valuation recent trends_2.pdf

DESCRIPTION

decribes about recent trends in valuation very important from valuation point of viewTRANSCRIPT

2010

www.clairfield.com

Part 2 : Valuation Recent Trends

2

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 2

M&A activity is driven by multiple macro-economic and industry forces and opportunities …

CHANGE IN INDUSTRY STRUCTURE

� Consolidation

� Pre-emptive M&A by competitors

� Technology advances

RISK OF UNDERPERFORMANCE

� Need to reduce debt (whilst preserving the core)

� Change in performance of different elements of the portfolio

REGULATORY AND POLITICAL PRESSURE

� Europe as a trading block post EMU

� Deregulation of global trade

� Interest in emerging markets: China etc

DESIRE FOR FOCUS AND SIMPLICITY

� Complexity of business unit

� Overload of business unit priorities

� Identification of synergies across the portfolio

Do we value them correctly?

CHANGE IN CAPITAL MARKET OPPORTUNITIES

� Availability of funding

� Investor expectations and sentiment

� Performance of stock market

� Relative values of stock prices versus hard assets

SEARCH FOR GROWTH OPPORTUNITIES

� Extend geographic coverage

� Acquire complementing assets

� Extend within or across industries

World M&A UK M&A

Note: Includes all cross border and domestic deals completed 1st Jan 2004 - December 2007. Excludes MBOs &

Privatisations.

Source: Datalogic, Thomsom Financial, KPMG analysis

0

UK Cross Border

UK Domestic

World Half-Year TotalTelecoms specific

2006 2007 20082004 20052004 2005 2006 2007

0

100

200

300

H1 H2 H1 H2 H1 H2 H1 H2 H1

£billion

200

600

1,000

1,400

£billion

H1 H2 H1 H2 H1 H2 H2 H1H1

2008

H2H2

3

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte

Buy-side deals are becoming more successful…

SELL-SIDE EXPERIENCE

� 35% of vendors completed their most recent disposal at a price significantly below their own valuation

� Of these, an average 20% price reduction from valuation to selling price was experienced

� 60% of all vendors suffer post deal issues

BUY-SIDE EXPERIENCE

Deals addingvalue

Deals that do not add value

Source: KPMG survey ‘Increasing value from disposals – A case study for professionalising the sell side’ - 2009

Source: KPMG survey ‘Beating the Bears’ - 2008

… but that sell-side activities are becoming more challenging

Value creation

17%31% 34%

30%

38% 34%

53%

31% 32%

0%

20%

40%

60%

80%

100%

1999 2004 2007

Enhance value Neutral Reduce value

4

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 4

Almost 70% of deals add no value

Source: Financial News, Briefing Note 19, 17 Sept 2001, Offer Information Week

UK-WIDE M&A VALUE CREATION WHY MERGERS FAIL

Underestimating the management effort required to realise benefits is the primary reason for failure to deliver value from mergers

Deals destroyed value

Deals produced no discernible difference

Deals added value

Source: KPMG surveys

2001 2008

17

30

30

39

53

31

0%

20%

40%

60%

80%

100%

% of deals

Deals that do notadd value

Deals that do add value

60%

43%

38%

36%

33%

30%

28%

18%

14%

0 10 20 30 40 50 60 70

Resistance to Change

Limitations of Existing Infrastructure

Lack of Executive Alignment

Lack of Executive Champion

Unrealistic Expectations

Lack of Cross-Functional Teams

Inadequate Team and User Skills

Key Stakeholders Not Involved

Project Charter Too Narrow

Contribution to Merger Failure (%)

5

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 5

Operational improvements:e.g, improved back office

processes, expanded customer service functionality, etc.

Operational performance improvement is recognised as being key to realising value from transactions

– “1992 was the last time the most

common form of exit was

receivership, as it is now.”(1)

– “The ability to supplement deal

skills with appropriate management

expertise will allow proactive

assistance to be given to portfolio

companies to add to product

value.”(2)

– “I wonder if people are coveting

operational skills simply because

they are more operationally

involved in the businesses at the

moment than they want to be

[because of under-performance].”(3)

Source: (1) Jon Moulton, Managing Partner, Alchemy

Partners, Super Return 2002 Conference

(2) KPMG/Manchester Business School Survey

(3) Simon Turner, joint Chief Executive

Inflexion, FT February 28

RATIONALE FOR DEAL

Consideration Value Creation

DealCosts

Price Paid

Premium

Standalone Value

SynergiesNew

Strategies

Value £m

Create Shareholder

Value

Destroy Shareholder

Value

Sales growth

Product development

Operational factors

Rationalisation of manufacturing

Almost 70% of deals add no value, why?

6

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 6

Choosing Valuation Methods

Market MethodsMarket Methods

Economic MethodsEconomic Methods

Asset-Based MethodsAsset-Based Methods

There are basically three valuation methods (market, asset-based and economic methods) which contain many models.

