virtual coaching classes organised by bos, icai ca final

TRANSCRIPT

VIRTUAL COACHING CLASSESORGANISED BY BOS, ICAI

CA FINALTOPIC : IND AS OVERVIEW

PAPER : FINANCIAL REPORTING (FR)

Faculty: CA Amit Jain

Table of Contents

1. What is Ind AS

2. IFRS and corresponding Ind AS

3. Ind AS categorised based on nature

4. Ind AS Roadmap

5. Net worth assessment

6. Case studies – Applicability

7. Carve outs

2ASB, THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

What is Ind AS ?

§ Ind AS are set of accounting standards notified by Ministry of Corporate Affairs (MCA), converged withInternational Financial Reporting Standards (IFRS), these accounting standards are formulated byAccounting Standard Board (ASB) of Institute of Chartered Accountants of India (ICAI).

§ Convergence means alignment of the standards of different standard setters with a certain rate ofcompromise, by adopting the requirements of the standards either fully or partially.

§ Indian Accounting Standards are almost similar to IFRS but with few carve outs so as to make themsuitable for Indian Environment.

§ Ind AS are named and numbered in the same way as the corresponding International FinancialReporting Standards (IFRS).

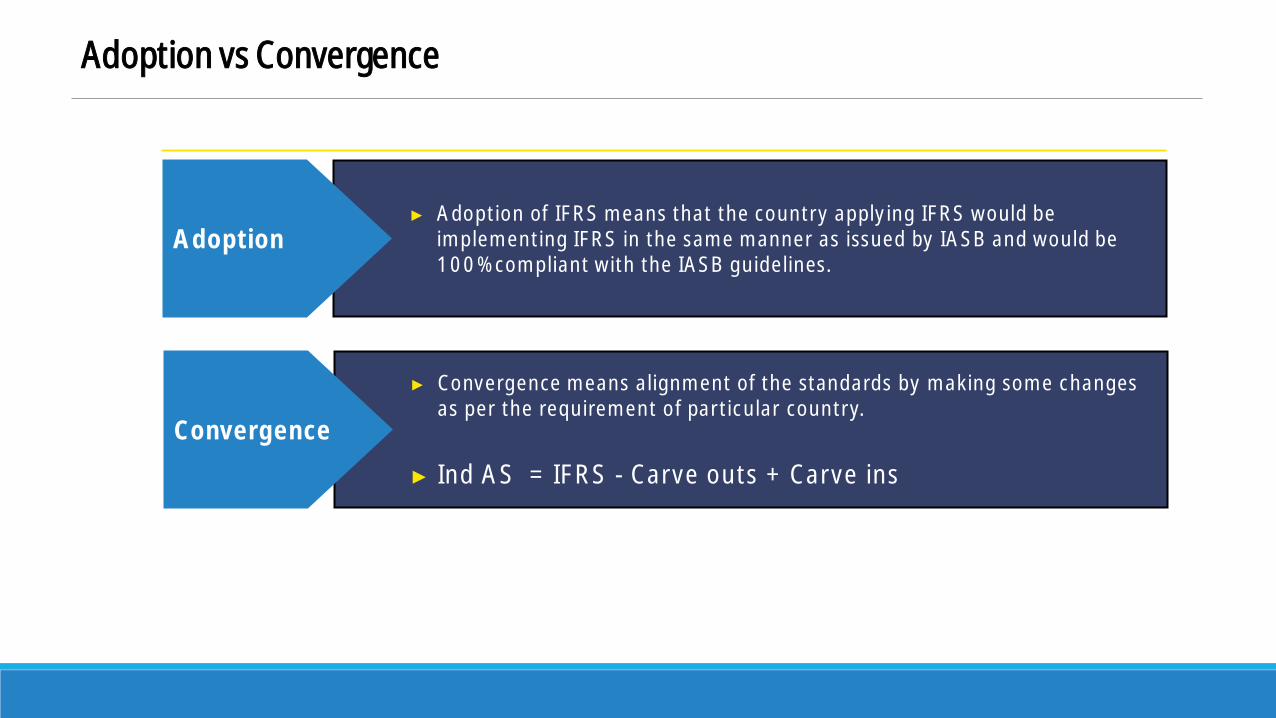

Adoption vs Convergence

Business combination restatement on the date of transition

► Convergence means alignment of the standards by making some changesas per the requirement of particular country.

► Ind AS = IFRS - Carve outs + Carve ins

Convergence

► Adoption of IFRS means that the country applying IFRS would beimplementing IFRS in the same manner as issued by IASB and would be100% compliant with the IASB guidelines.

Adoption

IFRS and corresponding Ind AS

5ASB, THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

IFRS and corresponding Ind ASS.No. IFRS/ IAS Ind AS Description

1 IAS 1 Ind AS 1 § Presentation of Financial Statements2 IAS 2 Ind AS 2 § Inventories3 IAS 7 Ind AS 7 § Statement of Cash Flows4 IAS 8 Ind AS 8 § Accounting Policies, Changes in Accounting Estimates and Errors5 IAS 10 Ind AS 10 § Events after the Reporting Period

IAS 11 Ind AS 11 § Construction Contracts (Replaced by Ind AS 115 w.e.f. 1 April 2018)

6 IAS 12 Ind AS 12 § Income Taxes7 IAS 16 Ind AS 16 § Property, Plant and Equipment

IAS 17 Ind AS 17 § Leases (Replaced by Ind AS 116 w.e.f. 1 April 2019)IAS 18 Ind AS 18 § Revenue (Replaced by Ind AS 115 w.e.f. 1 April 2018)

8 IAS 19 Ind AS 19 § Employee Benefits9 IAS 20 Ind AS 20 § Accounting for Government Grants and Disclosure of Government Assistance

10 IAS 21 Ind AS 21 § The Effects of Changes in Foreign Exchange Rates11 IAS 23 Ind AS 23 § Borrowing Costs12 IAS 24 Ind AS 24 § Related Party Disclosures

IAS 26 ** § Accounting and Reporting by Retirement Benefit Plans (Not issued under Ind AS)

13 IAS 27 Ind AS 27 § Consolidated and Separate Financial Statement14 IAS 28 Ind AS 28 § Investments in Associates and Joint Ventures

