vale’s performance in 2016 · 4q14 1q15 2q15 3q15 4q15 1q16 2q16 3q16 4q16 1 2014 and 2015...

TRANSCRIPT

1

Vale’s Performance in 2016

Ricardo Teles / Agência Vale

Rio de Janeiro, February 23rd, 2017

2 Ag

en

da“This presentation may include statements that present Vale's expectations about

future events or results. All statements, when based upon expectations about the

future and not on historical facts, involve various risks and uncertainties. Vale

cannot guarantee that such statements will prove correct. These risks and

uncertainties include factors related to the following: (a) the countries where we

operate, especially Brazil and Canada; (b) the global economy; (c) the capital

markets; (d) the mining and metals prices and their dependence on global

industrial production, which is cyclical by nature; and (e) global competition in the

markets in which Vale operates. To obtain further information on factors that may

lead to results different from those forecast by Vale, please consult the reports

Vale files with the U.S. Securities and Exchange Commission (SEC), the

Brazilian Comissão de Valores Mobiliários (CVM), the French Autorité des

Marchés Financiers (AMF) and in particular the factors discussed under

“Forward-Looking Statements” and “Risk Factors” in Vale’s annual report on Form

20-F.”

“Cautionary Note to U.S. Investors - The SEC permits mining companies, in their

filings with the SEC, to disclose only those mineral deposits that a company can

economically and legally extract or produce. We present certain information in

this presentation, including ‘measured resources,’ ‘indicated resources,’ ‘inferred

resources,’ ‘geologic resources’, which would not be permitted in an SEC filing.

These materials are not proven or probable reserves, as defined by the SEC, and

we cannot assure you that these materials will be converted into proven or

probable reserves, as defined by the SEC. U.S. Investors should consider closely

the disclosure in our Annual Report on Form 20-K, which may be obtained from

us, from our website or at http://http://us.sec.gov/edgar.shtml.” Dis

clai

mer

3 Ag

en

da

1. Vale’s performance in 2016

2. Capital expenditures

3. Capital structure

4. Business segment performance

Agen

da

4

Vale’s performance in

2016

5

Fe Pellets Ni Cu Coal

Another year of sound operational

performance

Production highlights 2016

Total: 348.8 Mt

Carajás: 148.1 Mt

Total: 46.2 Mt

Tubarão 8: 7.2 Mt

Total: 311.0 kt

VNC: 34.3 kt

Total: 453.1 kt

Salobo: 175.9 kt

Au by-product:

483,000 oz

Total: 7.2 Mt

Moatize: 5.5 Mt% % %

Annual record%

%

%

%

%

%

%

5

6

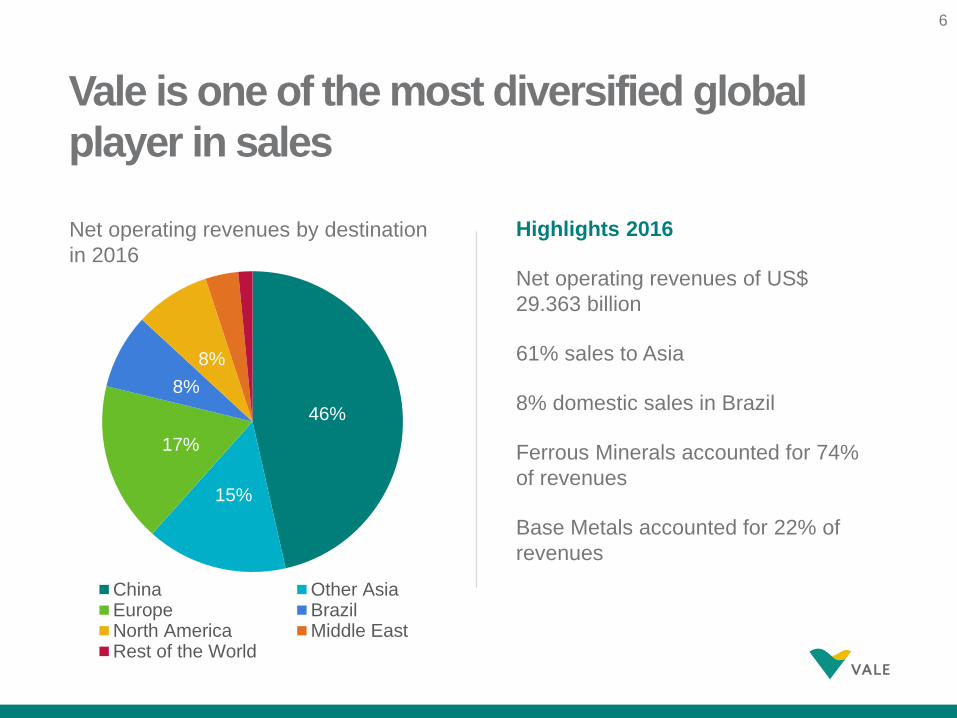

46%

15%

17%

8%

8%

China Other AsiaEurope BrazilNorth America Middle EastRest of the World

Vale is one of the most diversified global

player in sales

Highlights 2016

Net operating revenues of US$

29.363 billion

61% sales to Asia

8% domestic sales in Brazil

Ferrous Minerals accounted for 74%

of revenues

Base Metals accounted for 22% of

revenues

Net operating revenues by destination

in 2016

6

7

Focus on cost controls and operational

efficiency is delivering results

Highlights

Total costs and expenses reduced by

US$ 1.841 billion in 2016

A leaner and simpler structure set to

reduce overlaps among departments

and businesses

Cost and expenses reduction

initiatives amounted to US$ 2.010

billion in 2016

Cost cutting in iron ore has been driven

by operational efficiency, with iron ore

C1 Cash Cost + Expenses per ton

decreasing from BRL 60.1/t in 2015 to

BRL 54.7/t in 2016

19,2

17,4

2,0

0,4

0,9 0,4

2015 Cost and expenses reduction initiatives

FX Higher sales

volumes

Others 2016

Costs and expenses 2016 X 2015

US$ billion

7

8

1,391

3,022

4,770

4Q15 3Q16 4Q16

Significant EBITDA increase due to overall

strong performance

Highlights 4Q16

EBITDA increased 243% vs. 4Q15 and

58% vs. 3Q16

Ferrous Minerals increased US$ 1.616

billion vs. 3Q16

Base Metals increased US$ 93 million

vs. 3Q161

Coal increased US$ 163 million vs.

3Q16

EBITDA, q-o-q

58%

243%

US$ billion

8

1 Excluding the effect of the goldstream transaction in 3Q16.

9

Capital expenditures

10

Vale investment cycle: new projects coming

on line; capex going down

Highlights 4Q16

Total capex was US$ 1.408 billion in 4Q16,

decreasing US$ 785 million vs. 4Q15

S11D loaded 11 vessels up to January

2017, of which 2 Valemax

Sustaining capex per ton of production is

lower than our main competitors’ average

There are no other planned iron ore

projects in the pipeline for the next 6

years

Reaping the fruits of our investment cycle:

increased quality, production and

productivity

Project and sustaining capex

US$ million

1.366

741614

827

516794

4Q15 3Q16 4Q16

Growth projects Sustaining

2,193

1,2571,408

10

11

With S11D, we will achieve unprecedented

levels of competitiveness and price realization

Highlights

High-grade hematite

ore type with iron ore

grade of more than

66% on average

90 Mt per year of

nominal capacity

76% of physical

progress at the

logistics infrastructure

sitesRicardo Teles / Agência Vale

11

12

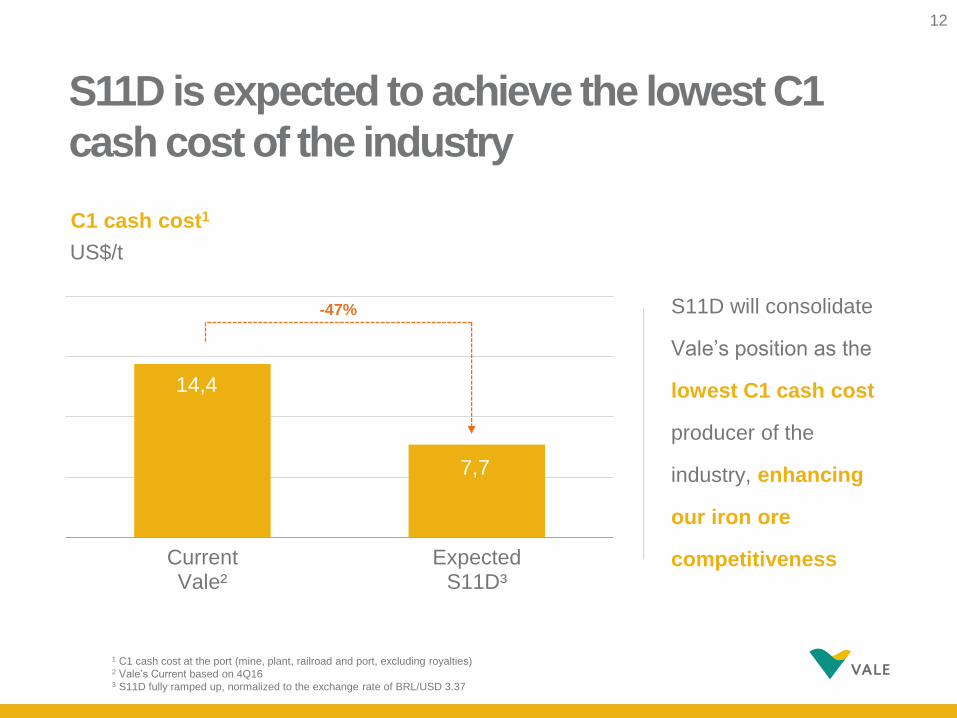

14,4

7,7

CurrentVale²

ExpectedS11D³

S11D is expected to achieve the lowest C1

cash cost of the industry

C1 cash cost1

S11D will consolidate

Vale’s position as the

lowest C1 cash cost

producer of the

industry, enhancing

our iron ore

competitiveness

1 C1 cash cost at the port (mine, plant, railroad and port, excluding royalties)2 Vale’s Current based on 4Q163 S11D fully ramped up, normalized to the exchange rate of BRL/USD 3.37

-47%

US$/t

12

13

3,2

1,81,1

0,3

2,3

2,5

2,5

2,52,5 2,3

0,20,9

1,2

0,70,6

5,5

4,5 4,54,0

3,22,9

2016 2017E 2018E 2019E 2020E 2021E

Growth approved

Sustaining

Replacement

Future CAPEX to remain low

US$ billion

Note: BRL/USD exchange rate of BRL/USD 3.37 from 2017 onwards

13

14

Capital structure

15

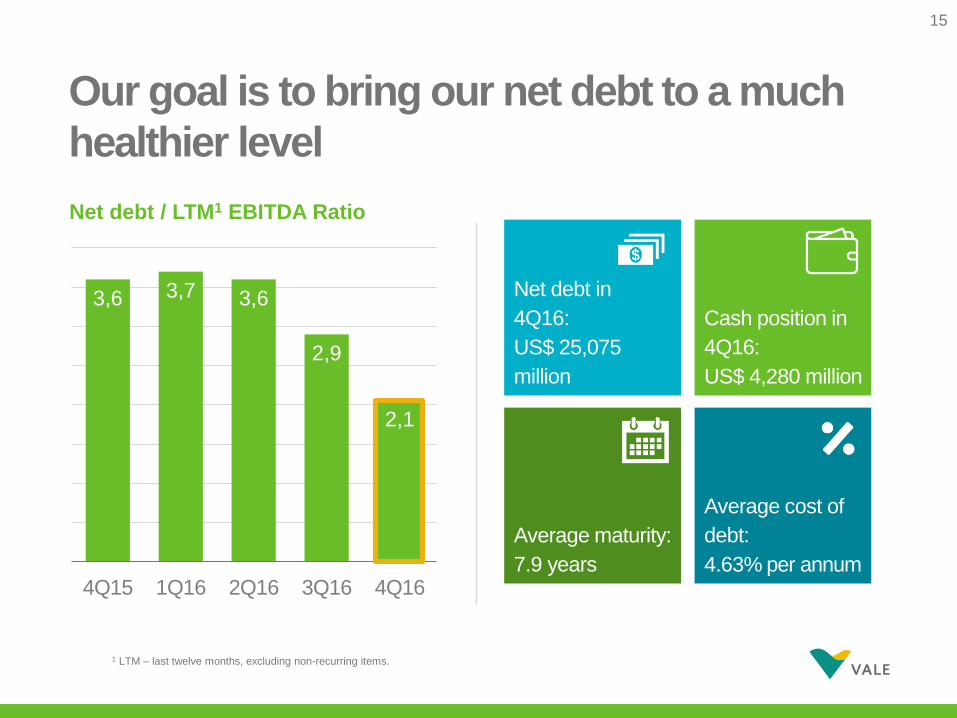

3,6 3,7 3,6

2,9

2,1

4Q15 1Q16 2Q16 3Q16 4Q16

Our goal is to bring our net debt to a much

healthier level

Net debt / LTM1 EBITDA Ratio

1 LTM – last twelve months, excluding non-recurring items.

Net debt in

4Q16:

US$ 25,075

million

Cash position in

4Q16:

US$ 4,280 million

Average maturity:

7.9 years

Average cost of

debt:

4.63% per annum

15

16

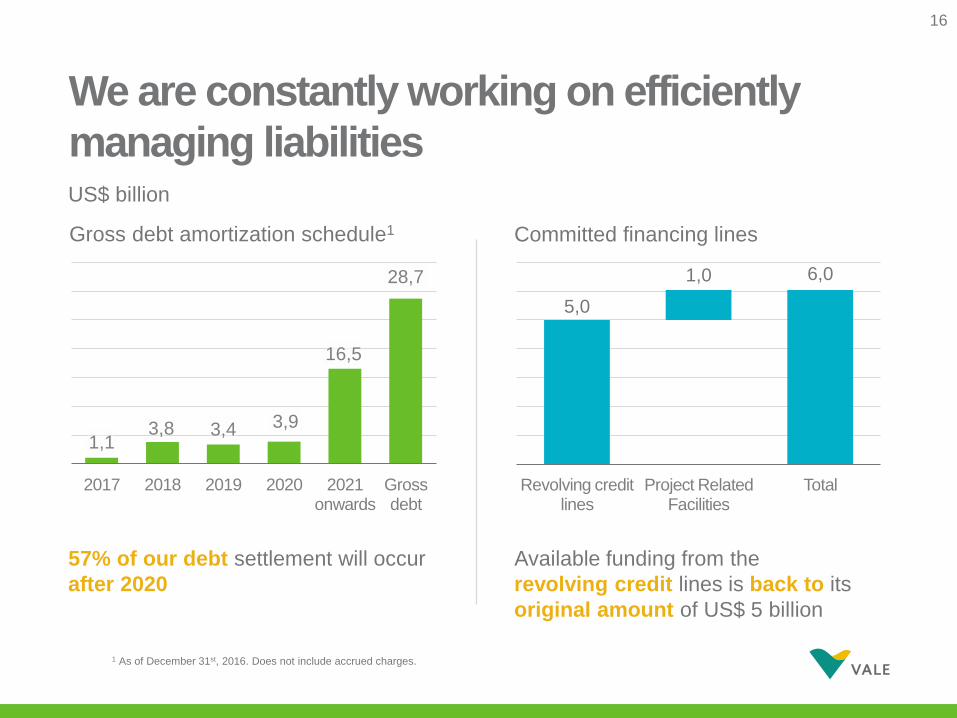

1,13,8 3,4 3,9

16,5

28,7

2017 2018 2019 2020 2021onwards

Gross debt

We are constantly working on efficiently

managing liabilities

Gross debt amortization schedule1

1 As of December 31st, 2016. Does not include accrued charges.

US$ billion

5,0

1,0 6,0

Revolving credit lines

Project Related Facilities

Total

Committed financing lines

Available funding from the

revolving credit lines is back to its

original amount of US$ 5 billion

57% of our debt settlement will occur

after 2020

16

17

Business segment

performance

18

Ferrous minerals EBITDA increased by our

efforts to reduce costs and improve pricing

5.899

2.727

244 347 357

421 212 607

86

10,476

EBITDA 2015

Price FX Bunker Commercial initiatives

Volume CFR Freight Sales

Cost saving &

productivity initiatives

Others EBITDA 2016

US$ million, 2016 vs. 2015

US$ 1,259 M

18

1

1 The negative impact of US$ 212 million in CRF freight sales was due to the higher CFR sales volumes, which increased from 189.2 Mt in 2015 to 202.4

Mt in 2016.

191 Ex-ROM

Annual cash break-even cost landed in

China for iron ore and pellets

13,3

12,2

3,6

0,5 2,6

1,7

30,5

1,5

28,9

2,6 31,5

C1 Cash Cost¹

Freight Royalties & Expenses

Distribuition Moisture Quality EBITDA Breakeven

Iron Ore fines

Pellet Adjustment

EBITDA Breakeven (pellets &

fines)

Sustaining Iron Ore & Pellets Cash Breakeven

Cost landed in China

US$/t, 2016

19

20

The right strategy – cash cost in BRL1 remains

at low levels despite inflationary pressure

55,2 54,6

50,0

46,9 46,347,5

46,1

42,2

44,8

0,73,0

4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16

1 2014 and 2015 figures were adjusted to the new allocation criteria, as reported in the 4Q15, and include acquisition costs of third party purchased ore

