veeco instruments inc -...

TRANSCRIPT

VEECO INSTRUMENTS INC

FORM 8-K(Current report filing)

Filed 11/05/07 for the Period Ending 11/05/07

Address TERMINAL DRIVE

PLAINVIEW, NY 11803Telephone 516 677-0200

CIK 0000103145Symbol VECO

SIC Code 3559 - Special Industry Machinery, Not Elsewhere ClassifiedIndustry Semiconductors

Sector TechnologyFiscal Year 12/31

http://www.edgar-online.com© Copyright 2014, EDGAR Online, Inc. All Rights Reserved.

Distribution and use of this document restricted under EDGAR Online, Inc. Terms of Use.

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Date of Report (Date of earliest event reported): November 5, 2007

VEECO INSTRUMENTS INC. ( Exact name of registrant as specified in its charter)

(516) 677-0200

(Registrant’s telephone number, including area code)

Not applicable (Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of

the following provisions (see General Instruction A.2. below):

� Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) � Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) � Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) � Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

Delaware (State or other jurisdiction

of incorporation)

0-16244 (Commission File Number)

11-2989601 (IRS Employer

Identification No.)

100 Sunnyside Boulevard, Suite B, Woodbury, New York 11797 (Address of principal executive offices, including zip code)

Section 7 - Regulation FD Item 7.01 Regulation FD Disclosure.

Veeco Instruments Inc. (“Veeco”) plans to attend certain investor meetings beginning on November 6, 2007. A copy of Veeco’s presentation for these meetings is furnished as Exhibit 99.1 to this report and will be available on Veeco’s website (www.veeco.com) prior to or simultaneously with the first of these meetings. Section 8 - Other Events Item 8.01 Other Events. On November 5, 2007, Veeco Instruments Inc. (“Veeco”) entered into a Memorandum of Understanding to settle and fully resolve the consolidated shareholder derivative action, Edward J. Huneke, et al. v. Edward H. Braun, et al. Case No. 05 MD 1695, pending in the U.S. District Court for the Southern District of New York against individual defendants, including certain current and former members of Veeco's Board of Directors and nominal defendant Veeco Instruments Inc., for a payment of $515,000 and for Veeco's agreement to adopt certain changes to its Corporate Governance Guidelines. Veeco expects that insurance proceeds will cover the settlement amount and any significant legal expenses related to the settlement. The settlement agreement is subject to court approval and would dismiss all pending claims against Veeco and the other defendants with no admission or finding of wrongdoing by Veeco or any of the other defendants, and Veeco and the other defendants would receive a full release of all claims pending in the litigation. To the extent that this report discusses expectations about Veeco’s future financial performance, the settlement of the lawsuit described above or otherwise makes statements about the future, such statements are forward-looking and are subject to a number of risks, uncertainties and other factors that could cause actual results to differ materially from the statements made. These factors include the risk that the court may not approve the settlement agreement with respect to the consolidated derivative action and the other factors discussed in the Business Description and Management’s Discussion and Analysis sections of Veeco’s Annual Report on Form 10-K for the year ended December 31, 2006, subsequent Quarterly Reports on Form 10-Q and current reports on Form 8-K. Veeco does not undertake any obligation to update any forward-looking statements to reflect future events or circumstances after the date of such statements.

The information in this report, including the exhibit, shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of

1934, as amended (the “Exchange Act”), or otherwise subject to the liabilities under that Section, nor shall it be deemed to be incorporated by reference into any filing under the Securities Act of 1933, as amended, or the Exchange Act, except as expressly set forth by specific reference in such a filing.

Section 9 - Financial Statements and Exhibits Item 9.01 Financial Statements and Exhibits. (c) Exhibits .

2

Exhibit Description

99.1

Veeco Instruments Inc. - Investor Presentation dated November 2007.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the

undersigned hereunto duly authorized.

3

VEECO INSTRUMENTS INC.

November 5, 2007 By: /s/ Gregory A. Robbins

Gregory A. Robbins

Senior Vice President and General Counsel

EXHIBIT INDEX

4

Exhibit Description

99.1

Veeco Instruments Inc. - Investor Presentation dated November 2007.

Exhibit 99.1

Veeco Investor Presenta tion November 2007

John Peele r, CEO November 2007

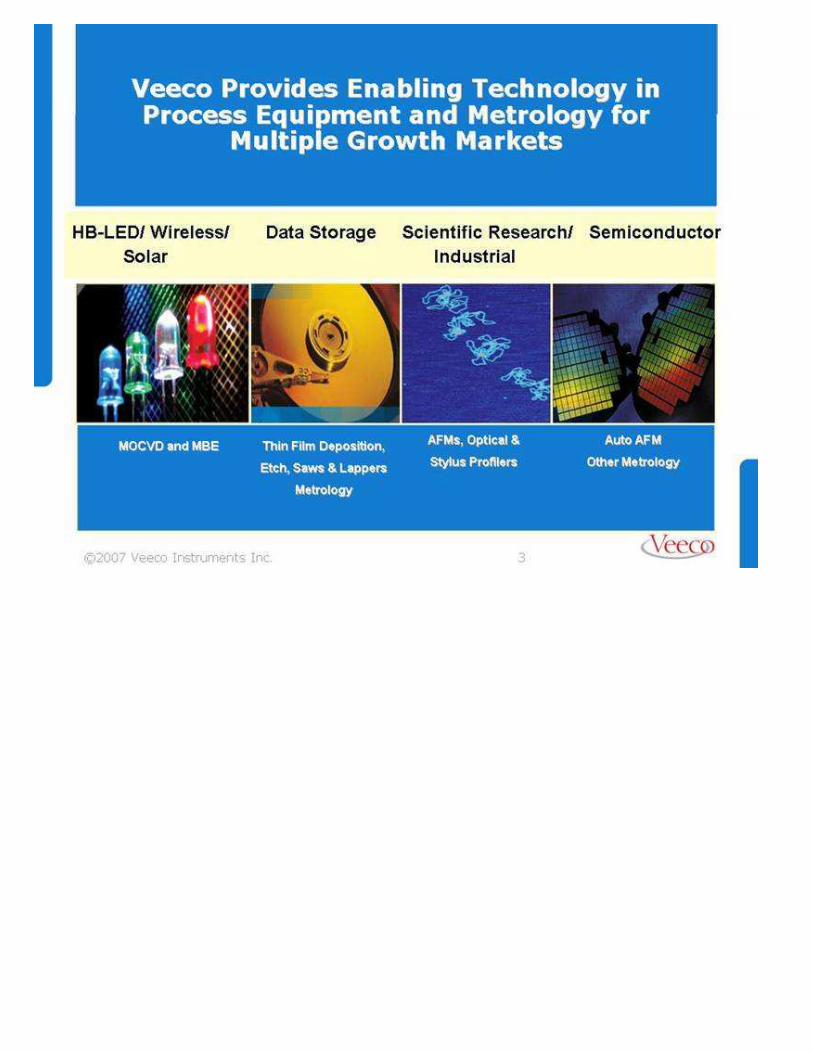

HB-LED/ Wireless/ Da ta Storage Sc ient ific Research/ Semiconduc tor Solar Industr ial Thin Fi lm Deposi tion, Etch, Saws & Lappers Metrol ogy Auto AFM O ther Me trol ogy MOCVD and MB E AFMs, Optical & S tylus Prof ile rs Veeco Provides Enabling Technology i n Process Equipment and Metrol ogy for Mult iple G row th Marke ts

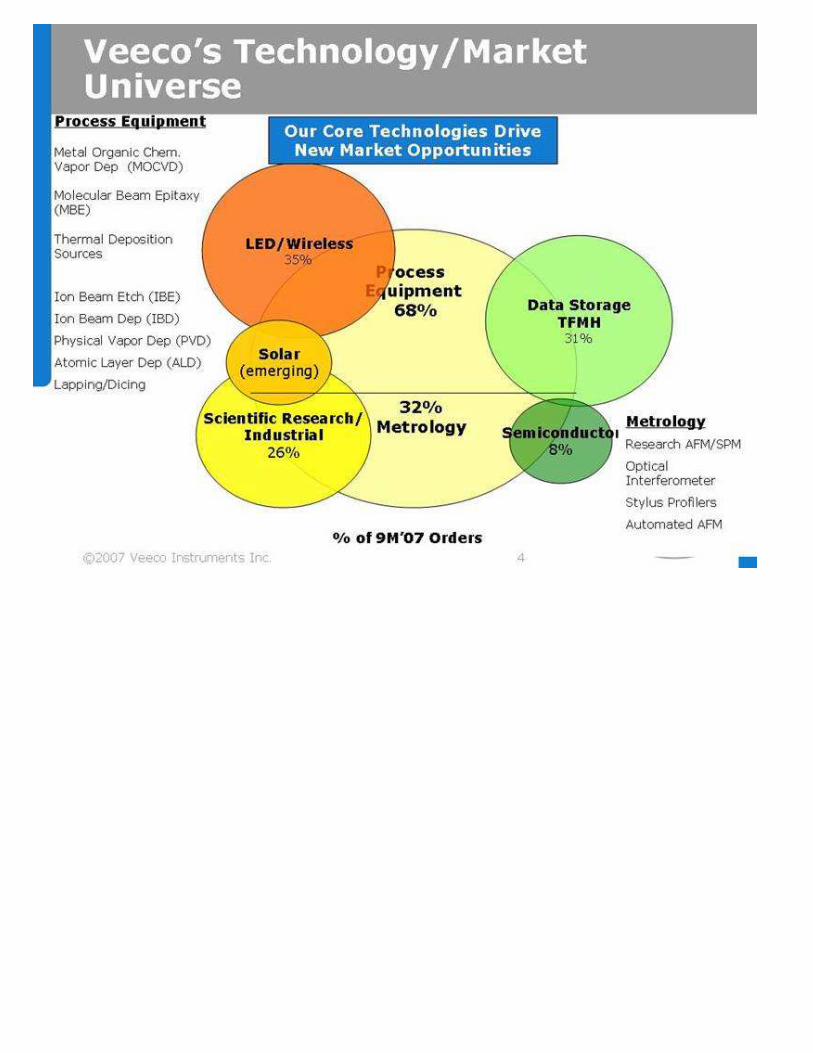

Veeco ’s Technology/Market Universe P rocess Equipment 68% 32% Metrol ogy Data Storage TFMH 31% Semiconduc tor 8% LED/Wireless 35% Scientif ic Research/ Industr ial 26% S olar (emergi ng) Process Equipment Me tal Organic C hem. Vapor Dep (MOCVD) Molecula r Beam Epitaxy (MBE) Therma l Deposi tion Sources Ion B eam Etch (IBE) Ion Beam Dep (IBD) Physical Vapor Dep (P VD) Atomic Layer Dep (ALD) Lappi ng/D ic ing % of 9M ’07 Orders Our Core Technologies Drive New Market Opport unit ies Me trol ogy Research AFM/ SPM Optica l Inte rferomete r St ylus Prof ile rs Automated AFM

