value preparedness discipline - keppel land · value preparedness readiness accountability can...

TRANSCRIPT

Preparedness

Quality

Sustainability

ValueSafety Integrity

ExecutionEnterprise

Collective Strength

Collective Strength

Can DoExecution

Value

Preparedness

ReadinessAccountability

Execution PreparednessCan DoPeople-Centredness

Collective Strength Enterprise

Value Customer Focus Agility Enterprise Safety

Accountability

Innovation

ValueTalent Customer Focus

Preparedness

Execution

Innovation

People-Centredness

Collective Strength Customer Focus Readiness

Can DoCollective Strength

Accountability

AgilityCan Do

Agility Integrity

Readiness

ValueCan DoAccountabilityExecution

Safety

ReadinessTalent

Talent

Collective Strength

Collective Strength

Do

Can Do

Talent CollectiveStrength

Enterprise Talent Innovation Readiness

Can Do

Enterprise

Innovation

Innovation

Innovation

Discipline

Focus

AccountabilityValue

Preparedness

People-Centredness Enterprise

AgilityValue Talent Integrity

Can

Enterprise

AgilityCollective

Strength

Talent

ExecutionReadiness

People-Centredness

People-Centredness Talent ValueAccountabilityReadiness Talent Preparedness

Innovation

Safety

Customer FocusReadinessAgilityValueEnterpriseExecution

Enterprise Value Can Do

Report to Shareholders 2015

Harnessing Strengths

Harnessing Strengths

Report to Shareholders 2015

Keppel Land Lim

ited

Keppel Land Limited(Incorporated in the Republic of Singapore)230 Victoria Street #15-05 Bugis Junction TowersSingapore 188024

Tel: (65) 6338 8111Fax: (65) 6337 7168www.keppelland.com

Co Reg No: 189000001G

FSCinsert by printer

Harnessing Strengths

Overview01 Key Figures for 201502 Group Financial Highlights03 Corporate Profile04 Chairman’s Statement10 Interview with the CEO15 Board of Directors20 Senior Management22 Key Personnel26 Awards and Accolades 28 Corporate Milestones29 Corporate Governance35 Risk Management38 Harnessing Strengths40 Special Feature

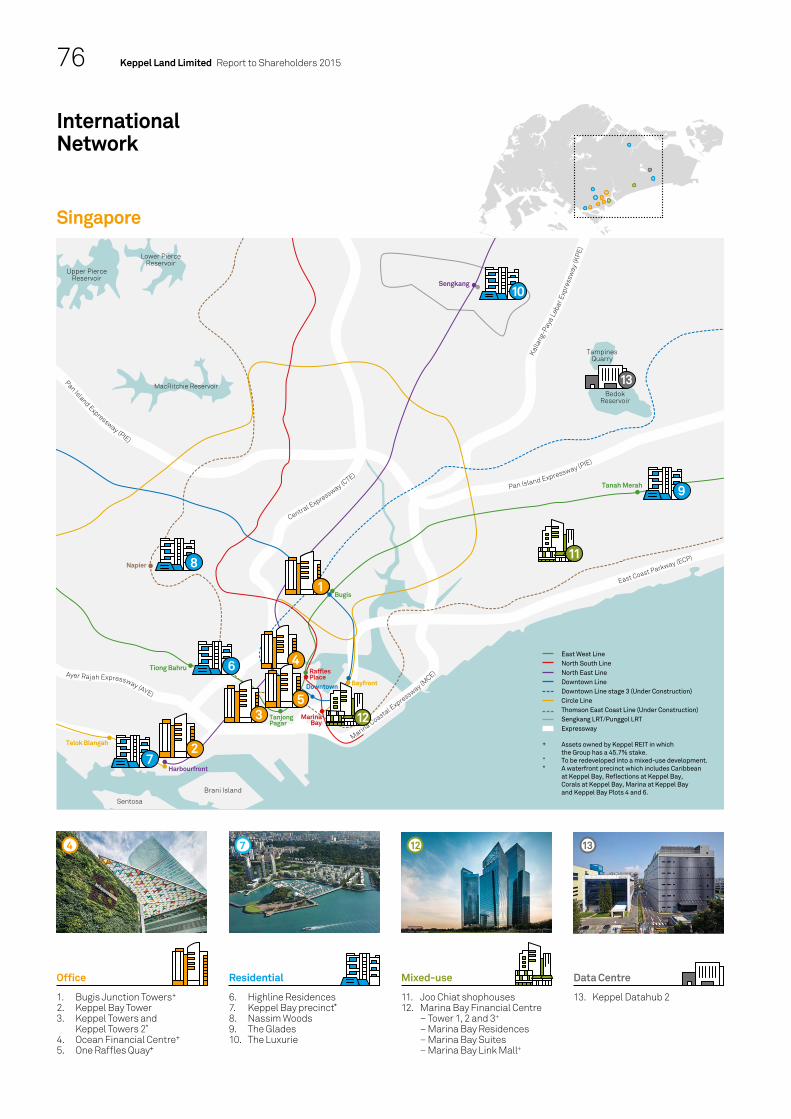

Operations and Market Review 42 Overview44 Singapore48 Property Fund Management52 Retail Management54 Hospitality Management56 China64 Vietnam68 Indonesia70 The Philippines, Myanmar71 United States, United Kingdom72 India, Sri Lanka73 Malaysia, Thailand74 International Network77 Property Portfolio

VisionA leading real estate company, shaping the best for future generations.

MissionGuided by our operating principles and core values, we will create value for all stakeholders through innovative real estate solutions.

Operating Principles1 Best value propositions

to customers.2 Tapping and developing

best talents from our global workforce.

3 Cultivating a spirit of innovation and enterprise.

4 Executing our projects well.5 Being financially disciplined to

earn best risk-adjusted returns.6 Clarity of focus and operating

within our core competence.7 Being prepared for the future.

The Keppel Group harnesses and synergises the distinctive strengths of its multi businesses to capture opportunities arising from the global demand for energy, sustainable urbanisation and connectivity. Our strong culture and enduring values drive our people to strive for execution excellence and operational efficiency. With financial discipline and sharp focus on optimising returns, we will seize opportunities as well as innovate solutions and services to build a long-term and competitive position and capture sustainable returns for our stakeholders.

Revenue

$1.6bRevenue rose by 6.8% year-on-year to $1.6 billion.

Total Assets

$14.9bTotal assets grew from $14.6 billion to $14.9 billion year-on-year.

Volunteerism

5,095hrsA total of 5,095 volunteer hours were clocked by staff for corporate social responsibility activities in Singapore and overseas.

Return on Equity

18.9%Return on equity is one of the highest amongst Asia’s leading property developers at 18.9% per annum over 10 years, from 2006 to 2015.

New Commercial Space Under Development

630,000smNew commercial properties under development overseas.

Safety Training

34,00034,000 workers trained to-date at Keppel Land’s Safety Awareness Centres in Vietnam and Malaysia.

Key Figures for 2015

Overview / Operations and Market Review

Key Figures for 2015

01

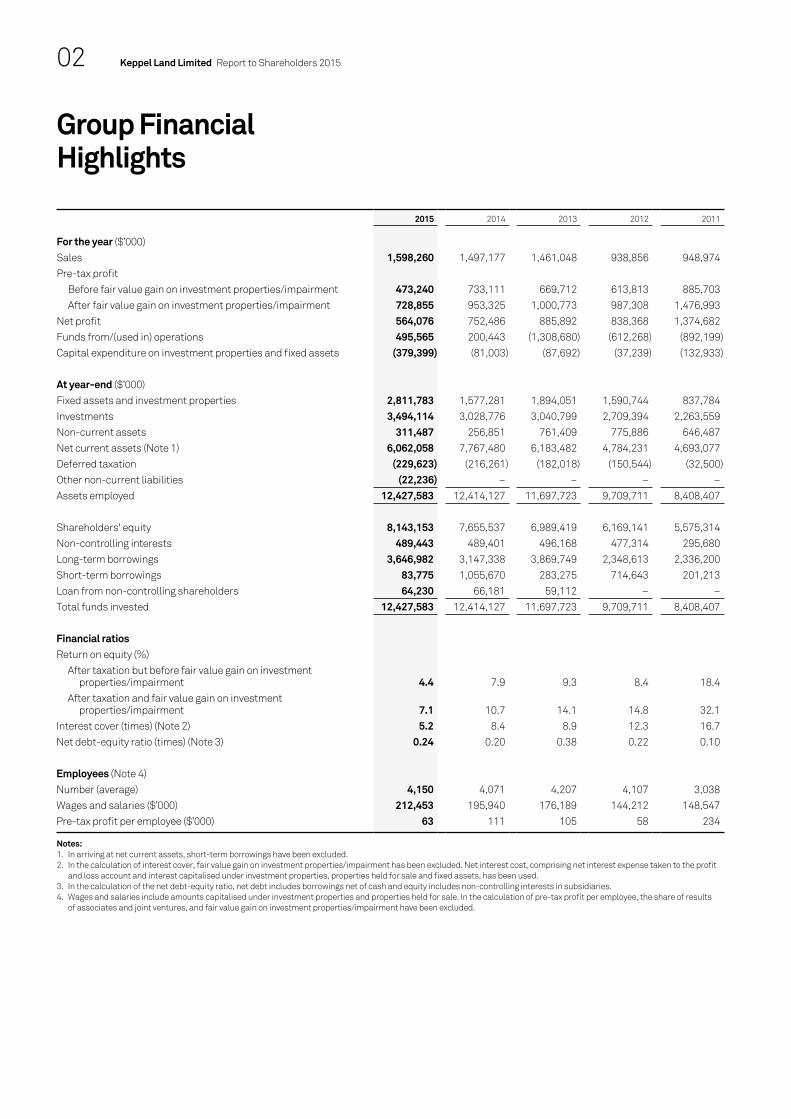

2015 2014 2013 2012 2011

For the year ($’000)Sales 1,598,260 1,497,177 1,461,048 938,856 948,974 Pre-tax profit

Before fair value gain on investment properties/impairment 473,240 733,111 669,712 613,813 885,703 After fair value gain on investment properties/impairment 728,855 953,325 1,000,773 987,308 1,476,993

Net profit 564,076 752,486 885,892 838,368 1,374,682 Funds from/(used in) operations 495,565 200,443 (1,308,680) (612,268) (892,199)Capital expenditure on investment properties and fixed assets (379,399) (81,003) (87,692) (37,239) (132,933)

At year-end ($’000)Fixed assets and investment properties 2,811,783 1,577,281 1,894,051 1,590,744 837,784 Investments 3,494,114 3,028,776 3,040,799 2,709,394 2,263,559 Non-current assets 311,487 256,851 761,409 775,886 646,487 Net current assets (Note 1) 6,062,058 7,767,480 6,183,482 4,784,231 4,693,077 Deferred taxation (229,623) (216,261) (182,018) (150,544) (32,500)Other non-current liabilities (22,236) – – – –Assets employed 12,427,583 12,414,127 11,697,723 9,709,711 8,408,407

Shareholders' equity 8,143,153 7,655,537 6,989,419 6,169,141 5,575,314 Non-controlling interests 489,443 489,401 496,168 477,314 295,680 Long-term borrowings 3,646,982 3,147,338 3,869,749 2,348,613 2,336,200 Short-term borrowings 83,775 1,055,670 283,275 714,643 201,213 Loan from non-controlling shareholders 64,230 66,181 59,112 – –Total funds invested 12,427,583 12,414,127 11,697,723 9,709,711 8,408,407

Financial ratiosReturn on equity (%)

After taxation but before fair value gain on investment properties/impairment 4.4 7.9 9.3 8.4 18.4

After taxation and fair value gain on investment properties/impairment 7.1 10.7 14.1 14.8 32.1

Interest cover (times) (Note 2) 5.2 8.4 8.9 12.3 16.7 Net debt-equity ratio (times) (Note 3) 0.24 0.20 0.38 0.22 0.10

Employees (Note 4)Number (average) 4,150 4,071 4,207 4,107 3,038 Wages and salaries ($’000) 212,453 195,940 176,189 144,212 148,547 Pre-tax profit per employee ($’000) 63 111 105 58 234

Notes:1. In arriving at net current assets, short-term borrowings have been excluded.2. In the calculation of interest cover, fair value gain on investment properties/impairment has been excluded. Net interest cost, comprising net interest expense taken to the profit

and loss account and interest capitalised under investment properties, properties held for sale and fixed assets, has been used. 3. In the calculation of the net debt-equity ratio, net debt includes borrowings net of cash and equity includes non-controlling interests in subsidiaries.4. Wages and salaries include amounts capitalised under investment properties and properties held for sale. In the calculation of pre-tax profit per employee, the share of results

of associates and joint ventures, and fair value gain on investment properties/impairment have been excluded.

