vic ashton 2013

TRANSCRIPT

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 1/31

8th annual Spring value investing congress•

May 7, 2013 • Las Vegas, NV

Dumb and Dumber Zeke Ashton, Centaur Capital Partners

Join us for the 9th Annual New York Value Investing Congress!

To register and beneft rom a special discount go to www.ValueInvestingCongress.com/SAVE

www.ValueInvestingCongress.com

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 2/31

Zeke AshtonCentaur Capital Partners

Learning From Mistakes

Value Investing Congress– May 2013

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 3/31

2

Legal Disclaimer THIS PRESENTATION IS FOR INFORMATIONAL AND EDUCATIONAL PURPOSESONLY AND IS NOT INTENDED AS INVESTMENT ADVICE. NOTHING CONTAINEDHEREIN SHALL CONSTITUTE A SOLICITATION, RECOMMENDATION OR ENDORSEMENT TO BUY OR SELL ANY SECURITY OR OTHER FINANCIALINSTRUMENT.

INVESTMENT FUNDS MANAGED BY CENTAUR CAPITAL PARTNERS (“CCP”)MAY OWN STOCK IN THE COMPANIES DISCUSSED IN THIS PRESENTATION. CCPHAS NO OBLIGATION TO UPDATE THIS INFORMATION AND THE VIEWSEXPRESSED IN THIS PRESENTATION ARE SUBJECT TO CHANGE.

WE MAKE NO REPRESENTATION OR WARRANTIES AS TO THE ACCURACY,

COMPLETENESS OR TIMELINESS OF THE INFORMATION, TEXT, GRAPHICS OR OTHER ITEMS CONTAINED IN THIS PRESENTATION. WE EXPRESSLY DISCLAIMALL LIABILITY FOR ERRORS OR OMISSIONS IN, OR THE MISUSE OR MISINTERPRETATION OF, ANY INFORMATION CONTAINED IN THISPRESENTATION.

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 4/31

3

About Centaur Capital Partners

Founded in 2002; based in Southlake, TX

Centaur specializes in value-oriented investing strategies based onfundamental securities research and analysis

The Centaur investment process emphasizes risk-averse, reliable returns.

Investment advisor to the Centaur Value FundLong/Short (long-biased) private investment partnershipLaunched in 2002

Portfolio manager for Tilson Dividend Fund (TILDX)Launched in 2005Long-only equity strategy that seeks to identify undervalued equitiesand emphasizes income through dividends & covered call options

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 5/31

4

Centaur Value Fund Cumulative Returns

*Returns shown through 3/31/13

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

Centaur Value FundS&P 500

Net Profit of $294,766

Net Profit of $113,383

Value of $100,000 Invested at Inception

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 6/31

5

Mistakes are Inevitable

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 7/31

6

Thoughts on Mistakes

“We are trying to make new and interesting mistakes, not the same stupidones over and over again.” - Jeffrey Bronchik, Cove Street Capital

“ Agonizing over errors is a mistake. But acknowledging them andanalyzing them can be useful” - Warren Buffett

Just when I thought you couldn’t possibly be any dumber, you go out anddo something like this … and totally redeem yourself!” – Harry, after Lloyd trades the van for a moped

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 8/31

7

Categories of Mistakes

EmotionalEXAMPLESShiny New ToyBeer Goggles

Attack of the Analysts

AnalyticalEXAMPLESTrailing 12 Month MirageHubble Effect

The Missing Link

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 9/31

8

Shiny New Toy

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 10/31

9

Shiny New Toy

“This is the best investment ever” syndrome

Similar to infatuation one gets on a first date

Causes chronic over-sizing of new ideas in the portfolio.

Over-weighting of positive attributes; the negative attributes andrisk factors often take time to make themselves known.

We have learned that the most dangerous idea in the portfolio isoften the newest.

“You never really know a stock until you’ve owned it for a year.”

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 11/31

10

Beer Goggles

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 12/31

11

Beer Goggles

Often occurs when good ideas are difficult to find

Typically stems from pressure to keep up with a rising market

Relaxing of standards and discipline

Results in sub-standard ideas entering the portfolio

Stocks that looked ugly 6 months ago look like beauty queenswhen you start to get desperate for ideas.

