vancouver international wine festival 2015 annual … · vancouver international wine festival 2015...

TRANSCRIPT

!!!!!

Vancouver International Wine Festival2015 Annual Wine Law Seminar !!Vancouver, BC February 23, 2015

!David Enns, Tony Holler, Al Hudec

1

MAKE MONEY IN THE BC WINERY INDUSTRY

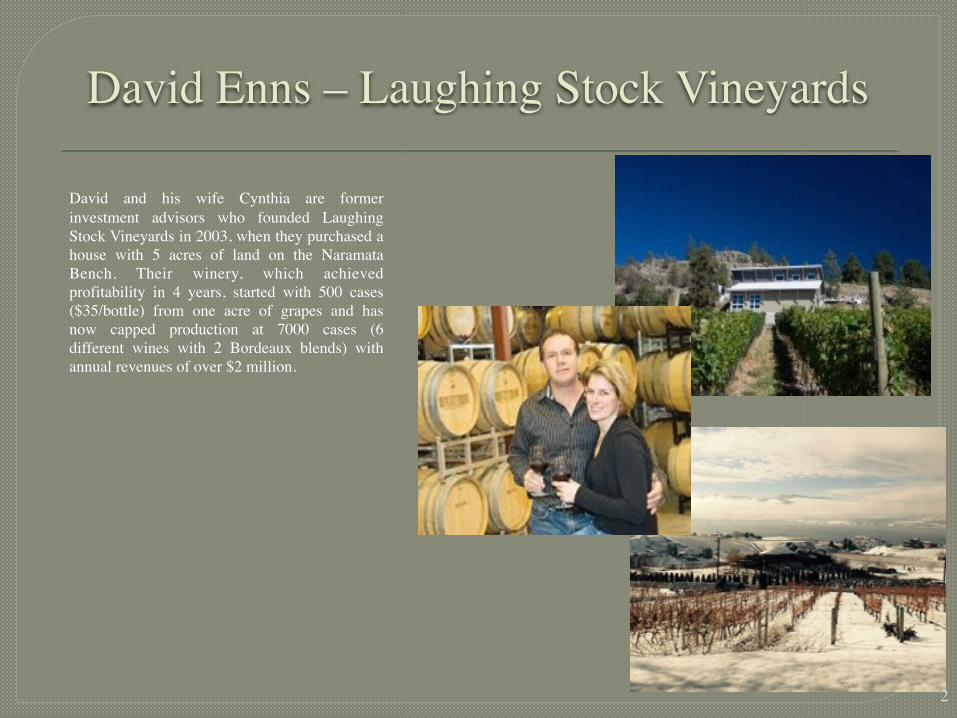

David Enns – Laughing Stock Vineyards David and his wife Cynthia are former

investment advisors who founded Laughing Stock Vineyards in 2003, when they purchased a house with 5 acres of land on the Naramata Bench. Their winery, which achieved profitability in 4 years, started with 500 cases ($35/bottle) from one acre of grapes and has now capped production at 7000 cases (6 different wines with 2 Bordeaux blends) with annual revenues of over $2 million.

2

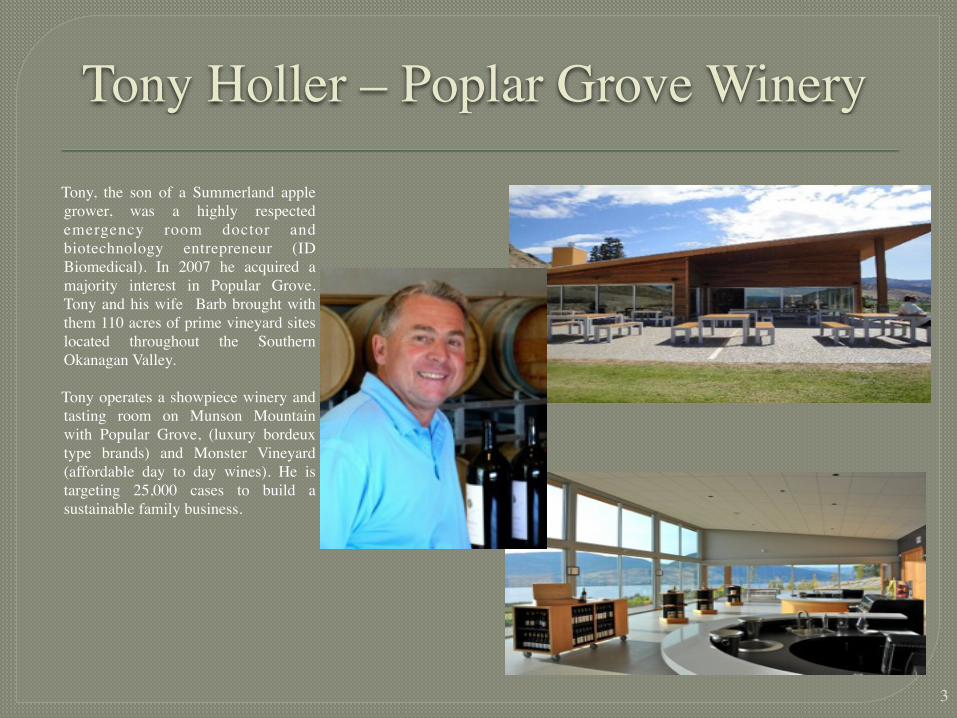

Tony Holler – Poplar Grove Winery

Tony, the son of a Summerland apple grower, was a highly respected emergency room doctor and biotechnology entrepreneur (ID Biomedical). In 2007 he acquired a majority interest in Popular Grove. Tony and his wife Barb brought with them 110 acres of prime vineyard sites located throughout the Southern Okanagan Valley. !Tony operates a showpiece winery and tasting room on Munson Mountain with Popular Grove, (luxury bordeux type brands) and Monster Vineyard (affordable day to day wines). He is targeting 25,000 cases to build a sustainable family business.

