w e l c o m e t o t h e f r a n c e t e l e c o m i n v e s t o r d a y

TRANSCRIPT

W e l c o m e t o t h W e l c o m e t o t h ee

F r a n c e T e l e c o F r a n c e T e l e c o m m

I n v e s t o r D a yI n v e s t o r D a y

W e l c o m e t o t h W e l c o m e t o t h ee

F r a n c e T e l e c o F r a n c e T e l e c o m m

I n v e s t o r D a yI n v e s t o r D a y

I n v e s t o r D a y

I n v e s t o r D a y

Innovation and GrowthInnovation and Growth

N o v e m b e r 1 2 t h , 2 0 0 3N o v e m b e r 1 2 t h , 2 0 0 3

Objectives of the Day Objectives of the Day

Explain France Telecom view of innovation and

partnerships as growth and cost efficiency drivers

Explain why and how France Telecom growth initiatives

will support our growth targets

Demonstrate ExCom members involvement in these

projects

Update on business trends for 2004 and 2005

Confirm guidance on upper range of 3 - 5% revenue growth

for 2003 - 2005

Confirm guidance on upper range of 3 - 5% revenue growth

for 2003 - 2005

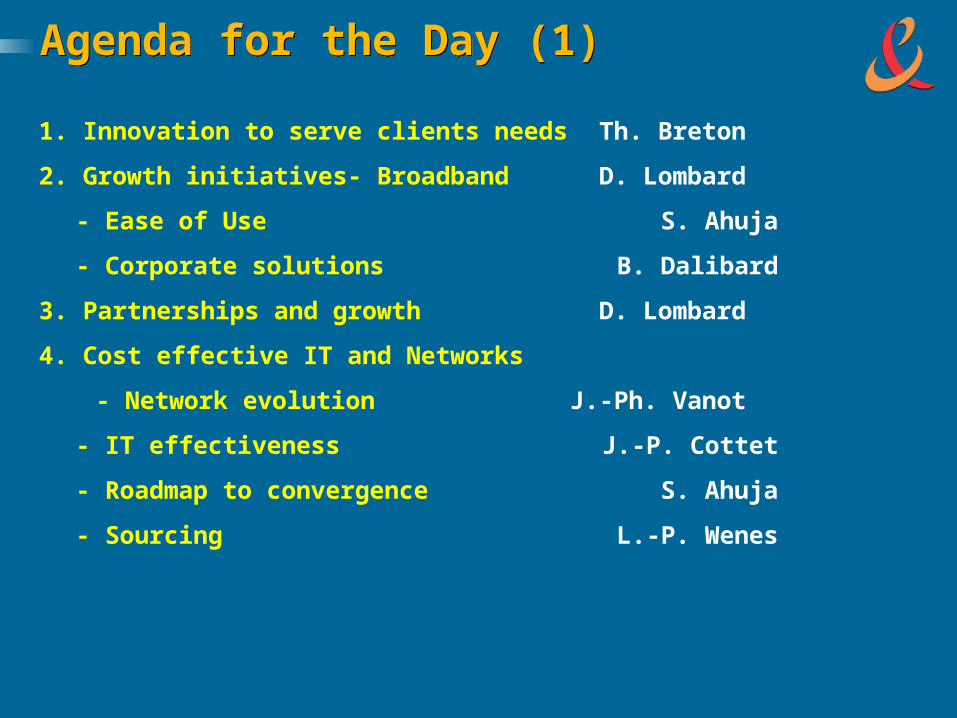

Agenda for the Day (1)Agenda for the Day (1)

1. Innovation to serve clients needs Th. Breton

2. Growth initiatives- Broadband D. Lombard

- Ease of Use S. Ahuja

- Corporate solutions B. Dalibard

3. Partnerships and growth D. Lombard

4. Cost effective IT and Networks

- Network evolution J.-Ph. Vanot

- IT effectiveness J.-P. Cottet

- Roadmap to convergence S. Ahuja

- Sourcing L.-P. Wenes

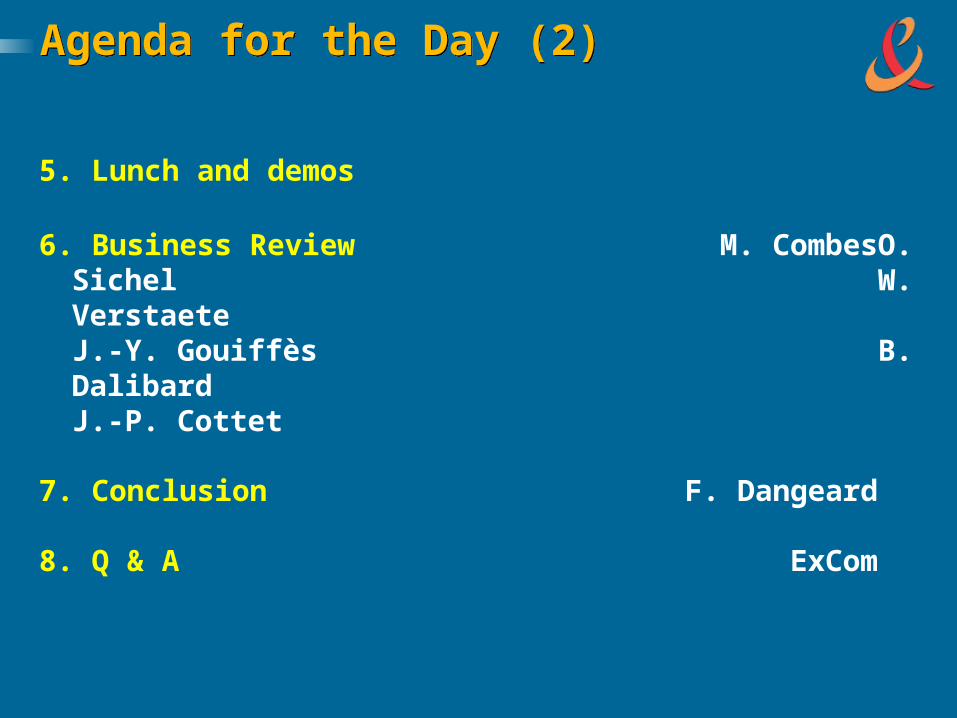

Agenda for the Day (2)Agenda for the Day (2)

5. Lunch and demos

6. Business Review M. CombesO. Sichel

W. VerstaeteJ.-Y. Gouiffès

B. DalibardJ.-P. Cottet

7. Conclusion F. Dangeard

8. Q & A ExCom

Building Momentum for

Growth

Building Momentum for

GrowthThierry Breton

Chairman and CEO

CAUTIONARY STATEMENT CAUTIONARY STATEMENT

This presentation contains forward-looking statements about France Telecom. Such statements are not historical facts and include expressions of management’s expectations about new and existing programs, opportunities, technology and market conditions. Although France Telecom believes its expectations are based on reasonable assumptions, these forward-looking statements are subject to numerous risks and uncertainties. These statements should not be regarded as a representation that anticipated events will occur or that expected objectives will be achieved. Important factors that could cause actual results or performance to differ materially from the results anticipated in the forward-looking statements include, among other things, the success of the announced FT 2005 plan, including the “15 + 15 + 15” plan and the TOP program, changes in economic, business and competitive markets, technological trends, France Telecom’s other strategic, financial and operating initiatives, risks and uncertainties attendant upon international operations, exchange rate fluctuations and market regulatory factors. More detailed information on the potential factors that could affect the financial results of France Telecom is contained in the Document de référence submitted to the COB on March 21, 2003 and in its Form 20-F filed with the U.S. Securities and Exchange Commission. The forward-looking statements contained in this document speak only as of the date of this presentation and France Telecom does not undertake to update any forward-looking statement to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

This presentation contains forward-looking statements about France Telecom. Such statements are not historical facts and include expressions of management’s expectations about new and existing programs, opportunities, technology and market conditions. Although France Telecom believes its expectations are based on reasonable assumptions, these forward-looking statements are subject to numerous risks and uncertainties. These statements should not be regarded as a representation that anticipated events will occur or that expected objectives will be achieved. Important factors that could cause actual results or performance to differ materially from the results anticipated in the forward-looking statements include, among other things, the success of the announced FT 2005 plan, including the “15 + 15 + 15” plan and the TOP program, changes in economic, business and competitive markets, technological trends, France Telecom’s other strategic, financial and operating initiatives, risks and uncertainties attendant upon international operations, exchange rate fluctuations and market regulatory factors. More detailed information on the potential factors that could affect the financial results of France Telecom is contained in the Document de référence submitted to the COB on March 21, 2003 and in its Form 20-F filed with the U.S. Securities and Exchange Commission. The forward-looking statements contained in this document speak only as of the date of this presentation and France Telecom does not undertake to update any forward-looking statement to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

Delivering on our commitments

Anticipating Industry structural changes

Building momentum for Growth

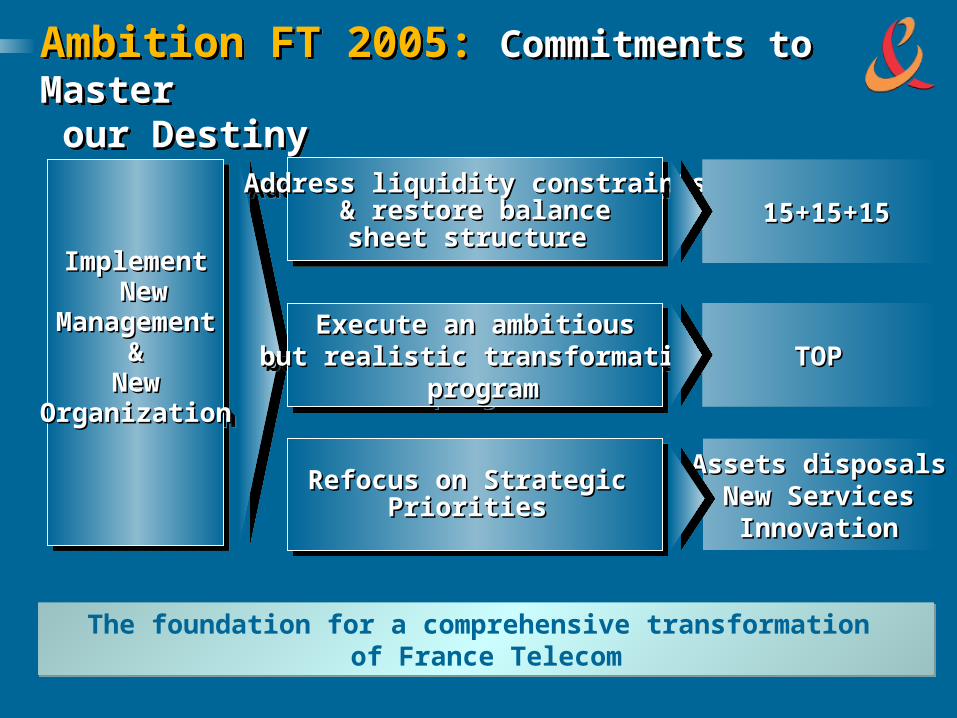

Ambition FT 2005: Commitments to Master our Destiny

Ambition FT 2005: Commitments to Master our Destiny

The foundation for a comprehensive transformation of France Telecom

The foundation for a comprehensive transformation of France Telecom

ImplementImplement New New

ManagementManagement&&

NewNewOrganizationOrganization

ImplementImplement New New

ManagementManagement&&

NewNewOrganizationOrganization

Address liquidity constraintsAddress liquidity constraints & restore balance & restore balance

sheet structure sheet structure

Address liquidity constraintsAddress liquidity constraints & restore balance & restore balance

sheet structure sheet structure

Execute an ambitiousExecute an ambitious but realistic transformation but realistic transformation

program program

Execute an ambitiousExecute an ambitious but realistic transformation but realistic transformation

program program

Refocus on Strategic Refocus on Strategic Priorities Priorities

Refocus on Strategic Refocus on Strategic Priorities Priorities

15+15+1515+15+15

TOPTOP

Assets disposalsAssets disposalsNew ServicesNew Services

InnovationInnovation

New management principlesNew management principles New management & new incentive schemes

– Renewal of the Executive committee– Assessment of the Executive committee members every 6 months

– 6 months objectives and assessment at all levels– Key executives talent review– 700 entrepreneurs network

Tightened operational integration:– Strong integration of Operations and Corporate Functions– SEVP in charge of FT 2005 coordination– New Internal governance bodies– Group level planning procedures for R&D, network and IT– Full integration of sourcing

Project based transformation approach – 100 TOP programs– 40 division-led growth projects– 14 transversal growth projects

Adapt permanently skills, talents and responsibilities according to performance and objectives

Adapt permanently skills, talents and responsibilities according to performance and objectives

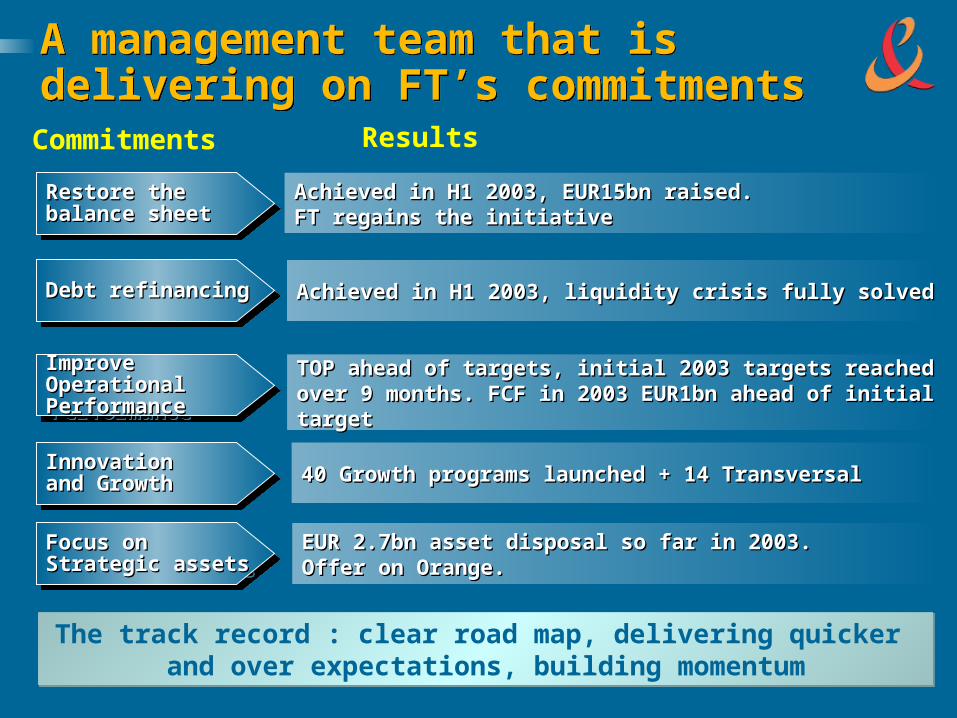

A management team that is delivering on FT’s commitmentsA management team that is delivering on FT’s commitments

TOP ahead of targets, initial 2003 targets reachedTOP ahead of targets, initial 2003 targets reachedover 9 months. FCF in 2003 EUR1bn ahead of initialover 9 months. FCF in 2003 EUR1bn ahead of initialtarget target

Improve Improve OperationalOperationalPerformancePerformance

Improve Improve OperationalOperationalPerformancePerformance

Achieved in H1 2003, liquidity crisis fully solvedAchieved in H1 2003, liquidity crisis fully solved

Debt refinancingDebt refinancingDebt refinancingDebt refinancing

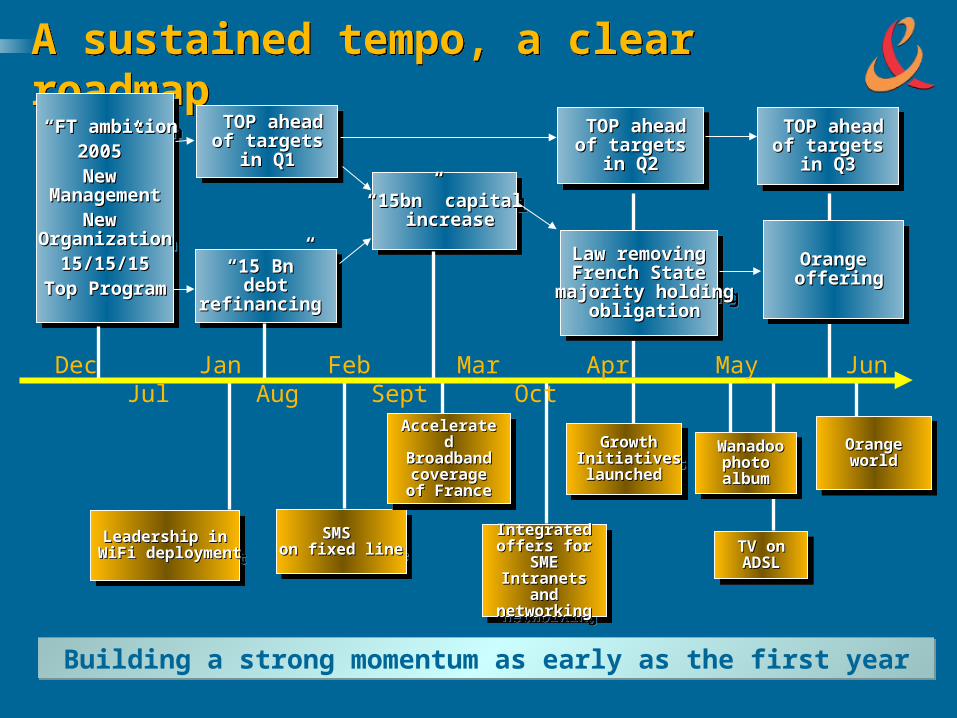

The track record : clear road map, delivering quicker and over expectations, building momentum

The track record : clear road map, delivering quicker and over expectations, building momentum

Achieved in H1 2003, EUR15bn raised.Achieved in H1 2003, EUR15bn raised.FT regains the initiativeFT regains the initiative

Restore theRestore thebalance sheetbalance sheetRestore theRestore thebalance sheetbalance sheet

EUR 2.7bn asset disposal so far in 2003.EUR 2.7bn asset disposal so far in 2003.Offer on Orange.Offer on Orange.

