us lodging industry overview - hotelnewsnow.com review ... data is for upper tier hotels only (lux...

TRANSCRIPT

1

US Lodging Industry Overview

Jan D. Freitag

Senior Vice President

2

www.hotelnewsnow.com Click on “Hotel Data Presentations”

3

Agenda • Total US Review

• Chain Scale Review

• Segmentation Review – Group & Transient

• 2012 / 2013 Forecast

• Channel Study Highlights

4

Total US Review

5

Supply / Demand Imbalance Drove Last 12 Months

% Change

• Room Supply* 1.8 bn 0.4% • Room Demand* 1.06 bn 4.4% • Occupancy 60.5% 4.0% • A.D.R. $102 3.9% • RevPAR $62 8.0% • Room Revenue* $109 bn 8.4%

12 Months Ending March 2012, Total US Results * All Time High

6

Q1 2012: Highest Demand - EVER

(245 Million Rooms Sold)

7

-8

-4

0

4

8

1990 2000 2010

Supply Demand

Demand Growth Expected To Revert To Mean. Supply Not An Issue

-6.9%

-0.9%

- 4.7%

*Total US, Supply & Demand % Change, 12 MMA 1/90 – 3/12

8.0%

4.4%

8

-10

-5

0

5

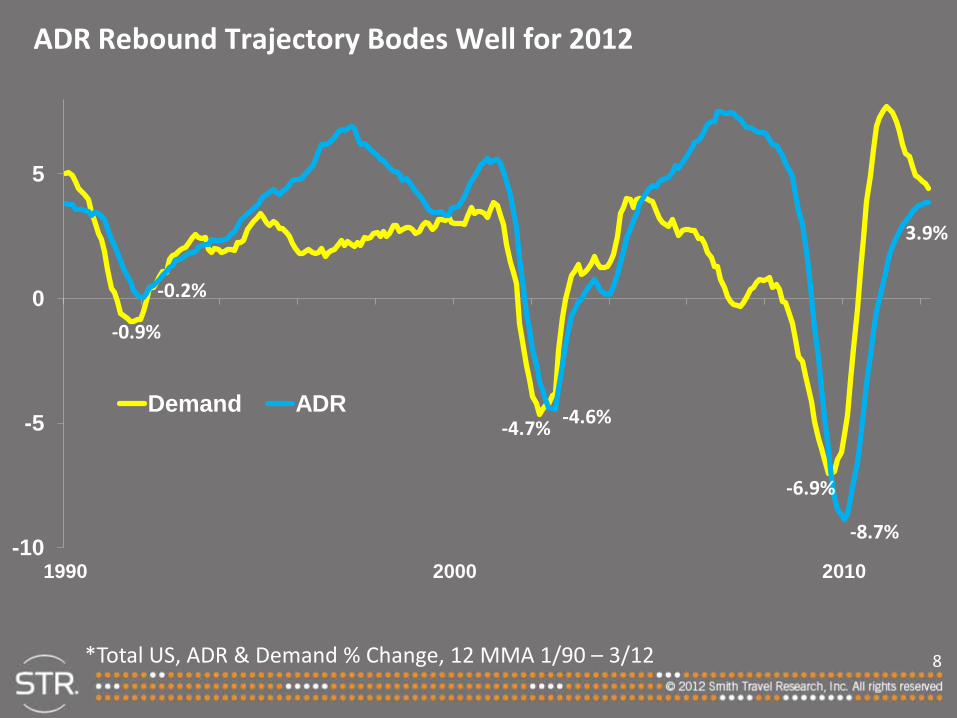

1990 2000 2010

Demand ADR

ADR Rebound Trajectory Bodes Well for 2012

-6.9%

-4.7%

-0.9%

-4.6%

-0.2%

-8.7%

3.9%

*Total US, ADR & Demand % Change, 12 MMA 1/90 – 3/12

9

ADR Discounting at Twice The Speed of ADR Increases

95

100

105

110

2008 2009 2010 2011

*Total US, ADR $, 12 MMA 2007 - 2011

Apr ‘10 $97

Sept ‘08 $108

Dec ‘11 $102

+4.6%

-10%

19 Months

19 Months

10

3.1

2.6

3.9

2.9

4.1

3.7 4.0

3.5

4.1 4.0 4.4

3.5 3.9 4.0 3.9

Jan-11 Jul-11 Jan-12

* Total US, ADR $ % Change, by Month, 1/11 – 3/12

ADRs Are Growing (But Comps Get More Difficult)

11

Do You Really Know Your Competitors?

National Nameback %: ??%

* % of hotels that use hotels in their compset which have named them Source: STR Analytics

12

Do You Really Know Your Competitors?