IFRS and corresponding Ind ASS.No. IFRS/ IAS Ind AS Description

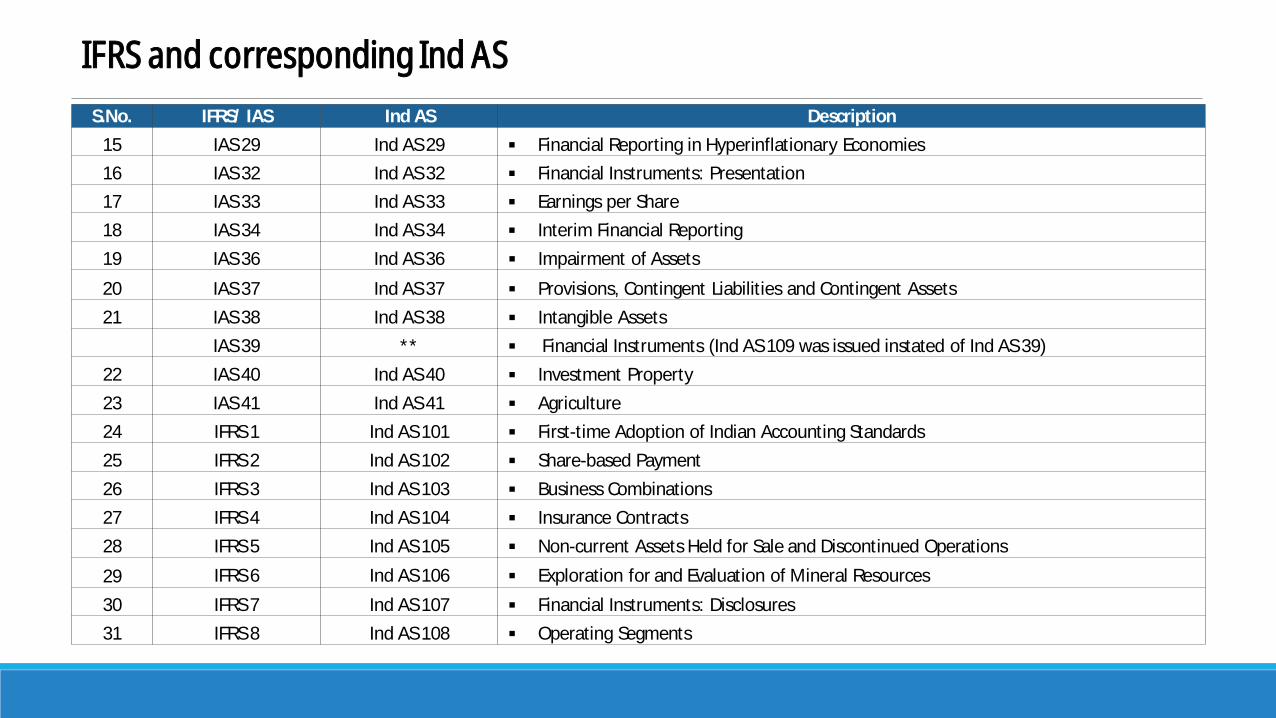

15 IAS 29 Ind AS 29 § Financial Reporting in Hyperinflationary Economies16 IAS 32 Ind AS 32 § Financial Instruments: Presentation17 IAS 33 Ind AS 33 § Earnings per Share18 IAS 34 Ind AS 34 § Interim Financial Reporting19 IAS 36 Ind AS 36 § Impairment of Assets

20 IAS 37 Ind AS 37 § Provisions, Contingent Liabilities and Contingent Assets21 IAS 38 Ind AS 38 § Intangible Assets

IAS 39 ** § Financial Instruments (Ind AS 109 was issued instated of Ind AS 39)22 IAS 40 Ind AS 40 § Investment Property23 IAS 41 Ind AS 41 § Agriculture24 IFRS 1 Ind AS 101 § First-time Adoption of Indian Accounting Standards25 IFRS 2 Ind AS 102 § Share-based Payment26 IFRS 3 Ind AS 103 § Business Combinations27 IFRS 4 Ind AS 104 § Insurance Contracts28 IFRS 5 Ind AS 105 § Non-current Assets Held for Sale and Discontinued Operations

29 IFRS 6 Ind AS 106 § Exploration for and Evaluation of Mineral Resources30 IFRS 7 Ind AS 107 § Financial Instruments: Disclosures31 IFRS 8 Ind AS 108 § Operating Segments

IFRS and corresponding Ind ASS.No. IFRS/ IAS Ind AS Description

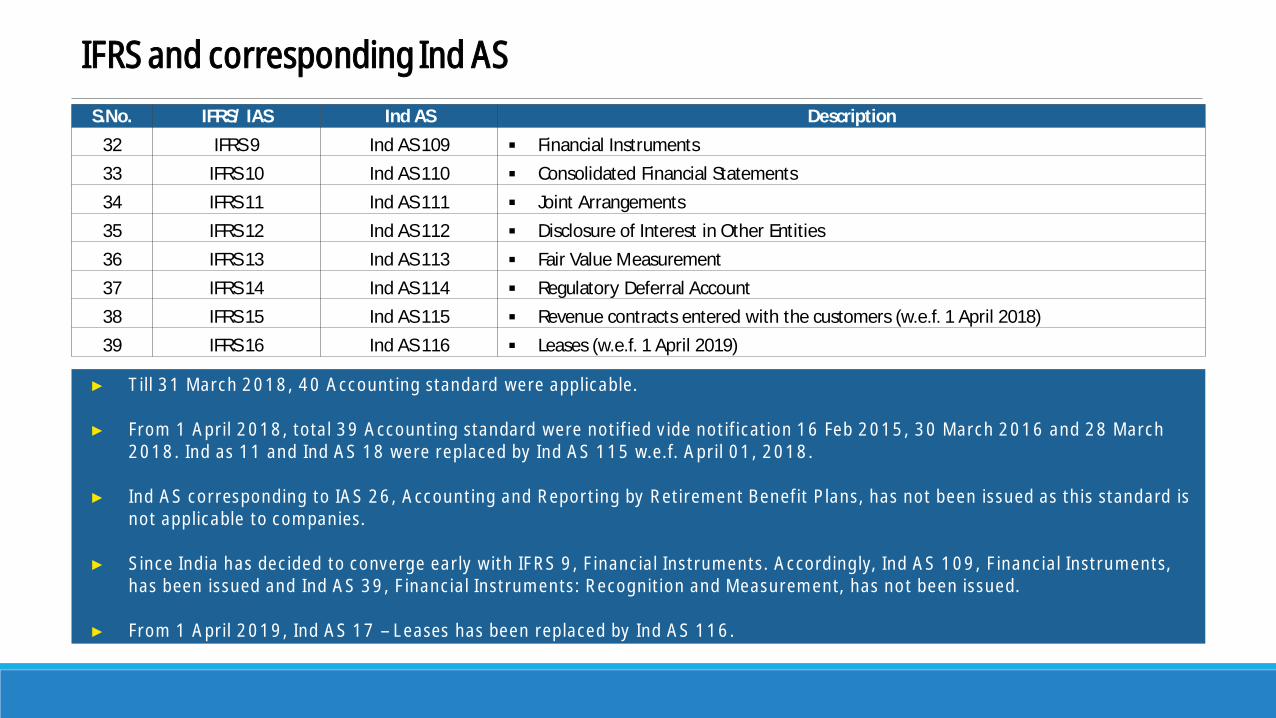

32 IFRS 9 Ind AS 109 § Financial Instruments33 IFRS 10 Ind AS 110 § Consolidated Financial Statements34 IFRS 11 Ind AS 111 § Joint Arrangements35 IFRS 12 Ind AS 112 § Disclosure of Interest in Other Entities36 IFRS 13 Ind AS 113 § Fair Value Measurement37 IFRS 14 Ind AS 114 § Regulatory Deferral Account38 IFRS 15 Ind AS 115 § Revenue contracts entered with the customers (w.e.f. 1 April 2018)39 IFRS 16 Ind AS 116 § Leases (w.e.f. 1 April 2019)

► Till 31 March 2018, 40 Accounting standard were applicable.

