vietnam grocery report annual updateannual updates3.amazonaws.com/zanran_storage/... · vietnam...

TRANSCRIPT

Vietnam Grocery ReportAnnual UpdateAnnual Update

August 2010August 2010

Vietnam Grocery Report

Executive Summary• Vietnam to continue displaying great promise over the next

10 years

– Young population (56% under 30) will join the workforceg p p ( ) j– High confidence towards country, economy & social life– Modern Trade continues to emerge while Traditional Trade is still

dominant– Majority of population comes from rural (>70%) where it has shown

strong growth in recent yearsg g y– Consumers become more sophisticated & demanding through their

wider product choice, concerns on health & beauty and smarter shopping way

– People are getting more connected through technology

However these opportunities come with challenges for• However, these opportunities come with challenges for businesses and investors alike

– Health concerns caused by air/water population and pesticides that could be an area for PR executionAbilit t th d i d di i i t Vi t

2

– Ability to cover the dynamic and discriminate Vietnamese consumer needs

– Rural would be a mystery land to explore the potential expansion

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Agenda

• Vietnam Heating UpA young country with positive economic indicatorsy g y

• Retail LandscapeHigh sales & store growthg gFMCG Snapshot

• Vietnamese Consumer InsightsVietnamese Consumer InsightsCapturing different consumer shopping behaviors

• New Trends

3

New TrendsAs the competitive market is always changing, new trends emerging

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Vietnam Heating Up

•56% of total population is under 30 years old

•GDP grows in both urban & rural

•Vietnam re-gains confidence index in Q2.2010 and ranked # 2 top confident countries in Q2.2010

•Business leaders show high expectation to their business conditions

4

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Vietnam country facts

Vietnam NotesVietnam Notes

Population 2009 86 millions

Male 2009Female 2009

42.6 millions (49.5%)43 4 millions (50 5%)

Hanoi

Female 2009 43.4 millions (50.5%)

Urban 2009Rural 2009

29.6%70.4%

Haiphong

Population growth rate 2009 1,06%

GDP growth rate 2008GDP growth rate 2009

6.3%5.3%

Inflation rate 2009 6.8%

Danang

Nhatrang

Key cities: •Ho Chi Minh (Economic capital)•Hanoi (Political capital)•Haiphong

CanthoHo Chi Minh

Nhatrang

5Source: Statistical Handbook of Vietnam 2009

Haiphong •Danang (the “bridge”)•Nhatrang •Cantho

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Statistical Handbook of Vietnam 2009

In Vietnam, growth is seen across measurable factsGDP Growth Inflation Wage GrowthUnemployment

+6.2%2008

+ 8.5%2007 +8.5%2007

+23%2008

+11.22007

+42008

5.1%2007

4.3 %2008

+5.3%2009 +6.9%2009 +1020092.9 %2009

+5.5%2010E +10%2010E <5 %2010E +12.32010E

Consumer ConfidenceFMCG Volume Growth

13%15%

+ +

118 106 97 85109 101

11910%

13%

++

6

2007 1st Half'08

2nd Half'08

1st Half'09

2nd Half'09

1st Half'10

2nd Half'10

▼12 t

▼9 t

▼12 t

▼8 t

▲24 t

4%

2007 2008 2009 MAT Jun10

+

▲18 t

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

12pt 9pt 12pt 8pt24pt•Sources: Wage growth, 2007 Economic Intelligence Unit , 2008-9 HRBS Asia-Pacific Pay Increase Guide 2009 (Survey Period: Jan 6 to Feb 6, 2009); 2010E by Vietnam government ; Consumer Confidence, Nielsen Global Online Survey 2007-10; GDP Growth ; Inflation, 2006-2007 data from IMF; And CIEC: 2008-2010 IMA Asia Brief December 2010; Asia Development Bank Outlook 2010 , 2010E by Vietnam government; ; FMCG Growth, Nielsen; Vietnam Retail Audit.

18pt

Vietnam shows sharp consumer confidence re-gains and is ranked #2 top confident country in Q2.2010

160 Changes 2H10 vs.1H10

2H 2010 Nielsen Consumer Confidence Index

2 3 18 2 -2 5 1 -3 -1 5 2 2 -2 1 0 5 1 4 3 5 2 2 -3 5 4 3 2 3 2 -2 -1 -1 7 2 -2 -17 -1 3 -4 -10 1 4 -5 -1 6 0 1 6▲ ▲ ▲ ▲ ▼ ▲ ▲ ▼ ▼ ▲ ▲ ▲ ▼ ▲ ▲▲▲▲ ▲ ▲ ▲ ▼ ▲ ▲ ▲▲▲ ▲ ▼ ▼ ▼ ▲▲ ▼ ▼ ▼ ▲ ▼ ▼ ▲▲ ▼ ▼ ▲ ▲ ▲

