value-add winn dixie retail center - turnvest cre marketing

TRANSCRIPT

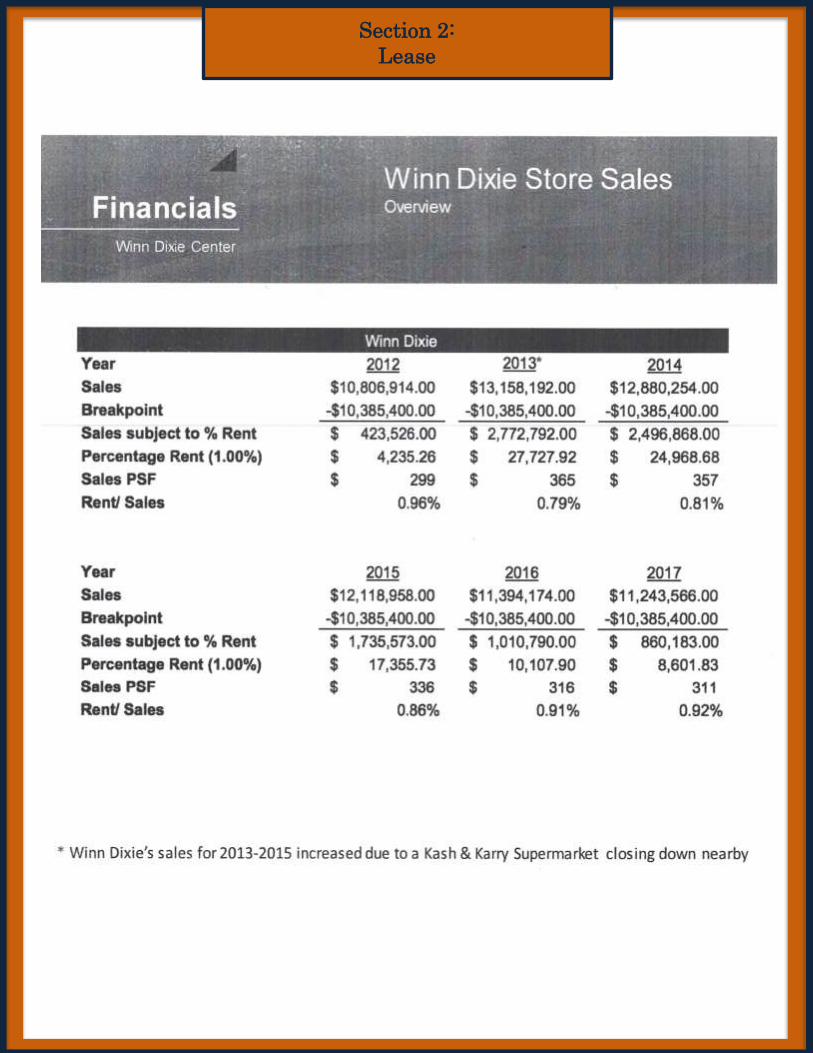

Winn Dixie

5802 54th Avenue N

Kenneth City, FL 33709

For More Information Contact:

John Burpee

727 828 9498

John Burpee & Associates

Commercial Real Estate Brokers, Inc.

11683 87th Street N

Largo, FL 33773

727-828-9498

BurpeeCommercial.com

Value-Add Winn Dixie Retail Center

Confidentiality Agreement and Disclaimer

This will serve as notice regarding the use of

certain material, data and information

contained herein (“Evaluation Material”)

which we have made available to you in

connection with a possible purchase of the

property by you or your client. As a

prerequisite to your accepting and utilizing the

Evaluation Material, you hereby represent and

agree as follows:

The Evaluation Material furnished by us will

be used solely for evaluating a possible

transaction exclusively for your own account,

as principal in the transaction, and not as a

broker or agent for any other person.

Therefore, you agree to keep all Evaluation

Material strictly confidential; provided

however, that any of such Evaluation Material

may be disclosed to your directors, officers or

employees as well as your counsel, accounting

firms and financial institution who need to

know such information of the purpose of

assisting you with your possible purchase of

the Property. Such directors, officers

employees, lawyers, financial institutions and

accountants shall be informed by you of the

confidential nature of such information and

shall be directed by you to treat such

information with strict confidence.

Although we have endeavored to include in the

Evaluation Material, information which we

believe to be accurate and relevant for the

purpose of helping you in your evaluation of

the Property for possible purchase, you

understand and acknowledge that neither the

Owner of the Property nor John Burpee &

Associates (“Agent”) make any representation

or warranty as to the accuracy or completeness

of the Evaluation Material except as set forth

in a definitive agreement. You agree that

neither the Owner nor the Agent shall have

any liability to you as a result of your use of

the Evaluation Material except as set forth in a

definitive agreement and it is understood that

you are expected to perform such due diligence

investigations and inspections of the Property

as you deem necessary or desirable and as

permitted by agreement with the Owner of the

property.

You also represent that no broker or agent

represents you or will represent you in any

possible transactions involving the Property

unless you disclose it in writing to John

Burpee & Associates prior to the receipt of the

Evaluation Material and you fully agree to

compensate your broker or agent. Neither

Agent nor the Owner is responsible for any

compensation to be paid to your broker or

agent whatsoever.

Table of

Contents

Section 1.

Section 2.

Section 3.

Section 4.

Section 5.

Section 6.

Section 7.

Section 8.

