via asx online for public release (26 pages including cover)

TRANSCRIPT

Suite 801, Level 8 Tel: (61 2) 8256 4800 Email: [email protected] 14 Martin Place Fax: (61 2) 8256 4810 Website: www.kingsgate.com.au Sydney NSW 2000 Australia

ABN 42 000 837 472

21 September 2010 Via ASX online FOR PUBLIC RELEASE (26 pages including cover) The Manager Company Announcements Office Australian Securities Exchange Dear Sir/Madam,

2010 Post Financials Presentation Please find attached Kingsgate presentation update which was provided to investors at the Excellence in Mining Conference held in Sydney, as well as the Denver Gold Conference held in Denver today. Yours faithfully, KINGSGATE CONSOLIDATED LIMITED PETER WARREN Company Secretary

Kingsgate Consolidated Limited

Kingsgate Consolidated Limited

High Margin Gold Production ASX 2nd

largest gold company

High Margin Gold Production ASX 2nd

largest gold company

September 2010September 2010

1st

Millionth Ounce Bar1st

Millionth Ounce Bar

These materials include forward looking statements. Forward looking statements inherently involve subjective judgment & analysis & are subject to significant uncertainties, risks & contingencies, many of which are outside of the control of, & may be unknown to, the company.

Actual results and developments may vary materially from that expressed in these materials. The types of uncertainties which are relevant to the company may include, but are not limited to,

commodity prices, political uncertainty, changes to the regulatory framework which applies to the business of the company & general economic conditions. Given these uncertainties, readers are cautioned not to place undue reliance on such forward looking statements.

Forward looking statements in these materials speak only at the date of issue. Subject to any continuing obligations under applicable law or any relevant stock exchange listing rules, the

company undertakes any obligation to publicly update or revise any of the forward looking statements, changes in events, conditions or circumstances on which any such statement is based.

These materials include forward looking statements. Forward looking statements inherently involve subjective judgment & analysis & are subject to significant uncertainties, risks & contingencies, many of which are outside of the control of, & may be unknown to, the company.Actual results and developments may vary materially from that expressed in these materials. The types of uncertainties which are relevant to the company may include, but are not limited to,

commodity prices, political uncertainty, changes to the regulatory framework which applies to the business of the company & general economic conditions. Given these uncertainties, readers are cautioned not to place undue reliance on such forward looking statements.Forward looking statements in these materials speak only at the date of issue. Subject to any continuing obligations under applicable law or any relevant stock exchange listing rules, the

company undertakes any obligation to publicly update or revise any of the forward looking statements, changes in events, conditions or circumstances on which any such statement is based.

Forward Looking Statements:Forward Looking Statements:

Information in this presentation that relates to Exploration Results, Mineral Resource and Ore Reserve estimates, geology, drilling and mineralisation, is based on information compiled by

Ron James, who is an employee of the Kingsgate Group and is a member of The Australasian Institute of Mining and Metallurgy.

Ron James is a Competent Person under the meaning of the JORC Code with respect to Exploration Results, Mineral Resource and Ore Reserve estimates, geology, drilling and mineralisation being presented. He has given his consent to the Public Reporting of these statements concerning Exploration Results, Mineral Resource and Ore Reserve estimates, geology, drilling and mineralisation, and is in agreement with the contents and format of this presentation.

Information in this presentation that relates to Exploration Results, Mineral Resource and Ore Reserve estimates, geology, drilling and mineralisation, is based on information compiled by

Ron James, who is an employee of the Kingsgate Group and is a member of The Australasian Institute of Mining and Metallurgy.

Ron James is a Competent Person under the meaning of the JORC Code with respect to Exploration Results, Mineral Resource and Ore Reserve estimates, geology, drilling and mineralisation being presented. He has given his consent to the Public Reporting of these statements concerning Exploration Results, Mineral Resource and Ore Reserve estimates, geology, drilling and mineralisation, and is in agreement with the contents and format of this presentation.