Can also result in holding on to ideas that should be monetizeddue to concerns about being under-invested.

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 13/31

12

Attack of the Analysts

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 14/31

13

Attack of the Analysts

This occurs when you make what you think is a goodinvestment decision

Negative sentiment becomes overwhelming

Sell-side analysts downgrade the stock and compete with eachother to invent the worst possible scenario.

Idea is pounded in the press; your own investors tell you it’s

stupid.

You finally give in and sell at the worst possible time, and youlook up 24 months later and the stock has doubled.

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 15/31

14

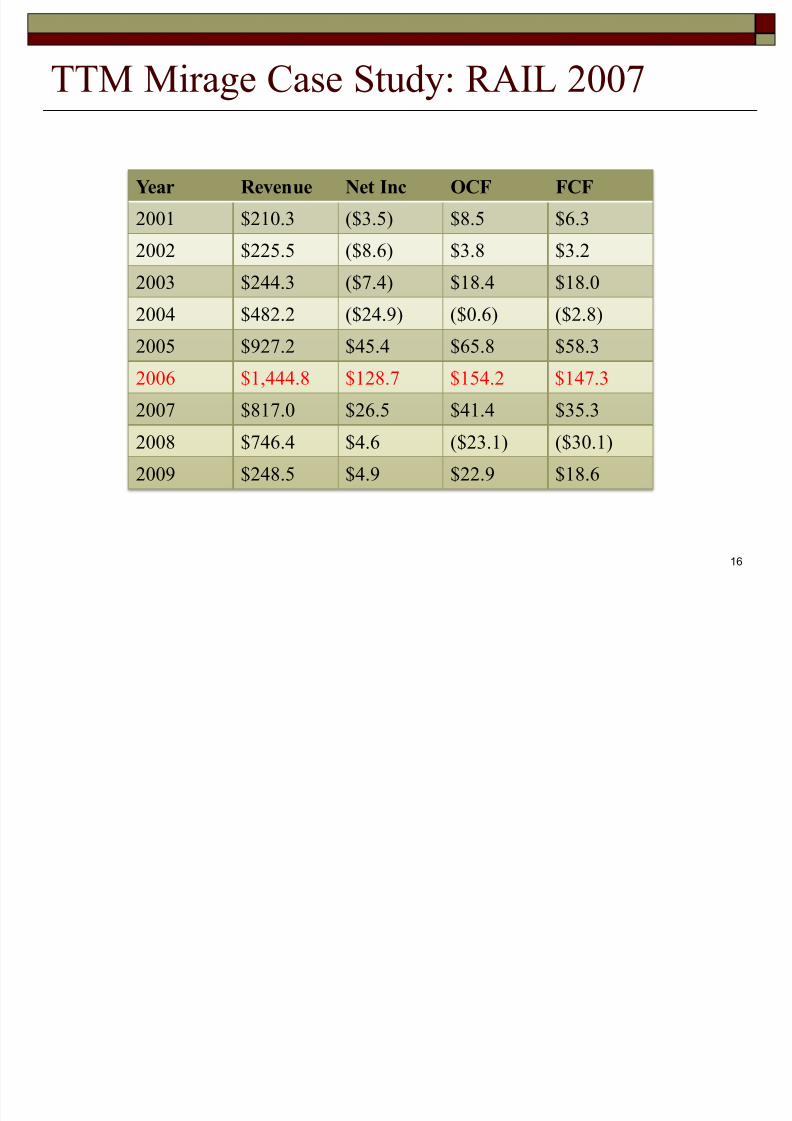

Trailing Twelve Month Mirage

Lloyd : What the hell are we doing here, Harry? We’ve gotta get outof this town!

Harry : Oh yeah, and go where? Where are we gonna go?

Lloyd : I’ll tell you where. Someplace warm. A place where the beer

flows like wine. Where beautiful women instinctively flock likesalmon of Capistrano. I’m talking about a little place called Aspen.

Harry: Oh, I don’t know, Lloyd. The French are so annoying.

