usaid libya public financial management (bab al ta …

TRANSCRIPT

USAID LIBYA PUBLIC FINANCIAL MANAGEMENT (BAB AL TAMKEEN) PROGRAM QUARTERLY REPORT FY 2020 Quarter 2 Report January 1, 2020 – March 31, 2020

The Pragma Corporation Principal Contact: Paul Davis 116 East Broad Street Falls Church, Virginia 22046 DISCLAIMER: This report was produced for review by the United States Agency for International Development. It was prepared by the Libya Public Financial Management Program, implemented by The Pragma Corporation. The author’s views expressed in this publication do not necessarily reflect the views of the United States Agency for International Development or the United States Government.

i | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

TABLE OF CONTENTS

Acronyms ............................................................................................................................................................ i

Executive Summary .......................................................................................................................................... 1

Component 1: Public Financial Management .............................................................................................. 1

Component 2: Reform Libya’s Electricity Sector ...................................................................................... 9

Component 3: Improve Business Environment ...................................................................................... 12

Self Reliance Grants ...................................................................................................................................... 14

Communications/outreach .......................................................................................................................... 15

Monitoring, Evaluation, and Learning (MEL) ............................................................................................ 15

LIST OF ANNEXES

ANNEX 1: LPFM PARTNER MUNICIPALITIES

ANNEX 2: MONITORING, EVALUATION, AND LEARNING (MEL) AND PITT TABLE

ANNEX 3: SUCCESS STORIES

ANNEX 4: ILLUSTRATIVE TRAVEL PLAN

ANNEX 5: ANALYTICAL REPORTS

5.1 - Wage Bill Analysis Report

5.2 - Exchange rate management report

5.3 - Technical note on the impact of the oil blockade

5.4 - Budget Execution Report

5.5 – Macro-fiscal Development Monthly Reports (January-March 2020)

i | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

ACRONYMS AmCham American Chamber of Commerce in Libya BEE Business Enabling Environment CBL Central Bank of Libya CoA Chart of Accounts COP Chief of Party CPI Consumer Price Index CSO Civil Society Organization CVA Customs Valuation Agreement DB Doing Business EE Energy Efficiency EPHS Essential Package of Primary Healthcare Services ES Electricity Sector FX Foreign Exchange GATT General Agreement on Tariffs and Trade GDP Gross Domestic Product GDSC Government Decision Support Center GECOL General Electricity Company of Libya GNA Government National Accord GoL Government of Libya GTEL GECOL Telecom GTZ German Agency for Technical Cooperation HCLA High Council for Local Administration HR Human Resources ICT Information Communications Technology IMF International Monetary Fund LBC Libyan Business Council LED light-emitting diode LESP Libya Economic Stabilization Program LLIDF Libyan Local Investment & Development Fund LPFM Libya Public Financial Management LWBC Libyan Women in Business Committee LYD Libyan Dinar MC Municipal Councils MEG Middle East Economic Growth MEL Monitoring, Evaluation, and Learning METAL Monitoring and Evaluation for Tunisia and Libya MF Team Macro-Fiscal Team MFU Macro Fiscal Unit MoEd Ministry of Education MoEcon Ministry of Economy MoF Ministry of Finance MoH Ministry of Health MoJ Ministry of Justice MoLG Ministry of Local Government

ii | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

MoP Ministry of Planning NEEAP National Energy Efficiency Action Plan NOC National Oil Corporation OPGW Optical Ground Wire OTJ On-The-Job Training OSR Own Source Revenue PC Presidential Council PE Primary Education PEFA Public Expenditure and Financial Accountability PFM Public Financial Management PHC Primary Health Care PIP Public Investment Program PITT Performance Indicator Tracking Table PPD Public-Private Dialogue PPP Public-Private Partnership PSAP Private Sector Advocacy Platform REMO Regional Education Monitoring Offices SME Small and Medium Enterprises SPS Sanitary and phytosanitary SWM Solid Waste Management TBT Technical Barriers to Trade TC Technical Committee TFA Trade Facilitation Agreement TFESR Task Force for Electricity Sector Reforms TPM Third-Party Monitoring TWG Technical Working Group UNDP United Nations Development Programme USAID United States Agency for International Development WTO World Trade Organization VTC Video Teleconference Center

1 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

EXECUTIVE SUMMARY USAID’s Libya Public Financial Management (LPFM) Program - known as “Bab Al Tamkeen” – is a 5-year initiative (currently with $14.9 million in funding over two years) designed to address critical macro-fiscal, electricity sector, and enabling environment constraints facing the post-Arab Spring Libyan economy.

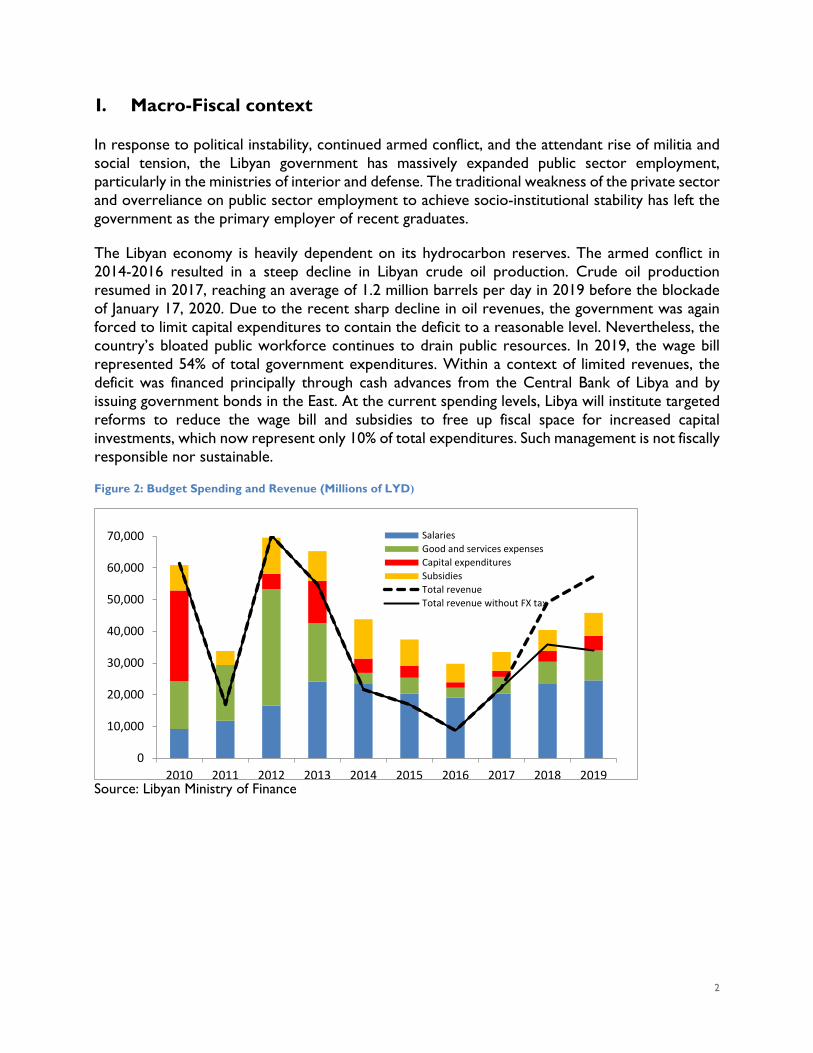

Public Financial Management (PFM). The PFM Component continued to effectively implement its activities at the subnational level, where the team deepened the capacity of municipalities to develop own source revenue (OSR) budgets that prioritize public service delivery and to identify and forecast their OSR resources. The PFM team also made progress with its municipal pilot programs in the areas of solid waste management (SWM), primary health care (PHC), and primary education (PE). The PFM team also developed a regulation on local revenue that is in line with best practice. At the national level, the Macro-Fiscal (MF) team increased the Macro-Fiscal Unit (MFU) capacity to track and analyze macro-fiscal trends. Furthermore, the MFU undertake related policy-relevant research activities to collate and analyze macro-fiscal data; and to produce critically important, regular, budget-relevant reporting documents. As a result, MFU staff produced a rigorous year-end budget execution table and monthly fiscal reports that are now published on the MoF’s website and Facebook page. The team also supported the MFU in preparing analytical reports on the wage-bill and the exchange rate regime.

Electricity Sector (ES). The ES Team worked with the technical committees of the Task Force for Electricity Sector Reforms (TFESR) on the finalization of an electricity sector decree that would establish an independent electricity sector regulator and enable competition and the unbundling of GECOL. During the reporting period, the ES Team met with GECOL Chairman, Abdelmajeed Hamza, in Tunis and provided him with an overview of the ES team’s work plan for the next two years. The Chairman agreed on the need to pursue the reforms that are the objective of the team’s work plan, including the adoption of the ES decree. The chairman also agreed with the ES Team’s goals of promoting the implementation of tariffs that will move GECOL closer to cost recovery, advancing the unbundling and restructuring of GECOL, and introducing measures to enable private sector electricity generation.