For example, under economic methods, there are three main models - DCF, Economic Profit (EVA, ROIC and CFROI) and option pricing models.

Within DCF models there are further sub-models depending on whether you are discounting dividends, FCFE or FCFF.

Even within each sub-model, further choices can be made as to whether 2-stage, 3-stage or multi-stage explicit growth periods are used.

Economic Methods

Economic Profit

APV Model

DCF Models

FCFF

FCFE

Dividend

Discount

Option Pricing

7

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 7

Prior Theories of valuation

• Miller and Modigliani – the “primitive firm” (1963)– Expected free cash flows from operations

– Discounted at a constant weighted average cost of capital

– Assumes that operating cash flows are unaffected by capital structure

– Optimal capital structure a tradeoff between the benefit of a debt tax shield and the present value of business disruption costs

• Leland – Four terms in the valuation equation (1998)– Value of the unlevered firm– PV of the tax shield on debt– Minus the PV of tax shield lost if debt becomes extreme– Minus the PV of business disruption costs (as a function of debt)

8

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 8

• Schwartz and Moon (1999)

– The value of the primitive firm is enhanced by real options

– They model the value of an abandonment option

– Other real options are also important:

• Growth options (Myers 1977)

• Options to exit and re-enter

• Options to abandon (liquidate)

• Options to enter and exit Chapter 11

Prior Theories of valuation

9

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 9

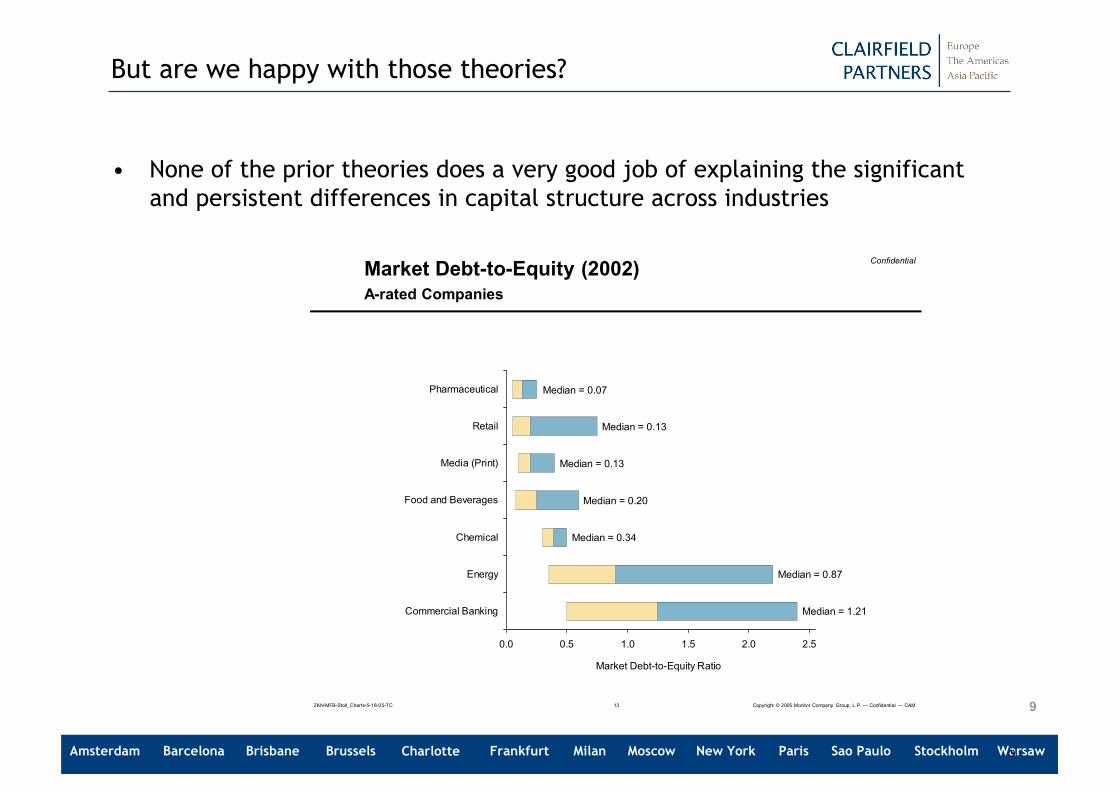

But are we happy with those theories?

