vol 6, no 10 (2018)

TRANSCRIPT

Vol 6, No 10 (2018)

Archives of Business Research

DOI: http://dx.doi.org/10.14738/abr.610.2018

Archives of Business Research

Volume 6, Issue 10 - October - 2018

Table of Contents

Articles

Users ’ attitude towards telecommunication

operators: a Study on Grameenphone and

Banglalink

S. M. Sohel Ahmed

Marketing Ethics in Creative Industry : an

Exploration Study

Sri Hartini

Composition of Ingredients in Syubhah Semi

Processed Food, Trust and Purchase Behavior - A

Conceptual Framework

Reezlin Rahman

An Analytical-Exploratory Approach to a Socially-

Optimal, Sustainable, and Balancing Social Security

System

Reza G. Hamzaee, Stephanie Michelle Dilley,

Mengmeng Wang

Supply Response of Potato to Price and Non-price

factors in Swaziland

Daniel Vusi Dlamini

A Survey of Benefit Approaches and Innovation

Loop Required for IT Governance

Amit Ghildyal, Elizabeth Chang, Keith Joiner

ANALYSIS OF INTENTION TO USE

ELECTRONIC MONEY IN DENPASAR CITY:

TAM APPROACH

I Komang Sumerta, I Made Wardana

Customer Centricity: The Road to Financial

Inclusion The Case of the Commercial International

Bank (CIB) in Egypt

Hanan Elmoursy, Nazly Hussein, Sherif Ahmed

The Effect of Community Empowerment Program

for Fisherman Community to Enhance the Market

Penetration a Case Studies in Tuban Indonesia

Muslichah Erma W., Nova Retnowati, Soeharjoepri

Soeharjoepri

The impact of health information systems on the

performance of human resources (HR) in King

Faisal Specialist Hospital in Taif

Adnan Awad Shawabkeh

Correcting the Incorrect: an Exploratory Study into

the Role of the Controller in Counteracting

Financial Fake News

W. Veldman, D. M. Swagerman

Assessing Multiple-Item Manufacturing Capability

Measures: A Critical Review

Rhonda L. Hensley, Joanne S. Utley

Empirical Studies Use The Balanced Scorecard To

Measure Government Performance

Muchriana Muchran

Perceptions of destination image and effects on

college football fans: A case study of conference

realignment

Cheryl Rode, Angela Sebby, Kenneth Jordan

The Impact of Cultural Similarity on Consumer

Ethnocentrism Tendencies Toward Foreign Products

eman alshammari, MICHAEL WILLIAMS

Supply Chain Management and Organization

Performance: A Value Creation Perspective

Evans Kyeremeh, Mawuko Dza

Capital Mobility in the World: TPP Experience

Yutaka Kurihara

How Strategic International Human Resource (IHR)

Strategies can manage Organizational Performance

Challenges

Rossano V. Gerald

THE EFFECT OF COMPETENCE,

COMPENSATION OF ORGANIZATIONAL

CITIZENSHIP BEHAVIOR AND

PERFORMANCE OF EMPLOYEES IN LIFE

INSURANCE COMPANIES IN BATAM CITY

Suhardi Suhardi

Learning Pyramid Models To Improve Early

Childhood Science Skills

Masitowati Gatot

Comparative Impact Of Corporate Social

Responsibility On Marketing Performance: A Study

Of ABC PLC And ALEX Industries PLC, Imo State

Nigeria.

Anthony Nduka Nwachukwu, Agu Godswill Agu

Performance

Appraisal and

Employee

Commitment in

Abia State Civil

Service: A

Focus on

Ministries of

Education and

Works

Onyemaechi

Uchenna, Agu

Godswill Agu,

Emmanuel

Uche Uche

UNTITLED PDF

The Effect of Asset Growth With Profitability and

Company’s Value (Case Study: Coal Company was

Listed in Bursa Efek Indonesia during 2014-2016

Period)

Mulyanto Nugroho Nugroho

An Application of Timmons Model in the Mini

Entrepreneurial Logistics Project

Wee Yu Ghee

EFFECT OF COMPENSATION,

COMMUNICATION AND SPIRITUALITY AT

WORK ON THE PERFORMANCE OF THE

TURNOVER INTENTION AS AN

INTERVENING VARIABLE

Sumiati Sumiati Sumiati

THE INFLUENCES OF HIGH PERFORMANCE

WORK SYSTEM ON TRUST IN

MANAGEMENT, AND PERSONAL SAFETY

ORIENTATION OF SURABAYA FIRE

FIGHTERS

Zainal arief

New Product Introduction Prize (NPIP) and the

Market Value of the Firm: An Empirical

Investigation into the Computer, Electronic and

Communication Industry (CECI)

Isaac Quaye, Yinping Mu, Braimah Abudu, Alfred

Sarbah

___________________________________________________________________

Archives of Business Research; ISSN 2054-7404

Copyright Society for Science and Education, United Kingdom

ArchivesofBusinessResearch–Vol.6,No.10PublicationDate:Oct.25,2018DOI:10.14738/abr.610.5356.

Sumerta, I. K.,&Wardana, I.M. (2018).AnalysisOf IntentionToUseElectronicMoney InDenpasarCity: TAMApproach.ArchivesofBusinessResearch,6(10),86-103.

AnalysisOfIntentionToUseElectronicMoneyInDenpasarCity:TAMApproach

I.KomangSumerta

EconomicsandBusinessFaculty,UdayanaUniversity,Bali-Indonesia

I.MadeWardana

EconomicsandBusinessFaculty,

UdayanaUniversity,Bali-Indonesia

ABSTRACTThe rapid development of technology has penetrated various sectors of life in thecommunity,oneofwhichisinthebankingsector.Electronicmoneyhasadvantagesanddisadvantages that can affect the behavior of consumers to use it.This study aims toexplaintheusefulnessandperceivedconsumers'useofelectronicmoneyproducts.Thepopulationofthisresearchis infinite.Thesamplingmethodusedinthisstudyisnon-probability sampling.The sampling technique in this study was purposivesampling.Thesampleusedwas108respondents.TheanalyticaltoolusedisWarpPLS3.0Theresultsof thisstudyareperceivedusefulnessandperceivedeaseofusehasapositiveandsignificanteffectonusingelectronicmoney.Perceivedusefulnesshaveapositiveandsignificanteffectontheintentiontouseelectronicmoney.Theattitudeofusing electronic money has a positive and significant effect on the intention to useelectronicmoney.Perceived ease of use have a positive and significant effect on theperceived the usefulness of electronicmoney.The practical implication of electronicmoney issuing companies can improve and improve in terms of the community'sintention to use electronic money as a medium for future micropaymenttransactions.Factors that influence the intention to use in this study are perceivedusefulness,perceivedeaseandattitude.Theoreticalimplicationsinthisstudytoenrichthe concept of consumer behavior in marketing, especially the results of previousresearchontheintentionofusingelectronicmoney.Keywords:TAM,IntentionofUse,ElectronicMoney

INTRODUCTION

The rapid development of technology has penetratedmany sectors of life in society, one of

which is inankkanPERBsector.Advances in technology in the sector has been very rapidbanking case, from the advent of automated teller machines (ATMs),mobilebanking,to

internetbanking.The technological progress did not stop there, in 2009 the Indonesian

government together with Bank Indonesia issued a new banking product basedontechnologynamely electronic money.Technological advancements have an impact on all

industries, including the banking industry which currently can facilitate customer bankingactivitiesto bemore efficient and also friendly to its users(Akincietal.2004).In general,

technologicaldevelopments in the fieldof financial transactionsshapeconsumerbehavior to

tend to use more effective and efficient transaction tools, one of which is to use non-cashtransactions.Non-cashtransactionsthatarecurrentlydevelopingareusingelectronicmoney.