Business Enabling Environment (BEE). The team organized three focus group discussions with Libyan businesses. Two were co-sponsored by the Libyan Business Council (LBC) for business representatives from Tripoli and Sabha. The third was co-sponsored by the Misrata Chamber of Commerce for its local members. The BEE Team also held individual interviews with SMEs in these cities. Using the results of its legal/regulatory assessment and the information obtained from the focus groups and interviews, the team updated its list of priority reforms. It began developing proposed reforms in the areas of access to credit and minority shareholder rights. The BEE team also prioritized competition law and public-private partnerships (PPP), which businesses identified as priorities. The BEE Team also completed its assessment following the conformity of Libya’s foreign trade regime with eight core WTO agreements. The BEE Team prepared recommendations to improve Libya’s conformity with these agreements, which are being integrated into the WTO Accession Action Plan that the BEE Team plans to deliver to the GoL during the first half of the third quarter.

COMPONENT 1: PUBLIC FINANCIAL MANAGEMENT The PFM Component continued to effectively implement its activities at the subnational level, where the team deepened the capacity of municipalities to develop OSR budgets that prioritize public service delivery and to identify and forecast their OSR resources. The PFM team also made progress with its municipal pilot programs in the areas of solid waste management (SWM), primary health care (PHC), and primary education (PE). The PFM team also developed a regulation on local revenue that is in line with best practice. Also, on February 4, USAID approved revisions to the LPFM Workplan, which

2 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

authorized LPFM to work across 44 total municipalities during Year 1, including a significant number of non-GNA municipalities.1

At the national level, the Macro-Fiscal (MF) team – through formal and on-the-job (OTJ) training – increased the capacity of the MFU to track and analyze macro-fiscal trends. Furthermore, the MFU team undertake related policy-relevant research activities, to collate and analyze macro-fiscal data, and to produce critically important, regular, budget-relevant reporting documents. As a result, MFU staff produced a rigorous year-end budget execution table and monthly fiscal reports that are now published on the MoF’s website and Facebook page. The team also supported the MFU in preparing analytical reports on the wage-bill and the exchange rate regime, with suggested adjustments that could improve macroeconomic stability and diversification.

Fiscal Decentralization & Subnational PFM

Developing Own Source Revenue Budget Capacity at the Municipal Level

The PFM Component continued to effectively implement its activities at the subnational level, where the program deepened the capacity of municipalities to develop OSR budgets that prioritize public service delivery. Through technical and OTJ training, the PFM Team also expanded the capacity of municipalities to identify and forecast their OSR resources. The PFM team also developed a regulation on local revenue that is in line with best practice.

For OSR budget development, the Team adopted a phased approach to ensure sustainable learning throughout the process. Municipalities applied a template that was customized to municipal needs, and that included detailed local revenue and expenditure classifications in accordance with a coding system. The PFM Team then fine-tuned those procedures and improved the municipalities’ budgetary allocation systems and objectives for revenue and expenditure items. The team developed a municipal chart of accounts (CoA) that was based on the Ministry of Finance's (MoF’s) CoA but adjusted to make it more suitable to municipalities. These improvements were complemented by integrating more realistic budget justification narratives into the budget document for each revenue/expenditure category.

The PFM team also provided targeted technical and OTJ training that helped develop local capacity to identify and forecast OSR in 21 original LESP municipalities. During the quarter, OSR budgets were approved by 14 of the concerned mayors and submitted to the Ministry of Local Government (MoLG). The mayors of two municipalities approved the OSR budgets, which are now being submitted to MoLG. In two other municipalities, the OSR budgets are still under mayoral review. The remaining three municipalities are developing their OSR budgets. OSR budgets that are submitted to MoLG require the approval of both MoLG and MoF. Once approved, MoF can provide the municipalities with their budget allocation. The approval of submitted OSR budgets is expected after the promulgation of the Regulation on Local Revenue.

1 While the re-intensification of conflict and the COVID-19 crisis have effectively restricted major programmatic interventions in Quarter 2 to the original set of 22 LPFM-supported municipalities, it is expected that major outreach activities across the network of new municipalities will be undertaken during Quarters 3-4. Further expansion of pilot municipalities in the SWM, PHC, and PE spheres is also expected to occur over this timeframe.

3 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

The PFM Team held a workshop on February 13 in Tripoli for the OSR budgeting staff of 14 partner municipalities.2 Six of the attending municipalities were more advanced, having already prepared draft 2020 OSR budgets and estimates (Kabaw, Khoms, Misurata, Zuwarah, Yafran, and Wadi Albwanies). At the workshop, the team worked with these six municipalities to finalize their OSR budgets, which were submitted to the MoLG later in February.

The other eight attending municipalities participated in the training to learn from the experience of the six more advanced partner municipalities. During the workshop, the PFM recommended that the MoLG issued follow-up letters on February 23 to the 14 attending municipalities to request their medium-term budgets, which include the investments needed to improve the infrastructure for critical municipal services; e.g., education and health, the focus of the Government of Libya (GoL) decentralization policy.

Enhancing the legislative foundations for municipal own-source revenues

In late December of 2019, the High Council for Local Administration (HCLA) provided the team with a draft of a “Regulation on Local Revenue.” The draft regulation was intended to advance decentralization by authorizing municipalities to collect and budget various types of OSR. The team reviewed the draft regulation and identified numerous drafting issues and inconsistencies with best practices. The team developed 25 pages of comments suggesting major revisions and provided these to the HCLA. Three meetings were held with the HCLA lawyers in February to review the team’s comments. The HCLA lawyers then asked the team to prepare an entirely new draft. In early March, the team delivered its 30-page draft regulation to the HCLA. The team and the HCLA lawyers held extensive discussions to clarify issues and discuss modifications. In mid-March, the agreement was reached on a draft that was far more in line with best practice and municipal financing needs than the original draft. The HCLA then submitted the draft to the Minister of MoLG, who delivered the draft to the Presidential Council (PC) on March 30. It is now being reviewed by the MoF. The regulation remains a high priority for the Government National Accord (GNA) and is expected to be finalized and promulgated by the end of April.

Primary Health Care (PHC)

In early January, the team – in collaboration with representatives of MoLG and Ministry of Health (MoH) – finalized the PHC operational plan. The team followed the completion of the plan with a workshop on January 21 to promote buy-in from both ministries and representatives of the municipalities of Tripoli

2 The other eight municipalities could not travel to Tripoli for security reasons and will receive training in April and May 2020, by VC if needed.

Representatives from 14 municipalities and the MoLG, MoF, and HCLA attend a workshop on OSR Budgeting in Tripoli on February 13

4 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

Center, Misurata, Gharyan, Sabha, and South Alzawiya. Within the week following the workshop, the plan was approved by both ministries. A central element of the plan is the establishment of a municipality-specific essential package of primary healthcare services (EPHS) that includes the basic PHC services of greatest importance to citizens of the concerned municipality. The team also carried out the basic costing of the EPHS for select clinics within Tripoli Center. The team assisted the pilot municipalities in establishing their PHC task forces with staff from both the municipality and the MoH regional health directorate. In February, the PHC team expanded this work to the PHC Centers of Nofliyeen, Fashloum, and Shuhada Al Mansoura. The PHC team worked with the MoLG to identify the departments within each pilot municipality that will serve on the task force that is to implement the PHC operational plan. The pilot municipalities and the MoLG then selected the specific staff from the concerned departments to be assigned to the task force. Brega, a non-GNA municipality, sent the PHC Team a letter committing to establish a task force to work on the piloting of PHC services.

The MoH agreed with the PHC team’s proposal to establish health offices in certain municipalities to replace the concerned Regional Health Directorates. The PHC team also met with the Department for Regional Health Services Directorates to clarify the respective responsibilities of the directorates and the municipal health offices. Because establishing the municipal health offices requires a legal foundation, the team held several meetings with the Director of the Legal Office of the General Secretariat of the HCLA, who confirmed that the PC would need to issue a decree formalizing the role of municipal health offices.

In early March, the PHC team identified the data that will be needed to develop a public investment plan (PIP) for each pilot municipality. The team started the data collection at the PHC centers of Nofliyeen and Fashloum in Tripoli Center. The PHC visited these facilities on several occasions to assess their infrastructure status and to discuss with staff the availability of vital inputs, including the basic medical equipment as per the list developed by the team. The PIP analysis for the centers in Tripoli Center also covers the infrastructure needed by the clinics to deliver the basic package of services. Once completed, the analysis will be used to conduct similar analyses for the PHC centers in the other pilot municipalities.

