volrv_db

DESCRIPTION

Relative value volTRANSCRIPT

Practical Relative-Value Volatility Trading

Stephen Blyth,

Managing Director, Head of European Arbitrage Trading

21 January 2005

2

Volatility modelling

� Construct a consistent framework to identify and extract value from interest-rate options markets

� Use this framework to inform decisions concerning inception and management of proprietary options trading positions

3

Modelling paradigm

� Insist on consistent pricing and hedging framework: only one US dollar (or euro) libor yield curve, therefore only one process –random or otherwise – driving this curve

� Avoid pragmatic use of simplest model per product – can result in inconsistent dynamics

� Make sensible choices about objective features to incorporate into modelling formulation: e.g. multifactor, skew dynamics

� Require advanced analytics to develop tractable pricing and riskmanagement tools – often an obstacle to successful implementation

4

Modelling paradigm (cont’d)

� Pricing inconsistencies between market and model can indicate:

– market features

– modelling errors

– trading opportunities

� Use market experience and judgment to identify the latter

� Warning: Models have Limitations!

– “It is wrong to think that the task of physics is to find out how nature is. Physics concerns what we can say about nature” Niels Bohr

– “A trader armed only with a clever model is soon removed from his capital”

Nature Financial markets

Physics Quantitative modelling

5

Modelling paradigm (cont’d)

� Significant advances in quantitative financial modelling over past ten years. Need judgment to harness these advances

� Tukey: judgment based on

– mathematical knowledge of the particular techniques

– experience of the particular field of subject matter

– experience of how these techniques have worked out in practice

6

Forward volatility surfaces

� Translate universe of option prices into how each point on yieldcurve (e.g. each Euribor future) oscillates over time

� More precisely: strip swaptions, caps and other option products into a forward volatility surface, σ (t,T)

� For fixed T, σ (t,T) represents the volatility of a particular Eurodollar (or Euribor) contract over its life. These “forward volatilities” are observable quantities about which can make subjective judgments

7

Forward volatility surfaces (cont’d)

� Framework adopts multifactor BGM Model

df(t, T) = a(t,T) dt + σσσσ(t, T) ΣΣΣΣ ρρρρi (t, T) dWi (t)

– f (t , T) 3m-forward rate from T at time t

– Drift a(t, T) determined from volatility σ(t, T)

