voice & messaging 2.0 market study survey results summary 2008.pdf · project management...

TRANSCRIPT

Voice & Messaging 2.0 Market Study – Survey Results

Respondent Summary from STL Partners‟ On-line SurveyFull report available separately

Martin Geddes

Chief Analyst

February 2008

- 2 -© STL Limited • Proprietary and Confidential

Contents

Background & Summary Results

About STL

About the survey – respondent breakdown

Summary survey results

Confidence in knowledge of customer needs

Revenue scenarios: will this industry grow?

Responding to low-cost and enhanced functionality competition

Identifying growth areas

User feature needs in telephony

FMC user needs

Voice & Messaging 2.0 Market Study

Contact details

- 3 -© STL Limited • Proprietary and Confidential

Background & Summary Results

Background

Thank you for taking part in the Telco 2.0™ December 2007 Voice & Messaging survey

This document contains the summary results which represent an extract of the full survey results and analysisavailable in the upcoming Telco 2.0™ Consumer Voice & Messaging 2.0 market study

(http://stlpartners.com/telco2_research-analysis_voice-messaging.php).

Summary Results

There is a strong consensus that telcos have a weak understanding of underlying user needs in this space, despite it being their core business – suggesting a need to partner.

A high level of optimism about the future, given current revenue slow-down and stagnation as well as attack from outside (e.g. Skype, internet portal players, arbitrageurs).

This also fits with the strong endorsement of open APIs into those core operator competences (network, identity, billing, care, retail, etc.).

Aggressive responses were favoured to product innovation by Internet competitors. Business as usual is not a good strategy!

Our companion report on future broadband business models (see final page for details) also suggested that over the next ten years there will be a major shift toward non-traditional voice services, both from private voice-enabled applications like Skype or Facebook, as well as voice embedded into games, satnav systems, e-commerce sites, etc. For ideas on what kinds of product and business strategies to follow, please see the full report.

- 4 -© STL Limited • Proprietary and Confidential

Consulting Research Brainstorms

www.telco2.net

About STL: Driving Innovation & Growth in Telco, Media & Technology

- 5 -© STL Limited • Proprietary and Confidential

New Research Reports

Voice &

Messaging 2.0

Broadband

Business ModelsAdvertising

(3rd Edition)

www.telco2.netTo order contact [email protected]

- 6 -© STL Limited • Proprietary and Confidential

STL Consulting Services

Education &

Training

Strategy

Development

New

Proposition

Devt

Business

Case

Development

Project

Management

Support

Frontline

GTM

support

STL‟s „Mindshare’ tools and techniques for value innovation

Industry developments –Telco 2.0

New:Technologies

Competitors

Products

Markets

Business Models

Strategy & Marketing implications

Market Analysis

Customer

Analysis (VOC)