Focus onFocus onStrategic assetsStrategic assetsFocus onFocus onStrategic assetsStrategic assets

Commitments Results

40 Growth programs launched + 14 Transversal40 Growth programs launched + 14 Transversal

Innovation Innovation and Growthand GrowthInnovation Innovation and Growthand Growth

A sustained tempo, a clear roadmapA sustained tempo, a clear roadmap

Building a strong momentum as early as the first yearBuilding a strong momentum as early as the first year

““15 Bn”15 Bn”debtdebt

refinancing refinancing

““15 Bn”15 Bn”debtdebt

refinancing refinancing

““15bn” capital15bn” capital increaseincrease

““15bn” capital15bn” capital increaseincrease

TOP aheadTOP aheadof targetsof targets

in Q1in Q1

TOP aheadTOP aheadof targetsof targets

in Q1in Q1

TOP aheadTOP aheadof targetsof targets

in Q2in Q2

TOP aheadTOP aheadof targetsof targets

in Q2in Q2

“ “FT ambitionFT ambition2005”2005”New New

ManagementManagementNew New

OrganizationOrganization15/15/1515/15/15

Top ProgramTop Program

“ “FT ambitionFT ambition2005”2005”New New

ManagementManagementNew New

OrganizationOrganization15/15/1515/15/15

Top ProgramTop Program

TOP aheadTOP aheadof targetsof targets

in Q3in Q3

TOP aheadTOP aheadof targetsof targets

in Q3in Q3

Leadership inLeadership in WiFi deployment WiFi deploymentLeadership inLeadership in

WiFi deployment WiFi deploymentSMS SMS

on fixed lineon fixed lineSMS SMS

on fixed lineon fixed line

GrowthGrowth Initiatives Initiativeslaunchedlaunched

GrowthGrowth Initiatives Initiativeslaunchedlaunched

TV on TV on ADSLADSL

TV on TV on ADSLADSL

Integrated Integrated offers for offers for

SME SME Intranets and Intranets and networkingnetworking

Integrated Integrated offers for offers for

SME SME Intranets and Intranets and networkingnetworking

Law removingLaw removingFrench StateFrench State

majority holding majority holding obligation obligation

Law removingLaw removingFrench StateFrench State

majority holding majority holding obligation obligation

OrangeOrange offering offeringOrangeOrange offering offering

Orange Orange worldworld

Orange Orange worldworld

Accelerated Accelerated Broadband Broadband coverage of coverage of

FranceFrance

Accelerated Accelerated Broadband Broadband coverage of coverage of

FranceFrance

Wanadoo Wanadoo photo photo albumalbum

Wanadoo Wanadoo photo photo albumalbum

Dec Jan Feb Mar Apr May Jun Jul Aug Sept Oct

Delivering on our commitments

Anticipating Industry structural changes

Building momentum for Growth

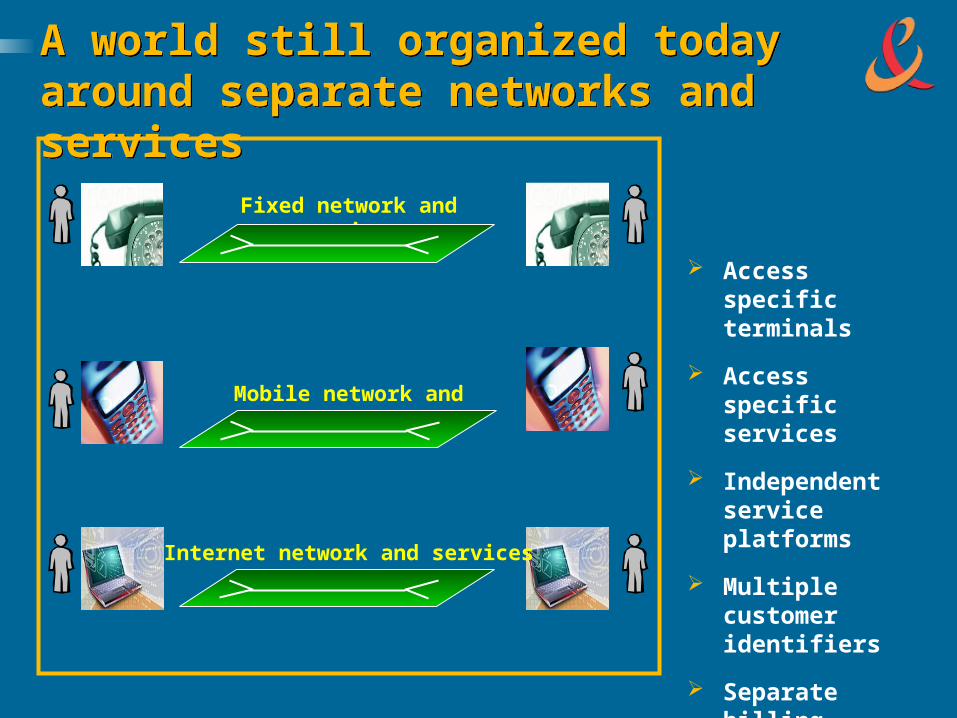

A world still organized today around separate networks and services

A world still organized today around separate networks and services

Mobile network and services

Internet network and services

Fixed network and services

Access specific terminals

Access specific services

Independent service platforms

Multiple customer identifiers

Separate billing

The most important paradigm

change the industry

has ever seen

The most important paradigm

change the industry

has ever seen

In our vision the user is the center of his communications universeIn our vision the user is the center of his communications universe

The customer defines and personalizes his services

Services become multi-access

Focal point is shifting from the network to the user

The customer is at the center of the network

Communication

Information/entertainment

Transactions

EXPLOSION OF USAGES: WHAT YOU WANT,

WHERE YOU WANT, WHEN YOU WANT

EXPLOSION OF USAGES: WHAT YOU WANT,

WHERE YOU WANT, WHEN YOU WANT

Five major technology discontinuities will enable this revolution

Five major technology discontinuities will enable this revolution

Broadband everywhereBroadband everywhere

Delayered Delayered and open and open networknetworkand IT platformsand IT platforms

IP networkIP network1

2

Multi-access Multi-access innovative devicesinnovative devices

45

Ubiquitous wirelessUbiquitous wireless3

Service platforms

2

•Physical networks / •transport

•Physical networks / •transport

1

Transaction

systems

3

IP Networks: The cornerstone of a delayered infrastructureIP Networks: The cornerstone of a delayered infrastructure

1

A revolution similar to the IT

revolution

A revolution similar to the IT

revolution

2G

TPS

Third parties

Data con-vergence applica-tions

Soft-switch(voice)

Content

IP gateway

3G

WIFI

Mobile

2G/2.5G

Backbonemobile

Network database (e.g.,HLR)

Fixed line (voice)

Switching PSTN

IN

Data

DSL

FR/X25/ATMLeased line

Edge router

ISP Platform

FR/X25/ATM

Subscriber switching

Back-boneIP

IN

IP access DSL FTTH Cable

IP backbone

Device Open network Services

Home Broadband: The connection for future multi-service delivery

Home Broadband: The connection for future multi-service deliveryHome services

Home gatewayHome

gatewayBroadband access

TV

Voice over IP

Interactive gaming

Internet

Visual phone

@

New bandwidth- enabled services

Access throughput continuously increasing

Devices capability upgrade and interoperability

Wireless home networkSecurity

Surveillance

2

cv

Wireless

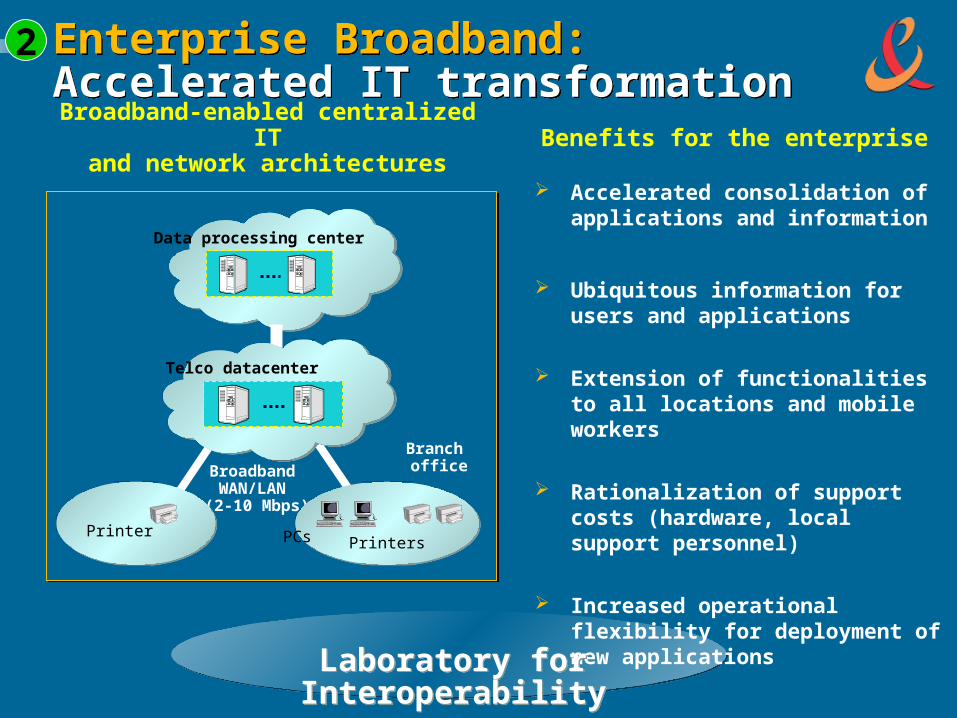

Broadband-enabled centralized ITand network architectures

Broadband WAN/LAN

(2-10 Mbps)

Data processing center

PrinterPrintersPCs

Branch office

Telco datacenter

Enterprise Broadband: Accelerated IT transformationEnterprise Broadband: Accelerated IT transformation

Benefits for the enterprise

Accelerated consolidation of applications and information

Ubiquitous information for users and applications

Extension of functionalities to all locations and mobile workers

Rationalization of support costs (hardware, local support personnel)

Increased operational flexibility for deployment of new applications

2

Laboratory for InteroperabilityLaboratory for Interoperability

Wireless: From mobility to ubiquitous accessibilityWireless: From mobility to ubiquitous accessibility

Personal services

Mobile Hotspots

Office

Ubiquitous accessibilityto personalized services

Access independent

Contact lists

Extended reachability

Unique authentication

3

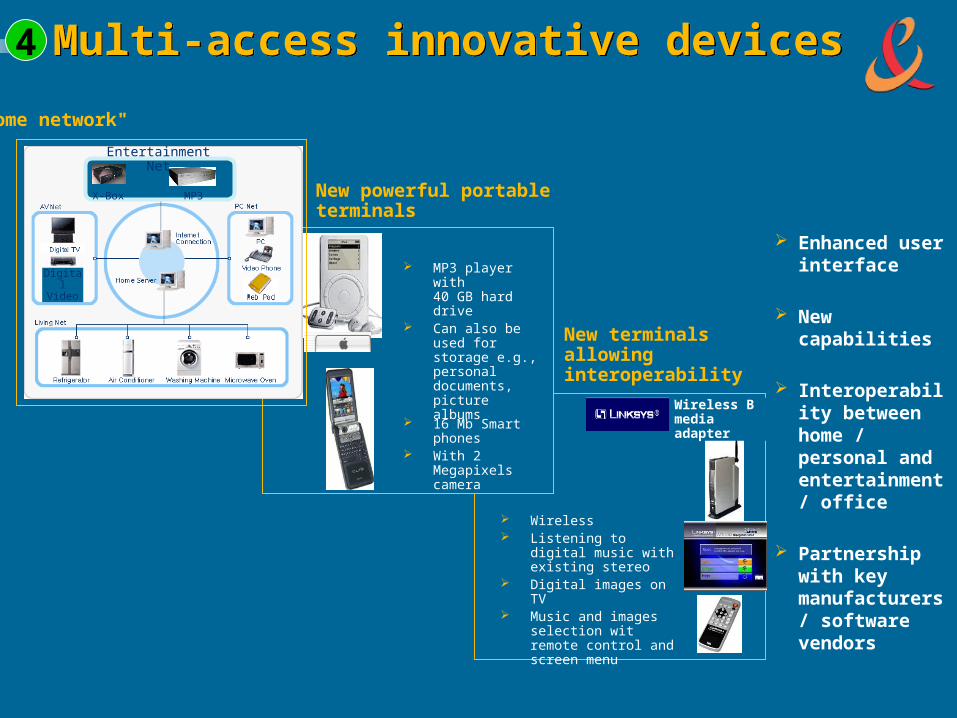

Multi-access innovative devices Multi-access innovative devices

New powerful portable terminals

MP3 player with 40 GB hard drive

Can also be used for storage e.g., personal documents, picture albums

16 Mb Smart phones

With 2 Megapixels camera

New terminals allowing interoperability

Wireless B media adapter

•<Digital Video

Entertainment Net

X-Box MP3

"Home network"

Wireless Listening to digital music

with existing stereo Digital images on TV Music and images

selection wit remote control and screen menu

Enhanced user interface

New capabilities

Interoperability between home / personal and entertainment / office

Partnershipwith key manufacturers / software vendors

4

Open systems enhancing interoperability of telecom services

Open systems enhancing interoperability of telecom services Services based on software platforms

connected to IP network

Standard APIs

Rapid service deployment

Network independent customer management

Innovative tariffs and products

Higher capillarity

Dynamic capacity managements

Lower operational costs

5

Transaction systems

Transaction systems

Transport network

Transport network

Service platformService platform

Customer identifierCustomer identifier

Reshaping France TelecomReshaping France Telecom

Close to local customer, Close to local customer, but leveraging global but leveraging global

platforms platforms

Close to local customer, Close to local customer, but leveraging global but leveraging global

platforms platforms

Access and voice narrowband

Access and voice mobile

Broadband and Internet services

Managed data services

From…

Home communication services

Personal communication services

Enterprise communication services

… To

Delivering on our commitments

Anticipating Industry structural changes

Building momentum for Growth

The engine of France Telecom transformationThe engine of France Telecom transformation

Network and IT infrastructure convergence

Strategic partnerships

World class customer management

Lean operations

High quality customer experience (QoS, Customer Care)

Home communications

Personal communications

Enterprise communications

Operational

excellence

Usage and

business

model

innovation

for growth

FT has a unique set of strengthsFT has a unique set of strengths

CustomersCustomers

SkillsSkills AssetsAssets

A committed management

team

Over 50 million Homes Over 50 million Personal Over 500K Enterprises

Fixed, mobile and internet networks

Strong brands Global IP network Presence in 220

countries

Strong R&D capabilities

Complex technology/system integration capabilities

Network deployment capabilities

Service quality culture

Experience in leveraging partnership

France Telecom masters technology and leverages it for services innovation

France Telecom masters technology and leverages it for services innovation

2G

TPS

Third parties

Datacon-vergence applica-tions

Soft-switch(voice)

Content

3G

WIFI

IP backbone

Tra

nsactio

n

pla

tform

s

Presence Reachability Payment Security

IP networks (IP-VPN, MPLS, QoS, …)

Gateways and home terminals

Handset middleware User-friendly interface

Identity and authentication

Contact list Instant messaging

High speed access

A structured growth program: Top LineA structured growth program: Top Line

40 Division-led growth projects

14 transversal growth projects to develop and launch new services

All projects under ExCom member leadership

Strong mobilization of the company

Quarterly review of program

Growth projectsGrowth projectsOrange

Improve customer mix Yield Management IN Services Key Non Voice Services Signature Devices 3G Rollout Business Services Transversal Projects Roaming Initiatives