n

i = 1

8

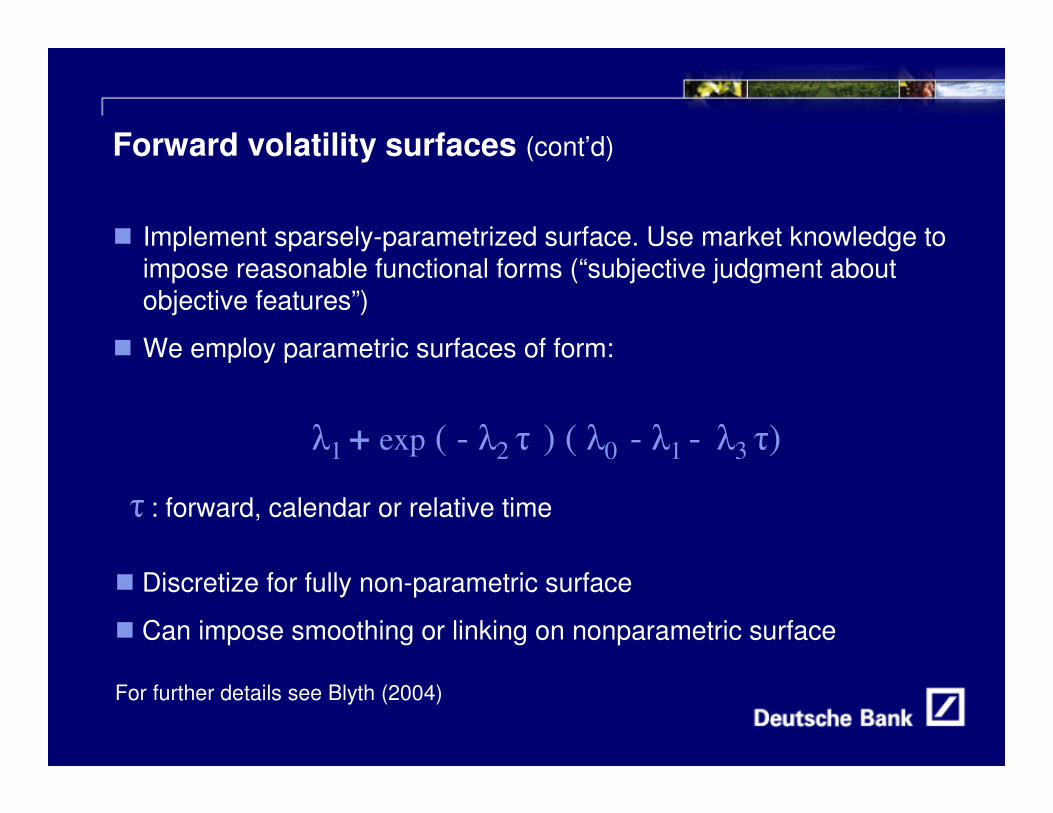

Forward volatility surfaces (cont’d)

� Implement sparsely-parametrized surface. Use market knowledge to impose reasonable functional forms (“subjective judgment about objective features”)

� We employ parametric surfaces of form:

� Discretize for fully non-parametric surface

� Can impose smoothing or linking on nonparametric surface

For further details see Blyth (2004)

�1 + exp ( - �2 � ) ( �0 - �1 - �3 �)