Keppel Land Limited Report to Shareholders 2015

Group Financial Highlights

02

as Marina Bay Financial Centre and Ocean Financial Centre.

The Company is committed to grow its commercial portfolio in key Asian cities. Its portfolio includes Seasons City in the Sino-Singapore Tianjin Eco-City, Life Hub @ Jinqiao, Park Avenue Central in Shanghai, China, Saigon Centre in Ho Chi Minh City, Vietnam, as well as International Financial Centre Jakarta in Indonesia. The Company plans to expand the SM-KL Project in the Philippines and develop Junction City Tower in Yangon, Myanmar.

Beyond Asia, Keppel Land has acquired an office building in London, the United Kingdom. To strengthen the Company’s retail capabilities, Keppel Land has acquired a 75% stake in retail management company Array Real Estate, which has been renamed Keppel Land Retail Management.

Keppel Land is Asia’s premier home developer with world-class

01

Keppel Land is the property arm of the Keppel Group, one of Singapore’s largest multinational groups with key businesses in offshore and marine, property, infrastructure and investments.

One of Asia’s premier property companies, Keppel Land is recognised for its sterling portfolio of award-winning residential developments and investment-grade commercial properties as well as high standards of corporate governance and transparency. Keppel Land was privatised and delisted from the Singapore Stock Exchange with effect from 16 July 2015. A selective capital reduction exercise to cancel all outstanding shares held by minority shareholders of Keppel Land was approved at an extraordinary general meeting on 13 April 2016 and the court on 5 May 2016.

The Company is geographically diversified in Asia, with Singapore and China as its core markets as well as Vietnam and Indonesia as its growth markets. Keppel Land focuses on a two-pronged strategy of property development for sale and property fund management. The Company’s total assets amounted to about $14.9 billion as at 31 December 2015.

Keppel Land was ranked fourth in the prestigious Corporate Knights’ Global 100 Most Sustainable Corporations in the World 2015, placing it first in Asia and among real estate companies worldwide. Keppel Land was a component of the Dow Jones Sustainability World and Asia Pacific Indices, as well as the Morgan Stanley International Global Sustainability and Socially Responsible Indices prior to its delisting.

As a leading prime office developer in Singapore, Keppel Land contributes to enhancing the city’s skyline with landmark developments such

01 Through its unwavering focus on sustaining growth in its businesses, empowering lives of its people, and nurturing communities wherever it operates, Keppel Land continues to shape the future for the benefit of tomorrow’s generation.

iconic waterfront residences at Keppel Bay and Marina Bay in Singapore. The Company has also ventured into the United States with a residential development in Manhattan, New York.

With a pipeline of about 70,000 homes in Singapore and overseas as well as an increasing commercial presence in the region, Keppel Land is well-positioned to meet the growing demands for quality residential, office and mixed-use developments.

An established property fund manager, Keppel Land has two property fund management vehicles, Keppel REIT Management Limited, the manager of Keppel REIT, a pan-Asian commercial real estate investment trust, and Alpha Investment Partners (Alpha). As at 31 December 2015, Keppel REIT and Alpha’s total assets under management have grown to $20.5 billion when fully leveraged and invested.

Overview / Operations and Market Review

CorporateProfile

Corporate Profile03

Dear Shareholders,

On behalf of the Board of Directors, I am pleased to present Keppel Land’s annual report for the year ended 31 December 2015.

Steady Financial Performance 2015 was a challenging year with the global economic environment affected by depressed oil prices, slowdown in China’s growth, as well as volatility in the international financial markets. Despite these headwinds, the Group performed creditably.

For the year ended 31 December 2015, Keppel Land achieved a revenue of $1.6 billion, up 6.8% from the previous year. However, net profit fell to $564.1 million, compared with $752.5 million a year ago, mainly due to fewer asset divestments. In 2014, we divested stakes in Marina Bay Financial Centre Phase 2 and Equity Plaza, as well as data centres to Keppel DC REIT. With a relatively low net debt to equity ratio of 0.24 and a strong cash position of $1.7 billion, we have the ability to pursue acquisitions and new investments. We will continue to focus on asset turnover and capital recycling to improve returns, while continuing to exercise prudent financial management.

In 2015, Keppel Corporation, which then held 54.5% of Keppel Land shares, took Keppel Land private through a voluntary unconditional cash offer. Keppel Land was delisted from the Singapore Stock Exchange on 16 July 2015, and became 99.3% owned by Keppel Corporation, with the remaining 0.7% held by various shareholders.

Since the delisting of Keppel Land, the Company had received many queries from shareholders on how they could trade their shares. As there is no public market for the shares of Keppel Land, on 14 March 2016, the Company proposed to undertake a selective capital reduction exercise to cancel all the shares held by the shareholders of Keppel Land (participating shareholders), apart from those held by Keppel Corporation.

At an extraordinary general meeting held on 13 April 2016, participating shareholders approved a special resolution for the selective capital reduction, following which court approval of the selective capital reduction was also obtained.

The selective capital reduction has allowed participating shareholders to realise the value of their investment in Keppel Land, with

participating shareholders receiving $4.24 for each share cancelled.

The privatisation of Keppel Land fully aligned the interests of the Company with the Keppel Group, providing a strong pillar for earnings and long-term value creation. Leveraging the Keppel Group’s financial and organisational strengths, Keppel Land will continue to scale up in the property arena as well as build on and create platforms for collaboration through realising synergies within the Group.

Focus on ReturnsWith a legacy of over a hundred years, Keppel Land has grown steadily to become a premier developer in Asia, with a strong track record and brand name. To be a leader in the property industry does not mean that we must aspire to be the biggest player. Instead, we want to be the developer with the highest return in Asia. Amongst Asia’s leading property developers, Keppel Land’s return on equity is one of the highest at 18.9% per annum over 10 years, from 2006 to 2015.

We continually review our investment portfolios. In line with the Keppel Group’s focus on higher returns, over the past two years, we seized opportunities to recycle capital, strategically monetising almost $2.4 billion worth of assets and re-investing the capital in new acquisitions.

Expanding Presence in Key MarketsOur aim is to develop Keppel Land into a multi-faceted property player, riding on urbanisation trends in Asia.

The Group is focused on its core markets of Singapore and China, as well as its growth markets of Vietnam and Indonesia. Being geographically diversified has served the Company well in 2015 as it helped offset the subdued sales in Singapore, and allowed us to commit our resources to scale up and strengthen our presence in our focus markets while seizing opportunities in other emerging markets and global gateway cities.

Keppel Land sold a total of 4,570 homes in 2015, almost double the 2,450 homes sold last year. China and Vietnam accounted for 72% and 20% of the total home sales respectively.

The property cooling measures implemented since 2013, coupled with rising interest rates, continued to weigh on the Singapore residential market. The Group sold about 190 homes in Singapore, mainly at The Glades at Tanah Merah

To be a leader in the property industry does not mean that we must aspire to be the biggest player. Instead, we want to be the developer with the highest return in Asia. Amongst Asia’s leading property developers, Keppel Land’s return on equity is one of the highest at 18.9% per annum over 10 years, from 2006 to 2015.

Loh Chin HuaChairman

Key Developments in 2015

Sold about 4,570 homes in Asia, mostly in China and Vietnam, almost double the units sold in 2014.

Keppel REIT and Alpha Investment Partners’ assets under management grew by 9.6% to $20.5 billion when fully leveraged and invested as at end-2015.

Strengthened retail capabilities with acquisition of Array Real Estate, which has been renamed Keppel Land Retail Management.

Overview / Operations and Market Review Keppel Land Limited Report to Shareholders 2015

Chairman’s Statement

Chairman’s Statement

0504

and Highline Residences in Tiong Bahru. Sales also came from Corals at Keppel Bay as well as Marina Bay Suites, our luxury residential project jointly developed with Cheung Kong Property Holdings and Hongkong Land, which is now fully sold.

With the easing of monetary and property market cooling measures in China, market sentiments and housing demand have improved.

We sold 3,280 units in the country, about 70% more than the 1,920 homes sold in 2014. These were mainly contributed by our projects in Shanghai, Chengdu, Tianjin and Wuxi.

We have embarked on our first joint venture project with China Vanke in China with V City, a large-scale residential development located between the third and fourth ring roads in Chengdu. This collaboration extends the strategic partnership with China Vanke to jointly develop residential projects in Singapore and China, which started in 2013 with The Glades in Singapore. Phase 1 of V City was launched in August 2015, and about 750 units were sold by end-2015. With a healthy pipeline of about 11,000 launch-ready units in China over the next three years, Keppel Land is

well-poised to capture demand for quality homes as the market continues to recover.

Vietnam, being our second largest overseas residential market after China, has recovered after a downturn in the property market for almost five years. Given the country’s strong GDP growth, expanding middle class and recent relaxation of foreign homeownership regulations, the residential market is expected to continue its upward trajectory.

Our projects achieved record sales of about 930 units in 2015, almost six times the 160 units sold in 2014. Estella Heights, our latest development in District 2 of Ho Chi Minh City (HCMC), achieved a strong take-up with 75% of a total of 872 units sold as of end-2015 following its launch in the same year. Phase 1A of our riverfront condominium in District 7, Riviera Point, also saw good response with about 260 units sold in 2015. In addition, together with our long-term Vietnamese partners Tien Phuoc and Tran Thai, as well as Hong Kong-based real estate private equity fund, Gaw Capital Partners, we will be developing a prime 14.6-hectare waterfront site in the Thu Thiem New Urban Area, which is poised to become the future central business district (CBD) of HCMC. We are excited that

01

01 Keppel Land, together with its joint venture partners, will be developing a prime 14.6-hectare waterfront site in the Thu Thiem New Urban Area, which is poised to become the future central business district of Ho Chi Minh City, Vietnam.

Keppel Land Limited Report to Shareholders 2015

Chairman’s Statement

06

through the project, we will bring the best in waterfront and urban lifestyles to HCMC as well as augment Keppel Land’s quality portfolio of prime residential and commercial properties in the city.

In Indonesia, we remain positive about the country’s longer term prospects which are supported by sound fundamentals of a large and young population, growing middle-class and continued urbanisation. We commenced sales and sold about 130 homes at West Vista, located in West Jakarta. In line with our strategy to focus on Greater Jakarta, Keppel Land secured a second residential site at Daan Mogot to tap on the demand for well-located and affordable homes in the growth corridor of West Jakarta.