► From 1 April 2018, total 39 Accounting standard were notified vide notification 16 Feb 2015, 30 March 2016 and 28 March2018. Ind as 11 and Ind AS 18 were replaced by Ind AS 115 w.e.f. April 01, 2018.

► Ind AS corresponding to IAS 26, Accounting and Reporting by Retirement Benefit Plans, has not been issued as this standard isnot applicable to companies.

► Since India has decided to converge early with IFRS 9, Financial Instruments. Accordingly, Ind AS 109, Financial Instruments,has been issued and Ind AS 39, Financial Instruments: Recognition and Measurement, has not been issued.

► From 1 April 2019, Ind AS 17 – Leases has been replaced by Ind AS 116.

Ind AS based on nature

9ASB, THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

Ind AS categorised based on natureS.No. IFRS/ IAS Ind AS Description

1 First Time Adoption Ind AS 101 § First-time Adoption of Indian Accounting Standards2 Assets and

liabilities

Ind AS 2 § Inventories3 Ind AS 16 § Property, Plant and Equipment4 Ind AS 23 § Borrowing Costs5 Ind AS 36 § Impairment of Assets6 Ind AS 37 § Provisions, Contingent Liabilities and Contingent Assets7 Ind AS 38 § Intangible Assets8 Ind AS 40 § Investment Property9 Ind AS 16 § Leases

10 Financial Instruments

and Forex

Ind AS 21 § The Effects of Changes in Foreign Exchange Rates11 Ind AS 32 § Financial Instruments: Presentation12 Ind AS 107 § Financial Instruments: Disclosures13 Ind AS 109 § Financial Instruments14 Ind AS 113 § Fair Value Measurement15 Group Accounts Ind AS 27 § Consolidated and Separate Financial Statement16 Ind AS 28 § Investments in Associates and Joint Ventures17 Ind AS 103 § Business Combinations18 Ind AS 110 § Consolidated Financial Statements19 Ind AS 111 § Joint Arrangements20 Ind AS 112 § Disclosure of Interest in Other Entities

Ind AS categorised based on natureS.No. IFRS/ IAS Ind AS Description

21 Income and

Expenses

Ind AS 12 § Income Taxes22 Ind AS 19 § Employee Benefits23 Ind AS 20 § Accounting for Government Grants and Disclosure of Government Assistance24 Ind AS 102 § Share-based Payment25 Ind AS 115 § Revenue contracts entered with the customers (wef 1 April 2018)26 Industry Specific Ind AS 41 § Agriculture27 Ind AS 104 § Insurance Contracts28 Ind AS 106 § Exploration for and Evaluation of Mineral Resources29 Ind AS 114 § Regulatory Deferral Account30 Ind AS 29 § Financial Reporting in Hyperinflationary Economies31 Presentation and

DisclosuresInd AS 1 § Presentation of Financial Statements

32 Ind AS 7 § Statement of Cash Flows33 Ind AS 8 § Accounting Policies, Changes in Accounting Estimates and Errors34 Ind AS 10 § Events after the Reporting Period35 Ind AS 24 § Related Party Disclosures36 Ind AS 33 § Earnings per Share37 Ind AS 34 § Interim Financial Reporting38 Ind AS 105 § Non-current Assets Held for Sale and Discontinued Operations39 Ind AS 108 § Operating Segments

Marks weightage

12ASB, THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

Financial Reporting - Marks WeightageDescription Weightage

1. Framework for Preparation and Presentation of Financial Statements in accordance with Indian Accounting Standards (Ind AS).

10 % - 15%2. Application of Indian Accounting Standards (Ind AS) with reference to General Purpose Financial Statements.§ (i) Ind AS on First time adoption of Indian Accounting Standards [Ind AS 101]§ (ii) Ind AS on Presentation of Items in the Financial Statements [Ind AS 1, 34, 7 and Schedule III]§ (iii) Ind AS on Measurement based on Accounting Policies [Ind AS 8, 10, 113]§ (iv) Ind AS on Income Statement [Ind AS 115] 10 % - 15%§ (v) Ind AS on Assets and Liabilities of the Financial Statements including Industry specific Ind AS

Ind AS on Assets – Ind AS 2, 16, 116, 23, 36, 38, 40, 105Ind AS on Liabilities – Ind AS 19 and 37Industry specific – Ind AS 41

15 % - 25%

§ (vi) Ind AS on Items impacting the Financial Statements [ Ind AS 12 and 21]15 % - 20%

§ (vii) Ind AS on Disclosures in the Financial Statements [ Ind AS 24, 33 and 108]§ (viiI) Other Ind AS [Ind AS 20, 102]

3. . Indian Accounting Standards on Group Accounting10 % - 20%§ (i) Business Combinations and Accounting for Corporate Restructuring (including demerger) [Ind AS 103]

§ (ii) Consolidated and Separate Financial Statements [ Ind AS 27, 28, 110, 111 and 112]

4. Accounting and Reporting of Financial Instruments [ Ind AS 32, 107 and 109] 10 % - 20%5. Analysis of Financial Statements

5 % - 10%6. Integrated Reporting7. Corporate Social Responsibility Reporting

Ind AS Roadmap

14ASB, THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

Ind AS – Mandatory Roadmap – Comparative Analysis

Phase Criterion Companies NBFC Insurance

PHASE I • Any Company / NBFC (Listed or Unlisted or inthe process of listing in India or Outside India)having Net worth of

• 500 Crore or More • 500 Crore or More• IRDA has deferred

the date ofimplementation ofInd AS for InsuranceCompanies tillfurther notice.

• Currently Ind AS isnot applicable toInsuranceCompanies.

• Applicability date • April 01, 2016 • April 01, 2018

• First Ind AS Reporting period• 31 March 2017• 31 March 2016

• 1 April 2015

• 31 March 2019• 31 March 2018

• 1 April 2017

PHASE II • Any unlisted Company / NBFC having Net worthof

• 250 Crore or More butless than 500 Crores

• 250 Crore or More butless than 500 Crores

• Other companies / NBFC not covered in Phase I• (Listed or in the process of Listing)• (Other than Companies listed on SME Exchange)

• All covered.• No net worth criterion.

• All covered.• No net worth criterion.

• Applicability date • April 01, 2017 • April 01, 2019

• First Ind AS Reporting period• 31 March 2018• 31 March 2017

• 1 April 2016

• 31 March 2020• 31 March 2019

• 1 April 2018

Ind AS – Mandatory Roadmap

For Companies• Once a companies is covered under MCA Roadmap, its Holding, Subsidiary, Associate and Joint venture are also covered.• Subsidiary, Associate and Joint venture includes direct and indirect subsidiary, associate & joint venture.• Companies not covered by the above roadmap shall continue to apply existing Accounting Standards notified in Companies

(Accounting Standards) Rules, 2006.• Overseas subsidiary, associate, joint venture and other similar entities of an Indian company may prepare its SFS in

accordance with the requirements of the specific jurisdiction. But in order to facilitate consolidation, they have to preparetheir FS under Ind AS.