� : forward, calendar or relative time

9

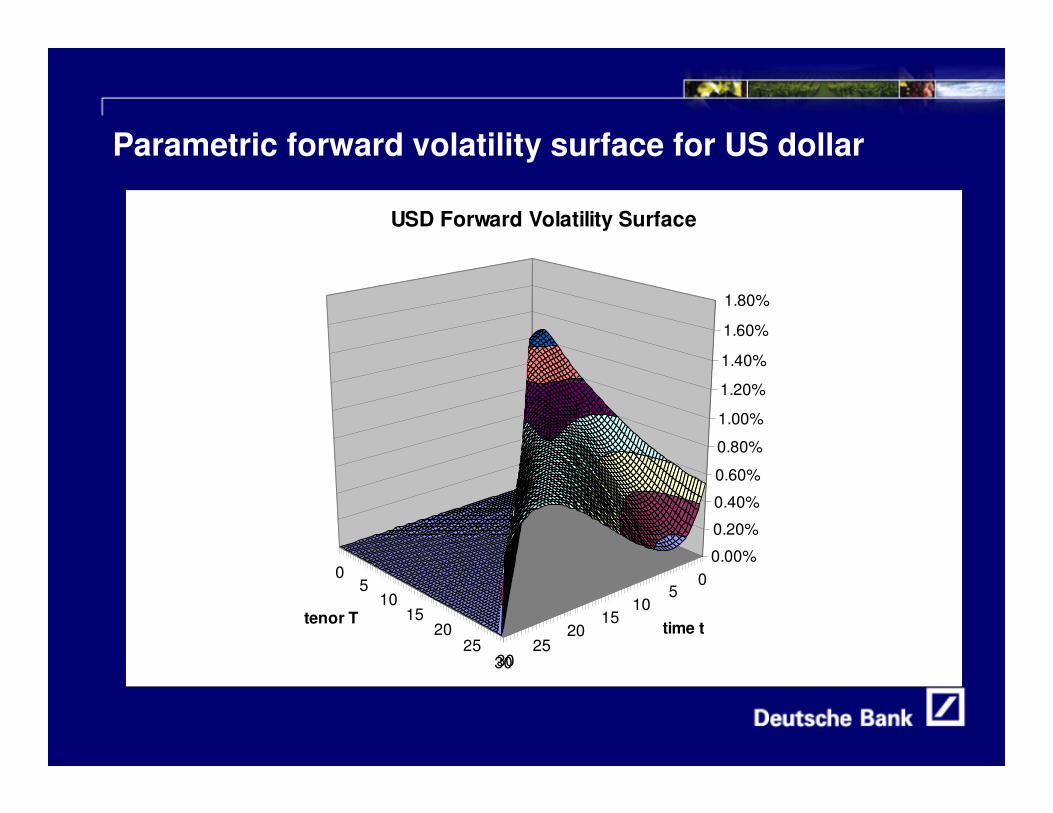

Parametric forward volatility surface for US dollar

05

1015

2025

30

05

1015

2025

30

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

1.60%

1.80%

time ttenor T

USD Forward Volatility Surface

10

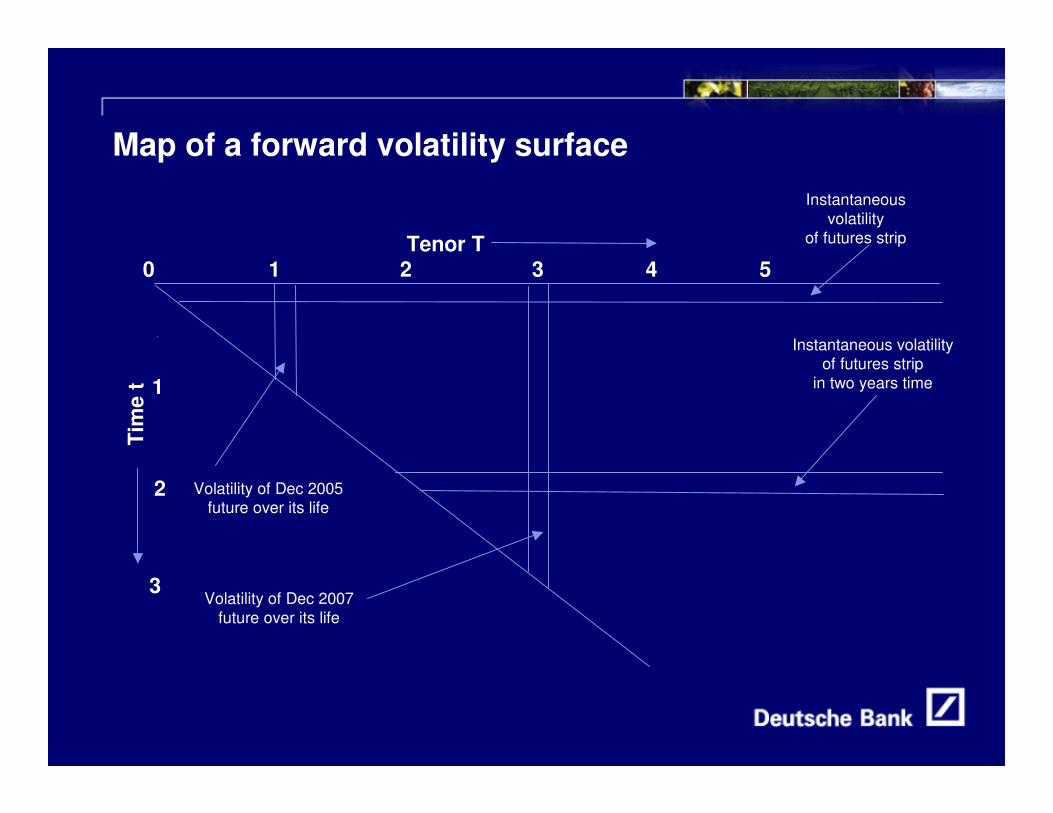

Map of a forward volatility surface

0 1 2 3 4 5Tenor T

1

2

3

Instantaneous volatility

of futures strip

Instantaneous volatilityof futures strip

in two years time

Volatility of Dec 2005future over its life

Volatility of Dec 2007 future over its life

Tim

e t

11

