vanistendael slides

DESCRIPTION

ANTI-ABUSE MEASURES AND TAX COMPETITION IN THE EUTRANSCRIPT

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

ANTI-ABUSE MEASURES AND TAX COMPETITION IN THE EU

Prof. Frans Vanistendael

Academic Chairman

International Bureau of Fiscal Documentation

Director European Tax College

Oxford, 4 October, 2008

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

Cadbury Schweppes: facts

CS, a U.K. resident company, is the parent

company of the CS group, which consists of

companies in the U.K., in other Member States and

in third countries. The group includes two

subsidiaries: Cadbury Schweppes Treasury

Services (CSTS) and Cadbury Schweppes Treasury

International (CSTI), established in the International

Financial Services Centre in Dublin and subject to a

tax rate of 10%. Both companies are used to raise

finance for subsidiaries in the CS group.

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

CS: the basic questions

Is the establishment of a subsidiary in

another Member State for the purpose of

enjoying a more favourable tax regime an

abuse of the right of establishment?

Does the U.K. CFC legislation hinder the

exercise of the freedom of establishment?

Is the hindrance justified?

(opinion a.g. nr. 38)

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

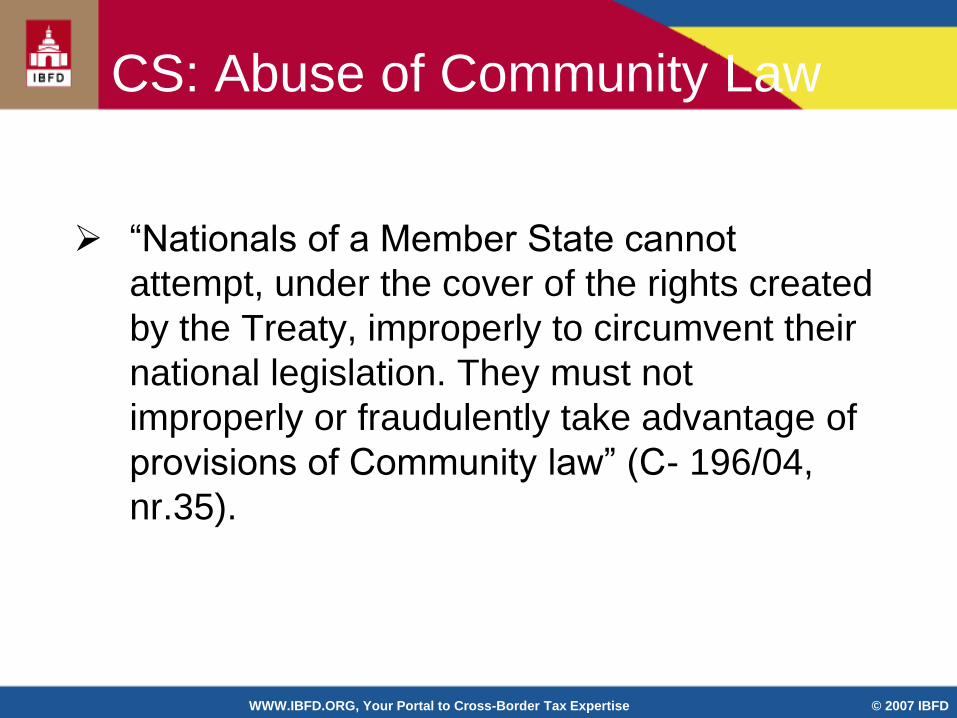

CS: Abuse of Community Law

“Nationals of a Member State cannot

attempt, under the cover of the rights created

by the Treaty, improperly to circumvent their

national legislation. They must not

improperly or fraudulently take advantage of

provisions of Community law” (C- 196/04,

nr.35).