Vietnam, 2nd most confident

113108 105

101 99 98 98 98 97 97 97 94 93 92 92

119119113 112109 107

102 101

129

88100

120

140

Global average

▲ ▲ ▲ ▲ ▼ ▲ ▲ ▼ ▼ ▲ ▲ ▲ ▼ ▲ ▲▲▲▲ ▲ ▲ ▲ ▼ ▲ ▲ ▲▲▲ ▲ ▼ ▼ ▼ ▲▲ ▼ ▼ ▼ ▲ ▼ ▼ ▲▲ ▼ ▼ ▲ ▲ ▲

94 93 92 9288 88

79 78 7873 73

69 6863 6165

595556 52

88 87 8785 84 84 81

71

60

80

100

93

20

40

7

0

IN ID VN PH NO SG CN AU BR CO CA HK AE MY NZ DK IL SE NL CH PK AR TH MX ZA PL RU FI US AT BE TW DE UA GB EG CZ TR IT ES IE HU FR EE LV KO JP LT

Base : All respondents n=26995

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

A ‘young’ population means an increase in purchasing power as it joins and progresses in the workforce

80+

FemaleMale Vietnam 2009Total Vietnam Population

55 - 5960 - 6465 - 6970 - 7475 - 79 Population under 30 years old: 56%

30 3435 - 3940 - 4445 - 4950 - 54

5 910 - 1415 - 1920 - 2425 - 2930 - 34

8General Economy: PopulationSource: U S Central Bureau International Database

0 1,000 2,000 3,000 4,000 5,000

0 - 4 5 - 9

010002000300040005000

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: U.S. Central Bureau, International Database

This workforce will further fuel the GDP Per Capita in the coming years

GDP Per Capita (in USD)Labor force (‘000 individuals)

50,000

60,000

1,0241,074

1,200

20,000

30,000

40,000

402 440552

725835

0

10,000

,

00 02 04 06 08 10 12 14 16 18 2000 2002 2004 2006 2007 2008 2009 Expected

9

200

200

200

200

200

201

201

201

201

201

Labor force ('000 individuals)

Source: Government’s General Office of Statistics (www gso gov vn)

2000 2002 2004 2006 2007 2008 2009 Expected2010

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Government s General Office of Statistics (www.gso.gov.vn)

Leaders show high growth expectations towards the Vietnam economy and their own business condition

What do you think GDP growth rate will be for the next 12 months?What do you think your industry growth rate will be for the next 12 months? 100%

What do you think your company growth rate will be for the next 12 months?

next 12 months?

10.2

11.3

13.6

12

14

2010 1st half

2009 1st half 2009 2nd half

17

2131

80%

25%+

21% - 25%

5.76

8

10

% 20

17

23

11

40%

60%16% - 20%

11% - 15%5.0

5.74.9

2

4

6

17 14

1712

20%

40%

6% - 10%

Less than 5%

10

0

2

Est. Next 12 months GDPgrowth rate

All industry est growth rate

4 50%

2009 2nd half 2010 1st half

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Nielsen Business Barometer

The workforce numbers and advertising spending are expected to increase to a good degree

4100%

Over the next 6 to 12 months, how do you anticipate your company's work

force numbers to change?

7 2100%

Over the next 6 to 12 months, how do you anticipate your company's spending on

advertising to change?

31

411

80%

Increasesignificantly(5)

Increaseh t (4)

32

7

4380%

Increasesignificantly

Increase

4660%

somewhat (4)

Remain thesame (3)

29

60%

somewhat

Remain thesame

53

3020%

40% Reducesomewhat (2)

Reducesignificantly(1)

21

43

20%

40%

Reducesomewhat

Reduce

11

1 211 2

0%

2009 1st Half 2010 1st Half

(1)

122

110%

2009 1st half 2010 1st half

Reducesignificantly

S

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Nielsen Business Barometer

Retail Landscape

•Modern Trade continues emerging from both sales & store growth while Traditional Trade is still dominantwhile Traditional Trade is still dominant

•The majority of Vietnam population lies in rural areas (74%) which also contributes biggest to FMCG sales (46%)

•The main purchasing power still comes from the 6 urban cities (only 14% population generates 39% FMCG sales) and continues to develop at the fastest rate

•Beverage & Food products are growing the fastest

12

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Retail Structure Change

13

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

The leading 6 cities account for 37% of Vietnam FMCG sales. Rural areas provide greater FMCG contribution to total Vietnam’s sales as this i h j it f th l ti li

National FMCG Retail Market Structure

is where a majority of the population lie

100

57

9

1425

39 3780

100

6 CITIES

7461

5

4

14

11 22

40

60 30 CITIES

53 CITIES61

46

27

0

20RURAL

14

0Population 2007 Store 2009 FMCG ACV 2009 Retail Sales

Estimated

Source: Six City, 30 cities and Rural store numbers and ACV (store turnover) from census results, 53 Cities estimated. Population, Retail Sales

(FMCG sales + Other retail sales such as Durable goods) from

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Page 14Page 14

(FMCG sales + Other retail sales such as Durable goods) from Government Statistics 2006

Both urban and rural are on a strong growth trend, yet there is still a great room to develop rural area further

Urban and Rural Growth GDP Per Capita

136%

145%151%

157%

137%Urban

104%109%

114%119%

127%

106% 109%113%

117% 120% 123%127%

UrbanRural

100%104%

100% 102%106%

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009E

15

2

S G S Off

Growth rate is calculated based on constant prices 1994 excluding inflation.