For NBFC• NBFC having net worth below 250 crore SHALL NOT apply Ind AS.• Irrespective of MCA roadmap, NBFC and Banks are required to adopt and follow RBI roadmap.• Voluntary adoption of Ind AS is not allowed.• Holding, Subsidiary, JV and Associate companies of NBFC roadmap (other than those already covered under corporate

roadmap) shall also apply from said date.

Common points for Companies & NBFC :

► Once a company is covered in any phase, its Holding, Subsidiary, Associates and JV are also covered in its respective Phases.► Once Ind AS are applicable (either mandatorily or voluntarily), an entity shall be required to follow the Ind AS for all the subsequent

financial statements.► Ind AS is applicable for both Consolidated and separate Financial Statements

Ind AS – Mandatory Roadmap for Banks

Scheduled Commercial banks (excluding RRB’s)

• Scheduled Commercial Banks (SCBs) excluding Regional Rural Banks (RRBs) were initially required to implement IndianAccounting Standards (Ind AS) from 1 April 2018. RBI vide a press release dated 5 April 2018, deferred the implementationof Ind AS by one year i.e. from 1 April 2019.

• However, later on it deferred the Ind AS implementation till further notice RBI through a notification dated 22 March 2019.

Ind AS Roadmap - Meaning of Listed or in the process of Listing

1. Covered for Ind AS applicability criteria• Equity listed or Debt listed• Stock exchange whether in India or outside India, both are covered.

2. Meaning of “In the process of Listing”• Company is in the process of filling of Draft Red hearing prospectus (DRHP) for listing.

Ind AS Not Applicable

Ind AS not Applicable to following entities :1. Partnership Firm2. Sole proprietorship3. Limited liability firm4. Trust5. Society6. Banks (deferred till RBI Further notification).7. Insurance companies (deferred till IRDA Further notification).8. Foreign companies (Registered as per foreign jurisdiction and not as per companies Act).9. Branch office10. Entities listed under SME exchange.

Important Point

► Ind AS is applicable to section 8 Companies – Non profit organization.

In the First Ind AS Financial statements for the year ended March 31, 2017

Ø Balance Sheet :§ Final : March 31, 2017,§ Comparative : March 31, 2016 and§ Opening : April 01, 2015

Ø Statement of profit and loss :§ For the year ended March 31, 2017§ For the year ended March 31, 2016

Ø Statement of changes in equity :§ For the year ended March 31, 2017§ For the year ended March 31, 2016

First Ind AS reporting year for PHASE I entities will be 2016-17

Comparative year under Ind AS First effective year under Ind AS

Q1 Q2 Q3 Q4 Q1

1 April 2015Ind AS openingbalance sheet

31 March 2016Last Indian GAAP

Financial statements

2015-16 2016-17Ind AS reporting

date

31 March 2017First Ind AS financial statements

Ind AS transitiondate

Q2 Q3 Q4

Ø Statement of cash flows :§ For the year ended March 31, 2017§ For the year ended March 31, 2016

Ø Reconciliations :§ Equity reconciliation from Indian GAAP to Ind AS as at March 31,

2016 and 2015§ Profit /loss reconciliations for the year ended 2015 -16.

Ø Related notes to accounts & disclosures : For the March 31, 2017and 2016.

Ind AS – Roadmap – Phase I entities

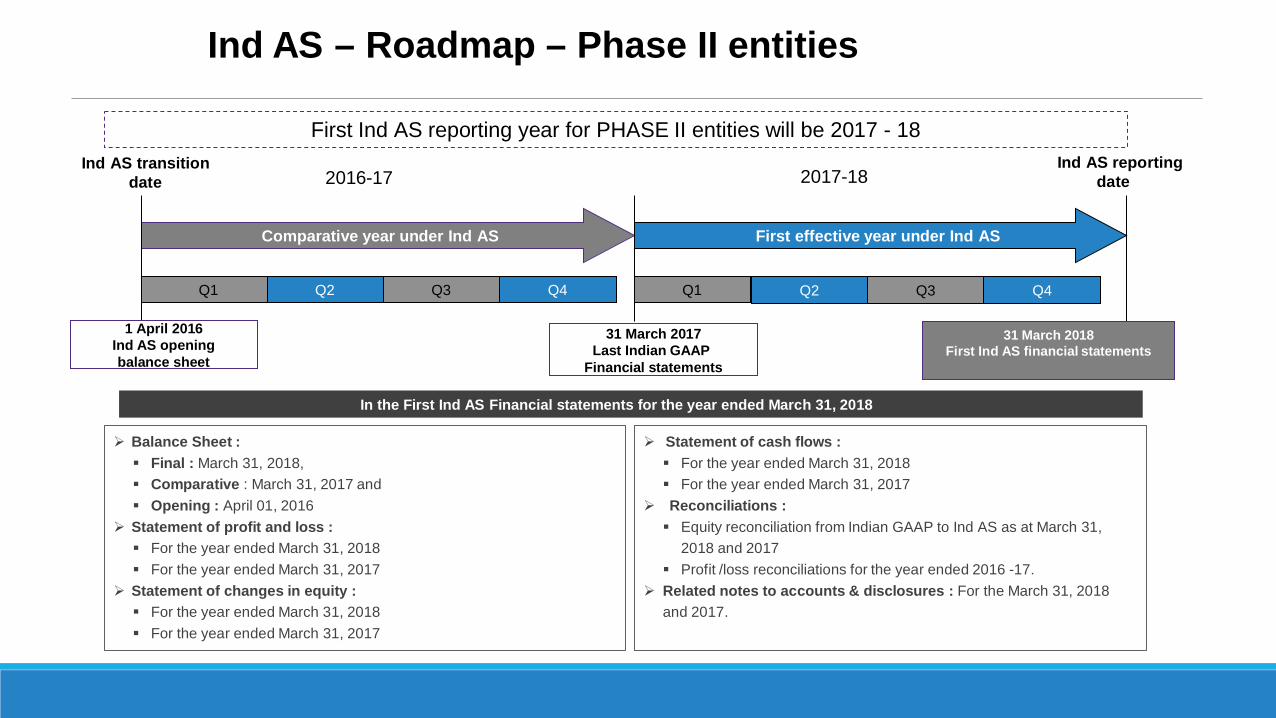

In the First Ind AS Financial statements for the year ended March 31, 2018

Ø Balance Sheet :§ Final : March 31, 2018,§ Comparative : March 31, 2017 and§ Opening : April 01, 2016

Ø Statement of profit and loss :§ For the year ended March 31, 2018§ For the year ended March 31, 2017

Ø Statement of changes in equity :§ For the year ended March 31, 2018§ For the year ended March 31, 2017

First Ind AS reporting year for PHASE II entities will be 2017 - 18

Comparative year under Ind AS First effective year under Ind AS

Q1 Q2 Q3 Q4 Q1

1 April 2016Ind AS openingbalance sheet

31 March 2017Last Indian GAAP

Financial statements

2016-17 2017-18Ind AS reporting

date

31 March 2018First Ind AS financial statements

Ind AS transitiondate

Q2 Q3 Q4

Ø Statement of cash flows :§ For the year ended March 31, 2018§ For the year ended March 31, 2017

Ø Reconciliations :§ Equity reconciliation from Indian GAAP to Ind AS as at March 31,

2018 and 2017§ Profit /loss reconciliations for the year ended 2016 -17.