Competitors

Analysis

Core Assets &

Competencies

Strategic Option

Evaluation

Implementation

Planning

Opportunity

Scoping

Concept

Development

Customer

segmentation

Proposition

Development

POC Planning &

Pilot Development

Pricing Strategy

Partner Strategy

Financial

Analysis

Strategic

Alignment

Action Planning

& Management

Stakeholder

Analysis &

Management

Deliverables

Management

Sales Training

Account Planning

Consultative Sales

Engagement

White Papers and Sales

& Marketing Collateral

Partner Programmes

Joint Proposition

Development

- 7 -© STL Limited • Proprietary and Confidential

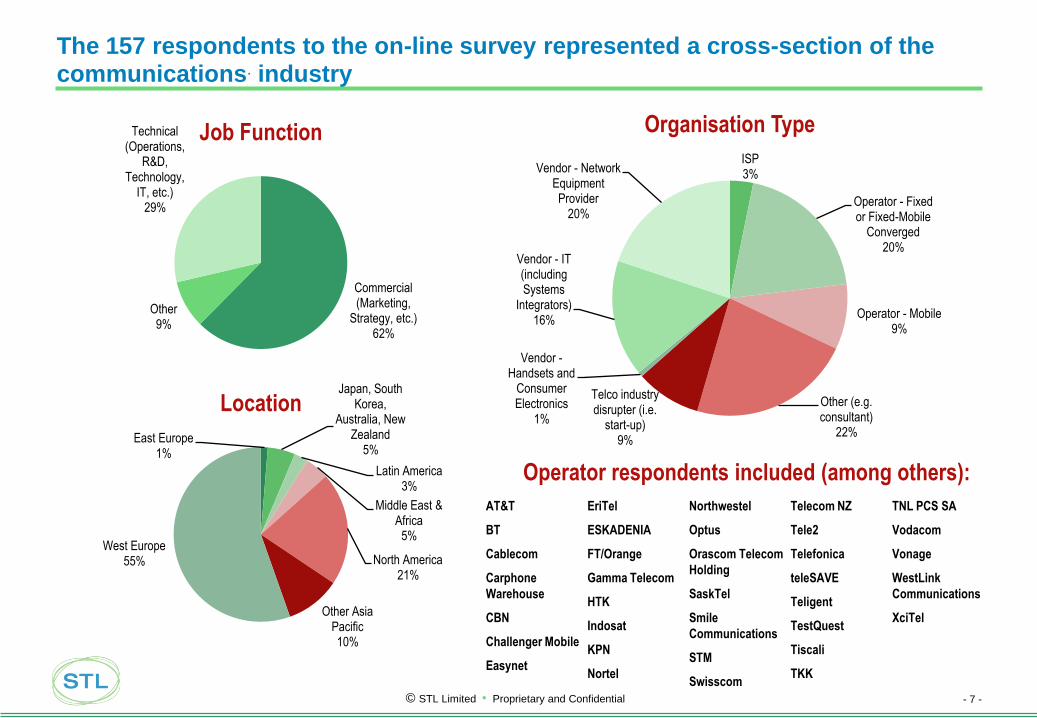

The 157 respondents to the on-line survey represented a cross-section of the communications. industry

Operator respondents included (among others):

Commercial (Marketing,

Strategy, etc.)62%

Other9%

Technical (Operations,

R&D, Technology,

IT, etc.)29%

Job FunctionISP3%

Operator - Fixed or Fixed-Mobile

Converged20%

Operator - Mobile9%

Other (e.g. consultant)

22%

Telco industry disrupter (i.e.