Wanadoo

Increase value for Broadband in France

Increase our position on Broadband in Spain

Improve our positioning in the UK

Develop paid services Develop B-to-B mobile

interactive services Capitalize on directories

Wanadoo

Increase value for Broadband in France

Increase our position on Broadband in Spain

Improve our positioning in the UK

Develop paid services Develop B-to-B mobile

interactive services Capitalize on directories

Fixed Line, Voice and Data Services in France

Increase market coverage Boost sales of accessories Develop self care Revisit marketing mix of small

business Relaunch fixed handsets sales Maximize value of high

potential customers PBX - IPBX Broadband everywhere with

satellite and WiFi Increase Intranet revenues on

SMEs Fight competition on dense

MAN areas Close large outsourcing deals Develop CPE services Application Managed Services

Fixed Line, Voice and Data Services in France

Increase market coverage Boost sales of accessories Develop self care Revisit marketing mix of small

business Relaunch fixed handsets sales Maximize value of high

potential customers PBX - IPBX Broadband everywhere with

satellite and WiFi Increase Intranet revenues on

SMEs Fight competition on dense

MAN areas Close large outsourcing deals Develop CPE services Application Managed Services

International, Voice and Data Services

Equant indirect channel efficiency

TP Group : Accelerate fixed line penetration

TP Group : Accelerate data development

TP Group : develop mobile penetration

Strengthen Uni2 market position

ROW new initiatives International voice revenues

International, Voice and Data Services

Equant indirect channel efficiency

TP Group : Accelerate fixed line penetration

TP Group : Accelerate data development

TP Group : develop mobile penetration

Strengthen Uni2 market position

ROW new initiatives International voice revenues

Identity / Authentication Address Presence Reach Payments Office ADSL Multiservice

Identity / Authentication Address Presence Reach Payments Office ADSL Multiservice

Video-Telephony VOIP DRM Content synergies Control of Services Data mining, Segmentations

and market studies synergies Distribution synergies

Video-Telephony VOIP DRM Content synergies Control of Services Data mining, Segmentations

and market studies synergies Distribution synergies

TransversalTransversal

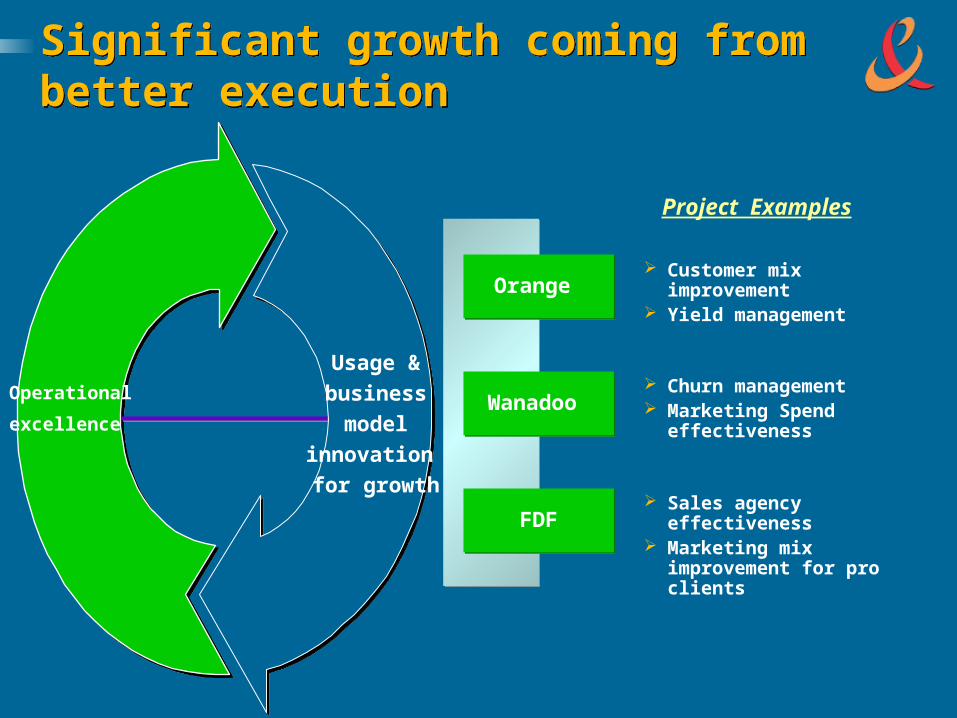

Significant growth coming from better executionSignificant growth coming from better execution

Orange Orange

Wanadoo Wanadoo

FDFFDF

Usage &

business

model

innovation

for growth

Customer mix improvement Yield management

Churn management Marketing Spend

effectiveness

Sales agency effectiveness Marketing mix improvement

for pro clients

Operational

excellence

Project Examples

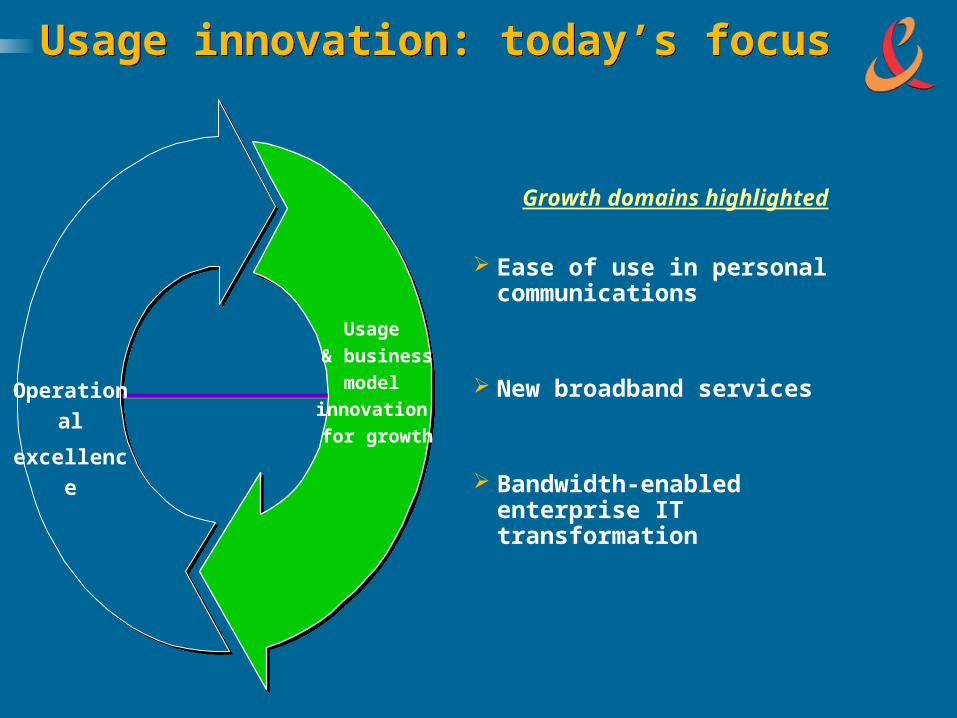

Usage innovation: today’s focusUsage innovation: today’s focus

Ease of use in personal communications

New broadband services

Bandwidth-enabled enterprise IT transformation

Usage

& business

model

innovation

for growth

Operational

excellence

Growth domains highlighted

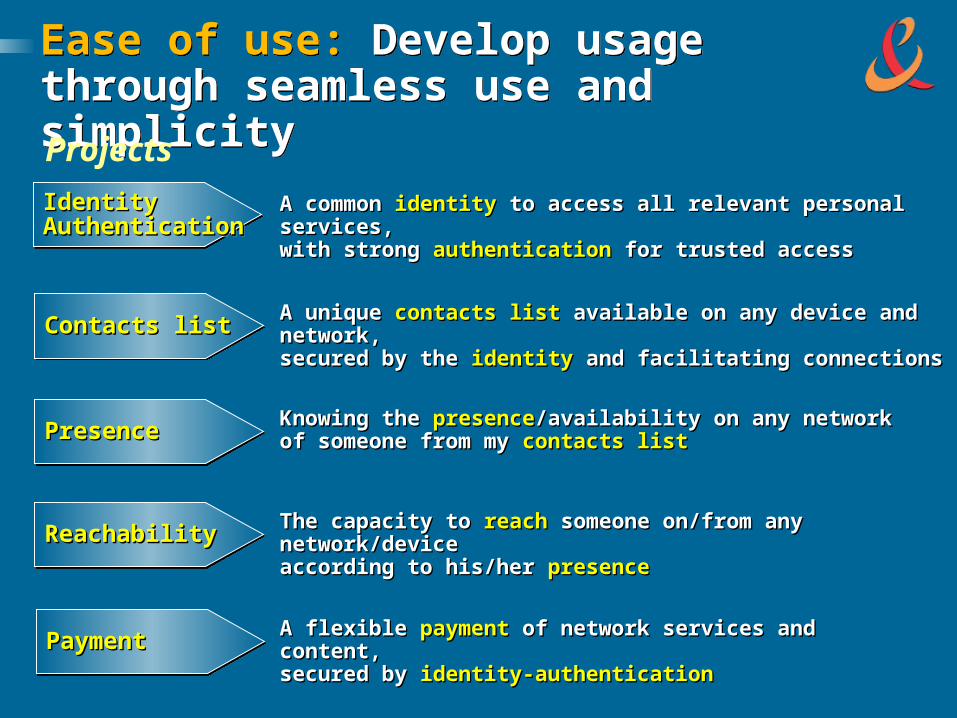

IdentityIdentityAuthenticationAuthenticationIdentityIdentityAuthenticationAuthentication

A commonA common identity identity to access all relevant personal services, to access all relevant personal services, with strongwith strong authentication authentication for trusted accessfor trusted access

Contacts listContacts listContacts listContacts list A uniqueA unique contacts list contacts list available on any device and network,available on any device and network,secured by thesecured by the identity identity and facilitating connectionsand facilitating connections

PresencePresencePresencePresence Knowing theKnowing the presence presence/availability on any network/availability on any networkof someone from myof someone from my contacts list contacts list

PaymentPaymentPaymentPayment A flexibleA flexible payment payment of network services and content,of network services and content,secured bysecured by identity-authentication identity-authentication

The capacity toThe capacity to reach reach someone on/from any network/devicesomeone on/from any network/deviceaccording to his/heraccording to his/her presence presenceReachabilityReachabilityReachabilityReachability

Ease of use: Develop usage through seamless use and simplicityEase of use: Develop usage through seamless use and simplicityProjects

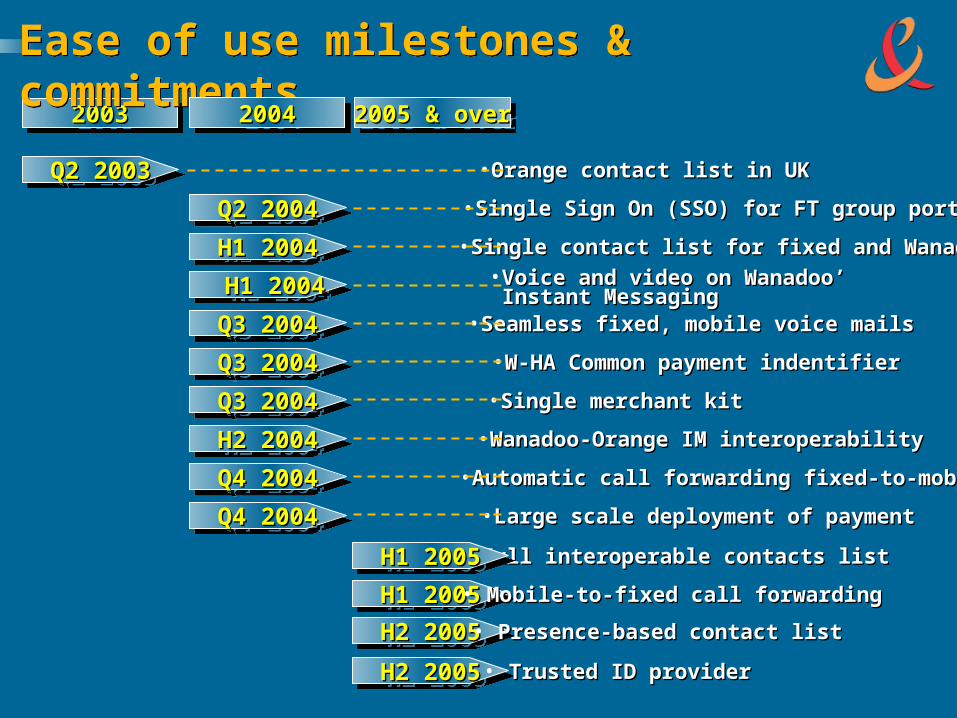

2003200320032003

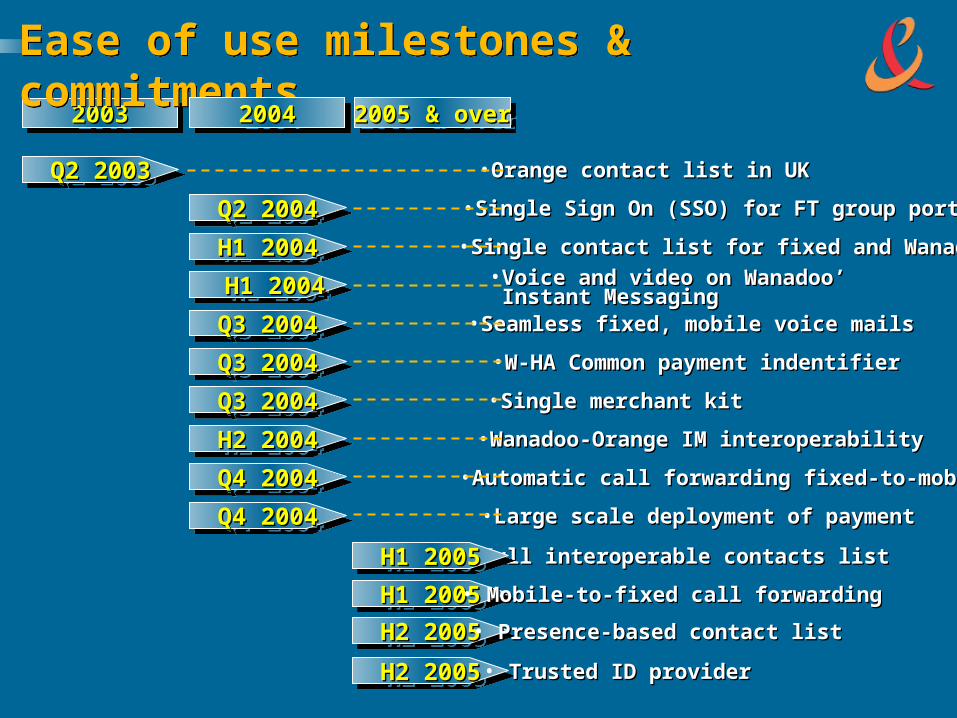

Ease of use milestones & commitmentsEase of use milestones & commitments

2004200420042004 2005 & over2005 & over2005 & over2005 & over

Q2 2003Q2 2003Q2 2003Q2 2003

H1 2004H1 2004H1 2004H1 2004

H1 2004H1 2004 H1 2004H1 2004

H2 2004H2 2004H2 2004H2 2004

H2 2005H2 2005H2 2005H2 2005

Q3 2004Q3 2004Q3 2004Q3 2004

• Single Sign On (SSO) for FT group portalsSingle Sign On (SSO) for FT group portals

• W-HA Common payment indentifierW-HA Common payment indentifier

• Orange contact list in UKOrange contact list in UK

• Single contact list for fixed and WanadooSingle contact list for fixed and Wanadoo• Voice and video on Wanadoo’Voice and video on Wanadoo’

Instant MessagingInstant Messaging

• Full interoperable contacts listFull interoperable contacts list

• Wanadoo-Orange IM interoperabilityWanadoo-Orange IM interoperability

• Presence-based contact list Presence-based contact list

• Seamless fixed, mobile voice mails Seamless fixed, mobile voice mails

• Automatic call forwarding fixed-to-mobileAutomatic call forwarding fixed-to-mobile

Q2 2004Q2 2004Q2 2004Q2 2004

Q3 2004Q3 2004Q3 2004Q3 2004

H1 2005H1 2005H1 2005H1 2005

H1 2005H1 2005H1 2005H1 2005 • Mobile-to-fixed call forwardingMobile-to-fixed call forwarding