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Government Statistics Offices

Business leaders also plan to expand their business to rural areas

131817

100%

In the next 12 – 18 months, to what extent will you look to rural Vietnam areas to drive your company growth?

1817

80%

Increase significantly

Increase somewhat

51

5358

40%

60%

Neither increase nor decrease

32

2526

20%

Decrease somewhat

Decrease significantly

16

4 20%2009 1st half 2009 2nd half 2010 1st half

g y

S

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Nielsen Business Barometer

Within channel types, Off-Premise continues increasing both in store numbers and sales especially in urban cities, which indicates an opportunity for in home consumption products

Off Premise On Premise

Store number (000s) by tier

+3%

FMCG Value % Contribution by tier

opportunity for in-home consumption products

+3%

+2%47% 46%

+14% +3%

+12% 1%447 458

267 264

11% 9%5% 4%

47% 46%

+14%+15%

+12%

+5%+3%

-1%

133 138 151 161

52 53 48 5130 30 29 29

38% 41%+19% +8%

17

2008 2009 2008 2009

S C

Off Premise On Premise

6 Cities 30 Cities 53 Cities Rural VN% Growth vs. YA

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Nielsen Retail Census 2009

Modern Trade grows fast through store numbers and overall sales per store, while Traditional Trade is still dominating. On-Premise is more skewed towards Café and Eatery

2009 St% Store

th% ACV

th 2009 St% Store

th% ACV

th

Store number and ACV growth by channels in Off and On channel in Vietnam

skewed towards Café and Eatery.

2009OFF PREMISE

Store Number

growth vs. YA

growth vs. YA

Modern Trade 752 45 63

Trad. Grocery 501,135 6 16

2009ON PREMISE

Store Number

growth vs. YA

growth vs. YA

Café 241,478 4 3

Eatery 171,673 4 8

SStreet Vendor 10,717 -23 -19

Personal Store 19,055 3 4

Market Stall 83,700 -4 0

Cosmetic Store 893 -9 -4

Sidewalk Eatery 10,068 -3 -1

Res. Vietnamese 9,826 -2 0

Billiard Centre 11,659 -27 -22

Karaoke 6,537 -15 -4

Beverage Store 19,327 6 0

MBS 1,566 -36 -24

Cigarette Kiosk 20,602 -14 -29

Ph 15 518 0 9

Others 52,802 -4 -1

Note: ACV = All Commodity Value (Store turnover)

18

Pharmacy 15,518 0 9

Other 6,130 1 3

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Nielsen Retail Census 2009

In 2009 shoppers only slightly increased their store repertoire

2008 2009

Number of Supermarket/ Hypermarket Used – Stores Used in Past 4 Weeks

32

54

2 stores

1 store

36

46

3

9

4 t

3 stores

4

13

1

3

5 stores

4 stores

1

4

19

1.66Average/(shops) 1.80

Base: All Supermarket/Hypermarket shoppers (2008 n=1494, 2009 n=1466)

S S

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Nielsen Shopper Trend 2010

There has been no increase in the number of supermarket visits yet consumers have increased spend per visit in the MT channel.

Average Frequency of Visits per month Trade Sectors Where Shoppers Spend the Most Money

1.2

1.4Hypermarkets

2

5 Hypermarkets

3.3

3.3Supermarkets

2008 2009

21

43 Supermarkets

28.1

25.2Wet Markets

77

51 Wet Markets

20Source: Nielsen Shopper Trend 2010

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Nielsen Shopper Trend 2010

The increased spend probably comes from a higher % of fresh foods being purchased from Modern Trade versus last year

Supermarket Cont. % (2008 report)

Place of Most Often Purchased by Category

7% 9% 7%

277

4 4 1 4 1 61

1819

5 2 2 11 2 2

80

100 Others

Confectionery Shops

% (2008 report) 7% 9% 7%

5663 60

78 81 8154

5360

40

60Wet market

Liquor Stores

13 15 1619 17 17

24 32

56

2920

40

Traditional Grocery

Supermarkets

21

4 2 2 8 7 134

15 16

0Fruit &

vegetablesMeat orpoultry

Fish orseafood

Snack CSD Dairyproducts

AlcoholicProducts

Personalcare

products

Householdcleaningproducts

Supermarkets

Hypermarket

S S

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Nielsen Shopper Trend 2010

This can explain why 2010 seems to be the year when manufacturers look for more contribution from Modern Trade

Modern Trade Contribution to Sales Revenue

2010 1st h lf

Question: How important is the modern trade to your business today (as a % of your business’s revenue)? What do you expect MT (as a % of your revenue) to be worth by the end of the year?