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 16/31

15

Trailing Twelve Month Mirage

Caused by the standard investor convention of puttingearnings multiples in “trailing twelve month” context.

For many businesses, the TTM may be a good approximationof earnings power. But it should never be assumed.

Be especially careful valuing variable and cyclical businesses.

Professional athletes have “career years.” Businesses have

“perfect storms.”

Our research template usually starts with a 10 year financialtable so that we can see a fuller history of the business.

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 17/31

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 18/31

17

RAIL Stock Chart 2005-2013

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 19/31

18

The Hubble Effect

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 20/31

19

Occupational Hazards of DCF Models

“If you change the assumptions even a little bit, you can end up in awhole new galaxy.”

Discounted Cash Flow analysis is a very useful tool, but limitationsmust be acknowledged. Best to use DCF as a sanity check and

“what -if” scenario generator.

Occupational Hazards of DCF models

DCF assumes all generated cash is returned to investors

If cash isn’t returned to investors, consideration must be givento the uses of that cash.It is easy to anchor on a DCF number “False precision” and illusion of rigor

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 21/31

20

The Missing Link

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 22/31

21

The Missing Link

Often occurs in net asset value or “sum -of-the- parts” analysis Particularly common when valuing natural resource & realestate companiesBut can also easily happening when valuing companies withmultiple business units.

Missing Variables from Analysis:TimeDelta between asset inflation and investor hurdle rateFrictional Costs (taxes, costs to develop assets)Operating Costs and Management Comp (value leakage)

We often apply a multiple to corporate overhead as part of our sum-of-the-parts and NAV analysis. We tend to use a multiple of 5-9X

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 23/31

22

Missing Link Case Study: JOE Late 2009

Enterprise Value of ~$2.5 billionBull argument: 585,000 acres, implied EV / acre of ~$4,30035,000 acres surrounding new airport development at $60K

per acre = $2.1 billion;Coming real estate recovery and low borrowing costs

Missing Variables from Analysis:

50-75 years that will be required to sell down assets.JOE needed to spend money on developmentCorporate expenses were ~$25 million / year Delta between assumed 3% inflation rate and 10% hurdlerate over 50 years

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 24/31

23

JOE: How the Math Works

Enterprise Value of $2.5 billion585,000 acresJOE sells 11,700 acres / year for 50 yearsLet’s pretend they get $10K / acre in Year 1 and every year thereafter they get an inflation-adjusted $10K We used 3% for inflation.First year revenue: $117 millionYear 50 revenue: $498 millionWe assume zero operating costs and zero taxesBUT……….. We discounted back the resulting revenue at 10% rateResults in EV of $1.6 billion ($17.50 stock price on 92M shares )

NOTE: We have no investment opinion on JOE. This is just amathematical thought experiment to illustrate the Missing Link

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 25/31

24

JOE Stock Chart 2008 -2013

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 26/31

25

Final Thoughts on Mistakes

QUESTIONS TO CONSIDER Do you have a defined process for making decisions?Do you analyze your bad outcomes to pinpoint possible mistakes?Do your mistakes tend to fall on the emotional side or the analyticalside most often?ACTIONS TO CONSIDER Finalize research / make initial new major purchase decisionsoutside market hours.For each stock you own, indicate a price at which the next actionshould be taken or contemplated (add, trim, or sell).For each stock you have researched, indicate a price at which youwould consider taking action (i.e., “trigger price”) Make an effort to differentiate process and outcome. Not all badoutcomes are due to mistakes.Accept mistakes as part of the learning process.

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 27/31

26

Intriguing Play on a Real Estate Recovery

A lower-risk way to play the real estate recoveryTitle insurers are almost like a royalty on real estate activity.Rational industry with only four major playersTop two players comprise 60% market share and ~80% profitshare.Title companies are leveraged to both increases in volume andincreases in prices.Also provide escrow services, closing documentation, andother real estate-related services.