• None of the prior theories does a very good job of explaining the significant and persistent differences in capital structure across industries

Confidential

Copyright © 2005 Monitor Company Group, L.P. — Confidential — CAMZKN-MFB-Stoll_Charts-5-18-05-TC 13

Market Debt-to-Equity (2002)A-rated Companies

0.0 0.5 1.0 1.5 2.0 2.5

Commercial Banking

Energy

Chemical

Food and Beverages

Media (Print)

Retail

Pharmaceutical Median = 0.07

Median = 0.13

Median = 0.13

Median = 0.20

Median = 0.34

Median = 0.87

Median = 1.21

Market Debt-to-Equity Ratio

10

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 10

The Reality – a new theory of the firm

• A firm is like a three-layer cake:– The cost of debt is suboptimal exercise of the firm’s real options and the benefit is its tax

shield– Greater operating flexibility allows for greater debt capacity

Financial Options — Debt and Equity are options on the firm’s

portfolio of assets (with flexibility)

Real Options — Payouts on the portfolio of assets are modified by real options (e.g., capacity caps, expansion, and bankruptcy)

The primitive firm is modeled without flexibility (DCF)

Financial Options

Real Options

The Primitive Firm

11

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 11

New trends in Valuation Methodologies

Comparable Multiples

Discounted Cash Flow (the primitive firm)

New trends such as APV, EVA and Monte Carlo

Option Pricing: real options

Option Pricing: financial options

The future of valuation: the firm as a 3-layer cake

12

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 12

Comparable Multiples:

Valuation based on actual transactions

• First, we should acknowledge that

– There are rarely any close comparables

– Often neither the assets nor the liabilities have liquid markets for trading

• All comparables are going concerns

• Recommended approach is a multiple regression

V (houses) = a + b (number of square feet)

+ c (number of rooms)

+ d (age of house)

+ e (acreage)

+ f (number of fireplaces)

+ g (taxes)

+ h (swimming pool)

Entity multiple = a + b (earnings before interest and taxes)

+ c (growth in earnings)

+ d (capital turnover)

+ e (return on invested capital)

13

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 13

Traditional DCFlow Valuation – the primitive firm

Most valuations of non-financial companies start with estimated free-cash flows to the entity, discount them at the weighted average cost of capital, then subtract out the value of debt

+CV=Entity Value

Discounted at the weighted average cost of capital

PV of (Expected Free Cash Flows + Continuing Value) = Entity Value

14

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 14

DCF - Predicted FCF follow an irregular pattern

-10

0

10

20

30

40

50

60

70

1 2 3 4 5 6 7 8 9 10

($ millions, 2004-2014)

Free Cash Flows of company X could be

Revenue growth:-- one year 31.6%-- 3-5 years 17.5%-- long-term 10.2%

15

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 15

DCF Valuation

The continuing value (CV) assumptions are also crucial

– Will the company’s ROIC fall to equal its WACC or remain at current levels?

– What is the cost of capital given the two alternatives?

– How will its cost of capital change, and what will its value drivers be? E.g., revenue growth, operating margin, capital turns?

– Which Continuing Value formula should one use?

– Are the ROIC and growth assumptions consistent with the assumed amount of earnings retention?

x

gWACC

rgNOPLATCV

1.3 multipleExit

x(243)1.10NOPLAT x multiple

)/1(

6.26ue/EBITDAMarket valEntity multipleEntry

11

=

==

−

−=

==

16

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 16

Frequency Chart

.000

.009

.018

.026

.035

0

8.75

17.5

26.25

35

-75% -31% 13% 56% 100%

1,000 Trials 4 Outliers

Forecast: Expected Annual Return

DCF Valuation (Cont.)

• A model in evolution

– From fixed discount rate to iteration process

– From fixed WACC to changing wacc per year

– From mono input to Monte Carlo Analysis

31/12/2005 31/12/2006 31/12/2007 31/12/2008 31/12/2009 31/12/2010

Equity 1.184.838 2.963.995 3.092.459 3.277.123 3.497.139 3.752.617

Debt 1.066.826 803.598 2.643.064 2.727.972 2.637.111 2.497.997

Total 2.251.664 3.767.593 5.735.523 6.005.095 6.134.250 6.250.614

Ratio equity 52,6% 78,7% 53,9% 54,6% 57,0% 60,0%

Ratio debt 47,4% 21,3% 46,1% 45,4% 43,0% 40,0%

Levered beta 0,71 0,52 0,69 0,69 0,66 0,64

WACC 7,71% 9,14% 7,78% 7,82% 7,95% 8,12%

XYZ NV

Cash flows in EUR per : 31/12/2006 31/12/2007 31/12/2008 31/12/2009 31/12/2010 31/12/2011 31/12/2012 31/12/2013 31/12/2014 31/12/2015 RV

EBIT 457.502 365.590 510.021 703.419 723.840 921.384 827.735 831.074 834.476 837.939 837.939Depreciation 87.879 247.410 249.279 243.119 258.344 225.011 228.692 245.853 263.351 281.192 281.192

Taxes on EBIT (-) (142.614) (114.860) (161.168) (225.918) (230.519) (295.161) (259.580) (254.865) (250.320) (245.335) (245.335)

Net operating cash flow 402.768 498.140 598.133 720.620 751.665 851.234 796.847 822.062 847.506 873.796 873.796