Executive Summary

Property Details

• Property Info

• Taxes

• Tenant Info

• Lease

Proforma

Location Overview

Property Photos

Sales Comps

• Sales Volume

• Sales Pricing

• Peer Comparison

Vacancy Rates

Demographics

• Summary

• Traffic Counts

• Growth Trends

• Market Summary

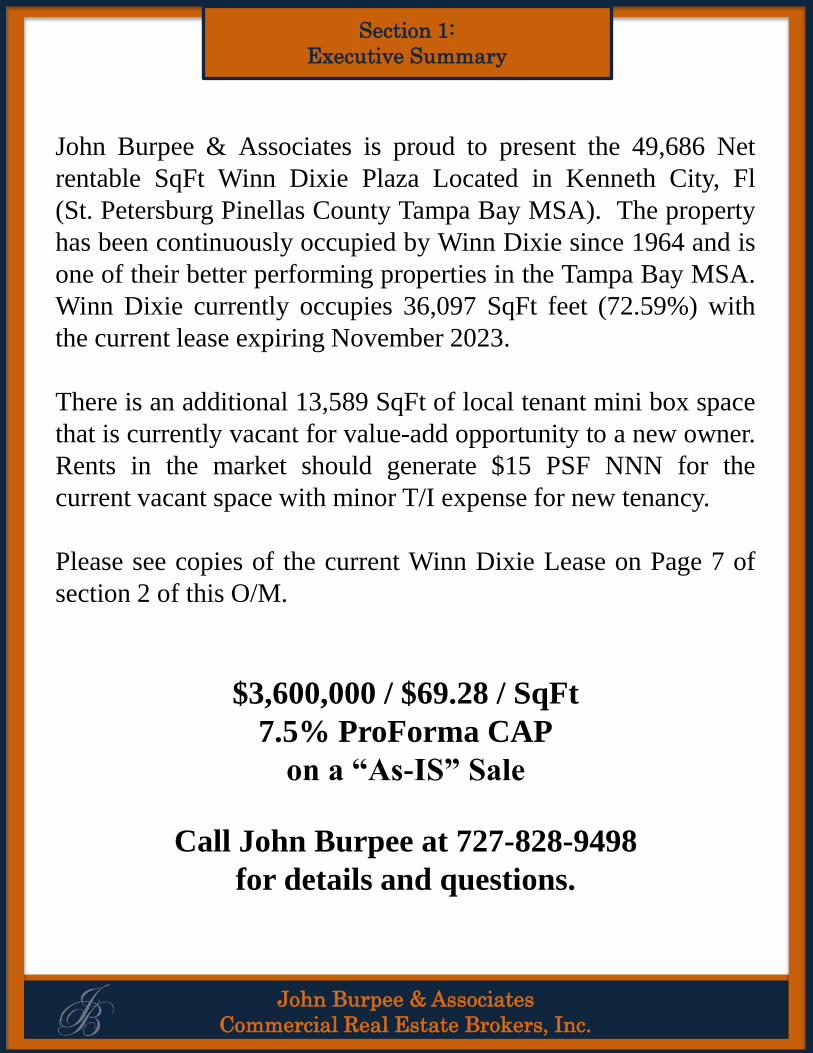

John Burpee & Associates is proud to present the 49,686 Net

rentable SqFt Winn Dixie Plaza Located in Kenneth City, Fl

(St. Petersburg Pinellas County Tampa Bay MSA). The property

has been continuously occupied by Winn Dixie since 1964 and is

one of their better performing properties in the Tampa Bay MSA.

Winn Dixie currently occupies 36,097 SqFt feet (72.59%) with

the current lease expiring November 2023.

There is an additional 13,589 SqFt of local tenant mini box space

that is currently vacant for value-add opportunity to a new owner.

Rents in the market should generate $15 PSF NNN for the

current vacant space with minor T/I expense for new tenancy.

Please see copies of the current Winn Dixie Lease on Page 7 of

section 2 of this O/M.

John Burpee & Associates

Commercial Real Estate Brokers, Inc.

Section 1:

Executive Summary

Call John Burpee at 727-828-9498

for details and questions.

$3,600,000 / $69.28 / SqFt

7.5% ProForma CAP

on a “As-IS” Sale

II. PROPERTY DETAILS

John Burpee & Associates

Commercial Real Estate Brokers, Inc.

Section 2:

Property Details

Type: 2 Star Retail Storefront

Stories: 1 Year Built: 1963

Avg. Unit Size: 772 Year Renovated: 2014

Stories: 1 Ceiling Height: 24’6”

GLA: 51,964 SF Construction: Masonry

Docs: 1 Ext Building Depth: 120’

Parking 232 Surface Spaces / 4.66 per/1,000 SF

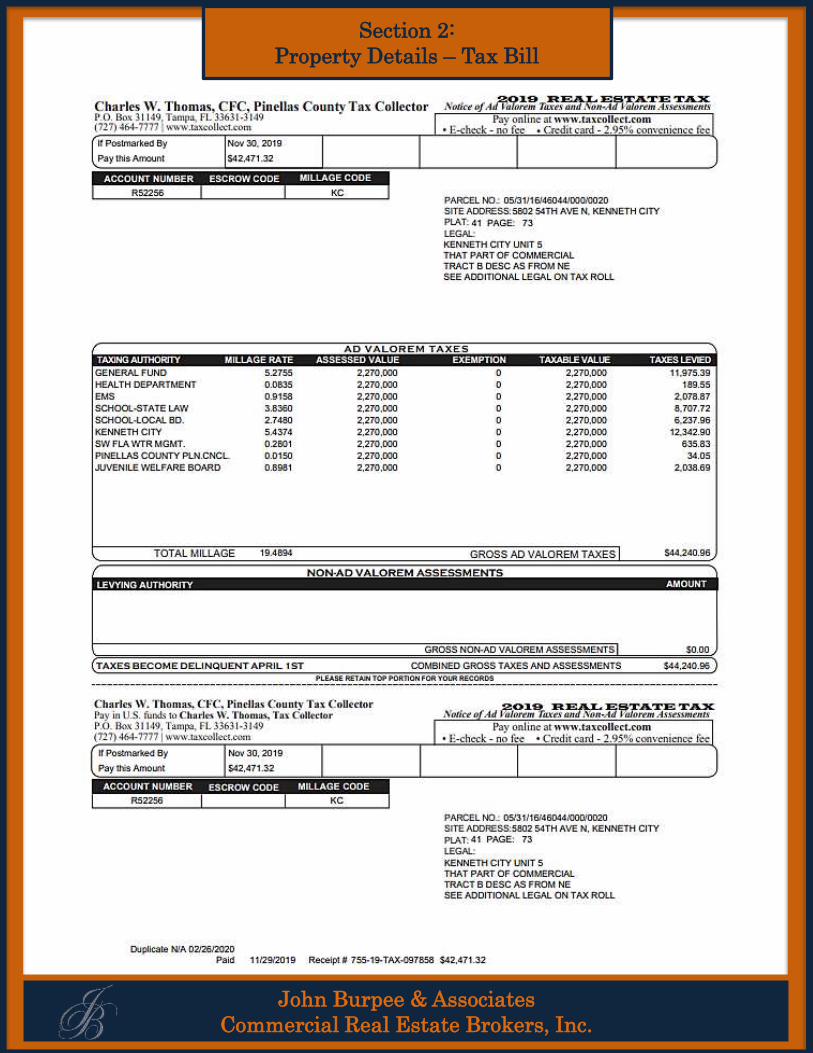

2018 Taxes: $.95/SF

Parcel ID: 05-31-16-46044-000-0020

Land Acres: 3.75 AC Land SF: 163,350 SF

Dimensions: 383’ x 683’ Building FAR 0.32

Building

Land

Amenities

Air Conditioning

II. PROPERTY DETAILS

John Burpee & Associates

Commercial Real Estate Brokers, Inc.

Section 2:

Property Details – Tax Bill

II. PROPERTY DETAILS

John Burpee & Associates

Commercial Real Estate Brokers, Inc.