• Single merchant kitSingle merchant kit

• Large scale deployment of paymentLarge scale deployment of payment

Q3 2004Q3 2004Q3 2004Q3 2004

Q4 2004Q4 2004Q4 2004Q4 2004

H2 2005H2 2005H2 2005H2 2005 • Trusted ID providerTrusted ID provider

Q4 2004Q4 2004Q4 2004Q4 2004

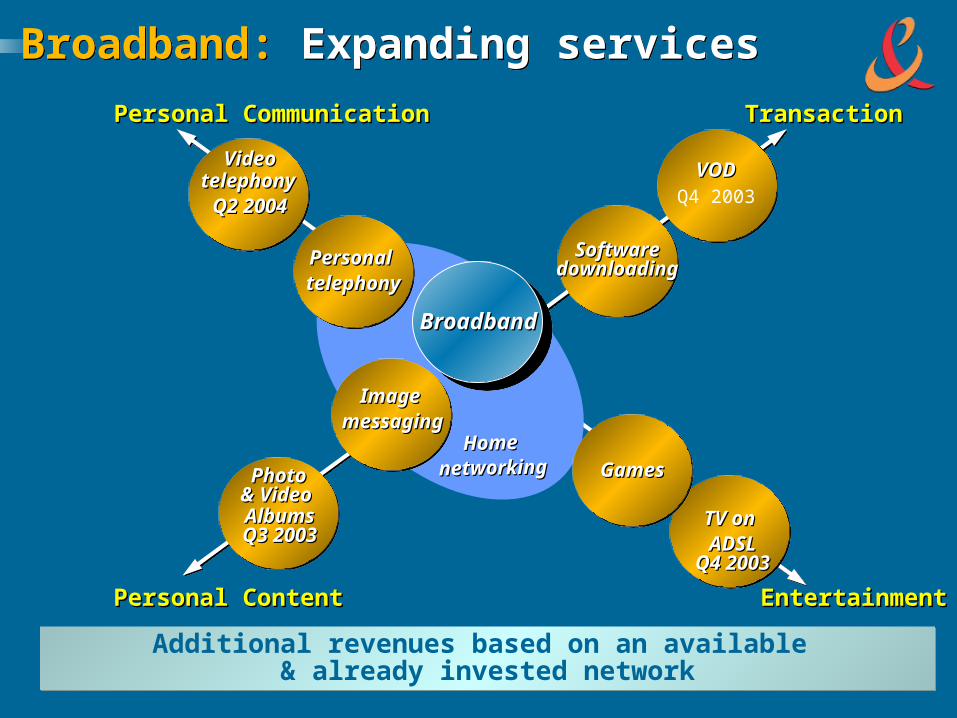

Additional revenues based on an available & already invested network

Additional revenues based on an available & already invested network

Personal CommunicationPersonal Communication TransactionTransaction

EntertainmentEntertainmentPersonal ContentPersonal Content

BroadbandBroadband

Personal Personal telephonytelephony

SoftwareSoftwaredownloadingdownloading

VODVODQ4 2003

TV onTV onADSLADSL

Q4 2003Q4 2003

GamesGames

Image Image messagingmessaging

Photo Photo & Video & Video AlbumsAlbumsQ3 2003Q3 2003

Home Home networkingnetworking

VideoVideotelephonytelephonyQ2 2004Q2 2004

Broadband: Expanding servicesBroadband: Expanding services

2003200320032003

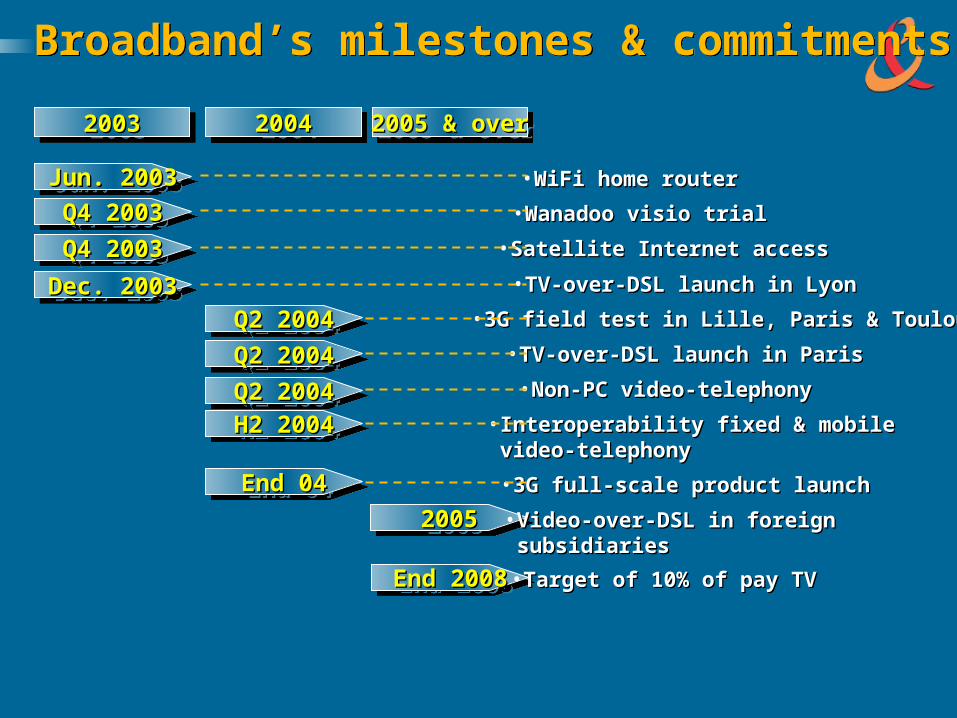

Broadband’s milestones & commitmentsBroadband’s milestones & commitments

2004200420042004 2005 & over2005 & over2005 & over2005 & over

Q4 2003Q4 2003Q4 2003Q4 2003

Dec. 2003Dec. 2003Dec. 2003Dec. 2003

Q2 2004Q2 2004Q2 2004Q2 2004

Q2 2004Q2 2004Q2 2004Q2 2004

H2 2004H2 2004H2 2004H2 2004Q2 2004Q2 2004Q2 2004Q2 2004

End 04End 04End 04End 04

2005200520052005

End 2008End 2008End 2008End 2008

• Satellite Internet accessSatellite Internet access

• TV-over-DSL launch in LyonTV-over-DSL launch in Lyon

• 3G field test in Lille, Paris & Toulouse3G field test in Lille, Paris & Toulouse

• TV-over-DSL launch in ParisTV-over-DSL launch in Paris

• Interoperability fixed & mobile Interoperability fixed & mobile video-telephonyvideo-telephony

• Non-PC video-telephonyNon-PC video-telephony

• 3G full-scale product launch3G full-scale product launch

• Video-over-DSL in foreign Video-over-DSL in foreign subsidiaries subsidiaries

• Target of 10% of pay TVTarget of 10% of pay TV

Q4 2003Q4 2003Q4 2003Q4 2003 • Wanadoo visio trialWanadoo visio trialJun. 2003Jun. 2003Jun. 2003Jun. 2003 • WiFi home routerWiFi home router

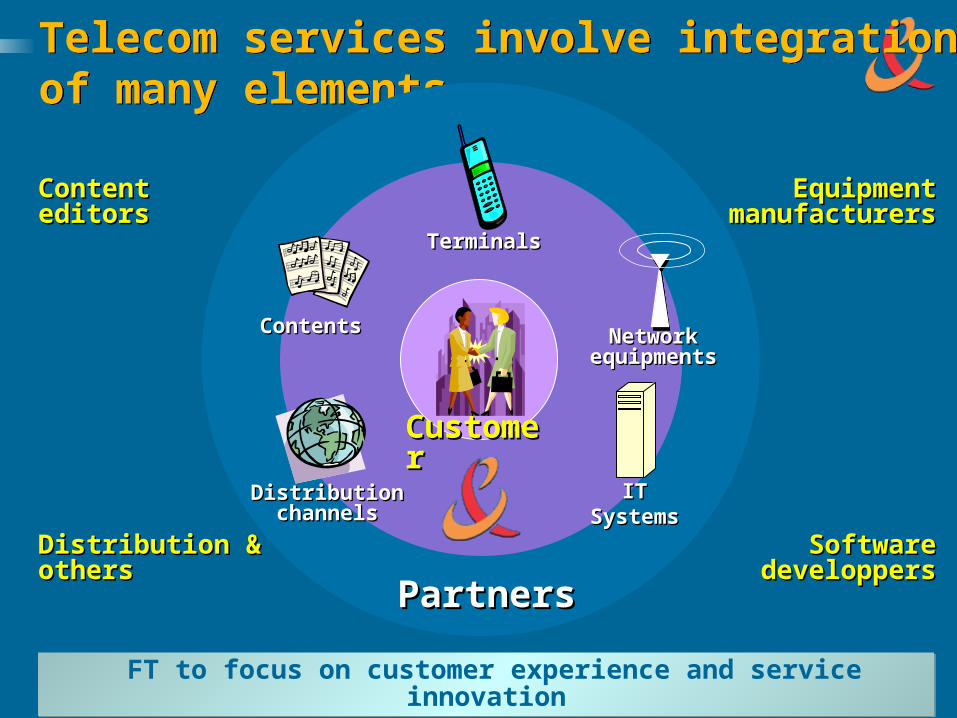

Corporate solutions: enhancing enterprise performance through bandwidth enabled IT-transformation

Corporate solutions: enhancing enterprise performance through bandwidth enabled IT-transformation

Offer employees on the move access to their work environment whatever their devices and networks, and wherever they are

Mobile workersMobile workers

Customer premises equipment

Customer premises equipment

OutsourcingOutsourcing

End-to-end management of customer communications needs including PBX, LAN/WAN integration and communications-based applications (messaging & security)

Integrated management of networks, IT infrastructure and services

Project Examples

2003200320032003

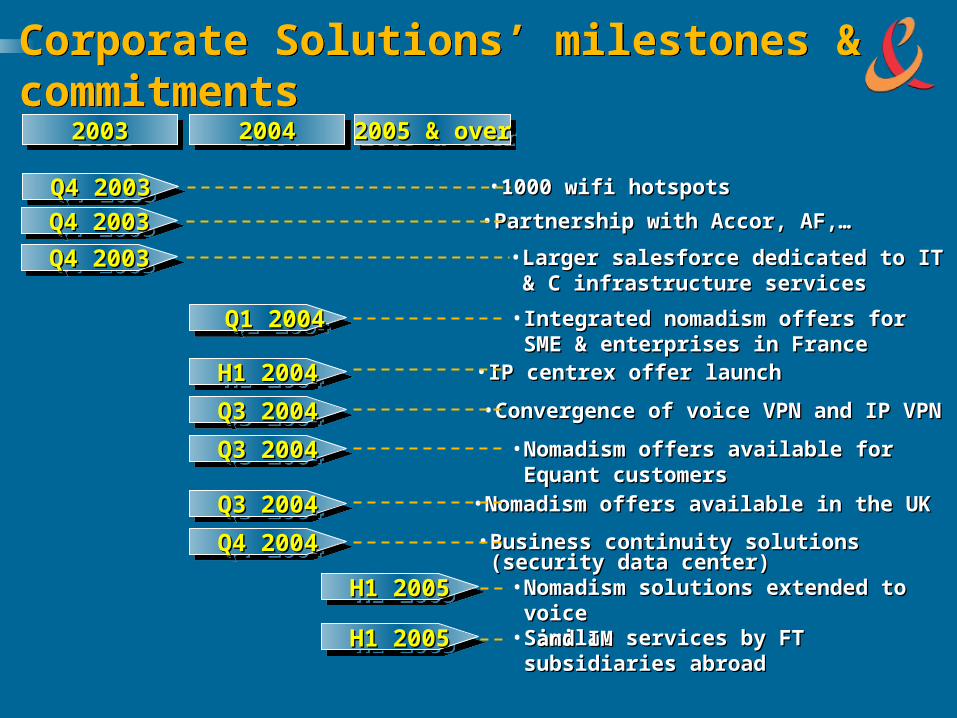

Corporate Solutions’ milestones & commitmentsCorporate Solutions’ milestones & commitments

2004200420042004 2005 & over2005 & over2005 & over2005 & over

Q4 2003Q4 2003Q4 2003Q4 2003

Q1 2004Q1 2004 Q1 2004Q1 2004

Q3 2004Q3 2004Q3 2004Q3 2004

H1 2004H1 2004H1 2004H1 2004

• Convergence of voice VPN and IP VPNConvergence of voice VPN and IP VPN

• 1000 wifi hotspots1000 wifi hotspots

• Integrated nomadism offers for SME & Integrated nomadism offers for SME & enterprises in Franceenterprises in France

• Similar services by FT subsidiaries Similar services by FT subsidiaries abroadabroad

• Nomadism offers available in the UKNomadism offers available in the UK

• IP centrex offer launch IP centrex offer launch

• Business continuity solutionsBusiness continuity solutions(security data center)(security data center)

Q3 2004Q3 2004Q3 2004Q3 2004

H1 2005H1 2005H1 2005H1 2005

• Nomadism offers available for Equant Nomadism offers available for Equant customerscustomers

Q3 2004Q3 2004Q3 2004Q3 2004

H1 2005H1 2005H1 2005H1 2005 • Nomadism solutions extended to voiceNomadism solutions extended to voice and IM and IM

Q4 2004Q4 2004Q4 2004Q4 2004

Q4 2003Q4 2003Q4 2003Q4 2003 • Partnership with Accor, AF,…Partnership with Accor, AF,…

Q4 2003Q4 2003Q4 2003Q4 2003 • Larger salesforce dedicated to IT & C Larger salesforce dedicated to IT & C infrastructure servicesinfrastructure services

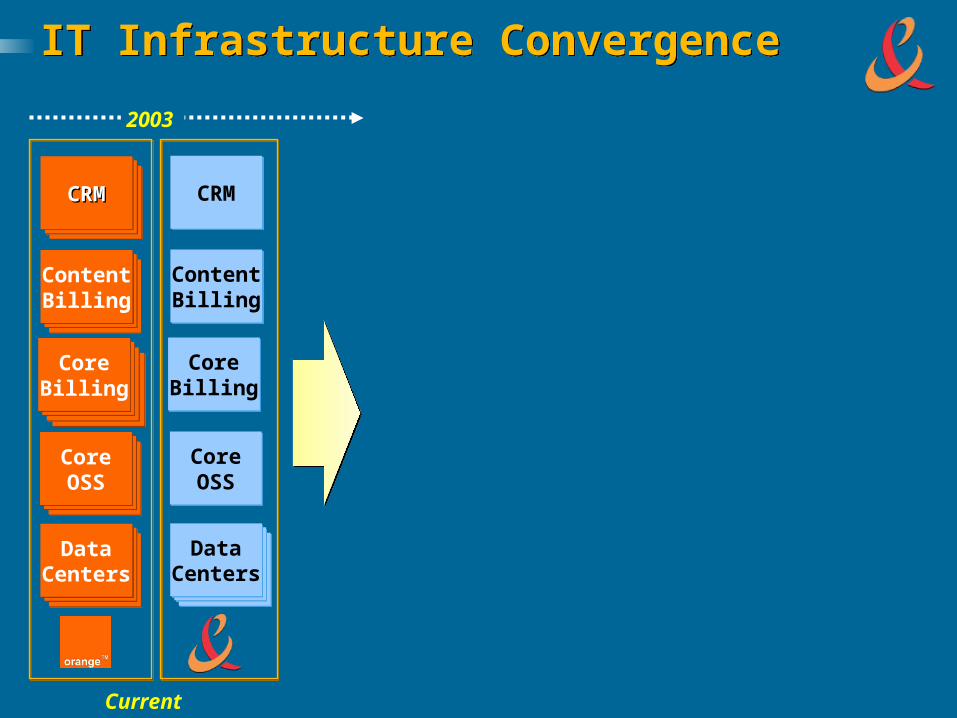

FT’s Network and IT: Convergence toenable usage innovation

FT’s Network and IT: Convergence toenable usage innovation

Availability of consistent services and applications Availability of consistent services and applications across networks based on open platformsacross networks based on open platforms

ServicesServicesplatformsplatformsServicesServicesplatformsplatforms

Convergence of transport of voice and data over Convergence of transport of voice and data over mobile and fixed networks, allowing reduced spending mobile and fixed networks, allowing reduced spending and consistent standard of servicesand consistent standard of services

ConvergenceConvergencenetworknetworkConvergenceConvergencenetworknetwork

Simplification and convergence of IT operations and Simplification and convergence of IT operations and key applications such as CRM and content billing key applications such as CRM and content billing across the companyacross the company

