vol. 30, issue 5 may 2019 retirement watchbob carlson’s · retirement watchbob carlson’s...

TRANSCRIPT

Retirement WatchBOB CARLSON’S Strategies for a Secure Future

Vol. 30, Issue 5 May 2019

Dear Reader:Most people spend too much time and

energy on investing and not enough on other personal finance matters.

When people learn what I do, most of them soon ask me questions about investing and the markets.

The smart ones ask me questions about other aspects of personal fi-nance. The questions depend on their situation, but they might cover estate planning, converting individual retire-ment accounts (IRAs), Medicare or other issues.

I say these are the smart people be-cause they know there’s a limited amount

you as an individual investor can do to increase investment returns. We can and do make a few key trades to catch an investment near its low or sell near its high before a significant decline. It is worthwhile to spend some time trying to get these major asset allocation changes right. But most people spend far too much time thinking and worrying about the markets given the limited effect they can have on what the markets will do. They also focus too much on short-term moves, trends and news.

In the end, many people either make too many trades in their portfolios or become paralyzed into inaction.

Often, the resources devoted to other personal finance issues have direct, substantial and immediate effects on your bottom line. You want to avoid paying too much in taxes or having an estate plan that is incomplete, out of date or nonexistent. You don’t want to leave a lot of money on the table when claiming Social Security benefits, managing your IRAs and taking other retirement-related actions.

It is important to manage your investments well. But be sure to spend your time and resources on a balance of retirement finance issues.

Roth IRAs Are Compelling Estate Planning Tools

Roth IRAs can be power-ful additions to your estate plan, regardless of your age.

Most people focus only on lifetime income taxes when discussing Roth IRAs. Roths can be powerful tools that help meet your estate planning goals, leaving your heirs with more after-tax wealth.

An IRA will be included in your

estate whether it is a traditional or Roth IRA. That doesn’t matter to most people these days, because their estate won’t face federal estate taxes. But it can matter if you live in a state with an estate or inheritance tax. It also will matter to more people if the current estate tax exemption amount expires after 2024 as scheduled and reverts back to the previous level.

The only way to keep an IRA from being included in your estate is to empty it, pay the income taxes and

transfer the after-tax amount outside of your estate.

The real issue for most of us is how the IRA distributions will be taxed, especially to our heirs.

A beneficiary who inherits a tradi-tional IRA must take required mini-mum distributions (RMDs) from the inherited IRA. Those distributions will be taxed the same way they would be for you. Most IRA distribu-tions will be fully taxed as ordinary

(Continued on page 2)

Strategies for Shifting Ownership of a Small Business . . . . . 3

Why Beneficiaries Overpay Taxes on Inherited IRAs . . . . . . 5

The War on Stretch IRAs Is Back . . . . . . . . . . . . . . . . . . . . . . . . . 6

Maximizing the Power of Donor-Advised Funds . . . . . . . . . . 7

In This IssueThe Tarkenton Plan to Avoid Financial Scams and Abuse . . . 9

Emerging Markets Have Value and Potential . . . . . . . . . . . . . 10

Speculative Markets Have a Few Pockets of Opportunity . . . 11

How to Become #1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Actions to Create the Retirement You DesireMay 2019 2

income.The beneficiary can take the dis-

tributions over his or her life expec-tancy or until the money is needed, taking advantage of the tax-deferred compounding of the IRA. But the beneficiary inherits only the after-tax value of the IRA, not the full value.

Also, consider the income taxes during your lifetime.

After age 70½, you must take RMDs from a traditional IRA, whether you need the money or not.

As we’ve discussed in the past, RMDs often cause income tax prob-lems for IRA owners. The RMDs generate taxable income. They also increase adjusted gross income (AGI). Higher AGI can mean more of your Social Security benefits are taxed and you might owe the Medi-care premium surtax.

An alternative as part of your estate plan is to convert a traditional IRA or 401(k) to a Roth account.

Of course, there is an income tax bill for converting the account. The amount you convert is included in gross income as ordinary income and taxed at your regular tax rate. In effect, you’re paying the taxes early instead of waiting for the IRA to be distributed over the years.

Once that is done, there will be several long-term benefits.

First, you’re in effect paying in-come taxes for your heirs. They would have owed the taxes in the

future when taking distributions from the IRA. Instead, you pay them now, and there are no estate or gift taxes on that gift. In addition, you and your heirs avoid any taxes on future income and gains earned by the IRA.

Second, paying the taxes now reduces the size of your estate and any taxes on it. This is key for taxable estates and also is important when you live in a state with an estate or inheritance tax.

Remember, the traditional IRA has an embedded income tax bill. Your beneficiary enjoys only the after-tax amount, not the market value of the traditional IRA. But federal and state death taxes will be imposed on the market value. The estate taxes would be paid on the embedded income taxes.

Third, the conversion provides lifetime income tax benefits to you. When you don’t need the RMDs after age 70½ to meet expenses, they simply increase your taxes. The older you are, the higher the percentage

of the IRA that must be distributed each year.

RMDs and all the taxes they trigger turn tax planning on its head. You and your beneficiary are likely to be better off when you pay the taxes early, such as in a conversion. After that, there are no RMDs for you, and the IRA compounds tax free.

There are several factors to consid-er before deciding that converting an IRA to a Roth IRA should be part of your estate plan.

• Compare current and expected future tax rates for you and your bene-ficiaries. A conversion makes the most sense when future income tax rates are expected to be higher. But it also can make sense when you expect tax rates to be the same, especially if distribu-tions will be spread over 12 years or more.

A conversion makes less sense when you anticipate the IRA ben-eficiaries are likely to be in a lower tax bracket than you. Then, it often is best to leave the traditional IRA intact and let beneficiaries pay in-come taxes on distributions over the years at their lower rate. But that also assumes you won’t be forced to draw down most of the IRA during your lifetime through RMDs.

• This strategy also shouldn’t be used if you’re likely to need most of the IRA balance during your lifetime. It’s best used by the many people who are reserving their IRAs for emergencies

Bob Carlson’s Retirement Watch™ (ISSN 1077-3924) is edited by Robert C. Carlson and published monthly by Eagle Products, L.L.C., 300 New Jersey Ave, NW, Suite 500, Washington, D.C. 20001, Customer service: 800-552-1152. E-mail: [email protected]. Website: www.RetirementWatch.com. Subscription cost is $99 annually. Copyright 2019 by Eagle Products, L.L.C. POSTMASTER: Please send address changes to Bob Carlson’s Retirement Watch, Subscriber Services Department, P..O. Box 1901, Williamsport, PA 17701. Postage paid at periodical rates at Centreville, VA and additional mailing offices. The information in this newsletter is from sources believed reliable, but no guarantee or warranty is made as to its accuracy. The editor, owners, and publisher, as well as their clients, employees, associates and/or family may have positions in securities and instruments recommended or reviewed in this newsletter. The editor and publisher assume no liability for the reader’s use of the information contained herein. Letters and e-mail from readers are encouraged. Editor: Robert C. Carlson; Editorial Director: Paul Dykewicz; Group Publisher: Roger Michalski.

A conversion makes the most sense when future

income tax rates are expected to be higher. But it also can make

sense when you expect tax rates to be the same

www.RetirementWatch.com May 2019 3

or as something to leave their heirs. The longer you can leave the IRA to compound after the conversion, the more a conversion pays off.

• Consider the amount of char-itable giving you plan during your lifetime and through your estate. It makes a lot of sense to make chari-table gifts through a traditional IRA. During your lifetime, you can make qualified charitable distributions. Through your estate, you can name one or more charities as beneficiaries

of your traditional IRA. To the extent you make charitable gifts, it is better to make these through your IRA than to leave the IRA to your loved ones. Leave your loved ones other assets, if you can.

• An IRA conversion is not an all-or-nothing event. You can convert part of your IRA when that makes sense. For example, you can retain enough in your traditional IRA to make planned charitable gifts and to have available as a cushion for your retirement

expenses. The rest you can convert to a Roth IRA to leave to your heirs. Or if you don’t want to pay the taxes to convert the entire IRA, you can con-vert only part of it or convert a portion each year for a period of years.

There’s still a myth circulating that Roth IRAs are only for relatively young people. In fact, they can be powerful estate planning tools that provide benefits to you and your heirs for decades.

Shrewd Strategies for Shifting Ownership of a Small Business

One of the more difficult estate planning problems is transferring a small business in

a way that maximizes after-tax value.Unfortunately, many business owners

don’t handle the transition well. Planning for a small business tran-

sition should begin at least five years before the transition might occur. You should take the key steps that make a business more attractive to potential buyers.

The business systems need to be much tighter than they are in most small businesses. A potential buyer wants reliable and comprehensive data. The accounting data is the most important to most buyers. But data analysis of all aspects of a business is a major tool these days. You might need to upgrade your systems to provide detailed data about all facets of sales, production, marketing and other functions.

You also want to convince buyers the business isn’t dependent on one person. Many small businesses are reliant on their founders and owners. To maximize the value, build a team of people who are responsible for different functions. A buyer will pay more for a quality workforce with low turnover that’s likely to remain when ownership changes.