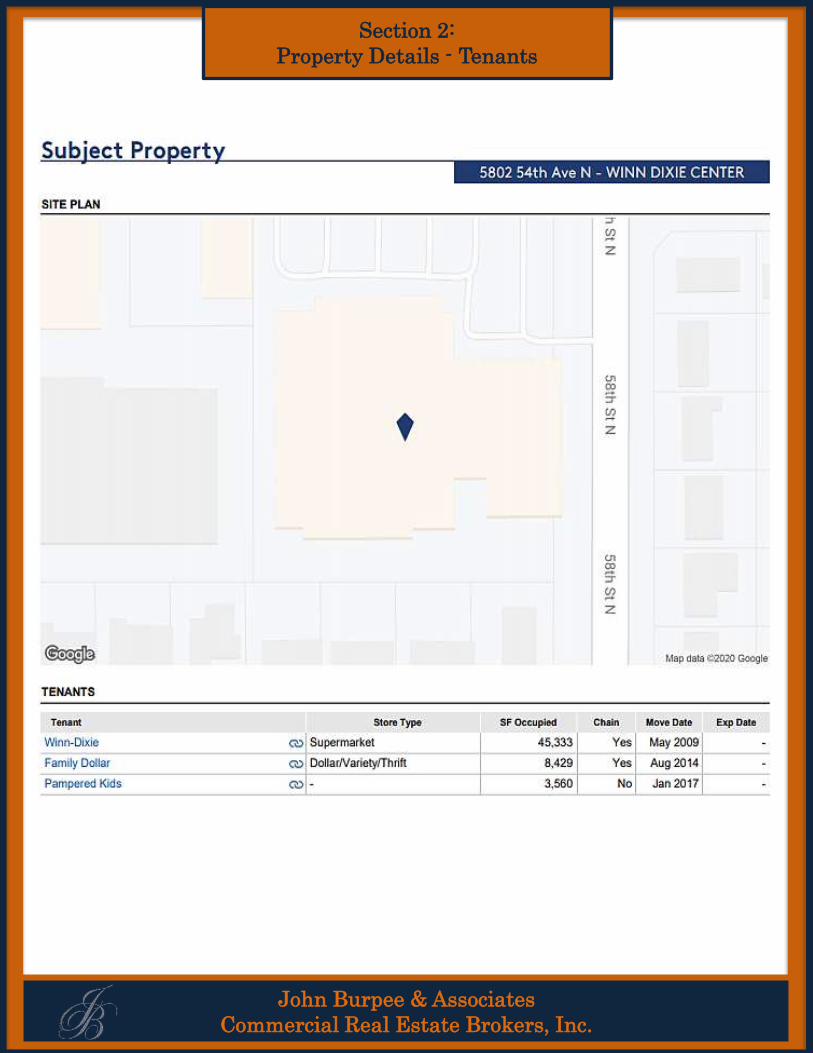

Section 2:

Property Details - Tenants

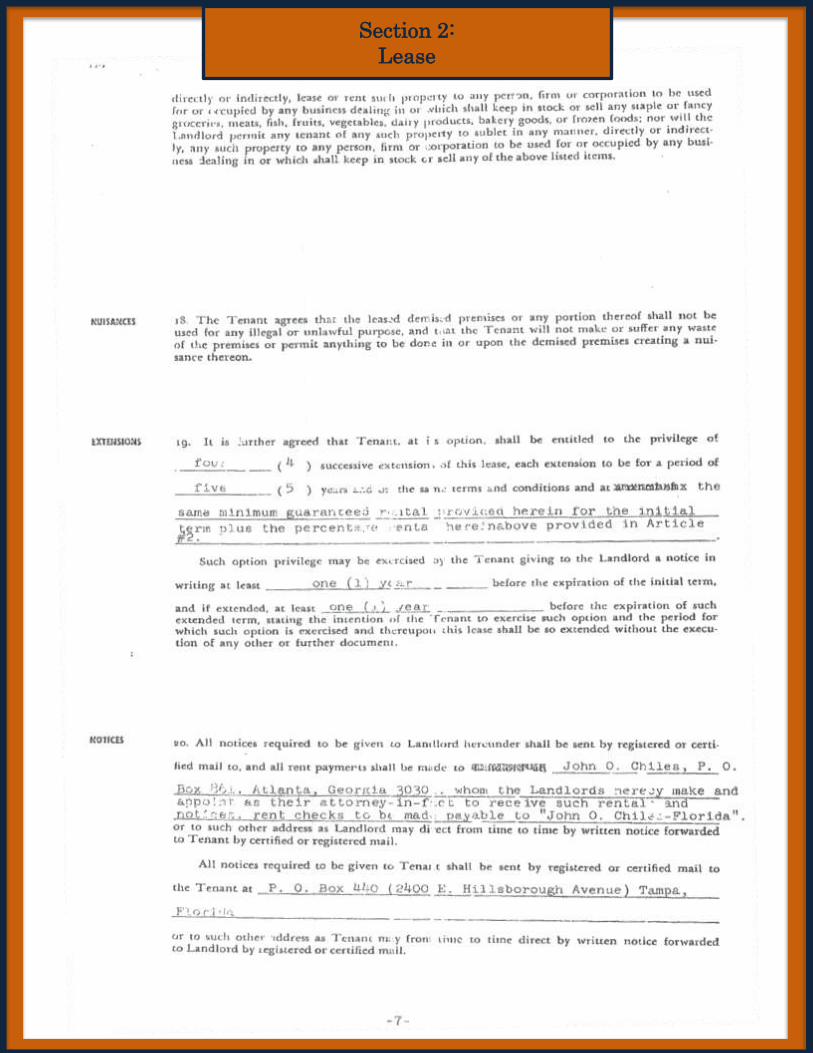

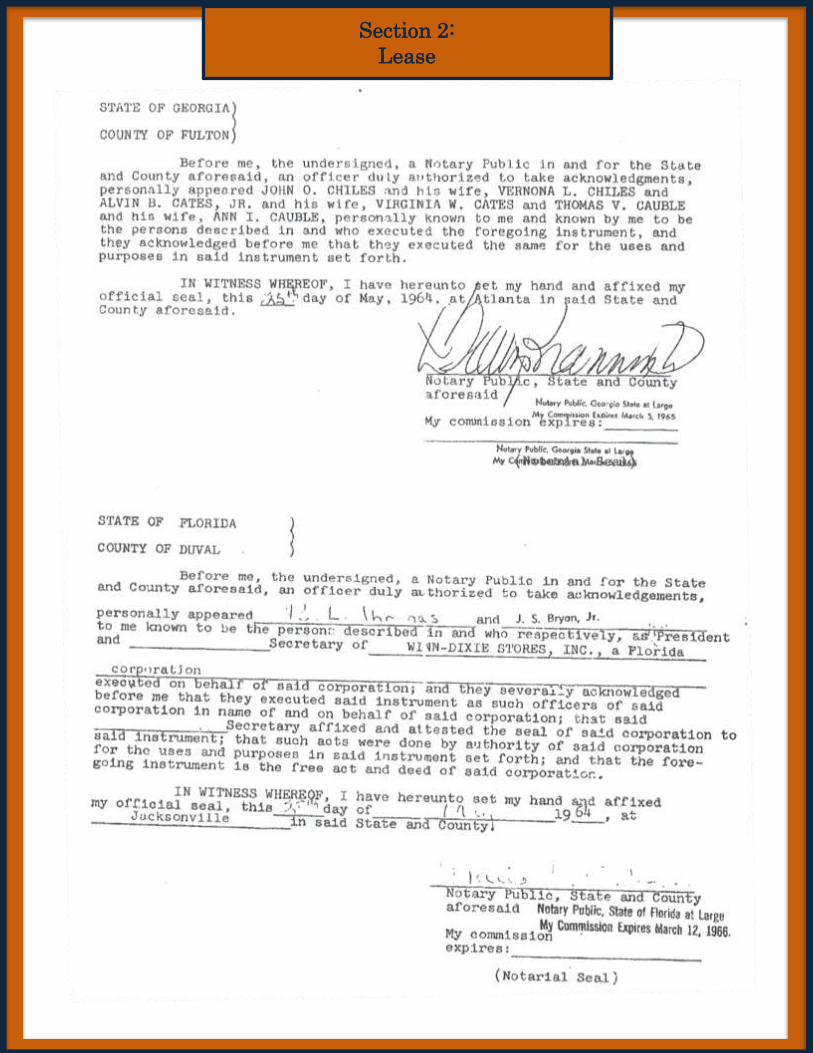

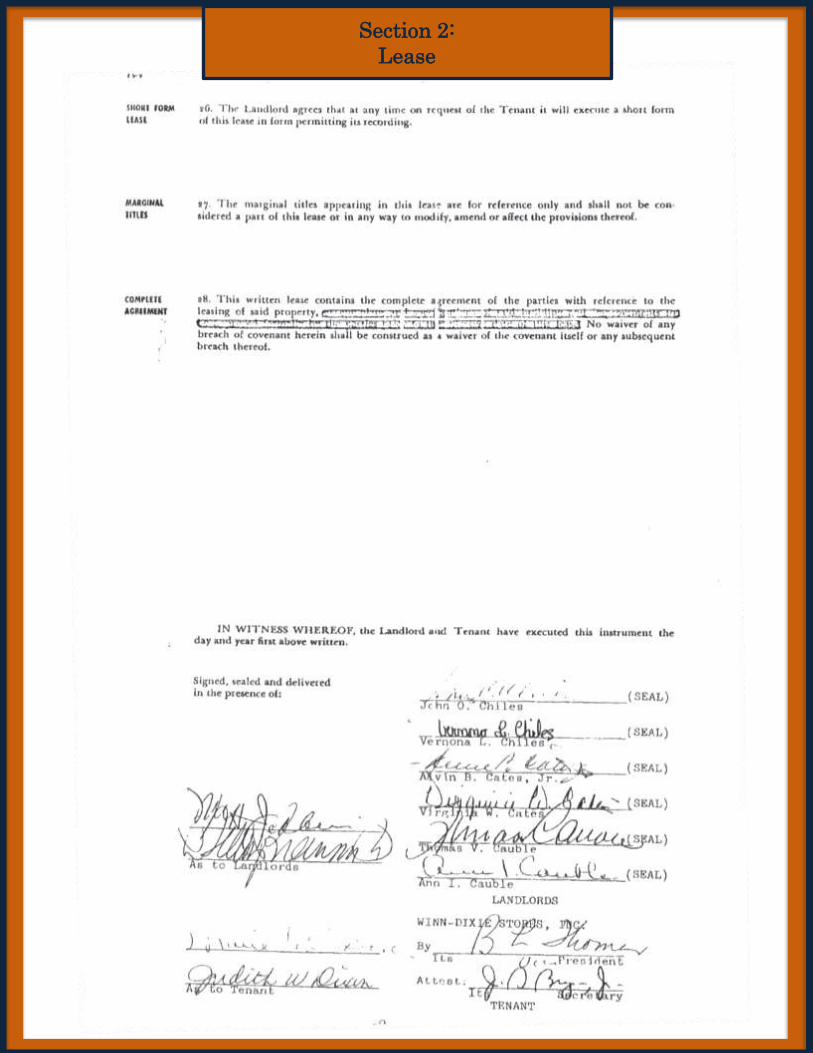

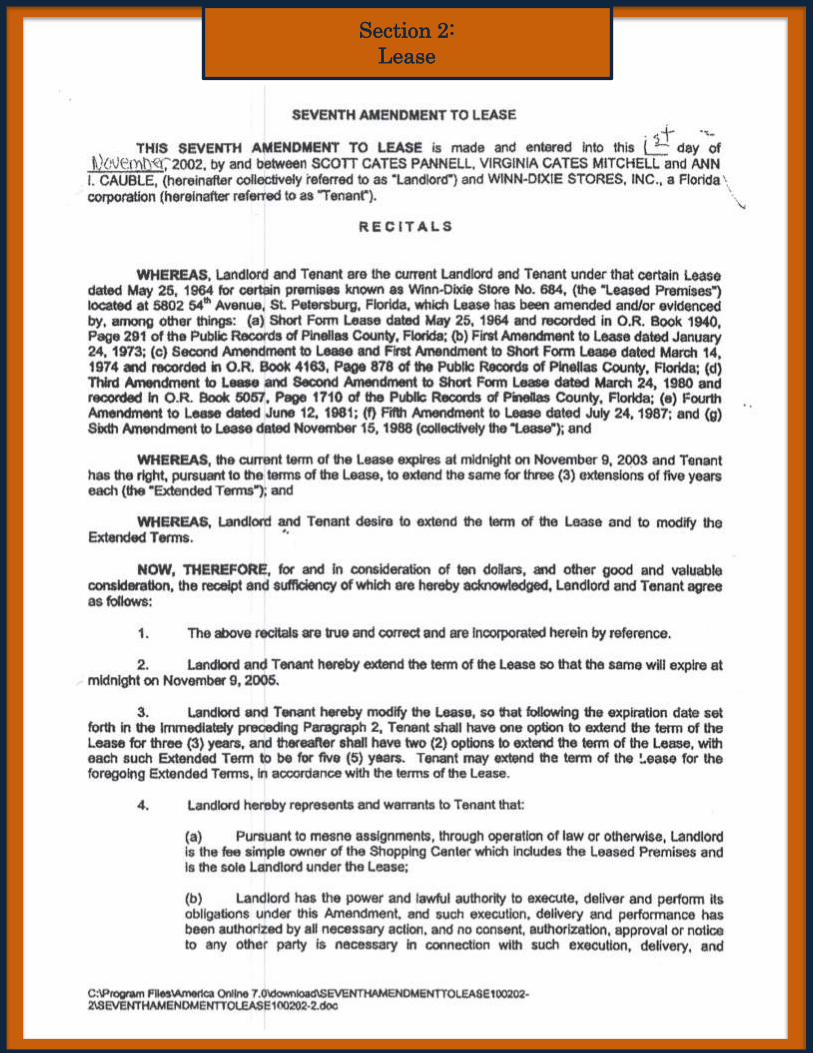

II. PROPERTY DETAILSSection 2:

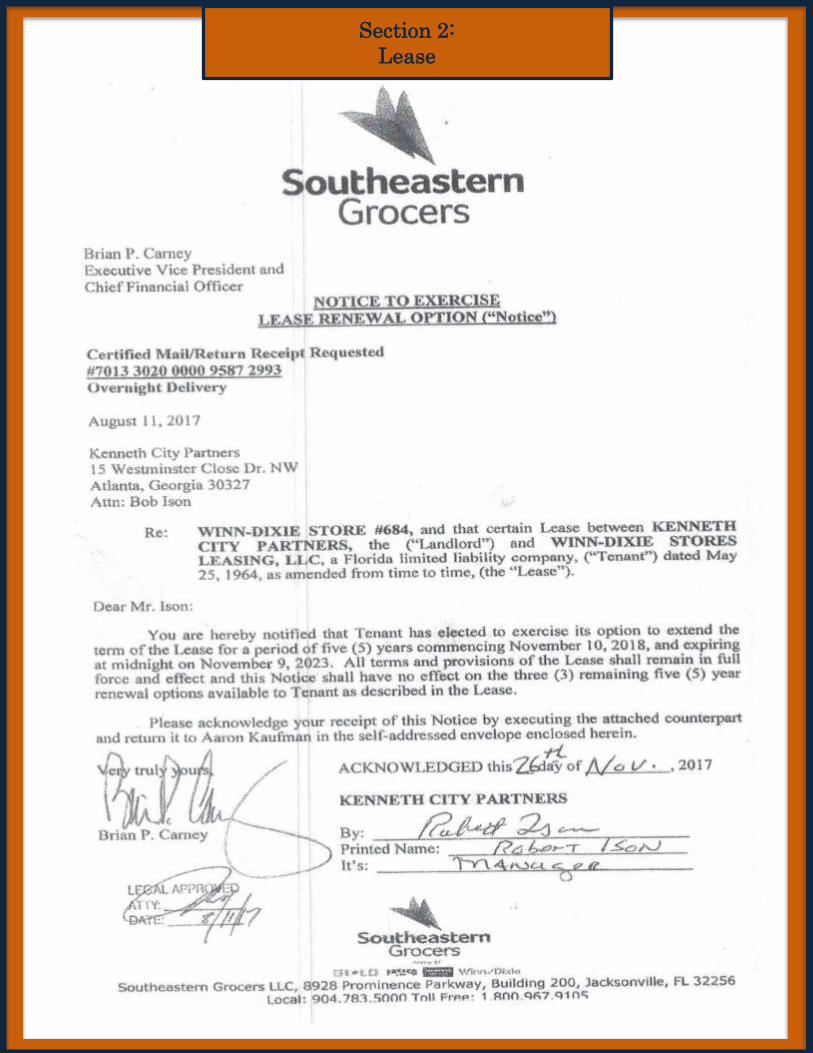

Lease

II. PROPERTY DETAILSSection 2:

Lease

II. PROPERTY DETAILSSection 2:

Lease

II. PROPERTY DETAILSSection 2:

Lease

II. PROPERTY DETAILSSection 2:

Lease

II. PROPERTY DETAILSSection 2:

Lease

II. PROPERTY DETAILSSection 2:

Lease

II. PROPERTY DETAILSSection 2:

Lease

II. PROPERTY DETAILSSection 2:

Lease

II. PROPERTY DETAILSSection 2:

Lease

II. PROPERTY DETAILSSection 2:

Lease

II. PROPERTY DETAILSSection 2:

Lease

II. PROPERTY DETAILSSection 2:

Lease

II. PROPERTY DETAILSSection 2:

Lease

II. PROPERTY DETAILSSection 2:

Lease

II. PROPERTY DETAILSSection 2:

Lease

II. PROPERTY DETAILSSection 2:

Lease

II. PROPERTY DETAILSSection 2:

Lease

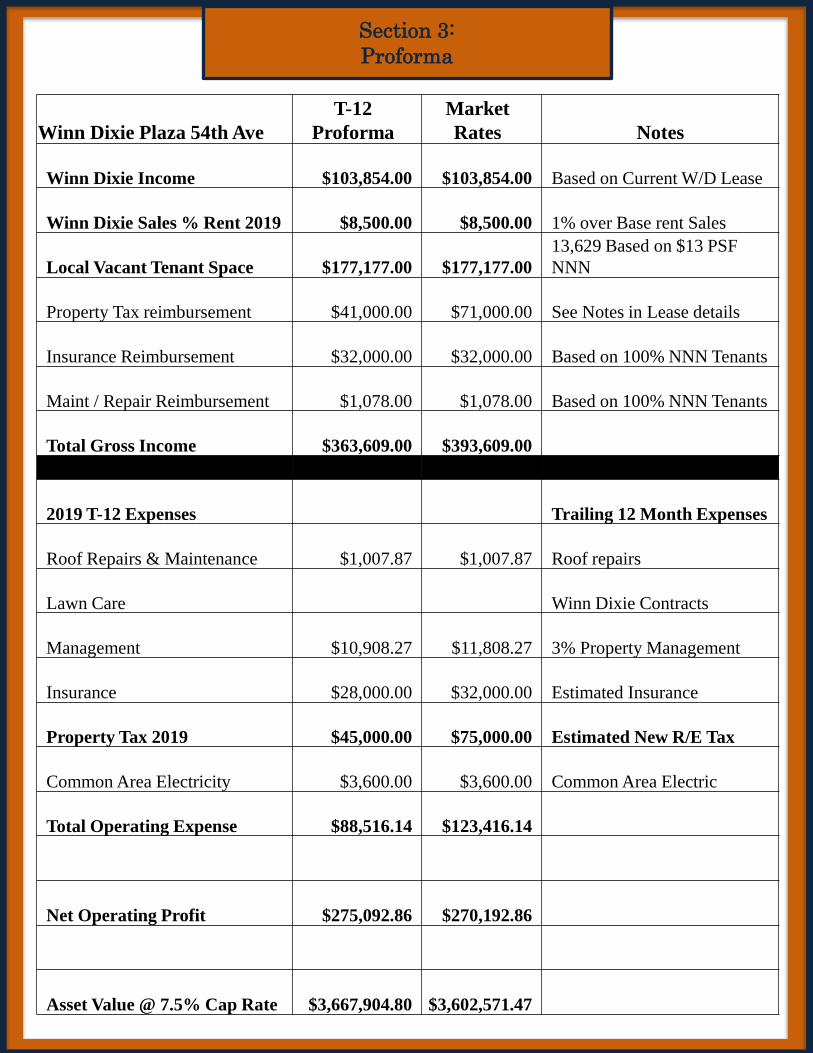

II. PROPERTY DETAILSSection 3:

Proforma

Winn Dixie Plaza 54th Ave

T-12

Proforma

Market

Rates Notes

