are never stable in financial markets; while they can last for

long periods of time, the prices of different assets will never perfectly track one another indefinitely.

Pattern Breaks US Equity Market Correlation to Yields/Funding Currencies

1.110

1.115

1.120

1.125

1.130

1.135

1.140

1.145

1.150

1,900

1,920

1,940

1,960

1,980

2,000

2,020S&P 500 Futures (Left Axis)

EURUSD (Right Axis)

2.800

2.850

2.900

2.950

3.000

3.050

3.100

3.150

1,900

1,920

1,940

1,960

1,980

2,000

2,020S&P 500 Futures (Left Axis)

30 Year Yield (Right Axis)

Page 2 of 8 The Closer 9/22/15 BespokePremium.com

For Personal Use Only—Do Not Forward

Asset S&P 500 Nasdaq Mid-Caps Smal l -Caps Value Growth Cons . Disc. Cons . Stap. Energy Financia ls H Care Industria ls Materia ls Technology Telecom Uti l i ties Oi l Gold Long Bond Dol lar

S&P 500 1.00 0.96 0.96 0.90 0.98 0.99 0.93 0.89 0.74 0.94 0.91 0.96 0.90 0.93 0.77 0.58 0.29 -0.15 -0.22 0.14

Nasdaq 0.96 1.00 0.92 0.91 0.91 0.98 0.91 0.81 0.63 0.88 0.90 0.91 0.83 0.96 0.69 0.49 0.22 -0.17 -0.20 0.20

Mid-Caps 0.96 0.92 1.00 0.95 0.95 0.94 0.92 0.84 0.72 0.92 0.87 0.93 0.88 0.85 0.73 0.56 0.30 -0.14 -0.22 0.14

Smal l -Caps 0.90 0.91 0.95 1.00 0.88 0.89 0.87 0.75 0.63 0.86 0.86 0.86 0.81 0.81 0.65 0.49 0.26 -0.13 -0.22 0.14

Value 0.98 0.91 0.95 0.88 1.00 0.94 0.91 0.88 0.81 0.95 0.87 0.95 0.92 0.87 0.79 0.57 0.36 -0.14 -0.25 0.10

Growth 0.99 0.98 0.94 0.89 0.94 1.00 0.93 0.88 0.66 0.90 0.92 0.94 0.86 0.95 0.73 0.57 0.21 -0.15 -0.18 0.16

Cons . Disc. 0.93 0.91 0.92 0.87 0.91 0.93 1.00 0.83 0.63 0.89 0.84 0.88 0.82 0.84 0.69 0.51 0.22 -0.22 -0.19 0.15

Cons . Stap. 0.89 0.81 0.84 0.75 0.88 0.88 0.83 1.00 0.60 0.82 0.81 0.85 0.77 0.79 0.70 0.64 0.17 -0.08 -0.16 0.07

Energy 0.74 0.63 0.72 0.63 0.81 0.66 0.63 0.60 1.00 0.67 0.57 0.71 0.79 0.60 0.59 0.39 0.66 -0.01 -0.24 -0.03

Financia ls 0.94 0.88 0.92 0.86 0.95 0.90 0.89 0.82 0.67 1.00 0.81 0.89 0.84 0.83 0.73 0.48 0.26 -0.22 -0.26 0.19

H Care 0.91 0.90 0.87 0.86 0.87 0.92 0.84 0.81 0.57 0.81 1.00 0.85 0.77 0.81 0.63 0.57 0.13 -0.11 -0.15 0.14

Industria ls 0.96 0.91 0.93 0.86 0.95 0.94 0.88 0.85 0.71 0.89 0.85 1.00 0.88 0.88 0.74 0.55 0.27 -0.14 -0.23 0.12

Materia ls 0.90 0.83 0.88 0.81 0.92 0.86 0.82 0.77 0.79 0.84 0.77 0.88 1.00 0.80 0.70 0.48 0.42 -0.06 -0.23 0.04

Technology 0.93 0.96 0.85 0.81 0.87 0.95 0.84 0.79 0.60 0.83 0.81 0.88 0.80 1.00 0.70 0.47 0.20 -0.15 -0.19 0.18

Telecom 0.77 0.69 0.73 0.65 0.79 0.73 0.69 0.70 0.59 0.73 0.63 0.74 0.70 0.70 1.00 0.48 0.25 -0.02 -0.13 0.03