ArchivesofBusinessResearch(ABR) Vol.6,Issue10,Oct-2018

Copyright©SocietyforScienceandEducation,UnitedKingdom 87

Table1.CashTransactionVolumeandElectronicMoney

No. Year Cash(BillionsofRp.)

E-money(BillionsofRp.)

Total(BillionsofRp.) E-Money(%)

1 2010 54.158.062 693 54.158.755 0.001

2 2011 66.921.296 981 66.922.277 0,001

3 2012 99.396.764 1.971 99.398.735 0,002

4 2013 90.959.927 2.907 90.962.834 0,003

5 2014 111.795.756 3.319 111.799.075 0,003

6 2015 112.845.451 5.283 112.850.734 0,005

7 2016 111.827.354 7.063 111.834.417 0,006

8 2017* 96.847.623 1.264 96.848.887 0,001

*)UntilOctober2017

Source:BankIndonesia,2017.

Electronicsmoney isthe latestinstrumentinapaymentsystem,electronicmoneydefinedby

Soefianto(2012)asameansofpaymenthasthefollowingelements;issuedonthebasisofthevalue ofmoneydeposited in advance, the value ofmoney stored electronically in amedium

such as a server or chip, usedas a means of payment to traders who are not issuers ofelectronic money, as well as the value of electronic money deposited by the holder and

managedbytheissuerratherthanisadepositasreferredtointhelawgoverningbanking.The

increasingly widespread issuance of electronic money issued by banking and non-bankinginstitutions such as;Bank Mandiri withe-tollproduct, BCA with theFlazz

Cardproduct,PT.Telekomunikasi Indonesia withFlexiCashproducts, and Telkomsel withT-

cashproductswhichraisescompetitionsotightlyintheelectronicmoneybusiness.

Thedevelopmentof electronicmoney in Indonesia is very rapid since itwas issued in2009ago.According to data from Bank Indonesia (2017) until October 2017 the number of

electronic money circulating in the community reached 75,846,689 units, a very significant

increase from the 2010 data which only amounted to 7,914,018 units.In sum, electronicmoneyhasindeedincreased,butthisincreasehascontinuedtodeclinesince2013.In2017the

useofelectronicmoney isstill categorizedas lowbecause it is stillbelow1percentwhich isstillfarfromtheexpectationsofBankIndonesiawhichtargetstheuseofelectronicscanreach

1percentoftotaltransactions(Bisnis.com,2014).

Electronicmoneyhasadvantagesanddisadvantagesthatcanaffectthebehaviorofconsumers

to use it.Consumer behavior is the behavior shown by consumers in finding, buying, using,

evaluating and disposing of products and services that are expectedtomeet various needs(Schiffman and Kanuk, 2010).In this case, individualswho are consumers have the right to

accept or reject a product, is one form of consumer behavior (Howard and Sheth, 1979)explainsthatthetheoryofconsumerbehaviorcanbeseenfromtheprocess,namelytheinput

intheformofmarketingstimuliandtheenvironmentthatwillproduceoutputintheformof

attitude(attitudetowardbehavior), intention(attention), andpurchasebehavior (purchasebehavior).This basis is used(Davis, 1985)in developing a technology adoption intention

model, namelyTechnology Acceptance Model(TAM) is influenced by two indicators,

namelyperceived usefulnessandperceived ease of usethat can affect the use of behavior.information Technology.This attitude will affect the intention, and then the intention will

influencetheuseofinformationtechnology.

Consideringelectronicmoneyisanewproductintheworldoffinancialtransactionsandbased

on the use of high technology, theTechnology Acceptent Model(TAM)theory isveryappropriatetoexplainhowtheintentionsofprospectiveelectronicmoneyconsumersareseen

fromtheirattitudesandperceivedusefulnessandperceivedeaseofuseoftheproduct..

Sumerta, I. K.,&Wardana, I.M. (2018). AnalysisOf IntentionToUseElectronicMoney InDenpasar City: TAMApproach.Archives of BusinessResearch,6(10),86-103.

URL:http://dx.doi.org/10.14738/abr.610.5356. 88

In the development of research carried out based on TAM, there are inappropriate results

between one study and another.In a study conducted byYadavet al.(2015)found thatperceivedeaseofusedidnothaveapositiveandsignificanteffectonconsumerattitudesinthe

useof internet banking, this indicates that consumers feel that it is not easy touse internet

bankingandthisresultiscontrarytotheconceptoftheTAMitselfwhichstatesthateaseofuseperceived influence positive attitude.Several other studies have found that perceived

usefulness have a significant and significant effect on the intention to use (HasioandTang,2013., Dakduketal.2017) but several other studies get different results, where in a study

conducted by Mutianah et al (2012), Yadavetal.(2014) and Weiet al.(2017) found the

opposite, namely the perceived usefulness did not have a significant effect onuse.Researchconducted by Weietal.(2017) states that all variables in TAM, both perceived usefulness,

perceived ease of use and attitude have no significant effect on intention.This is whatencouragesresearcherstoconductresearchwiththeresearchsubjectisTAMwithelectronic

moneyastheobjectofresearch.

Researchthatuseselectronicmoneyasanobjectofresearchisstillveryrarelydone,previous

research on electronic money was conducted in Jakarta (Rahmatsyah, 2011).Research on

electronicmoneywiththeTAMapproachinmajorcitiesinBalihasneverbeendone.Basedontheabovebackground,theresearchaimsto:

1) Toexplaintheeffectofperceivedusefulnessonattitudesusingelectronicmoney.2) Toexplaintheeffectofperceivedeaseofuseontheattitudeofusingelectronicmoney.3) Toexplaintheinfluenceofattitudestowardstheintentionofusingelectronicmoney?4) Toexplaintheeffectofperceivedusefulnessonelectronicuseintentions.5) To explain the effect of perceived ease of use on the perceived the usefulness of

electronicmoney.

LITERATUREREVIEWMarketingStrategyConceptThemarketing concept is a social andmanagerial process in which individuals and groups

obtainwhattheyneed(needs)anddesire(wants)throughthecreation,supplyandexchangeof

everything that has value(value)with another person or group (Kotler, 1999).To apply theconcept of marketing, organizations must understand and remain with their customers to

provideproductsandservicesthatconsumerswillbuyanduse(Hawkins2001).

InfluenceofMarketingStrategiesTo develop an effective marketing strategy, there are aspects that influence the marketingprocess as explained in theWheel of Consumer Analysistheory(PeterandOlson, 2008).This

theory explains three aspects that influence effectiveness in marketing strategies, namely

consumereffectandcognition,consumerbehavior,andconsumerenvironment.

InTeoretis,affectiveandcognitiveaspectsrefertoothertypesofreactionsorpsychologicalresponse to a stimulus from the events that occurred in the neighborhood.The aspect of

consumerbehaviorisanimportantfactorinmarketingstrategies.AccordingtoSchifmannand

Kanuk (2010), the definition of consumer behavior is the behavior shown by consumers infinding, buying, using, evaluating, and disposing of products and services that are

expectedtomeet various needs.The last aspect is the environment that refers towhatis afactorexternal to theconsumerwhich influences theconsumeronwhat theythink, feel,and

do.

ArchivesofBusinessResearch(ABR) Vol.6,Issue10,Oct-2018

Copyright©SocietyforScienceandEducation,UnitedKingdom 89

ConsumerKnowledgeofProducts(Consumer'sKnowledge)Consumershavedifferentknowledgeofaproduct.Thisknowledgeisusedasaninterpretation

of information in making purchasing decisions.The level of product knowledge can becategorizedby class, form, brand, andmodel or feature. PeterandOlson (1998), argues that

thetypesofconsumerknowledgeabouttheproductcanbecategorizedintothreecategories:

productsebgaicollectionofattributes,acollectionofbenefitsandvaluesatisfaction.