IT infrastructureIT infrastructureIT infrastructureIT infrastructure

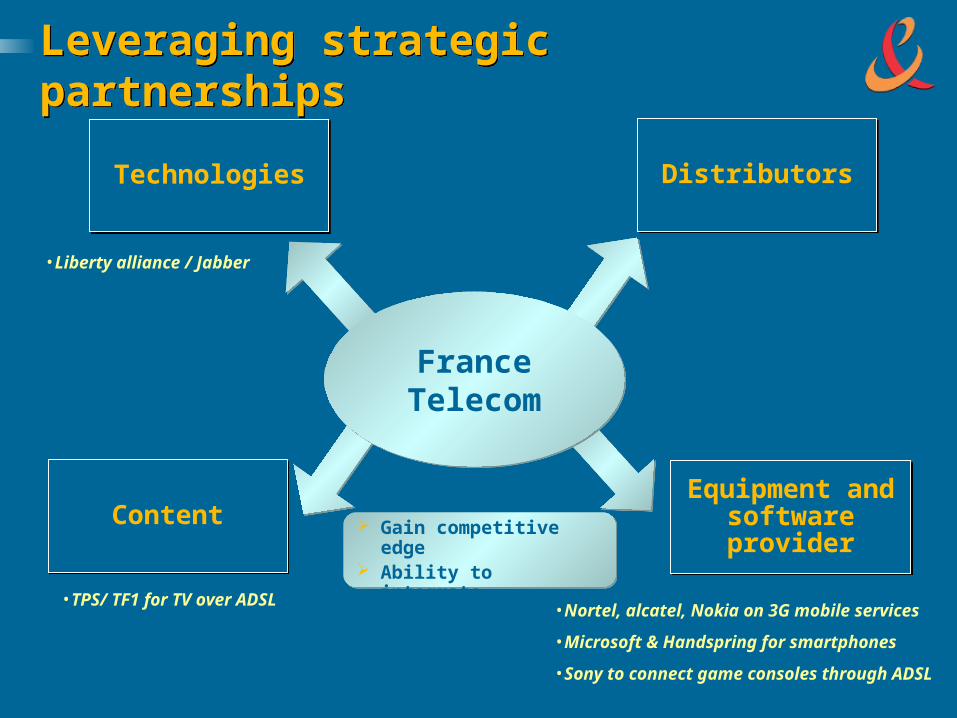

Leveraging strategic partnershipsLeveraging strategic partnerships

TechnologiesTechnologies DistributorsDistributors

ContentContent Equipment and software providerEquipment and

software provider

France TelecomFrance

Telecom

Gain competitive edge Ability to integrate

technologies

•Liberty alliance / Jabber

•TPS/ TF1 for TV over ADSL•Nortel, alcatel, Nokia on 3G mobile services

•Microsoft & Handspring for smartphones

•Sony to connect game consoles through ADSL

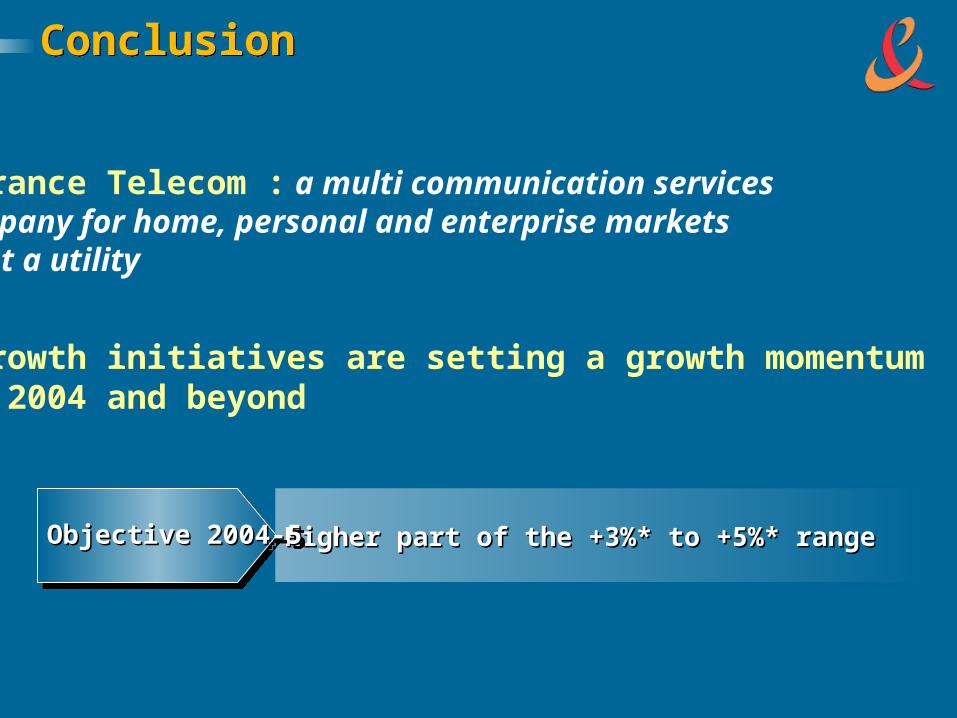

ConclusionConclusion

• France Telecom : a multi communication services company for home, personal and enterprise markets….not a utility

• Growth initiatives are setting a growth momentum for 2004 and beyond

Higher part of the +3%* to +5%* rangeHigher part of the +3%* to +5%* range

Objective 2004-5Objective 2004-5Objective 2004-5Objective 2004-5

Growth initiatives

Growth initiatives

BroadbandBroadband Didier Didier LombardLombard

Simplicity drives usageSimplicity drives usage Sanjiv AhujaSanjiv Ahuja Corporate SolutionsCorporate Solutions Barbara Barbara

DalibardDalibard

B r o a d b a n d B r o a d b a n d

Didier LombardDidier Lombard

CAUTIONARY STATEMENT CAUTIONARY STATEMENT

This presentation contains forward-looking statements about France Telecom. Such statements are not historical facts and include expressions of management’s expectations about new and existing programs, opportunities, technology and market conditions. Although France Telecom believes its expectations are based on reasonable assumptions, these forward-looking statements are subject to numerous risks and uncertainties. These statements should not be regarded as a representation that anticipated events will occur or that expected objectives will be achieved. Important factors that could cause actual results or performance to differ materially from the results anticipated in the forward-looking statements include, among other things, the success of the announced FT 2005 plan, including the “15 + 15 + 15” plan and the TOP program, changes in economic, business and competitive markets, technological trends, France Telecom’s other strategic, financial and operating initiatives, risks and uncertainties attendant upon international operations, exchange rate fluctuations and market regulatory factors. More detailed information on the potential factors that could affect the financial results of France Telecom is contained in the Document de référence submitted to the COB on March 21, 2003 and in its Form 20-F filed with the U.S. Securities and Exchange Commission. The forward-looking statements contained in this document speak only as of the date of this presentation and France Telecom does not undertake to update any forward-looking statement to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

This presentation contains forward-looking statements about France Telecom. Such statements are not historical facts and include expressions of management’s expectations about new and existing programs, opportunities, technology and market conditions. Although France Telecom believes its expectations are based on reasonable assumptions, these forward-looking statements are subject to numerous risks and uncertainties. These statements should not be regarded as a representation that anticipated events will occur or that expected objectives will be achieved. Important factors that could cause actual results or performance to differ materially from the results anticipated in the forward-looking statements include, among other things, the success of the announced FT 2005 plan, including the “15 + 15 + 15” plan and the TOP program, changes in economic, business and competitive markets, technological trends, France Telecom’s other strategic, financial and operating initiatives, risks and uncertainties attendant upon international operations, exchange rate fluctuations and market regulatory factors. More detailed information on the potential factors that could affect the financial results of France Telecom is contained in the Document de référence submitted to the COB on March 21, 2003 and in its Form 20-F filed with the U.S. Securities and Exchange Commission. The forward-looking statements contained in this document speak only as of the date of this presentation and France Telecom does not undertake to update any forward-looking statement to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

Broadband: a key market for FTBroadband: a key market for FT

BroadbandBroadbandTodayToday

BroadbandBroadbandTodayToday

Over 3mOver 3mlineslines

installedinstalledIn FranceIn Franceend of 03end of 03

Over 3mOver 3mlineslines

installedinstalledIn FranceIn Franceend of 03end of 03

StrongStrongleadershipleadershipfrom thefrom the

beginningbeginning

StrongStrongleadershipleadershipfrom thefrom the

beginningbeginning

2m 2m Wanadoo Wanadoo

customers customers in Europe in Europe (end of Q3)(end of Q3)

2m 2m Wanadoo Wanadoo

customers customers in Europe in Europe (end of Q3)(end of Q3)

Broadband: a key market for FTBroadband: a key market for FT

BroadbandBroadbandOpportunityOpportunity

BroadbandBroadbandOpportunityOpportunity

BetterBetterCoverageCoverage

BetterBetterCoverageCoverage

HigherHigherSpeedSpeedHigherHigherSpeedSpeed

ExpandingExpandingServicesServices

ExpandingExpandingServicesServices

450

0

50

100

150

200

250

300

350

400

1999 2000 2001 2002 2003 2004 2005

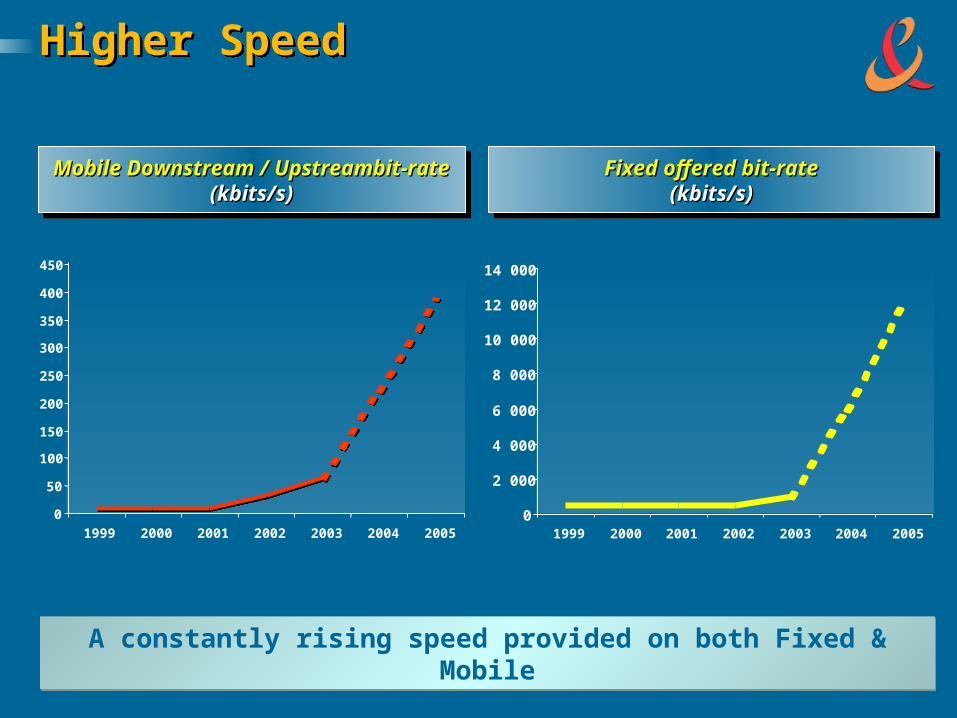

Higher SpeedHigher Speed

A constantly rising speed provided on both Fixed & Mobile

A constantly rising speed provided on both Fixed & Mobile

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

1999 2000 2001 2002 2003 2004 2005

Fixed offered bit-rateFixed offered bit-rate((kkbits/s)bits/s)

Fixed offered bit-rateFixed offered bit-rate((kkbits/s)bits/s)

Mobile Downstream / Upstreambit-rateMobile Downstream / Upstreambit-rate((kkbits/s)bits/s)

Mobile Downstream / Upstreambit-rateMobile Downstream / Upstreambit-rate((kkbits/s)bits/s)

Better CoverageBetter Coverage

Full broadband nation-wide coverage by 2005Full broadband nation-wide coverage by 2005

36%

66%74%

79%85%

90%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2001 2002 2003 2004 2005

ADSL Coverage French Market ADSL Coverage French Market ADSL Coverage French Market ADSL Coverage French Market 100% Coverage with Wifi & satellite 100% Coverage with Wifi & satellite 100% Coverage with Wifi & satellite 100% Coverage with Wifi & satellite

Satellite Satellite access access networknetwork

Satellite gatewaySatellite gateway

SatelliteSatellite

HUB

HouseholdHousehold

WiFiWiFiAccessAccessPointPoint

Expanding ServicesExpanding Services

Additional revenues based on a available & already invested network

Additional revenues based on a available & already invested network

Telephony +Telephony + Mobile +Mobile +

ImageImageInternet +Internet +

BroadbandBroadband

Personal Personal telephonytelephony

UMTSUMTSVideoVideo

TelephonyTelephony

Image Image messagingmessaging

TV onTV onADSLADSL

VODVOD

GamesGames

Image Image messagingmessaging

Photo Photo albumsalbums

Home Home networkingnetworking

VideoVideotelephonytelephony

nonnon PCPCPC,PC,

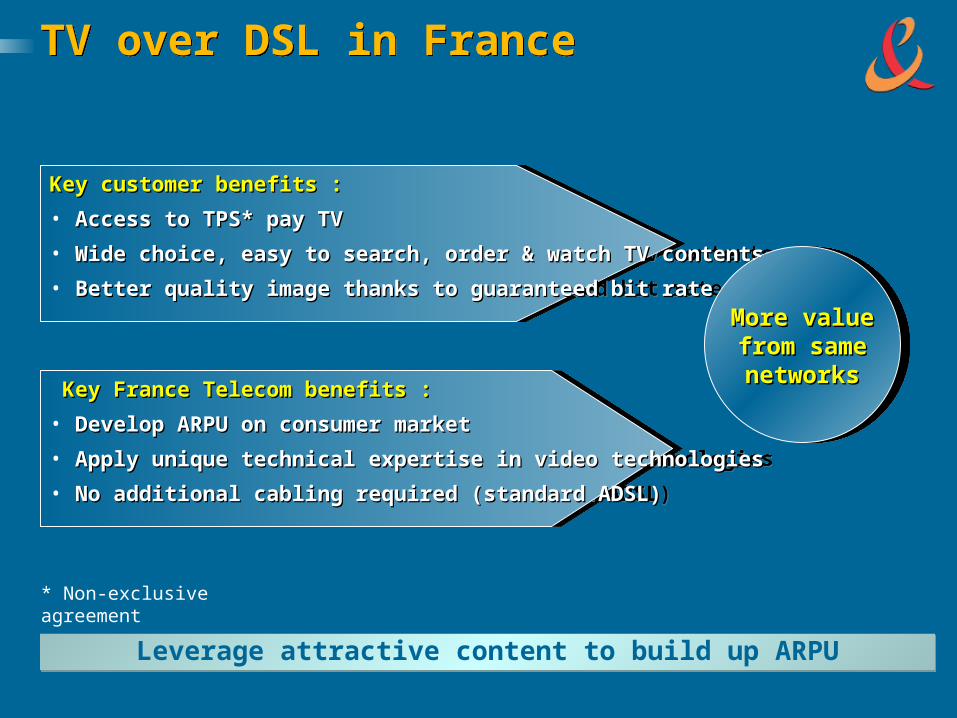

TV over DSL in France TV over DSL in France

Key customer benefits :Key customer benefits :

• Access to TPS* pay TVAccess to TPS* pay TV

• Wide choice, easy to search, order & watch TV contentsWide choice, easy to search, order & watch TV contents

• Better quality image thanks to guaranteed bit rateBetter quality image thanks to guaranteed bit rate

Key customer benefits :Key customer benefits :

• Access to TPS* pay TVAccess to TPS* pay TV

• Wide choice, easy to search, order & watch TV contentsWide choice, easy to search, order & watch TV contents

• Better quality image thanks to guaranteed bit rateBetter quality image thanks to guaranteed bit rate

Key France Telecom benefits :Key France Telecom benefits :

• Develop ARPU on consumer marketDevelop ARPU on consumer market

• Apply unique technical expertise in video technologiesApply unique technical expertise in video technologies

• No additional cabling required (standard ADSL)No additional cabling required (standard ADSL)

Key France Telecom benefits :Key France Telecom benefits :

• Develop ARPU on consumer marketDevelop ARPU on consumer market

• Apply unique technical expertise in video technologiesApply unique technical expertise in video technologies

• No additional cabling required (standard ADSL)No additional cabling required (standard ADSL)

More valueMore valuefrom samefrom samenetworksnetworks

More valueMore valuefrom samefrom samenetworksnetworks

* Non-exclusive agreement

Leverage attractive content to build up ARPULeverage attractive content to build up ARPU

Approx. 25,000 customers by end 2004Approx. 25,000 customers by end 2004Approx. 25,000 customers by end 2004Approx. 25,000 customers by end 2004

TVoDSL commercial rollout in Lyon late Dec. 2003,TVoDSL commercial rollout in Lyon late Dec. 2003,

then Paris in Q2 2004,and progressively reachthen Paris in Q2 2004,and progressively reach

in other French citiesin other French cities

TVoDSL commercial rollout in Lyon late Dec. 2003,TVoDSL commercial rollout in Lyon late Dec. 2003,

then Paris in Q2 2004,and progressively reachthen Paris in Q2 2004,and progressively reach

in other French citiesin other French cities

Develop partnerships with multiple TV content providersDevelop partnerships with multiple TV content providersDevelop partnerships with multiple TV content providersDevelop partnerships with multiple TV content providers

Target 10% of pay TV market by 2008Target 10% of pay TV market by 2008Target 10% of pay TV market by 2008Target 10% of pay TV market by 2008