13

13 15

15

2009 2nd half15

210

27

2010 1st half

23 21

15

46

29

27

2620

2530

22 17

1215

22

Now End of '09 Now End of '10

Less than 5% Less than 10% Less than 20%Less than 30% 30% or greater

S

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Nielsen Business Barometer

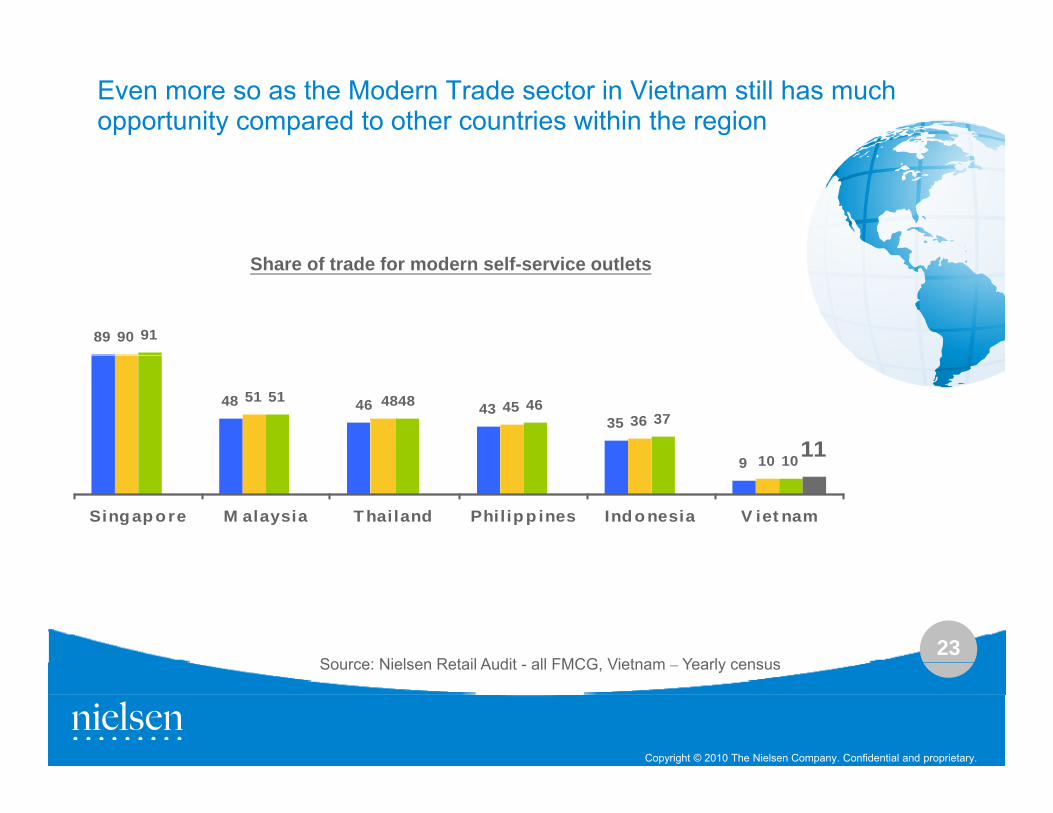

Even more so as the Modern Trade sector in Vietnam still has much opportunity compared to other countries within the region

89 9190

Share of trade for modern self-service outlets

48 4335

9

5145

36

10

51 48 4637

1011

46 48

9 10 10

Singapore M alaysia Thailand Phil ipp ines Indonesia V iet nam

23Source: Nielsen Retail Audit all FMCG Vietnam Yearly census

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Nielsen Retail Audit - all FMCG, Vietnam – Yearly census

FMCG Snapshot

24

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Nielsen Vietnam Tracked Categories

PERSONAL BEVERAGE HOUSEHOLD FOOD MILK BASED CIGCARE

Hair Conditioner

BEVERAGE

Ready ToDrink Tea

CARE

Laundry Product

FOOD

Biscuits

PRODUCTS

SweetenedCondensed Milk

CIG

Cigarette

Personal Wash

Toothbrush

Soft Drink

Packaged

Household Insec. Aerosol

Household

Gums

Instant Noodles

Cooking Oil

Milk Powder

Ready ToDrink Milk

Shampoo

Body Cream Lotion

Energy Drink

PackagedWater

Fabric Softener

Insec. Coil

MSG-Bouillon

g

Sauces

Deodorants

Toothpaste

Facial Care Products

Tonic FoodDrink

Fruit Juice

Dishwashing Liquid

Household Cleaners Snack

25

Products

Repellent

Feminine Protection

Tea Bag Tissue

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Value consumption increases across super groups with a positive picture from Beverage products

FMCG VALUE CONTRIBUTION - 6 CITIES TT

MAT JUN09 MAT JUN10

MATLY MATTY

MAT JUN09 MAT JUN10

Value % Chg YA

Volume % Chg YA

T t l FMCG 15 15Total FMCG 15 15

Personal care 10 3

Household care 13 5

Milk Based Product 6 8

26S

Food 11 11

Beverage (excluding Beer) 29 22

Cigarette 16 8

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Vietnam Retail Audit Tracking, ended period Jun2010

Beverage and Food categories are dominating both importance and growth

TOP FASTEST GROWING CATEGORIESTop 10 biggest categories – Value % Share Top 10 fastest growing category - value % Chg vs. YA

MATTY

TOP FASTEST GROWING CATEGORIES

27S

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Nielsen VN Retail Audit Tracking, ended period Jun2010