Any statement or information relating to the potential quantity and grade of an exploration target, specifically the Chokdee Prospect, is based on recent public announcements and is conceptual in nature. There has been insufficient exploration to define a Mineral Resource and it is uncertain if further exploration will result in the determination of a Mineral Resource.

Any statement or information relating to the potential quantity and grade of an exploration target, specifically the Chokdee Prospect, is based on recent public announcements and is conceptual in nature. There has been insufficient exploration to define a Mineral Resource and it is uncertain if further exploration will result in the determination of a Mineral Resource.

Competent Persons Statement:Competent Persons Statement:

Reporting on Exploration Targets:Reporting on Exploration Targets:

DisclaimerDisclaimer

ASX: Rising Mid-Tier MinerASX: Rising Mid-Tier Miner

Low Cost Gold ProductionLow Cost Gold Production

Increasing Reserves/ShareIncreasing Reserves/Share

Increasing Earnings/ShareIncreasing Earnings/Share

Proven Value CreatorProven Value Creator

Expanding ProductionExpanding Production

Kingsgate – Asian Gold Kingsgate – Asian Gold

ChatreeChatree

2nd

Largest ASX Gold Stock (by Mkt Cap)

Key asset -

Chatree Mine, Thailand

Producing: ~9 years, >1Moz poured

Mine life: 12+ years with expansion

Mkt Cap: ~A$1 Billion

Shares: 100.7 Million, 1.8M options

3rd

best performing ASX200 stock

over last decade

Highest dividend paying gold stock

Stock widely held by:

Insto’s: 20% Aust, 20% USA, 15% Europe/UK, 5% Asia

Retail: 25%Directors: 8%

2nd

Largest ASX Gold Stock (by Mkt Cap)

Key asset -

Chatree Mine, Thailand

Producing: ~9 years, >1Moz poured

Mine life: 12+ years with expansion

Mkt Cap: ~A$1 Billion

Shares: 100.7 Million, 1.8M options

3rd

best performing ASX200 stock

over last decade

Highest dividend paying gold stock

Stock widely held by:

Insto’s: 20% Aust, 20% USA, 15% Europe/UK, 5% Asia

Retail: 25%Directors: 8%

ThaiGold Belt

Global Cumulative Gold Production (%)Global Cumulative Gold Production (%)50%50% 100%100%25%25% 75%75%0%0%

Average Gold Only Producers(US$600/oz)

Average Gold Only Producers(US$600/oz)

US$850-900/ozCash

margin

US$850-900/ozCash

margin

Low Cost Gold ProducerLow Cost Gold Producer

Kingsgate 8 Year AverageUS$232/oz @ 2.5g/t Au (1 Moz)

Kingsgate FY2010

US$335/oz @ 1.7g/t Au

Kingsgate FY2010

US$335/oz @ 1.7g/t Au

US$/

ozUS

$/oz

-200-200

800800

600600

400400

200200

00

10001000 Global Cash CostCurve 2009

Global Cash CostCurve 2009

Low Cash CostsUS$335/oz costsLow Cash CostsUS$335/oz costs

Lowest 20% ofIndustry CostsLowest 20% ofIndustry Costs

Source: GFMS.Source: GFMS.

US$850-900/oz Cash Margin

US$850-900/oz Cash Margin

Gold

Pric

e Go

ld P

rice

Good Position on Cost CurveGood Position on Cost Curve

Low Cost ProductionLow Cost Production

Asian Competitive Advantage

Asian Competitive Advantage

Costs: US$15.50/t, Up15% in 9 yearsGrid power & labour keep costs lowCosts: US$15.50/t, Up15% in 9 yearsGrid power & labour keep costs low

Low Cost Gold Maintained

US$335/oz costs

Low Cost Gold Maintained

US$335/oz costs

132,628oz Gold Production FY10US$335/oz Cash Costs FY10US$257/oz + US$78/oz Thai Royalty

132,628oz Gold Production FY10US$335/oz Cash Costs FY10US$257/oz + US$78/oz Thai Royalty