Ø Related notes to accounts & disclosures : For the March 31, 2018and 2017.

Ind AS – Roadmap – Phase II entities

Net worth

22ASB, THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

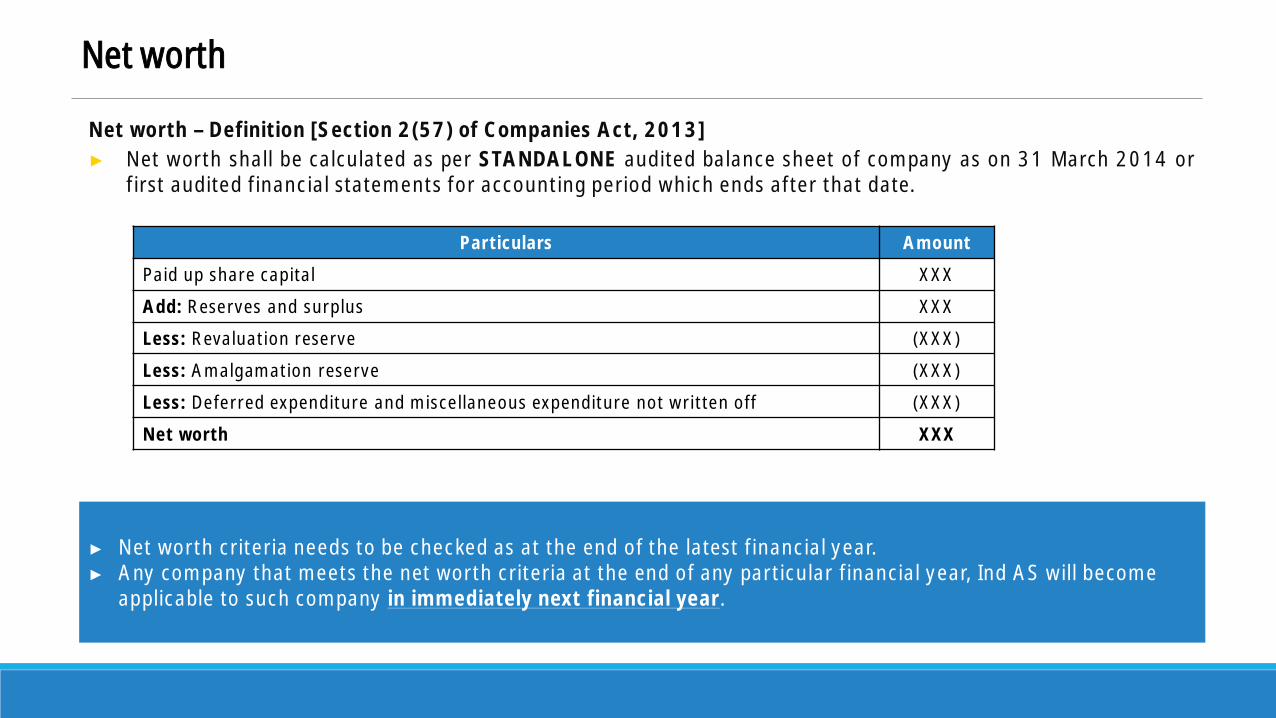

► What do you mean by Net Worth and how it is calculated?Net worth – Definition [Section 2(57) of Companies Act, 2013]► Net worth shall be calculated as per STANDALONE audited balance sheet of company as on 31 March 2014 or

first audited financial statements for accounting period which ends after that date.

Particulars Amount

Paid up share capital XXX

Add: Reserves and surplus XXX

Less: Revaluation reserve (XXX)

Less: Amalgamation reserve (XXX)

Less: Deferred expenditure and miscellaneous expenditure not written off (XXX)

Net worth XXX

► Net worth criteria needs to be checked as at the end of the latest financial year.► Any company that meets the net worth criteria at the end of any particular financial year, Ind AS will become

applicable to such company in immediately next financial year.

Net worth

Net worth

► YesInclusion for ESOP Reserve§ Whether ESOP reserve is required to be included while computing

net worth of a company to assess applicability of Ind AS on thecompany?

► Both Companies does not meet Phase I applicability criteria.

► Company A - Ind AS will be applicable from financial year 2017-18 to all listedcompanies having net worth less than Rs. 500 crore. In other words, Ind ASwill be applicable to A (listed) from F.Y. 2017-18 i.e. Phase II

► Company B (unlisted) - Not even a phase II Company. Ind AS will not beapplicable unless net worth criteria being met.

Negative net worth§ Will the following companies with negative net worth need to

comply with Ind AS?a) Company A (listed) having negative net worth of Rs. 600

crore.b) Company B (unlisted) having negative net worth of Rs. 300

crore.

► No.► Branch office is only an establishment of a foreign company in India. The

Branch office is just an extension of the foreign company in India.

Branch office

§ Whether Ind AS is applicable to Branch office?

► No.► Ind AS is applicable to corporates only. This cannot be applied by non-

corporate entities even voluntarily.

Partnership Firm

§ Whether Ind AS is applicable to Partnership Firm?

Net worth

► YesSection 8 Companies ?§ Whether Ind AS applicable to section 8 companies – Charitable

organisation , Non profit etc ?

Net worth – Case study

Whether Ind AS is applicable from the same year in which net worth exceeds INR 500 Cr, or from nextyear?

Case study :A company has net worth for the last 2 years as follows:

The company received a capital infusion of INR 800 crores during 16-17.

Whether Company A is required to comply Ind AS from FY ended March 2017 or March 2018?

Net worth Amount (INR Cr.)

31st March, 2016 200

31st March, 2017 1,000

Response :

► Net worth shall be calculated as on March 31st, 2016. Since, net worth criteria does not met, Ind AS is notapplicable.

► Net worth criteria needs to be re-checked as on March 31st 2017. Since, net worth criteria meets on March 31st

2017, Ind AS will be applicable from immediately next financial year i.e. 2017-18.

Net worth – Case study

Case Study► What will be the Ind AS applicability date for all the companies for SFS and CFS as mentioned in structure

below:

Response:► For SFS reporting :

§ NBFC (Holding) : First reporting under Ind AS will be from March 31, 2019.§ Non NBFC 1 (subsidiary) : First reporting under Ind AS will be from March 31, 2017.§ Non NBFC 2 (subsidiary) : First reporting under Ind AS will be from March 31, 2018.

► For CFS reporting :§ NBFC (Holding) : First reporting under Ind AS will be from March 31, 2019.§ Non NBFC 1 and 2 also prepare its financial statement under Indian GAAP till March 31, 2018 in order to facilitate CFS.

NBFCNet worth = INR 800 Cr (As at 31 March 2016)

Non NBFC 1(Subsidiary)

Net worth = INR 550 Cr

Non NBFC 2(Subsidiary)

Net worth = INR 450 Cr

Case Studies

28ASB, THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

Ind Applicability – Investor / Fellow Subsidiary§ Company A is an unlisted entity having net worth less than INR 250 crores and holding Company of Company B.

Company B is a listed entity covered in phase II of Ind AS roadmap.