start-up)9%

Vendor -Handsets and

Consumer Electronics

1%

Vendor - IT (including Systems

Integrators)16%

Vendor - Network Equipment Provider

20%

Organisation Type

East Europe1%

Japan, South Korea,

Australia, New Zealand

5%

Latin America3%

Middle East & Africa

5%

North America21%

Other Asia Pacific10%

West Europe55%

Location

AT&T

BT

Cablecom

Carphone

Warehouse

CBN

Challenger Mobile

Easynet

EriTel

ESKADENIA

FT/Orange

Gamma Telecom

HTK

Indosat

KPN

Nortel

Northwestel

Optus

Orascom Telecom

Holding

SaskTel

Smile

Communications

STM

Swisscom

Telecom NZ

Tele2

Telefonica

teleSAVE

Teligent

TestQuest

Tiscali

TKK

TNL PCS SA

Vodacom

Vonage

WestLink

Communications

XciTel

- 8 -© STL Limited • Proprietary and Confidential

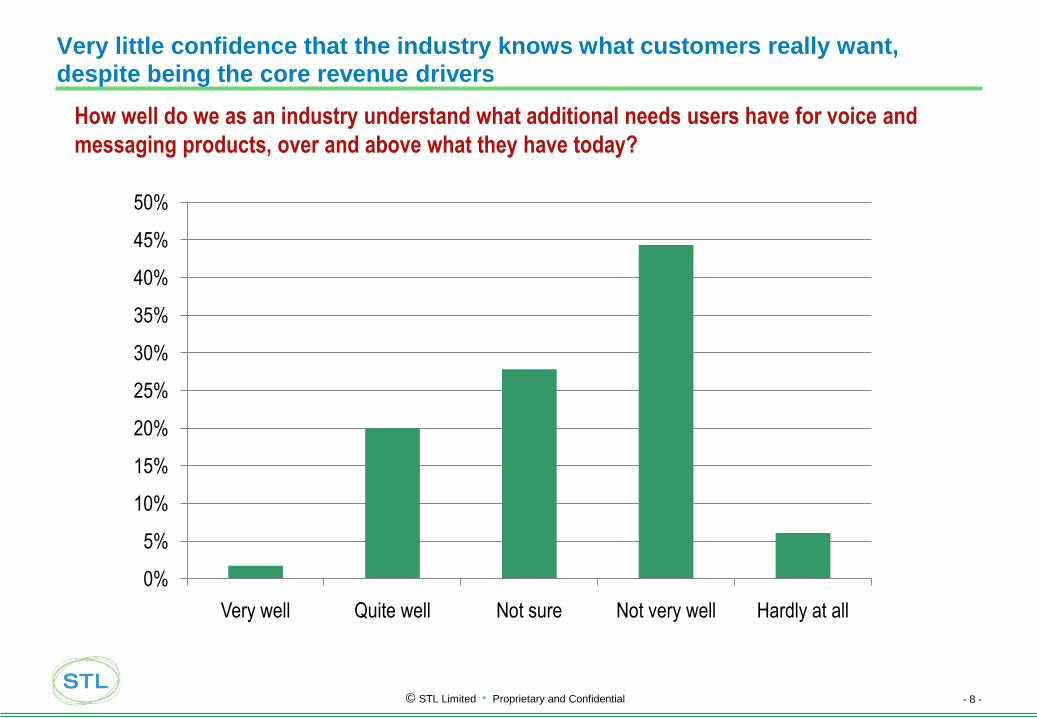

Very little confidence that the industry knows what customers really want, despite being the core revenue drivers

How well do we as an industry understand what additional needs users have for voice and

messaging products, over and above what they have today?

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Very well Quite well Not sure Not very well Hardly at all

- 9 -© STL Limited • Proprietary and Confidential

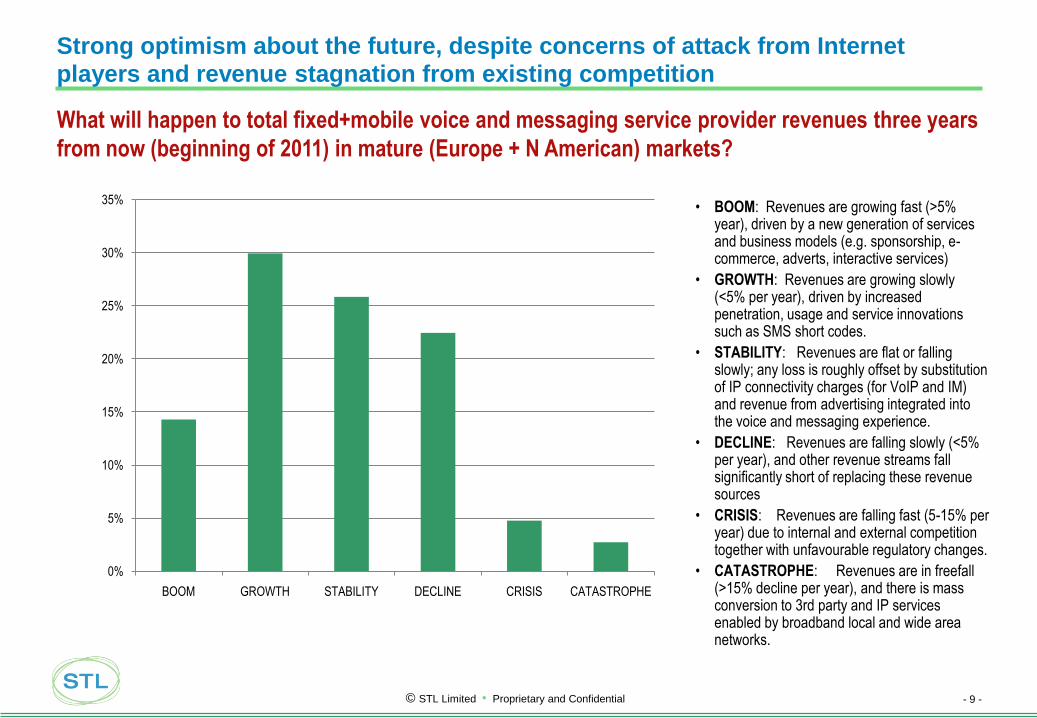

Strong optimism about the future, despite concerns of attack from Internet players and revenue stagnation from existing competition

• BOOM: Revenues are growing fast (>5% year), driven by a new generation of services and business models (e.g. sponsorship, e-commerce, adverts, interactive services)

• GROWTH: Revenues are growing slowly (<5% per year), driven by increased penetration, usage and service innovations such as SMS short codes.