3

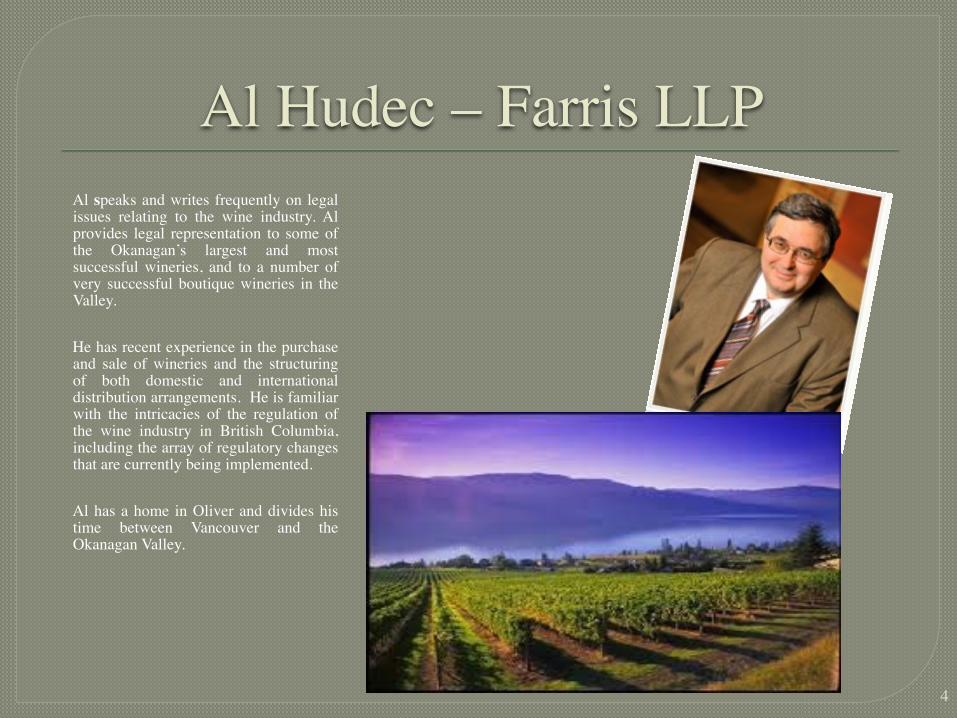

Al Hudec – Farris LLPAl speaks and writes frequently on legal issues relating to the wine industry. Al provides legal representation to some of the Okanagan’s largest and most successful wineries, and to a number of very successful boutique wineries in the Valley. !He has recent experience in the purchase and sale of wineries and the structuring of both domestic and international distribution arrangements. He is familiar with the intricacies of the regulation of the wine industry in British Columbia, including the array of regulatory changes that are currently being implemented. !Al has a home in Oliver and divides his time between Vancouver and the Okanagan Valley.

4

Legal Categories• Land-based wineries – 243 licenses

• Minimum production capacity of 4500 litres • 100% B.C. Grapes

• 2 acres on site • 25% owned or leased

• Commercial wineries – 3 largest players (11 licensees in total) • Virtual wineries – 17 non-licensed but manufacturing under another winery’s license

5

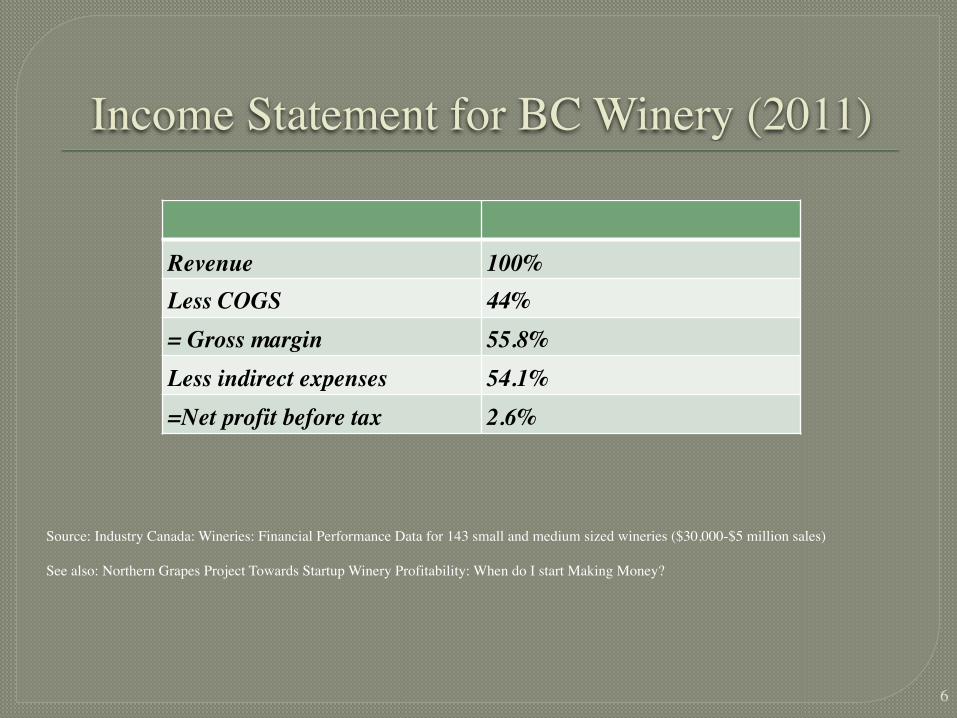

Income Statement for BC Winery (2011)

!!!!!!!!!!!!!!!!!!Source: Industry Canada: Wineries: Financial Performance Data for 143 small and medium sized wineries ($30,000-$5 million sales) !See also: Northern Grapes Project Towards Startup Winery Profitability: When do I start Making Money?