§ Company D is an unlisted entity and holds 25% in company B (i.e, Company D is an investor company of CompanyB) and has net worth less than INR 250 crores.

§ Company C is a fellow subsidiary of company B i.e. subsidiary of the holding company A.

§ Whether Ind AS is applicable to Company C and Company D?

Response :

► No. Company C is not mandatorily required to adopt Ind AS for its statutory reporting. Further, company C may apply Ind ASvoluntarily for its statutory reporting.

► No. Company D is just an investor company and does not qualify as a holding company of Company B. Company D is not requiredto comply with Ind AS by virtue of Company B falling under the threshold of Ind AS applicability

Listing Criteria Evaluation

§ XYZ Limited is a company having net worth less than INR 250 crores as on 31 March 2017.

§ What is the status of applicability of Ind AS for the company in the following scenarios:

# Particulars Ind AS Applicable period

1 § The company was in the process of listing as at thebeginning of the year (i.e. 1st April 2017) and thecompany ultimately gets listed as at the end of the year(March 2018);

2017–18

2 § The company is listed at the beginning of the year andduring the year it gets de-listed;

2017–18 irrespective that theCompany gets delisted during the year.

3 § The process of listing began during the year, for e.g. inthe month of May 2017 and the company ultimately getslisted as at the end of the year i.e. March 2018. Will therebe any difference if the company gets listed in April,2018. i.e. it was in process of listing as at the year end.

2017–18It shall be required to comply with Ind

AS from the same year in which itbegan the process of listing.

Applicability of Ind AS to NBFCs in case not registered with RBI

§ A Company ABC Ltd. performs role of NBFC and has applied for the registration as NBFC which is awaited fromthe Reserve Bank of India (RBI).

§ Whether roadmap for the applicability of Ind AS as applicable to NBFCs also applies to the Company ABC Ltd.,which performs role of NBFC however, it is not registered with the RBI?

Response :

► Rule 4(1)(iii) of the Companies (Indian Accounting Standards) (Amendments) Rules, 2016 lays down the roadmap for theapplicability of Ind AS to NBFCs. As per the said rules, “Non-Banking Financial Company” means a Non-Banking FinancialCompany as defined in clause (f) of section 45-I of the Reserve Bank of India Act, 1934 and includes Housing FinanceCompanies, Merchant Banking companies, Micro Finance Companies, Mutual Benefit Companies, Venture Capital FundCompanies, Stock Broker or Sub-Broker Companies, Nidhi Companies, Chit Companies, Securitisation and ReconstructionCompanies, Mortgage Guarantee Companies, Pension Fund Companies, Asset Management Companies and Core InvestmentCompanies.

► The definition of NBFC is given under the RBI Act, 1934. Hence the company which is carrying on the activity of NBFC but notregistered with RBI will also be subject to the roadmap for the applicability of Ind AS as applicable to any other NBFC. However,the requirements with regard to registration, eligibility of a company to operate as NBFC (pending registration) etc. aregoverned by the Reserve Bank of India Act, 1934 and Rules laid down thereon and should be evaluated by the entity based onits own facts and circumstances separately.

Applicability of Ind AS - Date of Transition

§ A company covered under Phase I, having net worth of INR 600 crores, decides to give comparatives for F.Y.2015-16 and F.Y. 2014-15.

§ What should be date of transition in this case?

Response :

► The Company is required to mandatorily adopt Ind AS from April 1, 2016, i.e., for the period 2016-17, and with comparativesas per Ind AS for 2015-16.

► Accordingly, the beginning of the comparative period will be April 1, 2015, which will be considered as the date of transition asper Ind AS. Therefore, the date of transition to Ind AS shall be April 1, 2015. The company cannot have the date of transition atApril 1, 2014.

Applicability of Ind AS - Change in status of listed company

§ As on March 31, 2014, Company A is a listed company and has a net worth of 50 crore.§ As on March 31, 2015, the company is no more a listed company.

§ Whether Company A is required to comply with Ind AS from financial year 2017-18.

Response :

► It may be noted that immediately before the mandatory applicability date, if the threshold criteria for a company are not met,then it shall not be required to comply with Ind AS, irrespective of the fact that as on March 31, 2014, the criteria was met.

► In the given case, before the mandatory applicable date (i.e. 2017-18), Company A ceases to be a listed company. Accordingly,it will not be required to apply Ind AS from FY 2017-18.

Applicability of Ind AS to holding company when subsidiary meets the criteria for applicability ofInd AS

§ Company X (Listed entity) has a net worth of above INR 500 crore and hence required to comply with Ind ASfrom financial year 2016-17. Company Y (Unlisted entity), on a standalone basis, has net worth below INR 250crore and hence it is not required to comply with Ind AS.

§ Company Y acquires shares of Company X during financial year 2016-17, whereby Company Y becomes theholding company of Company X.

§ Whether Company Y will be required to comply with Ind AS from financial year 2016-17, given that it has nowbecome a holding company of Company X during FY 2016-17?

Response :

► Company X is required to adopt Ind AS from financial year 2016-17, since net worth of Company X is more than INR 500 crore.Company Y has acquired shares of Company X resulting in Company Y becoming holding company of Company X during thefinancial year 2016-17.

► Accordingly, Company Y will prepare Ind AS financial statements for the year ended March 31, 2017.