ConsumerEngagement(Consumer'sInvolvement)Consumer involvement is referring to consumers' perceived things that are related or

importantfromcertainproducts,eventsoractivities(PeterandOlson,2008).Thisinvolvement

occurswhenconsumersperceiveorconsideraproduct,serviceormarketingmessagetofulfilltheir goals and needs.Consumer involvement or participation influences the level of

information search,decisionmakingprocesses, the formationofbeliefs, attitudes, intentionsandbehaviors,forexamplelookingforproductvariations,tryingotherproductbrands,brand

loyalty,frequencyofproductuse(BeharrelandDennison,1995).

ConsumerPerception.Consumerperceptionisafeelingorimpressionthataconsumerhasonaproduct.Perception

can be formed from consumer experience, as well as from the impression instilled byproducers,amongothersthroughtheappliedmarketingcommunication.Consumerperception

canaffecttheoveralldecisionmakingprocessindeterminingthepurchaseoruseofaproduct.

TheoryofReasonedAction(TRA)This theory was developed by FishbeinandAjzen (1975) and compiled using basicassumptions that humans are creatures with reason to decidewhatbehaviorto take, in a

consciousmanner and consider all available information.ThisTRA explains that behavior is

carriedoutbecauseindividualshavetheintentionordesiretoapplyit.

TheoryofPlannedBehavior(TPB)This theory is a development of TRA.This TPB develops TRA by adding a construct that

isperceivedbehavioralcontrolwill affect intention and behavior(Ajzen, 1991).At TPB there

arethreemainfactorsasdeterminantsofintention,firstisanattitudethatreflectstheextentto which individuals have an assessment of agreeing or disagreeing to conduct

behavior.Second, social factorsarealsocalledsubjectivenorms, referring toperceivedsocialpressuretodoornotconductbehavior.Thelastisbehaviorcontrol,whichreferstoperceived

easeordifficultyinperformingbehavior.

TechnologyAcceptanceModel(TAM)TheoryThe Technology Acceptance Model(TAM) developed by Fred Davis (1989) describes the

acceptanceoftechnologythatwillbeusedbytechnologyusers.Thistheorywasadoptedfromseveral models that were built to analyze and understand the factors that influence the

acceptanceoftheuseofnewtechnologies, includingthoserecordedinvariousliteratureandreferences to research results in the field of information technology areTheoryofReasoned

Action(TRA)andTheoryofPlannedBehavior(TPB).

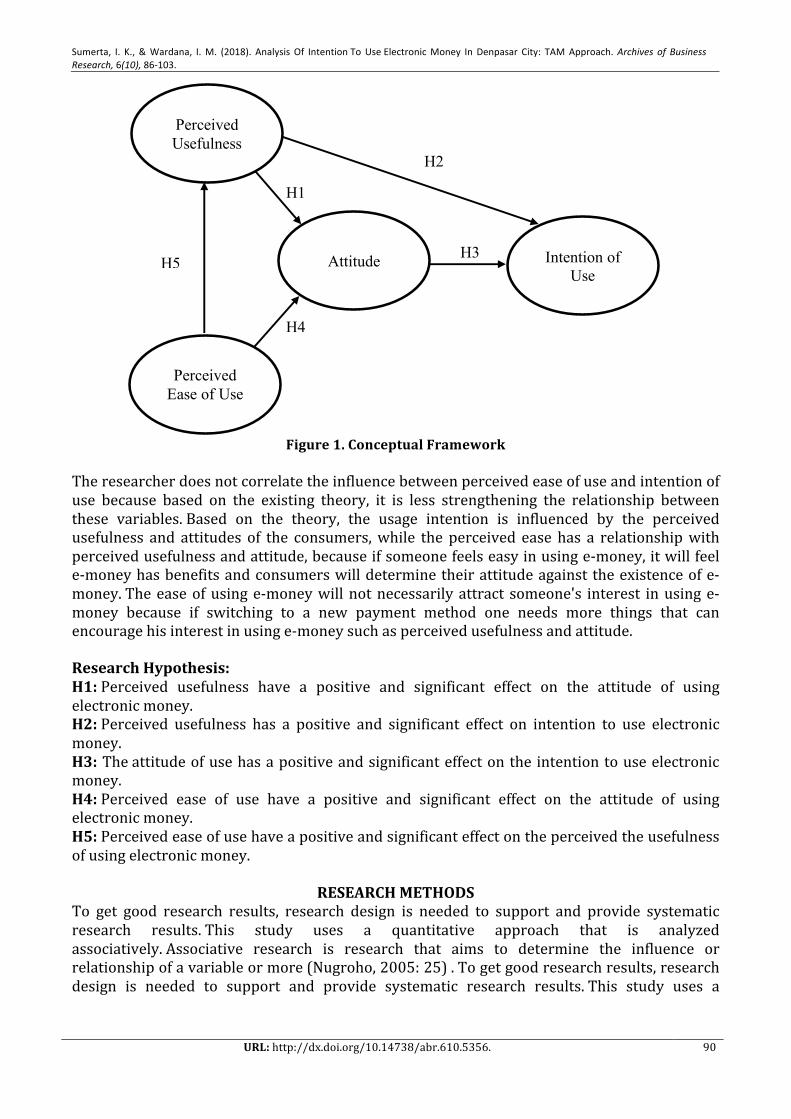

CONCEPTUALFRAMEWORK

Takingintoaccountalltheexposurestothetheoriesdescribedabove,alongwiththepositive

and negative aspects that exist in these theories, a model of a thinking and conceptualframeworkisarrangedasshownbelow:

Sumerta, I. K.,&Wardana, I.M. (2018). AnalysisOf IntentionToUseElectronicMoney InDenpasar City: TAMApproach.Archives of BusinessResearch,6(10),86-103.

URL:http://dx.doi.org/10.14738/abr.610.5356. 90

Figure1.ConceptualFramework

Theresearcherdoesnotcorrelatetheinfluencebetweenperceivedeaseofuseandintentionof

use because based on the existing theory, it is less strengthening the relationship between

these variables.Based on the theory, the usage intention is influenced by the perceivedusefulness and attitudes of the consumers,while the perceived ease has a relationshipwith

perceivedusefulnessandattitude,becauseifsomeonefeelseasyinusinge-money,itwillfeele-moneyhasbenefitsandconsumerswilldeterminetheirattitudeagainsttheexistenceofe-

money.Theeaseofusinge-moneywillnotnecessarilyattract someone's interest inusinge-

money because if switching to a new payment method one needs more things that canencouragehisinterestinusinge-moneysuchasperceivedusefulnessandattitude. ResearchHypothesis:H1:Perceived usefulness have a positive and significant effect on the attitude of usingelectronicmoney.H2:Perceived usefulness has a positive and significant effect on intention to use electronicmoney.

H3:Theattitudeofusehasapositiveandsignificanteffectonthe intentiontouseelectronicmoney.

H4:Perceived ease of use have a positive and significant effect on the attitude of usingelectronicmoney.

H5:Perceivedeaseofusehaveapositiveandsignificanteffectontheperceivedtheusefulnessofusingelectronicmoney.

RESEARCHMETHODSTo get good research results, research design is needed to support and provide systematic

research results.This study uses a quantitative approach that is analyzed

associatively.Associative research is research that aims to determine the influence orrelationshipofavariableormore(Nugroho,2005:25).Togetgoodresearchresults,research

design is needed to support and provide systematic research results.This study uses a

H3

H2

H1

H5

H4

Perceived Usefulness

Intention of Use

Attitude

Perceived Ease of Use

ArchivesofBusinessResearch(ABR) Vol.6,Issue10,Oct-2018

Copyright©SocietyforScienceandEducation,UnitedKingdom 91

quantitativeapproachthatisanalyzedassociatively.Associativeresearchisresearchthataims

todeterminetheinfluenceorrelationshipofavariableormore(Nugroho,2005:25).

Table2.