You want a diversified revenue base.

A buyer will be hesitant to purchase a company that relies on a small number of customers or products, especially when sales are dependent on a person-al connection with the owner.

You also want to focus on growth. Many buyers won’t pay top dollar for a firm with stagnant revenue, even if it’s

making a healthy profit. Make your business all about busi-

ness. Many small businesses often have some overlap between the owner’s per-sonal and family interests. There might be family members on the payroll who are being paid more than they would receive at other firms. Whenever possi-ble, personal expenses are run through the business.

That’s all smart when you plan to keep the business indefinitely. But as you prepare to sell, phase out the per-sonal and family subsidies.

You’re likely to receive more by using a team of experts to help sell the business.

One or more business valuation experts should help you determine a reasonable value. They should explain how they arrived at their values and the likely range of values outsiders will put on the business.

You’ll also want accountants and lawyers who specialize in small business transitions. Ideally, you have tax and non-tax specialists, though

Planning for a small business transition

should begin at least five years before the

transition might occur.

Actions to Create the Retirement You DesireMay 2019 4

some advisers are good at both angles. They’ll help implement the strategies already discussed and suggest others. When you select the right profession-als, their advice will more than pay for their fees.

Finally, consider how to structure the transaction to maximize your after-tax value. There are many op-tions. Begin reviewing them early in the process so you can substantially reduce the taxes. Too many business owners wait until a deal is reached and then start wondering how to reduce the taxes. By then, it’s often too late to take effective action. Here are some key strategies to consider.

The charitable trust bailout. Before you conclude or even negotiate a sale, transfer the business to a charitable remainder trust.

In the typical structure, the trust will pay you and your spouse income for as long as either is living. In most cases, the payout is either a percent-age of the trust’s value at the begin-ning of the year or a fixed annual annuity.

After you and your spouse pass away, a charity or charities you designated will receive the property remaining in the trust.

You receive a charitable contribu-tion deduction when a property is transferred to the trust. The deduction is equal to the present value of the charity’s expected future gift. There are no capital gains taxes when the busi-ness is sold, because it will be owned by a charitable trust. The trust is free to invest all the sale proceeds to generate income for you.

A variation of the strategy is to separate the business into different segments. For example, the operations of the business might be one segment and the real estate from which it oper-ates (if you own it) is another segment. You hold one segment in your name and sell. Transfer the other segment to a charitable remainder trust.

The strategy has two advantages.

One advantage is you retain control of some of the sale proceeds. The other advantage is that the charitable de-duction from transferring a segment to the trust offsets some or all of the taxable gain from the sale of the other segment.

Employee stock ownership plan (ESOP). When you want to sell to current employees, an ESOP can be a good tool.

There are many variations of the ESOP strategy, but here’s a standard one.

A small business owner creates the ESOP. The company borrows money from a bank and, in turn, lends that money to the ESOP. The owner sells some or all of his stock to the ESOP. Over time, the company makes annual contributions to the ESOP, which are deductible. The ESOP uses the money to repay the loan from the company, which the company uses to repay the loan from the bank.

Special tax breaks allow the company

to deduct both the interest and princi-pal it pays on the loan. It also deducts contributions made to the ESOP, as well as any dividends it pays on com-pany stock owned by the ESOP.

The owner also gets tax breaks. A gain from the sale of the stock to the ESOP is deferred if, within a year, the owner uses the proceeds to purchase securities issued by domestic com-panies and meets other restrictions. Taxes are due only as the owner sells those investments.

An ESOP is best for an owner who plans to sell to the employees and whose children don’t want to run or own the company. But it can work in other situations. There are a host of detailed rules for ESOPs. For example, all employees must be allowed owner-ship shares through the ESOP. Review the details with your advisors before making a decision.

Corporate redemption. This is a good strategy when you want to trans-fer the business to your children. Here’s how it worked in one case. A taxpayer owned 100% of a corporation. His adult children were directors, and he wanted them to take over both owner-ship and operation of the business.

He gave some of his stock to the kids. The business redeemed the rest of his shares in exchange for an installment note. The children now owned 100% of the outstanding stock, and he received regular payments from the company under the note.

A stock redemption qualifies for long-term capital gain treatment when the selling shareholder terminates all his interest in the corporation, other

You’re likely to receive more by using a team of experts to help sell the

business.

www.RetirementWatch.com May 2019 5

than any interest as a creditor. Also, the gift of stock to the children can’t be primarily tax motivated. The IRS said this particular transaction met all the requirements, so the owner paid long-term capital gains on the redemption

of the stock.But do this type of transaction

wrong, and the redemption will be treated as a dividend to either the chil-dren or to you.

Those are examples of tax-wise

strategies for selling a business. Talk with your advisers about different strategies early in the transition process to find the one that’s best for your goals and situation.

Why Beneficiaries Overpay Taxes on Inherited IRAs

The most frequent, most expensive mistakes with IRAs occur when it’s time to pass the

IRAs to the beneficiaries.Sometimes the fault is with the

original owner. Sometimes the fault is with the beneficiaries. In either case, the mistakes cause the tax-deferred compounding of the IRA to be lost. Income taxes are paid earlier than they needed to be, and beneficiaries have less after-tax wealth than they could have.

Most owners of large IRAs say they don’t plan to use all of the IRAs during their lifetimes. They’re saving as much of the balances as possible for the next generation to inherit. They also hope the beneficiaries will keep the bulk of the assets in the IRA for years, or even decades, so the tax-deferred com-pounding can continue working.

Yet, mistakes made when trying to navigate the tax law cause the IRA to be taxed earlier than hoped. A new obsta-cle to extending the life of your IRA is a law making its way through Congress. See the next article in this issue for details about that.

Here’s a checklist that every IRA owner and beneficiary should review

to make an IRA last as long as possible under current law.

The beneficiary form is the first key to maximizing the after-tax wealth of an inherited IRA.

To maximize the tax deferral of an IRA for your heirs, you need to name one or more individuals, and only individuals, as beneficiaries on a valid beneficiary form. The only exception is a qualified trust as beneficiary, but it must be a trust with the right terms.

If you don’t name a beneficiary of your IRA, your estate will be considered the beneficiary. Under IRS regulations, when an estate is the beneficiary, the en-tire IRA must be distributed and taxed quickly, usually within five years.

The same rule applies when the wrong kind of trust is named beneficia-ry or when you name any beneficiary other than an individual.

Your beneficiary designations should

be reviewed any time there is a major life event in your family, such as a birth, adoption, marriage, divorce, death, or someone coming of age. It’s a good idea to take a look at the designations every few years, even if there hasn’t been a major life event, in case you changed your mind.

Most estate planners recommend that you also name contingent beneficiaries and that they all be individuals. If your primary beneficiaries predecease you, choose to disclaim the inheritance, or for some other reason aren’t able to inherit the IRA, you want other indi-viduals to be able to do so. Otherwise, your estate becomes the beneficiary and the IRA must be distributed within five years. Another good idea is to name a charity as a final contingent beneficiary to ensure the estate never is beneficiary.

There are good reasons to name a trust as an IRA beneficiary. The main reason is the intended beneficiaries are minors or it is feared they wouldn’t be responsible with the money. So, a trust is created to ensure the beneficiaries are provided for but aren’t able to waste the money. The trust is the IRA beneficiary, and the individuals are beneficiaries of the trust.

But a trust must have specific terms when it is the IRA beneficiary.

Income taxes are paid earlier than they needed to be, and beneficiaries

have less after-tax wealth than they could

have.

Actions to Create the Retirement You DesireMay 2019 6

Otherwise, the IRA must be distributed within five years. We discussed the trust rules in detail in our May 2017 issue.

Another key point is the IRA des-ignation form must name the trust as the beneficiary. Many people have the trust drafted and then forget to name the trust on the beneficiary designation form.

In addition to naming proper benefi-ciaries, the IRA owner needs to keep a current copy of the beneficiary desig-nation form for each IRA. Be sure your executor and other key people know how to find the forms. If people can’t locate the forms, there might be legal and other fees incurred to determine who has the right to the IRA. Of course, there also could be higher taxes.

You shouldn’t rely on the IRA custo-dian to have the most current benefi-ciary designation form. Errors can be made, especially when there are merg-ers, changes of ownership or moves to new locations. You need to keep a copy of the latest form, be sure it is dated and write “superceded” or something similar on old forms.

Once the IRA owner has the benefi-ciary designation forms squared away,

the beneficiaries need to know the ac-tions they need to take and the mistakes to avoid.

You should talk with your beneficia-ries about your intentions and theirs for the IRA. IRA custodians report that a high percentage of beneficiaries fully distribute inherited IRAs within a few years. They don’t try to have stretch IRAs that take advantage of tax-de-ferred compounding for years.

What’s not known is if this is delib-erate or if it’s done because they don’t know all the options they have and the value of the tax-deferred compounding.

When your goal is to have the IRA provide for your beneficiaries over the years, tell them that and let them know the steps they need to take.

The first step for a beneficiary is to be sure the IRA is properly retitled.