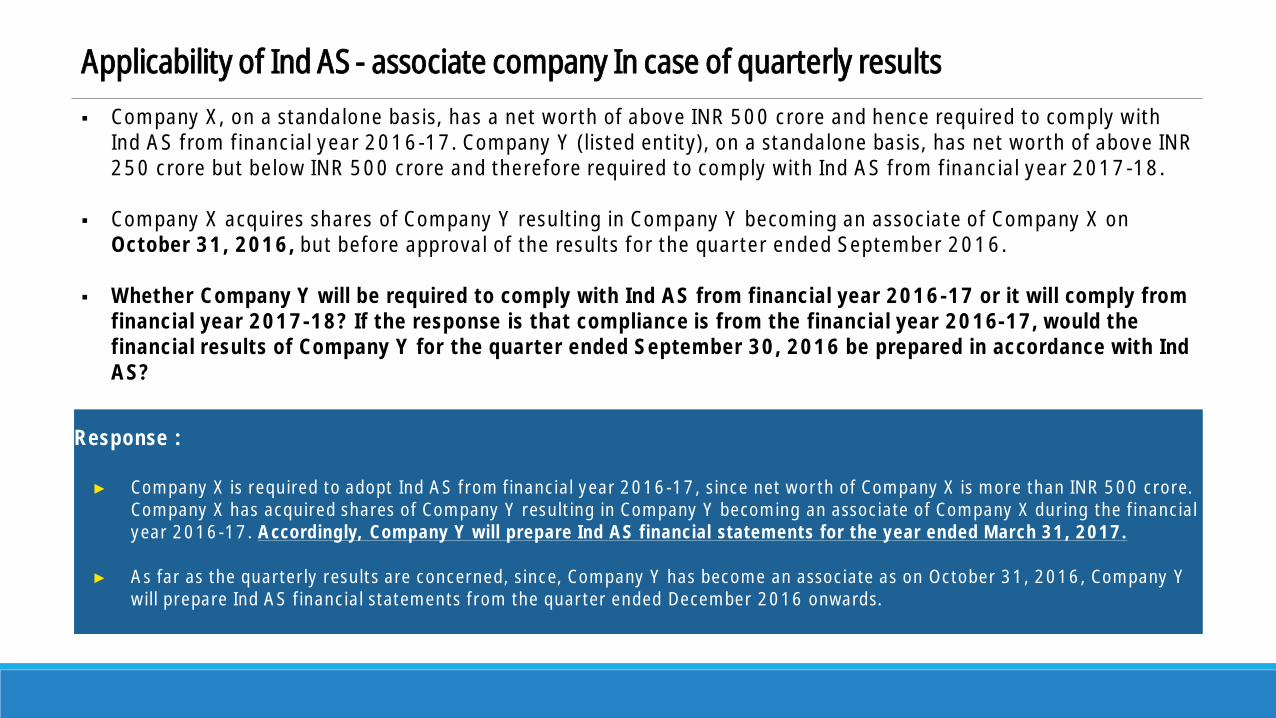

Applicability of Ind AS - associate company In case of quarterly results

§ Company X, on a standalone basis, has a net worth of above INR 500 crore and hence required to comply withInd AS from financial year 2016-17. Company Y (listed entity), on a standalone basis, has net worth of above INR250 crore but below INR 500 crore and therefore required to comply with Ind AS from financial year 2017-18.

§ Company X acquires shares of Company Y resulting in Company Y becoming an associate of Company X onOctober 31, 2016, but before approval of the results for the quarter ended September 2016.

§ Whether Company Y will be required to comply with Ind AS from financial year 2016-17 or it will comply fromfinancial year 2017-18? If the response is that compliance is from the financial year 2016-17, would thefinancial results of Company Y for the quarter ended September 30, 2016 be prepared in accordance with IndAS?

Response :

► Company X is required to adopt Ind AS from financial year 2016-17, since net worth of Company X is more than INR 500 crore.Company X has acquired shares of Company Y resulting in Company Y becoming an associate of Company X during the financialyear 2016-17. Accordingly, Company Y will prepare Ind AS financial statements for the year ended March 31, 2017.

► As far as the quarterly results are concerned, since, Company Y has become an associate as on October 31, 2016, Company Ywill prepare Ind AS financial statements from the quarter ended December 2016 onwards.

Applicability of Ind AS to Core Investment Company (CIC)

§ Company A is a Core Investment Company (CIC) having net worth of more than 500 crore as on March 31, 2014.During the year 2014-15, the Reserve Bank of India (RBI) had exempted Company A from certainregulations/directions governing CIC in India.

§ Whether Company A (exempted CIC) will be regarded as Non-Banking Financial Company (NBFC) for thepurpose of applicability of Ind AS?

Response :

► Core investment companies are specifically included in the definition of NBFC. Accordingly, exempted CIC will be regarded as‘NBFC’ for the purpose of roadmap for implementation of Ind AS irrespective of the fact that RBI may have given someexemptions to certain class of core investment companies from its regulations.

► Yes, Company A will be required to apply Ind AS from the financial year 2018-19. It may further be noted that it cannotvoluntarily adopt Ind AS before 1st April 2018.

Date of Transition in case a company is already preparing financials as per IFRS

§ Company X Ltd. has prepared its financial statements under IFRS for the first time for year ended March 31,2016. It had adopted its date of transition to IFRS as April 1, 2014. As per the Companies (Indian

§ Accounting Standards) Rules, 2015, Company X Ltd. is mandatorily required to prepare its financial statementsas per Ind AS for the year ended March 31, 2017 and hence under Ind AS, the date of transition would be April1, 2015.

§ Whether Company X Ltd. can select date of transition under Ind AS as April 1, 2014 instead of April 1, 2015since it has already carried out exercise of transition on April 1, 2014 for the purposes of IFRS.

Response :

► Date of transition for X Ltd. will be April 1, 2015 being the beginning of the earliest comparative period presented. To explain itfurther, X Ltd. is required to mandatorily adopt Ind AS from April 1, 2016, i.e. for the period 2016-17, and it will givecomparatives as per Ind AS for 2015-16. Accordingly, the beginning of the comparative period will be April 1, 2015 which willbe considered as the date of transition as per Ind AS.

► Although Company X Ltd. has already carried out exercise of transition on April 1, 2014 for the purposes of IFRS, Company X Ltd.cannot select date of transition under Ind AS as at April 1, 2014.

Applicability of Ind AS to holding, subsidiary, joint venture and associate company through director indirect association in case of voluntary adoption by the parent company

§ Company X Ltd. is the holding company of Company A Ltd. Company B Ltd. is an associate company of CompanyA Ltd.

§ Company X Ltd. has decided to adopt Ind AS voluntarily from 2015-16.

§ Whether Company A Ltd. and Company B Ltd. are statutorily required to comply with Ind AS from financialyear 2015-16?

Response :

► Yes.► If an entity voluntarily or mandatorily adopts Ind AS then its holding, subsidiary, joint venture or associate company whether

through direct or indirect association shall comply Ind AS from the financial year in which the entity company starts complyingwith Ind AS.

► Company B Ltd. is a direct associate company of Company A Ltd. but not of Company X Ltd. However, Company X Ltd, throughits subsidiary (i.e., Company B Ltd.), has significant influence over Company B Ltd., indirectly.

► In view of the above requirements, Company B Ltd. shall also comply with Ind AS from the financial year 2015-16.

Carve Outs and Carve Ins

39ASB, THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

Section I

40ASB, THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

Section I

IFRS corresponding to which Ind AS have not been notified :

Ø Ind AS corresponding to IAS 26 - Accounting and Reporting by Retirement Benefit Plans,is not being notified as this Standard is not applicable to companies.

Ø IFRIC 2, Members' Shares in Co-operative Entities and Similar Instruments, is not issuedas it is not relevant to the companies and the Ind AS, notified under the Companies Act,2013, are applicable to Companies incorporated under the Act.

Section II

42ASB, THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

Section II - Carve-outs which are due to differences in application of accounting principles andpractices and economic conditions prevailing in India

# Particulars IFRS Ind AS

1 § Previous GAAP as basisof accounting

§ (IFRS 1 Vs Ind AS 101)

§ IFRS 1defines previous GAAP as the basis ofaccounting used immediately before adoptingIFRS.

§ Ind AS 101 defines Previous GAAP as used forreporting requirement in India immediately beforeadopting Ind AS.

2 § Use of carrying cost ofPPE

§ (IFRS 1 Vs Ind AS 101)

§ No such option exits under IFRS 1. § Ind AS 101 allows the use of carrying cost of property,plant and equipment on the date of transition.

3 § Long-term monetaryitem translation reserve(FCTNR)

§ (IFRS 1 Vs Ind AS 101)

§ No such options exists under IFRS. § Exchange difference arising on translation of long-term foreign currency monetary items to becontinued for already recognized differences ondate of transition.

4 § Breach of materialcovenants in long-termloans

§ (IFRS 1 Vs Ind AS 1)

§ Long term loans shall be treated non-current incase of breach of material covenants of suchloan.