Winn Dixie Income $103,854.00 $103,854.00 Based on Current W/D Lease

Winn Dixie Sales % Rent 2019 $8,500.00 $8,500.00 1% over Base rent Sales

Local Vacant Tenant Space $177,177.00 $177,177.00

13,629 Based on $13 PSF

NNN

Property Tax reimbursement $41,000.00 $71,000.00 See Notes in Lease details

Insurance Reimbursement $32,000.00 $32,000.00 Based on 100% NNN Tenants

Maint / Repair Reimbursement $1,078.00 $1,078.00 Based on 100% NNN Tenants

Total Gross Income $363,609.00 $393,609.00

2019 T-12 Expenses Trailing 12 Month Expenses

Roof Repairs & Maintenance $1,007.87 $1,007.87 Roof repairs

Lawn Care Winn Dixie Contracts

Management $10,908.27 $11,808.27 3% Property Management

Insurance $28,000.00 $32,000.00 Estimated Insurance

Property Tax 2019 $45,000.00 $75,000.00 Estimated New R/E Tax

Common Area Electricity $3,600.00 $3,600.00 Common Area Electric

Total Operating Expense $88,516.14 $123,416.14

Net Operating Profit $275,092.86 $270,192.86

Asset Value @ 7.5% Cap Rate $3,667,904.80 $3,602,571.47

John Burpee & Associates

Commercial Real Estate Brokers, Inc.