Many beneficiaries mistakenly contact the IRA custodian and say they want the IRA shifted into their names or rolled over to their existing IRAs. Either move makes the full IRA balance immediately taxable.

Instead, the account needs to be reti-tled as an inherited IRA. The new title of the IRA should contain the name

of the original owner, that he or she is deceased, and that the IRA is being held “for the benefit of” or “FBO” the beneficiary. Each IRA custodian has a variation of the wording.

The beneficiaries also should double check and be sure only individuals are potential beneficiaries. If any non-in-dividuals are beneficiaries, they can be removed by having their shares fully distributed to them or by splitting the IRA into separate IRAs for each bene-ficiary.

Finally, the beneficiaries must begin RMDs by Dec. 31 of the year following the owner’s death.

When the first RMD is missed, the beneficiaries still might be able to reme-dy the situation. They can distribute the RMDs that should have been taken and pay the penalties for not taking them on time. (Or they can apply for a waiver of the penalty. See our April 2019 issue for details.) Then, they can take the rest of the RMDs on schedule.

Beneficiaries always can take more than the RMD. But they have to take at least the RMD each year if they want the option of maximizing the IRA’s tax deferral.

The War on Stretch IRAs Is Back

There long has been a group in Congress determined to end the Stretch IRA, and this

year they seem intent to have their way.I’ve reported in the past few years that

many in Washington were targeting the Stretch IRA. The Obama administration

called for an end to this valuable estate planning tool in its annual budgets. A bipartisan group in Congress agreed, and it appears that group is growing.

Their latest vehicles are two retirement bills working their way through Congress. The version in the House of Representa-tives is called “Setting Every Community Up for Retirement Enhancement” (the SECURE Act). The Senate version is titled

“Retirement Enhancement and Savings Act” (RESA).

The bills have a number of provisions, many beneficial to retirees and pre-retir-ees.

One goal is to give more workers, es-pecially small business employees, access to employer retirement plans. Small businesses would receive a credit of up to $500 annually to defray the start-up costs

www.RetirementWatch.com May 2019 7

of some retirement plans. Also, long-time part-time workers would be allowed to contribute to their employers’ plans.

Groups of unrelated employers would be allowed to band together to offer retire-ment plans to their employees, known as multiemployer plans. This should make the plans less expensive so more small employers can offer them. Currently, em-ployers must have a common bond, such as being in the same industry, to form a multiemployer plan.

There would be two key benefits for individuals.

Deductible IRA contributions could be made after age 70½. Currently, only Roth IRA contributions and nondeductible IRA contributions can be made after age 70½.

Also, required minimum distributions wouldn’t begin until age 72 for most indi-viduals, instead of the current 70½.

But Congress has to find a way to pay for these benefits. The main way to pay for them is to sharply curtail the Stretch IRA. The Stretch IRA isn’t a special type of account. Instead, it is a series of actions

and strategies that allow beneficiaries of an IRA to maximize its tax-deferred compounding, making it last for years or even decades after they inherit it.

The Senate and House bills have different limits on the Stretch IRA. The House would require beneficiaries to fully distribute inherited IRAs within 10 years. There would be exceptions for surviving spouses and minor children. The Senate version would allow the full Stretch IRA but only for the first $450,000 per IRA owner. The rest of an inherited IRA would have to be distributed to the beneficiary and taxed.

A version of the two bills is expected to become law, probably this year. The basics of the bills have strong support in both parties, and the House version already has made it through committee and could be voted on by the full House soon.

It is too early to know which limit on the Stretch IRA will be enacted. It is even possible neither will pass. A version ap-peared in early drafts of the Tax Cuts and Jobs Act enacted in 2017, but the Stretch IRA provision was dropped from the final

bill. Congress has changed since 2017. For the provisions to be dropped again, Congress would have to find another way to raise revenue to pay for the benefits in the bills.

Many members of Congress have been following the growing retirement plan balances of the Baby Boomers for de-cades. Federal budget planning anticipates this money being distributed from the plans in the coming years and boosting federal tax revenue. The attack on the Stretch IRA is to ensure the federal gov-ernment receives taxes on IRA balances during the Baby Boomers’ lifetimes. Many in Congress don’t want that money left in IRAs to be trickled out over the lifetimes of the Boomers’ children.

The Stretch IRA remains a viable and valuable estate planning tool. But it seems inevitable Congress will end or curtail it at some point. Next month we’ll discuss strategies that can ensure your IRA balance benefits your heirs for decades, regardless of what Congress does with these bills.

Maximizing the Power of Donor-Advised Funds

Donor-advised funds steadily increased in popularity over the years, but their use soared

after the Tax Cuts and Jobs Act of 2017. Their popularity is likely to continue increasing.

Also known as a charitable gift fund, the donor-advised fund (DAF) took off after the early 1990s. Fidelity Charitable is believed to have set up the first national

DAF in 1991. Local and regional DAFs existed for many years before that.

The DAF gives everyone else many of the tax and charitable giving advantages previously reserved only for those who were wealthy enough to set up private foundations. Now, planned charitable giv-ing is low-cost, national and convenient.

A DAF is created or sponsored by a charity. Most large national DAFs are related to charitable arms of major brokerage or mutual fund firms, with the largest organized by Fidelity, Schwab and Vanguard.

The taxpayer opens an account with

The DAF gives everyone else many of the tax

and charitable giving advantages previously reserved only for those

who were wealthy enough to set up private

foundations.

Actions to Create the Retirement You DesireMay 2019 8

the DAF and makes a contribution. The contribution qualifies for an immedi-ate charitable contribution income tax deduction.

Though you have an account in your name, it isn’t money you can get back. The money can only be donated to qualified charities.

Donations can be made whenever it suits the donor. Unlike a private founda-tion, there’s no minimum annual giving requirement. DAFs also are private; dona-tions aren’t publicly reported.

Money waiting in the account is invest-ed according to the donor’s choices from among investment options designated by the fund.

A big advantage of the DAF is you can take one large charitable deduction when it makes sense for you. You might want to make a large gift in a year when you have unusually high income, say, from a bonus or from selling an asset with a large capital gain. The DAF also can be used as a tax-efficient way to dispose of an asset in which you have a large gain. Instead of selling it and incurring the long-term capital gains taxes, you can donate all or part of the investment. You receive a char-itable contribution deduction equal to the current fair market value of the asset. You don’t pay taxes on the capital gain.

The DAF is more attractive now because of the changes made by the Tax Cuts and Jobs Act.

You take a charitable contribution de-duction only when you itemize expenses on Schedule A of your Form 1040. Far fewer people itemize expenses now be-cause of the tax law changes.

One change is that the standard deduc-tion was doubled. You itemize expenses

only when their total exceeds the standard deduction. With the standard deduction doubled, fewer people reach the threshold for itemizing expenses, so they receive no extra tax benefit from charitable giving.

Another change is that several itemized expenses were reduced or eliminated. State and local taxes are deductible only to a maximum of $10,000 annually. Miscel-

laneous itemized expenses were elimi-nated. Again, those reductions mean far fewer people itemize expenses.

That’s where the DAF can fill a gap.Instead of making charitable contri-

butions each year, you can bunch several years of contributions in one year by donating cash or property to a DAF. Give enough so that you’ll be able to itemize ex-

penses that year and receive a tax benefit from the contribution.

Once the contribution is in the DAF, you can make regular donations over time from the DAF to charities as you did in the past. Or you can let the invest-ment returns accumulate and give larger contributions in the future. You receive the deduction when you donate to the

DAF, even if you don’t have the DAF give to charity until a future year.

Deductions of cash contributions gen-erally are limited to 60% of your adjusted gross income for the year. The deduction limit for contributions of long-term capital gains property usually is 30% of adjusted gross income (AGI). Don’t forget to consider the effects of the alternative minimum tax when planning how much to give.

Many DAFs make giving easy by giving you a checkbook. When you’re ready to make a gift, simply write a check as you do when giving from your personal checking account. You can make it appear you have a private foundation through the name printed on the checks, such as “Max Profits Charitable Trust.” Some DAFs let you designate gifts through websites.

Technically, these are “donor-advised” funds, so you’re only making a recom-mendation to the DAF. But DAFs usually make the recommended contributions as long as they are to IRS-approved charities.

Most donor-advised funds allow you to start with $5,000. You can choose one of the DAFs sponsored by financial services companies or seek out a DAF sponsored by a local charity, coalition of charities, national charity, or university.

You can learn many local and regional options at www.cof.org/communityfoun-dationlocator. (Ignore any hyphens.) Be aware that DAFs sponsored by a charity or focused on a region usually require a minimum percentage of the contributions be made to the associated charities.

Of course, compare fees and expenses. They won’t reduce your charitable de-duction, but they will reduce the amount of money that’s available to give. Also,

A big advantage of the DAF is you can take one large charitable

deduction when it makes sense for you.

The DAF is more attractive now because of the changes made by the

Tax Cuts and Jobs Act.

www.RetirementWatch.com May 2019 9

examine any giving limits. Some funds limit the number of individual contri-butions you can make or checks you can write each year without incurring addi-tional expenses. There might be a mini-mum individual donation amount, and a minimum account balance might have to

be maintained. The financial services companies gen-

erally accept contributions to the account only in cash and securities. Some DAFs sponsored by charities, however, accept many kinds of assets, including real estate, art and limited partnerships.