Uti l i ties 0.58 0.49 0.56 0.49 0.57 0.57 0.51 0.64 0.39 0.48 0.57 0.55 0.48 0.47 0.48 1.00 0.03 0.05 0.02 -0.07

Oi l 0.29 0.22 0.30 0.26 0.36 0.21 0.22 0.17 0.66 0.26 0.13 0.27 0.42 0.20 0.25 0.03 1.00 0.07 -0.22 -0.16

Gold -0.15 -0.17 -0.14 -0.13 -0.14 -0.15 -0.22 -0.08 -0.01 -0.22 -0.11 -0.14 -0.06 -0.15 -0.02 0.05 0.07 1.00 0.12 -0.30

Long Bond -0.22 -0.20 -0.22 -0.22 -0.25 -0.18 -0.19 -0.16 -0.24 -0.26 -0.15 -0.23 -0.23 -0.19 -0.13 0.02 -0.22 0.12 1.00 -0.08

Dol lar 0.14 0.20 0.14 0.14 0.10 0.16 0.15 0.07 -0.03 0.19 0.14 0.12 0.04 0.18 0.03 -0.07 -0.16 -0.30 -0.08 1.00

Asset S&P 500 Nasdaq Mid-Caps Smal l -Caps Value Growth Cons . Disc. Cons . Stap. Energy Financia ls H Care Industria ls Materia ls Technology Telecom Uti l i ties Oi l Gold Long Bond Dol lar

S&P 500 1.00 0.96 0.96 0.94 0.99 0.99 0.94 0.83 0.88 0.88 0.84 0.95 0.91 0.92 0.72 0.71 0.48 0.09 -0.45 -0.40

Nasdaq 0.96 1.00 0.95 0.95 0.92 0.97 0.93 0.74 0.81 0.80 0.80 0.91 0.86 0.97 0.66 0.61 0.44 0.08 -0.43 -0.36

Mid-Caps 0.96 0.95 1.00 0.97 0.95 0.95 0.93 0.74 0.85 0.85 0.77 0.94 0.89 0.89 0.65 0.66 0.48 0.09 -0.43 -0.38

Smal l -Caps 0.94 0.95 0.97 1.00 0.92 0.93 0.90 0.72 0.82 0.83 0.76 0.91 0.86 0.87 0.64 0.63 0.46 0.09 -0.41 -0.36

Value 0.99 0.92 0.95 0.92 1.00 0.95 0.91 0.81 0.87 0.92 0.81 0.94 0.89 0.86 0.72 0.71 0.47 0.08 -0.44 -0.40

Growth 0.99 0.97 0.95 0.93 0.95 1.00 0.94 0.82 0.87 0.82 0.85 0.94 0.90 0.94 0.70 0.69 0.47 0.09 -0.44 -0.39

Cons . Disc. 0.94 0.93 0.93 0.90 0.91 0.94 1.00 0.76 0.78 0.80 0.76 0.91 0.84 0.87 0.65 0.62 0.41 0.03 -0.42 -0.33

Cons . Stap. 0.83 0.74 0.74 0.72 0.81 0.82 0.76 1.00 0.69 0.65 0.79 0.76 0.70 0.70 0.68 0.71 0.33 0.06 -0.36 -0.31

Energy 0.88 0.81 0.85 0.82 0.87 0.87 0.78 0.69 1.00 0.73 0.70 0.84 0.86 0.77 0.59 0.65 0.62 0.18 -0.42 -0.43

Financia ls 0.88 0.80 0.85 0.83 0.92 0.82 0.80 0.65 0.73 1.00 0.65 0.82 0.78 0.74 0.61 0.57 0.38 0.03 -0.36 -0.33

H Care 0.84 0.80 0.77 0.76 0.81 0.85 0.76 0.79 0.70 0.65 1.00 0.76 0.71 0.73 0.61 0.63 0.33 0.04 -0.38 -0.29

Industria ls 0.95 0.91 0.94 0.91 0.94 0.94 0.91 0.76 0.84 0.82 0.76 1.00 0.89 0.86 0.66 0.65 0.47 0.07 -0.44 -0.38

Materia ls 0.91 0.86 0.89 0.86 0.89 0.90 0.84 0.70 0.86 0.78 0.71 0.89 1.00 0.82 0.61 0.61 0.51 0.21 -0.40 -0.45

Technology 0.92 0.97 0.89 0.87 0.86 0.94 0.87 0.70 0.77 0.74 0.73 0.86 0.82 1.00 0.63 0.58 0.42 0.08 -0.42 -0.35