Section 4:

Location Overview

John Burpee & Associates

Commercial Real Estate Brokers, Inc.

Section 4:

Location Overview

John Burpee & Associates

Commercial Real Estate Brokers, Inc.

Section 5:

Property Photos

John Burpee & Associates

Commercial Real Estate Brokers, Inc.

Section 6:

Sales Comps

John Burpee & Associates

Commercial Real Estate Brokers, Inc.

Section 6:

Sales Comps – Sales Volume

John Burpee & Associates

Commercial Real Estate Brokers, Inc.

Section 6:

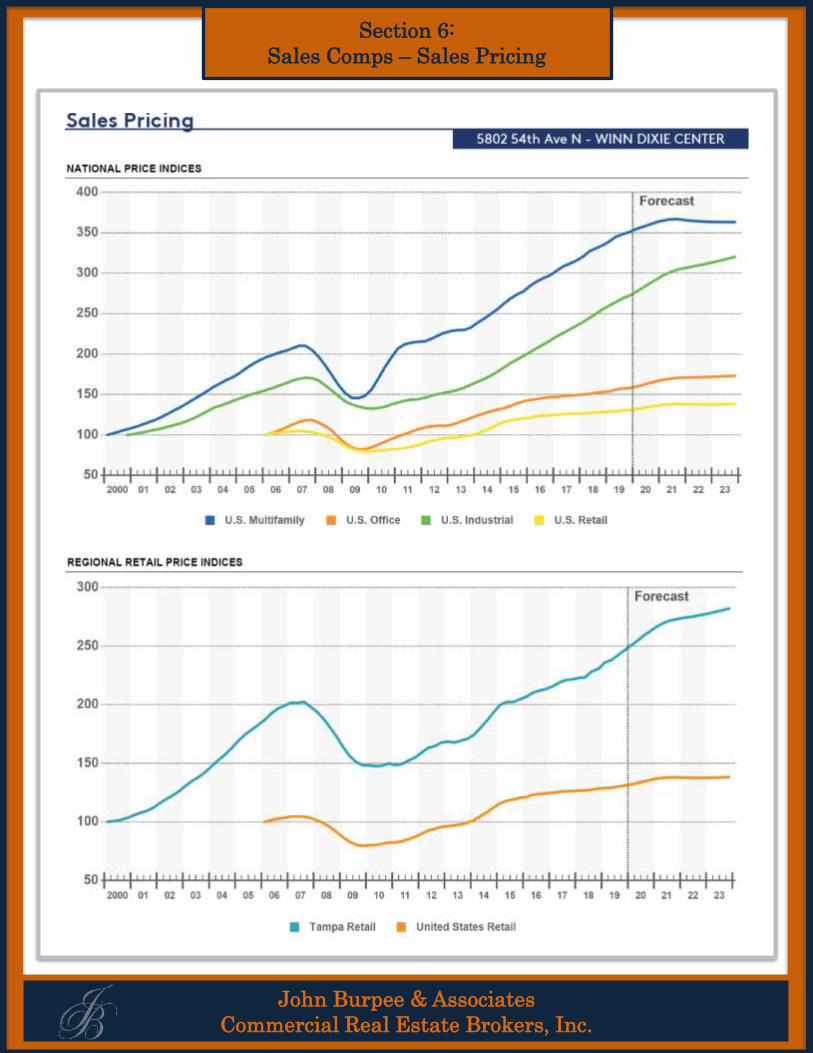

Sales Comps – Sales Pricing

II. PROPERTY DETAILSSection 6:

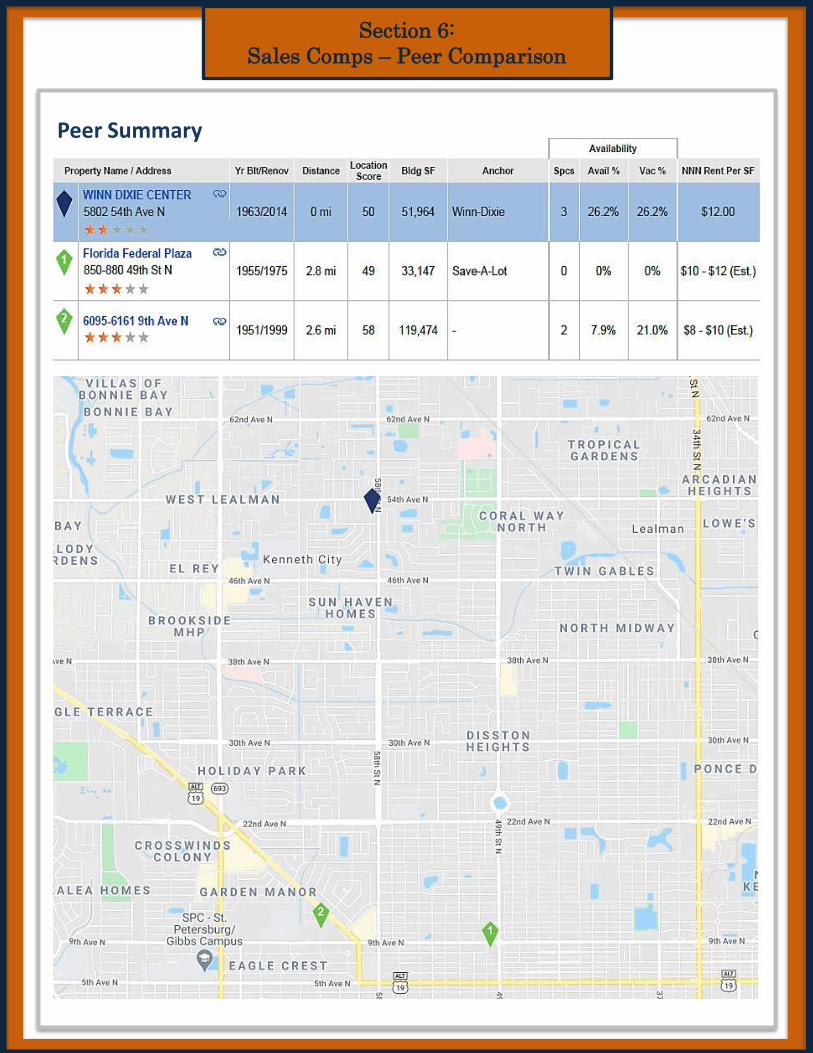

Sales Comps – Peer Comparison

Peer Summary

II. PROPERTY DETAILSSection 6:

Sales Comps – Peer Comparison

II. PROPERTY DETAILS

Fueled by robust population growth, elevated job growth, and record-setting tourism, Tampa's retail demand

over the past five years has been consistently strong. The market reached an all-time low vacancy rate in 2019,

though Tampa has effectively stayed in equilibrium for the past three years. Given the expectation for Tampa to

maintain job and population growth rates well above the national average and a muted pipeline, the market

appears unlikely to experience severe negative absorption shocks over the near term.