Cash CostsRoyalty

Mining

Costs

ProcessingSupport

20

10

5

15

0

15.20US$/t

17.10US$/t

14.40US$/t

17.50US$/t

14.80US$/t

15.10US$/t

Mar 09 Jun 10Mar 10Dec 09Sep 09Jun 09

US$/

tonn

e Or

e Pr

oces

sed Quarterly Cash Costs per TonneQuarterly Cash Costs per Tonne

1.61.61.71.72.32.3

1.51.52.02.0

1.51.5 g/tAug/tAu

Quarterly Cash Costs per OunceQuarterly Cash Costs per Ounce

0

100

200

300

400US$

Average:US$322/oz

364

309

Mar 09

32,992oz

228

169

Jun 09

43,036oz

Sep 09

359

288

29,302oz

332

247

Mar 10

32,646oz

345

261

Jun 10

30,456oz

312

239

Dec 09

40,224oz

Operating Cash Costs

Royalty

Expansion: Double CapacityExpansion: Double Capacity

Plant Expansion+ 2.7 Mtpa

Plant Expansion+ 2.7 Mtpa

Current Plant2.3 Mtpa

Current Plant2.3 Mtpa

Expanded Total+5 Mtpa

Expanded Total+5 Mtpa

Plant processing capacity increase from 2.3 to >5 MtpaMid-2011 Commissioning; Ausenco EPCM Increase production up to 200,000 ounces per year

Plant processing capacity increase from 2.3 to >5 MtpaMid-2011 Commissioning; Ausenco EPCM Increase production up to 200,000 ounces per year

Expansion Plant Areabeside current plantExpansion Plant Areabeside current plant

Construction UnderwayConstruction Underway

CIL Tanks & Grinding Circuit under constructionCapex

Remaining ~US$100m; Spent Further US$25m

Mandated Investec & Thai banks : Seek US$100m debt Tax incentives granted for production from new plant

CIL Tanks & Grinding Circuit under constructionCapex

Remaining ~US$100m; Spent Further US$25m

Mandated Investec & Thai banks : Seek US$100m debt Tax incentives granted for production from new plant

Grinding CircuitSAG & Ball Mill AreaGrinding CircuitGrinding CircuitSAG & Ball Mill AreaSAG & Ball Mill Area

CIL TanksCIL TanksCIL TanksTailings ThickenerTailings ThickenerTailings Thickener

Construction UnderwayConstruction Underway

Key items in place –

concrete footings/slab and steelworkKey items in place –

concrete footings/slab and steelwork

CIL TanksCIL TanksCIL Tanks

Primary CrusherPrimary CrusherPrimary CrusherStockpile ReclaimStockpile ReclaimStockpile Reclaim

1 km1 km

World Class DepositWorld Class Deposit

World Class Deposits are >5 Moz

World Class Deposits are >5 Moz

Chatree ~6Moz to date & growing

including mined to date

Chatree ~6Moz to date & growingincluding mined to date

1.9 Moz Reserve4.3 Moz Resource1.9 Moz Reserve

4.3 Moz Resource

Section5km5km

1 km1 km

WesternAustralia’sKalgoorlie Super Pit

(same scale)

WesternAustralia’sKalgoorlie Super Pit

(same scale)

Expanding Current PitsExpanding Current Pits

Current ‘A’

Pit design

is at limit of drill data

Drilling restricted due to blasting in mine

Current ‘A’

Pit design

is at limit of drill data

Drilling restricted due to blasting in mine

30m @ 16g/t gold30m @ 16g/t gold12m @ 30g/t gold12m @ 30g/t gold

Upside in Prior PitsUpside in Prior Pits

Prior pits to re-open at current gold price

Drilling to locate high-grade targets

Prior pits to re-open at current gold price

Drilling to locate high-grade targets

2.5 km2.5 km2.5 km

17m@ 4.7g/t1m@41g/t

26m@ 2.1g/t3m@17g/t

Conceptual PitsConceptual Pits

* Whittle Four-X modelling only at different pit optimisation scenarios

* Whittle Four-X modelling only at different pit optimisation scenarios

Q Pit(sth)