Telecom 0.72 0.66 0.65 0.64 0.72 0.70 0.65 0.68 0.59 0.61 0.61 0.66 0.61 0.63 1.00 0.61 0.28 0.03 -0.24 -0.29

Uti l i ties 0.71 0.61 0.66 0.63 0.71 0.69 0.62 0.71 0.65 0.57 0.63 0.65 0.61 0.58 0.61 1.00 0.34 0.08 -0.25 -0.32

Oi l 0.48 0.44 0.48 0.46 0.47 0.47 0.41 0.33 0.62 0.38 0.33 0.47 0.51 0.42 0.28 0.34 1.00 0.30 -0.30 -0.40

Gold 0.09 0.08 0.09 0.09 0.08 0.09 0.03 0.06 0.18 0.03 0.04 0.07 0.21 0.08 0.03 0.08 0.30 1.00 0.05 -0.34

Long Bond -0.45 -0.43 -0.43 -0.41 -0.44 -0.44 -0.42 -0.36 -0.42 -0.36 -0.38 -0.44 -0.40 -0.42 -0.24 -0.25 -0.30 0.05 1.00 0.09

Dol lar -0.40 -0.36 -0.38 -0.36 -0.40 -0.39 -0.33 -0.31 -0.43 -0.33 -0.29 -0.38 -0.45 -0.35 -0.29 -0.32 -0.40 -0.34 0.09 1.00

Asset S&P 500 Nasdaq Mid-Caps Smal l -Caps Value Growth Cons . Disc. Cons . Stap. Energy Financia ls H Care Industria ls Materia ls Technology Telecom Uti l i ties Oi l Gold Long Bond Dol lar

S&P 500 0.00 0.00 0.00 -0.04 0.00 0.00 0.00 0.07 -0.14 0.06 0.07 0.01 -0.01 0.01 0.05 -0.13 -0.19 -0.23 0.23 0.53

Nasdaq 0.00 0.00 -0.03 -0.04 -0.01 0.01 -0.02 0.08 -0.18 0.07 0.10 0.00 -0.03 -0.01 0.03 -0.13 -0.22 -0.25 0.22 0.56

Mid-Caps 0.00 -0.03 0.00 -0.03 0.01 -0.01 -0.01 0.09 -0.13 0.07 0.10 0.00 -0.02 -0.03 0.07 -0.10 -0.19 -0.23 0.21 0.52

Smal l -Caps -0.04 -0.04 -0.03 0.00 -0.04 -0.04 -0.03 0.03 -0.19 0.03 0.10 -0.05 -0.05 -0.06 0.01 -0.14 -0.20 -0.22 0.18 0.50

Value 0.00 -0.01 0.01 -0.04 0.00 -0.01 -0.01 0.07 -0.07 0.02 0.05 0.01 0.02 0.00 0.07 -0.14 -0.11 -0.22 0.19 0.49

Growth 0.00 0.01 -0.01 -0.04 -0.01 0.00 0.00 0.06 -0.21 0.09 0.08 0.00 -0.04 0.01 0.03 -0.11 -0.26 -0.24 0.26 0.55

Cons . Disc. 0.00 -0.02 -0.01 -0.03 -0.01 0.00 0.00 0.07 -0.15 0.09 0.08 -0.03 -0.02 -0.03 0.04 -0.11 -0.19 -0.25 0.24 0.48

Cons . Stap. 0.07 0.08 0.09 0.03 0.07 0.06 0.07 0.00 -0.09 0.17 0.02 0.09 0.08 0.09 0.02 -0.07 -0.17 -0.14 0.20 0.38

Energy -0.14 -0.18 -0.13 -0.19 -0.07 -0.21 -0.15 -0.09 0.00 -0.06 -0.13 -0.12 -0.07 -0.16 0.00 -0.26 0.04 -0.20 0.18 0.41

Financia ls 0.06 0.07 0.07 0.03 0.02 0.09 0.09 0.17 -0.06 0.00 0.16 0.07 0.06 0.09 0.12 -0.09 -0.12 -0.24 0.10 0.52

H Care 0.07 0.10 0.10 0.10 0.05 0.08 0.08 0.02 -0.13 0.16 0.00 0.09 0.06 0.09 0.02 -0.07 -0.20 -0.15 0.23 0.43

Industria ls 0.01 0.00 0.00 -0.05 0.01 0.00 -0.03 0.09 -0.12 0.07 0.09 0.00 0.00 0.02 0.08 -0.11 -0.20 -0.22 0.21 0.50