Vietnamese Consumer Insights

•67% of total consumers expenditure is on Fresh Food

•Most of consumers (64%) are aware of price changes and are looking for more promotions while rarely looking for new things. s

•“Vietnamese people use Vietnamese products” campaign might have created an advantage for local products to firm up better share position

28

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Fresh food still represents the major spend bucket, consistent across income levels

Average Monthly Spending on Food, Grocery & Personal Care vs. Fresh Food by social class

3 154 3,243

3,839Total Expenditure ('000 Dong) Fresh Food ('000 Dong)

66%3,154

2,411

,

2,098 2,180

2,58767%

67%

63%66%

1,549

29S Sh T d 2010

Total Low Medium High

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Shopper Trends 2010

Dynamic changes in Vietnam are afoot. After ‘premium trade-up’ & ‘promotional-junkies’, a ‘purchase Vietnamese’ trend is expected.

Do you anticipate that Vietnamese consumers will change their purchasingDo you anticipate that Vietnamese consumers will change their purchasing behavior next 6 to 12 months?

2009 2nd half2009 1st half 2010 1st half

57

54Change channel to

save money

Trade up to morepremium/indulgent

products48

31Trade down to

cheaper products

Purchase more onpromotion

49

44Buy bigger packs

to save money

Purchase morelocal/ Vietnamese

brands

39

51

Buy bigger packsto save money

Buy smaller packsof the same

products

y

24

27

Buy bigger packsto save money

Not buy some 'non-essentials'

p p

37

41

Change channel tosave money

Purchase more onpromotion

23

36

Trade down tocheaper products

Purchase more onpromotion

y

16

21

Change channel to

Buy less / smallerpacks of the same

products

to save money

22

22

Trade up to morepremium/indulgent

d t

Not buy some 'non-essentials'

30

5Not buy some 'non-

essentials'

p p

16

16

Trade up to morepremium/indulgent

products

gsave money

22Trade down tocheaper products

products

Source: Nielsen Business Barometer

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Nielsen Business Barometer

As already evidenced by strong share gains amongst some Vietnamese brands

Fastest Volume % Share Gain – 6 cities-TT

(+/- Volume % Share Change YA – MATTY)

Dr. Thanh

(Ready to Drink Tea)

Vinamilk Fresh Milk

(Liquid Milk)

Diana Sieu Tham

(Napkin)

Vinh Hao

(Carbonate Soft drink)

+7.3 pts +6 pts +3 pts +2.4 pts

31S Ni l VN R t il A dit l t t i d J 10

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Nielsen VN Retail Audit –latest period Jun10

Highly aware of price, Vietnamese consumers remain fairly loyal to their favorite brand, but are attracted to in-store promotions & new items.

Shopping Dynamics

PROMOTIONSENSITIVITY

PRICEAWARENESS ADOPTION

11% Changes stores based on best 64% Vietnamese consumer are f i h

20% seldom try new thingspromotion offered

55% Seldom change stores but when shopping, actively searching for promotions

aware of price changesy g

65% try new brands/things but usually stick to my favorite

32

promotions

S S

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Nielsen Shopper Trend 2010

However consumers behave differently in different regions

HanoiHCMC

• The role of advertising is more critical. Hanoians also claim to respond better to in store promotions and after sales service

Promotion • Saigonese consumer favor multiple promotion types

• Hanoian strongly prefer one type of promotion: PRICE

Price • Price promotions alone won’t appeal to Saigonese

33

• Hard to build initial trial (1 in 10 people from HN are early adopters)

Adoption • Saigonese are early adopters (1 in 5 people from HCMC are early adopters

S C C & ff

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Nielsen HCMC & HN consumer differences Jun09

Emerging Trends

34

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Emerging trends in summary

Getting sophisticated

Getting Connectedsophisticated Connected

Convenience(4)

Health &

PrivateLabel

(3)

Health &Beauty

Big Pack(1)

Refill(2)

35

(1)

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Smart shopping:(1) Consumers are upsizing

Do you anticipate that Vietnamese consumers will change their purchasing behavior in next 6 to 12 months?

Purchase more

Total 6 cities_TT

+/- Volume % Share vs. YA - MATTY

49

44Buy bigger packs

to save money

Purchase morelocal/ Vietnamese

brands Fabclean>2Kg Granules

>300gm

37

41

Change channel tosave money

Purchase more onpromotion +3% pts

>300gm

+2.1% pts

22

22

Trade up to morepremium/indulgent

products

Not buy some 'non-essentials'

Skin Cleaning >400ml

7 4%

36

22Trade down tocheaper products

products

Source: Business Barometer Wave 3 (Q2 2010) Nielsen VN Retail

+7.4% pts

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Business Barometer Wave 3 (Q2.2010), Nielsen VN Retail Audit – latest period Jun10

Smart Shopping: (2) Consumers buy more refill for money-saving purposes

Total 6 cities_TT

+/- Volume % Share vs. YA - MATTY

Fabric Softener

+4.8% pts DishwashingLiquid

+0 4% pts+0.4% pts

Floor Cleaner

37

+4.2% pts

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Nielsen VN Retail Audit, latest period Jun10