6

Revenue 100%Less COGS 44%= Gross margin 55.8%Less indirect expenses 54.1%=Net profit before tax 2.6%

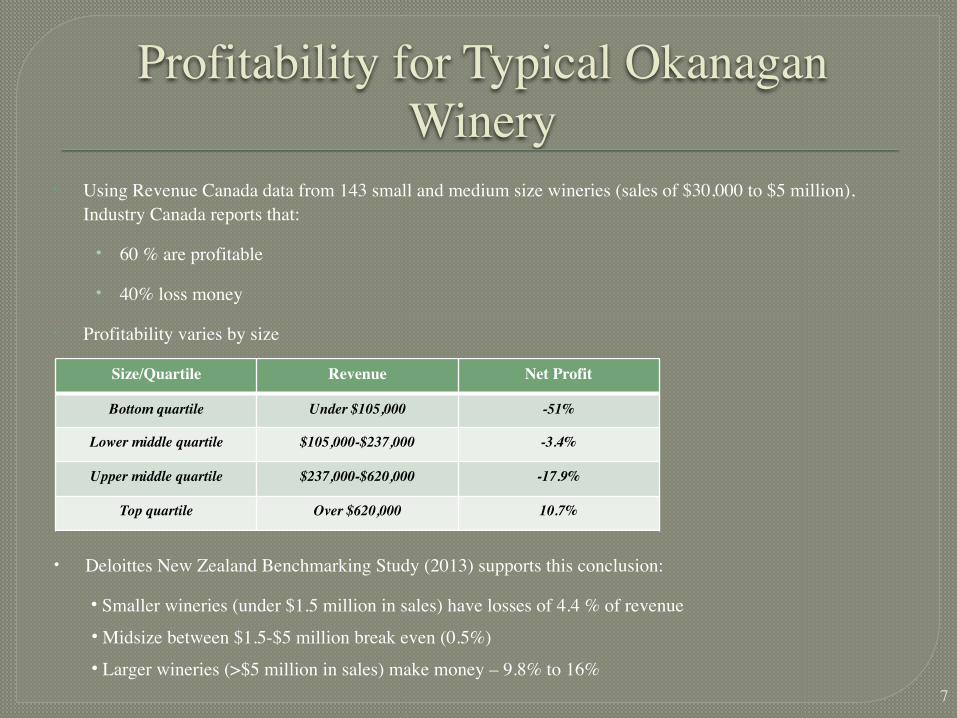

Profitability for Typical Okanagan Winery

• Using Revenue Canada data from 143 small and medium size wineries (sales of $30,000 to $5 million), Industry Canada reports that:

• 60 % are profitable • 40% loss money

• Profitability varies by size

7

Size/Quartile Revenue Net Profit

Bottom quartile Under $105,000 -51%

Lower middle quartile $105,000-$237,000 -3.4%

Upper middle quartile $237,000-$620,000 -17.9%

Top quartile Over $620,000 10.7%

• Deloittes New Zealand Benchmarking Study (2013) supports this conclusion: • Smaller wineries (under $1.5 million in sales) have losses of 4.4 % of revenue • Midsize between $1.5-$5 million break even (0.5%) • Larger wineries (>$5 million in sales) make money – 9.8% to 16%

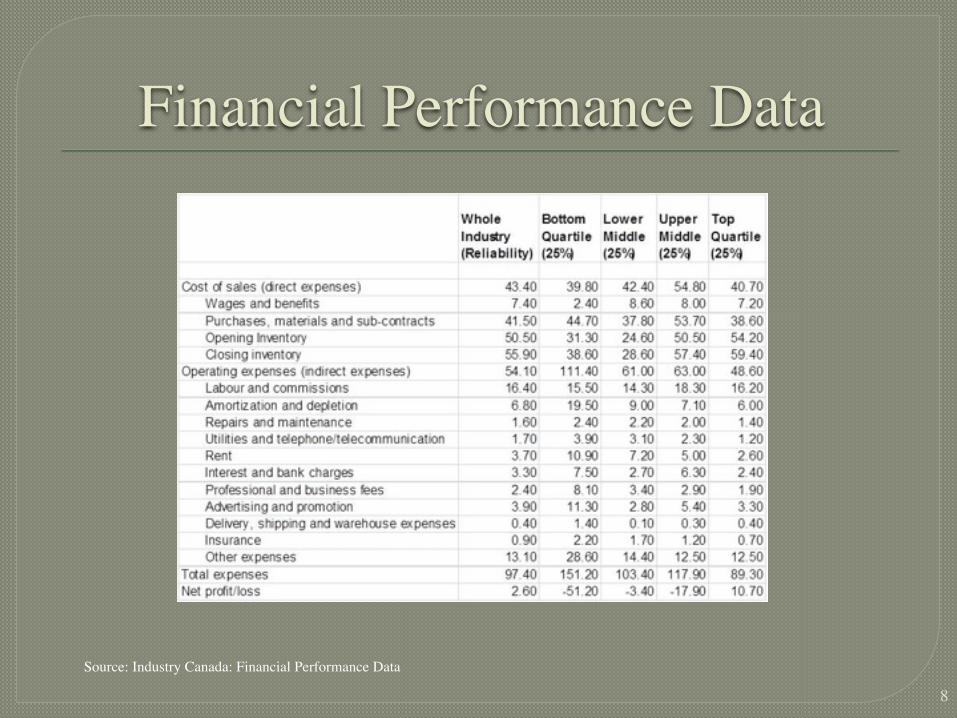

Financial Performance Data

8

Source: Industry Canada: Financial Performance Data

Economies of Scale(Average total costs)

9

Cases 2000 5000 10,000 15,000 20,000ATC/Case $154 $137 $126 $126 $124ATC/Bottle $12.87 $11.44 $10.54 $10.53 $10.41

!!Source: Small Winery Investment and Operating Costs, Extension Bulletin Washington Extension Study

Look for industry consolidation, reality in larger competitors with increased scale and resources; impact on margins and customer retention for the small Family businesses.

Pricing Points1. Premium/Ultra-premium – highest price and highest profitability

● To be a meaningful consumer you need to be in the top quartile of income earners (boomers) ● Rob McMillan of SVB is predicting a breakout year with 14-18% revenues growth !