• STABILITY: Revenues are flat or falling slowly; any loss is roughly offset by substitution of IP connectivity charges (for VoIP and IM) and revenue from advertising integrated into the voice and messaging experience.

• DECLINE: Revenues are falling slowly (<5% per year), and other revenue streams fall significantly short of replacing these revenue sources

• CRISIS: Revenues are falling fast (5-15% per year) due to internal and external competition together with unfavourable regulatory changes.

• CATASTROPHE: Revenues are in freefall (>15% decline per year), and there is mass conversion to 3rd party and IP services enabled by broadband local and wide area networks.

What will happen to total fixed+mobile voice and messaging service provider revenues three years

from now (beginning of 2011) in mature (Europe + N American) markets?

0%

5%

10%

15%

20%

25%

30%

35%

BOOM GROWTH STABILITY DECLINE CRISIS CATASTROPHE

- 10 -© STL Limited • Proprietary and Confidential

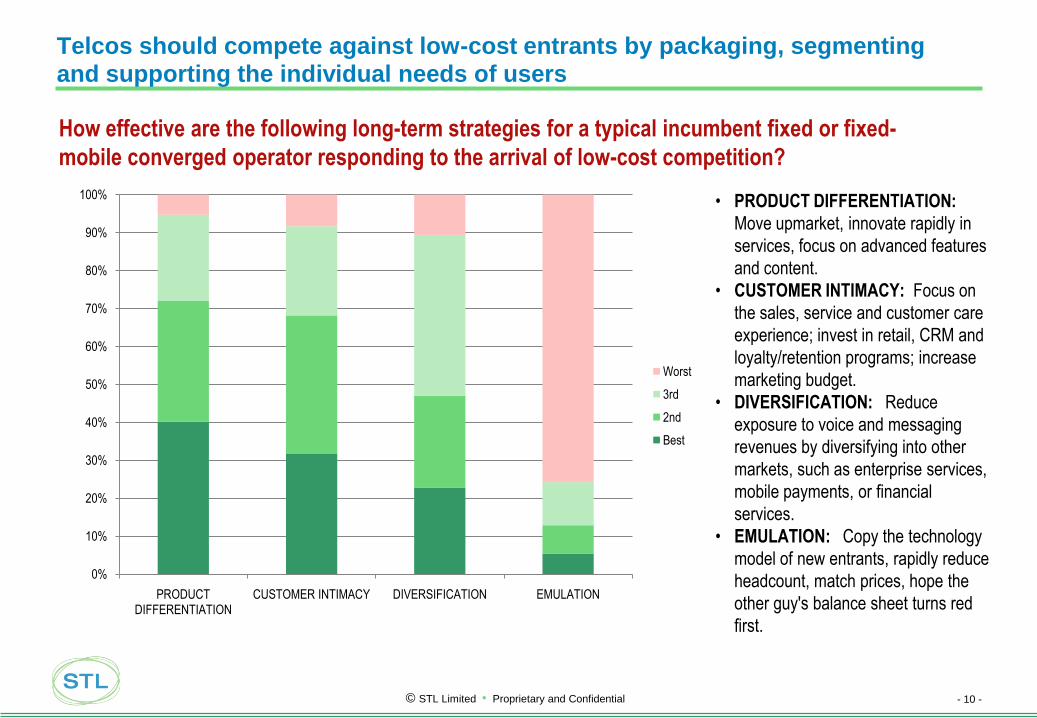

Telcos should compete against low-cost entrants by packaging, segmenting and supporting the individual needs of users

• PRODUCT DIFFERENTIATION:

Move upmarket, innovate rapidly in

services, focus on advanced features

and content.

• CUSTOMER INTIMACY: Focus on

the sales, service and customer care

experience; invest in retail, CRM and

loyalty/retention programs; increase

marketing budget.