Investment Formation Expenses 0 0 0 0 0 0 0 0 0 0

Investments Intangible Assets 0 0 0 0 0 0 0 0 0 0

Investments Tangible Assets 0 1.680.000 119.740 138.465 152.250 164.426 168.311 171.612 174.978 178.410 281.192

Investments Leasing 0 0 0 0 0 0 0 0 0 0

Divestment leasing 0 0 0 0 0 0 0 0 0 0

Investments Net Working Capital Long Term (695) (709) (723) (738) (752) (767) (783) (798) (814) (831)

Investments Net Working Capital Short Term (185.007) 440.979 287.081 213.634 186.047 31.372 62.900 49.063 49.839 51.939 0

Free Cash Flow 588.470 (1.622.130) 192.035 369.259 414.120 656.203 566.418 602.186 623.503 644.277 592.605

WACC 9,14% 7,78% 7,82% 7,95% 8,12% 8,45% 8,96% 9,53% 9,72% 9,69% 9,69%

Present Value of annual future FCF 539.176 (1.396.308) 153.179 271.829 280.230 403.134 310.570 290.537 270.385 255.354 2.423.625

Present Value of future FCFs 1.378.085

Present Value of Residual Value 2.423.625

Excess marketable securities as per 31-dec-05 0

Financial Assets (+) / Hidden liabilities (-) 0

Value of Company as per 31-dec-05 3.801.710 EQUITY VALUE AS OF 30/06/2006 2.763.708 EURDebt as at (-) 31-dec-05 (1.066.826)

Value of Equity as at 31-dec-05 2.734.884 in Euro 2.763.708 000 €

Equity value as of 31-dec-05 2.734.880

Equity value as of 30-jun-06 2.763.708

17

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 17

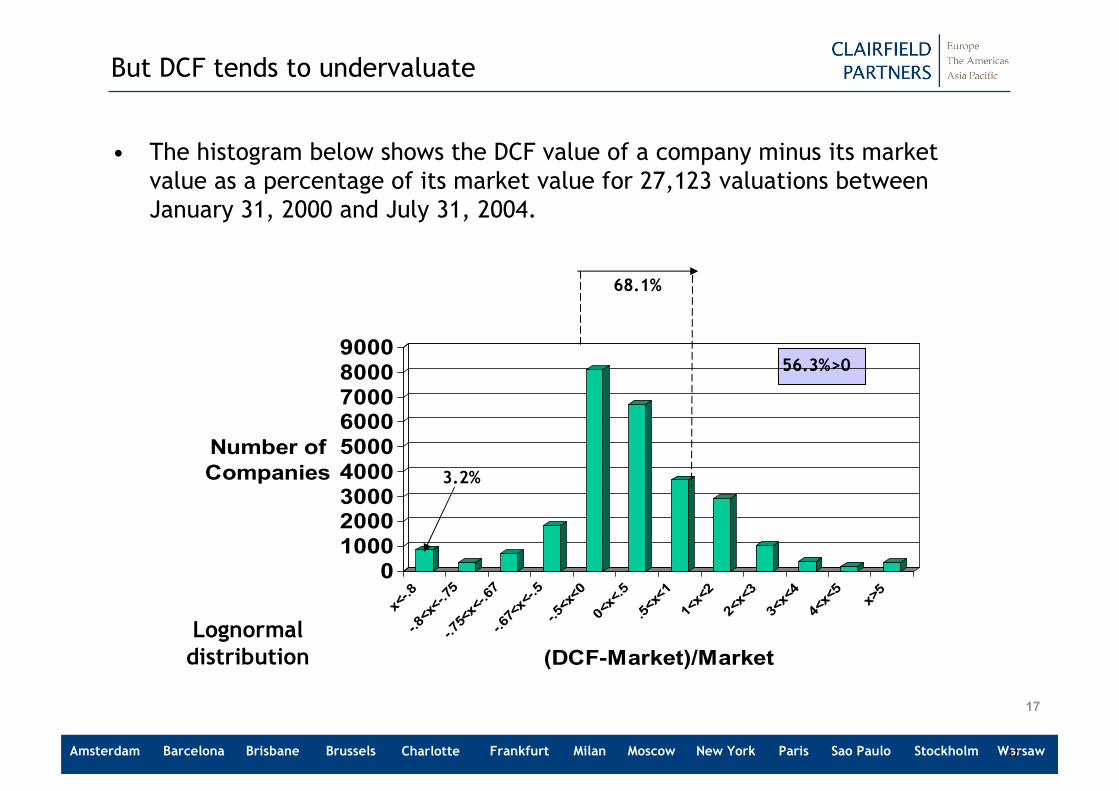

But DCF tends to undervaluate

• The histogram below shows the DCF value of a company minus its market value as a percentage of its market value for 27,123 valuations between January 31, 2000 and July 31, 2004.