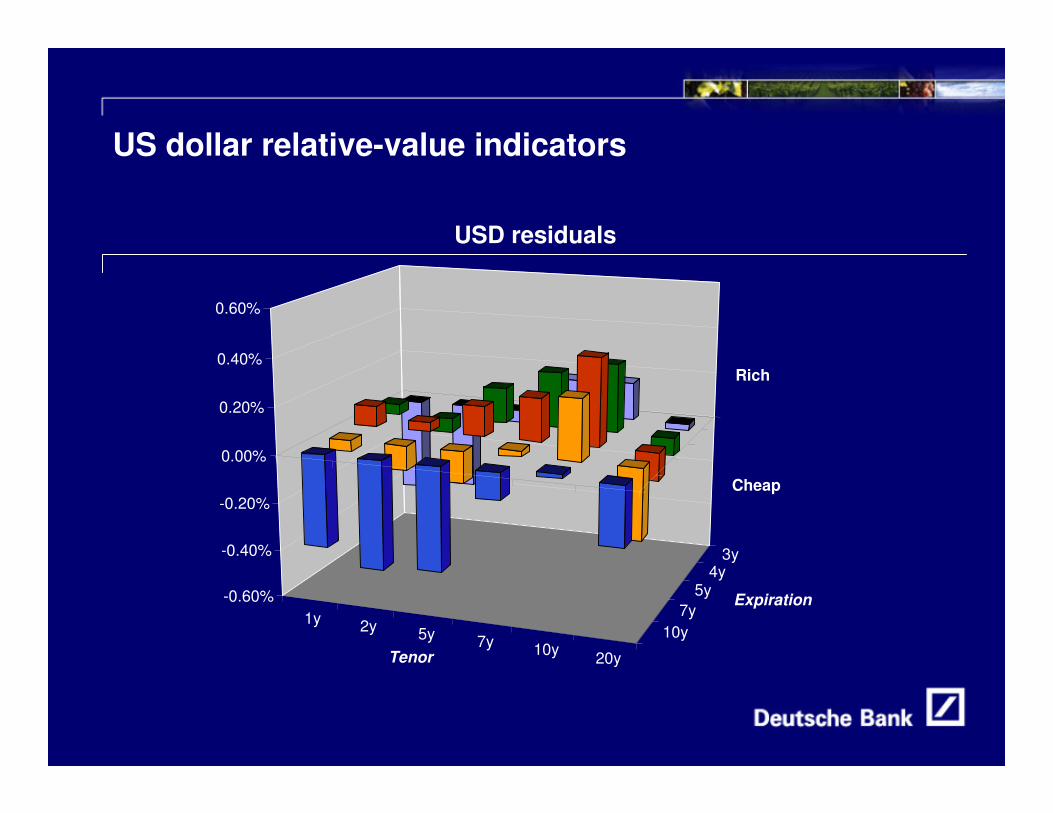

US dollar relative-value indicators

1y 2y 5y 7y 10y 20y

3y4y

5y7y

10y

-0.60%

-0.40%

-0.20%

0.00%

0.20%

0.40%

0.60%

Tenor

Expiration

Rich

Cheap

USD residuals

12

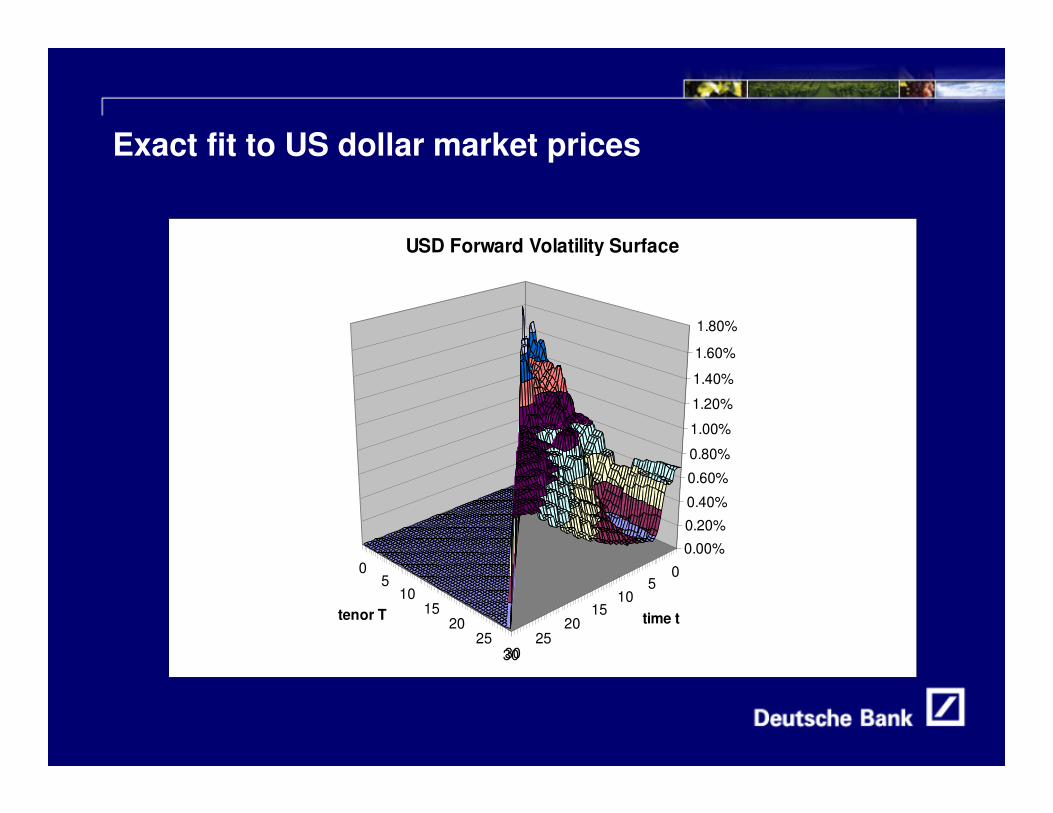

Exact fit to US dollar market prices

05

1015

2025

30

05

1015

2025

30

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

1.60%

1.80%

time ttenor T

USD Forward Volatility Surface

13

Using forward volatility surfaces in practice

� Implement both parametric smooth surface and exact-fit surface

� Trading decisions informed by:

– Residuals between market and smooth-fit prices

– Shape of exact-fit forward volatility surface

� Hedge trades under consistent dynamic

� Hold to maturity or close out strategies when volatility levels revert to fair value. Holding periods can vary from days to years

� Approach predicated on power of consistent dynamic to offset inevitable modelling shortcomings

14

Further examples 1. Hedge 10yr CMS liabilities with 5yr-tailed swaptions

� 10yr-tailed swaptions are rich due to hedging of 10yr CMS product

� Portfolio of 5yr-tail options with spectrum of expirations captures similar volatility, but at cheaper levels