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

CS: Moving is not abuse

… “As to the freedom of establishment … the fact

that the company was established in a Member state

for the purpose of benefiting from more favourable

legislation does not in itself … constitute abuse of

that freedom” (C-196/04, nr. 37)

“The fact that in this case CS decided to establish

CSTS and CSTI in the IFSC for the avowed purpose

of benefiting from the favourable tax regime does

not in itself constitute abuse” (C- 196/04, nr. 38)

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

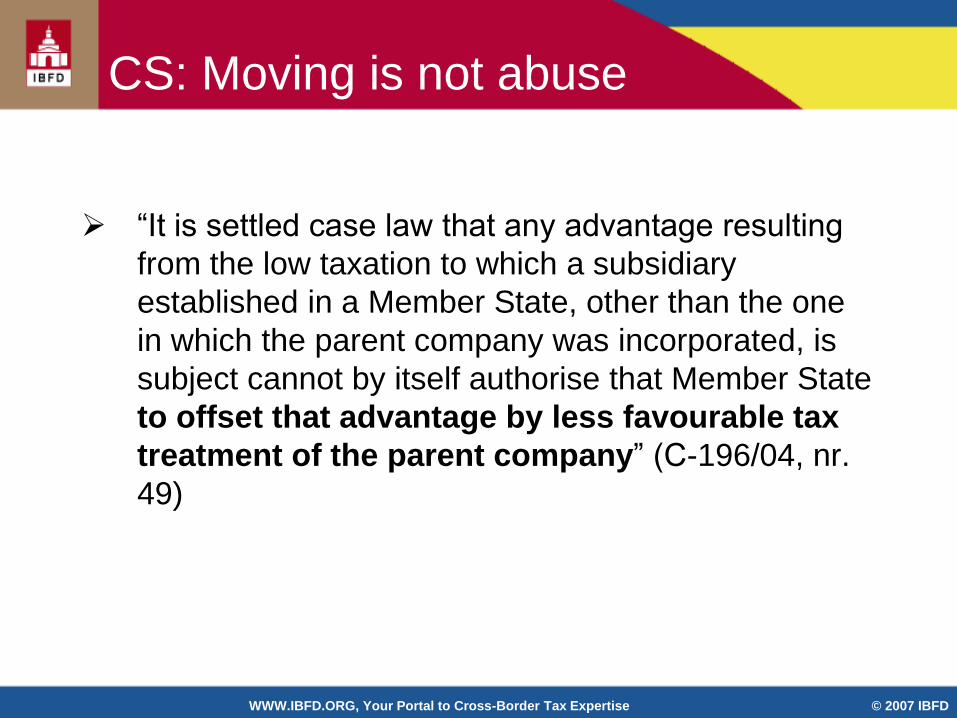

CS: Moving is not abuse

“It is settled case law that any advantage resulting

from the low taxation to which a subsidiary

established in a Member State, other than the one

in which the parent company was incorporated, is

subject cannot by itself authorise that Member State

to offset that advantage by less favourable tax

treatment of the parent company” (C-196/04, nr.

49)

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

CS: Moving is not abuse

“The mere fact that a resident company establishes a

secondary establishment … in another Member

State cannot set up a general presumption of tax

evasion and justify measures which compromise the

exercise of a fundamental freedom guaranteed by

the Treaty” (C-196/04, nr. 50)

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

CS: Is there a barrier?

“Even if the legislation at issue were tax neutral

compared to a purely domestic situation … that

would not call into question the existence of unequal

treatment and the disadvantage to Cadbury in

comparison with …a resident company which has

established a subsidiary in another Member State

which has a less favourable tax regime than that in

effect in the IFSC” (opinion nr. 77)

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

CS: Is there a barrier?

“ discrimination is defined as the application of different rules to comparable situations or the application of the same rule to different situations. The only question to be asked … is therefore whether those two situations are comparable. I take the view that that is the case in respect of Cadbury’s position and that of a resident company which has established a subsidiary in another Member State having a less favourable tax regime than that in effect in the IFSC”(opinion nr. 78)

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

CS: Is there a barrier?

“It is submitted that the disparity in the rates of

corporation tax in effect within the Union constitutes

an objective difference in situation justifying

…differentiated treatment” (opinion nr. 79)

“That would be tantamount to conceding that a

Member State is entitled, without infringing the rules

of the Treaty, to choose the other Member States in

which its domestic companies may establish

subsidiaries.. Such a situation would manifestly lead

to a result contrary to the very notion of single

market” (opinion nr. 80)