ShortShort TermTermShortShort TermTerm

MediumMedium TermTerm

MediumMedium TermTerm

TV over DSL milestonesTV over DSL milestones

More valueMore valuefrom samefrom samenetworksnetworks

More valueMore valuefrom samefrom samenetworksnetworks

Fixed Line video-telephonyFixed Line video-telephony

Key customer benefits:Key customer benefits:

• Enrich the telephony experienceEnrich the telephony experience

• Enhanced environment for teleworking & groupwareEnhanced environment for teleworking & groupware

• Interoperable with mobile video-telephonyInteroperable with mobile video-telephony

Key customer benefits:Key customer benefits:

• Enrich the telephony experienceEnrich the telephony experience

• Enhanced environment for teleworking & groupwareEnhanced environment for teleworking & groupware

• Interoperable with mobile video-telephonyInteroperable with mobile video-telephony

Key France Telecom benefits:Key France Telecom benefits:

• Renewing value of telephonyRenewing value of telephony

• Leveraging IP to build up valueLeveraging IP to build up value

Key France Telecom benefits:Key France Telecom benefits:

• Renewing value of telephonyRenewing value of telephony

• Leveraging IP to build up valueLeveraging IP to build up value

Enriching the telephony experienceEnriching the telephony experience

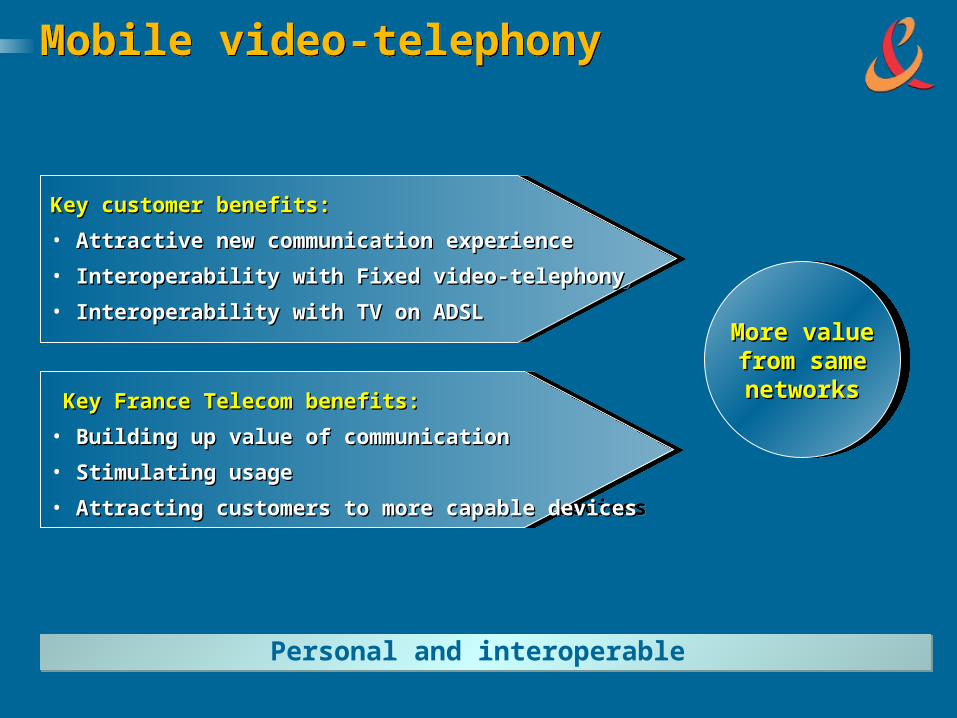

Mobile video-telephonyMobile video-telephony

Key customer benefits:Key customer benefits:

• Attractive new communication experienceAttractive new communication experience

• Interoperability with Fixed video-telephonyInteroperability with Fixed video-telephony

• Interoperability with TV on ADSLInteroperability with TV on ADSL

Key customer benefits:Key customer benefits:

• Attractive new communication experienceAttractive new communication experience

• Interoperability with Fixed video-telephonyInteroperability with Fixed video-telephony

• Interoperability with TV on ADSLInteroperability with TV on ADSL

Key France Telecom benefits:Key France Telecom benefits:

• Building up value of communicationBuilding up value of communication

• Stimulating usageStimulating usage

• Attracting customers to more capable devicesAttracting customers to more capable devices

Key France Telecom benefits:Key France Telecom benefits:

• Building up value of communicationBuilding up value of communication

• Stimulating usageStimulating usage

• Attracting customers to more capable devicesAttracting customers to more capable devices

Personal and interoperable Personal and interoperable

More valueMore valuefrom samefrom samenetworksnetworks

More valueMore valuefrom samefrom samenetworksnetworks

Field test with 1,500 customersField test with 1,500 customersLille, Paris, ToulouseLille, Paris, Toulouse

in Q2 2004in Q2 2004

Field test with 1,500 customersField test with 1,500 customersLille, Paris, ToulouseLille, Paris, Toulouse

in Q2 2004in Q2 2004 Non-PC product launch to 15,000Non-PC product launch to 15,000 customers before end of Q2 2004customers before end of Q2 2004Non-PC product launch to 15,000Non-PC product launch to 15,000 customers before end of Q2 2004customers before end of Q2 2004

Video-telephony milestonesVideo-telephony milestones

Full-scale product launch before end 2004Full-scale product launch before end 2004Full-scale product launch before end 2004Full-scale product launch before end 2004

Interoperability between consumer Fixed video-telephony Interoperability between consumer Fixed video-telephony & UTMS video-telephony (“villes Orange”)& UTMS video-telephony (“villes Orange”)

Interoperability between consumer Fixed video-telephony Interoperability between consumer Fixed video-telephony & UTMS video-telephony (“villes Orange”)& UTMS video-telephony (“villes Orange”)

Implementation in foreignImplementation in foreign subsidiaries in 2005subsidiaries in 2005

Implementation in foreignImplementation in foreign subsidiaries in 2005subsidiaries in 2005

Interoperability between TV on ADSLInteroperability between TV on ADSL

& video-telephony by end 2005& video-telephony by end 2005

Interoperability between TV on ADSLInteroperability between TV on ADSL

& video-telephony by end 2005& video-telephony by end 2005

MobileMobileMobileMobile FixedFixedFixedFixed

Wanadoo Visio currently trialedWanadoo Visio currently trialedWanadoo Visio currently trialedWanadoo Visio currently trialed

More valueMore valuefrom samefrom samenetworksnetworks

More valueMore valuefrom samefrom samenetworksnetworks

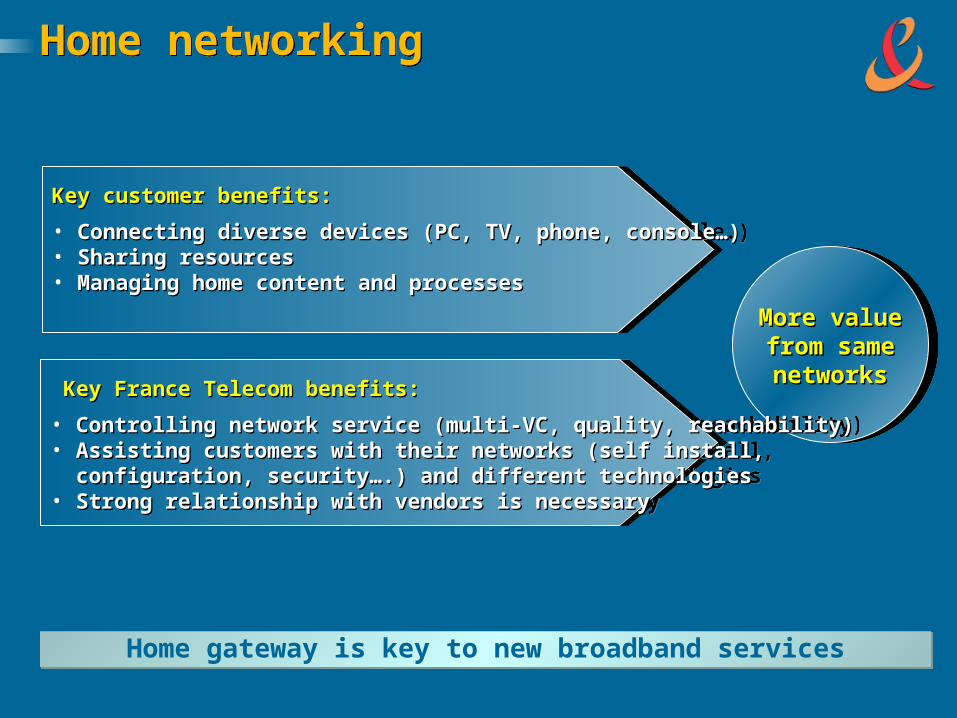

Home networkingHome networking

Key customer benefits:Key customer benefits:

• Connecting diverse devices (PC, TV, phone, console…)Connecting diverse devices (PC, TV, phone, console…)• Sharing resourcesSharing resources• Managing home content and processesManaging home content and processes

Key customer benefits:Key customer benefits:

• Connecting diverse devices (PC, TV, phone, console…)Connecting diverse devices (PC, TV, phone, console…)• Sharing resourcesSharing resources• Managing home content and processesManaging home content and processes

Key France Telecom benefits:Key France Telecom benefits:

• Controlling network service (multi-VC, quality, reachability)Controlling network service (multi-VC, quality, reachability)• Assisting customers with their networks (self install, Assisting customers with their networks (self install, configuration, security….) and different technologiesconfiguration, security….) and different technologies• Strong relationship with vendors is necessaryStrong relationship with vendors is necessary

Key France Telecom benefits:Key France Telecom benefits:

• Controlling network service (multi-VC, quality, reachability)Controlling network service (multi-VC, quality, reachability)• Assisting customers with their networks (self install, Assisting customers with their networks (self install, configuration, security….) and different technologiesconfiguration, security….) and different technologies• Strong relationship with vendors is necessaryStrong relationship with vendors is necessary

Home gateway is key to new broadband servicesHome gateway is key to new broadband services

2003200320032003

Broadband’s milestones & commitmentsBroadband’s milestones & commitments

2004200420042004 2005 & over2005 & over2005 & over2005 & over

Q4 2003Q4 2003Q4 2003Q4 2003

Dec. 2003Dec. 2003Dec. 2003Dec. 2003

Q2 2004Q2 2004Q2 2004Q2 2004

Q2 2004Q2 2004Q2 2004Q2 2004

H2 2004H2 2004H2 2004H2 2004Q2 2004Q2 2004Q2 2004Q2 2004

End 04End 04End 04End 04

2005200520052005

End 2008End 2008End 2008End 2008

• Satellite Internet accessSatellite Internet access

• TV-over-DSL launch in LyonTV-over-DSL launch in Lyon

• 3G field test in Lille, Paris & Toulouse3G field test in Lille, Paris & Toulouse

• TV-over-DSL launch in ParisTV-over-DSL launch in Paris

• Interoperability fixed & mobile Interoperability fixed & mobile video-telephonyvideo-telephony

• Non-PC video-telephonyNon-PC video-telephony

• 3G full-scale product launch3G full-scale product launch

• Video-over-DSL in foreign Video-over-DSL in foreign subsidiaries subsidiaries

• Target of 10% of pay TVTarget of 10% of pay TV

Q4 2003Q4 2003Q4 2003Q4 2003 • Wanadoo visio trialWanadoo visio trialJun. 2003Jun. 2003Jun. 2003Jun. 2003 • WiFi home routerWiFi home router

S i m p l i c i t y d r i v e s

u s a g e

S i m p l i c i t y d r i v e s

u s a g e

Sanjiv AhujaSanjiv Ahuja

CAUTIONARY STATEMENT CAUTIONARY STATEMENT

This presentation contains forward-looking statements about France Telecom. Such statements are not historical facts and include expressions of management’s expectations about new and existing programs, opportunities, technology and market conditions. Although France Telecom believes its expectations are based on reasonable assumptions, these forward-looking statements are subject to numerous risks and uncertainties. These statements should not be regarded as a representation that anticipated events will occur or that expected objectives will be achieved. Important factors that could cause actual results or performance to differ materially from the results anticipated in the forward-looking statements include, among other things, the success of the announced FT 2005 plan, including the “15 + 15 + 15” plan and the TOP program, changes in economic, business and competitive markets, technological trends, France Telecom’s other strategic, financial and operating initiatives, risks and uncertainties attendant upon international operations, exchange rate fluctuations and market regulatory factors. More detailed information on the potential factors that could affect the financial results of France Telecom is contained in the Document de référence submitted to the COB on March 21, 2003 and in its Form 20-F filed with the U.S. Securities and Exchange Commission. The forward-looking statements contained in this document speak only as of the date of this presentation and France Telecom does not undertake to update any forward-looking statement to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

This presentation contains forward-looking statements about France Telecom. Such statements are not historical facts and include expressions of management’s expectations about new and existing programs, opportunities, technology and market conditions. Although France Telecom believes its expectations are based on reasonable assumptions, these forward-looking statements are subject to numerous risks and uncertainties. These statements should not be regarded as a representation that anticipated events will occur or that expected objectives will be achieved. Important factors that could cause actual results or performance to differ materially from the results anticipated in the forward-looking statements include, among other things, the success of the announced FT 2005 plan, including the “15 + 15 + 15” plan and the TOP program, changes in economic, business and competitive markets, technological trends, France Telecom’s other strategic, financial and operating initiatives, risks and uncertainties attendant upon international operations, exchange rate fluctuations and market regulatory factors. More detailed information on the potential factors that could affect the financial results of France Telecom is contained in the Document de référence submitted to the COB on March 21, 2003 and in its Form 20-F filed with the U.S. Securities and Exchange Commission. The forward-looking statements contained in this document speak only as of the date of this presentation and France Telecom does not undertake to update any forward-looking statement to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

A typical customer may have... A typical customer may have...

Unnecessary complexitiesUnnecessary complexities

Work emailWork email

Home emailHome email

Work voicemailWork voicemail

Home voicemailHome voicemail

Mobile voicemailMobile voicemail

Work emailWork email

Home emailHome email

Work voicemailWork voicemail

Home voicemailHome voicemail

Mobile voicemailMobile voicemail

Web services passwordsWeb services passwords

Fixed numberFixed number

Bank account pin Bank account pin numbersnumbers

Mobile phone numberMobile phone number

Car phone numberCar phone number

Web services passwordsWeb services passwords

Fixed numberFixed number

Bank account pin Bank account pin numbersnumbers

Mobile phone numberMobile phone number

Car phone numberCar phone number

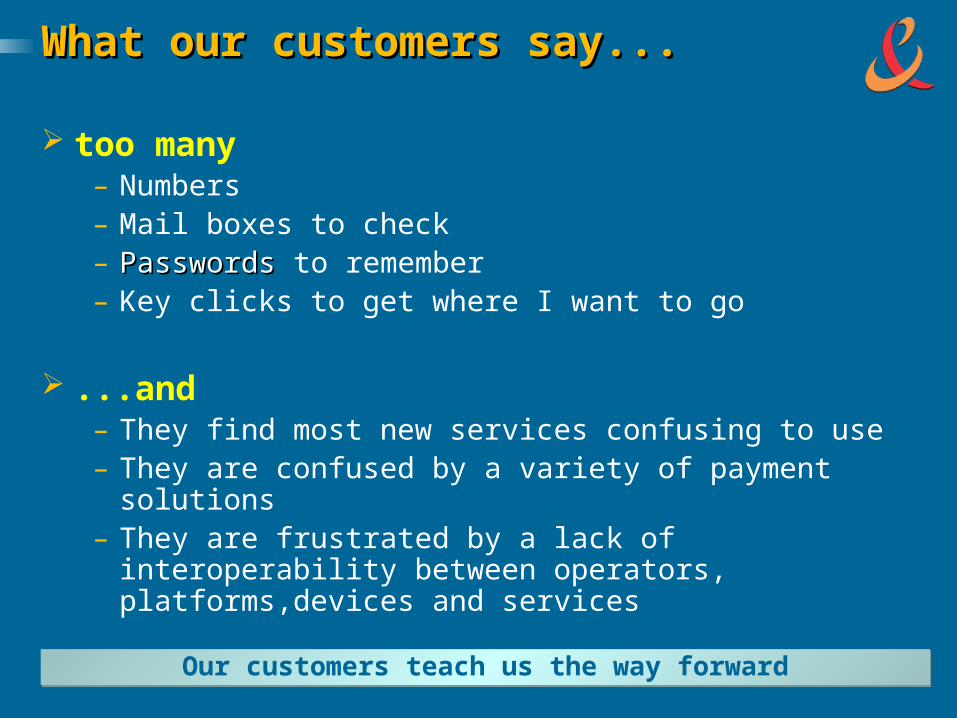

What our customers say...What our customers say...

too many– Numbers– Mail boxes to check– PasswordsPasswords to remember– Key clicks to get where I want to go