• DIVERSIFICATION: Reduce

exposure to voice and messaging

revenues by diversifying into other

markets, such as enterprise services,

mobile payments, or financial

services.

• EMULATION: Copy the technology

model of new entrants, rapidly reduce

headcount, match prices, hope the

other guy's balance sheet turns red

first.

How effective are the following long-term strategies for a typical incumbent fixed or fixed-

mobile converged operator responding to the arrival of low-cost competition?

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

PRODUCT DIFFERENTIATION

CUSTOMER INTIMACY DIVERSIFICATION EMULATION

Worst

3rd

2nd

Best

- 11 -© STL Limited • Proprietary and Confidential

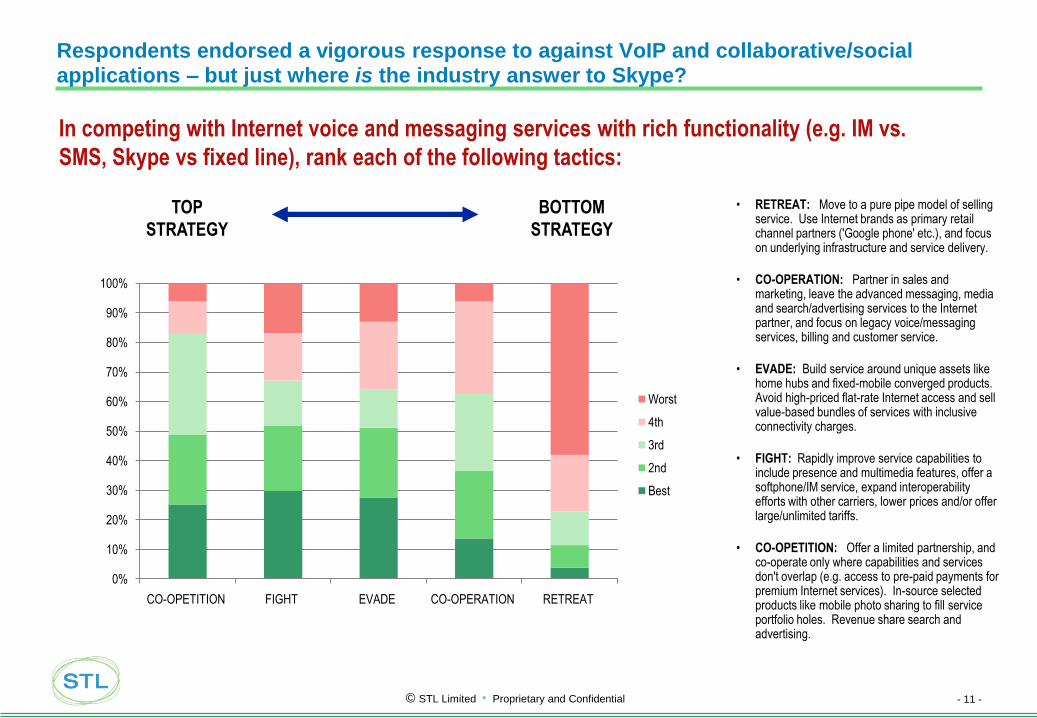

Respondents endorsed a vigorous response to against VoIP and collaborative/social applications – but just where is the industry answer to Skype?

• RETREAT: Move to a pure pipe model of selling service. Use Internet brands as primary retail channel partners ('Google phone' etc.), and focus on underlying infrastructure and service delivery.

• CO-OPERATION: Partner in sales and marketing, leave the advanced messaging, media and search/advertising services to the Internet partner, and focus on legacy voice/messaging services, billing and customer service.

• EVADE: Build service around unique assets like home hubs and fixed-mobile converged products. Avoid high-priced flat-rate Internet access and sell value-based bundles of services with inclusive connectivity charges.

• FIGHT: Rapidly improve service capabilities to include presence and multimedia features, offer a softphone/IM service, expand interoperability efforts with other carriers, lower prices and/or offer large/unlimited tariffs.

• CO-OPETITION: Offer a limited partnership, and co-operate only where capabilities and services don't overlap (e.g. access to pre-paid payments for premium Internet services). In-source selected products like mobile photo sharing to fill service portfolio holes. Revenue share search and advertising.