You can make the DAF a family activity. Family members can gather periodically to discuss which charities should receive gifts. Or you can give each child discretion over a DAF account or an amount of the account.

The Tarkenton Plan to Avoid Financial Scams and Abuse

Financial scams and abuse, especially against older Americans, more than doubled over the

last five years, according to reports from financial services firms.

Part of the reason for the increase is that financial firms are more alert for signs of fraud and abuse. They also have more actions they’re allowed to take when they see problems. Another reason is that the Baby Boomers are getting older, so there are more targets than in the past.

NFL Hall of Fame quarterback Fran Tarkenton recommends every person age 65 or older implement a plan he devel-oped and put into a book he co-authored, Safe and Secure (Regnery 2019). The plan is consistent with my past recommenda-tions. The 79-year-old Tarkenton says he’s concerned about fraud and abuse because it’s growing rapidly and is hurting people in his age group.

The first and most important step is to avoid isolation. Tarkenton recommends that everyone develop a team of at least four trusted people. He recommends for most people the team include a family member, accountant, attorney and finan-cial adviser.

Each member of the team should know

what’s going on with your finances and be consulted before major actions. Also, you need to be in charge as much as you can rather than letting one group member lead the agenda and control information.

At some point, you probably won’t be able to remain in charge and make good decisions. By that time, you should have selected someone to act as your agent under a power of attorney, what Tarken-ton calls a financial caregiver. It’s especially important to have established the team or circle of advisers before this point. You’ll want several people providing checks and balances. And with four people, it’s hard for them to conspire to take advantage of you.

Another recommendation is to sim-plify your finances as much as possible. Consolidate your investments at one or two brokers or mutual funds. If you own complicated or unconventional assets, at some point you should liquidate them, pass them on to the next generation, or hire trusted people to manage them.

Another way to simplify is to put a portion of your nest egg in annuities, such as immediate annuities providing guaran-teed income for life. The insurer does the investing. And it’s harder to steal money that’s being held by an insurer that pays you a fixed amount monthly.

Organizing your documents and

records also is key. As you age, good organization makes it easier to stay on top of things and helps your advisers stay fully informed. Good organization also ensures things won’t be lost or mishandled during the transition to the next generation of owners and managers of the assets.

Tarkenton says to be transparent. Don’t be secretive about your financial affairs with your team. It is tough for people to help you and protect you when they don’t have a clear picture of your financial affairs.

Simplification and transparency apply to your team of advisors as well. You should be able to understand what they’re doing or recommending, and they should be transparent about what they’re doing on your behalf.

Of course, Tarkenton urges people to protect their personal identity informa-tion. We’ve discussed this many times in the past.

The key step is not to be isolated. You should have a range of social activities and friends, of course. But it’s also good to seek advice from several people regarding your finances and be sure each of them knows what’s going on. These checks and balanc-es and different sources of information maximize your protection.

Investment Recommendations and PorfoliosMay 2019 10

Emerging Markets Have Value and Potential This is a good

time to make your portfolio more diversified globally.

The United States has led the global economy and mar-kets since about 2013 and especially since 2016. The global economy slowed and many markets around the world tumbled while U.S. markets marched higher.

But in late 2018, the U.S. economy slowed noticeably in response to the Fed-eral Reserve’s tighter monetary policy, and U.S. stocks finally had a correction.

After the Fed paused its tightening poli-cy, U.S. stocks began climbing back toward their all-time highs. But the economy probably will slow further, and stock prices are based on a lot of hope. Investors expect the Fed to cut interest rates in 2019. They think inflation won’t change and economic growth will stay near its 2018 rate.

I think there’s a lot more uncertainty about the economy than is priced into the U.S. markets. It is possible the Fed managed its policies just right. But there’s little room for error, because if economic growth falls too much, the Fed has few stimulus tools available after the extreme measures it took following the financial crisis.

The good news about the U.S. economy is that the banking sector is in better shape than it usually is this late in the cycle. It is not overleveraged. As the Fed withdrew

liquidity the last couple of years, banks were able to increase their lending to businesses to replace a lot of that liquidity.

While we wait to see if the Fed tightened too much, there are interesting opportuni-ties outside of the United States.

The Fed’s tightening affected other countries, especially emerging markets, before the United States. Many of those economies had recessions or severe slow-downs and bear markets in stocks, bonds and currencies.

A number of these overseas markets and economies began to form bottoms in 2018 as growth was stalling in the United States.

China, in particular, stum-bled and dragged down global growth. China’s policymakers deliberately slowed growth and took various regulatory actions to reduce imbalances in the economy and steer the economy away from ex-ports and excess real estate development.

China resumed economic stimulus policies last year, and the country is showing positive results. In addition, China has far more policy options than the United States and most devel-oped nations. It can add stimu-lus to its economy as needed.

Higher growth in China stimulates growth in many emerging economies, especially in other Asian economies. They are dependent on exports to China.

We began introducing emerging market assets into our portfolios a few months ago with the addition of emerging market bonds to the Retirement Paycheck portfo-lio. We’ll be adding more of these assets to our portfolios this month.

Not all international markets are healthy or provide a margin of safety.

Europe continues to struggle. Even

Investment Recommendations

2018

-04-09

2018

-06-09

2018

-09-09

2018

-11-09

2019

-02-09

2.00

2.20

2.40

2.60

2.80

2019

-04-09

3.40

3.20

3.00

10-Year Treasury Rate

Bank Lending to Businesses

0.0

4.0

6.0

8.0

2013

-10-01

2015

-01-01

2016

-04-01

2017

-02-01

2017

-12-01

2.0

10.0

2018

-10-01

12.0

www.RetirementWatch.com May 2019 11

Germany, which for a long time has been one of the few growing economies on the continent, is faltering. The European Central Bank had to back away from its announced intention to end quantitative easing. Interest rates are negative again in some European countries and inflation is extremely low.

Italy has significant debt problems

that I don’t think are receiving enough attention. It remains a potential powder keg for the region.

The U.S. economy is likely to slow for a few more months before it stabilizes at a lower rate than in 2017 and 2018. My best estimate is that a recession isn’t likely if the Fed maintains its neutral policy.

U.S. markets are priced with an

expectation that the Fed will begin easing policy in 2019. If the Fed doesn’t follow through, there’s likely to be an adverse reaction in the markets.

I like a margin of safety. I see it in some international markets now where there are lower valuations and expectations are modest. There’s far less of a margin and far more uncertainty in U.S. markets.

Speculative Markets Have a Few Pockets of OpportunityInvestors are

more speculative than a few months ago.

The closed-end mutual

funds in our portfolios show the specu-lation. Their share prices have increased more than their net asset values. As a result, these funds sell at lower discount to their net asset values than their six-month averages. Investors are taking more risk and accepting lower margins of safety.

That’s quite a turnabout from late 2018, when stock prices were declin-ing rapidly. Investors worried the Fed would tighten too much and plunge the economy into recession.

Another sign that investors are taking more risk is that growth stocks again are leading the way.

We benefit from the resurgence of growth stocks through WCM Focused International Growth (WCMRX).

The fund is highly selective, owning only 32 stocks, and holds most of its positions for years. The 10 largest posi-tions make up almost 40% of the fund.

WCMRX seeks companies with high growth that it believes are sustainable.