2. Popularly priced brands

3. Value price brands ● Dominated by bulk wine import (Cellared in Canada) ● OR uncontracted grapes

10

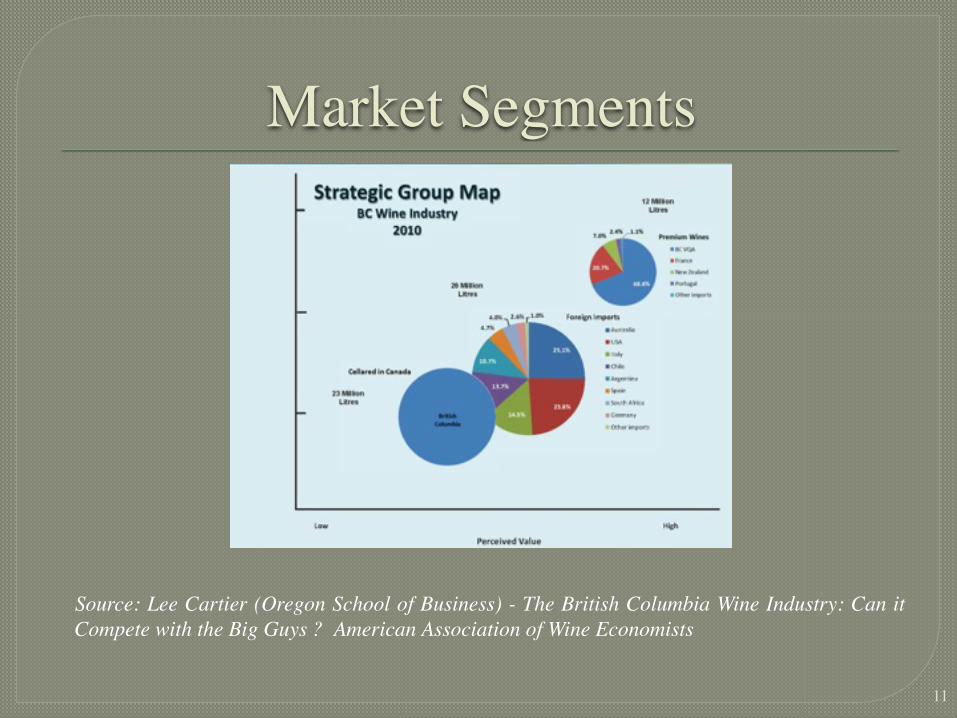

Market Segments!!!!!!!!!Source: Lee Cartier (Oregon School of Business) - The British Columbia Wine Industry: Can it Compete with the Big Guys ? American Association of Wine Economists

11

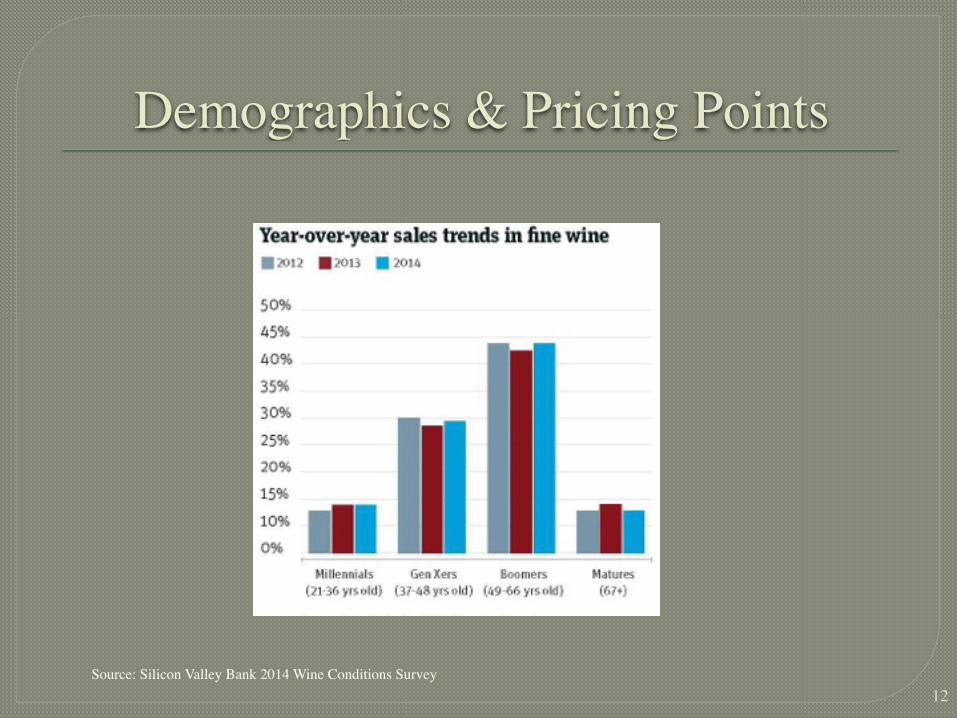

Demographics & Pricing Points

12Source: Silicon Valley Bank 2014 Wine Conditions Survey

Sales Channels• Direct sales ● Tasting room ● Wine club

● Internet ● Secondary tasting rooms ● Farmers’ markets ● Interprovincial sales

• Hospitality industry • Retailers ● LRS ● LDB ● Independent Wine Stores ● VQA stores

• Grocery stores – What is the opportunity?