...and– They find most new services confusing to use– They are confused by a variety of payment solutions– They are frustrated by a lack of interoperability

between operators, platforms,devices and services

Our customers teach us the way forwardOur customers teach us the way forward

Fragmented offeringsFragmented offerings

Introducing new services Introducing new services is hampered by is hampered by interoperability issuesinteroperability issues

Nothing is connected Nothing is connected (different networks, (different networks, platforms and devices)platforms and devices)

Fragmented offeringsFragmented offerings

Introducing new services Introducing new services is hampered by is hampered by interoperability issuesinteroperability issues

Nothing is connected Nothing is connected (different networks, (different networks, platforms and devices)platforms and devices)

Make it simpleMake it simple(simplicity drives usage)(simplicity drives usage)

IntegrationIntegration(between networks, (between networks, service providers, service providers, application developers application developers etc.) Will deliver etc.) Will deliver simplified services and simplified services and enhancements fasterenhancements faster

Make it simpleMake it simple(simplicity drives usage)(simplicity drives usage)

IntegrationIntegration(between networks, (between networks, service providers, service providers, application developers application developers etc.) Will deliver etc.) Will deliver simplified services and simplified services and enhancements fasterenhancements faster

Removing barriers to growthRemoving barriers to growth

ChallengesChallengesChallengesChallenges SolutionsSolutionsSolutionsSolutions

How to make it simple and integratedHow to make it simple and integrated

5 key areas of focus5 key areas of focus

The foundations for a coherent suite of France Telecom Group services

The foundations for a coherent suite of France Telecom Group services

Fixed servicesFixed services

Mobile servicesMobile services

Internet servicesInternet services

Identity Identity Identity Identity AuthenticationAuthenticationAuthenticationAuthentication

Payment solutionsPayment solutions

IdentityIdentityAuthentication Authentication

PresencePresence

ReachabilityReachability

Contacts listContacts list

IdentityIdentity

One secure password access to all servicesOne secure password access to all servicesOne secure password access to all servicesOne secure password access to all services

Consistent and personalised interface across all devices Access rights management Ability to sign a transaction Secure access to business services and corporate

intranet Interoperability across networks/operators Open solution (liberty alliance) Single-sign-on for all FT group portals in France: Q2 2004 Become a trusted ID provider for third parties by 2005

Personalization and securityPersonalization and security

Too many passwordsToo many passwordsToo many passwordsToo many passwords

One number, one mailbox, be in contact, One number, one mailbox, be in contact, be connected … anywhere with one devicebe connected … anywhere with one deviceOne number, one mailbox, be in contact, One number, one mailbox, be in contact,

be connected … anywhere with one devicebe connected … anywhere with one device

ReachReach

Integrated instant messaging and email alerts: 2004 Seamless management of fixed and mobile voicemails:

Q3 2004 Wireless ADSL gateway able to communicate with mobile

phones, with automatic call forwarding when called party is away from home: Q4 2004

Mobile to fixed call forwarding when called party is at home: 2005

Interoperabiliy for seamless servicesInteroperabiliy for seamless services

Too many phone numbers, too many mailboxes,Too many phone numbers, too many mailboxes,too many unconnected ways to communicatetoo many unconnected ways to communicate

Too many phone numbers, too many mailboxes,Too many phone numbers, too many mailboxes,too many unconnected ways to communicatetoo many unconnected ways to communicate

My personal contact list accessible through the network My personal contact list accessible through the network to any device, any location, anytimeto any device, any location, anytime

My personal contact list accessible through the network My personal contact list accessible through the network to any device, any location, anytimeto any device, any location, anytime

Contact lists everywhereContact lists everywhere(one in my computer, one in my home phone, (one in my computer, one in my home phone,

one in my mobile…)one in my mobile…)

Contact lists everywhereContact lists everywhere(one in my computer, one in my home phone, (one in my computer, one in my home phone,

one in my mobile…)one in my mobile…)

Contact listContact list

Orange BackupBackup launched 2002 Orange UK single contact list launched 2003 Fixed line (France): H1 2004 with new terminals or voice

access Wanadoo single contact list: H1 2004 Universal contact list: 2005

Orange BackupBackup launched 2002 Orange UK single contact list launched 2003 Fixed line (France): H1 2004 with new terminals or voice

access Wanadoo single contact list: H1 2004 Universal contact list: 2005

A Complex InfrastructureA Complex Infrastructure

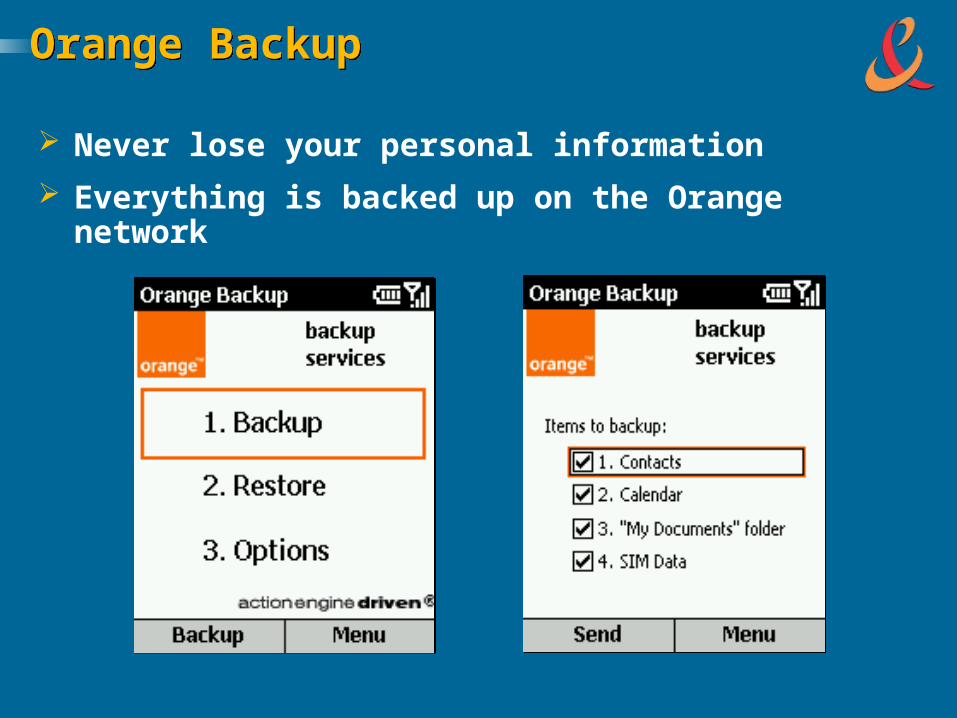

Orange BackupOrange Backup

Never lose your personal information

Everything is backed up on the Orange network

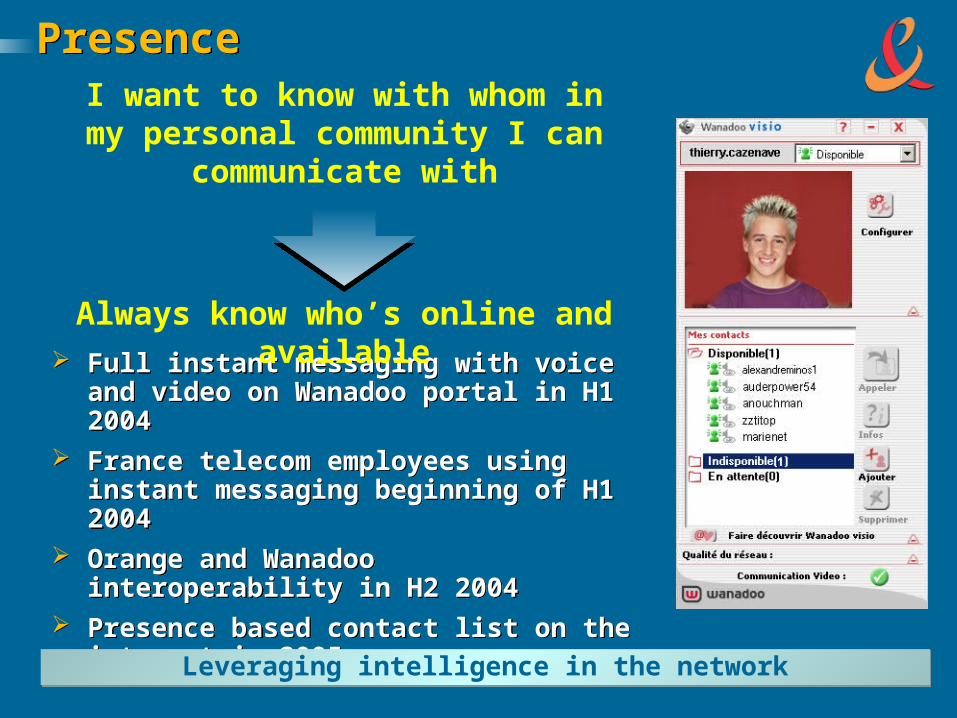

I want to know with whom in my personal community I can

communicate with

PresencePresence

Full instant messaging with voice and video on Wanadoo portal in H1 2004

France telecom employees using instant messaging beginning of H1 2004

Orange and Wanadoo interoperability in H2 2004

Presence based contact list on the internet in 2005

Full instant messaging with voice and video on Wanadoo portal in H1 2004

France telecom employees using instant messaging beginning of H1 2004

Orange and Wanadoo interoperability in H2 2004

Presence based contact list on the internet in 2005

Leveraging intelligence in the networkLeveraging intelligence in the network

Always know who’s online and available

Simple online payment solutionsSimple online payment solutionsSimple online payment solutionsSimple online payment solutions

I want a simple way to purchase itemsI want a simple way to purchase itemsI want a simple way to purchase itemsI want a simple way to purchase items

PaymentPayment

Capability to send out millions of bills and collect small amounts Sourcing of “best-of-breed” software platforms (kenan, portal, IPIN) Real-time account management and on-line purchase authorisation

on all networks Reputation with content providers inherited from Teletel and

Audiotel Single merchant kit for fixed, mobile and internet Q3 2004 Large scale deployment of content billing for m-commerce Q4 2004

Trusted, standardised and open Trusted, standardised and open

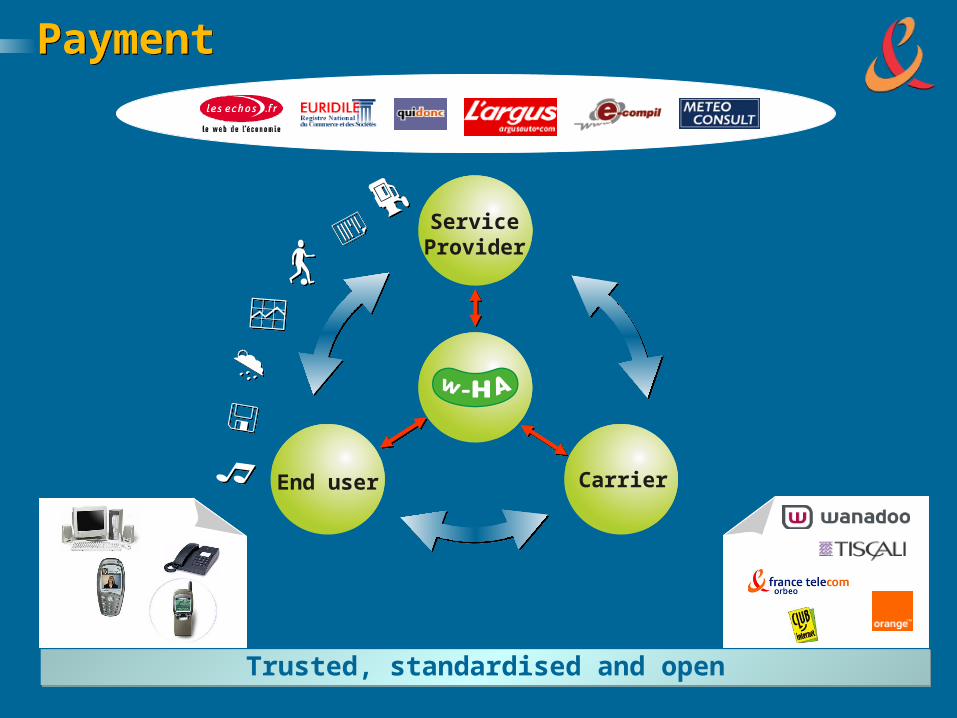

PaymentPayment

Trusted, standardised and openTrusted, standardised and open

CarrierEnd user

ServiceProvider

2003200320032003

Ease of use milestones & commitmentsEase of use milestones & commitments

2004200420042004 2005 & over2005 & over2005 & over2005 & over

Q2 2003Q2 2003Q2 2003Q2 2003

H1 2004H1 2004H1 2004H1 2004

H1 2004H1 2004 H1 2004H1 2004

H2 2004H2 2004H2 2004H2 2004

H2 2005H2 2005H2 2005H2 2005

Q3 2004Q3 2004Q3 2004Q3 2004

• Single Sign On (SSO) for FT group portalsSingle Sign On (SSO) for FT group portals

• W-HA Common payment indentifierW-HA Common payment indentifier

• Orange contact list in UKOrange contact list in UK

• Single contact list for fixed and WanadooSingle contact list for fixed and Wanadoo• Voice and video on Wanadoo’Voice and video on Wanadoo’

Instant MessagingInstant Messaging

• Full interoperable contacts listFull interoperable contacts list

• Wanadoo-Orange IM interoperabilityWanadoo-Orange IM interoperability

• Presence-based contact list Presence-based contact list

• Seamless fixed, mobile voice mails Seamless fixed, mobile voice mails

• Automatic call forwarding fixed-to-mobileAutomatic call forwarding fixed-to-mobile

Q2 2004Q2 2004Q2 2004Q2 2004

Q3 2004Q3 2004Q3 2004Q3 2004

H1 2005H1 2005H1 2005H1 2005

H1 2005H1 2005H1 2005H1 2005 • Mobile-to-fixed call forwardingMobile-to-fixed call forwarding

• Single merchant kitSingle merchant kit

• Large scale deployment of paymentLarge scale deployment of payment

Q3 2004Q3 2004Q3 2004Q3 2004

Q4 2004Q4 2004Q4 2004Q4 2004

H2 2005H2 2005H2 2005H2 2005 • Trusted ID providerTrusted ID provider

Q4 2004Q4 2004Q4 2004Q4 2004

C o r p o r a t eS o l u t i o n sC o r p o r a t eS o l u t i o n s

Barbara DalibardBarbara Dalibard

CAUTIONARY STATEMENT CAUTIONARY STATEMENT

This presentation contains forward-looking statements about France Telecom. Such statements are not historical facts and include expressions of management’s expectations about new and existing programs, opportunities, technology and market conditions. Although France Telecom believes its expectations are based on reasonable assumptions, these forward-looking statements are subject to numerous risks and uncertainties. These statements should not be regarded as a representation that anticipated events will occur or that expected objectives will be achieved. Important factors that could cause actual results or performance to differ materially from the results anticipated in the forward-looking statements include, among other things, the success of the announced FT 2005 plan, including the “15 + 15 + 15” plan and the TOP program, changes in economic, business and competitive markets, technological trends, France Telecom’s other strategic, financial and operating initiatives, risks and uncertainties attendant upon international operations, exchange rate fluctuations and market regulatory factors. More detailed information on the potential factors that could affect the financial results of France Telecom is contained in the Document de référence submitted to the COB on March 21, 2003 and in its Form 20-F filed with the U.S. Securities and Exchange Commission. The forward-looking statements contained in this document speak only as of the date of this presentation and France Telecom does not undertake to update any forward-looking statement to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

This presentation contains forward-looking statements about France Telecom. Such statements are not historical facts and include expressions of management’s expectations about new and existing programs, opportunities, technology and market conditions. Although France Telecom believes its expectations are based on reasonable assumptions, these forward-looking statements are subject to numerous risks and uncertainties. These statements should not be regarded as a representation that anticipated events will occur or that expected objectives will be achieved. Important factors that could cause actual results or performance to differ materially from the results anticipated in the forward-looking statements include, among other things, the success of the announced FT 2005 plan, including the “15 + 15 + 15” plan and the TOP program, changes in economic, business and competitive markets, technological trends, France Telecom’s other strategic, financial and operating initiatives, risks and uncertainties attendant upon international operations, exchange rate fluctuations and market regulatory factors. More detailed information on the potential factors that could affect the financial results of France Telecom is contained in the Document de référence submitted to the COB on March 21, 2003 and in its Form 20-F filed with the U.S. Securities and Exchange Commission. The forward-looking statements contained in this document speak only as of the date of this presentation and France Telecom does not undertake to update any forward-looking statement to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

Towards open networks shared with partnersTowards open networks shared with partners

Evolution of corporate customer infrastructureEvolution of corporate customer infrastructure

IP & Ethernet IP & Ethernet Multi networkMulti network

accessaccess

IP & Ethernet IP & Ethernet Multi networkMulti network

accessaccess

Toward an integrated network Toward an integrated network

IP SECIP SECXDSLXDSLWIFIWIFIVOIPVOIP

IP SECIP SECXDSLXDSLWIFIWIFIVOIPVOIP

19801980 19901990 19951995 2003200320002000 TomorrowTomorrow

IP VPNIP VPNMPLSMPLS

Voice VPNVoice VPN

IP VPNIP VPNMPLSMPLS

Voice VPNVoice VPN

Frame RelayFrame RelayATMATMISDNISDN

Frame RelayFrame RelayATMATMISDNISDN

Star networks,Star networks,Leased linesLeased lines

X25X25PSTNPSTN

Star networks,Star networks,Leased linesLeased lines

X25X25PSTNPSTN

Distributed Distributed computingcomputing

Multi-deviceMulti-device

Distributed Distributed computingcomputing

Multi-deviceMulti-device

IT evolutionIT evolution

19801980 19901990 19951995 2003200320002000

3 tier web3 tier webarchitecturesarchitectures

3 tier web3 tier webarchitecturesarchitecturesClient serverClient serverClient serverClient server

TomorrowTomorrow

Centralised ISCentralised ISCentralised ISCentralised IS

Business trendsBusiness trends

Employees are a key asset of Customer centric organisations and need efficient communication

Developing managed and integrated communication services

Developing managed and integrated communication services

NomadismNomadismNomadismNomadism

After optimisation, businesses want to take advantage of new technologies with simple and integrated solutions

Integration and outsourcing Integration and outsourcing of communication servicesof communication servicesIntegration and outsourcing Integration and outsourcing of communication servicesof communication services

Nomadism: market trendsNomadism: market trends

8 out of 10 employees are mobile within their company8 out of 10 employees are mobile within their company 3 out of 10 are mobile outside the company3 out of 10 are mobile outside the company Up to 60% of businesses have started an IT mobility project, Up to 60% of businesses have started an IT mobility project,

and 37% of CIOs consider that it is strategic to their businessand 37% of CIOs consider that it is strategic to their business

Source: IDC/Orange 12/2002

What applications do employees need? What applications do employees need?