National Nameback %: 45%

* % of hotels that use hotels in their compset which have named them Source: STR Analytics

13

Chain Scale Review

14

Q1: Strong Demand Growth, Supply Not An Issue

-0.9

0.2

1.5

3.2 3.7

4.9

Luxury Upper Upscale Upscale

Supply

Demand

*Supply / Demand % Change, by Scale, Q1 ‘12

15

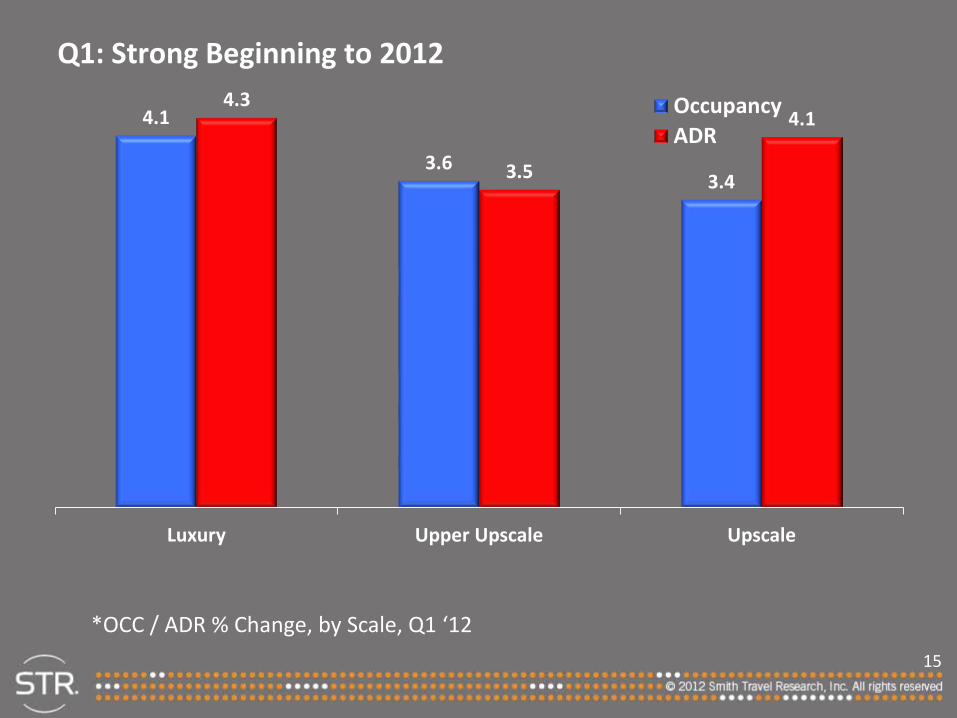

Q1: Strong Beginning to 2012

4.1

3.6 3.4

4.3

3.5

4.1

Luxury Upper Upscale Upscale

Occupancy ADR

*OCC / ADR % Change, by Scale, Q1 ‘12

16

Upper End Sells 7 out of 10 Rooms Every Night

72.5

70.5 69.6

71.7 69.9 70.1

Luxury Upper Upscale Upscale

2007 12 Months end 3/12

*Absolute OCC %, by Scale, 2007 & 12 Months ending 3/12

17

ADR Growth Is Strong – But Not Strong Enough (...yet)

$293

$159

$121

$264

$149

$113

Luxury Upper Upscale Upscale

2007 12 Months end 3/12

*Absolute ADR $, by Scale, 2007 & 12 Months ending 3/12

18

Segmentation Review

19

Transient Demand Breaks Records, But....

10

12.5

15

17.5

20

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2007 2011 2012

*Transient Demand in Millions of Rooms; 2007, 2011, 2012 Data is for upper tier hotels only (LUX & UU chains, & Upper Tier independents)

Mill

ions

20

… Transient ADR Still Lags 2007 Results

$140

$150

$160

$170

$180

$190

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2007 2011 2012

*Transient ADR $, 2007, 2011, 2012 Data is for upper tier hotels only (LUX & UU chains, & Upper Tier independents)

21

5.3

4.6

6.4

5.4 5.9

5.1 5.0

3.7

4.7 4.3

4.6

3.7 3.8 3.4

4.0

Jan-11 Apr-11 Jul-11 Oct-11 Jan-12

*Transient ADR % by Month, 1/11 – 3/12 Data is for upper tier hotels only (LUX & UU chains, & Upper Tier independents)

We Expect Transient ADR Growth To Continue

22

Group Demand Has Not Changed Over Time, But…

4

6

8

10

12

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Mill

ions

2007 2011 2012

*Group Demand in Millions of Rooms, 2007, 2011, 2012 Data is for upper tier hotels only (LUX & UU chains, & Upper Tier independents)

23

… Group ADRs Still Depressed (& Could Dampen Future Absolute ADRs)

$130

$140

$150

$160

$170

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2008 2011 2012

*Group ADR $, 2008, 2011, 2012 Data is for upper tier hotels only (LUX & UU chains, & Upper Tier independents)