Large Low Grade PotentialLarge Low Grade Potential

‘A’

Pit -

Chatree NorthLarger Pit potential

at current gold prices

‘A’

Pit -

Chatree NorthLarger Pit potential

at current gold prices

Chatree TotalReserves: 1.9 MozResources: 4.3 Moz

Chatree TotalReserves: 1.9 MozResources: 4.3 Moz

A PitChatree Grade/Tonnage Variance Versus Gold Price*

Gold Price(US$)

Gold Grade(g/t)

Tonnes(Millions)

Contained Gold(Moz)

1050 0.98 71 2.21150 0.96 78 2.41250 0.85 100 2.7

Best Ever Profit; Up 125%Best Ever Profit; Up 125%

EPS: 75.2 cents/share Solid profit from full productionMaintain low cash costs: US$335/oz

EPS: 75.2 cents/share Solid profit from full productionMaintain low cash costs: US$335/oz

FY10 Profit: A$73.1MUp 125%

FY10 Profit: A$73.1MUp 125%

‘Underlying Profit’ A$75.6M

‘Underlying Profit’ A$75.6M

Add back unrealised FX loss (A$3m)1st

year of Thai Tax (7mths at 15%)Pre-Tax Profit A$82.3M -

up 150%

Add back unrealised FX loss (A$3m)1st

year of Thai Tax (7mths at 15%)Pre-Tax Profit A$82.3M -

up 150%

Revenue: A$175MEBITDA: A$96M

Revenue: A$175MEBITDA: A$96M

Revenue up 54% from prior yearIncreased production:132,628 ozs

gold; 2.7Mt processed

Revenue up 54% from prior yearIncreased production:132,628 ozs

gold; 2.7Mt processed

Highest Gold Dividend YieldHighest Gold Dividend Yield

FY10 Dividend: 35c/shYield: 3.5%

FY10 Dividend: 35c/shYield: 3.5%

Strong Cash PositionStrong Cashflow

Strong Cash PositionStrong Cashflow

Differentiate KCN from ETF’sTotal: A$1.29/sh since 2002Highest yield of any gold miner

Differentiate KCN from ETF’sTotal: A$1.29/sh since 2002Highest yield of any gold miner