§ Long term loan arrangement need not be classified ascurrent on account of breach of material provision,for which the lender has agreed to waive before theapproval of financial statements for issue.

# Particulars IFRS Ind AS

5 § Accounting for bargainpurchase

§ (Business combination)§ (IFRS 3 Vs Ind AS 103)

§ Bargain purchase gain arising on businesscombination to be recognised in profit or loss asincome.

§ Bargain purchase gain to be recognised in othercomprehensive income and accumulated in equity ascapital reserve,

6 § Guidance on commoncontrol transactions

§ (IFRS 3 Vs Ind AS 103)

§ IFRS 3 excludes from its scope businesscombinations of entities under common control.

§ Appendix C of Ind AS 103 Business Combinationsgives guidance in this regard.

7 § Foreign currencyconvertible bonds

§ (IAS 32 Vs Ind AS 32)

§ As per IAS 32, the equity conversion optionembedded in a convertible bond denominatedin foreign currency to acquire a fixed number ofthe entity’s own equity instruments isconsidered a derivative liability instrument.

§ In Ind AS 32, an exception has been included to thedefinition of ‘financial liability’ whereby conversionoption in FCCB to acquire fixed number of entity’sown equity instruments is classified as equityinstrument if the exercise price is fixed in anycurrency.

Section II - Carve-outs which are due to differences in application of accounting principles andpractices and economic conditions prevailing in India

Section III

45ASB, THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

# Particulars IFRS Ind AS

1 § Single Vs Doubtstatement approach

§ IAS 1 provides an option either to follow the

- Single statement approach (both PL and OCI insame statement as two sections) or

- Two statement approach (PL and OCI in twostatements).

§ Ind AS 1 allows only single statement approach, bothPL and OCI in same statement as two sections.

2 § Function Vs nature-wise classification ofexpenses

§ IAS 1 requires expenses recognised in profit or lossusing a classification based on either their nature ortheir function.

§ Ind AS 1 requires only nature-wise classification ofexpenses.

4 § Employee benefits –Discount rate to beused

§ Discount rate will be based on high qualitycorporate bonds and where no deep market ofhigh quality corporate bond exist thengovernment bond can be used.

§ Discount rate as per market yield on Governmentbonds, instead of high quality corporate bonds.

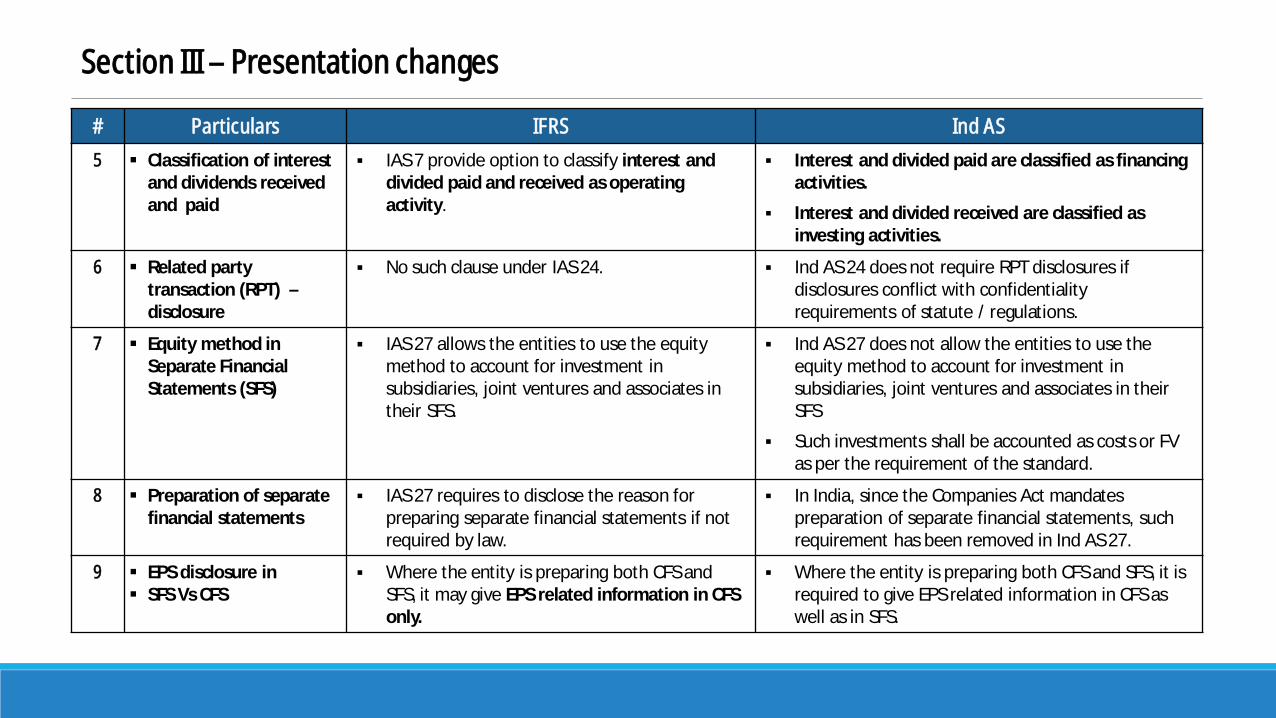

Section III – Presentation changes

# Particulars IFRS Ind AS

5 § Classification of interestand dividends receivedand paid

§ IAS 7 provide option to classify interest anddivided paid and received as operatingactivity.

§ Interest and divided paid are classified as financingactivities.

§ Interest and divided received are classified asinvesting activities.

6 § Related partytransaction (RPT) –disclosure

§ No such clause under IAS 24. § Ind AS 24 does not require RPT disclosures ifdisclosures conflict with confidentialityrequirements of statute / regulations.

7 § Equity method inSeparate FinancialStatements (SFS)

§ IAS 27 allows the entities to use the equitymethod to account for investment insubsidiaries, joint ventures and associates intheir SFS.

§ Ind AS 27 does not allow the entities to use theequity method to account for investment insubsidiaries, joint ventures and associates in theirSFS

§ Such investments shall be accounted as costs or FVas per the requirement of the standard.

8 § Preparation of separatefinancial statements

§ IAS 27 requires to disclose the reason forpreparing separate financial statements if notrequired by law.

§ In India, since the Companies Act mandatespreparation of separate financial statements, suchrequirement has been removed in Ind AS 27.

9 § EPS disclosure in§ SFS Vs CFS

§ Where the entity is preparing both CFS andSFS, it may give EPS related information in CFSonly.

§ Where the entity is preparing both CFS and SFS, it isrequired to give EPS related information in CFS aswell as in SFS.

Section III – Presentation changes

# Particulars IFRS Ind AS

10 § Option for 52 weeksperiod

§ IAS 1 permits the periodicity, for example, of 52weeks for preparation of financial statements.

§ Ind AS 1 does not permit 52 weeks period.

11 § Terminology used Following terminology used under IFRS :

§ Statement of financial position

§ Statement of comprehensive income

§ Authorised financial statements for issue

Following terminology used under Ind AS:

§ Balance sheet

§ Statement of profit and loss

§ Approved the financial statements for issue.

Section III – Presentation changes

Thank you

ASB, THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 49