24

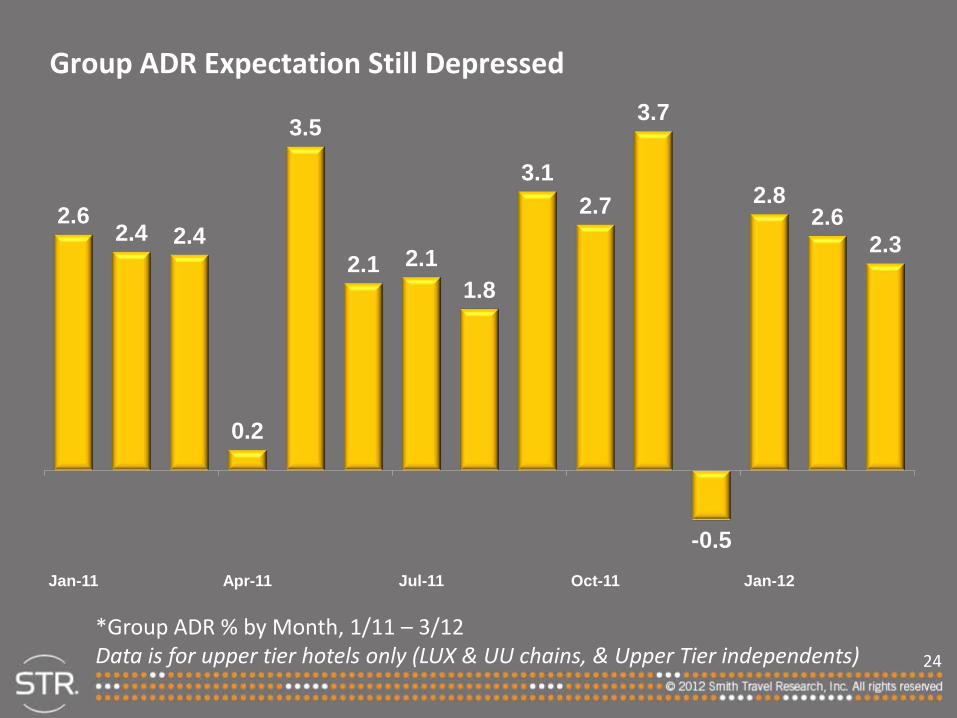

2.6 2.4 2.4

0.2

3.5

2.1 2.1 1.8

3.1 2.7

3.7

-0.5

2.8 2.6

2.3

Jan-11 Apr-11 Jul-11 Oct-11 Jan-12

*Group ADR % by Month, 1/11 – 3/12 Data is for upper tier hotels only (LUX & UU chains, & Upper Tier independents)

Group ADR Expectation Still Depressed

25

2012 / 2013 Forecast

26

Rooms Pipeline Still Not An Issue in 2012

Phase March 2012 March 2011 Dec 2007

In Construction 60 50 211 “Planned Pipeline” 233 274 204

Active Pipeline 293 324 415

*Total US Pipeline, in ‘000s of rooms, by Phase by Year Planned Pipeline includes projects in Final Planning and Planning phases Source: STR / McGraw-Hill Construction Dodge

27

U/C Pipeline By Selected Markets

Market Projects Rooms

Chicago 6 1,300

Miami 9 1,200

Nashville 4 1,400

NYC 50 7,600

Orlando 15 3,700

Washington, DC 12 2,700

28

Total United States Forecast 2012 / 2013 Key Performance Indicator % Change 2012

Forecast 2013

Forecast

Supply 0.5% 1.1%

Demand 2.0% 1.8%

Occupancy 1.5% 0.7%

ADR 4.0% 4.6%

RevPAR 5.5% 5.4%

29

Total United States Chain Scale Key Performance Indicator Outlook 2012F by Chain Scale

Chain Scale Occupancy

(% chg) ADR

(% chg) RevPAR (%chg)

Luxury +2.6% +5.1% +7.9%

Upper Upscale +1.5% +4.2% +5.7%

Upscale +2.3% +4.6% +7.1%

Total United States 1.5% 4.0% 5.5%

30

Channel Study Highlights

31

OTA Revenue: 8% Of Revenue, 88% Of Our Conversation

3.2

7.9 8.0 4.7

21.7

45.5

3.6

8.7 8.0 5.2

22.2

47.7

4.2

10.1 9.0 6.2

22.6

52.1

OTA Brand.com CRS/Voice GDS Prop Direct/Other Total US

2009 2010 2011

*Total rooms revenue in billions $, by channel, June YTD 2009 - 2011

32

Wide ADR Variance Between OTA and GDS Channel

75

109

128 127

89

99

73

110

127 126

87

97

74

115

127 128

89

101

OTA Brand.com CRS/Voice GDS Prop Direct/Other Total US

2009 2010 2011

*ADR $, by channel, June YTD 2009 - 2011

33

Wide ADR Variance By OTA Business Model

97

78

55

90

70

54

97

75

56

Retail Merchant Opaque

2009 2010 2011

*ADR $, by OTA channel, June YTD 2009 - 2011

34