It wants companies with little or no debt and high returns on capital. Those

companies should benefit from key global trends and benefit from one or

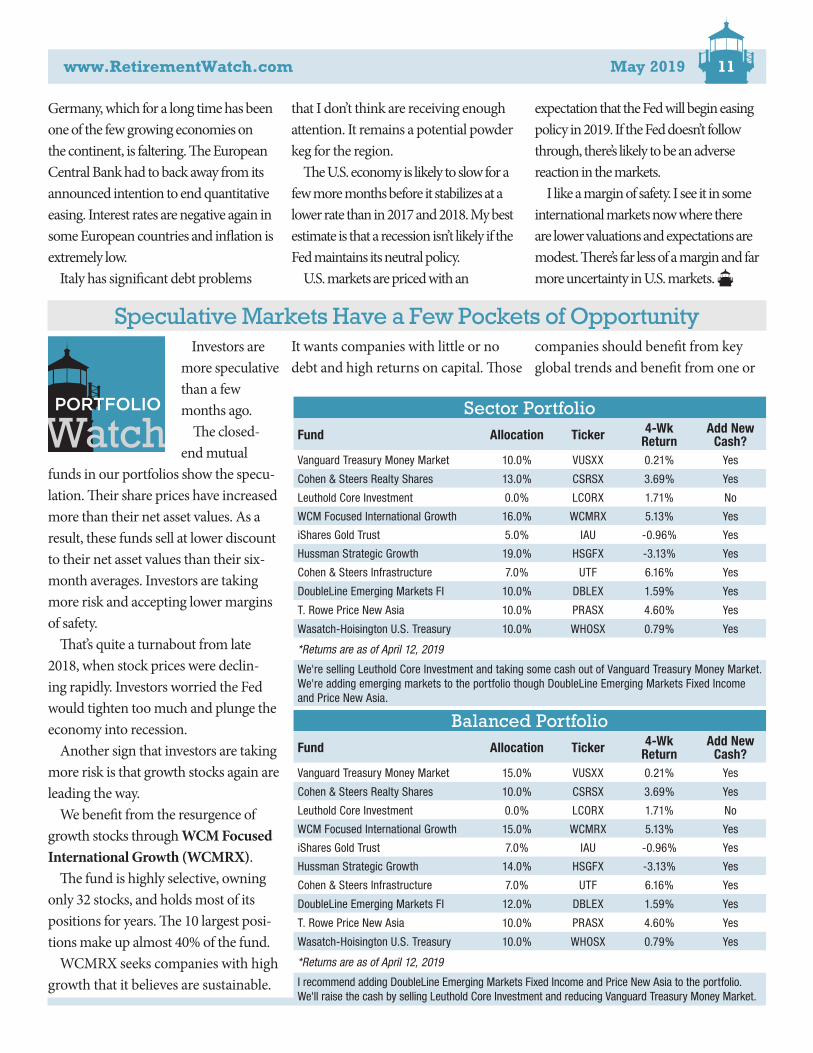

PORTFOLIO Sector Portfolio Fund Allocation Ticker 4-Wk

ReturnAdd New

Cash?Vanguard Treasury Money Market 10.0% VUSXX 0.21% Yes

Cohen & Steers Realty Shares 13.0% CSRSX 3.69% Yes

Leuthold Core Investment 0.0% LCORX 1.71% No

WCM Focused International Growth 16.0% WCMRX 5.13% Yes

iShares Gold Trust 5.0% IAU -0.96% Yes

Hussman Strategic Growth 19.0% HSGFX -3.13% Yes

Cohen & Steers Infrastructure 7.0% UTF 6.16% Yes

DoubleLine Emerging Markets FI 10.0% DBLEX 1.59% Yes

T. Rowe Price New Asia 10.0% PRASX 4.60% Yes

Wasatch-Hoisington U.S. Treasury 10.0% WHOSX 0.79% Yes

*Returns are as of April 12, 2019

We're selling Leuthold Core Investment and taking some cash out of Vanguard Treasury Money Market. We're adding emerging markets to the portfolio though DoubleLine Emerging Markets Fixed Income and Price New Asia.

Balanced PortfolioFund Allocation Ticker 4-Wk

ReturnAdd New

Cash?Vanguard Treasury Money Market 15.0% VUSXX 0.21% Yes

Cohen & Steers Realty Shares 10.0% CSRSX 3.69% Yes

Leuthold Core Investment 0.0% LCORX 1.71% No

WCM Focused International Growth 15.0% WCMRX 5.13% Yes

iShares Gold Trust 7.0% IAU -0.96% Yes

Hussman Strategic Growth 14.0% HSGFX -3.13% Yes

Cohen & Steers Infrastructure 7.0% UTF 6.16% Yes

DoubleLine Emerging Markets FI 12.0% DBLEX 1.59% Yes

T. Rowe Price New Asia 10.0% PRASX 4.60% Yes

Wasatch-Hoisington U.S. Treasury 10.0% WHOSX 0.79% Yes

*Returns are as of April 12, 2019

I recommend adding DoubleLine Emerging Markets Fixed Income and Price New Asia to the portfolio. We'll raise the cash by selling Leuthold Core Investment and reducing Vanguard Treasury Money Market.

Investment Recommendations and PorfoliosMay 2019 12

more barriers to competition. Manage-ment at those companies should foster a growth culture.

The system works well. The fund re-turned 5.13% in the last four weeks and 15.89% for the year to date.

Top holdings recently were CSL, Ca-nadian Pacific Railway, Tencent Hold-ings, Accenture and Shopify. The largest sectors in the portfolio are technology, health care and consumer cyclical.

Real estate investment trusts (REITs) also are riding high in this year’s stock rally. I’ve said for a while this is an ideal environment for commercial real estate. The economy is growing fast enough to reduce vacancy rates and allow prop-erty owners to increase rents. But in most areas we don’t have the speculative overbuilding that’s common late in the economic cycle.

I like Cohen & Steers Realty Shares (CSRSX) because of its outstanding long-term record and consistent approach.

CSRSX first develops an economic outlook and then determines which real estate investment trust (REIT) sectors are likely to benefit from the outlook. Finally, it selects REITs focused on those sectors that have quality manage-ment and own quality properties.

The fund returned 3.69% in the last four weeks and 19.08% for the year to date.

It recently owned 45 stocks and had 46% of the fund in the 10 largest positions.

Also joining in the global rally is Cohen & Steers Infrastructure (UTF), a closed-end fund. The fund returned 6.16% in the last four weeks and 29.36% for the year to date. The distribution yield is 7.43%. A small

part of the distributions this year have been returns of capital.

The long-term average discount to net asset value on its shares is over 11%. In late 2018, the discount was 10.51%. The six-month average discount is 6.77%. But the most recent discount was just over 3%.

This trend is why I occasionally like to buy closed-end funds selling at higher than their average discounts. Often, the discounts decline. That provides us an extra source of gains.

But shrinking discounts equal de-clining margins of safety. If discounts continue to decline, I’ll likely recom-mend selling.

UTF buys any type of infrastructure company located anywhere in the world, including firms that operate utilities, pipelines, toll roads, airports, railroads, ports, data towers and more. Top holdings recently were NextEra En-ergy, Crown Castle, American Tower, Enbridge and FirstEnergy.

We’ve had some low-risk exposure to U.S. stocks through Leuthold Core Investment (LCORX).

This tactical asset allocation fund can change its allocations to stocks, bonds, cash and commodities. It also can sell short stocks or buy futures and options that hedge stock positions.

The fund gradually became less con-servative through 2019 as the market appreciated and the Fed changed pol-icies. It’s delivered solid gains with low risk, returning 1.71% in the last four weeks and 5.21% for the year to date.

As I mentioned in this month’s Market Watch, I recommend emerging market assets to the portfolios. Let’s make room for those positions by sell-ing LCORX and reducing our money market fund allocation.

Put a portion of the sale proceeds into DoubleLine Emerging Markets Fixed Income (DBLEX).

DBLEX doesn’t try to mimic an index. The fund’s analysts determine the outlook for each emerging market country and decide the countries where they do not want to have exposure. The fund doesn’t own a country or a securi-ty simply because it’s in an index.