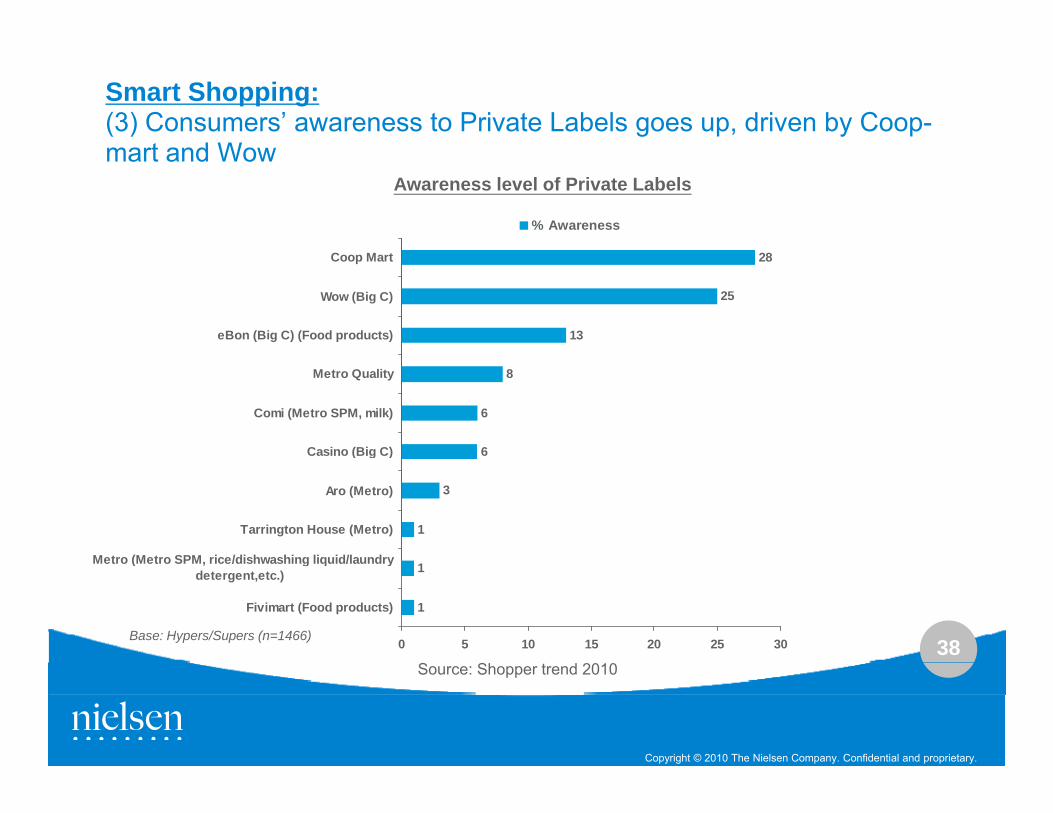

Smart Shopping:(3) Consumers’ awareness to Private Labels goes up, driven by Coop-mart and Wowmart and Wow

28C M t

% Awareness

Awareness level of Private Labels

13

25

28

eBon (Big C) (Food products)

Wow (Big C)

Coop Mart

6

6

8

Casino (Big C)

Comi (Metro SPM, milk)

Metro Quality

1

3

Metro (Metro SPM rice/dishwashing liquid/laundry

Tarrington House (Metro)

Aro (Metro)

( g )

38

1

1

0 5 10 15 20 25 30

Fivimart (Food products)

Metro (Metro SPM, rice/dishwashing liquid/laundrydetergent,etc.)

Base: Hypers/Supers (n=1466)

S Sh d 2010

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Shopper trend 2010

Smart Shopping:(4) Ease of access and consumption is driving channel and product choiceschoices

Choice of place

Choice of product

Derived Importance Ranking of Supermarket Store Attributes

p p

Package Contribution – Ready to Drink Beverage

0.52 Convenientto get to

Wide range0.40

Wide rangeof fresh meat

& fish

Hi h li

39

0.38 High qualityfresh food

Source: Nielsen Shopper Trend 2010 Nielsen VN Retail Audit –

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Nielsen Shopper Trend 2010, Nielsen VN Retail Audit latest period Jun10

Getting Sophisticated:At the same time, consumers show more interest in personal care by using more advanced productsusing more advanced products

29% (17%)

Value % Growth (Volume % Growth)Total 6 cities_TT - MAT TY

Deodorant 29% (17%)

Lotion 39% (32%)

Hair 18% (17%)

40

Treatment18% (17%)

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Nielsen VN Retail Audit, latest period Jun10

Getting Sophisticated (continued):Consumers also start seeking specific product benefits

Specific

Feminine Protection

Specific products for

maleDeodorant Shampoo

41Source: Nielsen VN Retail Audit latest period Jun10

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Nielsen VN Retail Audit, latest period Jun10

Getting Sophisticated (continued):More products are becoming non-exclusive. No matter what industry you’re in Tickle women with a price discount and assure men ofyou re in…Tickle women with a price discount and assure men of quality Important shopping considerations