VariableOperationalDefinitionVariable Indicator Source

PerceivedUsefulness(X1) PU1=Speedupthepayment

process

PU2=Increasestheaccuracyofthepaymentprocess

PU3=Feelsafer

PU4=Giveattractivepromotions

PU5=Moreefficient

TaylorandTodd(1995c),Mafeet

al.(2009),RigopouosandAskounis

(2007).

PerceivedEaseofUse(X2) PEOU1=Easeofuse

PEOU2=Easeofunderstanding

PEOU3=PracticalinusePEOU4=Flexibility

RigopouosandAskounis(2007),

Davis(1989).

Attitude(Y1)

A1=Desired

A2=Useful

A3=OK

A4=Fun

TaylorandTodd(1995c),

Bhattacherjee(2000),Peslaket

al.(2010

Intention(Y2) ITU1=LookingforInformation

ITU2=WillingtoBuy

ITU3=FindingOut

ITU4=LearnITU5=Willingtouse

TaylorandTodd(1995c),

RigopoulosandAskounis(2007),

Peslaketal.(2010)

Source:Dataprocessed,2018

Basedonitsnature,thetypeofdatausedinthisstudyisquantitativedata.Quantitativedataisdata that can be calculated and in the form of numbers (Nugroho, 2005: 27).Data were

quantified in this research thatthe datacanbeanumberinthe results of the questionnaire

datathathavebeendistributed.

Primary data sources come from distributing questionnaires to respondents in accordancewith predetermined criteria that have been obtained directly from respondents

regardingperceivedusefulness,perceivedeaseofuse,attitudeandintentiontouseelectronic

money.The population used in this study is the prospective consumer of electronic moneylocated inDenpasarwhosenumberscannotbe identified.Thesampledeterminationmethod

used in this study isnon-probability samplingwhere this technique does notprovideequalopportunitiesoropportunitiesforeachelementormemberofthepopulationto

bechosenasasample(Sugiyono,2015:44).

The sampling technique in this study waspurposive sampling.Thispurposive

samplingtechnique is a technique thatdetermines a samplebasedon certain considerations

and is determined intentionally by the researcher (Nugroho, 2005: 40).In this study using18indicators so that the number of respondents used for the sample is 18x6= 108

respondents.Determinationofasampleof108respondentsinaccordancewiththeprovisionsof sampling to obtainmaximum results should be used larger orequalto 100 samples.The

measurementscaleusedinthisstudyistheLikertscale,whichisascalethathasbeenwidely

used to ask respondents to mark the degree of approval or disagreement with a series ofstimulusobjects.TheLikertscaleusedis1tostronglydisagreeto5stronglyagree.

Sumerta, I. K.,&Wardana, I.M. (2018). AnalysisOf IntentionToUseElectronicMoney InDenpasar City: TAMApproach.Archives of BusinessResearch,6(10),86-103.

URL:http://dx.doi.org/10.14738/abr.610.5356. 92

DataanalysistechniqueInferentialStatisticalAnalysisDataanalysisinthisstudyusedPartialLeastSquare(PLS)approach.PLSisanequationmodel

forStructural Equation Modeling(SEM) based on components or variants.To praise the

hypothesisandproducea feasiblemodel, this studyusesStructuralEquationModeling(SEM)with avariance basedorcomponent basedapproachwithPartial Least Square(PLS).If the

structural model tobeanalyzed meets the recrusive model and the latent variable hasnormativeindicators.Reflectiveormixed,themostappropriateapproachtouseisPLS.

RESEARCHRESULTCharacteristicsofRespondents

Table3.CharacteristicsofRespondents

No. Variable Classification amount

Percentage(%)

1 Age(year) 19-23 26 24.1

24-28 57 52.8

29-33 16 14.8

34-38 5 4,6

39-43 1 0.9

44-48 1 0.9 49-53 1 0.9

54-58 1 0.9

2 Gender Woman 42 38.9

Man 66 61.1

3 Lasteducation Highschool 54 50

Diploma 5 4,6

Bachelor 47 43.5

Postgraduate 2 1.9

4 Work Student/Student 15 13,9 PNS/TNI/POLRI 2 1.9

Privateemployees 85 78.7

Entrepreneur 2 1.9

Professional 4 3.7

5 Expendituresin1month IDR1,000,000-IDR2,750,000 55 50,9

IDR2,750,001-IDR4,500,000 34 31.5

IDR4,500,001-IDR6,250,000 16 14.8

IDR6,250,000-IDR8,000,000 1 0.9 IDR.9,750,001-IDR.11,500,000 1 0.9

IDR13,250,001-IDR15,000,000 1 0.9

Source:Dataprocessed,2018

Table3shows several things related to the characteristics of respondents.Referring to thetable it can be seen that the male respondents more mmendominasi which amounted

to61,1percent comparedwith38.9percentof female respondents.Basedon theagegroup,

respondentsaged24 to28have thehighestpercentage,which is52.8percent.Basedon therespondents' last education, it can be seen that the level of high school education has the

highest percentage of 50 percent.Based on the type of work, can be seen in private sectoremployeeshavethehighestpercentagethatisequalto78,7percent.Basedonexpendituresin

one month, it can be seen spending of IDR 1,000,000 to IDR 2,750,000 has the highest

percentageof50,9percent.

ArchivesofBusinessResearch(ABR) Vol.6,Issue10,Oct-2018

Copyright©SocietyforScienceandEducation,UnitedKingdom 93

RespondentAnswerDistributionAccordingtoNataWirawan(2002:35)thedeterminationoffrequencydistributionisbasedon

theintervalvalue,sotoobtainthefrequencydistribution.Tofindouttheoverallassessmentoftheresearchvariables,itwillbeseenfromtheaveragescorewiththefollowingcriteria:

1.00-1.79=VeryLow

1.80-2.59=Low

2.60-3.39=Neutral

3,40-4,19=Height

4,20-5,00=VeryHighBased on the results of the study, it can be seen the responses of respondents from each

indicatorofeachvariableasfollows:

PerceivedUsefulnessTable4shows that the total average response scoreRespondents regarding the usefulnessperceptionvariablemeasuredusing5indicatorsis4.10.

Table4

AssessmentofRespondentsonVariablesPerceivedBenefit

No. StatementAnswerClassification

Average InformationSTS TS N S SS1 2 3 4 5

1 Speedupthepaymentprocess 0 1 7 62 38 4.27 Veryhigh

2Increasetheaccuracyofthepayment

process 0 4 13 56 35 4,13 High

3 Feelsafer 1 4 19 48 36 4.06 High

4 Giveattractivepromotions 4 6 30 45 23 3.71 High

5 Moreefficientintransactions 1 1 8 50 48 4.32 Veryhigh

AverageScoreTotal 4.10 HighSource:Dataprocessed,2018

Based on these results that the average respondent's overall answer about the perceived

usefulnessintheuseofelectronicmoneyinDenpasarCitywashigh.Indicatorwiththehighestaveragescoreismoreefficientintransactionsof4.32.

EaseofPerceptionTable 5shows that the total average score of respondents' responses regarding perceived

usefulnessvariablesmeasuredusing4indicatorsis4.07.

Table5AssessmentofRespondentsonEasePerceptionVariables

No. StatementAnswerClassification

Average InformationSTS TS N S SS1 2 3 4 5

1 Easytolearn 1 0 16 75 16 3.97 Veryhigh

2 Easytouseintransactions 0 0 13 59 36 4.21 Veryhigh

3 Practicalinuse 0 0 7 54 47 4.37 Veryhigh

4 Flexible(usedanytimeandanywhere) 1 11 27 45 24 3.74 High

AverageScoreTotal 4.07 HighSource:Dataprocessed,2018

Sumerta, I. K.,&Wardana, I.M. (2018). AnalysisOf IntentionToUseElectronicMoney InDenpasar City: TAMApproach.Archives of BusinessResearch,6(10),86-103.