Strengthening Commercial PortfolioThe Group is actively developing its portfolio of commercial properties which has increased to more than one million sm of gross floor area. Some of them will come on stream over the next two years, allowing us to attract quality tenants for steady income streams. In Singapore, Keppel Corporation and Keppel Land divested their combined 39% interest in Harbourfront Towers 1 and 2, and acquired the remaining 30% interest in Keppel Bay Tower through a share swap exercise with Mapletree Investments Pte Ltd. With the consolidation of ownership of the 450,000 sf Keppel Bay Tower, the Keppel Group will have greater flexibility to maximise the potential of the office building.

We are also progressing with Saigon Centre Phase 2 development in HCMC, Vietnam. The retail mall, with a gross floor area of 47,000 sm, is fully committed with leading Japanese retailer, Takashimaya Department Store, as the anchor tenant. The mall is expected to open in the second half of 2016.

In Indonesia, we topped out the 50,200 sm International Financial Centre (IFC) Jakarta Tower 2 in August 2015. The office tower is slated for completion in 2016. The existing IFC Jakarta Tower 1 is planned to be redeveloped into a 54-storey office tower, offering 71,700 sm of quality office space.

The Group is also expanding the SM-KL project in the Philippines with Phase 2 development comprising a 42-storey office building and an extension of the existing five-storey retail component, The Podium. When completed in 2017, the retail mall will have a total

gross floor area of about 73,000 sm, while the new office tower will offer about 110,000 sm of Grade A office space when completed in 2019. In Myanmar, Keppel Land entered into a joint venture with the Shwe Taung Group and acquired a 40% stake in a 23-storey Grade A office building, Junction City Tower, which is expected to be completed by 2017. The office building is part of Junction City, a mixed-use development in Yangon’s CBD, which also comprises the five-star Pan Pacific Hotel, a shopping centre as well as serviced residences.

While it remains focused on Asia, Keppel Land also invests opportunistically in key global cities with good growth potential. In February 2015, Keppel Land purchased a 126,000 sf freehold office building located at 75 King William Street, in London’s historic and central business district. The office tower is fully-tenanted, and is managed by Alpha Investment Partners (Alpha), the Group’s private property fund management arm.

Bolstering Retail Platform To strengthen our retail capabilities, we acquired a 75% stake in Array Real Estate in January 2015, which has since been renamed Keppel Land Retail Management (KLRM). KLRM will manage our existing retail assets and grow our retail and mixed-use commercial portfolio. KLRM has also been appointed the retail manager for 112 Katong, a lifestyle mall in the eastern part of Singapore. Keppel Land acquired a 22.4% stake in the mall in January 2016. The remaining 77.6% stake is held by Alpha Asia Macro Trends Fund (AAMTF), which is managed by Alpha.

With a retail development and management platform, Keppel Land will be able to harness the Company’s collective competencies to capitalise on opportunities in integrated mixed-use and retail developments to expand its commercial portfolio.

Growth in Fund ManagementKeppel REIT Management Limited and Alpha have grown their combined assets under management from $18.7 billion as at end-2014 to $20.5 billion as at end-2015. Both property fund management vehicles have monetised assets and recycled capital into the acquisition of new assets.

In October 2015, Keppel REIT completed the acquisition of three remaining prime street frontage retail units at 8 Exhibition Street in Melbourne, gaining strategic control of both

Our aim is to develop Keppel Land into a multi-faceted

property player, riding on urbanisation

trends in Asia.

Overview / Operations and Market Review

Chairman’s Statement07

the office and retail components of the building. In January 2016, Keppel REIT divested its 100% interest in 77 King Street in Sydney, Australia, for approximately A$160 million.

During the year, Alpha’s funds divested 10 assets across Singapore, Japan and South Korea. AAMTF II also acquired Kovan Heartland Mall and a suburban retail portfolio for about $380 million. Through the same fund, Alpha partnered City Developments Limited to invest in three prime office properties in Singapore – Central Mall (Office Tower), 7 & 9 Tampines Grande and Manulife Centre for a total value of $1.1 billion. Leveraging the macro trends of increasing urbanisation and consumerism in Asia, as well as riding on the successes of the first two Asia Macro Trends Funds, Alpha is embarking on its third such fund.

On 25 January 2016, Keppel Land received notification of Keppel Corporation’s intention to consolidate its interests in all four of its subsidiaries in business trust management, REIT management and fund management under Keppel Capital Holdings Pte. Ltd. This includes Keppel Land’s interests in Keppel REIT Management Limited as well as Alpha.

The proposed consolidation will help to strengthen the Keppel Group’s capital recycling platform and create an expanded capital platform for co-investing in new assets. It will also improve the performances of the managers of Keppel REIT and Alpha through centralising certain non-regulated support functions and creating a larger platform that will enhance recruitment and retention of talent, as well as sharing of best practices.

We have continued to set robust targets

for ourselves, benchmarking against

the best in class in Environmental,

Social and Governance aspects.

0101 In 2015, Keppel Land sold 3,280 units in China, about 70% more than the 1,920 homes sold in 2014.

Keppel Land Limited Report to Shareholders 2015

Chairman’s Statement

08

In the long run, Keppel Land will also benefit from improved investment returns from Keppel REIT and Alpha.

Driving Sustainability and Upholding Quality As a property developer, we are mindful of the impact that our business operations have on the environment. As such, we have continued to set robust targets for ourselves, benchmarking against the best in class in Environmental, Social and Governance aspects.

Keppel Land’s commitment to sustainability won us the Building and Construction Authority of Singapore’s (BCA) Green Mark Champion Award (Developer) and Built Environment Leadership (Gold Class) Award. Keppel Land also clinched seven Green Mark Platinum awards, and currently has in its portfolio more than 60 BCA Green Mark-certified projects in Singapore and overseas.

Keppel Land set a new milestone when it was ranked fourth in the prestigious Corporate Knights’ Global 100 Most Sustainable Corporations 2015, the first time an Asian company made it to the top 10. Back home, Keppel Land clinched the top award for the large organisations category at the inaugural Singapore Apex Corporate Social Responsibility Awards 2015 for demonstrating a high level of social responsibility and sustainability excellence in its business practices.

Keppel Land’s commitment to quality in its developments has also been widely recognised. In the Euromoney Real Estate Awards 2015, Keppel Land received a total of six awards for Singapore, Vietnam and Indonesia. We were named the Best Office/Business Developer in the three countries, as well as the Best Residential Developer in Singapore and Vietnam. For the first time, we clinched the Best Overall Investment Manager Award for Alpha. For its economic and social contributions to the local Chinese communities, Keppel Land China was conferred the Top 10 ASEAN Companies in China Award in 2016 by the China-ASEAN Business Council. It is the only company that has been awarded the accolade for four consecutive years.

Safety is one of the Group’s core values and remains a top priority. For our strong commitment to the health, safety and well-being of our workforce, Keppel Land garnered the bizSAFE Mentor Award by the Workplace Safety and Health Council for the third consecutive year. On the international front, we were also recognised at the prestigious International Safety Awards 2015 by the British Safety Council.

Recognising that our people are the most valuable asset of the Company, we have continued to attract, develop and retain our talent pool. Over the past few years, our HR emphasis has been on selection and recruitment, job rotation and enlargement, localisation, performance management and manpower planning. For our efforts, we were recognised at the 2015 Singapore HR Awards for Leading HR Practices in Talent Management, Retention and Succession Planning.

AcknowledgementsOn behalf of the Board, I would like to thank our shareholders, customers and business partners for their continued support.

My appreciation goes to our Directors for their guidance in navigating the Company through the challenging times. We would like to thank Mrs Lee Ai Ming and Mr Heng Chiang Meng, who have retired from the Board, for their invaluable contribution and wise counsel in the last 13 and 10 years respectively. I would also like to thank the management team and employees for their hard work and perseverance.

Although 2016 is expected to be another challenging year, I am confident that Keppel Land will be able to ride through the challenges with guidance from the Board, strong commitment of its management team and staff, as well as continued support from all stakeholders.

Yours sincerely,

Loh Chin HuaChairman31 May 2016

Overview / Operations and Market Review

Chairman’s Statement09

We will continue to strengthen presence in our core markets of Singapore and China, expand in our growth markets of Vietnam and Indonesia, as well as seize opportunities in other emerging markets and global gateway cities.

Ang Wee GeeCEO

Some of the property markets in Asia are expected to remain subdued in 2016. How confident is Keppel Land in riding out these headwinds?

A

Q2016 will continue to be challenging as the economy and the property sector in a few of our key markets are expected to remain subdued. However, I am confident that we will overcome these challenges, just as we had weathered headwinds over the years, including the Asian Financial Crisis in 1998 and the Global Financial Crisis in 2008. Each time, Keppel Land emerged stronger by being more focused on our business, as well as exercising prudence and discipline.

Being geographically diversified has served the Company well. In 2015, overseas contribution, most of which was from China, made up 57% of our earnings. We will continue to strengthen presence in our core markets of Singapore and China, expand in our growth

markets of Vietnam and Indonesia, as well as seize opportunities in other emerging markets and global gateway cities.

Another pillar of our strategy is the recycling of capital through the divestment of assets at the appropriate time. In 2002, we kick-started the divestment of our prime office portfolio with the sale of our 70% stake in Capital Square. In 2006, we spun off four office buildings valued at $630 million into a commercial real estate investment trust (REIT), K-REIT Asia, which has since been renamed Keppel REIT. Between 2007 and 2014, we divested to Keppel REIT our stakes in One Raffles Quay, Ocean Financial Centre, Marina Bay Financial Centre Phases 1 and 2, enabling it to grow into one of the largest commercial REITs in Singapore.

QIs Keppel Land moving its focus away from Singapore, as the Company has a limited residential landbank and no new commercial development in the pipeline in Singapore? Looking ahead, what is the Company’s strategy in Singapore?

A

We have continued to be disciplined in recycling assets and redeploying capital to seek higher returns. Over the past two years, we have monetised almost $2.4 billion worth of assets.

The success of Keppel Land’s strategy and execution shows in its return on equity which is one of the highest among Asian developers. We have continued to be disciplined in recycling assets and redeploying capital to seek higher returns. Over the past two years, we have monetised almost $2.4 billion worth of assets. This includes our stakes in Marina Bay Financial Centre Tower 3 and Equity Plaza in Singapore, as well as BG Junction retail mall in Surabaya, Indonesia. Part of these proceeds were recycled for the acquisition of two well-located residential sites in West Jakarta, an additional

Singapore remains one of our core markets and we will continue to pursue opportunities in residential, office and mixed-use developments. For example, we bought into Array Real Estate in January 2015, which we subsequently renamed Keppel Land Retail Management (KLRM), to strengthen our capabilities in the development and management of retail and mixed-use developments.

Residential demand in Singapore has softened in the last two years after the government implemented cooling measures to prevent the sharp escalation of prices. The market is however, showing signs of stabilising.

We will continue to selectively seek sites with good value propositions to augment our existing land bank. We currently have 1,210 homes in our pipeline, of which about 44% are located within the Keppel Bay precinct. These homes are valued for their unique designs, prime location and waterfront offerings.

As for the commercial market, there have not been many Grade A office or prime mixed-use developments released through the government land sales programme in the past few years. Apart from the government

stake in the Estella Heights residential project in Ho Chi Minh City, as well as stakes in an office tower in Yangon, a large-scale residential township joint venture project with China Vanke in Chengdu, a residential apartment block in New York and an office development in London. We have also recently announced the divestment of two properties in Vietnam, stakes in a Thai-listed company as well as a property company in Sri Lanka. We are also in the process of divesting several other assets in the region.

land supply, we will explore other avenues, such as acquiring existing developments, which will offer opportunities for us to value-add through asset enhancement or redevelopment.