-13.4%

R$/tNon-recurring costs

20

21

Iron ore price realization continued to

improve in 4Q16

70,8

79,1

69,4

1,7

0,4

4,8 1,3 1,0 1,7 3,8

5,9

AveragePlatts

4Q16 (dmt)

Quality Premium/Discount and commercial

conditions

Provisionalprices in

prior quarter¹

Laggedprices

Current Provisionalprices

in currentquarter²

CFR reference price (dmt)

Adjustmentfor

FOB Sales

Moisture Vale CFR/FOB price

(wmt)³

Impact of pricing system adjustments

1 Adjustment as a result of provisional prices booked in 3Q16 at US$ 54.4/t.2 Difference between the weighted average of the prices provisionally set at the end of 4Q16 at US$ 74.6/t based on forward curves and US$ 70.8/t from the 4Q16 IODEX.3 Vale price is net of taxes.

US$/t, 4Q16

+ 8.3 US$/t

21

22

Rising contribution of higher quality new

mines and infrastructure

Price indexIron ore production from Northern System

Date IODEX 62%

(A)

Metal

Bulletin 65%

(B)

(B-A)

09/15/2016 56.3 65.5 9.2

10/31/2016 64.7 75.5 10.8

12/15/2016 81.8 94.6 12.8

01/31/2017 83.5 97.0 13.5

02/21/2017 95.1 106.2 11.1

US$/dmt¹as % of total production

1 Dmt = dry metric ton

37,5%

42,5%

2015 2016

22

23

We are as competitive as our Australian peers

despite the geographical distance

49,6

24,0

18,0 17,5

24,3

36,0

67,9

45,2

32,1

24,6 24,7

35,9

62,7

45,0

31,9

24,5 25,4

35,935,1

17,8

13,215,7

22,2

30,7

18,321,2

13,9

7,0

1,1 -0,1

-35

-25

-15

-5

5

15

0,0

10,0

20,0

30,0

40,0

50,0

60,0

70,0

80,0

1H14 2H14 1H15 2H15 1H16 2H16

Vale

Peer 1

Peer 2

Peer 3

Gap to most competitive peer, US$/t

EBITDA per ton, US$/t

23

24

450

543123

21 17 1313

3Q16 Price realization

Costs FX Expenses Volume & others

4Q16

Base Metals EBITDA up 21% q-o-q

Highlights 4Q16

Base Metals EBITDA increased US$ 93 million q-o-q1

Nickel and copper pricerealization improvedwhile LME prices increased in the same period

Nickel and copper sales volumes increased, while PGMs as a by-product decreased

Quarterly EBITDA comparison

US$ million

24

1 3Q16 net of the one-off positive effect of the goldstream transaction (US$ 150 million)

25

-7

156

-43

200

6

3Q16 Costs & expenses

Realized price FX & others 4Q16

Coal EBITDA turned around with a

significant q-o-q increase

Highlights 4Q16

EBITDA increased US$

163 million in 4Q16

The hike in coal prices

was captured in the 4Q16

due to provisional pricing

Sales of metallurgical coal

increased 19.6% as a

result of the ramp-up of

Moatize II

Moatize production costs

FOB Nacala decreased

US$ 21/t to US$ 76.8/t in

January 2017

Quarterly EBITDA comparison

US$ million

25

1

1 Costs increased due to constraints on the supply of explosives affecting the blasting process and resulting in a lower production figure compared to 3Q16.

26

Additional

information

27

Evolution of iron ore fines cash cost, freight

and expenses

12,012,8 13,2

0,1

0,5

2H15 1H16 2H16

C1 Cash Cost FOB Port1 Freight

US$/t

15,2

11,612,6

2H15 1H16 2H16

Expenses2 & Royalties

3,74,0

3,4

2H15 1H16 2H164

1 Ex-ROM and ex-royalties; all figures as per new managerial allocation changes reported in 4Q15 and including acquisition costs of third party ore.2 Net of depreciation.3 US$ 0.5/t equates to the non-recurring events of 4Q16 (US$ 0.9/t) diluted in 2H16.4 Ex bunker oil hedge.