0100020003000400050006000700080009000

Number of Companies

x<-.8

-.8<x

<-.7

5-.7

5<x<

-.67

-.67<

x<-.5

-.5<x

<00<

x<.5

.5<x

<1

1<x<

2

2<x<

3

3<x<

4

4<x<

5

x>5

(DCF-Market)/Market

68.1%

3.2%

Lognormaldistribution

56.3%>0

18

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 18

Bias in the DCF model?

• We hypothesize that DCF works well for large, diversified companies that have low volatility and low growth, but undervalues companies that have high volatility and high growth. Cells Contain median difference between DCF and market value at the end of a month scaled by market value.

Lowestg<5.3% g<7.9% g<10.9 g<16.3%

Highestg<113.4%

Lowestv<1.50x

5.4%1,463

1.1% 1,518

8.7%1,344

7.7%861

40.4%239

v<1.82x 12.9%

1,21810.6%1,384

13.6%1,281

18.4%1,044

3.0%497

v<2.22x27.6%1,091

19.9%1.197

20.2%1,130

15.8%1,150

9.4%857

v<2.91x50.7%

99434.7%

79816.7%1,031

2.7%1,326

-3.1%1,275

Highestv<660.5x

51.4%659

21.8%527

2.9%639

-7.3% 1,043

-21.7%2,555

Analyst projection of 3-5 year revenue growth

Volatility one

Year forwardas a % of

SPX volatility

19

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 19

Criticism on DCF

False mutually exclusive scenarios

Volatility ignored

A key driver of value given option-pricing methodology

Difficult to incorporate in a DCF approach

Does not capture value of flexibility (real options)

Abandonment (divestiture, close-down)

Expansion/growth (greenfield, M&A)

20

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 20

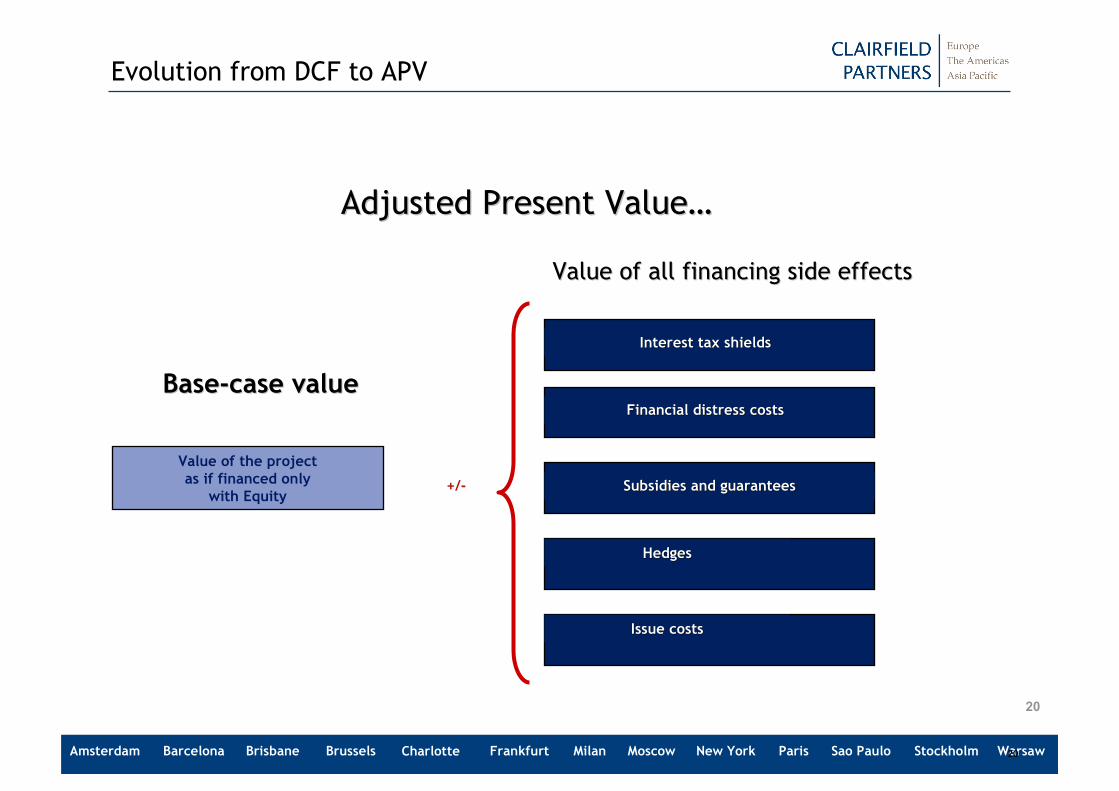

Adjusted Present ValueAdjusted Present Value……

Value of the projectas if financed only

with Equity

Interest tax shieldsInterest tax shields

Financial distress costsFinancial distress costs

Subsidies and guaranteesSubsidies and guarantees

HedgesHedges

Issue costsIssue costs

+/-

BaseBase--case valuecase value

Value of all financing side effectsValue of all financing side effects

Evolution from DCF to APV

21

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 21

How Does the APV Model Work?