For instance, we recently acquired the remaining 22.4% stake in 112 Katong mall, located in the eastern part of Singapore. The majority 77.6% stake is held under Alpha Investment Partners’ Alpha Asia Macro Trends Fund. KLRM, which assisted in the sale, has been appointed the retail manager for the property and will be carrying out asset enhancement works to reposition the property and enhance its value. The Keppel Group also recently consolidated ownership of Keppel Bay Tower in a share swap exercise with Mapletree Investments to acquire the remaining 30% stake in the property. These acquisitions have augmented our quality commercial portfolio, providing rental income, while their consolidated ownership will also make it easier for us to realise the value of the properties at the appropriate time.

In addition, we are substantially invested in the office sector in Singapore through our 45% stake in Keppel REIT, which owns about 2.6 million sf of attributable net lettable area of prime office space in Singapore.

Overview / Operations and Market Review Keppel Land Limited Report to Shareholders 2015

Interview with the CEO

Interview withthe CEO

1110

Keppel Land has extensive overseas exposure in Asia and beyond. What will be your key focus and how do you plan to grow these overseas markets over the next few years?

A

Q

Over the past three years, we have established greater geographical focus by concentrating on key cities in our core markets of Singapore and China, and growth markets of Vietnam and Indonesia. In China, the cities are Shanghai, Beijing, Chengdu, Tianjin and Wuxi, while in Vietnam, it is Ho Chi Minh City, and in Indonesia, it is Greater Jakarta.

In 2015, we deepened our presence in key markets by investing in a residential site in West Jakarta, a large-scale residential township in Chengdu through a joint venture with China Vanke, and acquiring a stake in Nam Long Investment Corporation, an affordable housing developer in Vietnam.

With China currently experiencing slower economic growth, the government has an interest to keep the property market healthy given that the real estate sector accounts for 25-30% of the country’s GDP. The lifting of home purchase restrictions in many cities, together with the lower downpayments and low mortgage rates, have made homes more affordable and will help to draw buyers back into the market. With our supply of about 11,000 launch-ready units in China over the next three years, we are well-positioned to capitalise on any uptick in demand.

Vietnam is expected to continue its growth momentum after posting the best growth in Asia in 2015. Demand for residential properties is expected to continue to be strong, driven by demand for quality housing as well as the relaxation of foreign homeownership regulations. We have more than 5,200 launch-ready units in Vietnam for the next three years.

As for Indonesia, although growth has slowed due to a fall in demand for oil and commodities, we are optimistic about the longer term prospects

as the country’s large and young population will continue to support demand for well-located and affordable homes.

Myanmar is a promising and up-and-coming country. We have already established our presence with two hotels in Yangon and Mandalay under the Sedona brand, and have taken a 40% stake in Junction City Tower, the office component of Junction City, a mixed-use development in Yangon’s central business district. As investors flock to explore opportunities in what is considered the next frontier in Asia, there will be demand for good quality office space and hotel accommodation. Sedona Hotel Yangon, where we have just added a new wing of more than 400 rooms, will benefit from the influx of business and tourist visitors.

With rapid urbanisation, a growing middle-class and infrastructure improvements, the urban landscape in Asia is fast evolving, creating opportunities for the development of quality residential, office, retail and mixed-use developments to meet rising demand for urban and sustainable living.

Keppel Land will strengthen its operating platforms and also ride on KLRM’s experience and network to capture opportunities in retail and mixed-use projects, and scale up our commercial presence in the region.

Leveraging our established networks and relationships with the local governments, partners and business associates in these markets, we will further strengthen our footprint in existing and new cities, build new capabilities as well as deliver innovative and thoughtful products and experiences to our homebuyers and tenants.

Our focus on developing people, driving a culture of innovation, collaboration

and sustainability as well as embracing new technologies will help to differentiate

us from the competition.

Keppel Land Limited Report to Shareholders 2015

Interview withthe CEO

12

A

What is your vision for Keppel Land?

QKeppel Land’s vision and mission were refreshed in early-2015 to reinforce our aspiration to be the leading real estate company, shaping the best for future generations.

To achieve our vision, we need to put in place the right culture, the right people and the right business strategy. Over the last few years, we have worked hard to build an open, collaborative, innovative and entrepreneurial culture at Keppel Land. The commendable score in our 2015 employee engagement survey is an affirmation of our efforts. However, building a positive culture and sustaining an engaged workforce require continual effort and there will always be areas which we need to improve on.

Our people remain central to our ability to do well and we will continue to attract, motivate,

develop and retain strong talents. Our emphasis on selection and recruitment, job rotation and job enlargement, localisation of our business operations overseas, as well as performance management and manpower planning over the recent years have yielded positive results. Looking ahead, we will further strengthen our bench strength through developing our internal talents and hiring exceptional external talents. We will continue with our push to localise so as to strengthen our operating platforms overseas, as well as seek to maximise productivity and improve operations.

We will continually review our strategies to ensure that they remain relevant in the challenging business environment. To maintain our competitive edge, we need to execute our strategies well and respond to market changes swiftly.

01

01 Indonesia is one of Keppel Land’s key growth markets where it will continue to further strengthen its presence. Pictured is the International Financial Centre Jakarta Tower 2, which topped out in August 2015.

Overview / Operations and Market Review

Interview with the CEO13

01 Keppel Land continues to engage and nurture communities wherever it operates. The Company was a major sponsor of the Green Corridor Run held in March 2016.

Keppel Land has garnered international recognition for its environmental, social and governance (ESG) performance. With increasing focus on ESG issues in Asia, what steps will Keppel Land take to tackle challenges such as climate change?

A

QSince we embarked on our sustainability journey about 10 years ago, we have been playing an active role in creating sustainable live-work-play environments and giving back to the communities wherever we operate.

Testament to our efforts, our ranking at Corporate Knights’ Global 100 Most Sustainable Corporations in the World rose from 17th in 2014 to a commendable 4th in 2015, topping Asian and real estate companies worldwide. During the year, we were also conferred the Building and Construction Authority of Singapore’s (BCA) Quality Champion Gold Award (Developer) and Built Environment Leadership (Gold Class) Award.

We will do our part to protect the environment by developing environmentally-friendly properties, preserving biodiversity and inculcating green mindsets among our stakeholders. We strive to reduce our carbon footprint and target to cut, by 2020, our carbon emissions intensity by 16% below 2010’s levels. Looking ahead, we will focus on engaging our stakeholders along the supply chain so that we can influence and encourage our contractors and suppliers to adopt sustainable and best procurement practices. As a responsible corporate citizen, we will continue to step up our community outreach initiatives, with a focus on education and the environment.

01

QCan you share your strategy on developing talent and driving innovation within the Company?

AWe recognise that people are our most valuable assets. We have put in place leadership development and localisation programmes to groom employees with high potential as well as provide multiple platforms to engage staff. We will continue to invest in our people by nurturing our talent pool and improving staff engagement to drive growth.

Upholding the Company’s brand tagline of “Thinking Unboxed”, we will continue to innovate and collaborate more closely with other businesses in the Keppel Group to leverage the Group’s diverse strengths to offer greener and smarter

solutions for our residential and commercial developments. Our recent partnership with Keppel’s associated company, M1, for the Smart Lives programme is one such initiative. We have also formed multi-disciplinary teams comprising staff from different business and functional units to explore a number of exciting new business and operational initiatives, some of which may be implemented as early as this year.

Our focus on developing people, driving a culture of innovation, collaboration and sustainability as well as embracing new technologies will help to differentiate us from the competition.

Keppel Land Limited Report to Shareholders 2015

Interview withthe CEO

14

Ang Wee Gee age 54Executive Director and Chief Executive Officer Date of first appointment as a director:1 January 2013Date of last re-election as a director:19 April 2013Length of service as a director (as at 31 December 2015):3 years

Board Committee(s) served on:Board Safety Committee (Member)

Present Directorships:Listed companiesKeppel REIT Management Limited (the Manager of Keppel REIT)

Other principal directorshipsKeppel Land China Limited (Chairman)Keppel Land Retail Management Pte Ltd (Chairman)Alpha Investment Partners Limited

Major Appointments(other than directorships):Member of the Board of the Building and Construction Authority of Singapore

Loh Chin Hua age 54Chairman, Non-Executive and Non-External Director Date of first appointment as a director:1 July 2012Date of last re-election as a director:19 April 2013Length of service as a director (as at 31 December 2015):3 years 6 months

Board Committee(s) served on:Board Safety Committee (Member)

Present Directorships:Listed companiesKeppel Corporation Limited Keppel Telecommunication & Transportation Ltd (Chairman)

Other principal directorshipsKeppel Offshore & Marine Ltd (Chairman)Keppel Infrastructure Holdings Pte Ltd (Chairman)Alpha Investment Partners Limited (Chairman)

Major Appointments(other than directorships):Chief Executive Officer of Keppel Corporation Limited

Overview / Operations and Market Review

Board of Directors

Board of Directors

15

Edward Lee Kwong Foo age 69Non-Executive andExternal Director Date of first appointment as a director:1 July 2006Date of last re-election as a director:19 April 2013Length of service as a director (as at 31 December 2015):9 years 6 months

Board Committee(s) served on:Board Risk Committee (Member)Board Safety Committee (Member)

Present Directorships:Listed companiesIndofood Agri Resources LtdQAF Limited

Other principal directorshipsAsia Mobile Holdings Pte LtdGas Supply Pte LtdPT Dermaga Perkasa PratamaPT Kawasan Industri KendalPT Fairfax Insurance Indonesia

Major Appointments(other than directorships):Member of the National University of Singapore President’s Advancement Advisory Council

Tan Yam Pin age 75Non-Executive andExternal Director

Date of first appointment as a director:1 June 2003Date of last re-election as a director:30 April 2015Length of service as a director (as at 31 December 2015):12 years 7 months

Board Committee(s) served on:Board Safety Committee (Chairman)

Present Directorships:Listed companiesGreat Eastern Holdings LimitedSingapore Post Limited

Other principal directorshipsNil

Major Appointments(other than directorships):Member of the Singapore Public Service Commission