DBLEX buys primarily bonds that

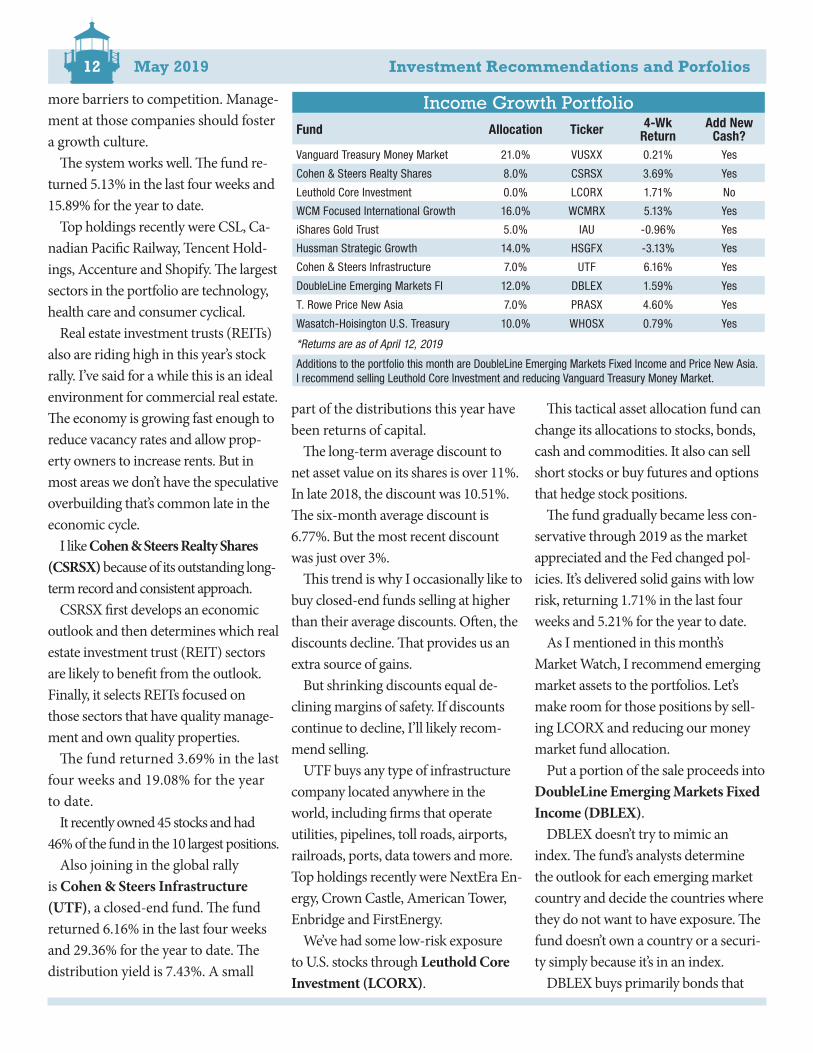

Income Growth Portfolio Fund Allocation Ticker 4-Wk

ReturnAdd New

Cash?Vanguard Treasury Money Market 21.0% VUSXX 0.21% Yes

Cohen & Steers Realty Shares 8.0% CSRSX 3.69% Yes

Leuthold Core Investment 0.0% LCORX 1.71% No

WCM Focused International Growth 16.0% WCMRX 5.13% Yes

iShares Gold Trust 5.0% IAU -0.96% Yes

Hussman Strategic Growth 14.0% HSGFX -3.13% Yes

Cohen & Steers Infrastructure 7.0% UTF 6.16% Yes

DoubleLine Emerging Markets FI 12.0% DBLEX 1.59% Yes

T. Rowe Price New Asia 7.0% PRASX 4.60% Yes

Wasatch-Hoisington U.S. Treasury 10.0% WHOSX 0.79% Yes

*Returns are as of April 12, 2019

Additions to the portfolio this month are DoubleLine Emerging Markets Fixed Income and Price New Asia. I recommend selling Leuthold Core Investment and reducing Vanguard Treasury Money Market.

www.RetirementWatch.com May 2019 13

are denominated in U.S. dollars. It largely avoids the currency risk so many emerging market bond funds take.

Finally, the fund emphasizes preserv-ing capital ahead of earning high yields.

The fund rose 1.59% in the last four weeks and 5.51% for the year to date. The yield is 5.31%.

The largest country exposures are Brazil, India, Mexico, Chile and Argen-tina. The largest industry exposures are banking, oil & gas, telecommunications, utilities and transportation. Almost 70% of the fund is in corporate bonds with the rest in quasi-sovereign bonds

and sovereign bonds.I also recommend exposure to Asian

emerging market stocks through T. Rowe Price New Asia (PRASX).

This is a long-time top-performing fund in the region that we’ve owned before.

The fund doesn’t try to follow an index. It focuses on the stocks and countries management likes. It recently owned 75 stocks and had 41% of the fund in the 10 largest positions.

PRASX follows T. Rowe Price’s process of buying stocks of well-managed growth companies selling at reasonable prices.

Top holdings recently were Tencent Holdings, Samsung Electronics, AIA Group, Alibaba Group and Taiwan Semiconductor Manufacturing. About 32% of the fund is in technology stocks and 22% in financial services.

The fund returned 4.60% in the last four weeks and 17.50% so far in 2019.

Last month, we added Wasatch Hoisington U.S. Treasury (WHOSX).

The fund owns U.S. Treasury securi-ties and can buy any duration of secu-rity. In recent years, its owned primar-ily very-long-term treasury bonds. It expects interest rates to remain low and even decline because the economy is weak and inflation is going to stay low.

The fund doesn’t try to trade short-term market moves or respond to every utterance by Fed officials. It focuses on economic trends and established mon-etary policy. Last year, the fund insisted that the Fed couldn’t maintain its policy of higher interest rates and its manage-ment team turned out to be correct.

The fund gained 0.79% in the last month and 1.93% for the year to date.

True Diversification PortfolioFund Ticker Alloc. 3 mos. 1-Yr. 3-Yr. 5-Yr. 10-Yr.Total Portfolio 100% 8.07 3.09 6.33 3.57 7.08

Plus or minus S&P 500 -5.58 -6.46 -7.30 -7.40 -8.99

Price Capital Appreciation PRWCX 11% 12.63 12.12 11.39 10.24 14.07

Price HY PRHYX 11% 6.97 4.41 7.48 4.00 10.19

FPA Crescent FPACX 18% 11.10 3.59 7.91 5.16 10.18

Berwyn Income BERIX 13% 3.95 2.94 4.15 2.69 7.85

Cohen & Steers Realty Sh CSRSX 5% 17.66 20.27 7.18 9.77 18.39

Oakmark** OAKMX 5% 13.73 -0.66 12.63 8.29 16.24

William Blair Macro Alloc*** WMCNX 12% 1.05 -0.85 2.34 0.29 n/a

Leuthold Core Investment**** LCORX 12% 4.66 -3.12 5.22 4.36 7.90

iShares Select Commodity COMT 8% 8.46 -0.55 10.52 n/a n/a

WCM Focused International Growth WCMRX 5% 13.71 2.51 11.12 7.54 n/a

Returns longer than one year are annualized. *Added to the portfolio in February 2012 issue. **Added in the December 2014 issue. ***Added in the September 2015 issue. ****Replaced MainStay Marketfield in the June 2016 issue. In the June 2018 issue we eliminated PAUDX and PRRDX. The PRRDX proceeds were put in COMT as were some of the proceeds from PAUDX. The remaining proceeds from PAUDX were put in LCORX, and WCMRX. Portfolio returns are as of March 31, 2019. Fund returns are as of March 31, 2019. N/A=Not Applicable.

Retirement Paycheck Portfolio

Fund Ticker Allocation12-mo. Yield

Add New Cash?

Vanguard Treasury Money Market VUSXX 40.0% 2.35% Yes

Verizon VZ 5.0% 4.10% Yes

Reaves Utility Income UTG 10.0% 5.97% Yes

DoubleLine Emerging Markets FI DBLEX 15.0% 5.31% Yes

C&S Infrastructure UTF 7.0% 7.43% Yes

C& S Ltd Duration Preferred & Inc LDP 10.0% 7.76% Yes

Cohen & Steers REIT & Preferred Inc RNP 13.0% 7.22% Yes

*Returns are as of April 12, 2019

I recommend moving some cash from Vanguard Treasury Money Market to Cohen & Steers Limited Duration Preferred & Income. There are no other changes to make this month.

Investment Recommendations and PorfoliosMay 2019 14

The yield is 2.19%.To remain balanced and diversi-

fied, we’ve owned Hussman Strategic Growth (HSGFX) since last fall. The fund has about 130 growth stocks that are selling at reasonable valuations and have good momentum and other tech-nical factors.

Manager John Hussman can use futures and options either to leverage the stocks when the market outlook is positive or hedge the stocks against a potential market decline. These strate-gies have a mixed record over the years, but Hussman overhauled his system to focus on what he calls market action.

The fund was fully hedged in last year’s market decline and had positive returns.

Near the market bottom in late 2018, Hussman wrote that investors shouldn’t be surprised to see a sharp rebound in equities in general. As the Fed changed its policy and the market recovered, Hus-sman switched to what he calls a neutral position. He said the market action

indicators that he follows don’t call for an aggressive or bullish outlook.

HSGFX is down 3.13% in the last four weeks and 8.31% for the year to date.

I’ve recommended owning a modest gold position as a hedge against either inflation or geopolitical problems through

One-Stop Recommended PortfoliosAlternative Funds

RW Recommended Fund NTF Funds* ETFs Fidelity Price VanguardVanguard Federal Money Market

Any MMF Any MMF Any MMF Any MMF Any MMF

Cohen & Steers Realty Shares

Cohen & Steers Realty Shares

iShares C&S REIT Real Estate Inv Real Estate REIT Index

WCM Focused Int'l GrowthWCM Focused International Growth

iShares MSCI ACWI Global Equity Europe Europe

Hussman Strategic Growth N/A N/A N/A N/A N/A

iShares Gold Trust N/A iShares Gold Trust N/A N/A N/A

VerizonRydex Telecomm Investors

iShares Telecomm (IYZ)Select Telecomm

Media & Telecom

N/A

Cohen & Steers Infrastructure

N/A N/A N/A N/A N/A

Wasatch-Hoisington U.S. Treasury

Wasatch-Hoisington U.S. Treasury

iShares 20+ TreasuryL-T Treasury Index

U.S. Treasury L-T

Long-Term Treasuruy

C&S REIT & Preferred Income

N/A N/A N/A N/A N/A

Reaves Utility Income N/A N/A N/A N/A N/A

T. Rowe Price New Asia Matthews Asia Growth iShares Asia 50 Pacific Basin New Asia Pacific

DoubleLine Emerging Mkts FIDoubleLine Emerging Mkts FI

iShares EM Corp BondNew Markets Inc

E Mkts Corp Bond

Em Markets Bond

*Not all NTF funds listed are available from all the NTF programs. Some are more restrictive than others, and some funds do not want to be available on all the NTF programs.

Simplify your investment life and probably improve returns for concentrating your investments at one or two mutual fund firms or brokers. It will be easier to track and manage your portfolio. The One-Stop Portfolios let you follow our margin-of-safety investment approach at the major fund companies and No Transaction Fee (NTF) broker programs. There is not always a good alternative to one of my recommended funds. Those cases are indicated by "N/A" in the table. In those cases, consider paying a fee to invest in my recommended fund or opening an account directly in that fund.