– 10yr-5yr and 15yr-5yr payers are better value than 10yr-10yr payer

15

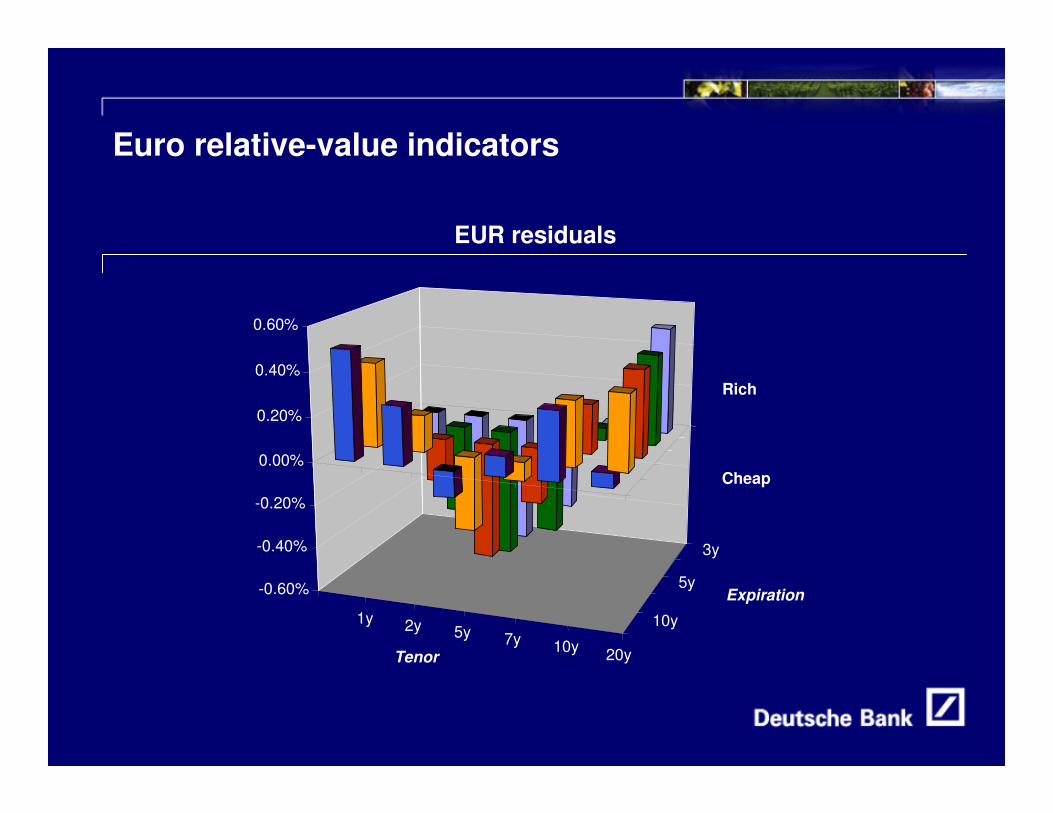

Euro relative-value indicators

EUR residuals

-0.60%

-0.40%

-0.20%

0.00%

0.20%

0.40%

0.60%

1y 2y 5y 7y 10y 20yTenor

3y

5y

10y

Expiration

Cheap

Rich

16

2. Caps versus swaptions, 1998-9

� Unwind of proprietary desks’ short positions in caps versus longpositions in swaptions widened volatility spread between products

� In forward volatility space, this resulted in large spikes in forward volatility of the front contracts