Materia ls -0.01 -0.03 -0.02 -0.05 0.02 -0.04 -0.02 0.08 -0.07 0.06 0.06 0.00 0.00 -0.02 0.09 -0.13 -0.09 -0.28 0.16 0.49

Technology 0.01 -0.01 -0.03 -0.06 0.00 0.01 -0.03 0.09 -0.16 0.09 0.09 0.02 -0.02 0.00 0.06 -0.11 -0.22 -0.23 0.23 0.53

Telecom 0.05 0.03 0.07 0.01 0.07 0.03 0.04 0.02 0.00 0.12 0.02 0.08 0.09 0.06 0.00 -0.13 -0.03 -0.05 0.11 0.33

Uti l i ties -0.13 -0.13 -0.10 -0.14 -0.14 -0.11 -0.11 -0.07 -0.26 -0.09 -0.07 -0.11 -0.13 -0.11 -0.13 0.00 -0.31 -0.03 0.27 0.24

Oi l -0.19 -0.22 -0.19 -0.20 -0.11 -0.26 -0.19 -0.17 0.04 -0.12 -0.20 -0.20 -0.09 -0.22 -0.03 -0.31 0.00 -0.23 0.08 0.24

Gold -0.23 -0.25 -0.23 -0.22 -0.22 -0.24 -0.25 -0.14 -0.20 -0.24 -0.15 -0.22 -0.28 -0.23 -0.05 -0.03 -0.23 0.00 0.08 0.04

Long Bond 0.23 0.22 0.21 0.18 0.19 0.26 0.24 0.20 0.18 0.10 0.23 0.21 0.16 0.23 0.11 0.27 0.08 0.08 0.00 -0.17

Dol lar 0.53 0.56 0.52 0.50 0.49 0.55 0.48 0.38 0.41 0.52 0.43 0.50 0.49 0.53 0.33 0.24 0.24 0.04 -0.17 0.00

Correlation Matrix: Daily % Change Correlation in 2015

Correlation Matrix: Daily % Change Correlation 3/9/09 to 12/31/2014

Correlation Matrix: 2015 vs. Bull Market Prior to 2015 (3/9/09-12/31/14)

Page 3 of 8 The Closer 9/22/15 BespokePremium.com

For Personal Use Only—Do Not Forward

The Richmond Fed Services Index disap-

pointed significantly in its release today,

with several major indicators dropping

to multi-month lows in a huge decline

from up-beat readings in August. We

think the Services index is much more

important than its more frequently-

quoted Manufacturing cousin, which

also missed today. That’s because we

have few readings on the health of the

vast majority of American businesses—

services providers–and many, many

readings on the much less significant

manufacturing sector. As shown at left,

huge declines MoM for Services Reve-

nues and employment point to negative

readings from the ISM Non-

Manufacturing survey. In the case of

revenues, the upward trend is still very

much intact, but as shown in the em-

ployment chart, that reading is making

lower lows and lower highs since the

middle of 2014.

Broadly speaking, consumer incomes

remain high, along with employment.

Regardless of whether consumers will

spend savings from energy price de-

clines, the reality is that the typical con-

sumer has much more flexibility and

room to keep spending stable right now

than at previous points in the current

expansion or the last one. We covered

that to close The Bespoke Report last

week (please see page 31).

Richmond Fed Services Decline Sharply From Local Highs

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Current Prices (3m Avg)

Expected Prices (3m Avg)

Core CPI

10

20

30

40

50

60

70

80

90

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Revenues (Rebased to 50 scale)

ISM Non-Manufacturing Activity

15

25

35

45

55

65

75

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Number of Employees (Rebased to 50)

ISM Non-Manufacturing (Employment)

1.32

1.64

60

64

5655

1.80

Page 4 of 8 The Closer 9/22/15 BespokePremium.com

For Personal Use Only—Do Not Forward

Looking at the like-for-like comparison

of the Services index to its Manufactur-

ing counterpart, we continue to see ro-

bust outperformance of Services versus

comparable Manufacturing indicators.

While there was a huge drop in Revenue

MoM, the uptrend visible at right re-

mains in place, which we can’t say for

the Manufacturing New Orders Series.

There’s a similar story for Employment,

with the Services industry seeing a back-

and-forth range of employment growth

versus a consistently weak and deterio-

rating employment picture. We would

note that Employment and Wages were

without doubt the two strongest areas

for the Manufacturing survey, sug-

gesting that the labor market continues

to outperform growth. Employment

indicators are also robust for Services,

where the outlook is still strong as well.