URL:http://dx.doi.org/10.14738/abr.610.5356. 94

Basedontheseresultsthattheaveragerespondent'soverallanswerabouttheperceivedease

of use of electronic money in Denpasar is high.Indicator with the highest average score ispracticalinusageof4.37

AttitudeTable6shows that the total average score of respondents' responses regarding attitude

variablesmeasuredusing4indicatorsis4.06.

Table6AssessmentofRespondentsonAttitudeVariables

No. StatementAnswerClassification

Average InformationSTS TS N S SS1 2 3 4 5

1 Iamveryinterestedinelectronicmoney 0 4 10 61 33 4,14 High

2 ElectronicMoneyisveryuseful 0 2 15 57 34 4,14 High

3 Electronicmoneyisgoodtouse 0 0 20 59 29 4.08 High

4 Funelectronicmoney 0 3 26 59 20 3.89 High

AverageScoreTotal 4.06 HighSource:Dataprocessed,2018

Based on these results, the average respondent's overall answers to attitudes in the use ofelectronicmoneyinDenpasarCitywerehigh.Theindicatorwiththehighestaveragescoreis

veryinterestedinelectronicmoneyandelectronicmoneyisveryusefulat4.14.

IntentionofUseTable7shows that the total average score of respondents' responses regarding the useintentionvariablemeasuredusing5indicatorsis4.17.

Table7

AssessmentofRespondentsonVariableIntentionsofUse

No. StatementAnswerClassification

Average InformationSTS TS N S SS1 2 3 4 5

1Iwilllookformoredetailedinformation

aboutelectronicmoney. 0 1 16 61 30 4,11 High

2 Iamwillingtobuyelectronicmoney. 1 2 15 53 37 4,14 High

3 Iwillfindoutwheretobuyelectronicmoney. 0 3 16 57 32 4.09 High

4 Iwillfindouthowtouseelectronicmoney. 0 2 11 59 36 4.19 High

5 Iamwillingtouseelectronicmoney. 1 2 9 45 51 4.32 Veryhigh

AverageScoreTotal 4,17 HighSource:Dataprocessed,2018

Based on these results that the average respondent's overall answer about the intention of

using electronicmoney in Denpasar Citywas high.Indicatorwith the highest average scorethatiswillingtouseelectronicmoneyof4.32.

TestingofResearchInstrumentsValiditytestValiditytestcanbedonebycorrelatingbetweeninstrumentitemscoreswithatotalscoreofall

statement items.If thecorrelationbetweeneach itemscorestatementon the totalscore, thestatement points indicate the correlation coefficient value ≥ 0, 3then each item of the

statementissaidtobevalid(Sugiyono,2012:178).

ArchivesofBusinessResearch(ABR) Vol.6,Issue10,Oct-2018

Copyright©SocietyforScienceandEducation,UnitedKingdom 95

Table8InstrumentValidityTestResults

No. Variable Indicator Correlationcoefficient Information1 PerceivedUsefulness X1.1 0.408 Valid

X1.2 0.688 Valid

X1.3 0.705 Valid

X1.4 0.730 Valid X1.5 0.710 Valid

2 EaseofPerception X2.1 0.493 Valid

X2.2 0.851 Valid

X2.3 0.629 Valid

X2.4 0.718 Valid

3 Attitude Y1.1 0.705 Valid

Y1.2 0.729 Valid

Y1.3 0.754 Valid Y1.4 0.87 Valid

4 IntentionofUse Y2.1 0.909 Valid

Y2.2 0.863 Valid

Y2.3 0.905 Valid

Y2.4 0.884 Valid

Y2.5 0.815 Valid

Source:Dataprocessed,2018BasedonthevaliditytestinTable8shows18indicatorsusedhaveacorrelationvaluegreater

than0.3sothattheoverallindicatorsusedaredeclaredvalid.

ReliabilityTestReliability or reliability testing of instruments shows the extent towhich ameasurement isreturned to thesamesymptoms.A reliable instrument is an instrument that is used several

timestomeasurethesameobjectwillproducethesamedataoranswer.Theinstrumentissaidtobereliableifithasacronbachalpha≥0,60.(Sugiyono,2012:172)

Table9

InstrumentReliabilityTestResultsVariable Cronbach'sAlpha Information

PerceivedUsefulness 0.845 ReliableEaseofPerception 0.676 ReliableAttitude 0.941 ReliableIntentionofUse 0.916 Reliable

Source:Dataprocessed,2018

DATAANALYSISEvaluationoftheGoodnessoffitPLSmodel.BasedontheresultsofWarp-PLSoutput,thefollowingresultsareobtainedfromAPC,ARS,andAVIF.

Table10

GoodnessofFitFitmodel Index p-value Criteria InformationAveragepathcoefficient(APC) 0.487 P<0.001 P<0.050 Beaccepted

AverageR-Squared(ARS) 0,594 P<0.001 P<0.050 BeacceptedAverageBlockVarianceInflationFactor(AVIF) 1,990 <5 Beaccepted

Source:Dataprocessed,2018

Sumerta, I. K.,&Wardana, I.M. (2018). AnalysisOf IntentionToUseElectronicMoney InDenpasar City: TAMApproach.Archives of BusinessResearch,6(10),86-103.

URL:http://dx.doi.org/10.14738/abr.610.5356. 96

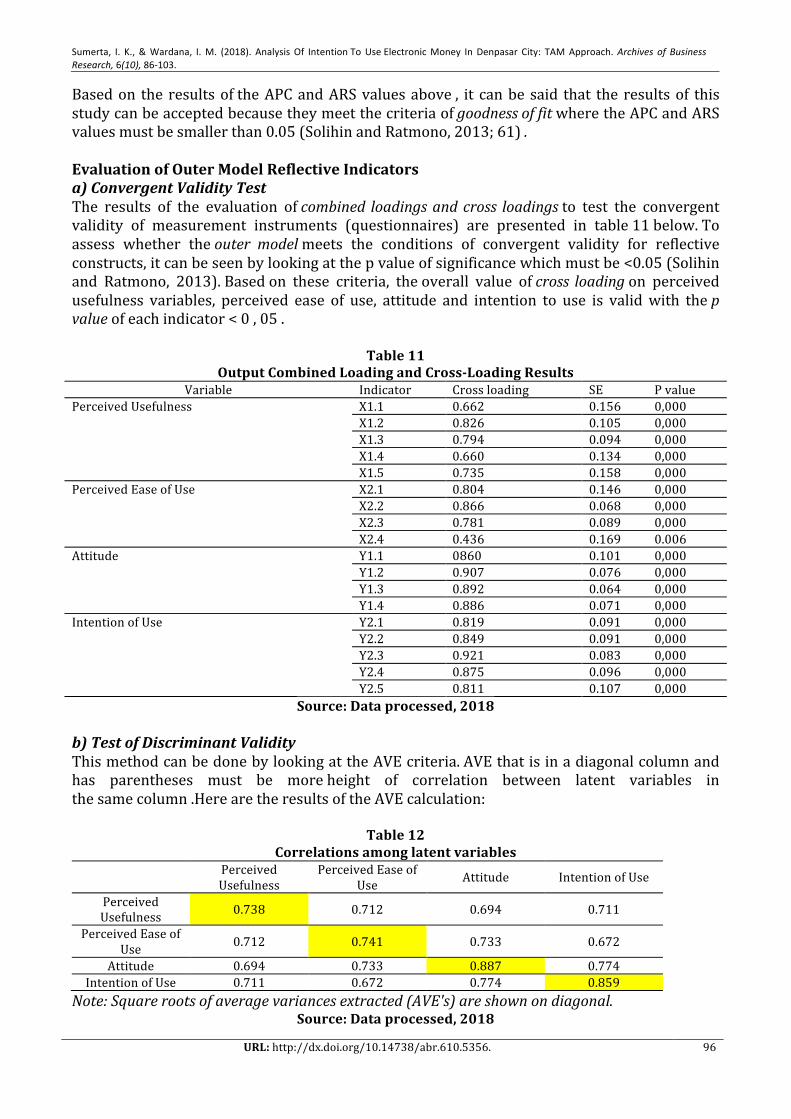

Basedon the resultsoftheAPCandARSvaluesabove, it canbesaid that the resultsof this

studycanbeacceptedbecausetheymeetthecriteriaofgoodnessoffitwheretheAPCandARSvaluesmustbesmallerthan0.05(SolihinandRatmono,2013;61).