Cash: A$49M at end June No debt; Unused US$30m facilityStrong cashflow

to support

exploration, development. US$100m debt being arranged

for expansion –

Investec, Thai

Cash: A$49M at end June No debt; Unused US$30m facilityStrong cashflow

to support

exploration, development.US$100m debt being arranged

for expansion –

Investec, Thai

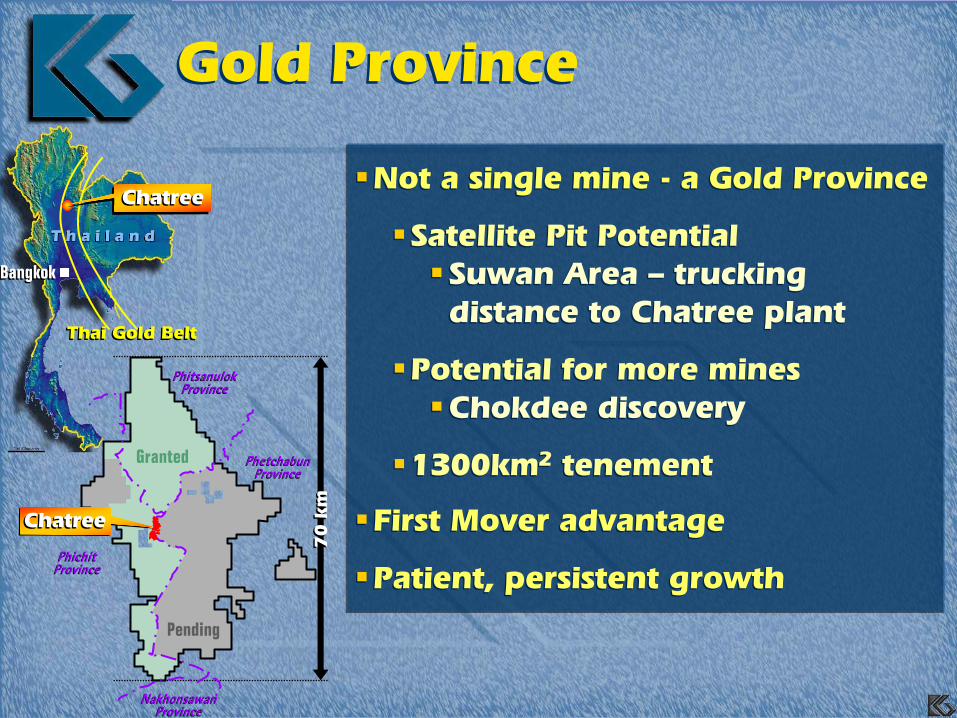

Gold ProvinceGold Province

T h a i l a n dT h a i l a n dT h a i l a n dT h a i l a n dT h a i l a n d

Not a single mine -

a Gold Province

Satellite Pit Potential

Suwan Area –

trucking

distance to Chatree plant

Potential for more mines

Chokdee discovery

1300km2

tenement

First Mover advantage

Patient, persistent growth

Not a single mine -

a Gold Province

Satellite Pit Potential

Suwan Area –

trucking

distance to Chatree plant

Potential for more mines

Chokdee discovery

1300km2

tenement

First Mover advantage

Patient, persistent growthPending

70

km

70

km

Granted

NakhonsawanProvince

PhitsanulokProvince

PhichitProvince

PhetchabunProvince

NakhonsawanProvince

PhichitProvince

PhetchabunProvince

PhitsanulokProvince

ChatreeChatree

Thai Gold BeltThai Gold Belt

ChatreeChatree

BangkokBangkok

Target: Fill The VoidTarget: Fill The Void

No major ASX gold companies except Newcrest

Mid tier Producers: 100-300,000 oz/year

No major ASX gold companies except Newcrest

Mid tier Producers: 100-300,000 oz/year

Lihir

& Andean gone from ASX Lihir

& Andean

gone from ASX

Opportunity exists to Fill the Void

Opportunity exists to Fill the Void

KCN –

2nd

largest gold producer on ASX by market capitalisation

KCN –

2nd

largest gold producer on ASX by market capitalisation

Market Demand:Mid Tier ProducerMarket Demand:Mid Tier Producer

Market seeking liquid mid-tier gold producer with >300,000 ozs/year

Market seeking liquid mid-tier gold producer with >300,000 ozs/year

Growing a Mid Tier MinerGrowing a Mid Tier Miner

Forecast production

~130,000 ounces at low costs

Expansion: to 200,000 ounces per year

Forecast production

~130,000 ounces at low costs

Expansion: to 200,000 ounces per year

Open pit upside; Underground potential

New discoveries

High grade structures to augment ore feed

Open pit upside; Underground potential

New discoveries

High grade structures to augment ore feed

Solid cashflow: exploration & development

Strong profits; prudent fiscal management

Solid dividend yield

Solid cashflow: exploration & development

Strong profits; prudent fiscal management

Solid dividend yield

www.kingsgate.com.au

IncreasingProduction/share

IncreasingProduction/share

IncreasingReserves/share

IncreasingReserves/share

Increasing Earnings/share

Increasing Earnings/share

AppendixAppendix

www.kingsgate.com.au

Income Statement -

Solid BaseIncome Statement -

Solid BaseA$ Million

:A$ Million

:

Revenue Gold/SilverInterest / OtherMining CostsInventory (Stockpiles)Employee CostsAdmin, Biz Devel, ConsultD & AFinance CostsExploration / DevelopmentUnrealised FX LossPre Tax ProfitTax (7mths Thai tax)