1. Value the firm as if it were financed entirely with equity

2. Evaluate the financing side effects of the interest tax shield

3. Assess the costs of financial distress

4. Estimate the other financing side effects

5. Aggregate the components to arrive at an enterprise APV value

22

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 22

Specific Applications for the APV Model

1. Changing debt structures (eg. LBOs and MBOs)

2. Multi-business valuations (especially HQ functions)

3. Tax loss carry forward situations

4. Project finance

5. Optimizing debt levels

6. Presenting synergies

7. As a quick sanity check

WACCWACC

APV tends to APV tends to infinityinfinity

EnterpriseEnterprisevaluevalue

GearingGearinglevelslevels

The Gap The Gap betweenbetween APV APV and WACC and WACC isis the the costcost

of of bankruptcybankruptcyWACCWACC

APV tends to APV tends to infinityinfinity

EnterpriseEnterprisevaluevalue

GearingGearinglevelslevels

The Gap The Gap betweenbetween APV APV and WACC and WACC isis the the costcost

of of bankruptcybankruptcy

23

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 23

What is EVA™

1. Registered trademark of Stern, Stewart & Co

2. Performance measure

3. Re-arrangement of DCF

4. Positive EVA implies shareholder value creation

5. McKinsey’s EVA is called ROIC Economic Profit Models

Residual Income Models

CFROI

EVAROIC

New trends in valuation …

24

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte

Economic Value Added defined

• EVA is the profit (or loss) remaining after deducting the cost of capital from the operating profit after taxes.

• EVA measures the shareholder value created (or destroyed) over a certain period. EVA shows that a company creates value only if operating earnings are sufficient to earn back its cost of capital

EVA = NOPAT – ((Cost of Capital) x (Capital))

EVA = Net assets x (RONA – WACC)

25

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 25

Real Options (the second layer) -- Value trees

FCF -9 4 22 54

1320

Positive cash flows are dividends while negative cash flows are investments. All cashflows are proportional to the value in each state of nature so that expected cash flows

are preserved

Valueat year t

Company X

Volatility = 97%

U= 2.65 = eσ√T

D = .38 = 1/u

P=.32

26

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 26

The firm’s real options…

1. Real options is the term used to denote the explicit valuation of

the opportunities associated with changing decisions in response

to the resolution of relevant uncertainty.

2. A real option is the right, but not the obligation, to take an action

(eg deferring, expanding, contracting or abandoning) at a

predetermined cost (exercise price), for a predetermined period

(Stewart Myers, MIT)

Invest

Don’tInvest

Bad news

Bad news

Good news

Good news Cash flow

Cash flow

Cash flow

Cash flow

Invest

Don’tInvest

Bad news

Good news

Cash flow

Cash flow

Cash flow

Cash flowInvest

Don’tInvest

This is not an option This is an option

27

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 27

A real option is the right, but not the obligation, to take an action in the future upon the receipt of information. A call is the right to buy (or invest) at a fixed price, and a put is the right to sell.

Examples:

Defer

Expand

Extend

Shrink

Abandon

Five factors affect the value of an option

Value of an underlying asset (+)

Exercise price (-)

Volatility (+)

Time to expiration (+)

Risk-free rate (+)

What is a Real Option?

Simple OptionsProbability

of V

Higher volatility increases the probability of finishing in-the-

money where V > D

D V

28

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 28

Compound Options are options on options

– Phased construction

– Research and development

– New product development

– Exploration and production

– Equity in a levered firm

– Call option on equity

Switching Options

– Shutting down and reopening

• Mines

• Automobile assembly plants

– Exit and reentry

– Turning off then on

• Peak load power plants

– Switching between modes of operation

• Dual fuel power plants

•Rainbow options (multiple sources of uncertainty)