We Have Strategi c Rela tionships With G loba l Technology Leaders & Strong Marke t Share Semiconduc tor #1 AFM, Leader Optical HB -LED / Wireless A Leader in MOCVD and MB E S cient ifi c Research #1 Research AF M Data St orage #1 TF MH Equipment THOUSANDS OF CUS TOMERS HDD COMP ANIES WHO MAKE TF MHS SERVING GLOB AL INDUSTRY LEADERS STRONG MARKET SHARE

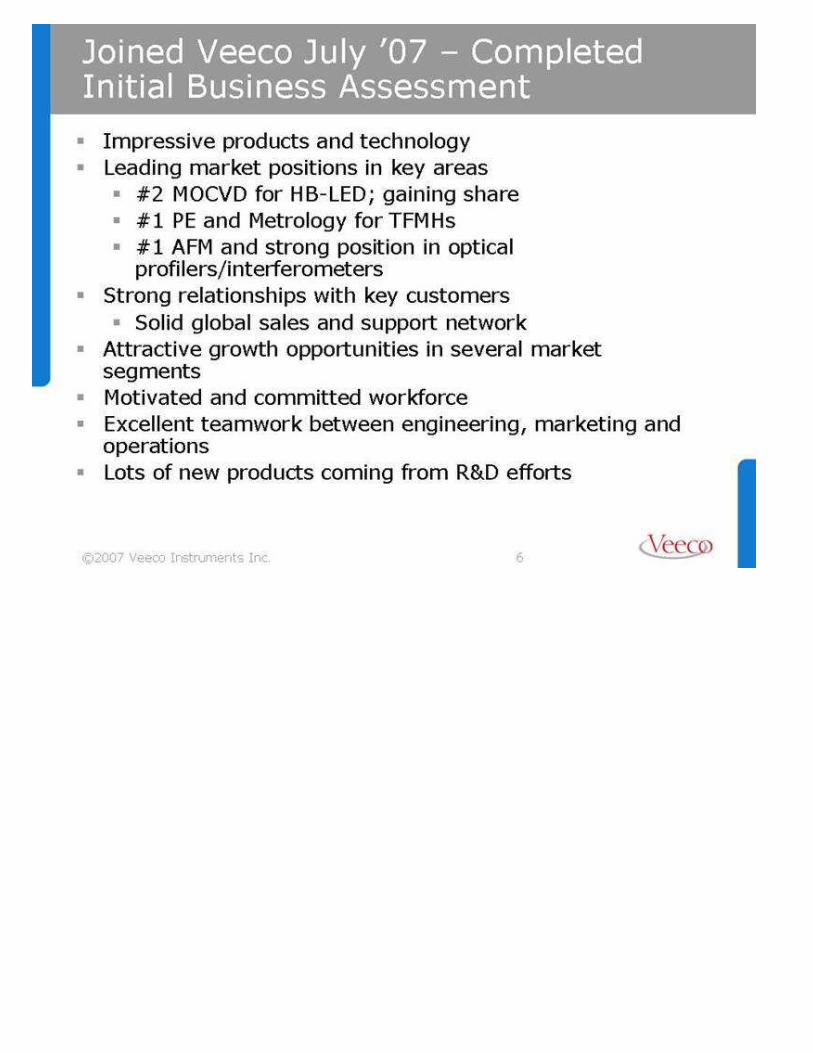

Joi ned Veeco Jul y ’07 – Compl eted Initia l Business Assessment Impressive products and technology Leadi ng marke t positions in key areas #2 MOCVD for HB -LED; gaining share #1 P E and Metrology for TF MHs #1 AF M and strong position in optica l profi lers/inte rferomete rs Strong rela tionships wit h key customers Solid gl oba l sales and support ne twork A ttracti ve growt h opportuni ties in several marke t segment s Moti va ted and committed workforce Exce llent teamwork be tween engineering, marketi ng and opera tions Lots of new products coming from R &D e fforts

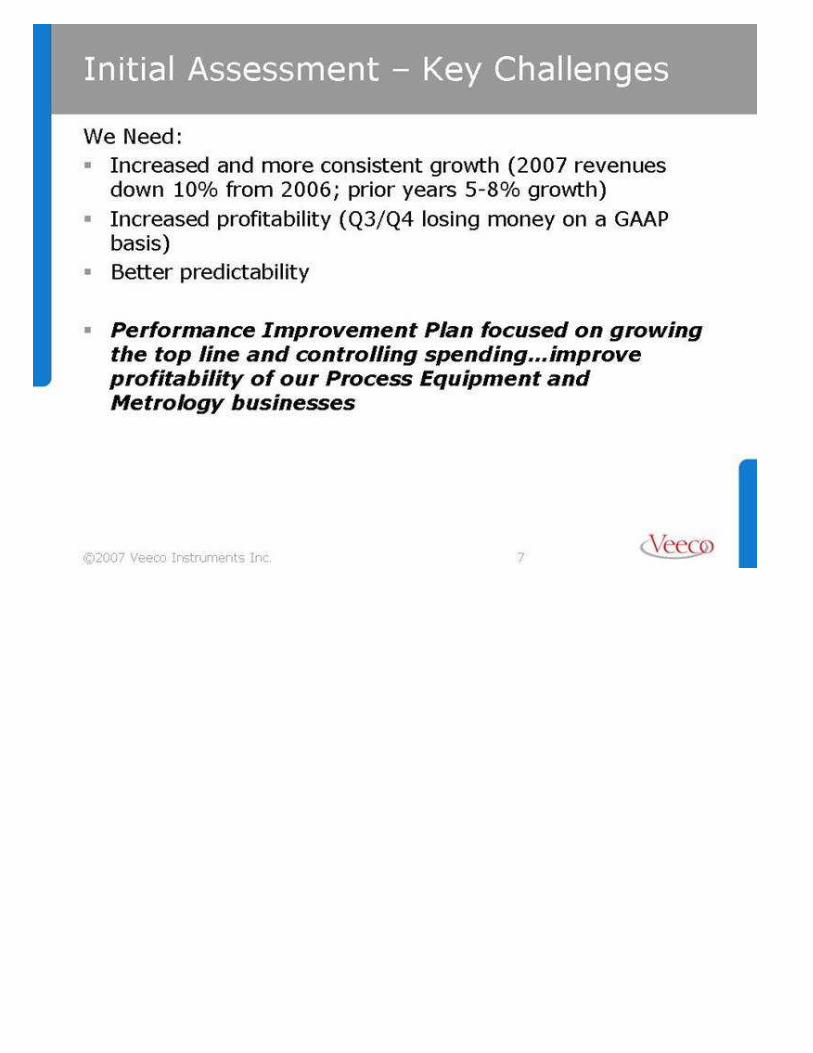

Initia l Assessment – Key C ha llenges We Need: Inc reased and more consistent growt h (2007 revenues down 10% from 2006; pr ior years 5 -8% grow th) Increased profi tabilit y (Q3/Q4 losing money on a GAAP basis) Bett er predic tabil ity Performance Improvement Pl an focused on growing the top line and controll ing spending...improve profi tabilit y of our Process Equipment and Metrology businesses

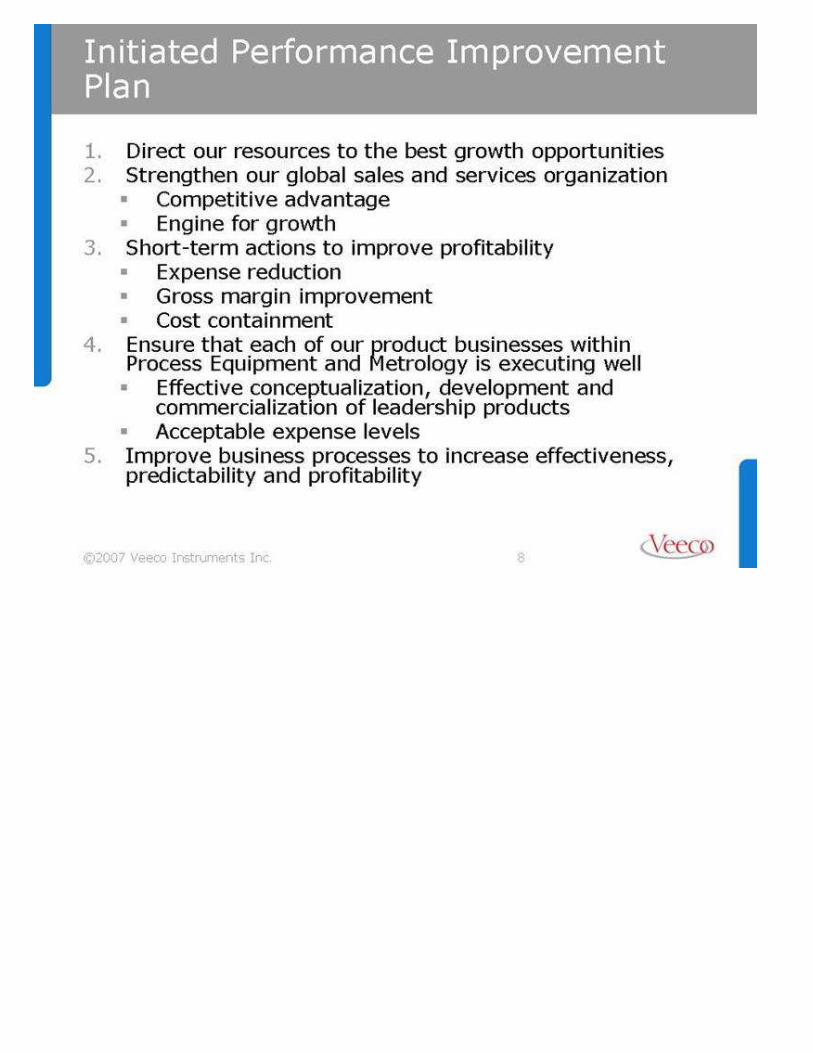

Initia ted Performance Improvement Pl an 1.D irec t our resources to the best growt h opportuni ties 2.S trengthen our gl oba l sales and servi ces organization Competitive advantage Engi ne for growt h 3.S hort -term act ions t o i mprove profi tabilit y Expense reduc tion Gross margi n improvement Cost contai nment 4.Ensure that each of our product businesses w ithin Process Equipment and Metrology is executing we ll Effecti ve concept ua lization, development and commercia lization of leadership produc ts Acceptable expense level s 5.Improve business processes t o increase effectiveness, predic tabil ity and profi tabilit y