Due to the COVID-19 pandemic, in mid-March, the PC issued instructions requiring civil servants to work from home, which has resulted in the suspension of the pilot training program. Consequently, the PHC team is developing a plan for the use of video teleconference centers (VTCs) to conduct the training. The PHC team is committed to implementing its work plan while tailoring its objectives and targets to respond to COVID-19 needs of municipalities at the PHC level. The team is reviewing the measures adopted by other countries to fight the pandemic at the PHC level.

Patient data manual registration process at Nofliyeen PHC clinic in Tripoli Center

5 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

Solid Waste Management (SWM)

During the quarter, the SWM Team worked at both the national level (with the PC, MoLG, and MoF) and the municipal level on a range of SWM issues. In January, the team followed up with the MoLG on the measures that had been taken to identify locations for temporary and permanent landfills. The team and MoLG discussed the operations of the MoLG’s newly formed committee, which was tasked to identify appropriate locations. Following the advice of the SWM Team, the PC also established a new committee tasked with coordinating all SWM measures. However, progress on cross-ministry coordination has so far been limited due to the lack of funds to procure SWM services and the impact of COVID-19.

The SWM team also worked to operationalize the SWM strategy at the nine legacy LESP municipalities by (1) assisting the Municipal Councils (MCs) to introduce rigorous SWM operational procedures; (2) assisting the MCs to take concrete steps towards implementing

transparent, competitive procurement of SWM collection and disposal services; and, (3) compiling the data needed to prepare 2021 budgets on SWM expenditures.

To institutionalize the municipal role in improving SWM services, the SWM team proposed that each municipality formally establish an SWM Working Group (SWMWG) to take charge of ensuring implementation of the SWM operational procedures. The SWM Team also provided the municipalities with the necessary procurement documentation. For some municipalities, such as Khoms, the team discussed the establishment of collection zones based on the daily volume of solid waste produced and the planned collection routes and transfer activities. Based on the SWM Team’s recommendation, Surman designated its General Sanitation Department as the organizer of all SWM operations in the municipality.

The team assisted Tripoli Center to finalize two open SWM procurements, which resulted in the award of two separate contracts in January. One contract exceeded LYD 5 million and therefore required approval by MoF’s Control Office, which has yet to be given. The other contract was less than LYD 5 million; however, the parties have delayed performance due to the failure of the MoLG and MoF – contrary to their prior commitments – to make the funding for the contracts available. The SWM team is working with the MoLG to advocate that the funding be included in the GoL’s 2020 Financial Arrangements.

The lack of funding for SWM procurements affects all SWM pilot municipalities. The interruption in the flow of oil revenue since January has caused the MoF to limit municipal expenditures. The LPFM Team has been making a concerted effort - using its contacts at the MoF - to arrange a meeting with the Minister, where the funding of SWM procurements will be a discussion point. The meeting, initially planned for March, was postponed due to intensification of the conflict and the GoL’s focus on COVID-19. These discussions are expected to be renewed early in Quarter 3.

At the same time, the SWM Team is working with all SWM municipalities to ensure they are prepared to launch SWM procurements as soon as the funding issue is resolved. As an alternative approach, the team is working with pilot municipalities and the MoLG to modify their OSR budgets to provide the needed funding as soon as the Regulation on Local Revenue is promulgated. The SWM team also

A GP Nofliyeen PHC clinic in Tripoli Center examines an ultrasound machine—photo taken as part of PIP data collection.

6 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

continues to dialogue with other donor programs (e.g., UNDP, GTZ) that may have funding to support municipal SWM activities.

The SWM team assisted the municipalities of Tripoli Center, Souq Al Jumma, Khoms, and Surman in compiling the data needed to prepare a 2021 budget on SWM expenditures. In Q3, the team will replicate this work in the five other SWM pilot municipalities. The SWM Team has already identified and started collecting the data for SWM public investment plans (PIPs) for the nine LESP municipalities. The main investments would be upgrading the available landfills by constructing sanitary-based space within the landfill footprint currently used as open dumpsites, while also considering developing transfer stations. The upgrade would cover the free remaining airspace in the landfills to help provide operational capacity, where applicable.

The LPFM advisors will determine the cost structure of these investments and will help compute the cost-benefit analysis parameters for the proposed public investments. Major types of data being analyzed include annualized solid waste quantities, the target citizens within municipalities who are the main beneficiaries, the solid waste collection vehicles, and the operational expenses that will complement the capital expenditures.

Primary Education (PE)

During the quarter, the PE Team and the MoEd identified five senior MoEd officials to work on the PE Technical Working Group (TWG). The PE Team then began assisting the TWG with the development of a three-year PE operational plan, which has required intensive collaboration between the Team and the TWG members, who previously had very limited familiarity with decentralized education systems. The PE Team worked tirelessly on orienting the TWG on the split between MoEd’s centralized role at the policy level and the administrative responsibilities to be mobilized at the pilot municipalities. Through intensive working sessions with the TWG, the PE team successfully advanced the understanding of MoEd officials on the options and approaches suitable for educational decentralization in Libya. This led to MoEd’s approval in January for the initiation of the PE pilots.

The PE Team and the TWG held several working sessions to assign tasks among TWG members and to ensure a division of labor between the TWG and the relevant Regional Education Monitoring Offices (REMOs). The REMOs play an important role in implementing MoEd directives at the subnational level, and the PE Team has identified them as key stakeholders in the PE operational plan. The Team then held a planning meeting in March involving the TWG and the REMOs. It was agreed that the team and the TWG will: (1) develop a legislative framework to govern the relationship between the REMOs and municipalities; (2) establish a list of prioritized education services; (3) define the required capacities of all staff who will occupy key positions under the operational plan.

Following up on its March 9 operational planning meeting with the PE TWG and representatives from the REMOs, the PE Team developed and distributed a questionnaire to the REMOs aimed at obtaining their input and assistance in determining the primary education services best suited for transfer to municipalities. The TWG is completing the process of collecting the questionnaires and, with the PE Team’s assistance, will expeditiously develop a targeted analysis of the results.

As part of outlining the sectoral PIP needs, the PE Team and the TWG agreed to update the “Nationwide School Assessment,” a study conducted by the Ministry of Education in 2012. Even though it is a somewhat dated analysis, the study currently provides the only baseline of the sector’s key indicators, and a 2012 assessment of the sector’s infrastructure and facilities. In parallel, the PE Team will target upgrading the schools’ infrastructure to improve the quality/coverage of cost-efficient PE services.

The PE Team also undertook the first-round mapping of 35 Civil Society Organizations (CSO)s that are potentially active in the area of PE, which included preliminary capacity assessment of these CSOs in the

7 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

10 PE Pilot municipalities in terms of their potential roles in monitoring and evaluating schools. Out of the 35 CSOs, the PE team was able to reach seventeen and collected information about the type of activities they engage in and their target beneficiaries. The PE Team also identified each CSO’s local and international counterparts, and, in some cases, the donors that fund their activities.

The PE Team was planning to hold a roundtable discussion in March for the CSOs and the TWG to confirm oversight/social accountability roles that could be assigned for CSOs within the PE operational plan. However, the session was canceled due to the current GoL measures restricting group activities to fight the COVID-19 pandemic. The PE Team will continue its efforts to map out CSOs that would be the suitable partners in improving the PE services at the subnational level, by seeking assistance from the REMOs to open up communication channels with potential CSOs and unlock information prospects. The Team will also work intensively with MoLG to identify the most feasible authority transfer opportunities in light of new municipal requirements in the wake of the COVID-19 pandemic.

National Level LPFM Engagement: MFU Capacity Development, Studies & Analysis For Use By Libyan Decision-Makers During Quarter 2, the LPFM Macro-Fiscal (MF) team – through technical support and formal and OTJ training – increased the capacity of the MFU to track and analyze macro-fiscal trends, to undertake related policy-relevant research activities, to collate and analyze macro-fiscal data, and to produce critically important, budget-relevant reporting documents. As a result, MFU staff produced a rigorous year-end budget execution table and monthly fiscal reports that are now published on the MoF’s website and Facebook page. The team also supported the MFU with preparing rigorous and practical analytical reports on the wage-bill and the exchange rate regime. Additionally, the MF team assisted MFU in developing an important technical note on the current and prospective impact of the blockade on budgetary performance. LPFM and MFU leadership also agreed on an MFU training program for the remainder of Year 1, including a rigorous curriculum for the MoF’s Institute for Public Financial Management.

The MF team worked to build the MFU’s capacity in various areas, particularly on core macro-fiscal issues and the four basic macroeconomic sectors: the system of national accounts, presentation of supply and use tables, input-output analysis, and financial programming. These sectors were used to assess the impact of and the potential policy responses to the oil blockade.