Overall, only one subindex registered

contraction (retailing employment).

All Services Sept Change Aug July June

Revenues 10 -20 30 32 19

Employees 5 -13 18 12 10

Wages 20 -6 26 25 21

Exp. Demand 24 -8 32 30 25

Retailers Sept Change Aug July June

Sales 16 -28 44 35 15

Employees -19 -24 5 10 -19

Wages 30 0 30 20 27

Inventories 35 23 12 15 8

Big Ticket 20 19 1 19 -2

Shoppers 39 -15 54 48 16

Exp. Demand 33 -12 45 27 11

Ex Retail Sept Change Aug July June

Revenues 10 -18 28 32 19

Employees 8 -12 20 12 15

Wages 19 -7 26 26 19

Exp. Demand 23 -8 31 31 27

Prices Sept Change Aug July June

Services 1.18 -0.35 1.53 1.26 1.36

Retail 1.25 -0.73 1.98 1.48 1.32

Non-Retail 1.17 -0.32 1.49 1.23 1.36

Exp. Prices Sept Change Aug July June

Services 1.65 -0.20 1.85 1.42 1.69

Retail 2.01 -0.23 2.24 1.32 1.65

Non-Retail 1.60 -0.21 1.81 1.44 1.70

Richmond Fed Services Sector Survey

Services "Catches Down" To Manufacturing; Still Stronger

-60

-50

-40

-30

-20

-10

0

10

20

30

40

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Reveneus (Services)

New Orders (Manufacturing)

-40

-30

-20

-10

0

10

20

30

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Number of Employees (Services)

Number of Employees (Manufacturing)

-20

-10

0

10

20

30

40

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Wages (Services) Wages (Manufacturing)

-12

10

15

20

15

Page 5 of 8 The Closer 9/22/15 BespokePremium.com

For Personal Use Only—Do Not Forward

It’ll be a busy session overnight. We have a Fed speaker this evening, followed by China Flash Manufac-

turing for the month of September. While we don’t think this number is necessarily the best way to

view the Chinese economy given the relatively robust services/non-industrial data recently, markets

will be focused very, very closely on the figure. It’s also viewed as relatively reliable given the non-

official (read: less manipulated) nature of the data, and it's very close to “real time” versus other much

more lagging indicators. If there’s a big miss of expectations, expect a sharp correction in stocks and

higher-beta (growth– and commodity-oriented) FX, and a rally in Treasuries. Other data overnight in-

cludes insights on European growth from their Markit PMIs and revised French GDP. Tomorrow in the

US we get ECB chief Mario Draghi speaking right before the open of stocks; watch for hints at expan-

sion or lengthening of ECB QE given the higher EUR recently and the overall sideways move in Europe-

an data over the last few months. A small miss and sequential decline in Eurozone Consumer Confi-

dence this morning is a good example of the less impressive improvement relative to the beginning of

the year. Later in the US, we get flash Manufacturing PMI, which should be weak if regional Fed indices

so far (Empire, Philly, Richmond) are any indication.

Price action today was brutal, with copper off 3.5% . WTI had a grim day but rallied following the equi-

ty market close based on an inventory drawdown number from the API survey of oil inventories ahead

of official data tomorrow courtesy of the DoE. Bonds got back most of their losses from yesterday as

the yield curve bull-flattened, while the dollar was up versus every currency except USDJPY. USDMXN

soared, up 1.6% amidst reserve declines at the Bank of Mexico. Within the US equity market, every

sector was lower including a 2.9% decline in Autos & Parts in sympathy with the pain felt across the

Atlantic. Breadth was horrible, with over 93% of the S&P 500 lower on the day.