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

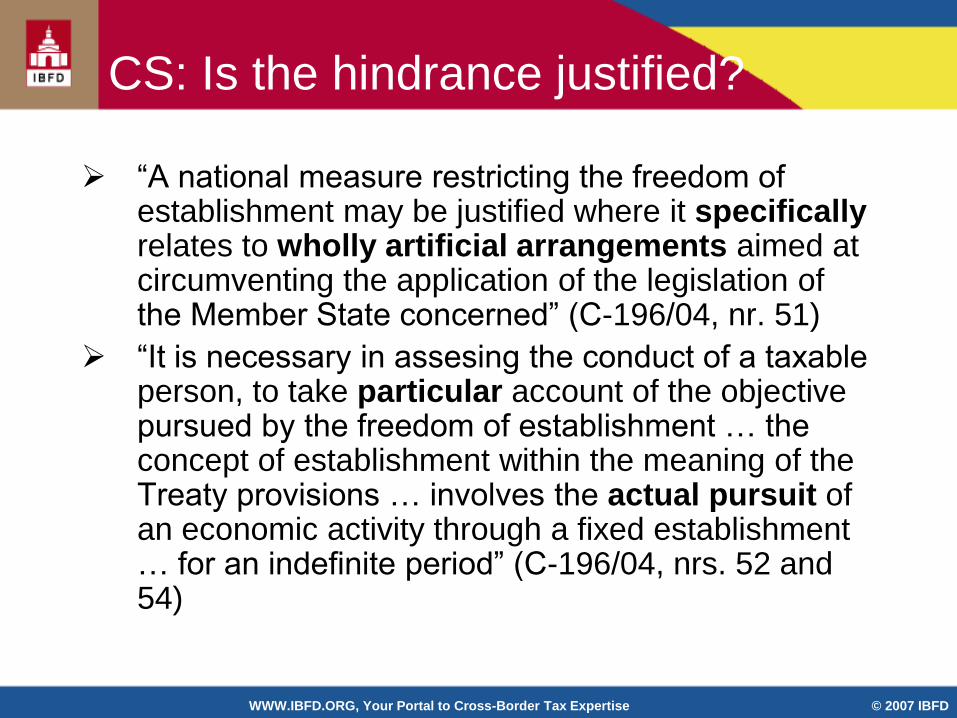

CS: Is the hindrance justified?

“A national measure restricting the freedom of establishment may be justified where it specifically relates to wholly artificial arrangements aimed at circumventing the application of the legislation of the Member State concerned” (C-196/04, nr. 51)

“It is necessary in assesing the conduct of a taxable person, to take particular account of the objective pursued by the freedom of establishment … the concept of establishment within the meaning of the Treaty provisions … involves the actual pursuit of an economic activity through a fixed establishment … for an indefinite period” (C-196/04, nrs. 52 and 54)

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

CS: Is the hindrance justified?

“It follows that, in order for a restriction on the freedom of establishment to be justified on the ground of prevention of abusive practices, the specific objective of such a restriction must be to prevent conduct involving the creation of wholly artificial arrangements which do not reflect economic reality” (C-196/04, nr. 55)

It must be determined whether the restrictions on freedom of establishment arising from the legislation on CFCs may be justified on the ground of prevention of wholly artifical arrangements and if so, whether it is porportionate in relation to its objective” (C-196/04, nr. 57)

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

Cadbury Conclusions

Exercising the right of secondary establishment to take advantage of a lower tax regime in another Member State does not constitute in it self an abuse.

The EC Treaty permits Member States to take action preventing abuse in circumventing national tax legislation.

An establishment in another Member State can never be treated as an abuse if it consists of an effective establishment in order to conduct a genuine economic activity.

Therefore within the Treaty framework, anti-abuse legislation must specifically target wholly artificial arrangements.

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

Columbus Container: facts

CC is a limited partnership under Belgian law

CC is owned by 8 German resident individuals, each owning 10% and a German partnership, owning 20%

CC is a Belgian coordination centre providing financial services for a multinational group and is subject to corporate tax at a preferential rate

Partnerships are treated in Germany as transparent entities, profits are taxed directly to the individual partners

As an anti-abuse measure Germany replaced the exemption system applicable under the DTA with Belgium with a credit system, thereby increasing considerably the tax burden of the German partners

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

CC: the basic questions

Is the switch-over from exemption to credit as an anti-abuse measure for passive income permitted under the EC Treaty?