These sessions were accompanied by OTJ training provided daily. These included collecting oil statistics from the National Oil Corporation (NOC), which allowed the MFU to estimate oil GDP as a share of national GDP. For non-oil GDP, the MF team engaged the MFU in analytical activities designed to improve estimates of the size and composition of the non-oil sector. The absence of statistical surveys since 2012 has increased the difficulty of estimating the magnitude and structure of Libya’s non-oil GDP. In response, the MF team introduced basic input-output tables to facilitate a simple GDP estimation process. The methodologies of different international institutions (IMF, World Bank) were studied, and a GDP deflator was used to demonstrate alternative methods for estimating real GDP. The team and the MFU then prepared detailed budget execution tables, which allow assessing each GDP

Internal macro-fiscal training for MFU and MoF officials.

8 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

component to make projections. Forecasting tools for assessing potential primary revenue sources were also introduced as part of this OTJ mentoring.

Development of Macro-Fiscal Monitoring & Analysis Reports

The afore-mentioned sessions significantly improved the organization of the databases the MFU is developing, and the preparation of the budget execution tables published on the MoF's website and Facebook page. A Budget Execution Report for 2019 was prepared and is currently being finalized. The team also worked intensively with MFU staff to strengthen their capacity to prepare the monthly macro-fiscal updates published on the MoF's website. The January and February reports contained a rigorous analysis of the effects of the oil blockade on the Libyan economy, the GoL budget, and the balance of payments. The March Macro-Fiscal Report includes an assessment of the economic consequences of the COVID-19 pandemic.

Given the current COVID-19 restrictions in Libya, the MF team is organizing weekly Skype calls with the MFU team and continues to be in daily contact individually with its various members. These discussions allow the team to continue to work with the MFU on the joint development of new economic forecasts that reflect changing economic circumstances. A short-term econometric model was prepared within the MFU that takes account of the impact of key variables (including money supply and the exchange rate) on the parallel market to assess the impact of changes in these variables on inflation.

Preparation of Technical Reports on Major Macro-structural Issues

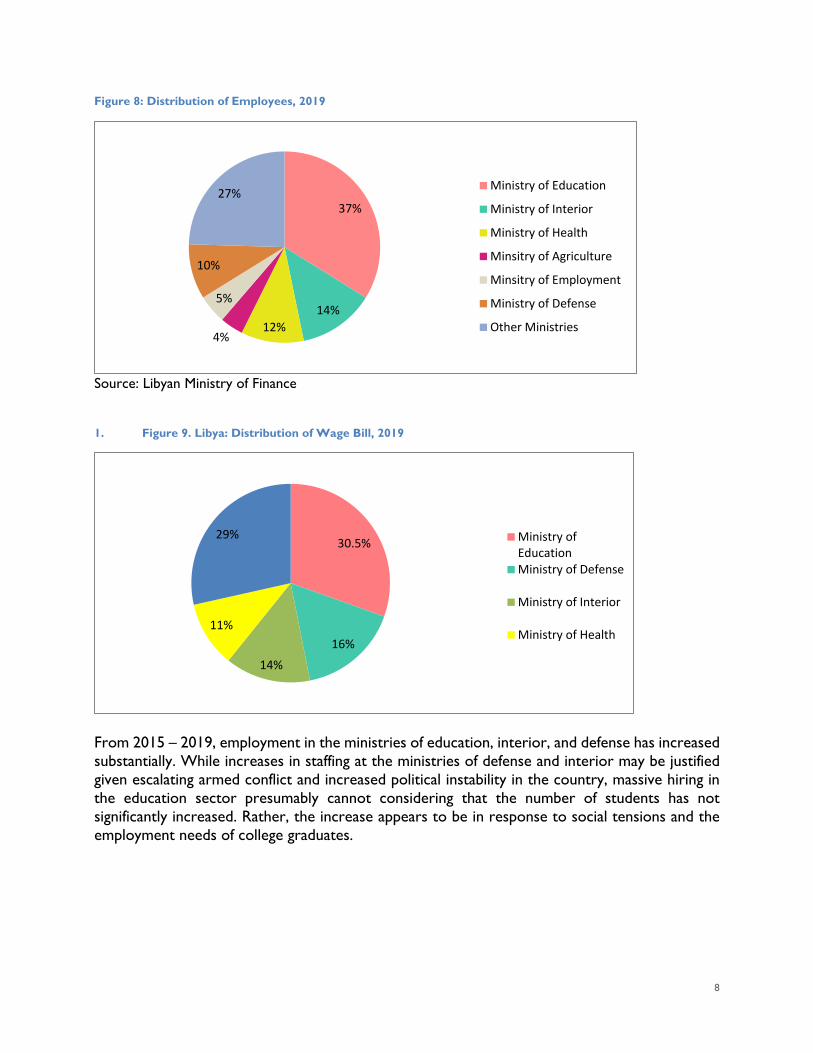

The MF Team supported the MFU in drafting a technical note on the structure of the excessive public sector wage bill, with international comparisons to illustrate how this issue impacts Libya’s macro-fiscal health and economic diversification prospects. The note includes detailed projections reflecting Libya's demographic evolution and the corresponding changes to the wage bill, as well as best practice recommendations to improve wage bill management. Another major analytical report was prepared by the MFU on the exchange rate regime. This report addresses the dual exchange rate problem caused by the foreign exchange (FX) tax, which severely penalizes exporters. The report also tackles the fundamental question of the optimal choice of exchange rate regime in an oil-dependent country like Libya. It analyzes the impact of an overvalued exchange rate on macroeconomic stability and economic diversification, the consequences of fluctuations in the parallel market on key macroeconomic performance variables, and the impact of alternative exchange rate regimes on government revenues and expenditures. The report proposes a gradual approach to introducing greater exchange rate flexibility, including specific macro-structural policy measures/actions needed to facilitate an efficient and relatively smooth transition to a flexible exchange rate.

Training Program for MoF Financial Institute and MFU Staff

The MF Team developed a detailed 9-month curriculum for the MoF’s Financial Institute that will provide officials from public sector institutions with a solid grounding in basic macro-fiscal policy analysis principles, as well as a practical understanding of the applied budget formulation and applied policy analysis. The Team also developed a core training program for MFU staff that focuses on macro-economic modeling, budget projections, and revenue modeling.

National-Level PFM Reforms In mid-December Q1, USAID requested LPFM to revise its Year 1 work plan to include several major national level PFM activities principally within the mandate of the MoF. LPFM presented the revised work plan to USAID in late December, which USAID approved on February 3. USAID met in mid-February with MoF leadership to discuss these changes. However, the MoF has since been heavily focused on the consequences of the re-intensification of the conflict and, more recently, the COVID-19 crisis and the loss of oil revenue. Furthermore, LPFM has not been able to position the concerned advisory experts in Tripoli due to COVID-19. Consequently, LPFM expects to initiate proactive

9 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

discussions on these potential program areas early in Quarter 3 with senior MoF stakeholders and to assess in coordination with USAID stakeholder engagement interest under current circumstances.

COMPONENT 2: REFORM LIBYA’S ELECTRICITY SECTOR

During the quarter, the Electricity Sector (ES) team worked with GECOL and other sector stakeholders to advance the component’s objectives. Weekly meetings were held with GECOL’s chairman and board members. The team assisted GECOL with the development of a draft National Energy Efficiency Action Plan (NEEAP) that aims to reduce consumption by 20% over five years, and the establishment of regional billing and collection targets to reduce commercial losses. The ES team also held workshops to advance the development of an electricity decree that authorizes the reform of the sector. And the team resumed its assistance to realign GECOL’s workforce and generate non-electric revenues.

Assist TFESR to develop and advocate for an electricity sector decree

During the quarter, the Task Force for Electricity Sector Reform (TFESR) established a Legal Technical Committee to develop a draft electricity sector decree providing for the reform of the sector by authorizing the unbundling of GECOL and the participation of the private sector in electricity generation and distribution.3 On January 27, the ES team held the first workshop for this committee to review the necessary elements of the decree. On March 9, a second workshop was held to initiate the drafting of the decree. .

Reduce Commercial Losses and Enhance Revenue at GECOL

The ES team continued to assist GECOL with the reduction of its commercial losses. The ES team held several workshops for GECOL’s Customer Service Regional Managers and key Customer Service support staff to review the details of the established 2020 regional billings and collections targets. The workshops also trained the participants on the use of the newly enhanced web-based dashboard tool developed by the ES team to assist in improving billings and collections and lowering commercial losses.

3 The construction of the first private sector electricity generation facility (a 100 MW solar plant) is proposed to begin later

this year. The proposed solar plant is expected to sell its output to GECOL under a Power Purchase Agreement (PPA).