EvaluationofOuterModelReflectiveIndicatorsa)ConvergentValidityTestThe results of the evaluation ofcombined loadingsandcross loadingsto test the convergentvalidity of measurement instruments (questionnaires) are presented in table11below.To

assess whether theouter modelmeets the conditions of convergent validity for reflective

constructs,itcanbeseenbylookingatthepvalueofsignificancewhichmustbe<0.05(Solihinand Ratmono, 2013).Basedon these criteria, theoverall value ofcross loadingon perceived

usefulness variables, perceived ease of use, attitude and intention to use is validwith thepvalueofeachindicator<0,05.

Table11

OutputCombinedLoadingandCross-LoadingResultsVariable Indicator Crossloading SE Pvalue

PerceivedUsefulness X1.1 0.662 0.156 0,000

X1.2 0.826 0.105 0,000

X1.3 0.794 0.094 0,000

X1.4 0.660 0.134 0,000

X1.5 0.735 0.158 0,000

PerceivedEaseofUse X2.1 0.804 0.146 0,000

X2.2 0.866 0.068 0,000

X2.3 0.781 0.089 0,000

X2.4 0.436 0.169 0.006

Attitude Y1.1 0860 0.101 0,000

Y1.2 0.907 0.076 0,000

Y1.3 0.892 0.064 0,000

Y1.4 0.886 0.071 0,000

IntentionofUse Y2.1 0.819 0.091 0,000

Y2.2 0.849 0.091 0,000

Y2.3 0.921 0.083 0,000

Y2.4 0.875 0.096 0,000

Y2.5 0.811 0.107 0,000

Source:Dataprocessed,2018b)TestofDiscriminantValidityThismethodcanbedonebylookingattheAVEcriteria.AVEthatisinadiagonalcolumnandhas parentheses must be moreheight of correlation between latent variables in

thesamecolumn.HerearetheresultsoftheAVEcalculation:

Table12Correlationsamonglatentvariables

Perceived

UsefulnessPerceivedEaseof

UseAttitude IntentionofUse

PerceivedUsefulness

0.738 0.712 0.694 0.711

PerceivedEaseof

Use0.712 0.741 0.733 0.672

Attitude 0.694 0.733 0.887 0.774IntentionofUse 0.711 0.672 0.774 0.859

Note:Squarerootsofaveragevariancesextracted(AVE's)areshownondiagonal.

Source:Dataprocessed,2018

ArchivesofBusinessResearch(ABR) Vol.6,Issue10,Oct-2018

Copyright©SocietyforScienceandEducation,UnitedKingdom 97

Table12showsthatthecriteriafordiscriminantvalidityhavebeenfulfilledasindicatedbythe

squarerootAVEgreaterthanthecorrelationcoefficientbetweenconstructsineachindicator

ofeachvariablecanmeasurethesevariablespreciselythanwithothervariables.

a)Testthevalidityofresearchinstruments

Table13Averagevariancesextracted

AveragevariancesextractedPerceivedBenefit 0.545PerceivedEaseofUse 0.549Attitude 0,786IntentionofUse 0.733

Source:Dataprocessed,2018(Attachment7)

Averagevarianceextracted(AVE)foreachindicatorismorethan0,50,soitcanbesaidthat

thefourconstructsmeettheconvergentvaliditycriteria.

b)Researchinstrumentreliabilitytest

Table14

Researchinstrumentreliabilitytest Composite reliability coefficients Cronbach's alpha coefficients Perceived Benefit 0.856 0.788 Perceived Ease of Use 0.822 0.708 Attitude 0.936 0.909 Intention of Use 0.932 0.908

Source:Dataprocessed,2018

The reliability of the research instrument was measured using two measures,composite

reliabilityandcronbach's alpha.Based on these data, each indicator has met the sizeofcompositereliabilityandCronbach'salphais>0,70.

InnerModelEvaluationInner model evaluation aims to determine the goodness of fit model with the following

methods:a)R-Square(R2)Showsthestrongweakinfluencecausedbyvariationsinexogenousvariablesonendogenousvariables.TheR-Square valueis greater than 0, 50categorized as a strong model.TheR-

Squarevalues of each endogenous variable from the results of data processing performed

arepresentedintheformofTable15below:

Table15RatedR-SquareResearch

R-Square Value Criteria(Chin,1998)PerceivedBenefit 0.519 StrongPerceivedEaseofUse - Attitude 0.602 StrongIntentionofUse 0.661 Strong

Source:Dataprocessed,2018

BasedonthesedatathevalueoftheR-squareconstructperceivedusefulnessof0.519indicates

that the variance of perceived usefulnesscan be explained by 51.9% by the variance of

Sumerta, I. K.,&Wardana, I.M. (2018). AnalysisOf IntentionToUseElectronicMoney InDenpasar City: TAMApproach.Archives of BusinessResearch,6(10),86-103.

URL:http://dx.doi.org/10.14738/abr.610.5356. 98

perceived ease of use.R-squaredconstruct constructsof 0.602 indicate that the variance of

attitudescan be explained by 60, 2% by the variance of perceived usefulness, and theperceived ease of use.R-squaredconstruct of use intentionof0.661 indicatesthat the

varianceofuseintentioncanbeexplainedby66.1%byvarianceofperceivedusefulness,and

attitude.

b)Q-SquareQ-squarepredictiverelevancetomeasurehowwell theobservationvalue is generatedby the

model and its parameter estimates.ValueQ-square> 0 indicates the model haspredictive

relevance, otherwise if the value ofthe Q-square<0 indicates the model lackspredicttiverelevance.

Table16

ValueQ-SquareResearch Q-SquarePerceivedBenefit 0.521PerceivedEaseofUse -Attitude 0.605IntentionofUse 0.664

Source:Dataprocessed,2018

Q-squareis the result of testing predictive validity and the value must be greater thanzero(SolihinandRatmono,2013).Themodelestimationresultsshowgoodpredictivevalidity

of 0.521, 0.605 and 0.664, so that the value is above zero,whichmeans that the predictivevalidity of each of these variables is categorized as good.TheoverallQ-Square(Predictive

Relevance)valueofthemodelcanbecalculatedasfollows:

Q2=1-(1-R21)(1-R22)(1-R23)

Q2=1-(1-0.519)(1-0.602)(1-0.661)

Q2=1-(0.481)(0.398)(0.339)

Q2=1-0.0649 Q2=0.9351

ThecalculationaboveobtainedvalueofQ2at0.9351,so that thevalue isgreater than0and

thusmayotherwisegoodpredictivevalidity.

a)TestingVariableRelationshipStatisticsTestingofvariablerelationshipstatisticscanbeseenbylookingattheeffectsizevaluewhichis

calculatedas theabsolutevalueof individualcontributions foreach latentvariablepredictoronthevalueofR-Squared.

Table17

PathCoefficient

Standard

ErrorEffect

SizePath

coefficientsP

valuesPerceivedUsefulness à Attitude 0.097 0.247 0.354 0.001PerceivedUsefulness à IntentionofUse 0.077 0.235 0.330 0.001

PerceivedEaseofUse àPerceived

Usefulness0.074 0.519 0.720 0.001

PerceivedEaseofUse à Attitude 0.090 0.355 0.484 0.001Attitude à IntentionofUse 0.074 0.426 0.547 0.001

Source:Dataprocessed,2018

ArchivesofBusinessResearch(ABR) Vol.6,Issue10,Oct-2018

Copyright©SocietyforScienceandEducation,UnitedKingdom 99

Sizeeffectscanbegroupedintothreecategories:weak(0.02),medium(0.15),andlarge(0.35)

(SolihinandRatmono,2013;33).Table5.16showsthattheeffectsizevalueofeachvariableis

greaterthan0.2sothatitisinthemediumandlargecategory.Testingofvariablerelationshipstatistics can also be seen from thevalueofthe path coefficients for

eachvariablerelationshipshowsapositive and significantrelationshipbecausep-value is less

than0.05(SolihinandRatmono,2013;62).