Time Release Period Estimate Reading Last

9:00 FHFA House Price Index Jul +0.4% +0.6% +0.2%

10:00 EZ Consumer Confidence (Flash) Sep -7.0 -7.1 -6.9

10:00 Richmond Fed Manufacturing Index Sep 2 -5 0

10:00 Richmond Fed Services Index Sep -- -- --

13:00 2 Year Note Auction ($26 billion): mixed auction results

16:30 API US Crude Oil Inventories (mm bbls) 22-Sep -- -3.68 -3.13

18:30 Atlanta Fed President Lockhart (voter) speaks on the economy

20:00 Australia Conf. Board Leading Indicatos Jul -- -- -0.2%

21:45 China Caixin Manf. PMI (Flash) Sep 47.5 -- 47.3

2:45 France GDP QoQ (Final) Q2 0.0% -- 0.0%

3:00 France Markit Manf. PMI (Flash) Sep 48.6 -- 48.3

3:00 France Markit Svcs. PMI (Flash) Sep 51.0 -- 50.6

3:30 Germany Markit Manf. PMI (Flash) Sep 52.6 -- 53.3

3:30 Germany Markit Svcs. PMI (Flash) Sep 54.5 -- 54.9

4:00 EZ Markit Manf. PMI (Flash) Sep 52.0 -- 52.3

4:00 EZ Markit Svcs. PMI (Flash) Sep 54.2 -- 54.4

7:00 MBA Mortgage Applications WoW 18-Sep -- -- -7.0%

8:30 Canada Retail Sales MoM Jul +0.7% -- +0.6%

8:30 Canada Retail Sales Ex Auto MoM Jul +0.5% -- +0.8%

9:00 ECB President Draghi Quarterly Hearing

9:35 Markit US Manufacturing PMI (Flash) Sep 52.8 -- 53.0

10:30 DoE US Crude Oil Inventories (mm barrels) 18-Sep -1162.5 -- -2104

11:30 2 Year Floating Rate Note Auction ($13 billion)

12:30 Atlanta Fed President Lockhart (voter) speaks on the economy

13:00 5 Year Note Auction ($35 billion)

US Data Recap and Overnight Preview

Page 6 of 8 The Closer 9/22/15 BespokePremium.com

For Personal Use Only—Do Not Forward

Popular Tweets From @bespokeinvest on Twitter

“German DAX on pace for a new short-term closing low. ” - 9:17

“Energy shares rallying here for the time being. $XLE ” - 9:58

“$XLE quickly approaching flat on the day, plenty of Energy stocks in the green. ” - 10:05

“75 stocks in the S&P 500 have hit 52-week lows following the decline on 8/24. ” - 16:12

Closing Charts & Tweets

Oil Future: Last 15 Trading Days Gold Front Month Future: Last 15 Trading Days

US Dollar Index: Last 15 Trading Days Long Bond Future Intraday: Last 15 Trading Days

S&P 500 Intraday: Last 15 Trading Days Nasdaq Composite: Last 15 Trading Days

42

43

44

45

46

47

48

49

9/1 9/3 9/8 9/10 9/14 9/16 9/18 9/22

94.0

94.5

95.0

95.5

96.0

96.5

97.0

9/2 9/4 9/8 9/10 9/14 9/16 9/18 9/22

151.0

152.0

153.0

154.0

155.0

156.0

157.0

9/1 9/3 9/8 9/10 9/14 9/16 9/18 9/22

1890

1910

1930

1950

1970

1990

2010

2030

9/1 9/3 9/8 9/10 9/14 9/16 9/18 9/22

4600

4650

4700

4750

4800

4850

4900

4950

5000

9/1 9/3 9/8 9/10 9/14 9/16 9/18 9/22

1090

1100

1110

1120

1130

1140

1150

9/1 9/3 9/8 9/10 9/14 9/16 9/18 9/22

Ticker Name Change Last 6 MosSPY S&P 500 -1.30IJH S&P 400 -1.34IJR S&P 600 -1.37DIA Dow 30 -1.15QQQ Nasdaq -1.50IWB Russel l 1000 -1.28IWM Russel l 2000 -1.52XLF Financia ls -1.27XLB Materia ls -1.86XLE Energy -1.06XLI Industria ls -1.45XLY Cons . Cycl ica l -1.33XLP Cons . Staples -1.09XLV Health Care -0.61IYZ Telecom -1.05XLK Technology -1.68XLU Uti l i ties -1.25GDX Gold Miners -4.57XME Metals & Mining -4.48XRT Reta i l -1.25XHB Homebui lders -1.97IYR US Real Estate -1.32KRE Regional Banks -0.86IWD Russel l 1000 Value -1.29IWF Russel l 1000 Growth -1.34VXX VIX 5.64AGG Total Bond Mkt 0.24TLT 20+ Yr Treasuries 1.39MUB Muni . Bonds 0.28LQD Invest. Gr. Bonds 0.43JNK High Yield Bonds -0.65BKLN Senior Loan -0.39GLD Gold -0.68SLV Si lver -2.42USO Oi l -0.86UNG Natura l Gas -0.33VT Tota l World -1.73CWI World Ex-US -2.43VEA Developed Mkts -2.35EEM Emerging Mkts -1.87EZU Eurozone -3.12DXJ Japan JPY Hdg'd -1.95EWZ Brazi l -2.71FXI China -1.74EWT Taiwan -2.20EWH Hong Kong -1.06EWW Mexico -1.86