Members of Legal Technical Committee participating in the electricity sector reform workshop

10 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

Members of the GECOL Commercial Losses Technical Committee participating in the electricity sector reform workshop

Revenue enhancement - non-electric revenue

The ES team developed a recommended strategy for GECOL to pursue nonelectric revenue generation through the monetization of GECOL’s vast fiber-optic network. GECOL management intends to present the strategy to its Board when conditions permit. The basic elements of the ES team’s proposed strategy are (1) Create a wholly-owned GECOL subsidiary – GECOL Telecom (GTEL) - providing telecom services; (2) Assign GTEL exclusive rights to use GECOL’s optical ground wire (OPGW) infrastructure for providing telecom services; (3) Have GTEL obtain a Class 1 telecommunications service license; (4) Transfer GECOL’s ICT department to GTEL and outsource all GECOL ICT service needs to GTEL; (5) Execute inter-company service agreements between GECOL and GTEL; and (6) Enter into a PPP arrangement for the management of GTEL with a competitively selected enterprise. Promote the establishment of an independent regulator

The ES team held several workshops early in the quarter for the TFESR’s Regulatory Technical Committee. The workshops were held to obtain the committee’s comments on the draft independent regulator decree. Representatives from the MoLG and CSOs attended. After incorporating the comments from the workshops, the ES team and the PC’s energy advisors met on March 1, where the team presented the decree. Discussions focused on the best way to present the decree to the Prime Minister (PM). The meeting concluded with an agreement that the ES team would prepare a package for the PM that includes an explanatory memorandum. The PC advisors committed to providing their comments on the decree in March, but these had not been received as of the writing of this report. The ES team plans to prepare the package and to deliver it to the advisors during the next quarter.

Members of the Regulatory Technical Committee unit participating in the workshop

11 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

Assist GECOL to realign and reduce its workforce

Libyan government subsidies to the electricity sector are the highest in the MENA region. They represented 9.1% of Libya’s GDP in 2018, with overstaffing at GECOL representing nearly 1%. The ES team resumed its work with GECOL’s Technical Committee on Workforce Realignment on a workforce realignment plan that moves GECOL closer to its regional peers in terms of workforce size. Currently, the work is focused on determining the recommended staffing for unbundled core businesses and support services. The ES team and the technical committee are identifying which of GECOL’s functions are core and which are not. The ES Team intends to prepare a five-year deployment, training, and HR development plan to support the transition from the current workforce of 41,000 to 14,000.

Improve private sector participation in the electricity sector

The ES team worked with the TFESR and GECOL to review modalities for private sector participation in the electricity sector. The ES Team assisted with assessing the costs and benefits of private sector participation and the technical and legal requirements. The ES Team emphasized the potential benefits of private sector participation in distribution services, including the introduction of smart meters, pre-paid meters, and collection kiosks. The ES team’s recommendations will be used as inputs to GECOL’s unbundling plan. The ES team developed an action plan for GECOL’s introduction of smart and prepaid meters, starting with a pilot in Tripoli Center and then expanding to other Tripoli municipalities. Prepaid and smart meters dramatically improve revenue collection and decrease commercial losses, major objectives of the LPFM program. The action plan was developed after LPFM sponsored meetings with Tripoli Center, MoLG, and GECOL. The plan aims for meter installation to commence by November 1, 2020. Increase Energy Conservation and Demand Side Management

During the quarter, the ES team and GECOL’s Energy Efficiency & Conservation Technical Committee completed a draft of the 2020 National Energy Efficiency Action Plan (NEEAP). The draft plan was provided by GECOL to the MoP’s Energy Efficiency (EE) Committee. The plan targets 20% less electricity consumption by 2025. The plan reflects the “Arab End Use Electricity Efficiency Improvement and Conversation Guidelines.” The ES team had planned to present the NEEAP to the EE Committee during a March 2020 workshop; however, all March workshops were postponed due to the COVID-19 pandemic. Feedback will now be obtained via VTCs with committee members during April and May. Achieving the NEEAP’s energy efficiency goals will require appropriate implementing measures, and the ES team will assist the MoP’s High Committee for Energy Efficiency to develop the needed measures. GECOL unbundling and restructuring

During the quarter, the ES team held a workshop for a new GECOL Technical Committee on the Financial Unbundling of GECOL. The ES team is assisting the committee with developing financial models for an unbundled GECOL with core and non-core businesses, as is consistent with best practice and international unbundling models. During its inaugural meeting, the committee agreed to split into four working groups. The ES team will conduct workshops and training events for each working group. The four working groups are assisted in their day-to-day work by the ES team. The assistance will continue until the financial models for unbundling are presented to the TFESR and GECOL.

12 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

Figure 1 - Members of the GECOL financial unbundling Technical Committee participating in the electricity sector reform workshop

COMPONENT 3: IMPROVE BUSINESS ENVIRONMENT The BEE component assists Libya with establishing a business environment that facilitates business creation and operation, thereby boosting economic growth and diversification. The BEE Team pursues this objective by assisting Libya reform and increase the transparency of its commercial legal/regulatory regime, increasing its integration into global markets by preparing the country for WTO accession, and enhancing its attractiveness to international investors by raising its scores on the World Bank’s Doing Business (DB) indicators. During the quarter, the BEE Team continued to gather, translate, and review the existing legislation and regulations that form the basis of the business environment. The team also advanced the development of the WTO Accession Action Plan and held in-depth discussions with key public and private sector stakeholders on its work on enabling environment reforms and WTO accession. In the public sector, the team held discussions with counterparts from the Government Decision Support Center (GDSC), the Ministry of Economy (MoEcon), the Ministry of Justice (MoJ), the Libyan Local Investment and Development Fund (LLIDF), the Customs Bureau, the legal office of the Presidential Council (PC), and the Libyan Capital Markets Authority. Of greatest significance, the GDSC committed to establish and lead working groups – that would include the BEE team and the PC’s legal office – to review and further develop the BEE team’s proposed legislative reforms. And the PC’s legal office agreed to establish a Legal Reform Unit that would participate in the GDSC working groups, and then advocate the agreed reforms at the PC. The BEE team also actively engaged in the private sector during the quarter. In February, the team and the Libyan Business Council (LBC) organized two focus groups. The participants in the two groups included 18 SMEs from Tripoli and Sabha, two business lawyers, the LBC’s Chairman and staff, and representatives from the GDSC, AmCham, and the Libyan Women’s Business Council (LWBC). In March, the BEE team and the Misrata Chamber of Commerce co-sponsored a third focus group for eight Misrata-based local businesses. The BEE Team also held individual interviews with 17 additional SMEs in Tripoli and Misrata. In total, the representatives of 35 SMEs operating in a wide range of sectors and industries participated in either the focus groups or individual interviews All stakeholders expressed enthusiastic support for the work of the BEE team to help Libya identify, develop, and adopt critical enabling environment reforms. Both public and private sector counterparts expressed a desire to collaborate with the BEE team. In particular, the private sector stakeholders identified many specific reforms to the enabling environment they deemed necessary. They strongly support the establishment of a publicly accessible online platform where all laws, regulations, and decrees can be obtained. There was broad consensus on the need for reforms that will (i) increase

13 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

access to credit; (ii) make customs processing and import/export licensing more streamlined, transparent, and uniformly applied; (iii) enable public-private partnerships for the infrastructure projects that will be needed when the conflict ends; (iv) address unfair competition by firms that operate outside the law; (v) lessen the current restrictions on foreign investment; and (vi) establish a more transparent, open, fair, and competitive government procurement process. Both public and private sector counterparts also expressed substantial interest in advancing the readiness of Libya for WTO accession and in need to implement a legal/regulatory review function to identify and correct the many inconsistencies, gaps, overlaps, and ambiguities in the current legislative/regulatory regime. Assess Libya’s Business Enabling Environment

During the quarter, the BEE Team continued its assessment of the legal and regulatory framework and bureaucratic practices affecting commerce and business operations. These work laws and regulatory instruments are relevant to WTO membership requirements and, therefore, the WTO Accession Action Plan. The review also covered many of the laws and regulations relating to the areas identified by the private sector as problematic. More specifically, the BEE team reviewed the regimes governing, access to credit, investment promotion, foreign investment, labor relations, taxes, customs and foreign trade regulation, government procurement, competition, business organizations, corporate governance, shareholder rights, capital markets, accounting and auditing, and intellectual property. Identify Priority Reforms and Develop Policy Briefs