13

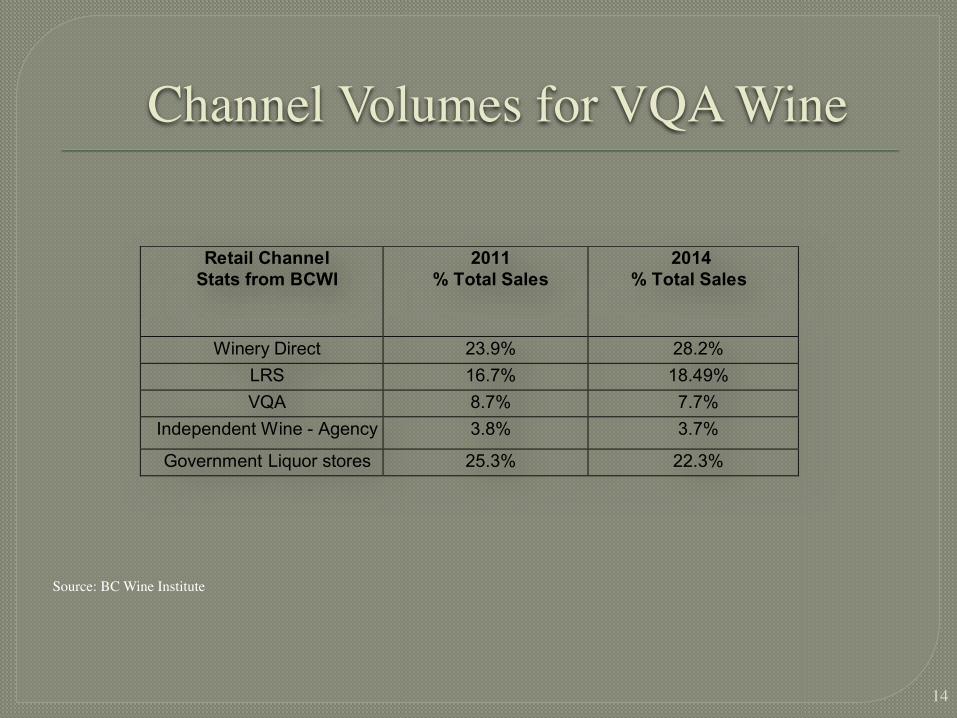

Channel Volumes for VQA Wine!!!!!!!!!!!!!!!!!!!Source: BC Wine Institute

14

Retail Channel Stats from BCWI

2011 % Total Sales

2014 % Total Sales

Winery Direct 23.9% 28.2% LRS 16.7% 18.49% VQA 8.7% 7.7%

Independent Wine - Agency 3.8% 3.7% Government Liquor stores 25.3% 22.3%

15

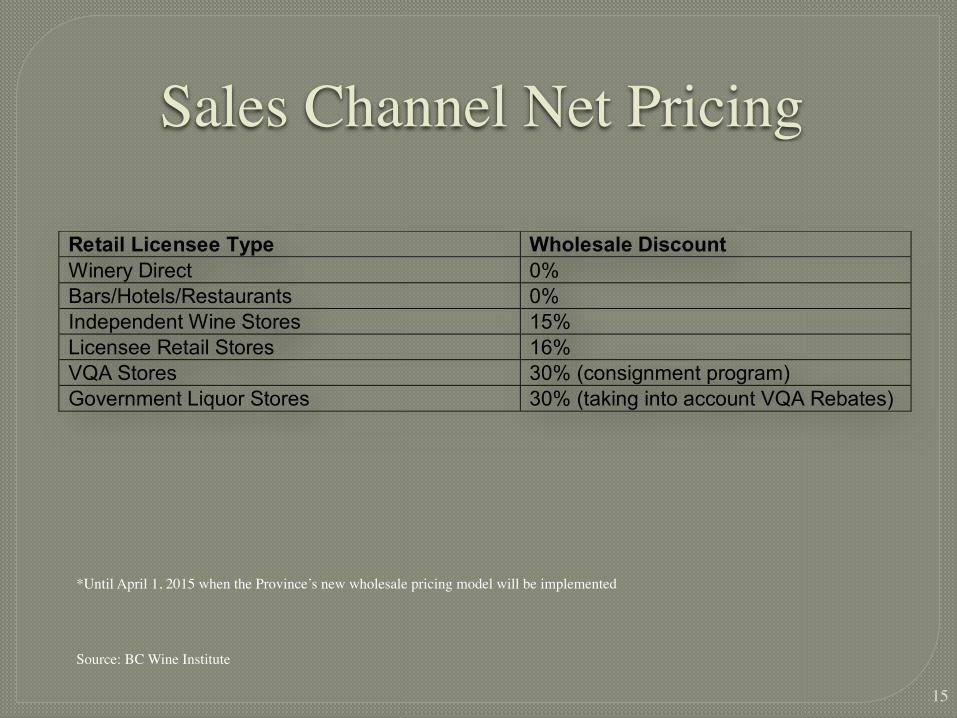

Sales Channel Net Pricing

Retail Licensee Type Wholesale Discount Winery Direct 0% Bars/Hotels/Restaurants 0% Independent Wine Stores 15% Licensee Retail Stores 16% VQA Stores 30% (consignment program) Government Liquor Stores 30% (taking into account VQA Rebates)

Source: BC Wine Institute

*Until April 1, 2015 when the Province’s new wholesale pricing model will be implemented

Making a Big Red- BC Boutique Winery -

• RETAIL PRICE $35.71 !

!!!

• PROFIT $11.96 • If selling through mainly ‘direct’ channels !• GST/PST – 12% $4.29

• Selling Costs $5.43

• Indirect Costs $6.17• Direct Costs $10.44

16

Making a White- BC Boutique Winery -

• RETAIL PRICE $19.64 !

!!!

• PROFIT $1.36 • Only if selling in mainly ‘direct’ channels • GST/PST – 12% $2.36 • Selling Costs $3.93 • Indirect Costs $6.79• Direct Costs $6.62