Portfolio PerformanceSector Balanced Income

GrowthRetirement Paycheck IWW ETFs

One Month 1.42% 1.29% 1.40% 2.09% 0.20%Year to Date 6.02% 5.59% 5.71% 7.03% 0.58%Last 12 Months -2.38% -1.37% 1.23% 5.64% -4.97%3 Years* 7.30% 7.05% 4.71% 5.83% -1.17%5 Years* 4.37% 3.81% 3.05% 5.84% -6.08%10 Years* 4.98% 4.57% 4.19% N/A 1.52%Compound Return 385.41% 346.58% 67.00% 77.16% 65.79%

*Annualized. Returns are as of March 31, 2019. The Income Growth Portfolio was begun in July 2001. The Retirement Paycheck Portfolio began Dec. 2010. The IWW-ETF Portfolio began December 2005. Other portfolios began Jan. 1995.

www.RetirementWatch.com May 2019 15

iShares Gold Trust (IAU). The ex-change-traded fund is a low-cost, conve-nient way to establish exposure to gold.

The fund is down 0.96% in the last four weeks and up 0.49% for 2019.

We have a portion of the portfolios in a money market fund. We were diversi-fying the portfolios with various bond funds but replaced those as interest rates began rising.

I recommend Vanguard Treasury Money Market (VUSXX), or its Ad-miral shares if you meet the minimum balance requirement. Vanguard has the lowest-cost money market funds, and treasury-only funds are the safest. You might find it more convenient to use a money market fund sponsored by your broker or mutual fund firm. If you want a higher yield, consider a fund that invests in more than treasury securities. The yield is 2.35%. It’s added 0.21% in the last four weeks and 0.67% for the year to date.

RETIREMENT PAYCHECKThe Retirement Paycheck portfolio

continues to generate above-average yields and capital gains.

Investors can’t earn decent income through the traditional retirement income investments such as CDs and treasury bonds. So, in this portfolio we add other investments that have higher yields plus the potential for appreciation.

We invest in preferred stock, master limited partnerships, high-yield bonds, closed-end funds and others. But we don’t buy and hold. Most of these investments are as volatile as stocks. We try to buy when their prices are low and sell when prices are high.

We already discussed Cohen & Steers Infrastructure, DoubleLine Emerging Markets Fixed Income and Vanguard Treasury Money Market.

Utility stocks are investor favorites in 2019, and Reaves Utility (UTG) is benefitting. It gained 4.65% in the last four weeks and 17.31% for the year to date. Its yield is 5.97%. It doesn’t make return-of-capital distributions. The fund uses about 20% leverage.

The latest discount is 1.64%, com-pared to a 2.76% six-month average dis-count. But this fund frequently trades at a premium.

I expect utility stocks to do well for a while. Interest rates will be stable or declining, and the economy is grow-ing modestly.

We also own REITs in this portfo-lio, but through the closed-end fund Cohen & Steers REIT & Preferred Income (RNP).

The fund is about evenly split between REITs and preferred securities. It has re-turned 2.82% for the last four weeks and 17.96% for the year to date. The yield is 7.22%. It hasn’t made any return-of-cap-ital distributions this year but has in the past three years. The fund uses about 24% leverage. RNP currently sells at an 10.51% discount compared to an average discount of 11.47% over six months.

Verizon (VZ) continues to generate solid returns and a high yield. It rose 3.33% for the last four weeks and 6.63% for the year to date. The yield is 4.10%.

This is a good time to return pre-ferred stocks to the portfolio. These hy-brids of stocks and bonds offer higher yields than investment-grade bonds or treasury bonds. With the Fed’s interest

rate increases on hold indefinitely, they have a solid margin of safety.

There are several ways to invest in pre-ferreds. I’m recommending the closed-end fund Cohen & Steers Limited Duration Preferred & Income (LDP), which we’ve owned in the past.

The fund’s managers focus on preser-vation of principal with high yield as a secondary consideration. The fund uses about 30% leverage.

LDP has a return of 2.23% over the last four weeks and 12.83% for the year to date. The yield is 7.76%. The current discount to net asset value is 3.71%, com-pared to a 6.19% average discount over six months. But over three years it has traded on average at a premium of 0.19%.

TRUE DIVERSIFICATIONOur True Diversification portfolio

delivers solid consistent returns, while taking less risk than traditional bal-anced portfolios and the S&P 500.

Every three months, we take a detailed look at this portfolio’s performance. This month we look at some highlights.

The funds with the highest correla-tions to the stock indexes are leading the portfolio since the market bottom last December. But all the funds have posi-tive returns for the latest three months.

Over longer periods, the returns are more diversified.

The highest returns over most periods are from CSRSX. This shows the impor-tance of true diversification. REITs have a low correlation with the stock indexes and have delivered higher returns over the long term. Most portfolios that are supposed to be balanced or diversified have little or no exposure to REITs.

Actions to Create the Retirement You DesireMay 2019 16

Robert C. Carlson wrote the book on retirement and retirement planning—twice: The New Rules of Retirement (Wiley, 2nd ed. 2016) and Personal Finance after 50 for Dummies (with Eric Tyson; 2nd ed. 2015). He also serves as Chairman of the Board of Trustees of the Fairfax County (Va.) Employees’ Retirement System (a more than $3.0 billion portfolio) and served on the Board of Trustees of the Virginia Retirement System (a $42 billion portfolio in 2005) from 2000-2005. He was educated at the University of Virginia School of Law and McIntire School of Commerce (M.S.) and Clemson University.

Challenges Investors Face: The TJT Solution to Portfolio Management Many investors need help with their portfolios. We saw that with the strong registration and turnout for the webinar featuring Bob Carlson and TJT Capital, “Challenges Investors Face: How TJT Capital Manages Portfolios to Participate in Bull Markets and Protect Capital in Bear Markets.” The webinar is available for replay at www.tjtcapital.com. If you like Bob Carlson’s margin of safety approach and methods of selecting mutual funds, log in or contact TJT Capital at 877-282-4609 or [email protected].

INVEST WITH THE WINNERSIt finally is time to move the portfolio

out of cash after four months.In this strategy, I use several models

to determine which exchange-traded fund (ETF) has strong recent perfor-mance that is likely to continue. After the decline of 2018 the models had trouble identifying such an ETF.

The models ultimately identified the Invesco QQQ (QQQ) as the ETF to buy. We’ll move this portfolio from cash into QQQ and hold it for at least the next month.

How to Become #1This is turning

out to be a championship year in the Carlson home. Both of my alma

maters, Clemson and Virginia, won major NCAA championships in 2019.

I don’t point this out to brag or to make you feel bad if you were pulling for other schools. Instead, there’s a lesson here.

Neither school was expected to end on top. They were highly ranked from the start of their respective seasons, but other teams were heavily favored to win the championships. In fact, according to many commentators, in each sport another team was con-sidered good enough to be under consideration as best of all time. But Clemson and Virginia went about their business, stuck to their processes and plans, and ended on top.

Often people compare their financial

situations with other people, or what they imagine other people’s situations are. Or when making decisions they rely heavily on the choices other people are making. Of course, what the media are saying influences far too many people.

With your finances, what other people are doing or saying isn’t neces-sarily what’s best for you.

Spend less time paying attention to what others do and say and more time developing a process for making the key financial decisions. Then, follow your process. At times, it might not seem to be working as well as you’d like. Others might seem to be doing better. That’s normal with finances, especially investing. But if you devel-oped a good process and followed it to develop your plans, there’s a high probability that things will work out well for you and there will be more highs than lows.

That’s all we have time for this

month. Next month, I’ll report again on my research and recommendations to help you maintain financial inde-pendence and security in retirement.

.

P.S. In between issues, you should listen to the conversations that make up my Retirement Watch Spotlight Series. This series of online seminars allows me to present one or two key retire-ment issues in more detail each month than is possible in the newsletter. You can view the seminars whenever you want from wherever you can access the internet. It’s a powerful learning tool that’s attracting more and more view-ers. To learn more about the Spotlight Series, go to the top of the Retirement-Watch.com home page, and select the Spotlight link.

“America’s #1Retirement Expert”

–StockInvestor.com, DividendInvestor.com

Bob Carlson is trained as a CPAand attorney. He currentlyoversees a $3.8 billion retirementfund as Chairman of Virginia’sFairfax County Employees’Retirement System.

His weekly column in Forbescovers estate planning, Medicare,long-term care, income taxes, IRAstrategies, annuities, investments,and more… and has been selectedas a Forbes Editor’s Pick.

Bob’s written America’s leadingretirement publication since 1991:RetirementWatch.com. It’s thefirst and only source to cover allthe financial aspects ofretirement, including exposingscams, schemes, and fraudstargeting retirees.

Additionally, Bob has authoredthree international bestsellers:

How to Create a “SecondSocial Security Check”…And potentially generate as much income as you need…

for as long as you need it.

Dear Friend,

If you are retired, or approachingretirement age, and want a guaranteedincome for life…

This will be one of the most importantthings you will read this year.

I’m going to show you a little understood,yet lucrative, retirement strategy.

It’s quietly (and 100% legally) beingexploited by thousands of savvy retireeseach year.