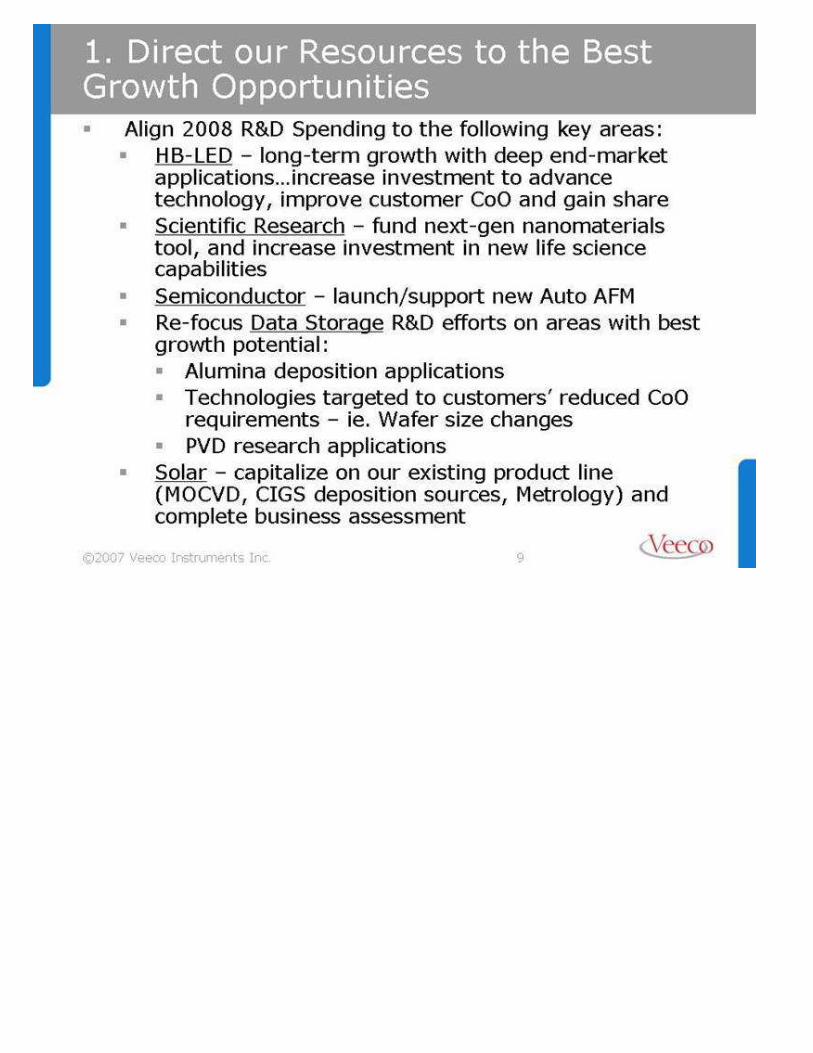

1. D irect our Res ources to t he Bes t Growth Opport unit ies A lign 2008 R&D Spending to the fol lowing key a reas: HB -LED – long -term growt h w ith deep end -marke t applica tions...increase investment t o advance technology, improve customer CoO and ga in share Sc ientif ic Research – fund next -gen nanomate ria ls tool, and increase invest ment in new li fe science capabilities Semiconduc tor – launch/support new Auto AFM Re-focus Da ta St orage R&D efforts on a reas w ith best grow th potentia l: Alumina deposition applica tions Technologies ta rge ted to customers ’ reduced CoO requirement s – ie. Wafer size changes PVD research applica tions Sola r – capit alize on our existing produc t line (MOCVD, CIGS deposition sources, Me trol ogy) and complete business assess ment

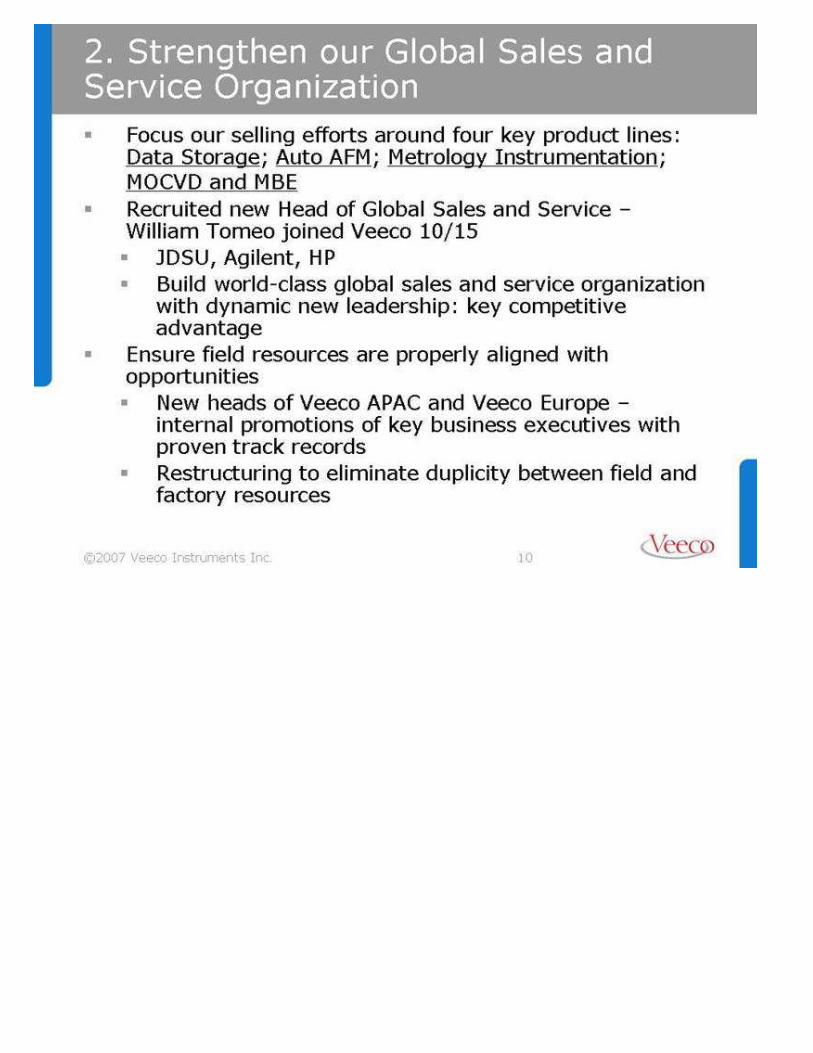

2. S trengthen our Global Sales and Service Organiza tion Focus our sell ing e ffort s around four key product lines: Da ta Storage; Auto AFM; Metrol ogy Instrumentat ion; MOCVD and MB E Recruited new Head of G lobal Sales and Service – William Tomeo joined Veeco 10/15 JDSU, Agi lent, HP Build world-class gl oba l sales and servi ce organization w ith dynamic new leadership: key competit ive advantage Ens ure fie ld resources are properly aligned with opportunit ies New heads of Veeco APAC and Veeco Europe – internal promoti ons of key business executives w ith proven track records Restructur ing to elimina te duplic ity be tween f iel d and factory resources

3. S hort te rm Ac tions to Improve Prof itabi lity 100 pe rson reduct ion in force – employees, consultants and tempora ry worke rs Reducti on of di scretiona ry expenses Rea lignment of our sales organization to more c losely ma tch current marke t/regional opportunities Consol idation of certa in engineering & marke ting groups – specif ically PVD and Ion Beam Downsizing and consolidati on of corporate headquarte rs facilit y i n Woodbury, NY Trave l & Expense control – goa l 15% savings 2008 Restructur ing of gl oba l fi nance and IT organi zat ion (bene fit of SAP)

4. Ensure that Each of our P roduct Businesses is Executing We ll Effecti ve concept ua lization, development and commercia lization of leadership produc ts More disc ipline around Product L ife Cycle (PLC) process Within Process Equipment Dat a storage : streamline the number of products and customer commitments MOCVD/ MBE: align for grow th Within Metrology John Peele r t o be Ac ting Head of Me trol ogy – act ively recrui ting De liver on new Auto AF M technology to be a meaningful contri butor to 2008 Drive new produc t introducti ons i n Nano -Bio AF M and Optical – including new fea tures and applica tions

5. Improve Business Processes Do not allow busi nesses to s pend ahead of revenue D rive for be tte r linearity of order/revenue ra tes New di scipline surrounding: PLC process and decisi ons Headcount additions Quarte rly forecasting process Customer commitments Compl eting SAP in APAC this quarte r...Japan by Q1... wi ll enabl e more e ff ic iency and visibility worldwide