– Price and quantity uncertainty

– Quadranomial

A Few War Stories That Introduce More Real Options

Sequential

Simultaneous

Examples

$650 million chemical plant

$7,000 million high-tech clean room

Examples

Valuation of peak-load power

Exit from PC assembly

Exit from aerospace division

Mine operation

Depends on

Switching cost

Volatility of underlying

Non-recombining binomial tree

Example

$1,000 million oil field development

29

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 29

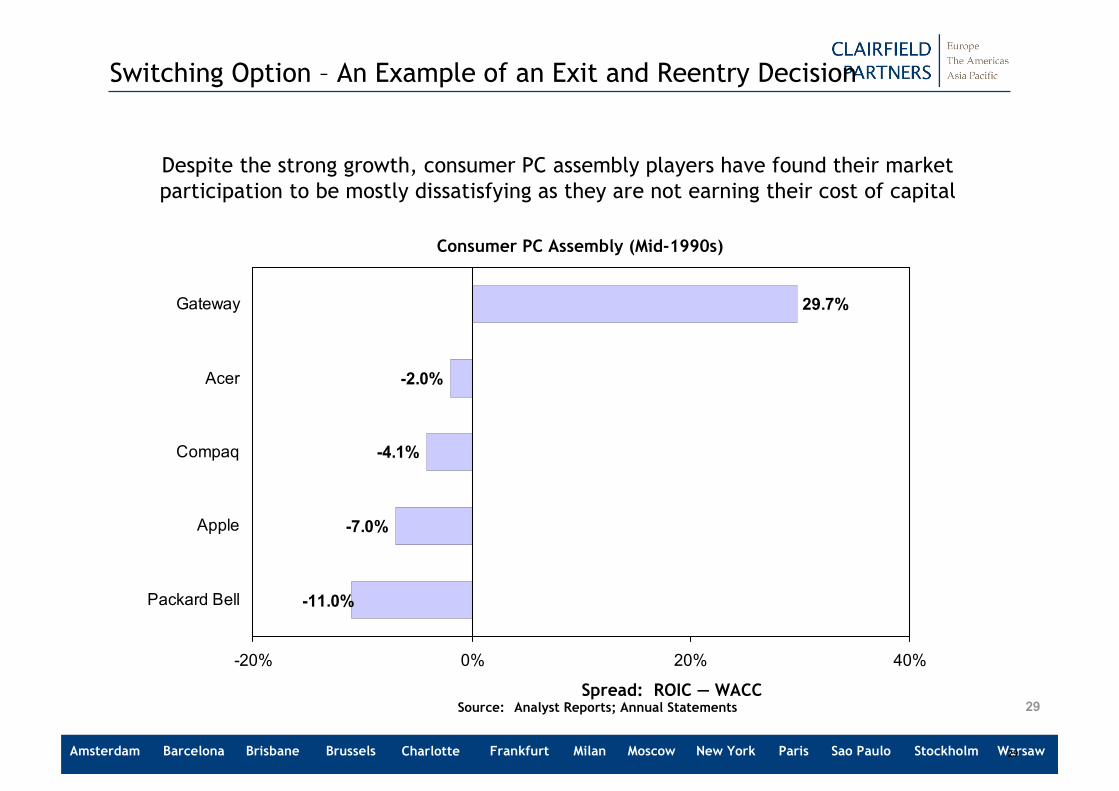

Despite the strong growth, consumer PC assembly players have found their market participation to be mostly dissatisfying as they are not earning their cost of capital

Switching Option – An Example of an Exit and Reentry Decision

Source: Analyst Reports; Annual Statements

-7.0%

-4.1%

-2.0%

29.7%

-11.0%

-20% 0% 20% 40%

Packard Bell

Apple

Compaq

Acer

Gateway

Consumer PC Assembly (Mid-1990s)