Title insurers get paid on virtually every real estate transactionin the United StatesMortgage Refinancing - $1,000 avg. premiumHome sale (new homes or existing) - $2,000 avg. premiumCommercial property ($7,800 avg. premium)

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 28/31

27

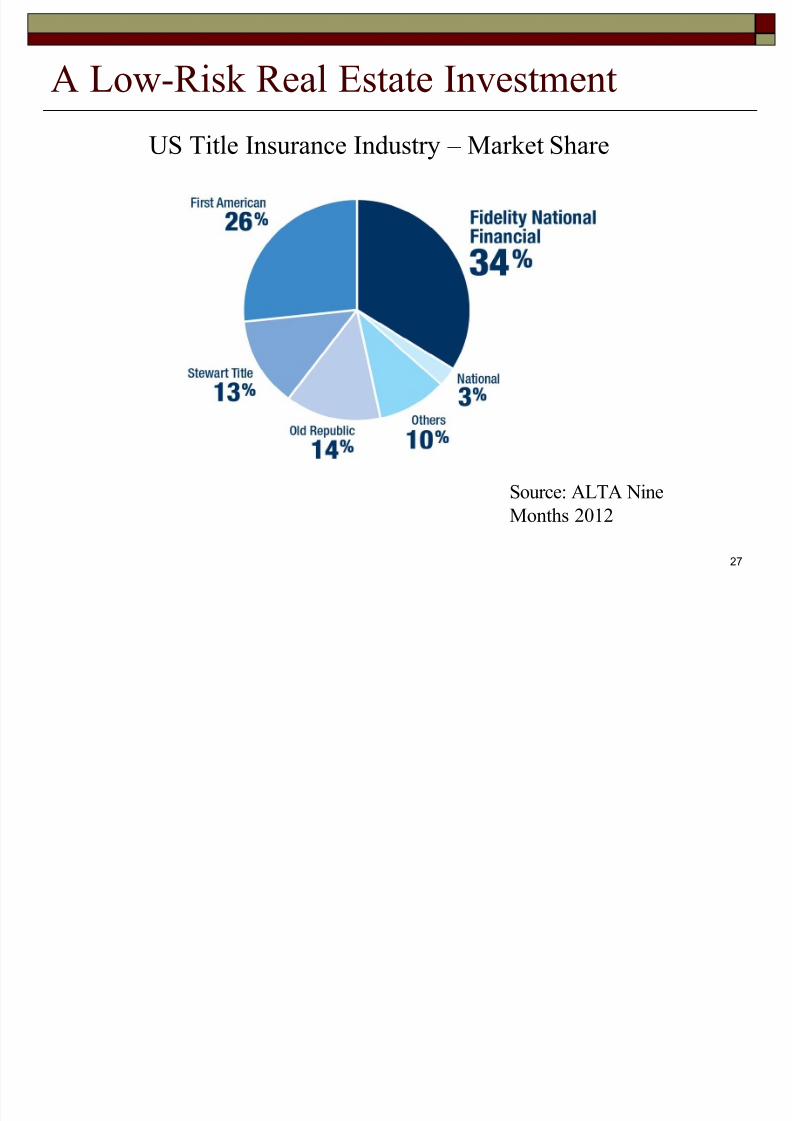

A Low-Risk Real Estate Investment

US Title Insurance Industry – Market Share

Source: ALTA NineMonths 2012

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 29/31

28

The Tale of the Tape

Market and valuation data as of May 2, 2013

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 30/31

29

Which One Is Better?

FAF is more of a pure-play on title insurance / escrowFNF has a side business of LBO-type investments(restaurants, Remy auto parts, Ceridian, timber, etc).FNF has historically been the industry profitability leader.FAF is improving operating efficiency and is a strong #2.Importantly, neither carries leverage typical of most real estateinvestment vehicles at insurance subsidiaries.FNF has significant leverage in its private equity portfoliocompanies.

FAF is a leader in international title insurance, which isstarting to become more common outside the U.S.My preference currently is for FAF; but I expect that both willwork out if real estate transaction volumes and pricesimprove.

7/28/2019 VIC Ashton 2013

http://slidepdf.com/reader/full/vic-ashton-2013 31/31

Zeke Ashton

Centaur Capital Partners

Q & A