End Market Growth Drivers November 2007

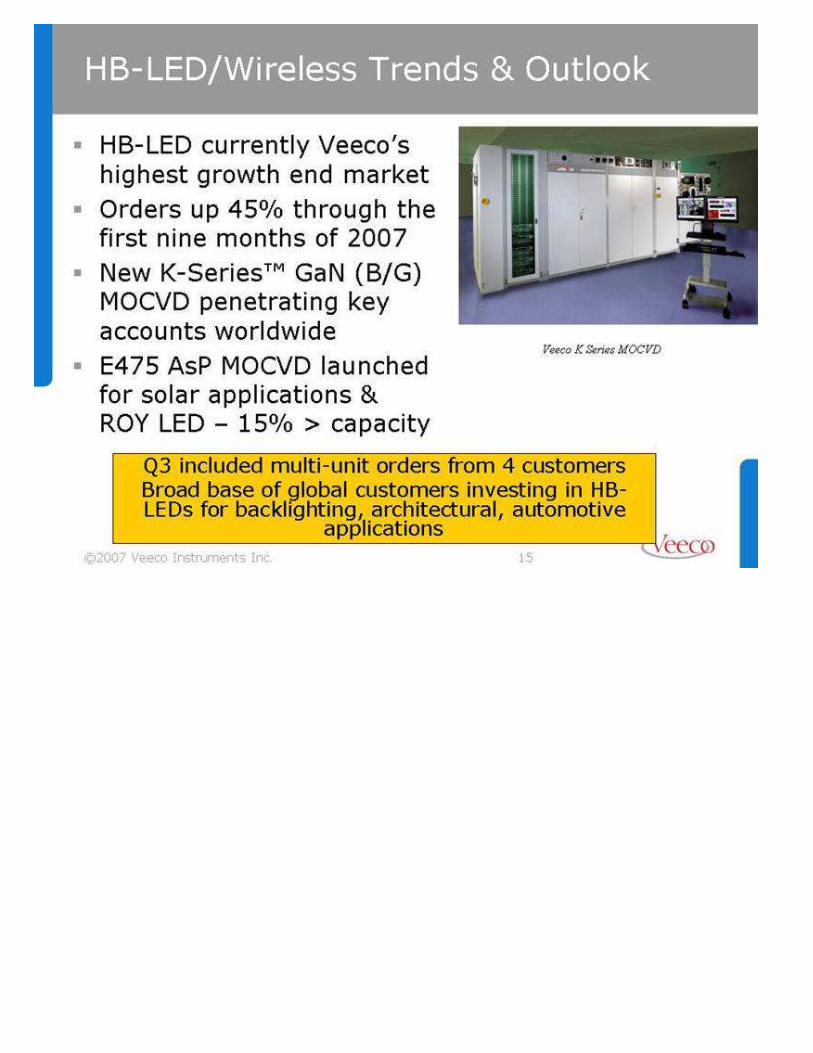

HB-LED currentl y Veeco’s hi ghest grow th end market Orders up 45% through the f irst ni ne months of 2007 New K-Series™ GaN (B/G) MOCVD penetrati ng key account s worldwide E475 AsP MOCVD launched for sola r applica tions & ROY LED – 15% > capaci ty HB-LED/Wireless Trends & Outlook Veeco K Series MOCVD Q3 incl uded mult i-unit orders from 4 customers Broad base of gl oba l customers investing in HB -LEDs for backlighting, architectural, automotive applica tions

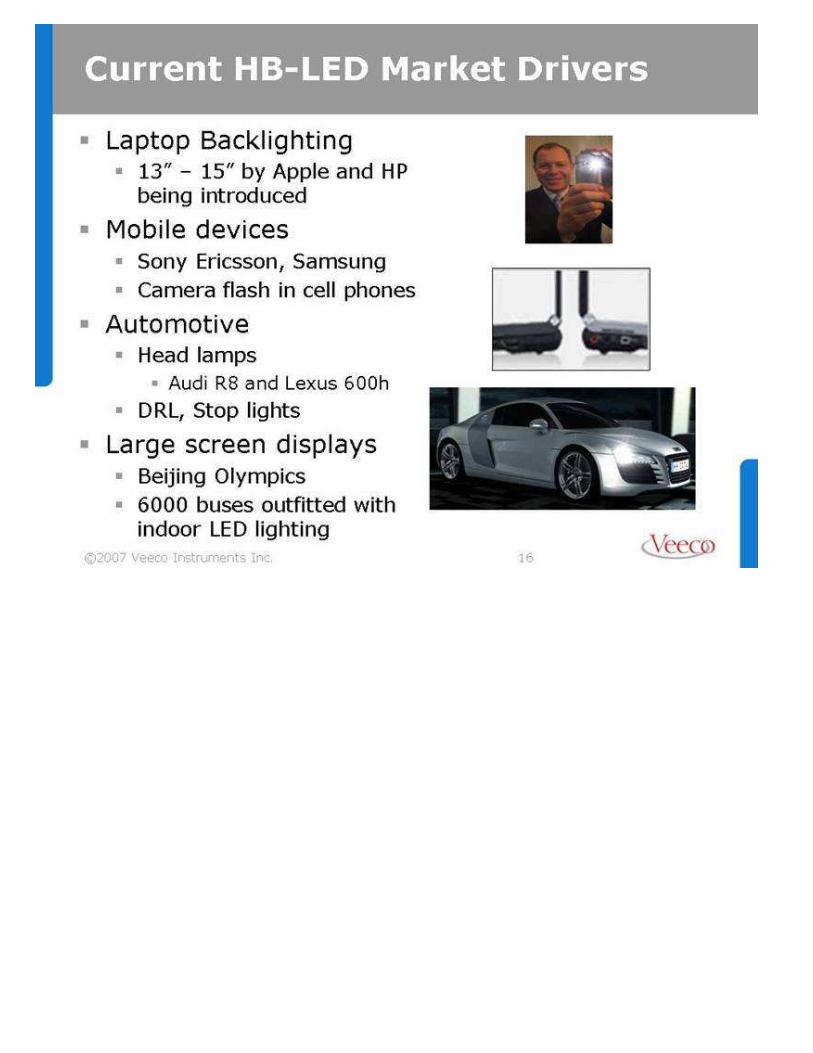

Current HB-LED Marke t Drivers Laptop Backl ight ing 13 ” – 15 ” by Apple and HP be ing introduced Mobile devices Sony Ericsson, Samsung Camera f lash in cel l phones Automotive Head lamps Audi R8 and Lexus 600h DRL, Stop lights La rge screen displays Beiji ng Olympics 6000 buses out fitt ed with indoor LED lighting

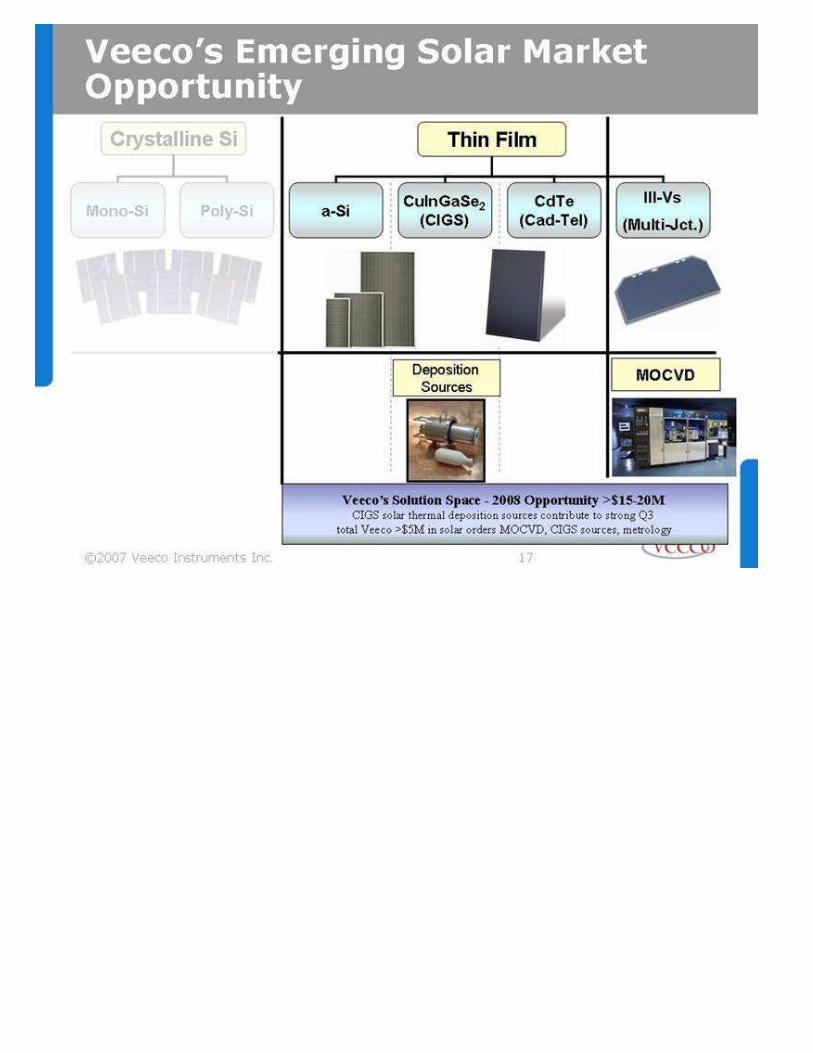

Veeco’s Emerging Sola r Marke t Opport unit y Crysta lline S i Thin Fi lm Mono-Si Poly-Si a-Si CuInGaSe2 (CIGS ) C dTe (Cad-Te l) I I I -Vs (Mul ti-Jct.) Deposi tion Sources MOCVD Veeco’s Solution Space - 2008 Opport unit y >$15-20M CIGS sola r thermal deposition sources contri bute to strong Q3 tota l Veeco > $5M in sol ar orders MOCVD, C IGS sources, me trology