Profit

Revenue Gold/SilverInterest / OtherMining CostsInventory (Stockpiles)Employee CostsAdmin, Biz Devel, ConsultD & AFinance CostsExploration / DevelopmentUnrealised FX LossPre Tax ProfitTax (7mths Thai tax)

Profit

2008-092008-09

113 4

(70)20

(11)(9)

(12)(2)

--

33-

A$33

113 4

(70)20

(11)(9)

(12)(2)

--

33-

A$33

175 1

(82)28

(12)(9)

(14)(2)

-(3)82 (9)

A$73

175 1

(82)28

(12)(9)

(14)(2)

-(3)82 (9)

A$73

2009-102009-10

55%

8%

--

17%---

148% -

121%

55%

8%

--

17%---

148% -

121%

Asian Competitive Advantage

Established Infrastructure

Grid Power

Sealed roads

Lower cost support

Skilled manufacturing

“Buy Thai”

sourced supplies

Labour –

Skilled & available

Robust Deposit

Simple mining & metallurgy

Safe Mine = Efficient Mine

Safest gold mine globally

Asian Competitive Advantage

Established Infrastructure

Grid Power

Sealed roads

Lower cost support

Skilled manufacturing

“Buy Thai”

sourced supplies

Labour –

Skilled & available

Robust Deposit

Simple mining & metallurgy

Safe Mine = Efficient Mine

Safest gold mine globally

Low Cost DriversLow Cost Drivers

Cost Comparisons – Thailand vs Australia

Open Pit Mining (US$):

Waste:

$1.70/t

vs $2.50/t Ore:

$3.40/t vs $4.00/t

Power:

8c/Kwh vs 20c/Kwh

Assays:

$3/sample vs $20/smp

Cost Comparisons – Thailand vs Australia

Open Pit Mining (US$): Waste:

$1.70/t

vs $2.50/t

Ore:

$3.40/t vs $4.00/t

Power:

8c/Kwh vs 20c/Kwh

Assays:

$3/sample vs $20/smp

Current OperationsCurrent Operations

A East PitA East PitA HillA Hill

A Pit looking WestA Pit looking WestA Pit looking West

K WestK West

K West Pit looking SouthK West Pit looking SouthK West Pit looking South

1st

Millionth oz -

Feb 20101st

Millionth oz -

Feb 2010

Chatree Mine History1993-95 Discovery2000-01 Construct 1Mtpa Plant2001 First gold pour (Nov ’01)2006 Expansion 2Mtpa Plant2008 New Mining Leases2010 1st

millionth ounce

Chatree Mine History1993-95 Discovery2000-01 Construct 1Mtpa Plant2001 First gold pour (Nov ’01)2006 Expansion 2Mtpa Plant2008 New Mining Leases2010 1st

millionth ounce

9 years operatingAv Cash Costs:

US$245/oz

9 years operatingAv Cash Costs:

US$245/oz

World’s Safest Gold Mine*

Zero Environmental Incidents

ISO standards on all activities

Only mining company granted Social Accountability SA8000

Amnesty’s CSR ‘Benchmark’

Training focus -

99% Thai

80% workforce –

local villagers

31% women in management

21 Masters grads -

supported

Created new local industries

World’s Safest Gold Mine*

Zero Environmental Incidents

ISO standards on all activities

Only mining company granted Social Accountability SA8000

Amnesty’s CSR ‘Benchmark’

Training focus -

99% Thai

80% workforce –

local villagers

31% women in management

21 Masters grads -

supported

Created new local industries

Sustainability FocusSustainability Focus

Proven AbilityProven Ability

Opportunity exists to stand-out amongst ASX mid-cap gold producers

Focus on growth in Asia/Australia

‘Critical Mass’

in S.E. Asia

Favourable track record: social/local development & environmental record

Track record of investing in major value creating assets/companies (>3x returns)

Opportunity exists to stand-out amongst ASX mid-cap gold producers

Focus on growth in Asia/Australia

‘Critical Mass’

in S.E. Asia

Favourable track record: social/local development & environmental record

Track record of investing in major value creating assets/companies (>3x returns)