17

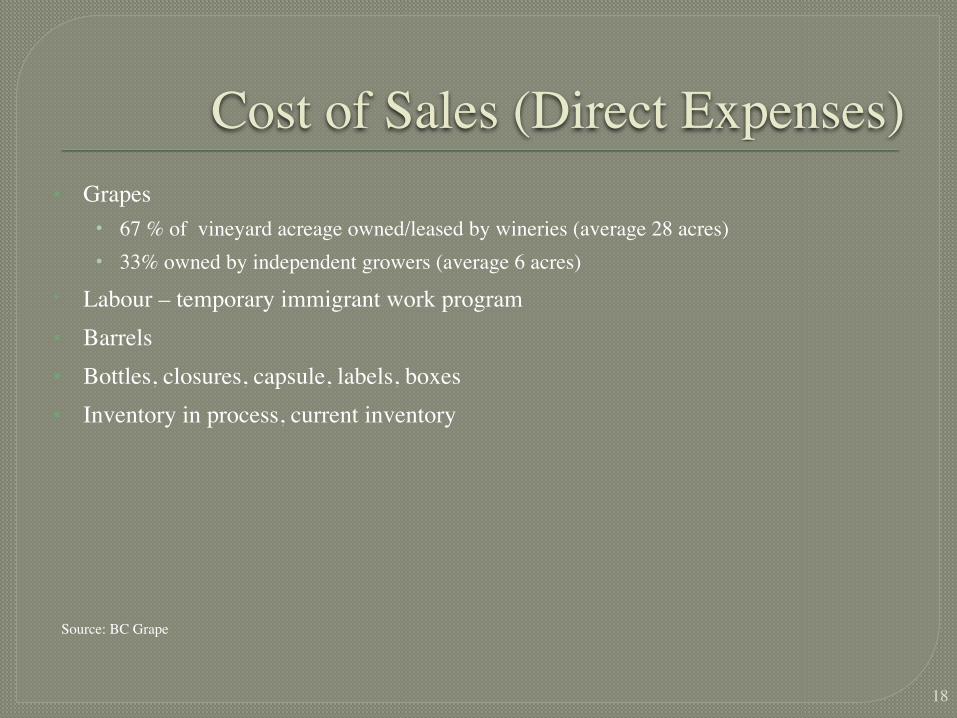

Cost of Sales (Direct Expenses)▪ Grapes

• 67 % of vineyard acreage owned/leased by wineries (average 28 acres) • 33% owned by independent growers (average 6 acres)

• Labour – temporary immigrant work program ▪ Barrels ▪ Bottles, closures, capsule, labels, boxes ▪ Inventory in process, current inventory

18

Source: BC Grape

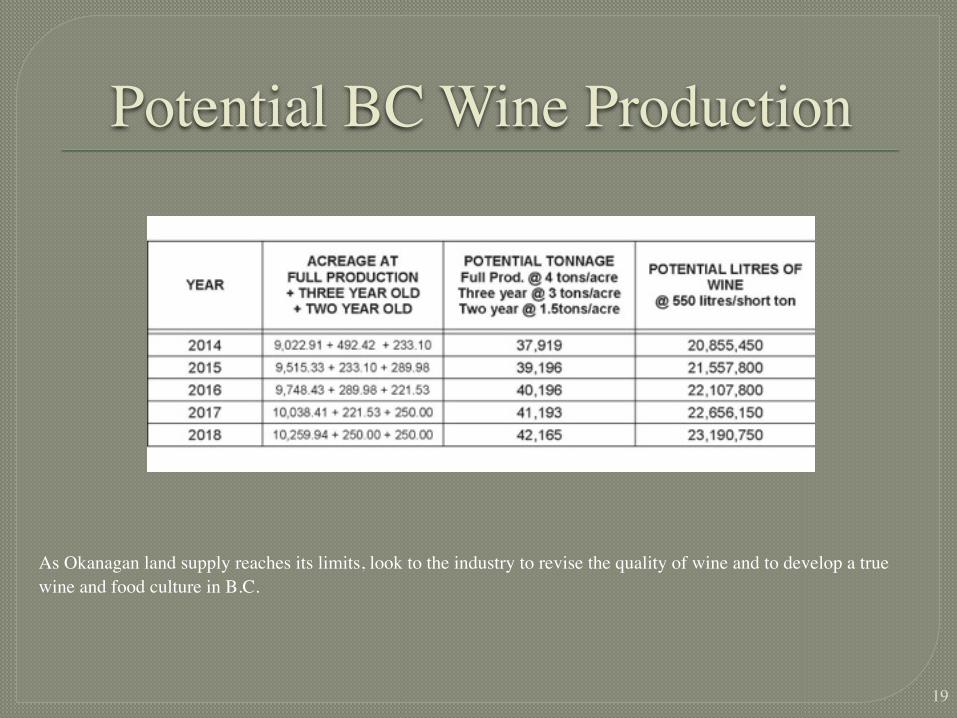

Potential BC Wine Production!!!!!!!!!!!!As Okanagan land supply reaches its limits, look to the industry to revise the quality of wine and to develop a true wine and food culture in B.C.