� Volatility dynamic implied by these prices absurd

17

Euro forward volatility surface, Aug 98-June 99:The approach of the storm

0.00

2.00

4.00

6.00

8.00

10.0

0

0.00

2.00

4.00

6.00

8.00

10.00

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

time

tenor

June 1999

0.00

2.00

4.00

6.00

8.00

10.0

0

0.00

2.00

4.00

6.00

8.00

10.00

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

time

tenor

August 1998

18

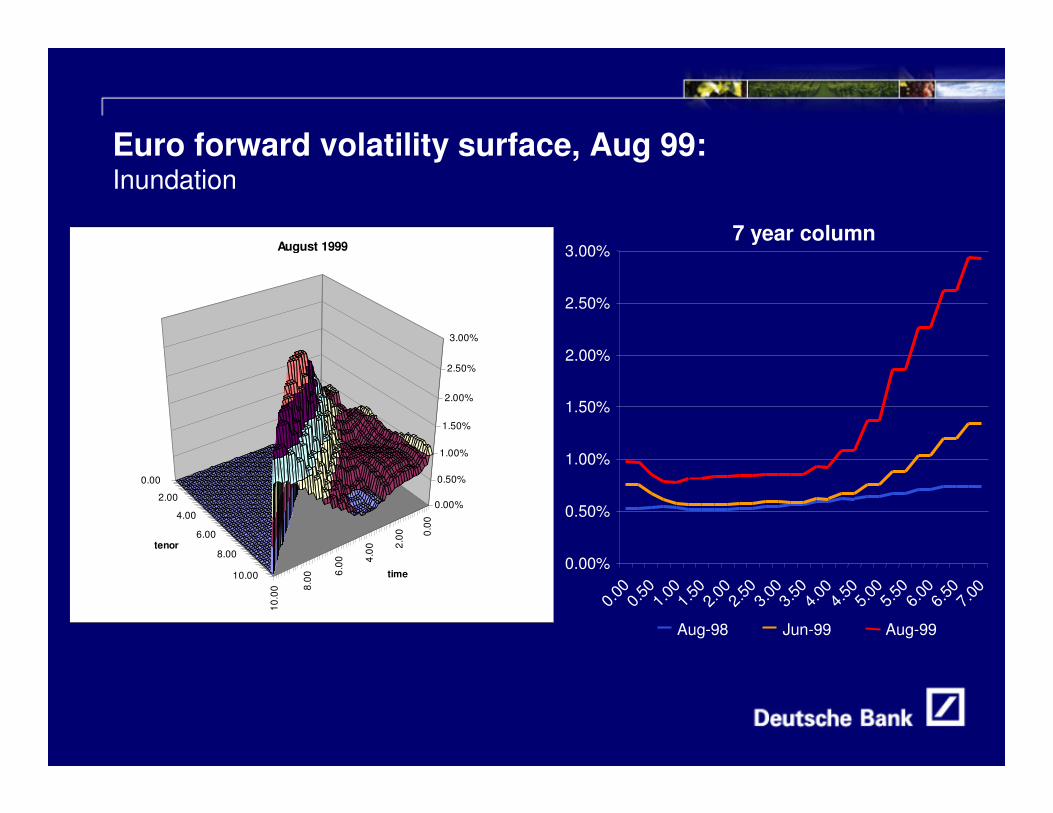

Euro forward volatility surface, Aug 99:Inundation

0.00

2.00

4.00

6.00

8.00

10.0

0

0.00

2.00

4.00

6.00

8.00

10.00

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

time

tenor

August 1999

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

5.50

6.00

6.50

7.00

Aug-98 Jun-99 Aug-99

7 year column

19

3. Euro swaption relative value: comparing indicators

� Consistent modelling framework can identify better trading strategies to simpler historical implied analysis - although often indicators concur.

� Consider performance of relative-value trades in euro swaption market.

20

Euro swaption relative value (cont’d)

Relative Value Indicators

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

Jan-02 Jul-02 Jan-03 Jul-03 Jan-04 Jul-04

Perc

enta

ge R

ich/

Che

ap

Buy 2y5ySell 2y20y

Buy 1y5ySell 1y20y

21

Euro swaption relative value (cont’d)

Ratio of Implied Normalised Volatilities

1.05

1.10

1.15

1.20

1.25

1.30

1.35

1.40

Jan-02 Jul-02 Jan-03 Jul-03 Jan-04 Jul-04

2y-5y/2y-20y

1y-5y/1y-10y

22

Additional dimensions

� Skew Modelling: demand consistency between pricing of skew and

dynamics of implied volatility under market movements

� Term Structure of Skew: skew structure for short-term rates coupled

with specified dynamics may not be consistent with certain skew

structure for longer-dated rates

� Stochastic Volatility: demand consistency between stochastic

volatility overlays used to price option smile and prices of compound

options

Practical Relative-Value Volatility Trading

Stephen Blyth,

Managing Director, Head of European Arbitrage Trading

21 January 2005