“whether freedom of establishment and the free movement of capital preclude a Member State … for the purpose of avoiding double taxation of the income and capital …derived from particular investments in another Member State, from unilaterally replacing the “exemption” method by the “set-off” method (opinion a.g. nr. 4)

whether the decision in Columbus Container nullifies the decision in Cadbury Schweppes.

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

CC: different classificartion allowed

“it is not the difference between… Germany and … Belgium in respect of the legal and fiscal classification of Columbus which the referring court regards as involving a possible restriction on the freedoms of movement under the Treaty, but merely the replacement of the exemption method by the set-off method as regards taxation of the income … of a permanent establishment located abroad” (opinion, nr. 38).

“At the current state of development of Community law, it does not require Member States to recognise … the legal and tax status afforded by the domestic law of the other Member States to entities which carry out their economic activites there” (nr. 41).

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

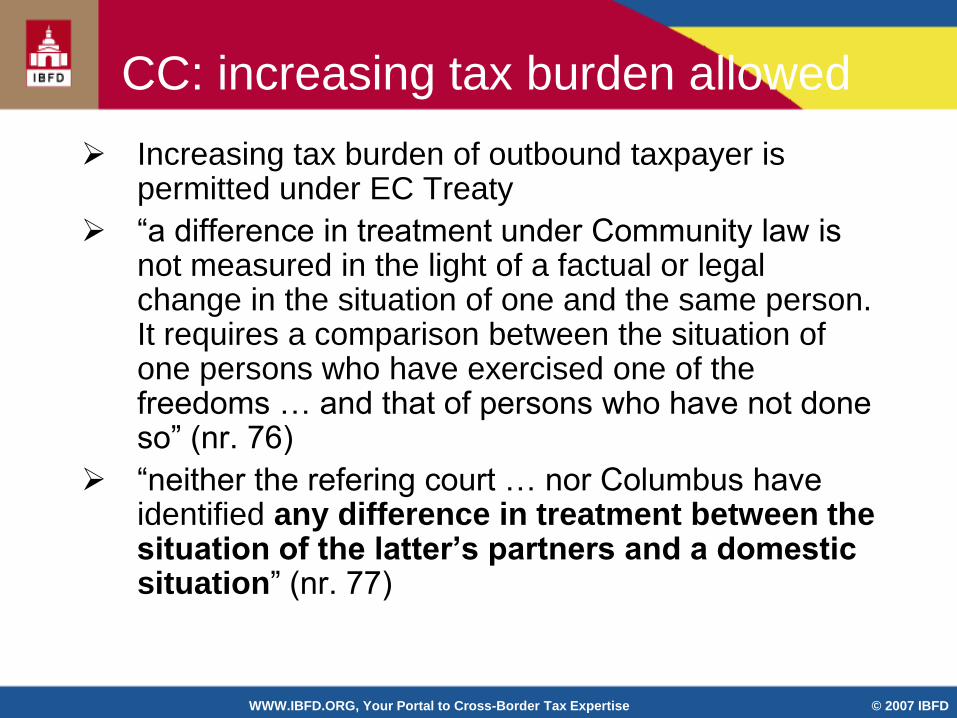

CC: increasing tax burden allowed

Increasing tax burden of outbound taxpayer is permitted under EC Treaty

“a difference in treatment under Community law is not measured in the light of a factual or legal change in the situation of one and the same person. It requires a comparison between the situation of one persons who have exercised one of the freedoms … and that of persons who have not done so” (nr. 76)

“neither the refering court … nor Columbus have identified any difference in treatment between the situation of the latter’s partners and a domestic situation” (nr. 77)