78Product

LipcareLipcareBody

Life InsuranceLife InsuranceLaptop/PC

78

59

70

48

Productquality

Durability

BeerWine

CigarettesCigarettes Anti-shadow eyes cream

Moisturizer

Body cream/ lotion

Credit cardsCredit cardsp p

TVsMobile phonesMobile phones Bar

Soap

ToothpasteToothpaste

40

9

25

19

Functions

Vietnamesebrand

RazorsRazorsWine

Hygiene Hygiene washwash

Sun blockShampoo Soap

DeodorantsShower gel Facial Facial

CleanseCleanseHair

Beer

6

6

15

31

After saleservices

Discountedprice

MalesFemales

42

rrMilkConditioner2

17Promotions

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Nielsen Study on Gender Difference Jun10

Getting Connected (continued):Vietnamese consumers are the savviest on technology products

% of respondents who spend on new technology products

4741

37 36 35 33

%

Question: Once you have covered your essential living expenses, which of the following statements best describes what you do with your spare cash: I spend on

36 3528 28 27

2419 18 15 13

8

33

8

VN CN ID IN PH SG TH HK MY TW AU NZ JP KO APAverage

43

g

Base : All respondents n=7014

Source: Nielsen Global Omnibus study

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Nielsen Global Omnibus study

Getting Connected (continued):Internet and social networks are very important for the younger generationgeneration

% Access Internet

64

41

HCM+HN 18-25 yearsold

44Source: Nielsen Omnibus April09 Nielsen Gen V Study Oct 2009

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Nielsen Omnibus April09, Nielsen Gen V Study Oct 2009

Getting Connected (continued):The internet could be the next media platform apart from other traditional media forms media forms

411

211

4 5 2 2 7 2100%

Over the next 6- 12 months, how do you anticipate your company's spending on the following media channels for advertising?

34 25

29 2027 30

34

1111

36

80%

Increase significantly

Increase Somewhat

2

9

2 230

32

43 3930

40%

60% Remain the same

Reduce somewhat

27 34

59

25

5922

2

11

7

9

5 182

36

20%

40%

Reduce significantly

No spending on thischannel

45

27

720

925

4 2

0%TVC Point-of-Sale-

MaterialsOutdoor posters In-store

banners/postersPrint

PublicationsRadio Internet Mobile Phone

channel

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Nielsen Barometer Wave 3

Health & Beauty:Health continues to be a key concern for Vietnamese consumers

Top 5 consumer concerns

1) Health

Major Concerns over the next 6 monthsHealth - Top 10

1) Health

2) Increasing food prices %

Biggest concern Second biggest concern

3) Increasing utility bills (gas, electricity, water…)

4) J b it

$24

1316 14 15 14 14 10 13 12 15

4) Job security

5) Increasing fuel / petrol prices

2415 15 14 13 16 12 12 913

VN CN CZ HK PL RU IL HU UA BR

46Source: Nielsen Business Barometer Nielsen Consumer Confidence

Which of the following issues concern you in terms of the impact they may have on your business? Rank the top three issues that concern you where 1=most concern, 2=second most concern, etc...

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Nielsen Business Barometer, Nielsen Consumer Confidence

Health & Beauty (continued):Vietnam is ranked as most concerned country when it comes to air pollution and use of pesticidespollution and use of pesticides

% of global consumers concerned about air pollution

100

% of global consumers concerned about use of pesticides

21 2234 39 37

24 2715

2839 45

3144

3080

100

3243 43

23

4331

80

100

77 7664 58 60

73 7081

6857 51

6552

6640

60

59 6251

43 43 46 40 46 51

40

60

57 51 52

0

20

ID PH GR HK MY CO VE VN CL VN SG TH RO MX

47 44 40 3651

41 35 30

0

20

GR FR TH VN VE PH LT MX AT ES

47Source: Nielsen 2H 2009 Global Omnibus Study

Very concerned Quite concerned

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Source: Nielsen 2H 2009 Global Omnibus Study

Health & Beauty (continued):Vietnamese consumers seek natural and safe products

Toilet Cleaner: Fabcon: Bar soap: Green Tea Ingredientso et C ea eVim killing germs

abcoComfort Antibac

a soapLifebuoy killing bacteria

Green Tea Ingredients

L'occitane

Instant noodles: Instant noodles: Cooking Oil:

48Natural Products

Instant noodles:Omachi made by potato

Instant noodles:Tien Vua good for health

Cooking Oil:De Nhat good for health

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Health & Beauty (continued): Most companies’ corporate social responsibility programs are geared towards supporting consumer health

Does your company currently have any initiatives relating to social responsibilities such as: the environment, local charities,

Which social responsibilities initiatives does your company prioritize?

towards supporting consumer health.

3945

5363 67

, ,education...?