In competing with Internet voice and messaging services with rich functionality (e.g. IM vs.

SMS, Skype vs fixed line), rank each of the following tactics:

TOP

STRATEGY

BOTTOM

STRATEGY

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

CO-OPETITION FIGHT EVADE CO-OPERATION RETREAT

Worst

4th

3rd

2nd

Best

- 12 -© STL Limited • Proprietary and Confidential

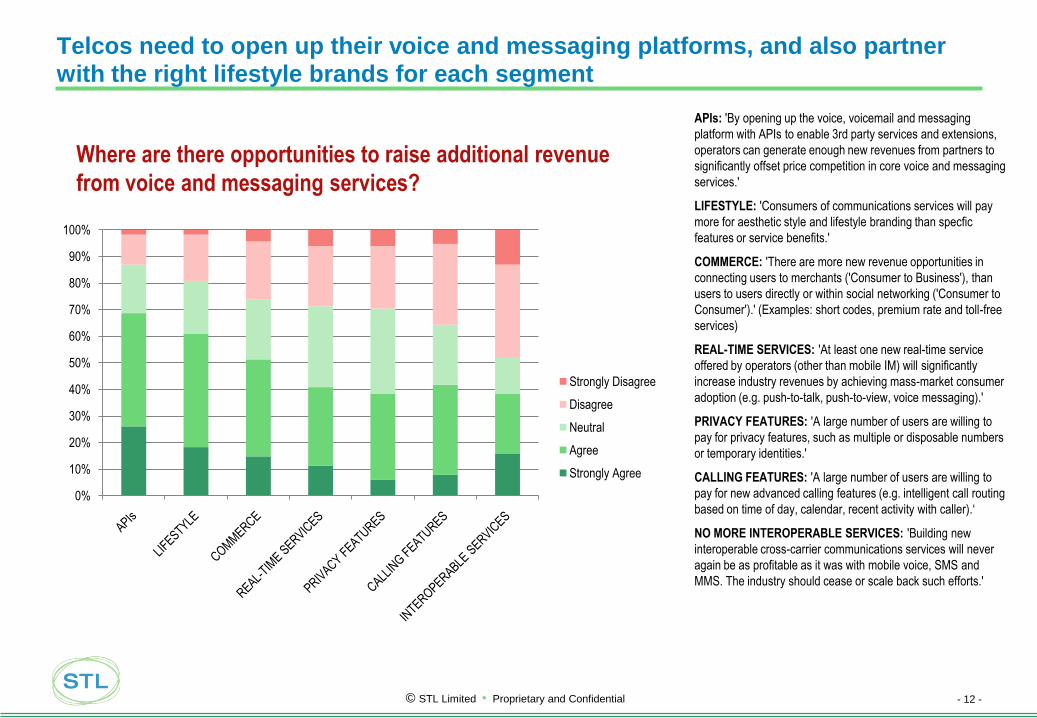

Telcos need to open up their voice and messaging platforms, and also partner with the right lifestyle brands for each segment

APIs: 'By opening up the voice, voicemail and messaging

platform with APIs to enable 3rd party services and extensions,

operators can generate enough new revenues from partners to

significantly offset price competition in core voice and messaging

services.'

LIFESTYLE: 'Consumers of communications services will pay

more for aesthetic style and lifestyle branding than specfic

features or service benefits.'

COMMERCE: 'There are more new revenue opportunities in

connecting users to merchants ('Consumer to Business'), than

users to users directly or within social networking ('Consumer to

Consumer').' (Examples: short codes, premium rate and toll-free

services)

REAL-TIME SERVICES: 'At least one new real-time service

offered by operators (other than mobile IM) will significantly

increase industry revenues by achieving mass-market consumer

adoption (e.g. push-to-talk, push-to-view, voice messaging).'

PRIVACY FEATURES: 'A large number of users are willing to

pay for privacy features, such as multiple or disposable numbers

or temporary identities.'

CALLING FEATURES: 'A large number of users are willing to

pay for new advanced calling features (e.g. intelligent call routing

based on time of day, calendar, recent activity with caller).„

NO MORE INTEROPERABLE SERVICES: 'Building new

interoperable cross-carrier communications services will never

again be as profitable as it was with mobile voice, SMS and

MMS. The industry should cease or scale back such efforts.'