Key ETFs (1 Day % Change)

ATML 12.72 MNK -10.18 ATML 826.98 SZMK -83.54

UNT 7.93 ZEUS -9.55 FOR 398.12 OMG -79.48

BBG 7.65 NEOG -9.30 MNK 218.02 SWI -79.26

MTRX 7.40 NRG -8.57 ANIP 199.70 RYAM -78.37

WRLD 5.84 SUPN -7.73 AEIS 180.91 CYT -76.86

CENTA 5.06 LCI -6.83 NEOG 175.41 KOPN -76.38

UFCS 4.83 VDSI -6.49 THO 138.67 NATI -76.02

DV 4.79 ENTA -6.41 AFFX 133.96 RAX -75.49

FOR 4.67 AVP -6.11 HUB/B 130.64 CTRE -75.40

SGY 4.32 BIIB -5.91 FSP 117.68 ASTE -75.40

SBRA 4.27 IO -5.60 LDR 117.32 VIAV -74.76

OFG 4.27 BLD -5.50 NRG 112.70 PCP -74.75

CC 4.22 AKS -5.34 HRC 104.96 VRTV -74.59

ANIP 4.11 LL -5.15 BWA 95.98 NPBC -74.33

ALK 4.04 VRTX -5.11 APOG 95.76 ESE -73.68

Most Down

Price (%)

S&P 1500 Biggest MoversVolume vs Historical Avg (%)

Most Up Most Down Most Up

The Tale of The Tape: 30 Year Treasury Yield (Left Axis) vs Front Month Copper (Right Axis)

228.50

229.00

229.50

230.00

230.50

231.00

1,928

1,933

1,938

1,943

1,94830 Year Treasury Yield (Left Axis)

Front Month Copper (Right Axis)