19

20Source: The Wine Industry Symposium Group

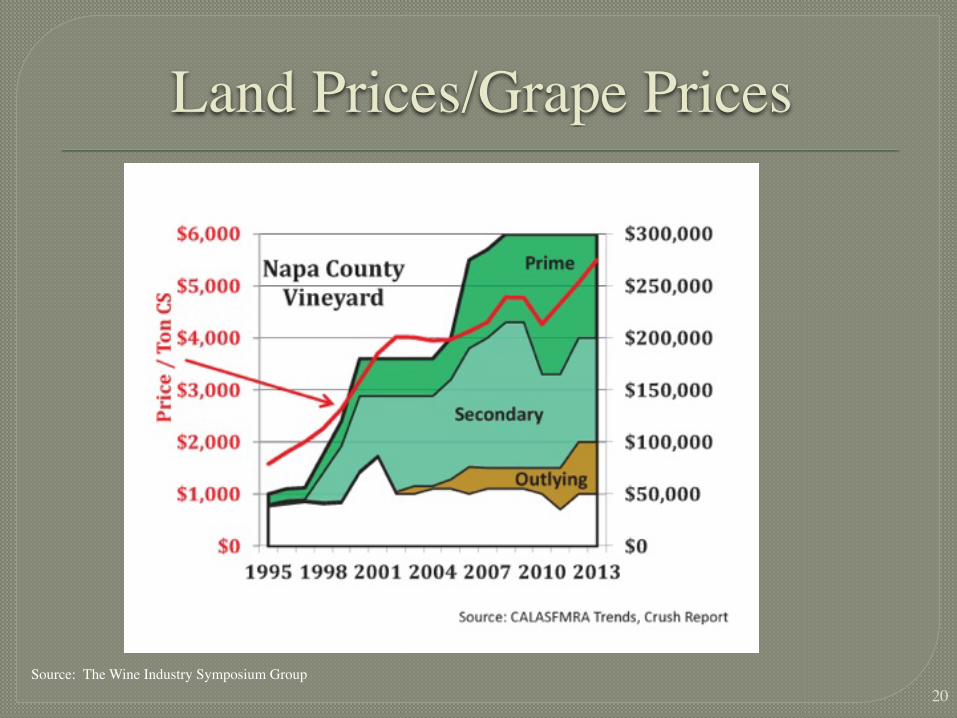

Land Prices/Grape Prices

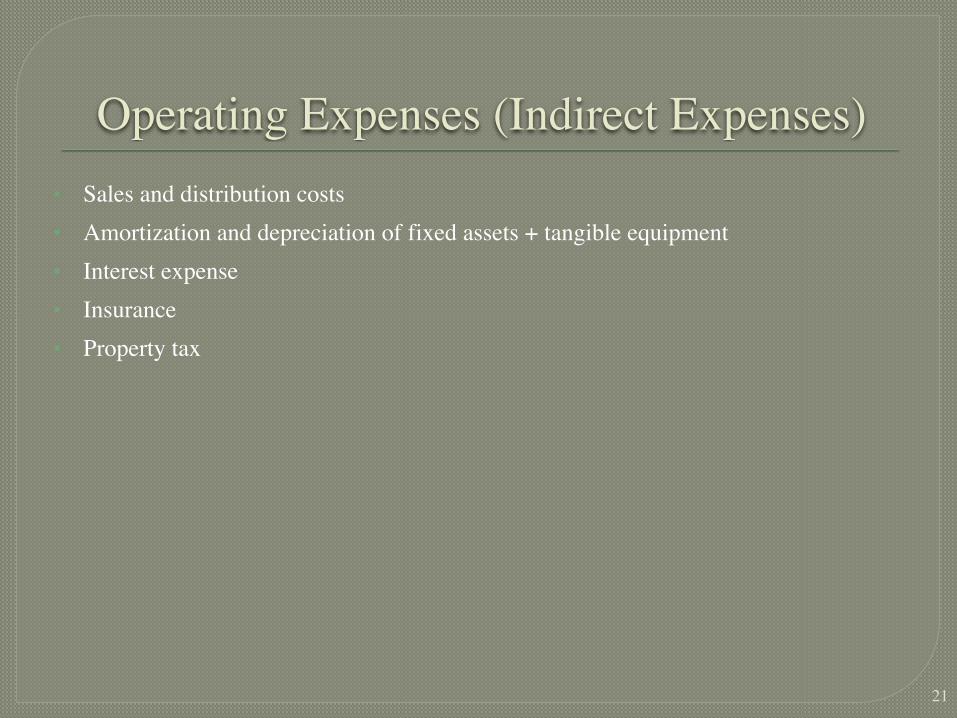

Operating Expenses (Indirect Expenses)▪ Sales and distribution costs ▪ Amortization and depreciation of fixed assets + tangible equipment ▪ Interest expense ▪ Insurance ▪ Property tax

21

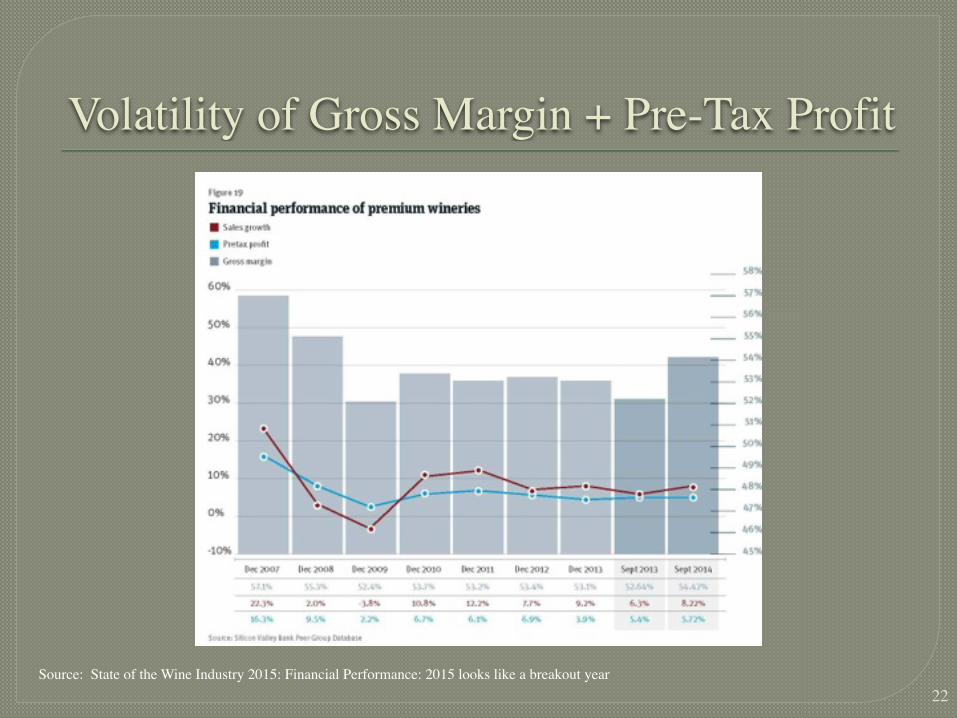

Volatility of Gross Margin + Pre-Tax Profit

22Source: State of the Wine Industry 2015: Financial Performance: 2015 looks like a breakout year

Risk Factors

23

• Agricultural risks • Long manufacturing cycle • Industry consolidation (resulting in larger competitors within increased scale and

resources – impact on margins and customer retention) • Changing consumer preferences • Regulatory changes • Trade challenge by California or European producers

Exit AlternativesA successful exit is the single largest contributor to return on investment 1. Strategic buyer – portfolio building, geographic expansion, leverage existing

infrastructure 2. Financial buyer – DCF + terminal value - winery value negatively impacted by

relatively low year to year earnings up front, but dominated by amount and timing of the terminal or exit value

3. Romantic buyer – intangible lifestyle benefits

24

Exit Valuation▪ Values run the gamut from one of a kind to commodity ▪ Value builds in growth in value of unique vineyards and brands ▪ A non-descript brand without a compelling story will probably garner no more than

value of the vineyard property + tangible equipment (deferred maintenance and profitability issues) – landscape littered with meaningless and storyless brands

▪ Restate financial statements to exclude family expenses; provide transitional support (consulting role)