Keppel Land Limited Report to Shareholders 2015

Board of Directors

16

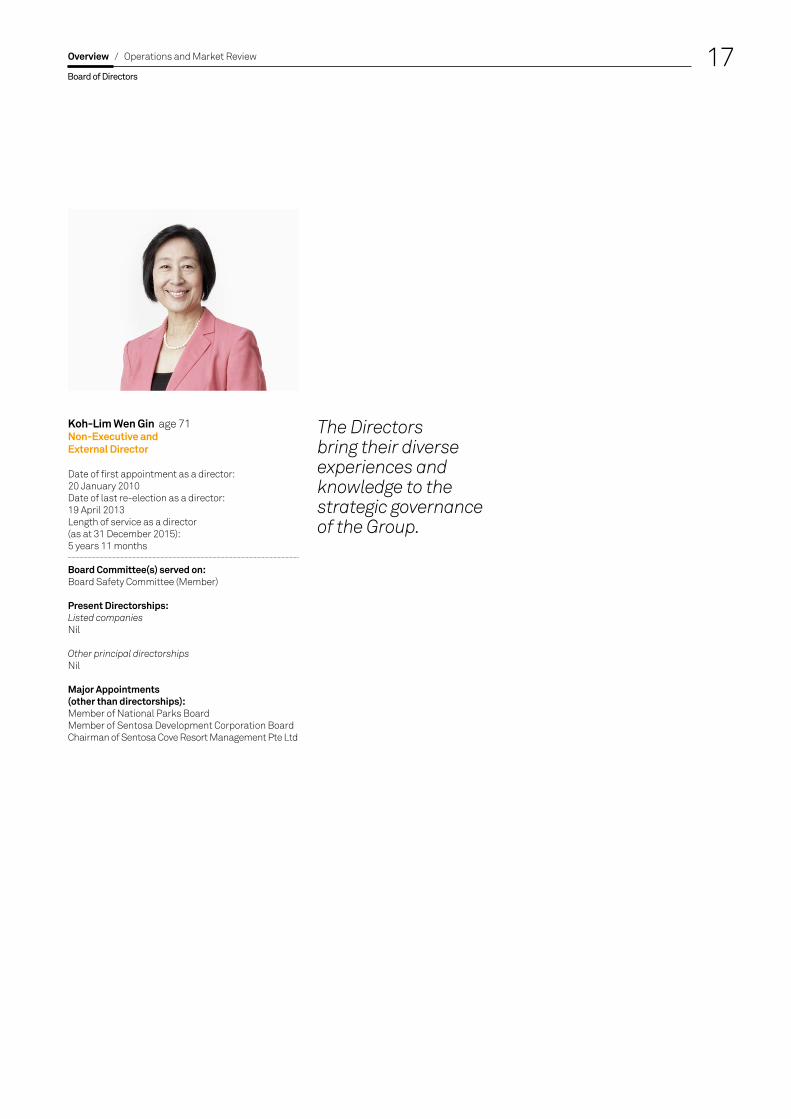

Koh-Lim Wen Gin age 71Non-Executive andExternal Director

Date of first appointment as a director:20 January 2010Date of last re-election as a director:19 April 2013Length of service as a director (as at 31 December 2015):5 years 11 months

Board Committee(s) served on:Board Safety Committee (Member)

Present Directorships:Listed companiesNil

Other principal directorshipsNil

Major Appointments(other than directorships):Member of National Parks BoardMember of Sentosa Development Corporation BoardChairman of Sentosa Cove Resort Management Pte Ltd

The Directors bring their diverse experiences and knowledge to the strategic governance of the Group.

Overview / Operations and Market Review

Board of Directors17

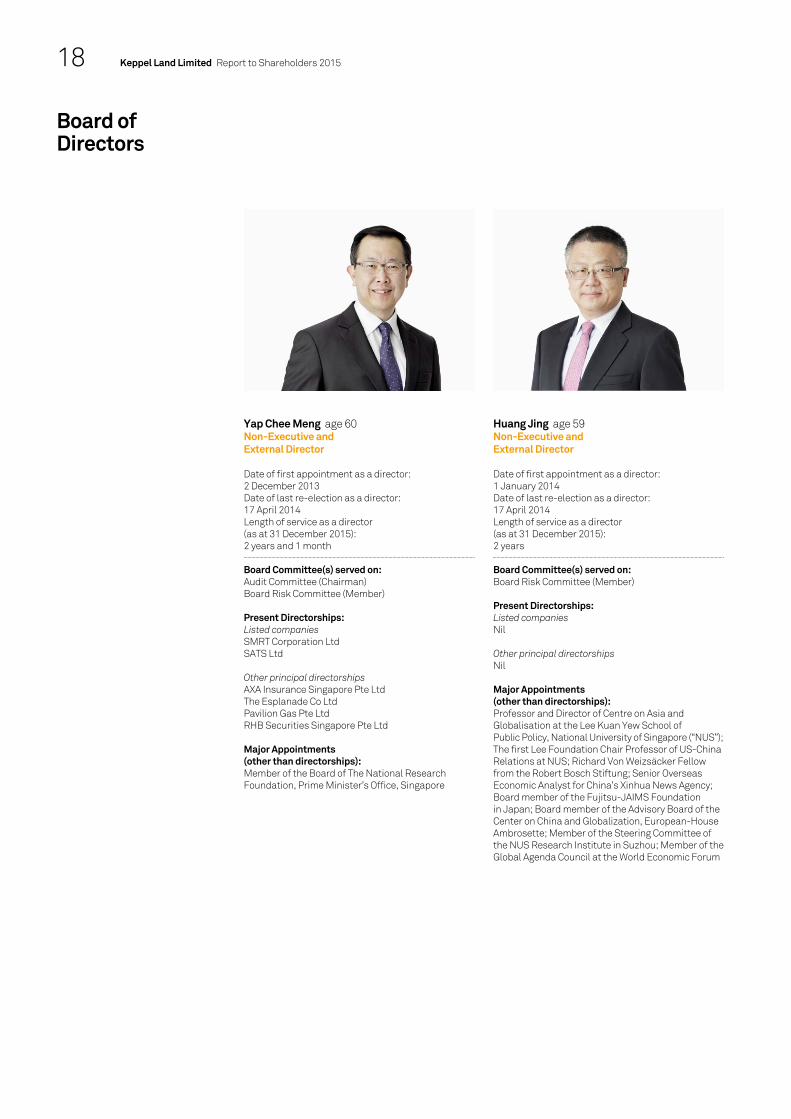

Huang Jing age 59Non-Executive andExternal Director Date of first appointment as a director:1 January 2014Date of last re-election as a director:17 April 2014Length of service as a director (as at 31 December 2015):2 years

Board Committee(s) served on:Board Risk Committee (Member)

Present Directorships:Listed companiesNil

Other principal directorshipsNil

Major Appointments(other than directorships):Professor and Director of Centre on Asia and Globalisation at the Lee Kuan Yew School of Public Policy, National University of Singapore (“NUS”);The first Lee Foundation Chair Professor of US-China Relations at NUS; Richard Von Weizsäcker Fellow from the Robert Bosch Stiftung; Senior Overseas Economic Analyst for China’s Xinhua News Agency;Board member of the Fujitsu-JAIMS Foundation in Japan; Board member of the Advisory Board of the Center on China and Globalization, European-HouseAmbrosette; Member of the Steering Committee of the NUS Research Institute in Suzhou; Member of the Global Agenda Council at the World Economic Forum

Yap Chee Meng age 60Non-Executive andExternal Director

Date of first appointment as a director:2 December 2013Date of last re-election as a director:17 April 2014Length of service as a director (as at 31 December 2015):2 years and 1 month

Board Committee(s) served on:Audit Committee (Chairman)Board Risk Committee (Member)

Present Directorships:Listed companiesSMRT Corporation LtdSATS Ltd

Other principal directorshipsAXA Insurance Singapore Pte LtdThe Esplanade Co LtdPavilion Gas Pte LtdRHB Securities Singapore Pte Ltd

Major Appointments(other than directorships):Member of the Board of The National Research Foundation, Prime Minister’s Office, Singapore

Keppel Land Limited Report to Shareholders 2015

Board of Directors

18

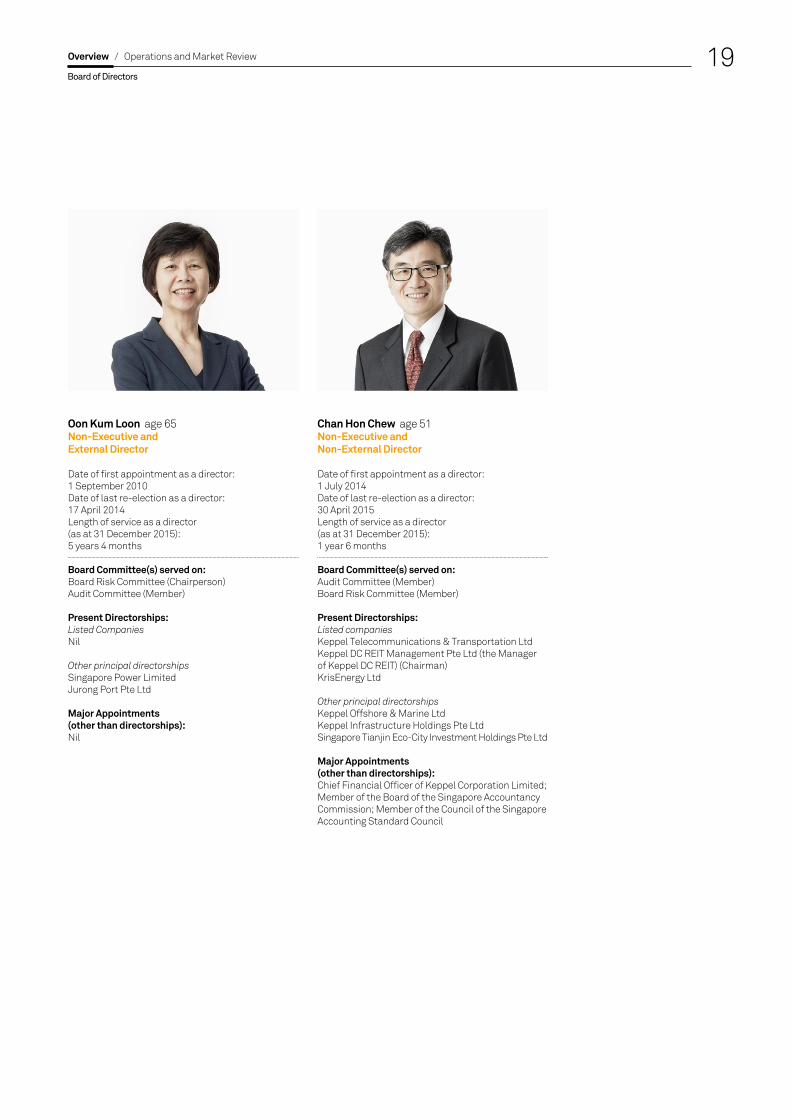

Chan Hon Chew age 51Non-Executive andNon-External Director

Date of first appointment as a director:1 July 2014Date of last re-election as a director:30 April 2015Length of service as a director (as at 31 December 2015):1 year 6 months

Board Committee(s) served on:Audit Committee (Member)Board Risk Committee (Member)

Present Directorships:Listed companiesKeppel Telecommunications & Transportation LtdKeppel DC REIT Management Pte Ltd (the Manager of Keppel DC REIT) (Chairman)KrisEnergy Ltd

Other principal directorshipsKeppel Offshore & Marine LtdKeppel Infrastructure Holdings Pte LtdSingapore Tianjin Eco-City Investment Holdings Pte Ltd

Major Appointments(other than directorships):Chief Financial Officer of Keppel Corporation Limited;Member of the Board of the Singapore Accountancy Commission; Member of the Council of the Singapore Accounting Standard Council

Oon Kum Loon age 65Non-Executive andExternal Director Date of first appointment as a director:1 September 2010Date of last re-election as a director:17 April 2014Length of service as a director (as at 31 December 2015):5 years 4 months

Board Committee(s) served on:Board Risk Committee (Chairperson)Audit Committee (Member)