Figure2.Modeltestingresults

Source:Dataprocessed,2018

DISCUSSION

TheinfluenceofperceptionsofusefulnessontheattitudeofusingelectronicmoneyThe resultsof hypothesis testingshowthat perceptions of usefulness have a positive and

significanteffectontheattitudeofusingelectronicmoney.Thisresultmeansthatthemoreapersonfeelsthatelectronicmoneyisbeneficial,itwillencouragesomeonetobepositiveabout

the use of electronic money.This is supported by researchsuch as that conducted

byAlagozandHekimoglu, (2012),Yadavet al.(2015),Baileyet al.(2017),Maet al.(2017)andWeiet al.(2017)get the same results, namely the Perceived usefulness has a positive

effectonattitude.

TheinfluenceofperceptionsofusefulnessontheintentionofusingelectronicmoneyBased on the hypothesis test, it is found that the Perceived usefulness has a positive andsignificant effect on the intention of using electronic money.This means that the more

someonefeelselectronicmoneyisuseful,thepersonwillhavemoreintentiontouseelectronic

money.ThisisconsistentwiththeresearchconductedbyGiovanisetal.(2012),

Safeenaet al.(2013),Awaet al.(2015),Dakduketal.(2017)andWeietal.(217)found thatperceptionsofusefulnesshaveapositiveandsignificanteffectonconsumerintentions.

Theeffectofusageattitudeontheintentionofusingelectronicmoney.Basedonthehypothesistest foundthattheattitudeofusingelectronicmoneyhasapositive

andsignificanteffecton the intentionofusingelectronicmoney.Thismeans that themorea

person has a positive attitude towards the use of electronic money, it will bepossibletoincreasetheperson'sintentiontouseelectronicmoney.Thisisconsistentwiththeresearch

ofYadav,et al.(2015),Dakduketal.(2017) andWeietal.(2017)found that attitude had apositiveandsignificanteffectonintention.

Effectofperceptionsofeaseofuseontheattitudeofusingelectronicmoney.BasedonthehypothesistestfoundthatthePerceivedeaseofusehasapositiveandsignificant

effectontheattitudeofusingelectronicmoney.Thismeansthatthemoresomeonefeelsthe

ease with the existence of electronic money, the person will have a more positive attitude

Sumerta, I. K.,&Wardana, I.M. (2018). AnalysisOf IntentionToUseElectronicMoney InDenpasar City: TAMApproach.Archives of BusinessResearch,6(10),86-103.

URL:http://dx.doi.org/10.14738/abr.610.5356. 100

towardselectronicunag.This is consistentwithprevious research that thePerceivedeaseof

usehasapositiveandsignificanteffectonattitudes,suchasresearchconductedbyHsiaoandTang(2014),Dakduketal.(2017)andWeietal.(2017).

TheinfluenceofperceptionsofeaseofuseonthePerceivedtheusefulnessofelectronicmoneyBasedonthehypothesistestfoundthatthePerceivedeaseofusehasapositiveandsignificanteffectonthePerceivedtheusefulnessofelectronicmoney.Thismeansthatthemoreaperson

feelsthattheeasegainedbyusingelectronicmoneywill improveone'sperceptionrelatedto

the usefulness of electronic money.This is supported byresearchbyRauniaretal.(2014),Phonthanukitithaworn,etal.(2015),Dakduketal.(2017)an

dWeietal.(2017)who found that the Perceived ease of use had a positive and significanteffectonperceptionsofusefulness.

IMPLICATIONSOFRESEARCHRESULTSImplicationsTeoretisBasedonthefindingsinthisLitianpene,thentheimplicationTeoretiscouldbesaidthatthis

research model, enrich the concept of consumer behavior in marketing, especially in theintention of using electronic money.The results of this study indicate thatperceptions of

usefulness,perceivedeaseandattitudehaveapositiveandsignificanteffectontheintentiontouse electronicmoney.The results also reinforce dansupportthe results of previous studies

relatedtotheintentionofusingelectronicmoney.It isexpectedthattheresultsofthisstudy

can be used as reference material in knowing the development of marketing strategies forelectronicmoneyproductsandthedevelopmentofconsumerbehaviortowardsintentionsor

interests and consumer responses in using electronic money and / or other new productsbasedontechnology.

PracticalImplicationsBased on the results of the study obtained practical implications about the factors that

influence the intention to use electronicmoney.Intention of usein this study is aconsumer

behaviorwhereconsumershaveadesiretouseanelectronicmoneyproduct.Thefactorsthatinfluence the intention to use in this study are perceptions of usefulness, perceived ease of

use,and attitude.The results of this study also enable electronicmoney issuing companies,especially those domiciled in Denpasar, to bemore aware of aspects that can improve and

improve in promoting or implementing appropriate marketing strategies to increase the

interest of the community's intention to use electronic money as a mediumforfuturemicropaymenttransactions.

CONCLUSIONSANDRECOMMENDATIONS ConclusionBasedon theresultsof thediscussions thathavebeencarriedout, the followingconclusionsareobtained:

1) Perceived usefulness and significant positive effect on the attitudes of the use ofelectronicmoney.Thisresultmeansthatthemoreapersonfeelsthatelectronicmoneyisbeneficial,itwillencouragesomeonetobepositiveabouttheuseofelectronicmoney.

2) Perceivedusefulnesspositiveandsignificanteffectontheintentionofuseofelectronicmoney.Thismeansthatthemoresomeonefeelselectronicmoneyisuseful,theperson

willhavemoreintentiontouseelectronicmoney.

ArchivesofBusinessResearch(ABR) Vol.6,Issue10,Oct-2018

Copyright©SocietyforScienceandEducation,UnitedKingdom 101

3) Theuseofelectronicmoneyhasapositiveandsignificanteffectontheintentiontouseelectronicmoney.Thismeansthatthemoreapersonhasapositiveattitudetowardsthe

useofelectronicmoney,itwillincreaseone'sintentiontouseelectronicmoney.4) Perceived ease of use positive and significant impact on the attitudes of the use of

electronicmoney.Thismeans themoreone feels feel the easewith electronicmoney

thensomeonewillincreasinglyhaveapositiveattitudetowardsuangelectronics.5) PerceivedeaseofusepositiveandsignificanteffectonthePerceivedtheusefulnessof

electronicmoney.Thismeansthatthemoreapersonfeelsthattheeasegainedbyusingelectronicmoneywill improveone'sperceptionrelatedtotheusefulnessofelectronic

money.

SUGGESTION

After studying, analyzing, discussing and drawing conclusions, the writer gives somesuggestions as a consideration in the future.The suggestions that can be submitted are as

follows.

ForPractitionersElectronicmoneypublisherswhouseelectronicmoneywillbemoregoodifyoucanincrease

marketingrelatedtotheusefulnessandusefulnessofelectronicmoneysothatitcancreateapositive attitude for its users.Based on the characteristics of respondents, the dominant

respondent'sageis24yearsto28years.Sothatbusinesspeoplewhoissueelectronicmoneytobemorelikelytotargetpeopleaged24to28yearsbecauseatthatagethecommunitytends

tobeinterestedintherenewalofpaymenttechnology,sothiswillfurtherfacilitatethespread

ofelectronicmoney.