And most importantly, it pays you anincome for life.

I call this a “Second Social Security,”because it can pay you a check each andevery month for the rest of your OR yourspouse’s life.

And you get this Second Social Securitycheck in addition to your regular SocialSecurity check.

Supplement to the Retirement Watch newsletter

The New Rules of Retirement…Invest Like a Fox, Not aHedgehog… and Personal FinanceAfter 50 – for Dummies.

In other words, getting this second checkdoesn’t take away one cent from yourregular one.

Plus, depending on your situation, it can pay you between a few hundreddollars… up to tthhoouussaannddss ooff ddoollllaarrss ppeerr mmoonntthh.. (Contact your accountantfor exact figures.)

More importantly, your new Second Social Security check is as bulletproofas your regular one. You collect even if…

The stock market crashes

The economy nosedives

Interest rates go to zero… or through the roof

In other words, the cash flows in like clockwork. Every month, you’ll openthe mail and smile when you see your extra Social Security check.

Of course, the sooner you act, the sooner you’ll get the cash flowing. In fact,you can collect your first check in as little as four weeks.

And what’s more, this “Second Social Security check” is an excellentalternative to IRAs and 401(k)s. Why?

Because with an IRA or 401(k), when the markets drop… you losethousands… maybe tens of thousands from your precious retirement funds.

And (worse!) the experts tell you to “spend down” 4% of your IRA or 401(k)each year. Sure, you need this for income… yet each withdrawal is one stepcloser to outliving your money.

But if you instead switch to a Second Social Security check, you get a steady,dependable, and predictable monthly income ffoorr lliiffee… regardless of whatWall Street or Washington throws at you…

Which means you can end any worries about outliving your money.

So, let me show you…

Three Reasons You Need ThisSecond Social Security Check

We all want enough money to carry us safely through retirement. A lifetimeincome can provide you with that security.

And this is the most powerful source for lifetime income I’ve ever seen.

Here are three reasons why you need to consider this Second SocialSecurity check:

Starting in 2022, the U.S. Social Security will beunderwater, paying out more than it brings in

Twelve years later, it will run out of moneycompletely

But this Second Social Security fund is awash withcash – almost always bringing in more money thatit pays out – because it’s managed by some ofAmerica’s most brilliant financial minds

So, as you think about how important a “Second Social Security check” is foryour future, let me anticipate a question:

Why Haven’t I Heard About thisLucrative Strategy Before?

Frankly, most who have heard of it don’t understand it. So, they don’t give ita second thought.

But it’s not going to stop me from exposing the tremendous benefits of thislittle-understood strategy for you today.

After all, those in the know already use it to secure a rock-solid financialfuture in the face of an uncertain one.

In fact, many prominent people benefit – and have benefited – from thisSecond Social Security check…

Even if they don’t talk about it publicly:

Babe Ruth, who had to retire because of healthreasons… the same year Social Security wasenacted. His manager made sure he had a “SecondSocial Security check.” It helped him when hishealth failed.

Ben Bernanke, former Fed chair, gets two of theseSecond Social Security checks.

Elaine Larsen, the famed 285-mph drag-racingchamp, has a Second Social Security check. Shesaid it has “…allowed me to look at the next stage ofmy life with a new attitude. It’s allowed me to relax.I’m not looking at the downside of things. I’mlooking at what I can do next.”

But it’s not just for the rich and famous. All kinds of people have created aSecond Social Security check for themselves: Businessmen, housewives,teachers, doctors, factory workers…

So why not you? I’ve created a no-nonsense resource that shows you how todo just that. It’s called…

How to Generate GuaranteedLifetime Income

This special presentation is all meat. No frills. No sales pitch.

You get hard-hitting information that could give you a life-long secure

retirement.

Here’s why you need this:

Lifetime income security is what everyone wants in retirement. But it’sincreasingly hard to achieve. Major obstacles stand in your way:

Low interest rates – making the safest investmentsthe least lucrative

Stock market volatility – threatening the value ofyour retirement account with each violent swing ofthe Dow

Longer life spans – and 401(k) or IRA moneyrunning out, before you run out of life

That’s why you need a steady cash flow that’s guaranteed for life. And youcan get that with what I call, “Your Second Social Security Check.”

I show you exactly how to get that started right away in mylatest RReettiirreemmeenntt WWaattcchh SSppoottlliigghhtt SSeerriieess.

This retirement income source is poorly understood by Main Streetinvestors… But it’s recommended by most economists. It’s transparent,simple, low cost, and guaranteed. It is not some newfangled, complicatedproduct developed by the whiz kids on Wall Street who use algorithms andextreme computing power.

In fact, experts say this strategy makes your entire portfolio last longer,making it easier for you to achieve your retirement goals.

But there are numerous traps in the road to a guaranteed lifetime income. Iwill make sense of all of these, revealing them in a straightforward mannerand showing you how to deal with them.

In just a few minutes, you’ll know how to maximize your “Second SocialSecurity paycheck” and enjoy a guaranteed lifetime income.

And all you have to do to get this retirement-saving presentation is…

Take a 30-Day Preview of theTop Retirement Resource Today:

“Retirement Watch Spotlight”

The rules of retirement change quickly… and without notice.

That’s why, every month, I spotlight the latest changes – along with thebiggest retirement issues of the day – and break them down into a plain-English, easy-to-understand video presentation.

And, at the end of each presentation, you get helpful action steps for eachcrucial point.

TThhiinnkk ooff iitt aass tthhee ““6600 MMiinnuutteess”” ffoorr rreettiirreeeess..

I can’t imagine anyone retiring today without this kind of protection fortheir income.

Topics I’m covering include how you can:

Avoid costly traps in your IRAs and 401(k) beforethey cost you HUGE money

Minimize your taxes – your tax rates with little-known, yet valid exemptions, deductions, creditsand strategies… including the new Tax Cut bill

Protect and build your retirement portfolio withconservative investments that pay generousreturns

Maximize what’s yours, and give less to the IRS

Get the best long-term medical care (LTC) optionsavailable today

Each month you’ll get usable information that will save you from comingretirement catastrophes, as well as fatten your nest egg.

It’s like having a top financial retirement advisor, 24/7, who keeps up on allthe breaking news and changes in retirement rules and regulations… yetgives it to you in a simple and straight-forward presentation.

Like Warren W., from San Jose who happily wrote me, ““……TThhaannkkss ffoorr tthheecclleeaarr aanndd ccoonncciissee eessttaattee aanndd rreettiirreemmeenntt iinnffoorrmmaattiioonn.. AAggaaiinn,, mmyy hheeiirrssaanndd II hhaavvee ggrreeaattllyy bbeenneefifitteedd ffrroomm yyoouurr vvaasstt wweellll ooff kknnoowwlleeddggee..””

He also said, ““[[YYoouurr]] ssuuggggeessttiioonn ssttrruucckk aa cchhoorrdd…… aanndd tthhaatt rreepprreesseennttss aappootteennttiiaall $$110000,,000000 iinn aavvooiiddeedd eessttaattee ttaaxxeess..””

But you may be wondering… how much is this going to cost?

I have good news. Recent price cuts have made your subscription feesalmost trivial…

In the past, I’ve asked $47 each for these high-impact video presentations. Iwouldn’t dream of asking you for that much, because a full year would havecost $564.

Yet, even at that price, many retirees thank me, grateful for how thesepresentations paid for themselves many times over… saving them fromcostly mistakes, and giving them a safer retirement than they could haveimagined.

BBuutt,, ffoorr tthhee nneexxtt 2244 hhoouurrss,, yyoouu ggeett aa ffuullll yyeeaarr ooff hhiigghh--vvaalluueepprreesseennttaattiioonnss ffoorr jjuusstt $$113399 —— wwhhiicchh iiss aa $$442255 ssaavviinnggss……

And you get immediate, 24/7 access to each presentation – and ALL myarchives – on our secure site, RetirementWatch.com.

Just $139? Yes, you heard that right.

That’s a trivial 39 cents a day. (They want to charge me that for a paper bagat the discount grocery store.)

For 39 cents a day, you can get retirement advice that can save your nest

egg… and make it grow into the lifestyle of your dreams.

And there are no worries. You are fully protected by a 100%satisfaction guarantee for a full 30 days. You MUST becompletely satisfied in every way with your RReettiirreemmeennttSSppoottlliigghhtt presentations during the first 30 days of yoursubscription…

Or I will INSIST you accept a complete and immediate refund. No questionsasked.

You risk nothing. In fact, I urge you to watch every presentation on my dimefor the next 30 days. THEN decide if you want to keep your subscription forthe full year. But for now, let’s start you on your 30-day mmoonneeyy--bbaacckkpprreevviieeww:

Now, upon signing up, I suggest you watch my January 2019 presentation,HHooww ttoo GGeenneerraattee GGuuaarraanntteeeedd LLiiffeettiimmee IInnccoommee. Please write that down.That is the presentation that shows you all you need to set up your SecondSocial Security check.

Then I strongly suggest you download my top report with your 24/7 accessto my growing RReettiirreemmeenntt PPrrootteeccttiioonn LLiibbrraarryy::