+13.2% -17.1% -8.1%

3

Non-recurring costs

27

28

11% 10%

61%

45%

28%

45%

3Q16 4Q16

Lagged

Current

Provisional

Iron ore pricing systems

Provisional - prior quarter Lagged

Current Provisional - current quarter

1,6

4,8

3Q16 4Q16-0,4

-1,3

3Q16 4Q16

-0,8

1,0

3Q16 4Q16

-1,2

1,7

3Q16 4Q16

Pricing system breakdown Impact of pricing mechanisms

US$/t

28

29

Price realization nickel

10,810 10,803

283 290

Average LME nickel price

Price premium on refined products

Price discount on intermediate products

Average nickel realized price

29

US$/t, 4Q16

30

Price realization copper

5.277

5.063

5.497

5.093

214

434 403

Average LME copper price

Current period price adjustments

Copper gross realized price

Prior period price adjustments

Copper realized price before discounts

TC/RCs, penalties, premiums and

discounts

Average copper realized price

US$/t, 4Q16

30

31

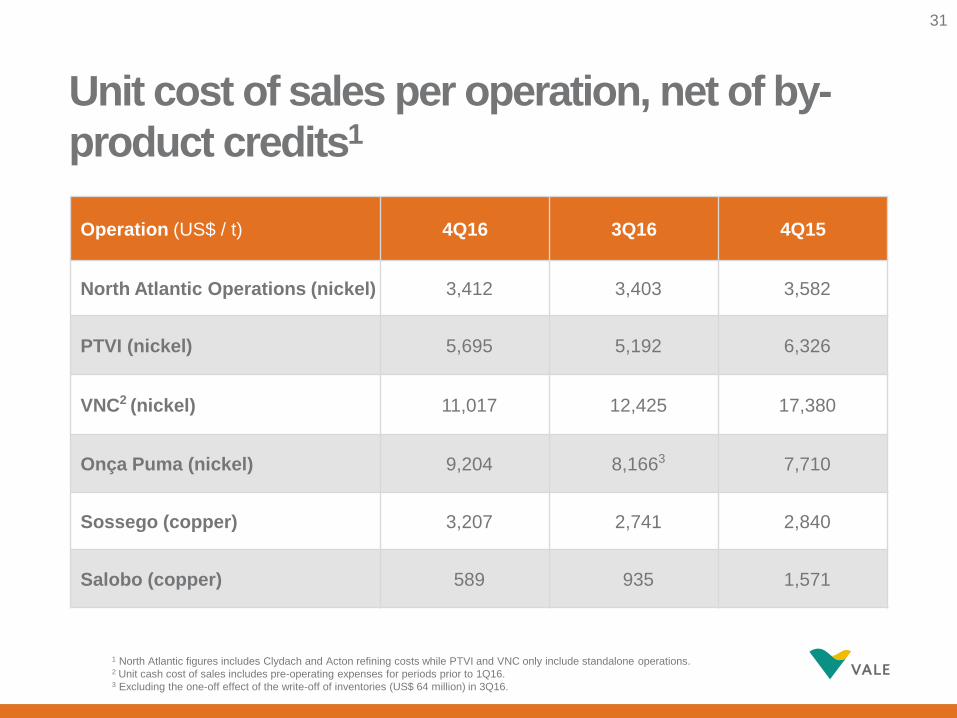

Unit cost of sales per operation, net of by-

product credits1

Operation (US$ / t) 4Q16 3Q16 4Q15

North Atlantic Operations (nickel) 3,412 3,403 3,582

PTVI (nickel) 5,695 5,192 6,326

VNC2 (nickel) 11,017 12,425 17,380

Onça Puma (nickel) 9,204 8,1663 7,710

Sossego (copper) 3,207 2,741 2,840

Salobo (copper) 589 935 1,571

1 North Atlantic figures includes Clydach and Acton refining costs while PTVI and VNC only include standalone operations.2 Unit cash cost of sales includes pre-operating expenses for periods prior to 1Q16.3 Excluding the one-off effect of the write-off of inventories (US$ 64 million) in 3Q16.

31

32

Price realization Moatize metallurgical coal

266,2

232,4

7,4

14,9 10,3 0,1 1,1

Averagereference price

4Q16

Quality Lagged priceindex

Lagged pricequarterly

benchmark

Freightdifferential

Others Valeprice

US$/t, 4Q16

32

33

Price realization Moatize thermal coal

85,4

67,9

9,4 3,5

4,6

- 5,0

10,0 15,0 20,0 25,0 30,0 35,0 40,0 45,0 50,0 55,0 60,0 65,0 70,0 75,0 80,0 85,0 90,0

Averagereference price

4Q16

Quality Index and fixed lagged price index

Commercial discount and others

Vale realizedprice

US$/t, 4Q16

33

34