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

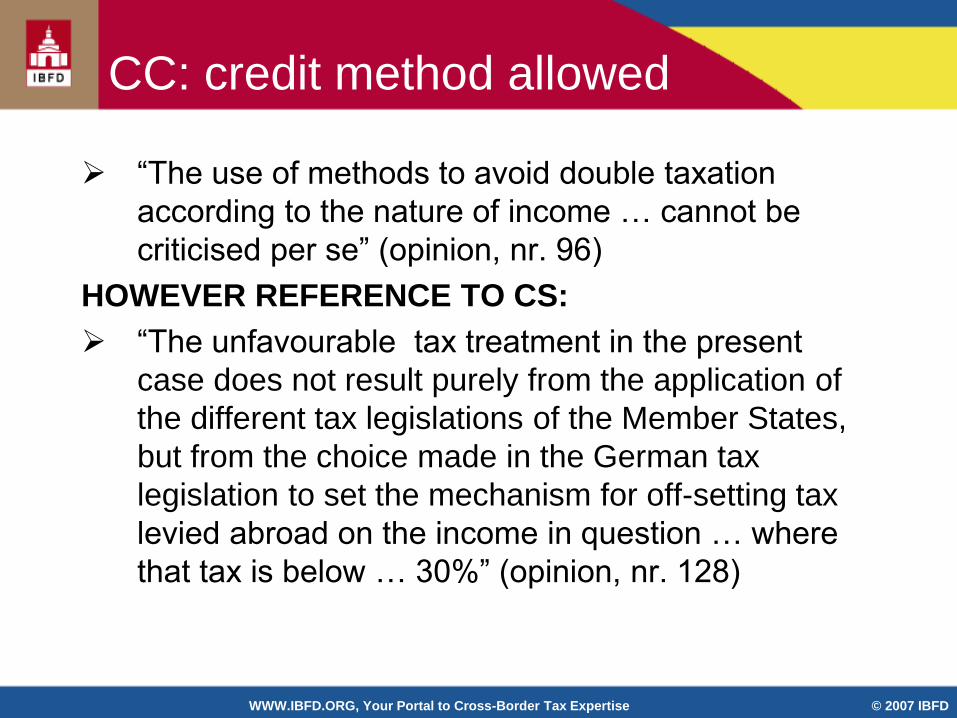

CC: credit method allowed

“The use of methods to avoid double taxation

according to the nature of income … cannot be

criticised per se” (opinion, nr. 96)

HOWEVER REFERENCE TO CS:

“The unfavourable tax treatment in the present

case does not result purely from the application of

the different tax legislations of the Member States,

but from the choice made in the German tax

legislation to set the mechanism for off-setting tax

levied abroad on the income in question … where

that tax is below … 30%” (opinion, nr. 128)

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

CC: reference to CS

“a Member State of residence cannot restrict the

freedom of establishment of its nationals to part of

the common market … Thus the obligation on the

… State of residence … is to ensure, in addition to

respect for equal treatment among its residents as

regards whether they have or have not exercised

their freedom of movement, that they are not

deterred from establishing themselves in the

Member State of their choice, inter alia by means of

tax measures” (opinion nr. 133)

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

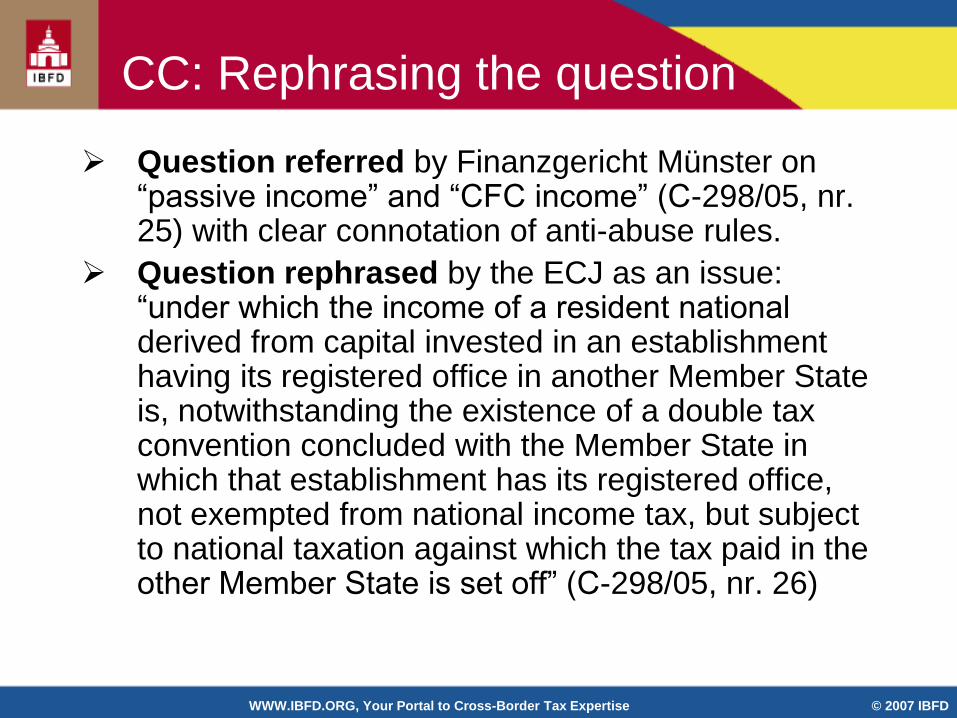

CC: Rephrasing the question

Question referred by Finanzgericht Münster on “passive income” and “CFC income” (C-298/05, nr. 25) with clear connotation of anti-abuse rules.