ForAcademicsSuggestions for future researchare tobe considered to conduct research indifferentplacesand also expand the research area and target respondents who are more specializedforexampleinadolescentsoradults.Futurestudiesarealsoexpectedtoanalyzetherelationship

mediationofvariables -variables thatexist in theTAMtheory tomeasureandbroader lookfactorsthatmayaffectattitudesandintentionsintheuseofaproduct.Inthefuture,itisalso

expectedthatresearcherscanconductresearchnotonlytomeasureintentions,butalsotothe

variablesofconsumerbehaviortowardstheintentionstheyobtain.

RESEARCHLIMITATIONS1) This researchscopeonlyon the consumer electronicmoneyproducts inDenpasar, so

thatresearchresultscannotbegeneralizedtotheconsumerelectronicmoneyproducts

inotherregions.2) This research only examines the extent to the intention of prospective consumers

towardstheuseofelectronicmoney,atwhereinTAMisitpossibletoconductresearch

tomeasuretheattitudesofprospectiveconsumersthatariseasaresultoftheintentiontouseelectronicmoney.

3) This research is only carried out in certain time points (cross section),while theenvironment changes every time (dynamic), so this research is important to be done

againinthefuture.

ReferenceAjzen,I.1991.‘Thetheoryofplannedbehavior’,OrgnizationalBehaviordanHumanDecisionProcesses.Academia

Press.Inc.Vol.50,pp.179–211.

Akinci,S.,Aksoy,Ş.danAtilgan,E.2004.‘AdoptionofInternetbankingamongsophisticatedconsumersegmentsinanadvanceddevelopingcountry’,InternationalJournalofBankMarketing.Vol.22.No.3,pp.212–232.

Sumerta, I. K.,&Wardana, I.M. (2018). AnalysisOf IntentionToUseElectronicMoney InDenpasar City: TAMApproach.Archives of BusinessResearch,6(10),86-103.

URL:http://dx.doi.org/10.14738/abr.610.5356. 102

AlagozdanHekimoglu.2012.‘AStudyonTam:AnalysisofCustomerAttitudesinOnlineFoodOrderingSystem’,

Procedia-SocialdanBehavioralSciences.Vol.6.No.2,pp.1138–1143.

Bhattacherjee,A.2000."Acceptanceofe-commerceservices:thecaseofelectronicbrokerages",IEEETransactions

onSystem,Man,danCybernetics-PartA:SystemHumans,Vol.20.No.4.pp.411-20.

Chin,W.W.1998.ThePartialleastsquaresapproachforstructuralequationmodeling.inG.A.Marcoulides(Ed.),

Modernmethodsforbusinessresearch(pp.295-236).London:LawrenceErbaumAssociates.

Dakduk,S.EnriqueterHorst,ZuleymaSantalla,GermanMolinaandJoséMalavé.2017.‘Customerbehaviorin

electroniccommerce:Abayesianapproach’,JournalofTheoreticaldanAppliedElectronicCommerceResearch,Vol.

12.No.2,pp.1–20.

Davis.1989.S‘PerceivedUsefulness,PerceivedEaseOfUse,danUserAcceptance’,MISQuarterly,Vol.13.No.3,

pp.319–339.

Giovanis,A.N.,Binioris,S.danPolychronopoulos,G.2012‘AnextensionofTAMmodelwithIDTdan

security/privacyriskintheadoptionofinternetbankingservicesinGreece’,EuroMedJournalofBusiness.Vol.7.

No.1,pp.24–53.

Hawkins.2001.ConsumerBehavior:BuildingMarketingStrategy,NewYork:McGraw-HillInc.

Hawkins,D.I,danMothersbaugh,D.I.2010.ConsumerBehaviour:BuildingMarketingStrategy.11thedition.New

York:McGraw-Hill,Irwin.

HowarddanSheth.1979.TheTheoryofNuyerBehaviour,NewYork,JohnWiley.

Hsiao,C.-H.danTang,K.-Y.2014.‘Explainingundergraduates’behaviorintentionofe-textbookadoption’,Library

HiTech,Vol.32No.1,pp.139–163.

Kotler,PdanKevin,L,K.2006.MarketingManagement12e.PearsonInternationalEdition.NewJersey.

Kotler,Philip,danK.L.Keller.2009.ManajemenPemasaran.DiterjemahkanolehBobSabran.Jakarta:

Erlangga.

Latan,hengky,2012.StructuralEquationModeling,KonsepdanAplikasiMenggunakanProgramLisrel8.80,PenerbitAlfabeta,Bandung.

Li,J,.Dick,m.,Alvin,L.andFang,L.,2008.“TheRelationshipBetweenAttitudedanBehavior;AnEmpiricalStudyin

China”.UWABusinessSchool,TheUniversityofWesternAustralia,Crawley,Australia.

Ma,YoonJin,HaeJinGamandJenniferBanning.2017.‘Perceivedeaseofusedanusefulnessofsustainability

labelsonapparelproducts:applicationofthetechnologyacceptancemodel’,FashiondanTextiles.SpringerBerlin

Heidelberg,Vol.4.No.3.pp.1-20.

Mafe.2009.AComparativestudyofmobilemessagingserviceacceptancetoparticipateintelevisionprogrammes,

JournalofServiceManagement,Vol.2No.1.pp.69-102.

Nugroho,Agung.2005.StrategiJituMemilihMetodeStatisticPenelitiandenganSPSS.Jogyakarta.

Peter,P.J.,Olson,J.C.2008.“ConsumerBehaviorinMarketingStrategy”.EightEdition.McGraw-HillInternational

Edition.

Peslak,A.,Ceccucci,W.danSendall,P.2010,AnEmpiricalStudyofInstantMessaging(IM)BehaviorUsingTheory

OfReasonedAction.

PhonthanukitithawornChanchai,CarmineSellittoandMichelleFong,2015.‘UserIntentionstoAdoptMobile

PaymentServices:AStudyofEarlyAdoptersinThailandCHANCHAI’,JournalofInternetBankingdanCommerce,

Vol.20No.1,pp.1–11.

RigopoulosdanAskounis.2007.ATAMFrameworktoEvaluateUsers'PerceptiontowardsOnlineElectronic

Payments,JournalofInternetBankingdanCommerce,Vol.12.No.3.pp.1-20.

SafeenaR.HemaDate,NisarHundewale,andAbdullahKammani.2013.‘CombinationofTAMdanTPBinInternet

BankingAdoption’,InternationalJournalofComputerTheorydanEngineering,Vol.5.No.1.pp.146–150.

Schiffman,L.GdanKanuk,L.K,2010.“ConsumerBehavior”,10thedition.NewJersey,PearsonPrenticeHall.

Sugiyono,2015.MetodePenelitianKuantitatifKualitatifdanRdanD.Bandung.Afabeta.

Taylor,S.danTodd,P.A.1995.DecompositiondanCrossoverEffectsintheTheoryofPlannedBehavior:AStudyof

ConsumerAdoptionIntentions.InternationalJournalofResearchinMarketing,Vol.1No.2.pp.137-55.

ArchivesofBusinessResearch(ABR) Vol.6,Issue10,Oct-2018

Copyright©SocietyforScienceandEducation,UnitedKingdom 103

Taylor,SdanTood,P.A.1955c,UnderstandingInformationTechnologyUsage:ATestofCompetingModels,

InformationSystemResearch,Vol.6.No.2.pp.144-76.

Wei,QijunXie,SongXiaobaoPeng,andMuhammadShabbir.2017‘Predictorsfore-governmentadoption:

integratingTAM,TPB,trustdanperceivedrisk’,TheElectronicLibrary,Vol.35.No.1.pp.2–20.

Yadav,R.,Chauhan,V.danPathak,G.S.2015‘Intentiontoadoptinternetbankinginanemergingeconomy:a

perspectiveofIndianyouth’,InternationalJournalofBankMarketing,334,pp.530–544.doi:10.1108/EL-01-

2014-0022.

OnlineSource:htttp://www.bi.go.id

http://www.bisnis.com