Present Directorships:Listed CompaniesNil

Other principal directorshipsSingapore Power LimitedJurong Port Pte Ltd

Major Appointments(other than directorships):Nil

Overview / Operations and Market Review

Board of Directors19

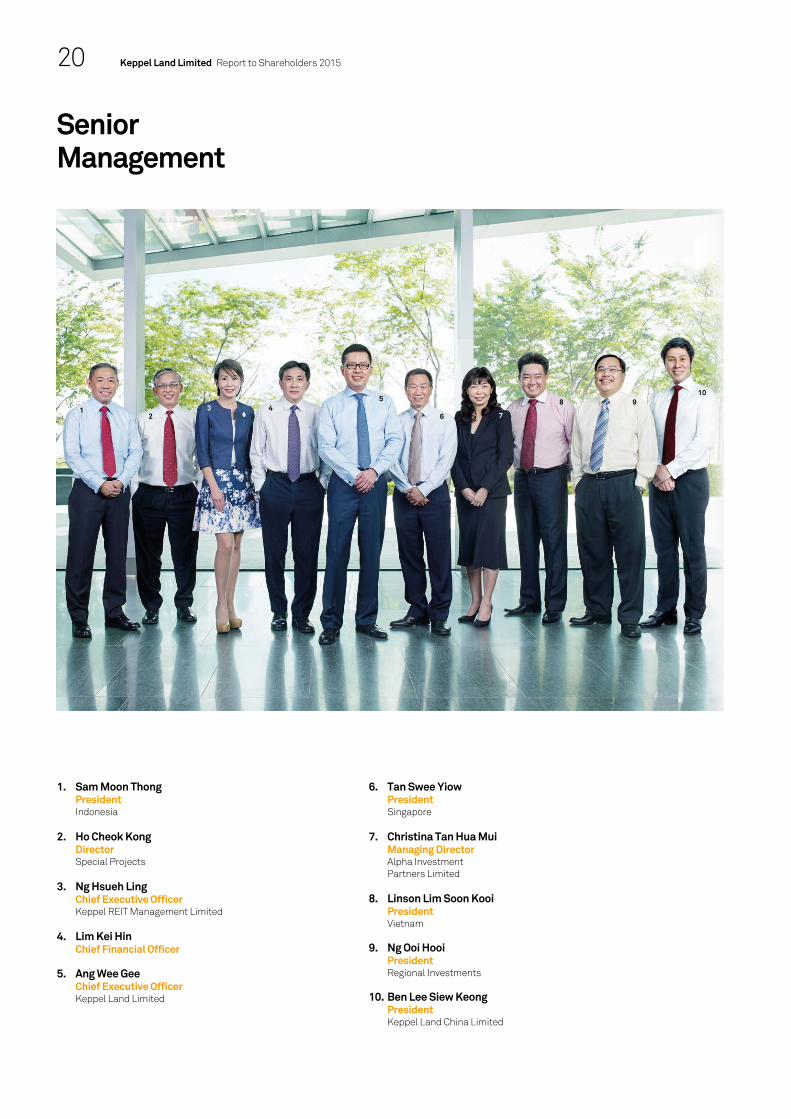

1. Sam Moon Thong President Indonesia

2. Ho Cheok Kong Director Special Projects

3. Ng Hsueh LingChief Executive Officer Keppel REIT Management Limited

4. Lim Kei HinChief Financial Officer

5. Ang Wee GeeChief Executive Officer Keppel Land Limited

6. Tan Swee YiowPresident Singapore

7. Christina Tan Hua MuiManaging DirectorAlpha Investment Partners Limited

8. Linson Lim Soon KooiPresident Vietnam

9. Ng Ooi HooiPresident Regional Investments

10. Ben Lee Siew KeongPresident Keppel Land China Limited

12

3 45

6 7

8 910

Keppel Land Limited Report to Shareholders 2015

Senior Management

20

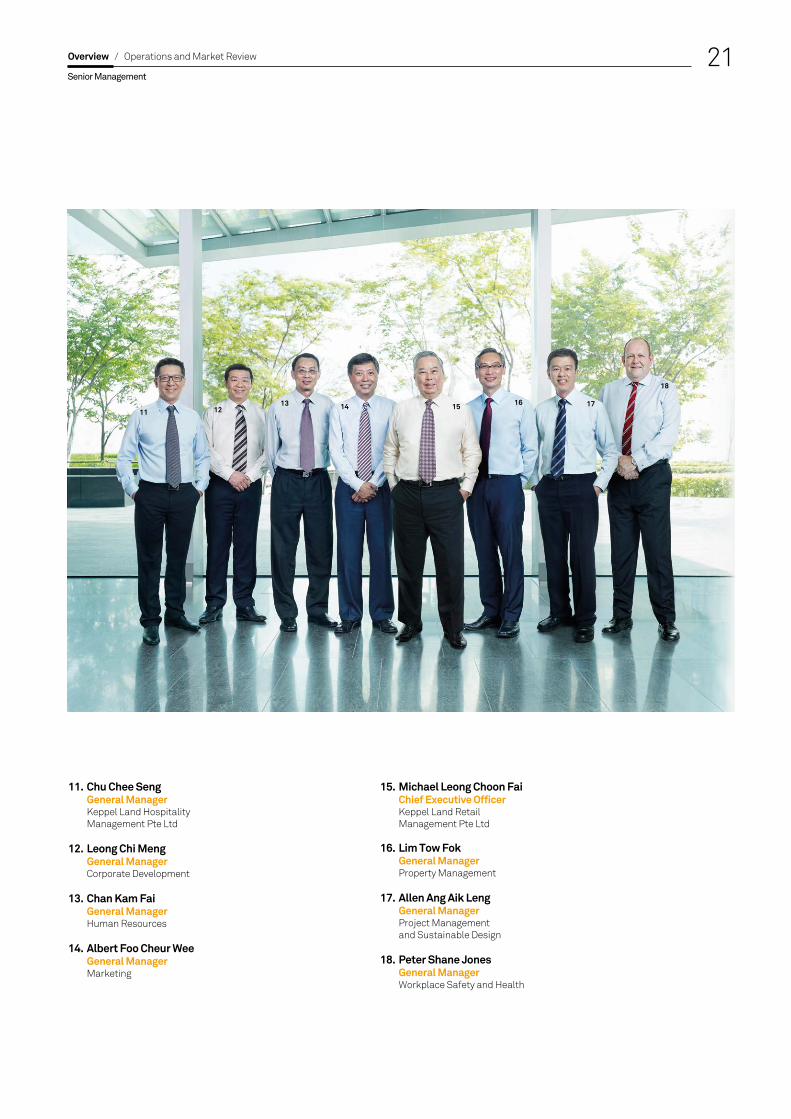

11. Chu Chee SengGeneral Manager Keppel Land Hospitality Management Pte Ltd

12. Leong Chi MengGeneral Manager Corporate Development

13. Chan Kam FaiGeneral Manager Human Resources

14. Albert Foo Cheur Wee General Manager Marketing

15. Michael Leong Choon FaiChief Executive OfficerKeppel Land Retail Management Pte Ltd

16. Lim Tow FokGeneral Manager Property Management

17. Allen Ang Aik LengGeneral Manager Project Management and Sustainable Design

18. Peter Shane Jones General Manager Workplace Safety and Health

11 1213 14 15 16 17

18

Overview / Operations and Market Review

Senior Management21

Keppel Land Limited

Loh Chin HuaChairman

Ang Wee GeeChief Executive Officer

Property Investment, Development and Management

Keppel Land International Limited

Lim Kei HinChief Financial Officer

Singapore

Tan Swee YiowPresidentSingapore

International ChinaHo Cheok KongPresidentKeppel Land China Limited(until 29 February 2016)

Ben Lee Siew KeongPresidentKeppel Land China Limited(effective 1 March 2016) Vietnam Linson Lim Soon KooiPresidentVietnam IndonesiaSam Moon ThongPresidentIndonesia India, Malaysia, Myanmar, Sri Lanka, The Philippines and ThailandNg Ooi HooiPresidentRegional Investments

Keppel Land Limited Report to Shareholders 2015

KeyPersonnel

22

Property Fund Management

Ng Hsueh LingChief Executive OfficerKeppel REIT Management Limited

Kelvin Chow Chung YipChief Financial OfficerKeppel REIT Management Limited

Christina Tan Hua Mui Managing DirectorAlpha Investment Partners Limited

Goo Li LingChief Financial OfficerAlpha Investment Partners Limited

Hospitality Management

Tan Swee YiowDirectorKeppel Land Hospitality Management Pte Ltd

Chu Chee SengGeneral ManagerKeppel Land Hospitality Management Pte Ltd(effective 2 November 2015)

Khoo Peck KhoonGeneral Manager (Golf and Marina Operations)Keppel Land Hospitality Management Pte Ltd(effective 2 November 2015)

Retail Management

Michael Leong Choon FaiChief Executive OfficerKeppel Land Retail Management Pte Ltd

Special ProjectsHo Cheok KongDirector(effective 1 March 2016)

Group Finance and AccountsTan Boon PingFinancial Controller(until 31 October 2015)

Wong Man LiFinancial Controller(effective 1 November 2015)

Finance and AdministrationMelissa Tan Siew NgokGeneral Manager

MarketingAlbert Foo Cheur WeeGeneral Manager

Project Management and Sustainable DesignAllen Tan Kuang LiangDeputy General Manager(until 11 January 2016)

Allen Ang Aik LengGeneral Manager(effective 12 January 2016)

Property Management Lim Tow FokGeneral Manager

Workplace Safety and HealthPeter Shane JonesGeneral Manager

Human ResourcesChan Kam FaiGeneral Manager

Corporate Services and Corporate Social ResponsibilitySerena Toh Lai SiongGeneral Manager

Corporate DevelopmentLeong Chi MengGeneral Manager

Information TechnologyKevin Chua Kee WeeDeputy General Manager

Group Internal AuditJessica Cheong Weai MunDeputy General Manager

Risk ManagementYeo Hwee PeyAssistant General Manager

Corporate

Overview / Operations and Market Review

Key Personnel23

Vietnam

Linson Lim Soon KooiPresidentVietnam

Doan Anh HungGeneral ManagerVietnam

Joseph Low Kar YewDeputy General ManagerOperations

Keppel Land China Limited

Ho Cheok KongPresident(until 29 February 2016)

Ben Lee Siew KeongPresident(effective 1 March 2016)General ManagerOperations(until 29 February 2016)

Patrick Lim Jean LoongChief Financial Officer(until 30 November 2015)

Tan Boon PingChief Financial Officer(effective 1 December 2015)

William Tan Tin KwangGeneral ManagerNorthern China

Desmond Wong Hong KiongGeneral ManagerRegional Head Daniel Chong Siew HoeGeneral ManagerRegional Head

Benjamin Kang Min ShinGeneral ManagerBusiness Development

Lee Eng BengGeneral ManagerMarketing Tan Joo ChuahGeneral ManagerProject Management(until 3 January 2016)

Gavin Lu Yee LiangGeneral ManagerProject Management(effective 4 January 2016) Wong Wai FooDeputy General ManagerProperty Management Vincent See Wing Chuen General ManagerHuman Resources

Kenny Phua Boon PeowDeputy General ManagerChengdu

Frank Ong Cheng PohDeputy General ManagerTianjin

Eric Cheng LuAssistant General ManagerWuxi

Keppel Land Limited Report to Shareholders 2015

KeyPersonnel

24

Indonesia

Sam Moon ThongPresidentIndonesia

Wong Chee WaiDeputy General ManagerOperations

Regional Investments

Ng Ooi HooiPresidentRegional Investments

MyanmarGoh York LinPresident

ThailandOh Lock SoonManaging DirectorKeppel Thai Properties Public Company Limited

IndiaYeo Chee KianDeputy General ManagerBangalore

MalaysiaSteven Shum Wing OnDeputy General Manager

Sri LankaR. Pannir Chelvam s/o RamayaDeputy General Manager(until 29 February 2016)

The PhilippinesLee Foo TuckPresidentKeppel Philippines Properties, Inc.