Question rephrased by the ECJ as an issue: “under which the income of a resident national derived from capital invested in an establishment having its registered office in another Member State is, notwithstanding the existence of a double tax convention concluded with the Member State in which that establishment has its registered office, not exempted from national income tax, but subject to national taxation against which the tax paid in the other Member State is set off” (C-298/05, nr. 26)

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

CC: decision: no disadvantage

“It is not contested that the German tax legislation in issue … which is comparable to the Belgian tax legislation that applied in Case C-513/04 Kerckhaert and Morres … does not make any distinction between taxation of income derived from the profits of partnerships in Germany and … partnerships in another Member State, which subjects the profits made by those partnerships … to a rate of tax below 30%” (C-298/05, nr. 39).

“Since partnerships such as Columbus do not suffer any tax disadvantage in comparison with partnerships established in Germany there is no discrimination” (C-298/05, nr. 40)

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

CC: parallel fiscal sovereignty

“the adverse consequences which might arise from

the application of the system for the taxation of

profits such as that put in place by the AstG result

from the exercise in parallel by two Member States

of their fiscal sovereignty (Kerkckhaert-Morres)”

“In this respect double taxation conventions such as

those envisaged by Article 293 are designed to

eliminate or mitigate the negative effects on the

functioning of the internal market resulting from

the coexistence of national tax systems” (nrs. 43-

44)

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

Columbus: conclusions

Parallel exercise of fiscal sovereignty is allowed

Selective choice of credit system next to exemption system is exercise of fiscal sovereignty

Credit system is not a disadvantage for outbound investments and therefore no discrimination

No discussion on issue of fragmentation of the internal market

No discussion of abuse as a wholly artificial arrangement

Conclusion: parallel case law, no nullification of Cadbury Schweppes

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

Why discuss VAT cases?

The doctrine of “Abuse of Community law” is part of

a wider non-tax doctrine (33/74, van Binsbergen v

Bestuur van de Bedrijfsvereniging voor de

Metaalnijverheid)

In Halifax the principle of the applicability of abuse

of Community rights was specifically discussed and

decided (C-255/02, nrs. 69 and 70)