Our customers expect to be connectedanywhere, anytime, from any device

Our customers expect to be connectedanywhere, anytime, from any device

0 10 20 30 40 50 60 70 80 90 100

NSP

Accès fax

File Transfer

Internet Access

Intranet / Applications accesses

Email Access 75.0%75.0%

60.4%60.4%

39.4%39.4%

35.4%35.4%

16.7%16.7%

4.2%4.2%

55%

44%

27%

23%

21%

15%

9%

9%

6%

3%

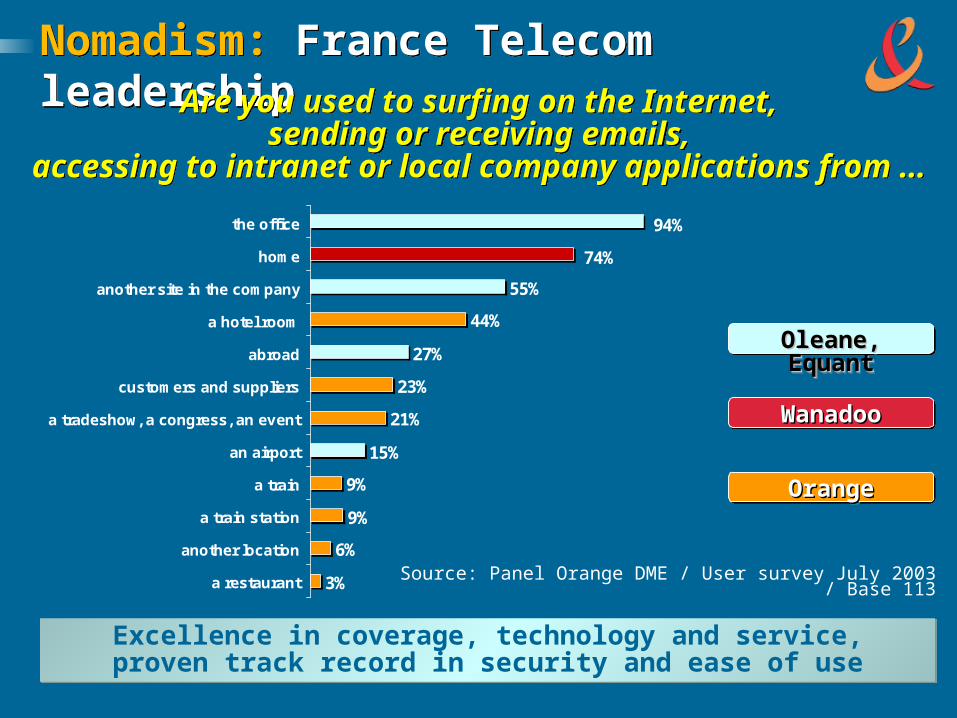

74%

94%the office

home

another site in the company

a hotel room

abroad

customers and suppliers

a tradeshow, a congress, an event

an airport

a train

a train station

another location

a restaurant

Nomadism: France Telecom leadershipNomadism: France Telecom leadershipAre you used to surfing on the Internet,

sending or receiving emails,accessing to intranet or local company applications from …

Are you used to surfing on the Internet,sending or receiving emails,

accessing to intranet or local company applications from …

Source: Panel Orange DME / User survey July 2003 / Base 113

Excellence in coverage, technology and service,proven track record in security and ease of useExcellence in coverage, technology and service,proven track record in security and ease of use

Oleane, EquantOleane, EquantOleane, EquantOleane, Equant

WanadooWanadooWanadooWanadoo

OrangeOrangeOrangeOrange

Nomadism: our propositionNomadism: our proposition

Offer employees on the move, whatever the Offer employees on the move, whatever the network and device, the set of services they neednetwork and device, the set of services they need– ““User friendliness”: connection kit, single sign-on…User friendliness”: connection kit, single sign-on…– End-to-end securityEnd-to-end security– Integrated customer careIntegrated customer care

Developed in partnership with key clientsDeveloped in partnership with key clients

First market to launch: FranceFirst market to launch: France– 1,7 million blue collars1,7 million blue collars– 2,6 million white collars / professionals2,6 million white collars / professionals

A France Telecom Group wide projectA France Telecom Group wide project

Nomadism: a segmented offerNomadism: a segmented offer

Solution for professionalsSolution for professionals

– Access through Wanadoo and Orange to Wanadoo Mail Access through Wanadoo and Orange to Wanadoo Mail and Portal using SSL securityand Portal using SSL security

Solution for SMEsSolution for SMEs

– Access through Oleane and Orange to Oleane Mail, Portal Access through Oleane and Orange to Oleane Mail, Portal and Business Services using IPSEC securityand Business Services using IPSEC security

Solution for CorporatesSolution for Corporates

– Access via Equant IP VPN, Orange and Wanadoo to Access via Equant IP VPN, Orange and Wanadoo to Equant Mail and to corporate Intranet through security Equant Mail and to corporate Intranet through security (IPSEC, MPLS) and corporate authentication services(IPSEC, MPLS) and corporate authentication services

Coverage, Technology, Service, Security, SimplicityCoverage, Technology, Service, Security, Simplicity

VOIP, IPBX, IP centrex, WLANVOIP, IPBX, IP centrex, WLAN

Single voice and data networksSingle voice and data networks

Desktop to desktop multimedia Desktop to desktop multimedia streams to managestreams to manage

VOIP, IPBX, IP centrex, WLANVOIP, IPBX, IP centrex, WLAN

Single voice and data networksSingle voice and data networks

Desktop to desktop multimedia Desktop to desktop multimedia streams to managestreams to manage

Customers need help to manage a major transitionCustomers need help to manage a major transition

POTS, PBX, LANPOTS, PBX, LAN

Separate voice and data Separate voice and data networksnetworks

Building to building Building to building network engineeringnetwork engineering

POTS, PBX, LANPOTS, PBX, LAN

Separate voice and data Separate voice and data networksnetworks

Building to building Building to building network engineeringnetwork engineering

Businesses encounter major technology changesBusinesses encounter major technology changes

IT&C infrastructure management:Customer challenges

IT&C infrastructure management:Customer challenges

IT&C infrastructure management:Simplifying the landscapeIT&C infrastructure management:Simplifying the landscape

PracticesPractices– Plan: Consulting, application/network performance analysisPlan: Consulting, application/network performance analysis

– Build: project management, deployment (including equipment supply)Build: project management, deployment (including equipment supply)

– Run: ORun: Operation, maintenance, user and telecom manager assistanceperation, maintenance, user and telecom manager assistance

TechnologiesTechnologies– Telephony: PBX, IPBX, IP centrexTelephony: PBX, IPBX, IP centrex

– LAN, MAN: infrastructures, servers, cabling and WLANLAN, MAN: infrastructures, servers, cabling and WLAN

– Messaging: MS Exchange, Lotus NotesMessaging: MS Exchange, Lotus Notes

– Servers: Unix, Linux, Windows, JEE, .NETServers: Unix, Linux, Windows, JEE, .NET

– Security: firewalls, antivirus, antispam, intrusion detection, IP SECSecurity: firewalls, antivirus, antispam, intrusion detection, IP SEC

Simplifying the technological transitionSimplifying the technological transition

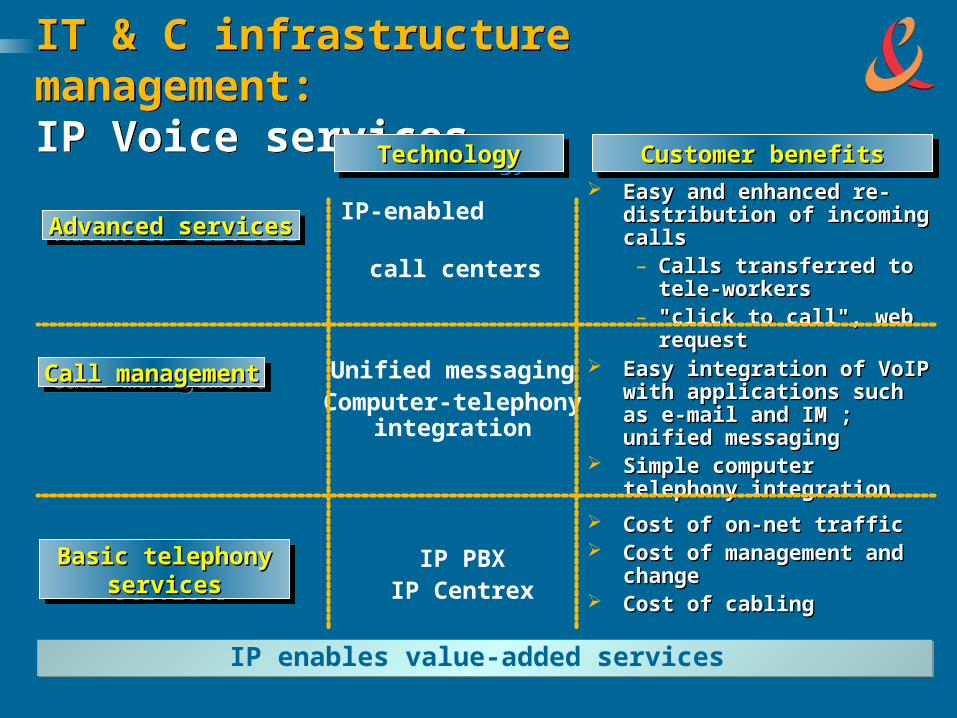

IT & C infrastructure management: IP Voice services

IT & C infrastructure management: IP Voice services

TechnologyTechnologyTechnologyTechnology Customer benefitsCustomer benefitsCustomer benefitsCustomer benefits

Advanced servicesAdvanced servicesAdvanced servicesAdvanced servicesIP-enabled

call centers

IP PBX IP Centrex

Easy and enhanced re-Easy and enhanced re-distribution of incoming callsdistribution of incoming calls– Calls transferred to tele-Calls transferred to tele-

workersworkers– "click to call", web request"click to call", web request

Basic telephonyBasic telephonyservicesservices

Basic telephonyBasic telephonyservicesservices

Cost of on-net trafficCost of on-net traffic Cost of management and Cost of management and

change change Cost of cablingCost of cabling

Call managementCall managementCall managementCall management Unified messagingComputer-telephony

integration

Easy integration of VoIP with Easy integration of VoIP with applications such as e-mail applications such as e-mail and IM ; unified messagingand IM ; unified messaging

Simple computer telephony Simple computer telephony integrationintegration

IP enables value-added services IP enables value-added services

IT & C infrastructure management : Security services

IT & C infrastructure management : Security services Consulting, AssessmentsConsulting, Assessments

Comprehensive Services portfolio, from single firewall Comprehensive Services portfolio, from single firewall management to complete security out-taskingmanagement to complete security out-tasking– Internet access protectionInternet access protection

– Intranet segmentationIntranet segmentation

– Remote access securisationRemote access securisation

– Intrusion detection, antispam, anti-virus…Intrusion detection, antispam, anti-virus…

We partner with leading vendorsWe partner with leading vendors

We protect the NetworkWe protect the Network

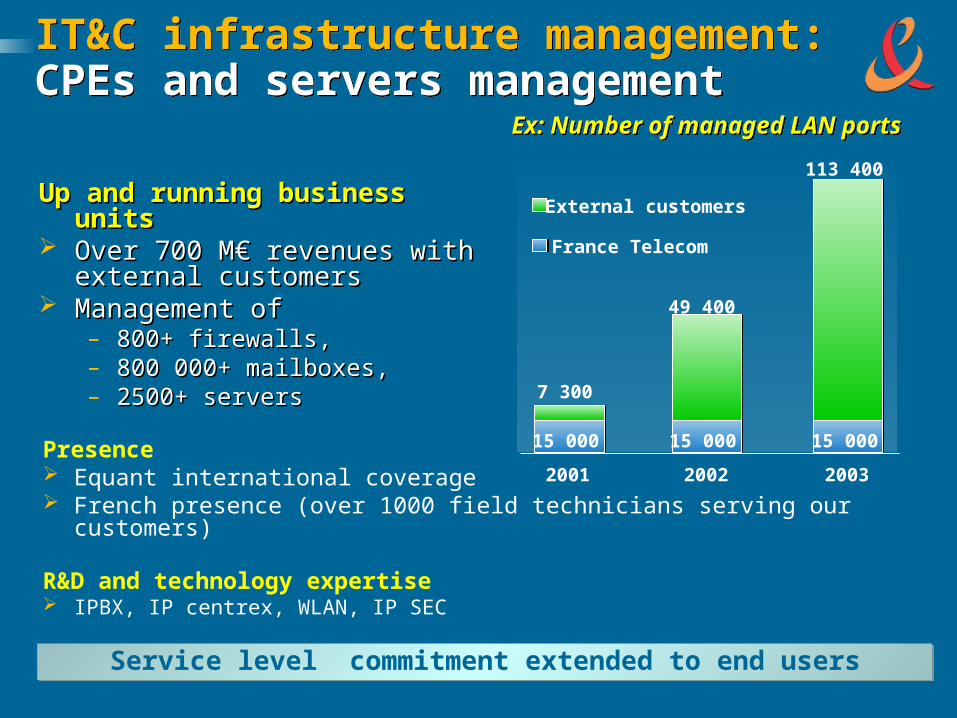

IT&C infrastructure management: CPEs and servers managementIT&C infrastructure management: CPEs and servers management

Presence Equant international coverage French presence (over 1000 field technicians serving our customers)

R&D and technology expertise IPBX, IP centrex, WLAN, IP SEC

Service level commitment extended to end usersService level commitment extended to end users

Up and running business unitsUp and running business units Over 700 M€ revenues with Over 700 M€ revenues with

external customersexternal customers Management ofManagement of

– 800+ firewalls,800+ firewalls,– 800 000+ mailboxes,800 000+ mailboxes,– 2500+ servers2500+ servers

Ex: Number of managed LAN portsEx: Number of managed LAN ports

15 000 15 000 15 000

7 300

49 400

113 400

2001 2002 2003

External customers

France Telecom

Communications Outsourcing: MarketCommunications Outsourcing: Market

ED

SE

DS

Geo coverage

Fixed telecom Fixed telecom networksnetworks

Infrastructure ITInfrastructure IT

Application Application ManagementManagement

AT

&T

AT

&T

CS

CC

SC

FT

/ E

qu

ant

FT

/ E

qu

ant

Wo

rld

Co

mW

orl

dC

om

Acc

entu

reA

ccen

ture

Info

net

Info

net

International(multi-regional)RegionalNational

Na

tio

na

l T

elc

os

Na

tio

na

l T

elc

os

IBM

IB

M

Ato

s O

rig

inA

tos

Ori

gin

CG

E&

YC

GE

&Y

BT

BT

Kin

d o

f o

uts

ou

rcin

g

C&

WC

&W

Key Players and Segment in target marketKey Players and Segment in target marketKey Players and Segment in target marketKey Players and Segment in target market

Mobile telecom Mobile telecom networksnetworks