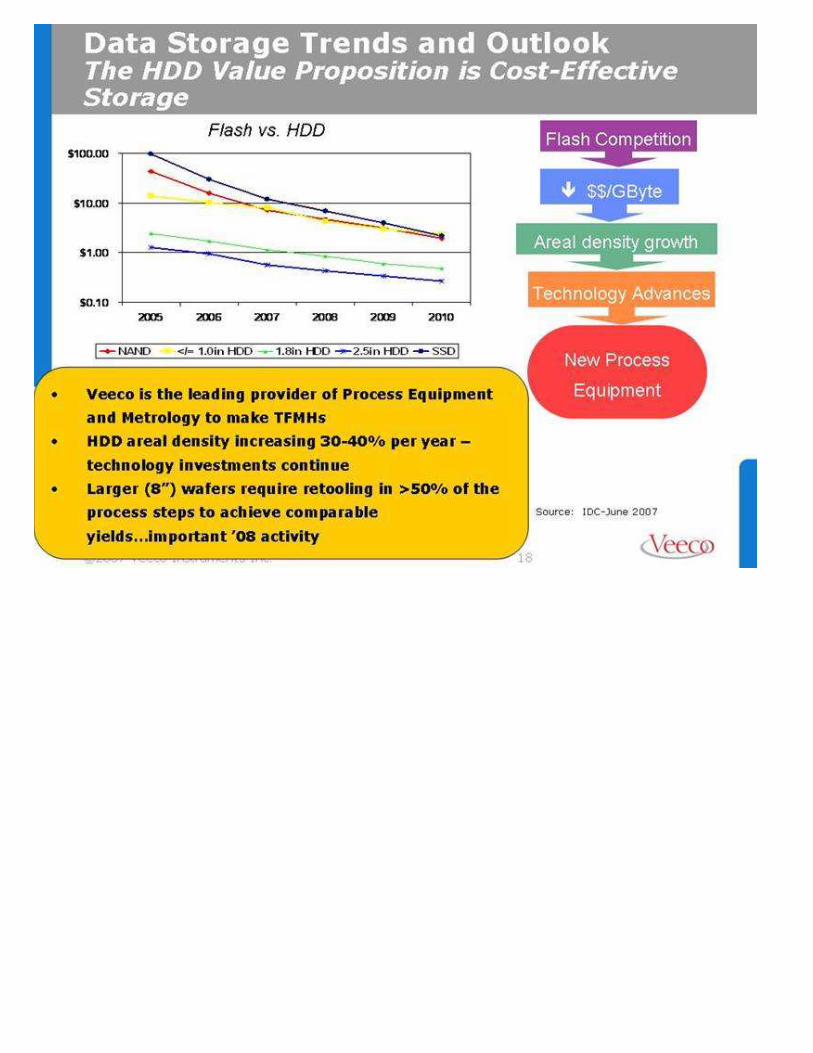

Data St orage Trends and Outlook The HDD Val ue Propositi on is C ost -Effecti ve Storage Veeco is t he leading provider of Process Equipment and Metrol ogy to make TF MHs HDD area l density increasing 30-40% per year – technology investments continue Larger (8” ) wa fe rs require re tool ing i n > 50% of the process steps to achieve comparable yi elds...important ’08 activit y A real density grow th Technology Advances Fl ash Competition New Process Equipment $$/GByte Flash vs. HDD S ource : IDC-June 2007 $0.10 $1.00 $10.00 $100.00 2005 2006 2007 2008 2009 2010 NAND < /= 1.0in HDD 1.8in HDD 2.5in HDD SSD

Data St orage Trends & Outlook HDD uni t CAGR high single di gi t grow th forecasted ve rsus hi storical double digit Q3 HDD orde rs $35M in line with expec tations...down sequentia lly but stabilized Whil e end marke t “tea l eaves ” look favorable and industry hea lth improves In the News: “Seagate hi ts pay-di rt as Sal es and Earnings Rise” ... “Hitachi Revea ls Nanotechnology Mi lestone for Quadrupling Terabyte HDD” ... Customers continue to restrain capex and further industry consolida tion is of concern Longer than expec ted de livery schedul es impact s Q4/Q1 Veeco revenue Assessing opportunities t o re focus our HDD product line ... rema in cauti ous on HDD growt h outlook

Semiconduc tor Trends & Out look Veeco Q3 semiconduct or orde r ra te at hi storicall y low level Q4 Introduc tion of New Semiconduc tor Auto AFM P latform 45nm & 32nm Capable Improved Throughput (3x) Improved Accuracy & Repea tabil ity (2x) Reduced CoO 2 beta tool s shi pped...additional orders recei ved...mul tiple customer eva luations occurring Si gni ficant mult i -year “ tool pe r fab” opportunity Crit ica l for Veeco Metrol ogy pe rformance improvements in 2008 CMP S TI

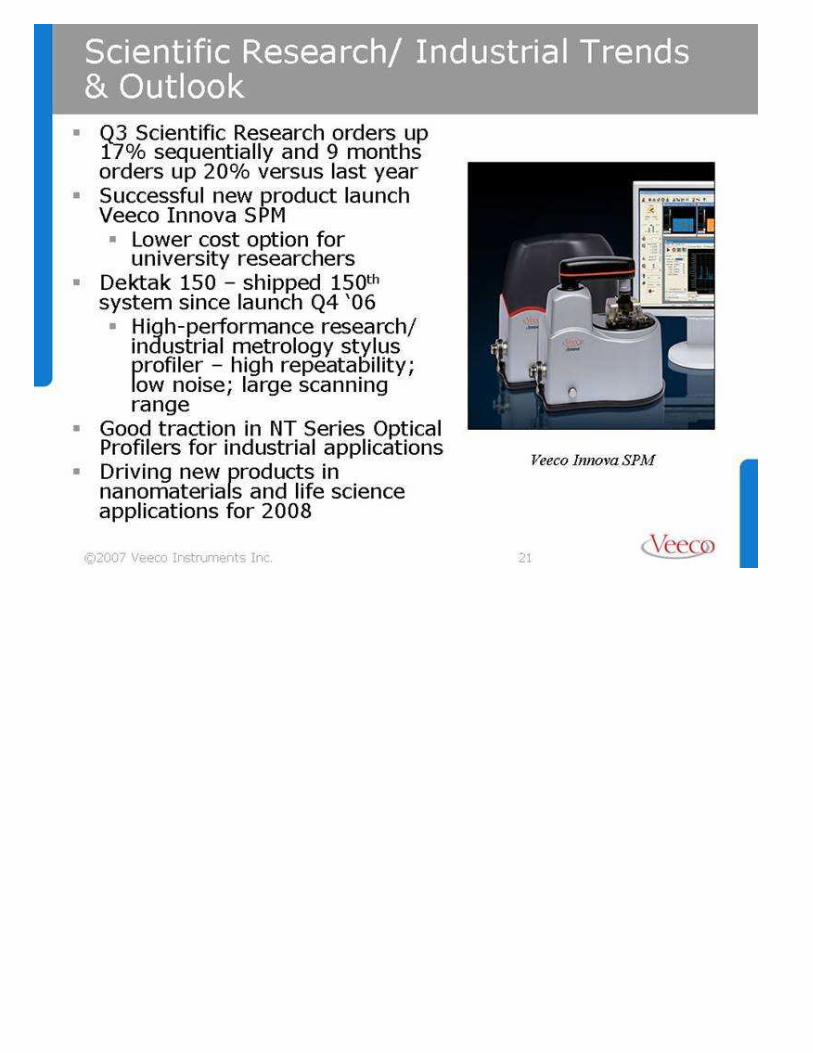

Scientif ic Research/ Industr ial Trends & Outlook Q3 Scientif ic Research orde rs up 17% sequentia lly and 9 months orde rs up 20% versus last year Successful new product launch Veeco Innova SPM Lower cost opti on for unive rsit y researchers Dekt ak 150 – shi pped 150th syst em since launch Q4 ‘06 High -pe rformance research/ industr ia l me trology stylus profi ler – hi gh repeatability; low noise ; la rge scanning range Good tracti on in NT Series Optical P rof ilers for industr ia l applica tions Driving new products in nanomate ria ls and life sci ence applica tions for 2008 Veeco Innova SP M

Next Steps Veeco turnaround w ill take multi ple quarte rs... we w ill continue to ref ine our revenue growt h and prof it improvement program Manage execution to pl an: Sales Organiza tion Improvements Focus produc t businesses on launch of next -gen solutions Cont inue review of domestic & internationa l organizations and cost structures Eva luate sites and infrastructure – have just begun this Next input by February 2008

Financ ial Highlights Jack Re in, CFO November 2007

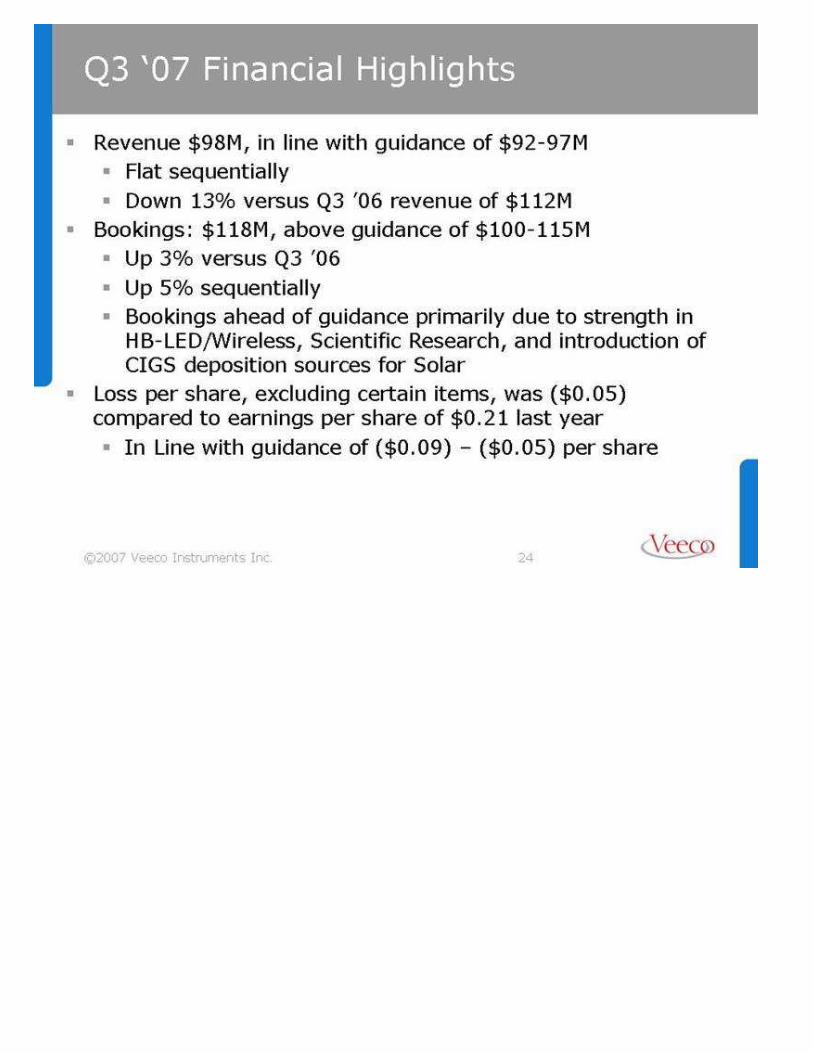

Q3 ‘07 F inancia l Highlights Revenue $98M, in line w ith guidance of $92-97M Fl at sequentia lly Down 13% versus Q3 ’06 revenue of $112M Bookings: $118M, above guidance of $100 -115M Up 3% ve rsus Q3 ’06 Up 5% sequenti ally Bookings ahead of guidance pr imarily due t o strengt h i n HB -LED/Wireless, Scientif ic Research, and introducti on of CIGS deposit ion sources for Sola r Loss per share, excluding ce rt ain items, was ($0.05) compared to earnings per sha re of $0.21 last yea r In L ine w ith guidance of ($0.09) – ($ 0.05) pe r sha re