Overview / Operations and Market Review

Key Personnel25

Awards and Accolades

Awards and Accolades

01

Corporate Recognition

Global 100 Most Sustainable Corporations in the WorldKeppel Land was ranked fourth in Corporate Knights’ Global 100 Most Sustainable Corporations in the World 2015, placing it first in Asia and among real estate companies worldwide.

Top 10 ASEAN Companies in ChinaFor the fourth consecutive year, Keppel Land China was conferred the Top 10 ASEAN Companies in China Award by the China-ASEAN Business Council in 2016. The award honours model ASEAN companies which have achieved business success and contributed positively to the local Chinese communities they operate in. Keppel Land China is the only company that has been awarded the accolade for four years running.

Governance and Transparency IndexKeppel Land was ranked seventh out of 639 listed companies in Singapore at the annual Governance and Transparency Index, jointly organised by CPA Australia, NUS Business School’s Centre for Governance, Institutions and Organisations as well as The Business Times.

ASEAN Corporate Governance AwardsKeppel Land was lauded for its high standards of corporate governance at the 2015 ASEAN Corporate Governance Awards, an initiative of the ASEAN Capital Markets Forum and supported by the Asian Development Bank. The award recognises companies that continuously implement good corporate governance in their operations and services.

Corporate Social Responsibility

The RobecoSAM Sustainability YearbookFor the fifth consecutive year, Keppel Land was featured in the RobecoSAM Sustainability Yearbook 2015 as one of the top 15% of companies worldwide in sustainability leadership.

International Safety AwardsFor its commitment to upholding good safety practices, Keppel Land was recognised at the prestigious International Safety Awards 2015 by the British Safety Council.

BizSAFE MentorFor its exemplary Workplace Safety and Health management and performance, Keppel Land was conferred the bizSAFE Mentor certificate for the third consecutive year.

BCA AwardsKeppel Land garnered five awards at the annual Building and Construction Authority of Singapore (BCA) Awards. This includes the coveted BCA Built Environment

Singapore Corporate AwardsKeppel Land won the Bronze Award for Best Annual Report in the large capitalisation category at the Singapore Corporate Awards 2015.

Euromoney Real Estate AwardsKeppel Land garnered six Euromoney Real Estate Awards, including Best Office/Business Developer in Singapore, Indonesia and Vietnam, Best Residential Developer in Singapore and Vietnam as well as Best Investment Manager (Overall) in real estate services in Singapore.

BCI Asia AwardsKeppel Land was named one of the top 10 developers in Vietnam at the BCI Asia Top 10 Awards.

Singapore HR AwardsKeppel Land was recognised for Leading HR Practices in Talent Management, Retention and Succession Planning, and accorded special mentions in Performance Management.

02

Leadership Award (Gold Class), BCA Quality Excellence Award (Quality Champion, Gold), BCA Universal Design Mark GoldPlus (Design) Award for Highline Residences, BCA Universal Design Mark Gold (Design) Award for The Luxurie and the inaugural BCA Green Mark Pearl Award for Marina Bay Financial Centre Tower 3.

Singapore Apex CSR AwardsKeppel Land took top honours in the Large Organisations category at the inaugural Singapore Apex Corporate Social Responsibility (CSR) Awards. The award recognises companies for their social responsibility and sustainability excellence in their business practices.

Fish Friendly MarinaMarina at Keppel Bay was accredited as Asia’s first Fish Friendly Marina by the Marina Industries Association for its efforts in improving the habitat of marine life within its waters.

Sustainable DevelopmentsOcean Financial Centre and Marina Bay Financial Centre were among six buildings that were awarded the Water Efficient Building (Gold) certification by the PUB. Bugis Junction Towers received the Silver certification.

Separately, for its efficient energy management practices, Ocean Financial Centre was named the winner in the Large Green Building category at the ASEAN Energy Awards 2015. The award aims to promote regional cooperation on projects relating to energy efficiency and sustainability.

Product Excellence

FIABCI Prix d’ExcellenceMarina Bay Suites was conferred the Silver Award in the Residential (High Rise) category at the highly acclaimed FIABCI Prix d’Excellence Awards. Marina Bay Financial Centre Phase 1 was also awarded the FIABCI Singapore SG50 Special Award in the Office category at the Singapore Property Awards.

Design ExcellenceKeppel Land was conferred the Singapore Good Design Mark Gold Award for Reflections at Keppel Bay and for the interactive multimedia wall at Highline Residences’ sales gallery. In addition, the multimedia wall at Highline Residences won Silver in the Multimedia-Interface Design category at the 8th International Design Awards.

Quality DevelopmentsKeppel Land emerged as one of the big winners at the

inaugural Vietnam Property Awards. Saigon Centre Phase 2 was named the winner for Best Commercial and Best Retail Development, while Riviera Point was named the Best Mid-range Condominium Development in Ho Chi Minh City (HCMC). The Company also received the Highly Commended Award for Best Office Development and Best Retail Architectural Design for Saigon Centre Phase 2, Best Residential Architectural Design for Riviera Point, and Best Luxury Condominium Development in HCMC for Estella Heights.

Distinction in HospitalitySedona Suites Hanoi was named the Best Serviced Residence at the 14th Golden Dragon Awards organised by the Vietnam Economic Times and Ministry of Planning and Investment.

Spring City Golf & Lake Resort (Spring City) and Tianjin Eco-City International Country Club were named among the Top 10 Most Outstanding Golf Resorts by China’s Golfers’ Choice Awards. Spring City was also named one of the Top 10 Most Outstanding Golf Courses at the same event. Golf Digest (China edition) also listed Spring City among China’s Top 10 Golf Resorts.

03

01 Keppel Land was conferred the Bronze Award for Best Annual Report in the large capitalisation category at the Singapore Corporate Awards 2015. 02 At the annual Building and Construction Authority Awards 2015, Keppel Land garnered five awards. 03 Keppel Land garnered six Euromoney Real Estate Awards in 2015.

Overview / Operations and Market Review Keppel Land Limited Report to Shareholders 2015 2726

CorporateMilestones

2015

January• Keppel Land acquired a

well-located 4.6-hectare (ha) site in West Jakarta, Indonesia, to develop a high-rise condominium with ancillary shophouses and shop units.

• Keppel Land acquired a 75% stake in retail management company Array Real Estate, which was subsequently renamed Keppel Land Retail Management.

February• Keppel Land acquired a

freehold nine-storey office building at 75 King William Street in the City of London.

• Keppel Land and China Vanke extended their strategic alliance into China to jointly develop a 16.7-ha prime residential site in Chengdu.

March• Keppel Land increased its

stake in Estella Heights in Ho Chi Minh City from 55% to 98%.

• Keppel REIT topped out the David Malcolm Justice Centre office tower in Perth, Australia.

April• Keppel Land topped out the

Inya Wing of Sedona Hotel Yangon in Myanmar.

July• Keppel Land was privatised

with Keppel Corporation owning over 99% of the Company at the completion of the privatisation.

August• The Company topped out

International Financial Centre Jakarta Tower 2, a landmark commercial development in the central business district of Jakarta, Indonesia.

• Keppel REIT received the Certificate of Practical Completion for the David Malcolm Justice Centre.

October• Sedona Hotel Yangon celebrated

the soft opening of its new Inya Wing which adds an additional 431 guest rooms and suites.

December• Alpha Investment Partners,

through Alpha Asia Macro Trends Fund II, partnered City Developments Limited (CDL), in a $1.1 billion joint office investment platform that acquired three of CDL’s prime office assets.

• Keppel Land and M1 launched the pilot Smart Lives programme at The Luxurie to provide smart living solutions for Keppel Land’s residential and commercial properties.

• Keppel Corporation and Keppel Land consolidated the Group’s ownership of Keppel Bay Tower through a share swap exercise with Mapletree Investments. Keppel acquired the remaining 30% interest in Harbourfront One Pte Ltd which holds Keppel Bay Tower, in exchange for its 39% interest in Harbourfront Two Pte Ltd, which holds Harbourfront Towers 1 and 2.

01

Keppel Land Limited Report to Shareholders 201528

Corporate Governance

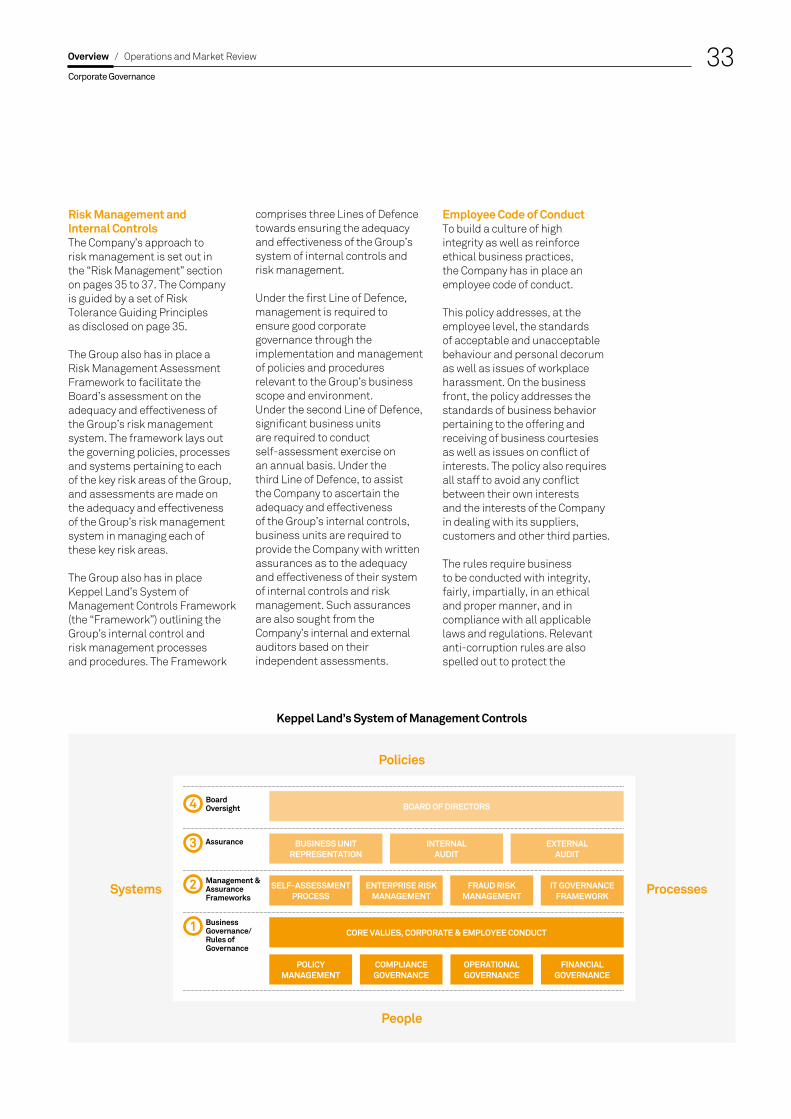

The Company’s Directors and Management firmly believe that full commitment to high standards of corporate governance is essential to ensure the sustainability of the Company’s businesses and performance as well as to safeguard shareholders’ interests and maximise long-term shareholder value.

Board MattersThe Board’s Conduct of AffairsThe Board oversees the effectiveness of Management as well as the corporate governance of the Company with the objective of maximising long-term shareholder value and protecting the Company’s assets. Its key roles include the review and approval of the Group’s corporate strategies and directions, annual budgets, major investments, divestments and funding proposals and the review of the Group’s financial performance, risk management processes and systems, and sustainability considerations including corporate governance practices. The Board is also responsible for setting the Company’s core values and ethical standards.