Using the information obtained from its own legislative/regulatory review and analysis, as well as the insights of the private sector, the BEE team revised its list of priority reforms areas, focusing on the areas where significant reforms are both needed and achievable under the prevailing circumstances, which do not currently permit the adoption of new laws or amendments to laws. The team began developing drafts of legislation (decrees) and accompanying memoranda (policy briefs) in the areas of secured transactions, import/export licensing, and minority shareholder rights. The proposed drafts and explanatory memoranda are expected to be delivered to GoL counterparts in late April/early May. The explanatory memoranda will review the need for the reform – how Libya’s current regime is inconsistent with BEE best practices – and the main elements of the draft legislation. The BEE team also prioritized the development of proposed reforms in the areas of unfair competition, public-private partnerships, foreign investment, customs, and government procurement, all of which have been identified by the BEE Team as key private sector priorities, where meaningful reforms are achievable under current circumstances. The BEE Team also established a group of “second-tier” reforms: (i) a decree governing commercial arbitration; (ii) streamlined court procedures to more expeditiously resolve contract disputes; (iii) procedures enabling the expeditious enforcement of judgments resulting from commercial cases; and (iv) amendments to the Labor Code to ease hiring/firing restrictions and to reduce impediments to women participation in the workforce; Develop the WTO Accession Action Plan

During the quarter, the BEE Team also completed its assessment of the conformity of the relevant elements of Libya’s foreign trade regime with the core WTO agreements: the Trade Facilitation Agreement; the Agreement on Trade-Related Aspects of Intellectual Property; the Agreement on Technical Barriers to Trade; the Agreement on the Application of Sanitary and Phytosanitary Measures; the Customs Valuation Agreement; the Rules of Origin Agreement; the General Agreement on Tariffs and Trade; and the Government Procurement Agreement. This assessment involved a review of Libyan

14 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

legislation as well as on-the-ground research that included discussions with private sector firms, the Libya Customs Authority, customs brokers, and the Ministry of Economy. As an output of the assessment, the team prepared recommendations to improve the conformity of Libya’s regime with the WTO agreements, and these are being integrated into the WTO Accession Action Plan under development by the team. The Action Plan identifies the areas where Libya’s legislative framework governing WTO-relevant subject matter requires modification; it also provides an accession roadmap for the GoL that describes the significant milestones and how to achieve them efficiently. The BEE Team plans to deliver the Action Plan to the GoL during by early May. Establish PSAP at LBC and Hold Focus Groups

During the quarter, the BEE Team met regularly with the Chairman of the LBC. They agreed on the steps for establishing the Private Sector Advocacy Platform (PSAP) and scheduled the first two private sector focus groups for February. The BEE Team and LBC staff then collaboratively planned the focus groups, which were held on February 5 and 16. The participants in the first focus group included the LBC Chairman, two business lawyers, representatives from 10 Tripoli SMEs, the GDSC, AmCham, and the LWBC. The participants in the second focus group, also co-sponsored with the LBC, included representatives from eight Sabha-based SMEs. In March, the BEE team held another focus group that was co-sponsored by the Misrata Chamber of Commerce for eight local businesses from that municipality. The BEE Team also conducted individual interviews with SMEs in all three cities. In total, 35 SMEs operating in a wide range of sectors and industries participated in the focus groups and interviews. Through this engagement, the team identified the reforms of the greatest interest to the private sector. Technical Reform Secretariat, PPD, Training, Legislative Database

In January, the BEE team met on several occasions with the two GDSC officials that had been assigned by the Head of the GDSC to coordinate with LPFM. The GDSC officials agreed that the GDSC’s Secretariat will serve as the technical reform secretariat and will establish the working groups to review the recommended legislative reforms and explanatory memoranda developed by the BEE team. It was agreed that the BEE team and the PC’s legal office would be included in all working groups. The SMEs that participated in the focus groups and interviews broadly expressed strong interest in the establishment of a central publicly accessible on-line database where all laws, regulations, and decrees can be obtained. By the end of the quarter, the Team had collected and organized a substantial number of the concerned legal and regulatory instruments. The team, therefore, began planning for the award of a grant to fund the establishment and initial operation of the database. The award is expected to be made in the third quarter.

SELF RELIANCE GRANTS In this quarter, the operationalization of the Grants Program commenced. The LPFM Grants Manual was developed and subsequently approved by USAID on January 22. The Grants Officer was recruited and joined the LPFM team from January 19, 2020. Following the appointment of the Grants Manager, development began on finalizing all the relevant grants documentation for the project, including a Standard Operating Procedure for grants making; the grants templates; the grants file structure and checklist.

15 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

To support the grants program, two CSO mapping exercises were designed to identify appropriate CSOs that could be potential grantees supporting LPFM’s activities. The first was completed by the PE Team in January-February to identify education-oriented CSOs, which could collaborate with the PE Team’s support to the government’s education decentralization program. The second CSO mapping exercise, which would cover CSOs across the full spectrum of LPFM activities, was designed and subcontracted to Counterpart International (CI) to cover all of Libya. This exercise commenced in mid-March 2020, but due to the movement limitations imposed due to the COVID-19 pandemic and the increase in conflict, the exercise is now being redesigned to account for these factors. The CSO mapping report, which is expected to be completed by the end of May, will identify local CSOs that may be considered for the LPFM’s Self-Reliance Grants Program.

With the completion of the CSO mapping in May, we expect grant activities to accelerate in Q3. We envisage the completion of impactful grant actions even during the COVID-19 crisis.

COMMUNICATIONS/OUTREACH LPFM/Bab al Tamkeen’s communications/outreach efforts this quarter focused on highlighting project achievements at both the national and municipal levels in Libya, underscoring both the complexities of project objectives and their relevance to the Libyan people. A new communications specialist, based in Tripoli, was able to conduct interviews and collect testimonials from project partners and stakeholders to give voice to the impacts of the project’s technical assistance and support from a Libyan perspective. The communications specialist also launched a dissemination plan to reach out to Libyan media and social media, obtaining agreements from journalists from 11 local radio stations, three television stations, the two major English news websites, one daily newspaper, and other sites to feature our newsworthy stories or interview partners we recommend to discuss project activities and relevance. LPBM/Bab Al Tamkeen highlights were featured in the monthly USAID/Libya newsletter for January, February, and March. Five spotlight stories were produced, featuring improving the business enabling environment, WTO accession, supporting young entrepreneurs, decentralization and OSR, and electricity conservation.

MONITORING, EVALUATION, AND LEARNING (MEL) Please see Annex 2 for the MEL Summary and the LPFM Performance Indicator Tracking Table for FY20 Q2.

1 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

ANNEX 1: LPFM PARTNER MUNICIPALITIES

Table 1: New Municipalities to be included under LPFM

Municipality Population Diversity

GNA Elected Mayor

Deal w/

GNA

Probability of success Security

PFM

Region Size Political will

Administrative Capacity LESP LPFM

1 Zawiyah 163,325 North West Medium X X X X X X X 2 Sirte 118673 North Middle Medium X X X X 3 Harawa 5654 North Middle V.Small X X X X X X X 4 Kaleej Alsedra 22933 North East Small X X X X X 5 Awbari 32382 South West Small X X X X X X X 6 Alriyayna 14774 West. Mountain Small X X X X X X X 7 Alkufra 44314 Far Southeast Small X X X X X X 8 Jalu 19033 South Middle Small X X X X X X 9 Oujla 9028 South Middle V.Small X X X X X X 10 Suluq 24280 North East Small X X X X X 11 Tajoura 143516 Greater Tripoli Medium X X X X X X X 12 Garabulli 52407 Greater Tripoli Small X X X X X X X 13 Msallata 75174 North Middle Small X X X X X X X

14 Ghadames 10943 Southwest Middle Small X X X X X X X

15 Derej 12,098 Wes. Mountain Small X X X X X X X 16 Ejdabia 125,613 North East Medium X X X X 17 Benghazi 732,114 North East Large X X X X 18 Albayda 164611 North East Medium X X X X X 19 Sahel Eljabal 37242 North East Small X X X X X X 20 Tokra 23180 North East Small X X X X X X 21 Shahat 59,027 North East Small X X X X X

22 Derna 104,755 North East Medium X X X X

2 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

Table 2: Municipalities to be supported under LPFM (Including municipalities retained from LESP)

Cluster Municipality Population Region Size GNA Elected Mayor

Deal w/

GNA

Political will

Admin Capacity Security LESP LPFM SWM PHC Pedu

1

A

Souq Alghoma 320000 Greater Tripoli Large X X X X X X X X X X 2 Abu Saleem 280000 Greater Tripoli Large X X X X X X X X X X 3 Janzour 300000 Greater Tripoli Larage X X X X X X X X X X 4 Tripoli Center 200000 Greater Tripoli Medium X X X X X X X X X X 5 Tajoura 143516 Greater Tripoli Medium X X X X X X X 6 Alsayeh 24018 Greater Tripoli Small X X X X War zone 7

B

Zawara 34503 North West Small X X X X X X X X X X 8 South Zawiyah 11739 North West Small X X X X X X X X X 9 Sebratha 102038 North West Medium X X X X X