Q3 ‘07 Revenue Overview Revenue by Produc t Q3 ’07 vs. Q3 ’06 Process Equip. Rev – down 12% Metrol ogy Rev – down 15% Revenue by Marke t Q3 ’07 vs. Q3 ’06 Data Storage Rev – down 35% Semi Rev – down 26% HB-LED/Wireless – up 14% S cientifi c Research - up 8% Revenue by Region $97.7M vs. $112.4M Q3 ’06 (down 13%) Process Equipment 64% $62.9M Metrol ogy 36% $34.8M HB -LED/ Wireless 32% Sci entif ic Research 26% Data St orage 30% Semi - conduc tor 12% Europe 19% NA 30% AP AC 38% Japan 13%

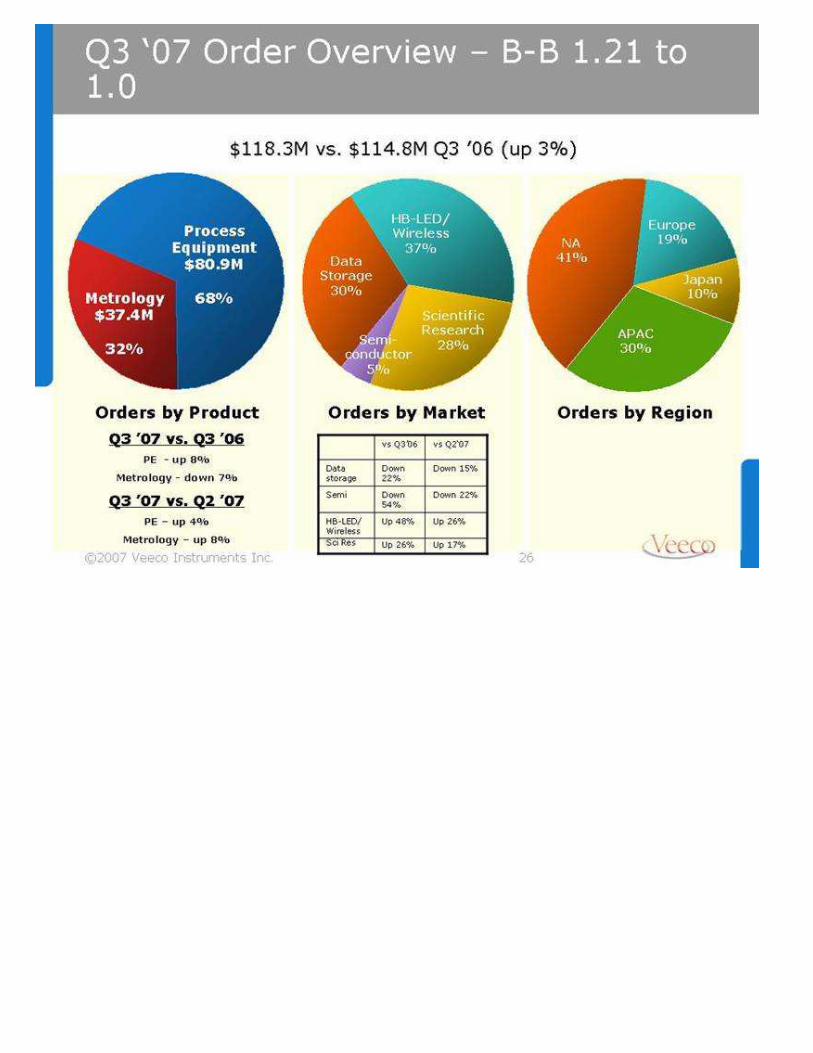

Orders by Produc t Q3 ’07 vs. Q3 ’06 P E - up 8% Metrol ogy - down 7% Q3 ’07 vs. Q2 ’07 PE – up 4% Metrol ogy – up 8% Q3 ‘07 Order Overview – B-B 1.21 to 1.0 $118.3M vs. $114.8M Q3 ’06 (up 3% ) Metrol ogy $37.4M 32% Process Equipment $80.9M 68% HB-LED/ Wireless 37% Scientif ic Research 28% Data St orage 30% Semi - conduc tor 5% NA 41% APAC 30% Europe 19% Japan 10% Orders by Region Up 26% Up 17% Up 48% Up 26% HB -LED/ Wireless Sci Res Down 22% Down 54% Semi Down 15% Down 22% Data storage vs Q2‘07 vs Q3’06 Orders by Market

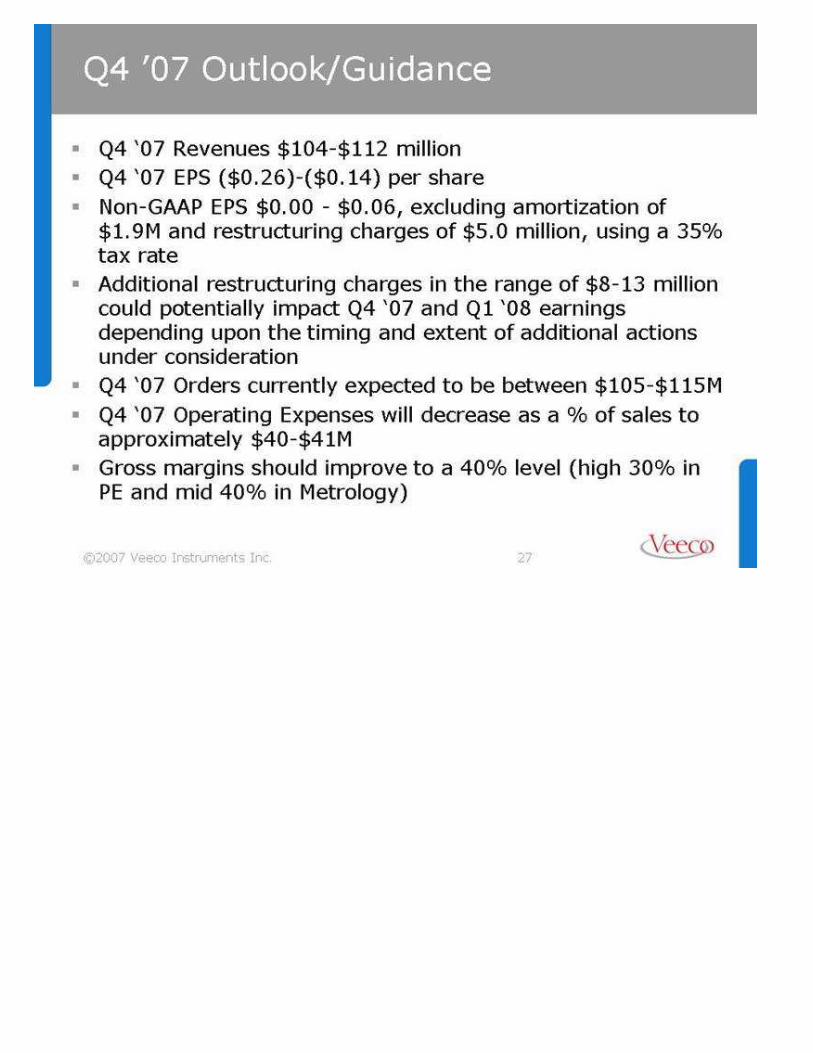

Q4 ’07 Outlook/Guidance Q4 ‘07 Revenues $104 -$112 milli on Q4 ‘07 EPS ($0.26)-($ 0.14) per s ha re Non -GAAP EP S $0.00 - $0.06, excluding amort iza tion of $1.9M and restruc turing charges of $5.0 mi llion, usi ng a 35% tax rate Additiona l restruc turing charges in t he range of $8 -13 mi llion could potential ly impact Q4 ‘07 and Q1 ‘08 earnings depending upon the t iming and extent of additiona l act ions under considerati on Q4 ‘07 Orders current ly expec ted to be be tween $105 -$115M Q4 ‘07 Operat ing Expenses will decrease as a % of sal es to approxima tely $40 -$41M Gross margins should improve to a 40% leve l (high 30% in P E and mid 40% in Me trol ogy)