Halifax and Cadbury Schweppes, one European

theory of abuse of tax law? (EC Tax Review,

2006/4, pp. 192-195

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

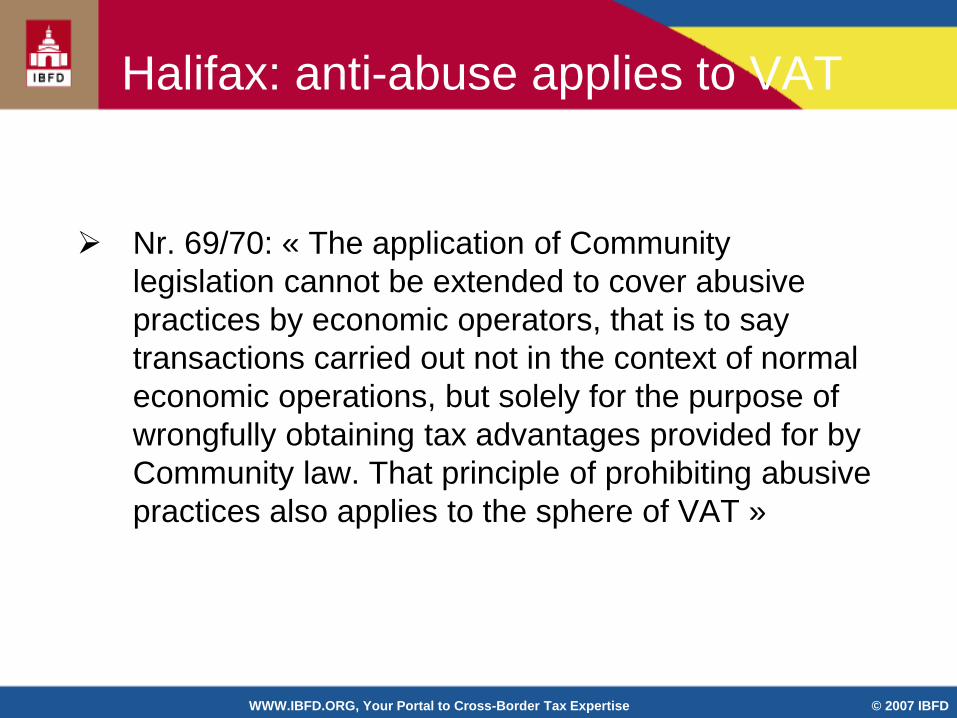

Halifax: anti-abuse applies to VAT

Nr. 69/70: « The application of Community

legislation cannot be extended to cover abusive

practices by economic operators, that is to say

transactions carried out not in the context of normal

economic operations, but solely for the purpose of

wrongfully obtaining tax advantages provided for by

Community law. That principle of prohibiting abusive

practices also applies to the sphere of VAT »

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

Halifax: principle of interpretation

Opinion AG nr. 69: « … this notion of abuse

operates as a principle governing the

interpretation of Community law… »

Opinion AG nr. 79: « The result of its application is

that the legal provision interpreted cannot be

regarded as conferring the right at issue because

the right claimed is manifestly beyond the aims and

objectives pursued by the provision abusively relied

upon »

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

Halifax: principle of intrepretation

Opinion AG nr. 89: « The prohibition of abuse as a

principle of interpretation, is no longer relevant

where the economic activity carried out may

have some explanation other than the mere

attainment of tax advantages … In such

circumstances, to interpret a legal provision as not

conferring such an advantage on the basis of an

unwritten general principle would grant an

excessively broad discretion to the tax

authorities in deciding which of the purposes of a

given transaction ought to be considered as

predominant ».

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

Halifax: wider national provision

Opinion AG nr. 90: « There can be little doubt that

the possibility must be recognised that also in such

cases, where activities are accounted for by a

mixture of tax and non-tax considerations,

further restrictions could be introduced for claims

arising from activities, which, to varying extents,

predominantly seek to achieve tax advantages. This

however, will require the adoption of appropriate

national legislative measures. Mere

interpretation will not suffice ».