25

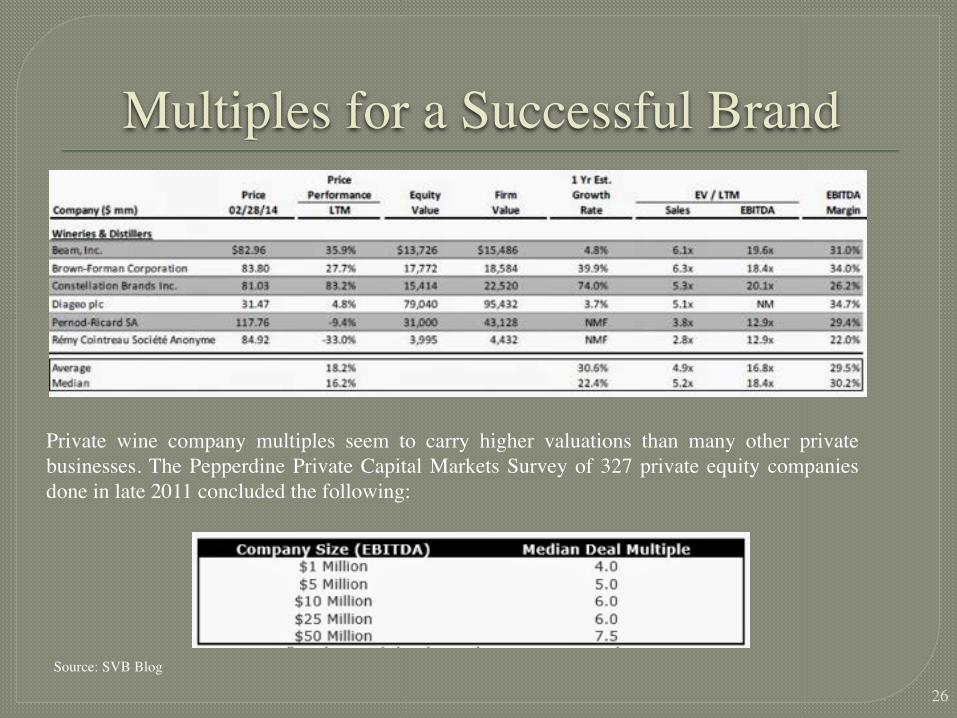

Multiples for a Successful Brand

26

!Private wine company multiples seem to carry higher valuations than many other private businesses. The Pepperdine Private Capital Markets Survey of 327 private equity companies done in late 2011 concluded the following:

Source: SVB Blog

How to Make Money in the Winery Industry▪ Focus on drawing profitable volume through sales channels appropriate for price

point and business model ▪ Quality constant grape supply ▪ Carefully manage expenses ▪ Asset and capital structure appropriate to revenue and case volume

27

A Business Plan for the Future● Vertically integrate – forwards and backwards – own your own vineyard, develop your own

distribution (Is a ‘virtual winery’ a viable way to start?) ● Focus marketing on the next generation – Gen X and Millennials – this means social

media marketing ● Focus on premium/super-premium wines – rising land and grape prices will force a

migration towards high quality ● Focus your business model on price appreciation rather than volume growth –

maintaining super premium quality requires meticulous focus on every detail – mitigates against growing beyond a small to mid-sized winery

● Focus on Varietals best suited to the Valley – will sub-appellations (or bench specific marketing groups) be a significant factor in the future

● Be sure you are well capitalized from the outset - you need to build up front to the size you intend to grow; you will achieve positive accounting net income before you become cash flow positive

● Focus on a business plan synergistic with the coming to age of the Okanagan Valley – increasingly it is a major internationally prominent ‘local food and wine’ tourist destination

28

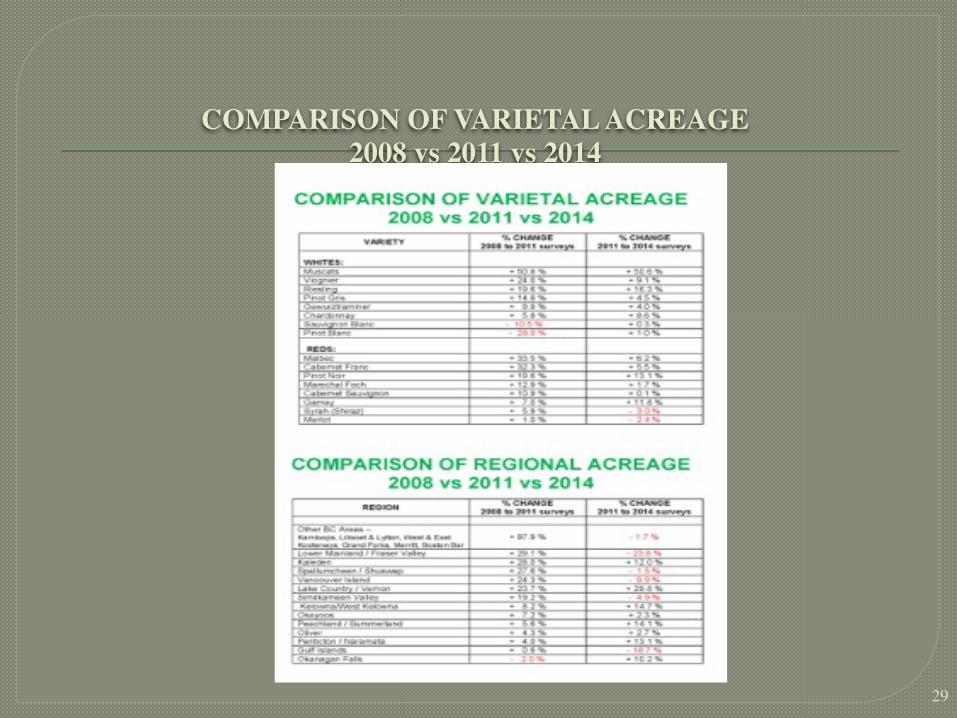

COMPARISON OF VARIETAL ACREAGE 2008 vs 2011 vs 2014

29