10 Surman 67884 North West Small X X X X X 11 Zawiyah 163325 North West Medium X X X X X X X 12

C

Misurata 487693 North Middle Large X X X X X X X X X X

13 Brega 34,519 North East Small X X X X X X X X 14 Sirte 118673 North Middle Medium X X X X X X X 15 Harawa 5654 North Middle V.Small X X X X X X X 16 Kaleej Alsedra 22933 North East Small X X X X X X X 17 Tarhouna 146966 North Middle Medium X X X X War zone 18

D

Albouanis 9494 South Middle V.Small X X X X X X X X X 19 Algherifa 35064 South Middle Small X X X X X X X X X X 20 Brak 36847 South Middle Small X X X X X X X X X 21 Sebha 128388 South Middle Medium X X X X X X X X 22 Awbari 32382 South West Small X X X X X X X

3 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

Cluster Municipality Population Region Size GNA Elected Mayor

Deal w/

GNA

Political will

Admin Capacity Security LESP LPFM SWM PHC Pedu

23

E

Gheryain 212000 Wes. Mountain Medium X X X X X X X X X X 24 Alasabaa 35354 Wes. Mountain Small X X X X X X X X X 25 Alriyayna 14774 West. Mountain Small X X X X X X X 26 Yefern 21559 Wes. Mountain Small X X X X X X X X X X 27

F

Suluq 24280 North East Small X X X X 28 Alkufra 44,314 Far Southeast Small X X X X X X 29 Jalu 19,033 East Middle Small X X X X X X 30 Benghazi 732,114 North East Large X X X X 31 Oujla 9,028 East Middle V.Small X X X X X X 32 Ejdabia 125,613 North East Medium X X X X X 33

G

Zelitin 280000 North Middle Large X X X X X X X X X 34 Garabulli 52407 Greater Tripoli Small X X X X X X X 35 Alkhoms 191943 North Middle Medium X X X X X X X X X 36 Msallata 75174 North Middle Small X X X X X X X 37

H Kabou 9657 Wes. Mountain V.Small X X X X X X X X X

38 Ghadames 10943 Southwest Middle Small X X X X X X X 39 Derej 12098 Wes. Mountain Small X X X X X X X 40

I

Emsaed 16256 Far Northeast Small X X X X X X X X 41 Tobruq 158826 East Medium X X X X 42 Albayda 164611 North East Medium X X X X X X 43 Sahel Eljabal 37242 North East Small X X X X X X 44 Tokra 23180 North East Small X X X X X X 45 Shahat 59027 North East Small X X X X X 46 Derna 104755 North East Medium X X X X

46 46 44 24 22 19 19 10

4 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

5 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

Western area details

1 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

ANNEX 2: MONITORING, EVALUATION, AND LEARNING (MEL) AND PITT TABLE FY20 Q2 Activities Summary

During the second quarter of FY 2020, the LPFM MEL team finalized tasks and activities. As a result, during the quarter, the MEL team accomplished the following tasks:

• January 15, 2020: Submitted LPFM Q1 report to USAID/Libya COR, • January 23, 2020: Submitted LPFM Activities GIS Information to USAID/Libya COR, • March 11, 2020: Received USAID/Libya COR request for amendment of AMELP and ITT, and • March 31, 2020: The submitted final version of LPFM AMELP & ITT to USAID/Libya COR for

approval.

Building MEL capacity within LPFM: During FY19 Q2, the MEL team continued conducting weekly calls with the MEL field team members as well as one-on-one coaching calls, to support MEL practices and procedures and respond to MEL-related data collection and verification questions. In addition, the LPFM MEL Team arranged an intensive onsite training and working group event in LPFM Tunis office in early February 2020 for seven working days, led by the MEL Senior Advisor in order to: support the on-boarding of the new MEL Specialist for Tripoli; conduct a quality control review of the LPFM MEL system; enhance awareness and involvement of component teams to align work plan deliverables to LPFM MEL outcomes indicators; brief the incoming LPFM COP on the status of the MEL tasks and systems; and to support the baseline survey efforts for the component teams. Further coaching was also delivered to the MEL field Manager on the grant process, indicators definitions, and standard operating procedure (SOP) development.

As part of MEL Team capacity building, MEL team conducted two Quality Assurance/Quality Control internal assessments on Feb 27th and March 24th to confirm that all performance data is backed up with robust supporting evidence, to verify data accuracy, ensure that all MEL documents are compliant with ADS standards, and that data is up to date and aligned across all MEL system tools. Finally, as part of communication across the Pragma MEL team, on March 30-31, the MEL Tripoli field specialist participated in a USAID/METAL-facilitated collaborative learning crash course to learn from experience and best practices examples as shared by MEG YESS team and acquired from Third Party Monitoring.

LPFM Adaptive Management /CLA Efforts:

In addition to the CLA capacity building training course of MEL team with the USAID/METAL Third Party Monitoring implementor, the MEL Team has engaged in exchanges with METAL to explore and share methodologies for remote monitoring of LPFM events conducted remotely in response to the global COVID-19 crisis. The LPFM MEL team is working with the Component Teams to institute a system for remote monitoring in a way that guarantees accurate attendance tracking and an independent interviewing process of beneficiaries. In addition, USAID/METAL has agreeing to share its monitoring analytics data that can be used for activities trend analysis and assessments by LPFM.

As part of an internal feedback loop to share performance data with decision-makers, the LPFM MEL Team has consolidated and shared all events/workshops lessons learned and requirements with technical teams (sign-in sheets, photos, etc.) to be used for their internal reports and activity follow up and planning. In addition, TPM reports are shared with the Public Outreach and Communication Team so that they can identify relevant quotes and information/data from this objective source for some of their YESS-related communications products. The MEL team has postponed its Annual Adaptive Management

2 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

Training for all LPFM management and senior staff until after the end of the COVID-19 crisis and/or Ramadan.

LPFM GIS Information: By Component

LPFM MAP FY20 Q2

Activity Theory of Change and Logic Model

The purpose of the “Libya Public Financial Management” (LPFM) activity is to advance Libya’s national stability through three objectives. First, LPFM will strengthen the Government of Libya’s (GOL) public financial management (PFM) policies and processes to strengthen the fiscal foundations for sustainable and inclusive growth. Second, LPFM will provide technical assistance and capacity building for Libya’s electricity sector. Third, LPFM will seek to improve Libya’s business, enabling the environment to stimulate the growth of the private sector.

LPFM supports USAID’s development hypothesis which states that if the GOL can achieve greater efficiency and effectiveness in the management of public finances, including through more efficient management of the electricity sector, then macroeconomic stability will be restored, creating the fiscal space for greater public investment in critical services and infrastructure, increasing Libya’s political and social stability. It further hypothesizes that if Libya can create a business environment that is conducive to economic growth and job creation, then this will help to legitimize the state, increase political and economic stability, and give the Libyan people hope for the future.

Pragma’s approach is based on the fundamental premise that in order to establish responsive and participatory governance, Libya requires well-functioning institutional and legal systems. LPFM presents a unique opportunity to support the design and implementation of systems that ensure rational, systematic, transparent, and efficient allocation and use of public money (including oil revenue), as well as expand and diversify private sector development by actively promoting competition, access to finance, and foreign and domestic trade and investment.

3 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

The LPFM team has identified a set of critical assumptions and risks, including: • Security conditions – that security conditions will remain the same or deteriorate. In addition to

analyzing changes in security from credible sources (including the Pragma LPFM security provider) in real-time to make prudent and expeditious program decisions, a context indicator Fragile States Index for Libya, which will be used to assess how changes in security and conflict in Libya may impact the achievement of results. If the security conditions deteriorate to the point that the program staff cannot safely implement the program and participants are restricted in their movements, LPFM contingency planning includes the following options: (1) move the TCN staff from Tripoli to Tunis and have them remotely manage the program until security improves; (2) explore options to have events scheduled/located in Tunisia or another relevant third country; and (3) utilize DVCs when possible;

• Macro-economic stability – that economic indicators either remain stable or improve, again so that Libyan stakeholders can make decisions with the expectation that the economy will not deteriorate significantly over the next 12 to 18 months. This assumption will be tracked by a context indicator GDP Annual Growth Rate and through discussions with the LPFM stakeholders; and

• Political stability – that there is sufficient governance that Libyans can make decisions with the expectation that things will not change significantly over the next 12 to 18 months. This assumption/risk will be tracked not only through discussions with LPFM stakeholders, including leadership of other USAID programs such as the Libya Local Governance/Civil Society Project. It will be measured through context indicators, including the World Bank’s Ease of Doing Business Score for Libya and Freedom House’s Freedom Rating for Libya.