Board Committees include the Audit Committee, Board Risk Committee and Board Safety Committee. The Nominating Committee and the Remuneration Committee have been dissolved. These Board Committees have clearly defined written terms of reference. Matters which are delegated to Board Committees for more detailed evaluation and approval are reported to and monitored by the Board.

The Board has included in its oversight, consideration of sustainability issues such as environmental, social and governance factors in the strategic formulation and execution of the Company’s objectives. Every Board meeting includes an update on sustainability issues. The Board meets regularly on a quarterly basis and as warranted.

Board Composition Presently, there are nine Directors. With the exception of Mr Ang Wee Gee, who is the Chief Executive Officer (“CEO”), the rest of the eight Directors are non-executive Directors. With the exception of Mr Loh Chin Hua, Mr Ang Wee Gee and Mr Chan Hon Chew, the rest of the six

Directors are external Directors (“External Directors”). External Directors are directors who do not have an executive position within the Company and its related companies.

The Directors provide an appropriate balance and diversity of skills, experience, gender and knowledge of the Company, as well as relevant core competencies in areas such as accounting or finance, legal, business or management experience, industry knowledge, strategic planning experience, and customer-based experience or knowledge. The Chairman of the Board is Mr Loh Chin Hua. In terms of composition of the Board, External Directors form the majority.

Chairman and Chief Executive OfficerTo ensure an appropriate balance of power, increased accountability and a greater capacity of the Board for independent decision-making, the Company has a clear division of responsibilities at the top level of the Company, with the non-executive Chairman and the CEO having separate roles.

02

Keppel Land is committed to achieving high standards of corporate governance to ensure the sustainability of the Company’s businesses as well as to safeguard shareholders’ interests.

01 Keppel Land topped out International Financial Centre Jakarta Tower Two in Indonesia in August 2015. 02 Keppel Land proactively engages shareholders on the Company’s strategic directions at its Annual General Meetings.

Corporate Governance

Overview / Operations and Market Review 29

Corporate Governance

The Chairman leads the Board and is responsible for the management of the Board, encourages Board’s interaction with Management, facilitates effective contribution of the Directors, encourages constructive relations among the Directors, and promotes high standards of corporate governance. The Chairman approves the agenda for Board meetings and ensures sufficient time is spent to cover all items in the agenda, especially on strategic issues. The Chairman and CEO are separate persons and are not related to each other.

The CEO has full executive responsibilities over the business directions set by the Board and operational decisions of the Group. The CEO is accountable to the Board for the conduct and performance of the Group.

Board MembershipProcess and Criteria Used for Selection and Appointment of New DirectorsTo increase the reliability of the process, the Board’s

diversity in terms of mix of expertise, knowledge and experience on the Board is evaluated and, in consultation with Management, the role and the desirable competencies for a particular appointment is determined. Recommendations from, inter alia, Directors and Management are the usual source for potential candidates. However, external search consultants are also considered.

Formal interviews with the short-listed candidates are conducted to assess their suitability and the candidates are verified of their awareness of the expectations and the level of commitment required, after which suitable candidates will be approved.

The following criteria are used to assess all new appointments:

(a) Integrity;(b) Independent mindedness;(c) Possession of core

competencies that meets the needs of the Company and complements the

skills and competencies of the existing Directors on the Board;

(d) Ability to commit time and effort to carry out duties and responsibilities effectively;

(e) Track record of making good decisions;

(f) Experience in high-performing organisations; and

(g) Financial literacy.

The internal guideline adopted by the Company to address the issue of multiple board representations is that Directors should not have more than six listed company board representations and other principal commitments.

The Board recognises that proper succession planning plays an important role in ensuring continuous and effective stewardship of the Company. As such, the Company’s succession plans are reviewed annually to ensure the progressive renewal of the Board, including the Chairman and the CEO. Succession and leadership development plans for Management are also reviewed.

01

01 Keppel Land was lauded for its high standards of corporate governance at the 2015 ASEAN Corporate Governance Awards. Receiving the award on behalf of Keppel Land was Mr Linson Lim (second from left), President (Vietnam).

Keppel Land Limited Report to Shareholders 201530

Corporate Governance

Remuneration MattersRemuneration Policy for Executive Directors and Other Key Management PersonnelThe Company adopts a remuneration system that is aimed at attracting, retaining and motivating talent on a sustainable basis. In designing the compensation structure, the Company seeks to ensure that the level and mix of remuneration is competitive, relevant and appropriate in finding a balance between current versus long-term compensation and between cash versus equity incentive compensation.

The annual fixed cash component comprises the annual basic salary plus fixed allowances which the Company benchmarks with the relevant industry market data.

The annual performance incentive which is tied to the performance of the Company, business unit and individual employee,

is inclusive of a portion which is tied to economic value added (“EVA”) performance. The EVA performance incentive is currently extended to only key management personnel who have greater line of sight to value creation.

The compensation structure is directly linked to corporate and individual performances, both in terms of financial, non-financial performance and the creation of shareholder wealth.

Accountability and AuditThe Board, supported by the Audit Committee (“AC”) and Board Risk Committee (“BRC”), oversees the Group’s system of internal controls and risk management.

Audit CommitteeThe AC’s primary role is to assist the Board to ensure the integrity of financial reporting and the existence of sound internal control systems. The AC is kept abreast of changes to

accounting and governance standards and issues which have a direct impact on financial statements through quarterly updates and discussion with the external auditor.

The AC is guided by the following terms of reference:

(1) Review financial statements relating to financial performance, and review significant financial reporting issues and judgements contained in them, for better assurance of the integrity of such statements;

(2) Review and report to the Board at least annually the adequacy and effectiveness of the Group’s internal controls, including financial, operational, compliance and information technology controls (such review can be carried out internally or with the assistance of any competent third parties);

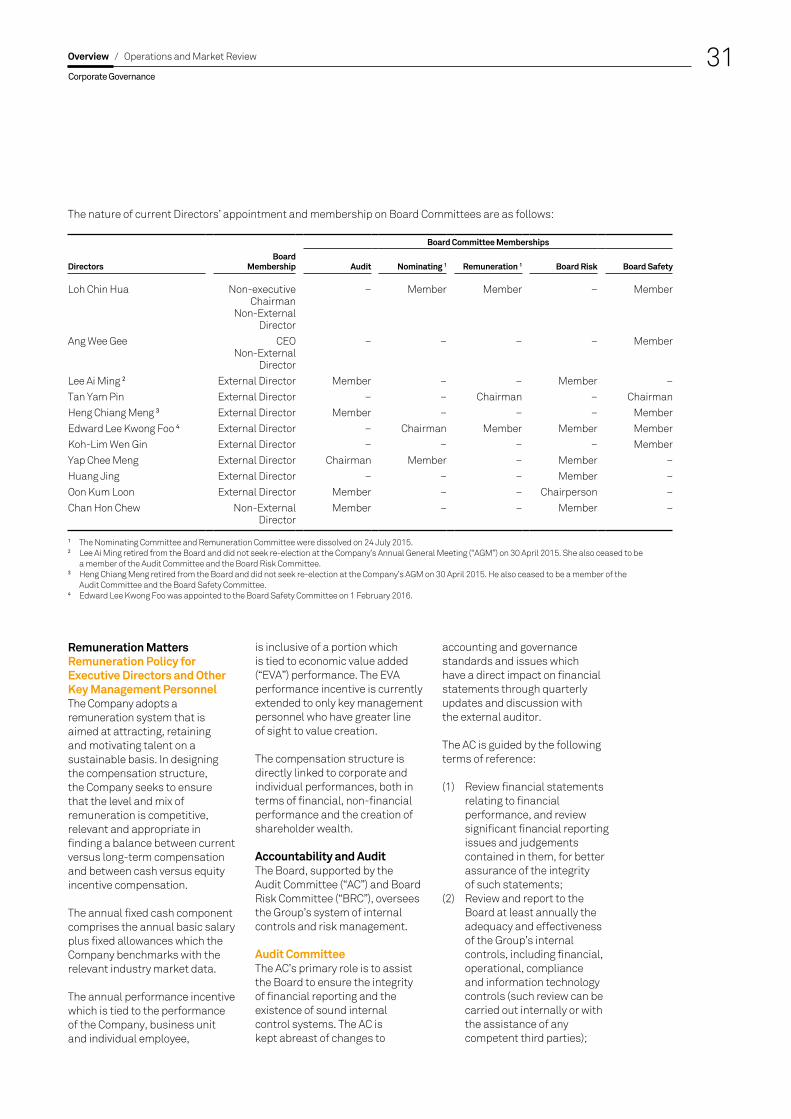

The nature of current Directors’ appointment and membership on Board Committees are as follows:

Board Committee Memberships

DirectorsBoard

Membership Audit Nominating 1 Remuneration 1 Board Risk Board Safety

Loh Chin Hua Non-executive Chairman

Non-External Director

– Member Member – Member

Ang Wee Gee CEONon-External

Director

– – – – Member

Lee Ai Ming 2 External Director Member – – Member –Tan Yam Pin External Director – – Chairman – ChairmanHeng Chiang Meng 3 External Director Member – – – MemberEdward Lee Kwong Foo 4 External Director – Chairman Member Member MemberKoh-Lim Wen Gin External Director – – – – MemberYap Chee Meng External Director Chairman Member – Member –Huang Jing External Director – – – Member –Oon Kum Loon External Director Member – – Chairperson –Chan Hon Chew Non-External

DirectorMember – – Member –

1 The Nominating Committee and Remuneration Committee were dissolved on 24 July 2015.2 Lee Ai Ming retired from the Board and did not seek re-election at the Company’s Annual General Meeting (“AGM”) on 30 April 2015. She also ceased to be

a member of the Audit Committee and the Board Risk Committee.3 Heng Chiang Meng retired from the Board and did not seek re-election at the Company’s AGM on 30 April 2015. He also ceased to be a member of the

Audit Committee and the Board Safety Committee.4 Edward Lee Kwong Foo was appointed to the Board Safety Committee on 1 February 2016.

Overview / Operations and Market Review 31

Corporate Governance

(3) Review audit plans and reports of the external auditor and internal auditor, and consider the effectiveness of actions or policies taken by Management on the recommendations and observations;

(4) Review the independence and objectivity of the external auditor;

(5) Meet with external auditor and internal auditor, without the presence of Management, at least annually;

(6) Review the adequacy and effectiveness of the Company’s internal audit function, at least annually;

(7) Investigate any matters within the AC’s purview, whenever it deems necessary;

(8) Report to the Board on material matters, findings and recommendations;

(9) Review the AC’s terms of reference annually and recommend any proposed changes to the Board;

(10) Perform such other functions as the Board may determine; and

(11) Sub-delegate any of its powers within its terms of reference as listed above from time to time as the AC may deem fit.

During the year, the AC reviewed the internal and external auditors’ plans and findings to ensure that they are sufficient to assess the adequacy and effectiveness of the Company’s significant internal controls, including financial, operational, compliance and information technology controls and management of risks of fraud and other irregularities. The AC also reviewed the effectiveness of the actions taken by Management on the recommendations made by the internal and external auditors in this respect.

The AC also performed independent reviews of the financial statements of the Company. The AC has explicit authority to investigate any matter within its terms of reference, full access to and cooperation by Management and full discretion to invite any Director or executive officer to attend its meetings, and has reasonable resources to enable it to discharge its functions properly.

The AC held five meetings during the year. The Company’s internal and external auditors reported their audit findings and recommendations independently to the AC. The AC also met with the internal and external auditors, without the presence of Management. At the meetings, the external auditor briefed the members of the AC on the latest developments in accounting and governance standards and practices. In addition, the AC reviewed the independence and objectivity of the external auditor through discussions with the external auditor.