Mirroring national trends, Tampa has seen an increase in recent retail store closures. While this has impacted

available inventory levels, particularly in big-box retail sites, Tampa has managed to backfill these vacancies

more quickly than much of the nation. Spaces are often only on the market for a few months, such as when RH

Outlet took down the former Babies R Us space in the Drew 19 Shopping Center in Clearwater.

The metro has also benefited from a large influx of grocers expanding their Tampa presence over recent years,

including new entries like Sprouts and EarthFare. Adaptive-reuse strategies have experienced increasing

success with other sectors, such as converting to help satiate the region's robust medical office demand.

Retail in Tampa draws heavily from the vibrant tourism industry, with both Hillsborough and Pinellas among

only nine counties in Florida to achieve "high-impact" tourism status. The record-setting visitor counts

continue to drive retail spending, particularly in the core CBD areas and along the metro's famous beaches.

Strategic Property Partners recently began the initial phase of its $3 billion Water Street Tampa development.

The project is expected to add approximately 1 million SF of retail space by 2027 and drive personal

consumption and retail demand. The primary retail component is a redeveloped area along the waterway

known as Sparkman Wharf. The concept plans to avoid national chains, as evident from allowing Hooter's to

vacate their location after 15 years. Instead, the focus will be on local chefs and dining experiences to promote

a walkable environment.

Section 7:

Vacancy Rates

II. PROPERTY DETAILSSection 7:

Vacancy Rates Overview

Tampa is one of the strongest retail rent growth markets in the nation and has remained so for roughly the past

six years. Annual gains have shown few signs of slowing, with the market establishing a record growth rate in

2019. Though there has been some relative cooling since then, the current growth rate is still over three times

the national average and well above the long-term trend.

Despite a relative uptick in recent deliveries and current construction, the metro has seen little impact on rent

growth. The moderate supply and expected continued strong demand levels should insulate rent growth from

significant downward pressure. Furthermore, retail starts slowed in 2019, though the proposed pipeline remains

active.

Rent growth throughout the entire metro is elevated, with even the outlying submarkets such as Pasco County,

Southeast Hillsborough County, and Hernando County seeing growth well above their historical averages.

Even the lowest retail rent growth submarket is also drastically outperforming the national average. Westshore,

home to some of Tampa's premier shopping districts, maintains the highest asking rents in the metro. The other

top rent growth submarkets include perennial performers such as Downtown Tampa and Downtown

St. Petersburg.

John Burpee & Associates

Commercial Real Estate Brokers, Inc.

Section 6:

Demographics

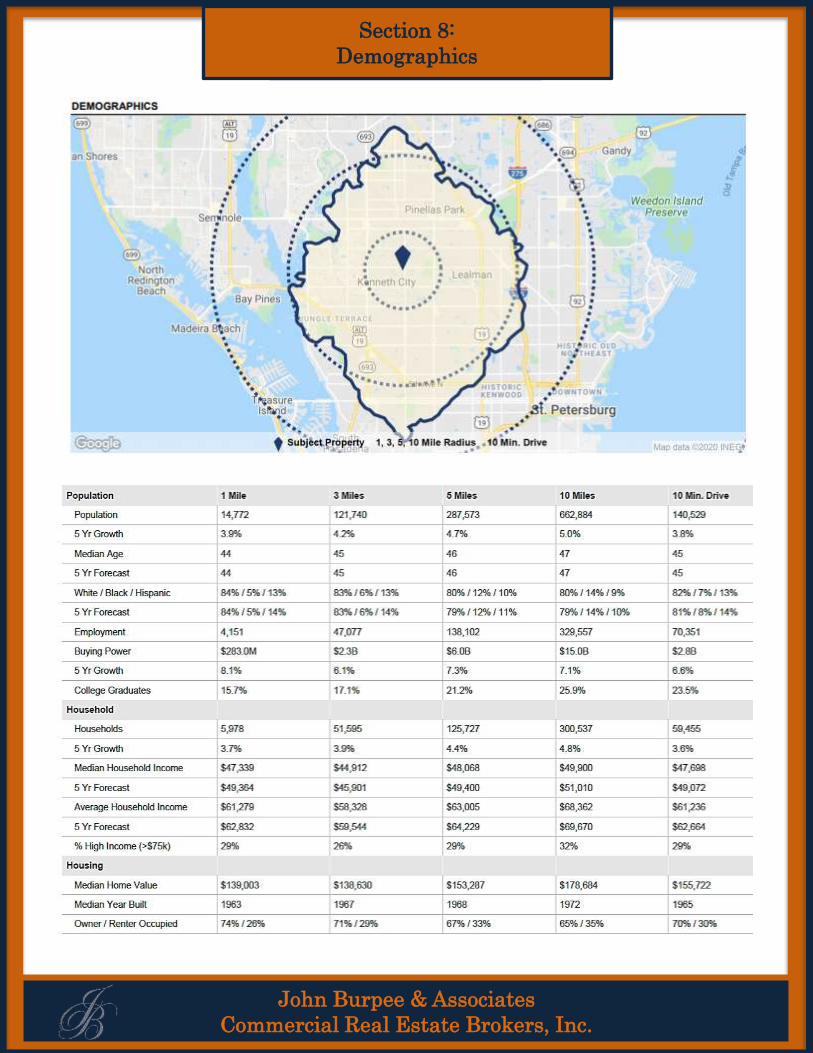

Section 8:

Demographics

II. PROPERTY DETAILS

John Burpee & Associates

Commercial Real Estate Brokers, Inc.

Section 8:

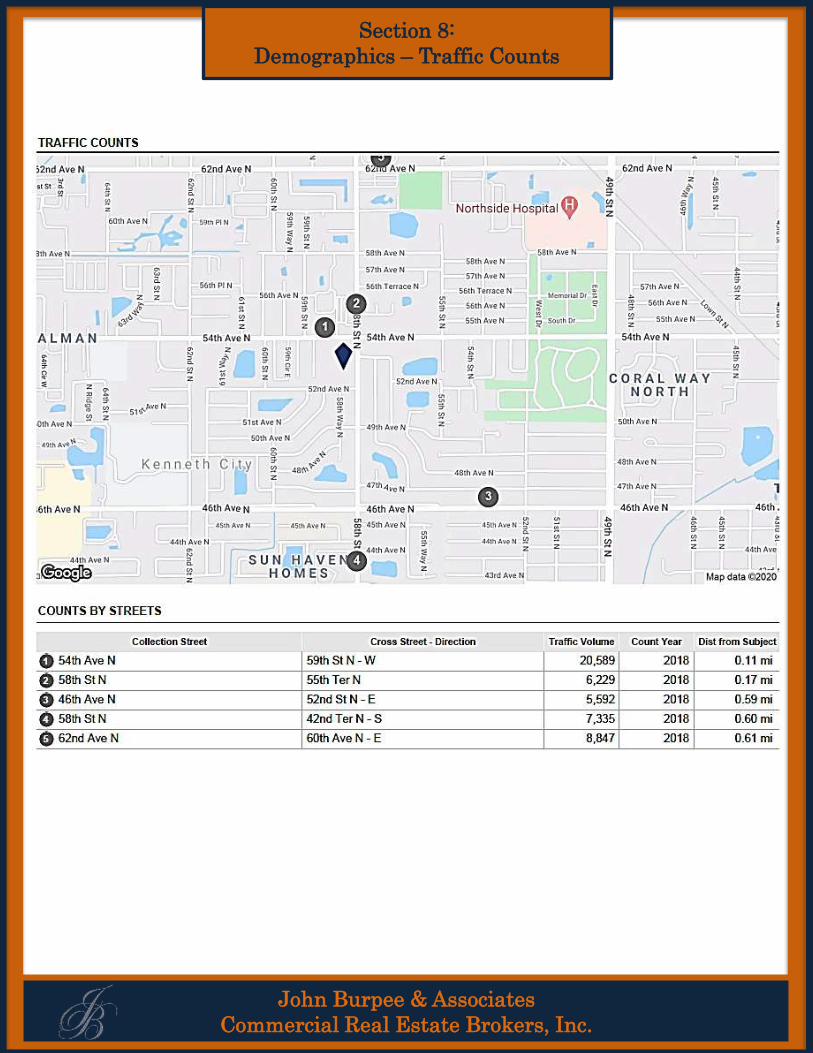

Demographics – Traffic Counts

II. PROPERTY DETAILSSection 8:

Demographics – Growth Trends

II. PROPERTY DETAILS

Tampa's retail market is flourishing, thanks to elevated personal consumption from the metro's robust

population and wage growth, as well as significant lift provided by vibrant tourism. After outperforming the

nation for the past five years with both tighter vacancies and stronger rent growth, the market continues to see

both metrics improve. In 2019, both the average vacancy rate and annual rent growth established record levels.

While Tampa’s retail trade employment has been one of the highest growth sectors over the past two years,

with over 5% job growth, retail trade has slowed substantially and even shed over 1,000 jobs over the past

twelve months. This may be having a lagged impact on net absorption which has started to gradually taper off,

though this could as easily be a function of a market at full occupancy with vacancies sitting near record lows.

Retail starts have slowed since the start of 2019, with only a little over 600,000 SF underway in 2020, the

lowest amount in seven years. This has also pushed Tampa's retail pipeline below the pace of the nation as

measured by percent of existing inventory. The Channel District of the Downtown Tampa Submarket is a

particular hotbed of activity, with multiple apartment complexes recently delivered and underway, spurring

retail demand such as the submarket's first Publix location, organic grocer GreenWise, and a CVS lease

signing.

Redevelopment plays of big-box vacancies have also taken center stage in 2020. The former Sears location at

University Mall is being demolished for future development and the vacant Sears at Citrus Park recently sold

with the new Miami owner planning significant renovations.

One key component of Water Street Tampa is the ongoing transitioning of Channelside Bay Plaza into the new

concept Sparkman Wharf. The redeveloped plaza, along the fringes of Downtown Tampa, caters to a

destination retail environment through features such as a biergarten and a dining garden by Tampa-based chefs

in repurposed shipping containers.

Investment activity has remained elevated and relatively consistent for the past seven years, though sales

volume slightly slowed in 2019 from the prior year's cyclic-high. However, cap rates have continued to gently

compress, and pricing is at an all-time high.

Section 8

Demographics – Market Summary

II. PROPERTY DETAILS

Tampa’s strong economic expansion continues to roll in 2020, once again among the nation’s leaders for job and

population growth rates. The sustained, long-term job growth has tightened Tampa’s labor market to one of the best in

the U.S., which has ultimately driven up wages and incomes across the metro. Over the past two years, Tampa has

posted some of the higher income growth in the country, increasing the market’s buying power and personal

consumption, which has provided ample fuel for both strong retail and industrial demand. The market has some

challenges, including a below-average median

income level, a nearly complete reliance this cycle upon in-migration, and some of the nation’s worst infrastructure

and public transit options.

Job growth is the market’s biggest success story and has been for nearly a decade, outperforming the nation for 35

consecutive quarters. During this timeframe, Tampa has averaged a 2.5% annual growth rate, nearly twice the U.S.

average. Job growth has steadily cooled over the past four quarters, as the market is nearing full employment.

Tampa’s unemployment rate has compressed significantly over recent years and is now below the U.S. unemployment

rate, with the spread in 19Q2 growing to over 50 basis points. The slowing pace of jobs added to the market is likely to

continue over the next few quarters, though Tampa is likely to continue seeing annual employment gains greater than

the nation as a whole. The market’s labor force is also growing at roughly half the pace of job growth, which will

continue to apply downward pressure on the unemployment rate.

The Oxford Economics Base Case forecast is calling for job growth to slow considerably in 2020 – 2021. While the

slowdown in U.S. job growth would also heavily weigh upon Tampa’s future employment growth expectations, the

market is expected to hold up relatively well and is likely to continue outperforming the nation.

Over the past year, the best performing job sector has been financial activities, growing at a 4.5% annual clip, roughly

five times the national average. The financial services sector is also historically one of Tampa’s strongest performers,

which spurred the metropolitan area's reputation as a financial hub. Other recent stalwarts include construction (2.9%),

professional and business services (2.7%), leisure and hospitality (2.5%), and manufacturing (2%).

The leisure and hospitality job growth rates also reflect an increasing focus on tourism, especially in Hillsborough

County, which recently joined Pinellas County across the bay as one of only nine high-impact tourism counties in the

state of Florida. While Pinellas County benefits from world-renowned beaches, Hillsborough has relied upon hosting

conferences and major sporting events, including landing the upcoming Wrestlemania 36 and Super Bowl LV.

While the job growth and overall tight labor market have improved Tampa’s median income level to nearly $55,000, it

still trails the U.S. average by over 15%. However, the market has many factors to help offset this large spread,

including no state income taxes and one of the nation’s more affordable housing markets.

Tampa’s relative affordability has been a primary driver of the region’s strong net migration patterns. Since 2013,

roughly 300,000 people moved into the market, tied for the most in-migration in the state of Florida. However, this

strength also belies a potential weakness. Net migration accounted for virtually all of Tampa’s population growth

during this timeframe. The natural population growth has also slowed during this timeframe and over the past two

years has even turned negative.

The market could be overexposed to recessionary influences, as migration, particularly domestic, is often

quick to dry up in adverse economic times.

Infrastructure has long been a sore spot for Tampa. There is virtually no public transit, and only four roadways

connecting Pinellas and Hillsborough counties. Improving public transit is a key focus across the region in 2019, as

reflected by the Tampa City Council approving a $3 billion infrastructure plan.

Section 8:

Demographics – Market Summary