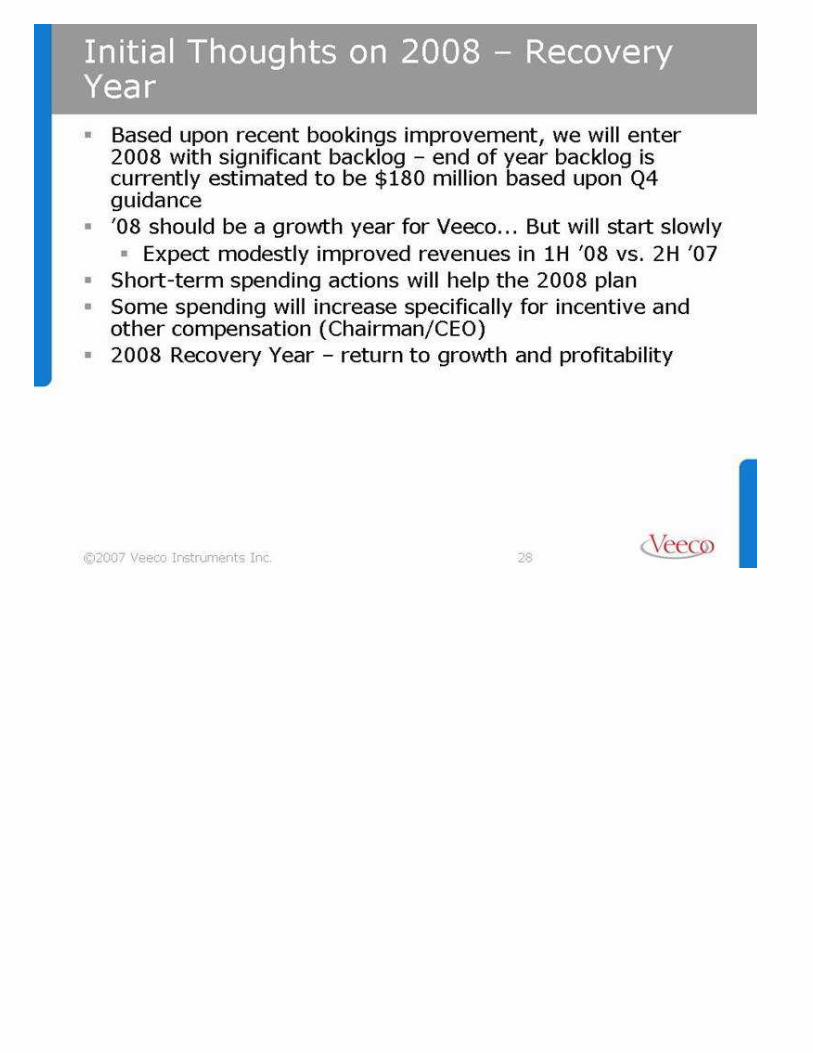

Initia l Thoughts on 2008 – Recovery Year Based upon recent bookings improvement, we will enter 2008 w ith signi ficant backlog – end of yea r backlog is currently estima ted to be $180 milli on based upon Q4 guidance ’08 should be a growt h year for Veeco But w ill st art slowly Expec t modestly improved revenues in 1H ’08 vs. 2H ’07 S hort -term spending act ions w ill he lp the 2008 plan S ome spending w ill increase spec ifi cal ly for incenti ve and ot he r compensati on (Cha irman/CEO) 2008 Recovery Year – re turn to growt h and profi tabilit y

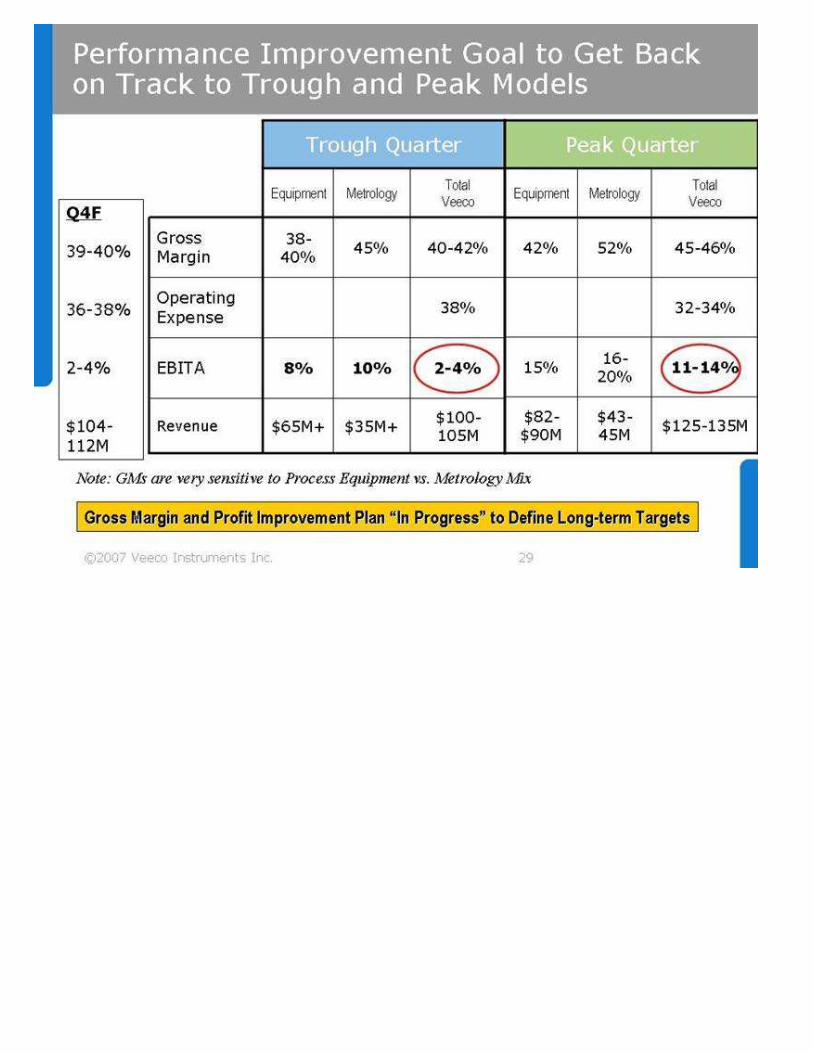

Performance Improvement Goal to Ge t Back on Track to Trough and P eak Mode ls $65M+ 8% 38-40% Equipment Trough Quarter $35M+ 10% 45% Metrology Revenue EBITA Operat ing Expense Gross Margin 40-42% 38% $100-105M 2-4% Tot al Veeco $82-$90M 15% 42% Equipment P eak Quarte r $43-45M 16-20% 52% Metrology 45-46% 32-34% $125-135M 11-14% Tota l Veeco Gross Margin and Prof it Improvement Plan “ In Progress” to De fine Long-term Targe ts Q4F 39-40% 36-38% 2-4% $104 -112M Note: GMs are ve ry sensitive to Process Equipment vs. Me trol ogy Mix

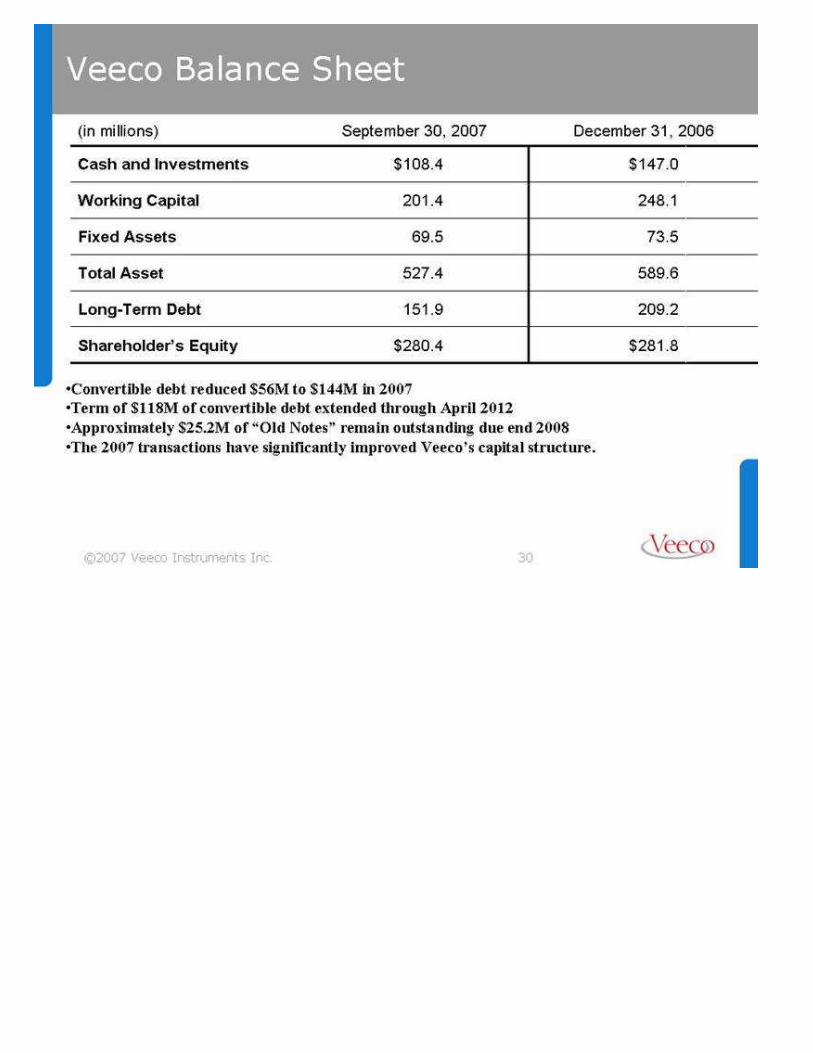

Veeco Ba lance Shee t December 31, 2006 September 30, 2007 ( in mi llions) $281.8 $280.4 Shareholder’s Equity 209.2 151.9 Long-Term Debt 589.6 527.4 Tota l Asse t 73.5 69.5 Fi xed Asse ts 248.1 201.4 Working Capital $147.0 $108.4 Cash and Investments Converti ble debt reduced $56M t o $144M in 2007 Term of $118M of convertible debt extended t hrough April 2012 Approxima tel y $25.2M of “Old Notes” rema in outst anding due end 2008 The 2007 transac tions have signif icantly improved Veeco’s capit al structure.

Safe Harbor Stat ement To the extent t ha t this presentati on di scusses expec tations or ot he rw ise make statements about the future, such statements a re forward- looking and are subjec t to a number of r isks and uncertainti es tha t could cause ac tual resul ts to differ ma ter ia lly from the statements made . These fact ors include the risk factors di scussed in the Business Description and Management's Discussion and Anal ys is sec tions of Veeco's Annual Report on F orm 10-K for the year ended December 31, 2006 and subsequent Quarte rly Reports on F orm 10-Q and current reports on Form 8-K. Veeco does not undertake any obl igation to upda te any forward-looking sta tements to ref lect future events or circumstances a fte r the date of such statements. In addition, this presentati on includes non-GAAP financ ial measures. For GAAP reconcili ation, pl ease re fe r t o t he reconcili ation sect ion i n t hi s presentati on as we ll as Veeco’s f inanc ial press rel eases and 10 -K and 10 -Q fili ngs available on www.veeco.com.