11%

2939

Z

Top 3 Box Priority

Control/reduce carbon-dioxide emission Environmentally- friendly packaging

Energy saving Education

Ch it C h lth b fit

89%

49

Charity Consumer health benefits

Yes No

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Vietnam Topline1st 2nd 1st 2nd1st

Half 2009

2nd

Half 2009

1st

Half 2010

2nd

Half 2010

Nielsen Market Index Volume* Volume growth records high & stable levels

Nielsen Market Index Value**

MFR outlook of the market

Value growth remains high

Manufacturers continue to see Vietnam as a growing market

MFR outlook of own industry

Advertising Spend

Own industry will also experience growth

Advertising levels are expected to pick up

Hiring levels

Modern Trade importance

Ni l Vi t

MT contribution expected to increase in 2010

Most manufacturer’s plan to significantly increase their hiring levels

C fid h b d b k t

50

Nielsen Vietnam Consumer

Confidence^

Very Strong Growth: >= +5% Neutral: between -1 and +1%

Negative: between -1% and -4%

%

Consumer confidence has bounced back to top 3 countries

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

* Nielsen Market Index Volume defined as unit change vs. YAGO** Nielsen Market Index Value defined as dollar change vs. YAGO^ Nielsen Global Consumer Confidence measure is from 10/08 & is benchmarked vs. the Global Confidence avg. of 84

Growth: between +1 and plus 4% Very Negative: <= -4%

Food for thought…

Growth is still on the radar for Vietnam with a number of areas to keep in mind:

• The younger generation will become an increasingly important group: wealthier, more sophisticated and responding to different marketing / promotional strategiesresponding to different marketing / promotional strategies

• FMCG growth is still positive and fueled by rebounding consumer and business leaders confidence

• Both Off & On-Premise increase store numbers & salesBoth Off & On Premise increase store numbers & sales, translating into increasing future in/out home consumption occasions

• The development of modern trade will influence the way

51

p ypeople shop and create new category opportunities

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Page 51

Food for thought…T t d t d t t i d d i Vi tTargeted trade strategies are needed in Vietnam• Modern trade and specific convenience management

systems will need fast development• Maximizing portfolio efficiency in store will be key to• Maximizing portfolio efficiency in store will be key to

succeed in the still dominant traditional trade channel• Rural strategies must be part of long term planning in

VietnamVietnam Consumers’ needs constantly evolve and one strategy does not fit all. Marketing strategies will need to stand out as consumers arebombarded with new messagesbombarded with new messages• Understand package trends and meet demands of quality and

price conscious consumers• Invest in NDP to propose sophistication and convenience in

52

p p pproducts benefits

• Know the segments in your consumer base (geographies, age…)

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Page 52

Thank you

53

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Appendix

54

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

All Country Index

Australia (AU)

Austria (AT)

Belgium (BE)

Japan (JP)

South Korea (KO)

Malaysia (MY)

Mexico (MX)

UK (GB)

U S (US)

Czech Republic (CZ)

Hungary (HU)Brazil (BR)

Canada (CA)

Chile (CL)

China (CN)

Mexico (MX)

Netherlands (NL)

New Zealand (NZ)

Norway (NO)

Philippines (PH)

Hungary (HU)

UAE (AE)

Argentina (AR)

Vietnam (VN)

Estonia (EE)Denmark (DK)

Finland (FI)

France (FR)

Germany (DE)

Philippines (PH)

Poland (PL)

Portugal (PT)

Russia (RU)

Singapore (SG)

Estonia (EE)

Latvia (LV)

Lithuania (LT)

Romania (RO)

Egypt (EG)Germany (DE)

Greece (GR)

Hong Kong (HK)

India (IN)

Indonesia (ID)

Singapore (SG)

South Africa (ZA)

Spain (ES)

Sweden (SE)

Switzerland (CH)

Egypt (EG)

Pakistan (PK)

Columbia (CO)

Israel (IL)

Venezuela (VE)

55

Indonesia (ID)

Ireland (IE)

Italy (IT)

Switzerland (CH)

Taiwan (TW)

Thailand (TH)

Turkey (TR)

e e ue a ( )

Saudi Arabia (SA)

Ukraine (UA)

Copyright © 2010 The Nielsen Company. Confidential and proprietary.

Nielsen’s commitment to deliver you the Bigger Picture in Vietnam

Senior Leaders of manufacturers in Vietnam• Total sample N=57

• Conducted July 2010• Global online study in 55 countries

Understanding consumer differences•Total sample N = 600•Period: May 2nd to 15th 09ABC HIB l & f l 20 t 45

p• Period: July 2010 •ABC HIB, males & females, 20 to 45 yo

Others source of information:

•Macro Economic data

NielsenRetail Audit

•City coverage: HCMC, Hanoi, Danang, Cantho• Target respondent: Males/Females

•Macro Economic data•Nielsen Omnibus April 2009•Nielsen Global Omnibus•Vietnam Govt. Statistics Office•Nielsen Vietnam Census 2009

•City coverage: 6 cities traditional trade (HCMC, Hanoi, CanTho, Nhatrang,

Audit

56

aged 18-65 years• Methodology: face to face interview•Total sample N=1500•Period: 15th Oct to 15th Nov09

Danang, Haiphong)• Ended period: June 2010• Covered 43 FMCG categories

Copyright © 2010 The Nielsen Company. Confidential and proprietary.