Therefore, to measure and report on the achievement of the LPFM’s ten results statements, the Pragma Corporation will use 32 performance indicators. Of these performance indicators:

• A total of four (4) or 13% are LPFM task order required indicators;

• A total of five (5) or 16% are context indicators;

• A total of eight (8) or 25% are a democracy and governance indicators;

• A total of four (4) or 13% are linked to the LPFM strategic communications cross-cutting theme;

• A total of six (6) or 19% are Foreign Assistance Framework Economic Growth and Capacity Building standard indicators;

• A total of three (3) or 9% are linked to UNDP or World Bank indicators; and

• A total of 26 or 81% are custom indicators.

Performance Indicator Analysis

The LPFM program’s monitoring, evaluation, and learning plan function as a key element that is fully integrated into technical implementation. As a result, there is a functioning feedback-loop between implementation tasks and MEL, so that performance data and information is shared in near real-time with the LPFM managers and decision-makers. For FY20 Q2, LPFM will report on ten performance indicators, reflecting an increase of seven additional performance and one context indicators related to LPFM sub-component activities. Over the next quarter (FY20 Q3), an additional three performance indicators are anticipated to be reported to USAID. By the end of FY20, LPFM is expected to be able to

4 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

report on a total of 17 performance indicators. The remaining LPFM performance indicators4 are either end-of-program indicators or will be available for collection during year two, and as a result, will be reported in FY21.

Component Result 1: Capacity for Libya’s public financial management at the national and sub-national levels will be strengthened

Indicator 1.1b: Number of executive branch personnel trained with USG assistance (Archived Standard DR 2.2): This key LPFM contract required output indicator measures the breadth and depth of training focused on executive branch personnel. Data for this indicator is collected through daily sign-in sheets. In the final approved LPFM AMELP (March 2020), it was determined by USAID that this indicator will also be disaggregated by age; beginning in FY20 Q3, this disaggregation will be included in the reporting of this data to USAID. To date, LPFM has trained officials from seven executive branch institutions.

MEL Table 1: Actuals for LPFM 1.1b Number of executive branch personnel trained with USG assistance (Archived Standard DR 2.2)

LOP TARGET 200

ACTUALS FY20 TARGET 100

ACTUALS (CUM.) 38

LOP % ACHIEVED 38% FY 20 Q1 TOTAL FY 20 Q2 TOTAL

Q2 TARGET 35

Q2 % ACHIEVED 109% TOTAL POP 5 TOTAL POP 33

SEX OF PARTICIPANTS MALES 4 MALES 27

FEMALES 1 FEMALES 6

Executive Office of Participant Ministry of Local Government

Ministry of Local Government, Presidential Council, Ministry of

Planning, Ministry of Health, Ministry of Finance, MoF/Macro Fiscal Unit,

Ministry of Education, Supreme Council for Local Administration

Topic of Training

Second Workshop on the Assessment of the Municipal PFM Project, Workshop with MFU team

covering - report preparation on macroeconomic projections and

wage bill

Launching the Primary Health Care Operational Plan in Libya (in six pilot

municipalities), 2020 municipal budget improvements workshop,

Workshop on OSR Budgets for the additional wave of LPFM

4 Not including LPFM context indicators, which will be used to analyze overall performance when these secondary data sources become available.

5 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

municipalities

Location of the Training (Number of events at the

location) Two events held in Tripoli Three events held in Tripoli

Indicator 1.1c: Number of government officials receiving USG-supported anti-corruption training (Standard DR 2.4-1): This key LPFM contract-required output indicator measures the breadth and depth of anti-corruption training focused on municipal-level personnel. To address anti-corruption, the PFM Team designed and developed a municipality-oriented anticorruption training workshop and materials with the expectation that the training would commence in March. In addition, the LPFM PFM team has also built anticorruption sessions into the OSR budget workshops that took place during the period of performance (and is included in the performance data for both indicators 1.1b and 1.2c). Unfortunately, before the dedicated anti-corruption training could begin, the Libyan borders were closed due to the COVID-19 crisis, and the STTA consultant was therefore unable to enter Libya to start the training. The dedicated anti-corruption training is now rescheduled for the next quarter; the PFM team is exploring remote and/or on-line training options to deliver this training in case the Libyan COVID-19 response makes training in Libya logistically impractical.

Indicator 1.2b: Number of Sub-national governments entities receiving USG assistance to improve their performance (Archived Standard DR 2.3, Linked to UNDP/Libya 3.1.1): This contract required key output indicator tracks the number LPFM-partner municipalities who are key targets of efforts to increase the capacity of municipalities to operate effectively and transparently while preserving accountability. Data for this indicator is collected through activity records (in this case, a diagnostic tool that assessed the capacity of the municipalities against Public Expenditure and Financial Accountability (PEFA) priority areas and dimensions, training activities, and consultations). LPFM conducted and completed the baseline assessment of PEFA scores on eight priority areas of PEFA in FY20 Q1 with 19 municipalities. During this reporting period, the PFM team conducted training sessions, consultations, and providing other TA to a total of 25 targeted municipalities, including six new municipalities.

6 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

MEL Table 2: Actuals for LPFM 1.2b: Number of Sub-national governments entities receiving USG assistance to improve their performance (Archived Standard DR 2.3, Linked to UNDP/Libya 3.1.1)

LOP TARGET 28 ACTUALS

FY20 TARGET 18

LOP % ACHIEVED

89% FY 20 Q1 TOTAL FY 20 Q2 TOTAL

ACTUALS 25

FY20 % ACHIEVED

139% TOTAL POP 19 TOTAL POP 25

SUB-NATIONAL ENTITIES

Cluster A Suq-Aljumah, Abu-Saleem, Janzour, Tripoli Center Cluster A

Suq-Aljumah, Abu-Saleem, Janzour, Tripoli Center,

Tajoura

Cluster B South Azzawia, Zuwarah Cluster B South Azzawia, Zuwarah,

Sabratha, Surman, Zawiyah

Cluster C Misurata, Zelitin, Alkhomes Cluster C Misurata, Brega

Cluster D Wadi-Albwanies, Alghoriafa,

Brak-Elshati Cluster D

Wadi-Albwanies, Alghoriafa, Brak-Elshati, Sabha, Awbari

Cluster E Gharyan, Alasabaa, Yefern Cluster E Gharyan, Alasabaa, Yefern,

Alriyayna

Cluster F --- Cluster F ---

Cluster G Khoms, Zletin Cluster G Khoms

Cluster H Kabaw Cluster H Kabaw, Derej, Ghadames

Cluster I Emsaad, Tobruq Cluster I ---

Indicator 1.2c: Number of sub-national government entity personnel trained with USG assistance: This key LPFM output indicator measures the breadth and depth of training focused on municipal-level personnel. In the final approved LPFM AMELP (March 2020), it was determined by USAID that this indicator will also be disaggregated by age; beginning in FY20 Q3, this disaggregation will be included in the reporting of this data to USAID. To date, LPFM has trained representatives from 25 sub-national government entities. During the period of performance, the PFM team also trained a representative from the Libyan Commission of Civil Society.5

5 Because this individual does not work for a sub-national government entity, the individual is not included in the totals for indicator 1.2c.

7 | BAB AL TAMKEEN ACTIVITY REPORT (QUARTER 2, FY 2020) USAID.GOV

MEL Table 3: Actuals for LPFM 1.2c: Number of sub-national government entity personnel trained with USG assistance

LOP TARGET 175 ACTUALS

ACTUALS (CUM.) 64

LOP % ACHIEVED 37% FY 20 Q1 TOTAL FY 20 Q2 TOTAL

Q2 TARGET 25

Q2 % ACHIEVED 256% TOTAL POP 34 TOTAL POP 64 (cum.)

SEX OF PARTICIPANTS MALES 31 MALES 30

FEMALES 3 FEMALES 0

Municipalities Represented at the PFM

training

Cluster A (Suq-Aljumah, Abu-Saleem, Janzour, Tripoli-Center); Cluster B

(Zuwarah, South Azzawia, Sabratha, Surman); Cluster C (Misurata, Brega);

Cluster D (Wadi-Albwanies, Alghoriafa, Brak-Elshati, Sabha); Cluster E

(Gharyan, Alassaba, Yafarn); Cluster G (Khoms); Cluster H (Kabaw)

Cluster A (Suq-Aljumah, Tripoli-Center, Tajoura); Cluster B (Zuwarah, South

Azzawia, Surman, Zawiyah); Cluster C (Misurata); Cluster D (Alghoriafa, Brak-

Elshati, Sabha, Awbari); Cluster E (Gharyan, Alriyayna); Cluster G

(Khoms); Cluster H (Kabaw, Ghadames, Derej)

The topic of the Training Second Workshop on the Assessment

of the Municipal PFM Project

Launching the Primary Health Care Operational Plan in Libya (In Six Pilot Municipalities), 2020 municipal budget improvements workshop, Workshop on

OSR Budgets for new LPFM municipalities

Location & Number of Training

One event held in Tripoli Three events held in Tripoli