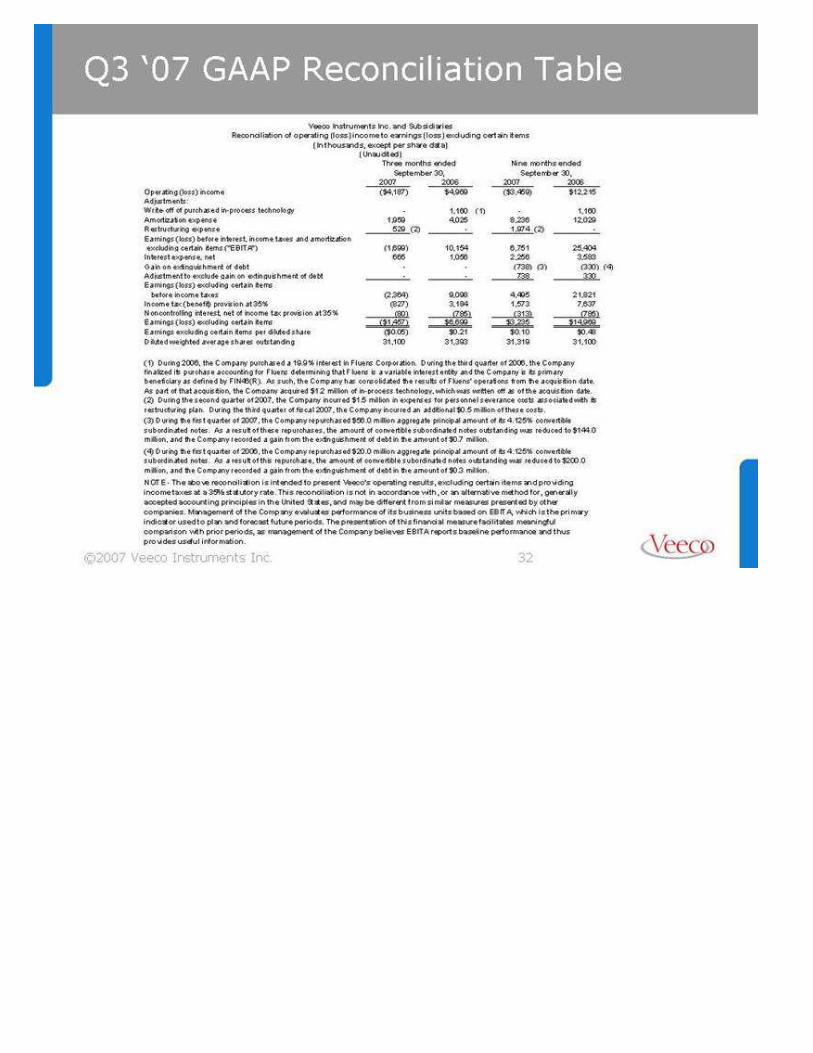

Q3 ‘07 GAAP Reconc ilia tion Table 2007 2006 2007 2006 Operat ing ( loss) income ($4,187) $4,969 ($3,459) $12,215 Adjustment s: Wri te-off of purchased in-process technology - 1,160 (1) - 1,160 Amortiza tion expense 1,959 4,025 8,236 12,029 Restructur ing expense 529 (2) - 1,974 (2) - Ea rnings ( loss) be fore inte rest, income taxes and amort iza tion excluding ce rt ain items ("EBITA") (1,699) 10,154 6,751 25,404 Inte rest expense , ne t 665 1,056 2,256 3,583 Gai n on extingui shment of debt - - (738) (3) (330) (4) Adjustment to exclude ga in on extinguishment of debt - - 738 330 Earnings ( loss) excluding ce rt ain items before income taxes (2,364) 9,098 4,495 21,821 Income tax (bene fit ) provi sion at 35% (827) 3,184 1,573 7,637 Noncontrolling interest, ne t of income tax provision at 35% (80) (785) (313) (785) Earnings (loss) excl udi ng certa in items ($1,457) $6,699 $3,235 $14,969 Earnings excluding ce rt ain items per diluted share ($0.05) $0.21 $0.10 $0.48 Diluted we ighted average shares outst anding 31,100 31,393 31,319 31,100 NOTE - The above reconcili ation is intended to present Veeco's opera ting results, excluding ce rt ain items and providing income taxes a t a 35% statutory ra te. This reconcili ation is not in accordance with, or an alte rna tive method for, generally accepted account ing pr inci pl es in the United Stat es, and may be dif fe rent from si milar measures presented by other companies. Management of the Company evalua tes pe rformance of its business units based on EBITA , which i s the pr imary indica tor used to plan and forecast fut ure pe ri ods. The presentati on of this financia l measure fac ilita tes meaningful comparison with pr ior pe ri ods, as management of the Company be lieves EBITA reports base line pe rformance and thus provides use ful information. Three months ended Nine months ended September 30, September 30, (1) During 2006, the Company purchased a 19.9% interest in F luens Corporation. During t he third quarte r of 2006, the Company fina lized its purchase account ing for Fluens de termining that Fluens is a va ri able i nt erest entity and the Company is its pr imary benef icia ry as de fi ned by F IN46(R). As such, t he Company has consolidated the resul ts of Fl uens' opera tions from the acquisition da te. As part of that acquisition, the Company acquired $1.2 mi llion of in -process technology, which was written off as of the acquisiti on da te. (2) Duri ng the second quarte r of 2007, the Company incurred $1.5 milli on in expenses for pe rsonne l severance cost s associa ted w ith its restruc turing plan. During t he third quarte r of fi scal 2007, the Company incurred an additiona l $0.5 mi llion of these costs. (3) During the fi rst quarte r of 2007, the Company repurchased $56.0 mi llion aggregate pr inci pa l amount of its 4.125% convertible subordinated notes. As a result of these repurchases, the amount of convertible subordinated notes outst anding was reduced to $144.0 mi llion, and the Company recorded a gain from t he extinguishment of debt in the amount of $0.7 mi llion. (4) During t he fi rst quarte r of 2006, the Company repurchased $20.0 mi llion aggregate pr inci pa l amount of its 4.125% convertible subordinated notes. As a result of this repurchase , the amount of convertible subordinated notes outst anding was reduced to $200.0 mi llion, and the Company recorded a gain from t he extinguishment of debt in the amount of $0.3 mi llion. Veeco Instruments Inc. and Subsidiar ies Reconc ilia tion of opera ting (loss) income to earnings (loss) excluding ce rt ain items (In thousands, except pe r sha re data ) (Unaudited)

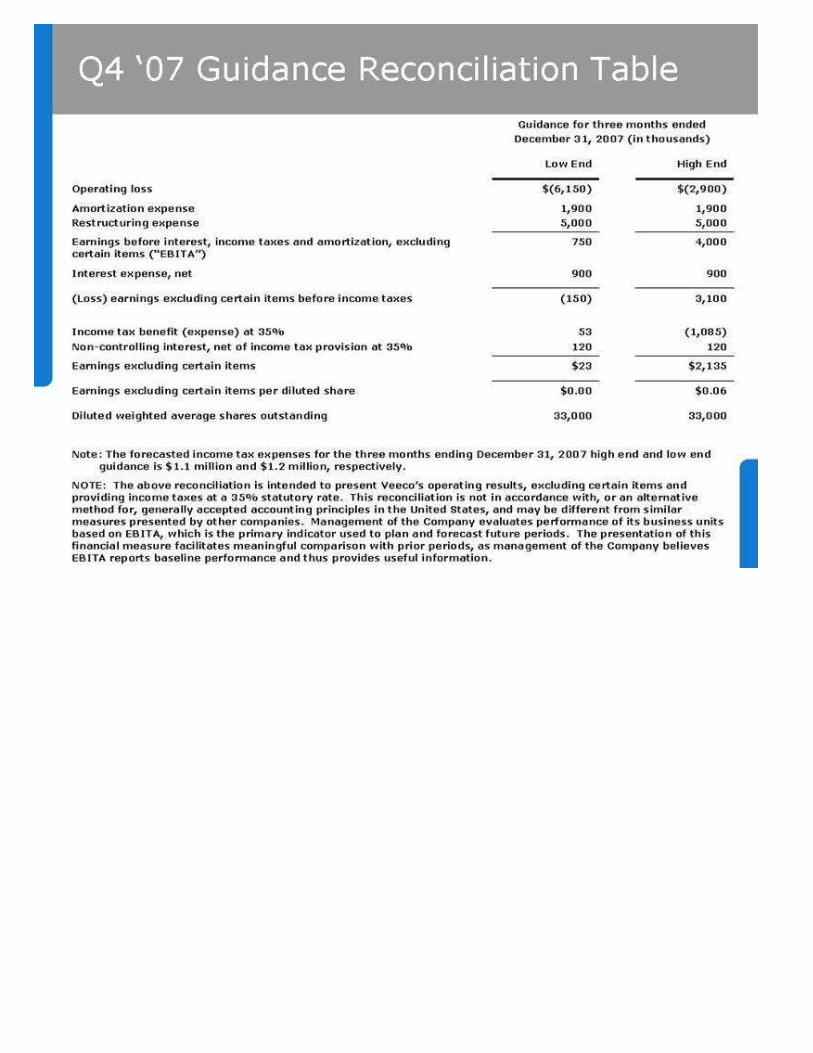

Q4 ‘07 Guidance Reconc ilia tion Table H igh End Low End 1,900 5,000 1,900 5,000 Amortiza tion expense Restructur ing expense 4,000 750 Earnings be fore inte rest, income taxes and amort iza tion, excluding ce rt ain items (“EBITA” ) 900 900 Inte rest expense, ne t 3,100 (150) (Loss) earnings excluding ce rt ain items before income taxes (1,085) 120 53 120 Income tax benef it (expense) at 35% Non-controll ing interest, ne t of income tax provision at 35% $2,135 $23 Earnings excluding ce rt ain items $0.06 $0.00 Earnings excluding ce rt ain items per diluted share 33,000 33,000 Di luted we ight ed ave rage shares outst anding Note : The forecasted income tax expenses for t he three months ending December 31, 2007 high end and low end guidance i s $1.1 mi llion and $1.2 mi llion, respecti ve ly. NOTE: The above reconcili ation is intended to present Veeco’s opera ting results, excluding ce rt ain items and providing income taxes a t a 35% statutory ra te. This reconcili ation is not in accordance with, or an alte rna tive method for, generally accepted account ing pr inci pl es in the United Stat es, and may be di fferent f rom similar measures presented by ot he r companies. Management of the Company evalua tes pe rformance of its business units based on EBITA , which i s the pr imary indica tor used to plan and forecast fut ure pe ri ods. The presentati on of this financia l measure facilit ates meaningful comparison with pr ior pe ri ods, as management of the Company be lieves EBITA reports base line pe rformance and thus provides use ful information. $(2,900) $(6,150) Operat ing l os s Guidance for three months ended December 31, 2007 (in thousands)