Page 7 of 8 The Closer 9/22/15 BespokePremium.com

For Personal Use Only—Do Not Forward

Sentiment Indicator vs Historical One Week Two Weeks One Month

CBOE Call Volume 1.3 ## -1.2 0.08 -0.11 -0.12

NYSE Up vs Total Volume (%) 46.5 ## -0.6 0.21 0.12 -0.13

Nasdaq Up vs Total Volume (%) 48.7 ## -0.3 0.13 0.12 0.37

Index vs Equity PC Ratio 0.9 ## 1.0 0.31 0.29 0.03

VIX 50-Day ROC (%) 61.4 ## 1.6 -0.61 -0.13 0.12

VIX 10-Day ROC (%) -9.9 ## -0.6 0.07 0.34 0.18

Investors Intelligence Bullish (%) 26.8 ## -2.7 0.59 1.18 2.08

Investors Intelligence Bearish (%) 26.8 ## 0.1 0.10 0.40 0.94

Inv Intell. Bull Bear Spread 0.0 ## -1.5 0.10 -0.90 -1.84

AAII Bullish (%) 33.3 ## -0.7 0.03 -0.15 -0.14

AAII Bearish (%) 29.1 ## -0.4 0.11 0.12 0.08

AAII Bull Bear Spread 4.1 ## -0.2 0.02 0.49 0.21

Overall Sentiment ## -0.4 0.10 0.12 0.10

Technical

S&P 500 10-Day Avg. Spread (%) -1.1 ## -0.6 0.35 0.46 0.28

S&P 500 50-Day Avg. Spread (%) -3.5 ## -1.0 0.20 0.15 0.04

S&P 500 200-Day Avg. Spread (%) -6.0 ## -0.9 0.20 0.32 0.70

S&P 500 Monthly ROC (%) 4.0 ## 0.8 0.08 0.11 0.20

S&P 500 Weekly ROC (%) -1.8 ## -0.8 0.31 0.37 0.22

S&P 500 Quarterly ROC 1 (%) -7.9 ## -1.2 -0.22 -0.66 -1.26

Group 10-Day A/D Line 8.0 ## 0.0 -0.02 -0.03 -0.19

Group 50-Day A/D Line -60.0 ## -1.1 0.64 0.82 1.55

S&P 500 10-Day A/D Line -280.0 ## -0.5 0.23 0.11 0.06

S&P 500 50-Day A/D Line -1204.0 ## -1.1 0.44 0.52 1.25

NYSE TRIN Index 1.3 ## 0.5 0.07 0.29 0.58

Overall Technical ## -0.5 0.20 0.29 0.22

Fundamental/Monetary

Corporate Spreads (10-Day ROC) -1.0 ## -0.1 0.26 0.20 0.55

Corporate Spreads (50-Day ROC) 18.0 ## 0.4 0.07 0.17 0.20

High Yield Spreads (10-Day ROC) 13.0 ## 0.3 0.07 0.01 0.47

High Yield Spreads (50-Day ROC) 84.0 ## 0.6 0.22 0.34 0.48

S&P 500 P/S Ratio 1.7 ## 1.1 -0.06 -0.36 -1.16

S&P 500 P/E Ratio 17.2 ## -0.1 0.37 0.33 0.24

S&P 500 P/B Ratio 2.9 ## 0.7 0.21 0.25 0.59

Yield Curve (50-Day ROC) -0.5 ## 0.0 -0.03 -0.04 -0.08

Yield Curve (10-Day ROC) -1.9 ## -0.1 0.05 0.18 0.54

Overall Fundamental ## 0.3 0.07 0.18 0.47

Bottom Line ## -0.3 0.10 0.17 0.20 Average S&P 500 Performance (All Days) 0.10 0.19 0.38

Average S&P 500 Performance (%)Current Level

Direction

Bespoke Market Timing Model: 9/22/15

Neutral Bearish Bullish

Page 8 of 8 The Closer 9/22/15 BespokePremium.com

For Personal Use Only—Do Not Forward

Sentiment Indicator vs Historical One Week Two Weeks One Month

CBOE Call Volume 1.7 0.6 0.6 0.13 -0.22 -0.44

Overall Sentiment 0.3 0.3 0.14 0.16 0.28

Bottom Line 0.3 0.3 0.12 0.21 0.27

Average S&P 500 Performance (All Days) 0.12 0.24 0.50

Current Level Average S&P 500 Performance (%)

Direction

The Bespoke Market Timing Model is a compilation of some widely (and not so widely) followed market indicators. While

most investors have one or two indicators they rely on, we all recognize that no indicator by itself is correct all of the time.

With this in mind, we set out to create a series of indicators from multiple disciplines in order to see what the 'crowd' of

indicators are telling us. Just as no individual is bigger than the market, we contend that no single indicator is more accurate

at forecasting the market than the sum of them all. What follows below is an explanation of the various fields in our report.

Indicator: Current level of the given indicator. In this example, CBOE call volume is 1.7 times CBOE put volume.

Direction: Change in the indicator (positive or negative) over the last week. In this example, calls relative to puts have

increased during the last week.

vs Historical: This field measures the distance in standard deviations that the indicator is currently at versus its average

over the last five years. In the above example, the volume of calls relative to puts is 0.6 standard deviations above its histori-

cal average.

Indicator: Current level of the given indicator. In this example, CBOE call volume is 1.7 times CBOE put volume.

Average S&P 500 Performance: This field displays the average performance of the S&P 500 following previously occasions

when the indicator was at similar levels to the present. Values highlighted in green indicate the two indicators for that

group which are predicting the biggest gains, while indicators highlighted in red highlight the indicators which are signaling

the most negative returns going forward.

Overall Scores: Averages all the indicators for a given category. In the example above, overall sentiment is 0.3 standard

deviations from its long-term average. At similar levels in the past, the S&P 500 has gone up an average of 0.14% over the

next week, 0.16% over the next two weeks, and 0.28% over the next month.

Bottom Line: This line shows the average of all the indicators in the study. In the example above, the aggregate level of

all the indicators is currently 0.3 standard deviations above the historical average, and based on prior experiences, the S&P

500 has gone up an average of 0.12% in the next week, 0.21% in the next two weeks, and 0.27% in the next month. Values

highlighted in red indicate returns that underperform the S&P 500 over the entire period covered (regardless of the indica-

tor level), while green highlights indicate that they outperformed the overall average S&P 500 performance.

Average S&P 500 Performance (All Days): This line measures the average historical performance of the S&P 500 over all

periods for one week, two week, and one month time frames. These levels are then compared to the average level the

indicators are predicting.in the next two weeks, and 0.27% in the next month. Values highlighted in red indicate returns

that underperform the S&P 500 over the entire period covered (regardless of the indicator level), while green highlights

indicate that they outperformed the overall average S&P 500 performance.