Where are there opportunities to raise additional revenue

from voice and messaging services?

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Strongly Disagree

Disagree

Neutral

Agree

Strongly Agree

- 13 -© STL Limited • Proprietary and Confidential

Customers are tired of “voicemail tag” and poor UIs – help them get through to the right person at the right time, and make it easy to use

% Of respondents rating unmet needs of users in the following areas of voice telephony

1. Presence data on the called party (e.g. on call, device on/off, location, calendar data)

2. Increased network coverage and reliability, indoors and outdoors

3. Improved directory services to contact people you know

4. Better comprehension of who is talking and what they are saying

5. Easier purchase and provisioning of voice service

6. Additional multimedia features, to share text, URLs, photos and videos as part of a

conversation

7. Improved control over availability for inbound calls, and better call screening.

8. Better security against snooping and eavesdropping

9. More privacy features to enable anonymity or partial disclosure of identity (e.g.

disposable numbers).

10. Improved ease of use of the voice, conferencing and voicemail functions.

11. The ability to remit payment to the other party as a standard function of the user

interface

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Presence data

Network coverage

Directory services

Audio quality

Easier provisioning

Multimedia features

Screening control

Security

Privacy features

Ease of use

Payment features

1. CRITICAL NEEDS REMAIN

2

3

4

5. NO NEED FOR IMPROVEMENT

- 14 -© STL Limited • Proprietary and Confidential

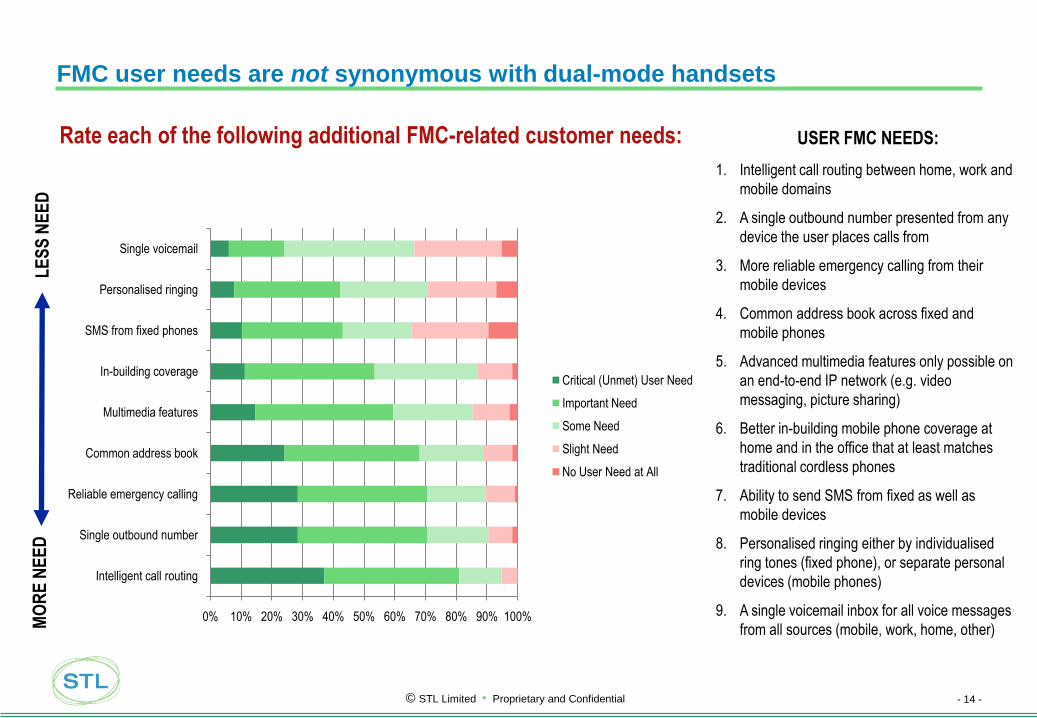

FMC user needs are not synonymous with dual-mode handsets

Rate each of the following additional FMC-related customer needs:

1. Intelligent call routing between home, work and

mobile domains

2. A single outbound number presented from any

device the user places calls from

3. More reliable emergency calling from their

mobile devices

4. Common address book across fixed and

mobile phones

5. Advanced multimedia features only possible on

an end-to-end IP network (e.g. video

messaging, picture sharing)

6. Better in-building mobile phone coverage at

home and in the office that at least matches

traditional cordless phones

7. Ability to send SMS from fixed as well as

mobile devices

8. Personalised ringing either by individualised

ring tones (fixed phone), or separate personal

devices (mobile phones)

9. A single voicemail inbox for all voice messages

from all sources (mobile, work, home, other)

USER FMC NEEDS:

MO

RE

NE

ED

LE

SS

NE

ED

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Intelligent call routing

Single outbound number

Reliable emergency calling

Common address book

Multimedia features

In-building coverage

SMS from fixed phones

Personalised ringing

Single voicemail

Critical (Unmet) User Need

Important Need

Some Need

Slight Need

No User Need at All

- 15 -© STL Limited • Proprietary and Confidential

Consumer Voice & Messaging 2.0 Market Study: proposed table of contents

Background and key issues

Key macro trends

User adoption trends for VoIP, IM and real-time services

Internet user growth trends: broadband, portal IM and VoIP

The changing nature of voice and messaging

The end of pricing plans as the focus of competition

The inversion of the telephony business model

No nines: understanding the user‟s goals -- gossip, information and presence

Balance of power: changes in the value chain

Short-term issues to address: optimising and extending today‟s business

The changing competitive landscape

Disruption from new low-cost operators: Telio, Iliad, Tesco

Disruptors from the edge: PhoneGnome , Truphone

Arbitrage players

Near-term opportunities

Optimising the current business: up-sell, cross-sell of services

Working with private voice applications – IM services, Skype, SocNets

IM meets SMS and MMS: issues and strategies

Medium-term issues to address: developing new products and services

A framework for service and product innovation

Modelling user needs, and how the existing services meet them

The “Voice 2.0” movement: what is it, and why does it matter?

Featured innovators: iotum , Grand Central , En Thinnai

Near-term opportunities

Voice messaging

“Show and tell” communicator

FMC: what do the users *really* want?

Long-term issues to address: re-thinking the business model and value chain

Contextual voice: the Web goes real-time

V-commerce: the road beyond click-to-call

Telephony in new contexts – extending the reach of telephony

Re-thinking the call model – less interruption, more conversation

From telephony to telepresence: a journey worth taking?

Case studies:

From walled garden to open garden: 3 UK and Skype

Practical pricing and product strategies: Sprint PCS Vision

Product innovation is possible: Verizon iobi

Survey results & market timing

Technology changes

Market changes

Market-by-market Telco 2.0 voice & messaging strategy plan

Fixed operators

Mobile operators

Fixed-mobile converged operators

Access-independent service providers

Equipment and software vendors

Action steps

Product planning and management

Sales and marketing; channel

Network and product development

Partner and business development

For the full Consumer Voice & Messaging 2.0 Market Study go to:

www.stlpartners.com/telco2_research-analysis_voice-messaging.php

NOTE: Subject to change

Final report includes full directory of 80+ “Voice 2.0” vendors, plus full survey results and analysis

- 16 -© STL Limited • Proprietary and Confidential

Thank You

If you would like to comment on the results of this survey or would like to explore how STL Partners could help your company be more successful in a Telco 2.0™ world, please contact Martin Geddes at the details below:

Tel: +44 (0)7957 499219

Skype ID: eddes

Read our blog for free insight and analysis: www.telco2.net/blog/

Click below to see details of our reports:

Telco 2.0™ market study: How to Make Money in an IP-based World (www.stlpartners.com/telco2_report.php)

Telco 2.0™ Strategy Reports:

Voice & Messaging 2.0 (www.stlpartners.com/telco2_research-analysis_voice-messaging.php)

Advertising-Funded Services (www.stlpartners.com/telco2_research-analysis_ad-funded.php)

Broadband Business Models 2.0 (www.stlpartners.com/telco2_broadband-business-models/index.php)

2-sided Telecoms Market Opportunity (www.stlpartners.com/telco2_2-sided-market/index.php)

For more details about Telco 2.0™ and STL Partners, please visit our website www.stlpartners.com