Spread: ROIC — WACC

30

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 30

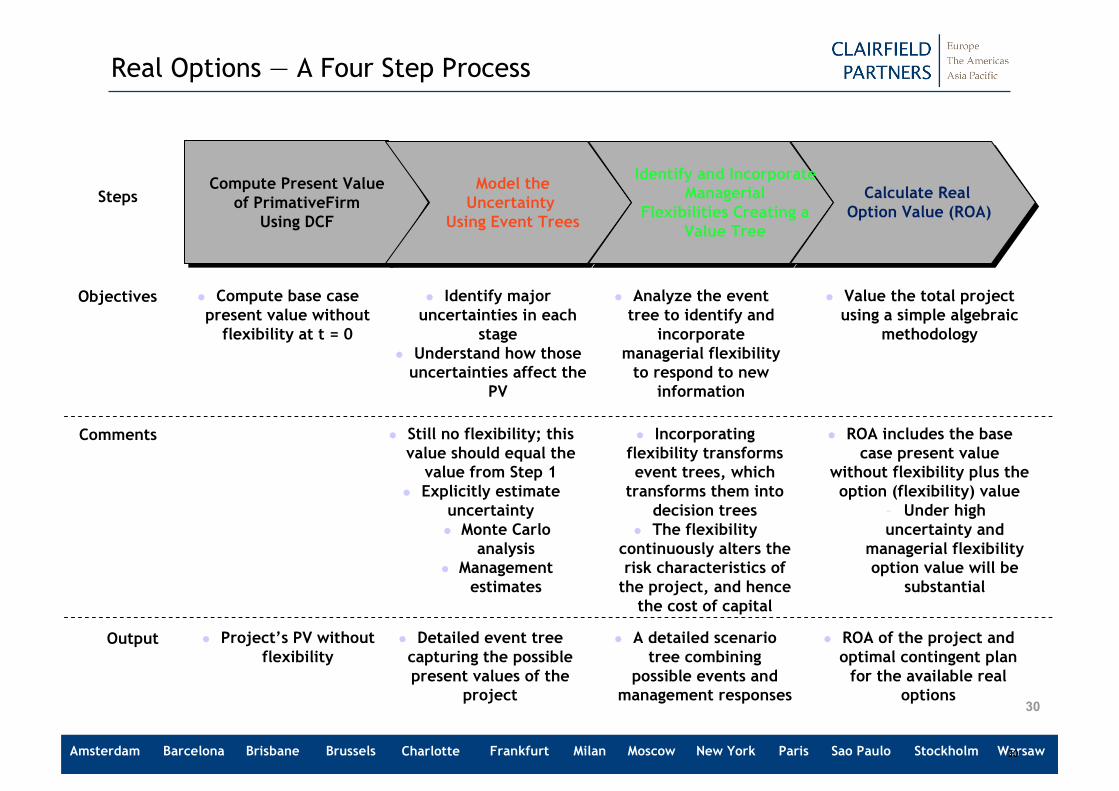

Real Options — A Four Step Process

Objectives

Comments

� Compute base case present value without flexibility at t = 0

� Value the total project using a simple algebraic

methodology

� Identify major uncertainties in each

stage� Understand how those uncertainties affect the

PV

� Analyze the event tree to identify and

incorporate managerial flexibility to respond to new

information

� Still no flexibility; this value should equal the value from Step 1

� Explicitly estimate uncertainty� Monte Carlo

analysis� Management

estimates

� Incorporating flexibility transforms event trees, which transforms them into

decision trees� The flexibility

continuously alters the risk characteristics of the project, and hence the cost of capital

� ROA includes the base case present value

without flexibility plus the option (flexibility) value

– Under high uncertainty and

managerial flexibility option value will be

substantial

Steps

Output � Project’s PV without flexibility

� Detailed event tree capturing the possible present values of the

project

� A detailed scenario tree combining

possible events and management responses

� ROA of the project and optimal contingent plan for the available real

options

Model theUncertainty

Using Event Trees

Identify and Incorporate Managerial

Flexibilities Creating a Value Tree

Calculate Real Option Value (ROA)

Compute Present Valueof PrimativeFirm

Using DCF

31

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 31

Financial Options -- the third layer

• The cumulative cash flow along each possible path determines the cash available for payment of zero-coupon debt.

• The equity is an option on the second layer of the cake

• And the real options on the second layer are options on the primitive firm.

• Assumptions:

1. Cumulative cash flows calculated along each path

2. Zero coupon debt

• Due if liquidation occurs

• Otherwise due in year 10

• At face value

3. Liquidation value

4. Growth (Expansion) option

• Expansion factor = X%

• Execution cost = $xxx million

5. Equity is an option on the firm with real options – residual CF is valued

32

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 32

With and Without Debt – Interactive boundary conditions

-100

0

100

200

300

400

500

600

700

800

900

0 1 2 3 4 5 6 7 8 9 10

Cumulative Cash w/o Debt Cumulative Cash w/ Debt

0

500

1000

1500

2000

2500

0 1 2 3 4 5 6 7 8 9 10

Entity Value w/o Debt Entity Value w/ Debt

This panel shows that the entity value (layer 2) is affected as one adds debt in layer 3 – the abandonment decision

without debt is altered when the firm takes on (zero coupon) debt because abandonment (liquidation) amounts to early payment, therefore abandonment

occurs later with debt.

Here abandonment takes place in year 7 when there is no debt. But if there is debt, abandonment is deferred because the entity

value is greater than the residual after liquidation and debt payment.

33

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 33

Optimal Capital Structure

322

411

329

247

169

84

494

194145

102

52

169

172

217

160

102

67

320

100

200

300

400

500

0 500 1,000 1,500 2,000 2,500 3,000

Tax Benefit of Debt

Cost of Debt –suboptimal exercise of abandonment

Net Benefit of Debt

Parameters

Tax rate = 20%Abandonment price =

$1,100

$ Value

Debt

34

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte 34

Next Steps

• Extension from value branch to value tree

– Need to study ways of estimating volatility

– Model growth as a series of one-period European call options

– Capture inter-dependency between financial and real options

– Optimal capital structure is tradeoff between

• Cost of debt as suboptimal exercise of abandonment and growth options

• Benefit of debt as tax shelter

– Explains why

• DCF undervalues high growth and high volatility situations

• There are cross-sectional regularities in debt-to-equity ratios

• CFOs say that flexibility is the single most important variable

when considering capital structure

35

Amsterdam Barcelona Brisbane Brussels Frankfurt Milan New York Paris StockholmSao Paulo WarsawMoscowCharlotte

2010

+32 475 44 46 32www.clairfield.com

Syncap Management gmbh, member of Clairfield Partners

Hans Buysse, Partner