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

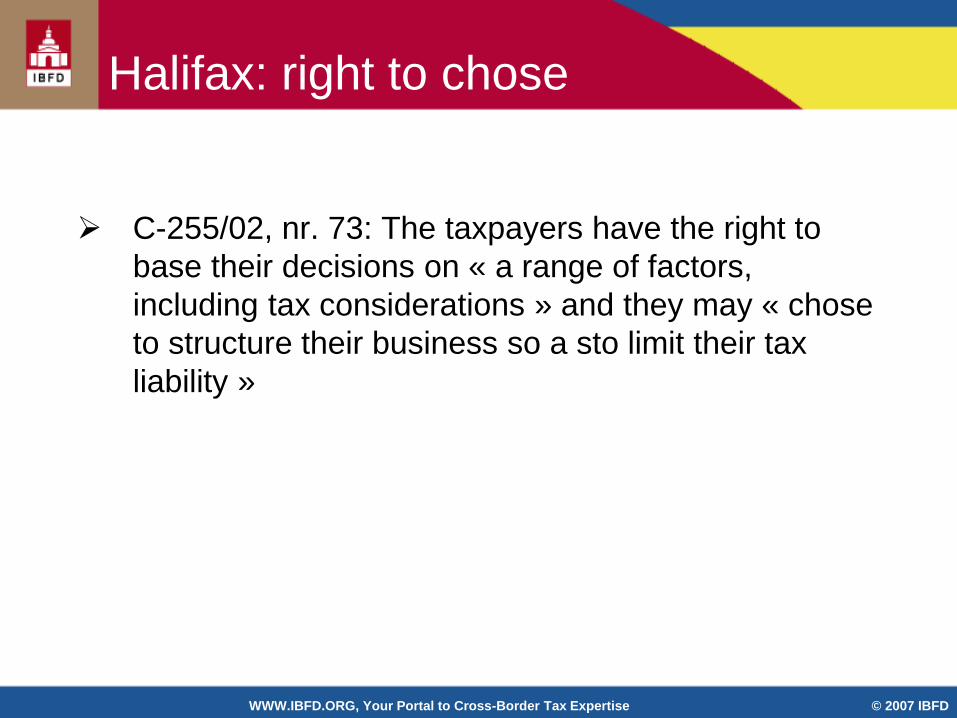

Halifax: right to chose

C-255/02, nr. 73: The taxpayers have the right to

base their decisions on « a range of factors,

including tax considerations » and they may « chose

to structure their business so a sto limit their tax

liability »

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

Halifax: defining abuse

Nrs. 74/75: «… in the sphere of VAT, an abusive

practice can be found to exist only if first, the

transactions concerned, notwithstanding formal

application of the conditions laid down by the

relevant provisions of the Sixth Directive and the

national legislation…, result in the accrual of a tax

advantage the grant of which would be contrary to

the purpose of those provisions. Second it must be

apparent from a number of objective factors that the

essential aim of the transaction concerned is to

obtain a tax advantage. As the A.G. observed, the

prohibition of abuse is not relevant, where the

economic activity…may have some other

explanation than the attainment of tax advantages.

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

Halifax: is AG = judgement?

Essential aim = extremely important or fundamental

Sole consideration = the one and only consideration

What is the exact meaning?

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

Part services: principal aim

C-425/06 nr. 40 Rephrasing the preliminary

question: « when the accrual of a tax advantage is

the principal aim of the transaction … or if such

finding can only be made if the accrual of the tax

advantage constitutes the sole aim pursued, to the

exclusion of other economic objectives ».

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

Part services: principal aim

Nr. 45 : « … the Sixth Directive must be intrepreted

as meaning that there can be a finding of an abusive

practice when the accrual of a tax advantage

constitutes the principal aim of the transaction or

transactions at issue ».

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

Part services: principal aim

Nr. 62: « … the national court, in the assessment

which it must carry out, may take account of the

purely artifical nature of the transactions and the

links of a legal, economic and /or personal nature

between the operators involved …, those aspects

being such as to demonstrate that the accrual of a

tax advantage constitutes the principal aim

pursued, notwithstanding the possible

existence, in addition of economic objectives

arising from, for example marketing,

organization or guarantee considerations ».

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

Leur-Bloem: abuse in directives

C-28/95 nr. 48 (b): « … in determining whether the

planned operation has as its principal objectives

tax evasion or tax avoidance, the competent

national authorities must carry out a general

examination of the operation in each particular case

… Member States may stipulate that the fact that

the planned operation is not carried out for valid

commercial reasons constitutes a presumption of

tax evasion or avoidance … However the laying

down of a general rule automatically excluding

certain categories of operations from the tax

advantage, on the basis of criteria such as those

mentioned … under (a) would go further than is

necessary ».

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

Kofoed: abuse in directives

C-321/05, nr. 38: « Article 11(1)(a) Directive 90/343

(anti-abuse article) reflects the general Community

principle that abuse of rights is prohibited ».

Nr. 40: « it is necessary … to determine whether, in

the absence of a specific transposition provision,

transposing Article 11(1)(a) … that provision may

nevertheless apply … ».

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

Kofoed: abuse in directives

Nr. 44: « Provided that the legal situation arising

from the national transposition measures is

sufficiently … clear and the persons concerned are

put in a position to know the full extent of their rights

and obligations, transposition of the directive into

national law does not necessarily require

legislative action of each Member State ».

Nr. 44: « … the transposition of a directive may,

depending on its content, be achieved through a

general legal context, so that formal and express

re-enactment of the provisions of the directive in

specific national provisions is not necessary ».

© 2007 IBFD WWW.IBFD.ORG, Your Portal to Cross-Border Tax Expertise

More than one abuse concept?

Is it possible to have more than one abuse concept

under Community law?

For the exercise of the fundamental freedoms a

strict abuse concept can be used

For secondary tax legislation a wider abuse concept

could be used giving the national tax administration

more leeway, or should this wider concept be based

on an explicit statutory provision?