wb-1461 understanding margin webinar 20120515 jpohl · • merger: two companies combine into a...

TRANSCRIPT

1

Interactive Brokers presents

Corporate Actions

Bruce Turner

Webinar begins @ 12:00pm EDT

Member SIPC www.sipc.org

[email protected] www.ibkr.com/webinars

Agenda

• Overview of Corporate Actions • Types of Corporate Actions • Categories of Corporate Actions • Corporate Action Tool • Examples of Corporate Actions

2

What is a Corporate Action?

• An event that brings material change to a company and affects its investors

• The term is used differently by different people • We will use the term in the broadest sense • This broad definition includes everything from a cash

dividend to a restructuring in bankruptcy or complete dissolution of a corporation

3

Purpose of Corporate Actions

The primary purposes of corporate actions are: • Distribute profits to shareholders • Influence share price • Corporate Restructuring

4

Distribute Profits to Shareholders

• Cash Dividends • Share Repurchases

5

Cash Dividends

• Paid in proportion to shares held on the Record Date • Distribution of earnings of the corporation on the

Payment date • Usually fixed dates (e.g., quarterly) • Sometimes special dividends are paid • Stock price is expected to decrease on ex-div date

6

Share Repurchases

• Company purchases shares of its own stock – Most often through open market purchases – Companies also purchase shares through tender offers

• The effect of a share repurchase is that remaining shareholders own a greater proportion of the company as fewer shares remain outstanding

• If earnings stay the same, per-share measures such as earnings per share increase

7

Share Repurchases

• Value is only created for shareholders if the company pays less than the inherent value of the shares

• If the stock is undervalued, share repurchases should create value for remaining shareholders

• If shares are overvalued or a corporation overpays, it may destroy value for remaining shareholders – Management may overestimate share value – Management may repurchase in spite of a high price

8

Influence Share Price in the Market

• Stocks Splits • Stock Dividends

9

Stock Split and Stock Dividends

• Distribution of new shares to existing shareholders • Stock dividends and stock splits are similar

– Stock dividends are expressed as a percentage – Stock splits are expressed as a ratio

• Real difference is the accounting treatment for the issuing corporation – not important to most investors

10

Stock Split and Stock Dividends

• Ordinarily won’t change overall value of an investment

• Lower price may increase liquidity • Reverse splits may help a very low stock price

– Some exchanges have price minimums for listing

• Bonus issue is a stock dividend expressed as a ratio instead of a percentage

11

Structural Changes

There are a many corporate actions used for structural changes. We will focus on: • Mergers and acquisitions • Spin-offs • Tender offers

12

Mergers and Acquisitions

• Combine two companies into a single company • Terms interchangeable, although there are technical

legal differences • Many different mechanisms can be used • Sometimes require shareholder approval of one or

both companies • Shareholders may be cashed out, may receive new

shares or may retain their old shares

13

Mergers and Acquisitions

• Merger: two companies combine into a single larger company

• Acquisition: one company acquires the stock/assets of another. Acquirer’s stock remains outstanding

• Common use in financial media: – Merger: combination of equal companies, friendly – Acquisition: Stronger company buys weaker company, may

be hostile

14

Mergers and Acquisitions

• Stockholders of larger company often retain stock • Stockholders of weaker company often receive cash

or stock of stronger company • Many different exchanges are possible • Sometimes voluntary component

15

Spin-Offs

• Creation of an independent company by the distribution or sale of shares of the new company

• Separates a division, subsidiary or business line

16

Reasons for a Spin-Off

• Unrelated businesses may be separated so that the market may better appreciate the spun-off company

• A poor performing business can be separated so that the core remaining businesses will be more appealing to investors

• Can solve strategic, antitrust or regulatory issues and impediments to other acquisitions, etc.

17

Tender Offers

• Offer to buy some or all of the shares of a corporation – Usually at a premium to market price – Can be friendly or unfriendly

• Possible restrictions: – A minimum number of shares that must be tendered – A maximum number that will be accepted

• Can be made by issuer (buyback) • Can be made by an unrelated party (acquisition)

18

Other Corporate Actions

There are many other corporate actions for the purpose of structural change:

– Restructuring in bankruptcy • May involve a stock and/or bond exchange

– Rights issues – Exchange offers – Bond Redemption

19

Categories of Corporate Actions

• Mandatory • Voluntary • Mandatory with Choice

20

Mandatory Corporate Actions

• A stock dividend is paid to all shareholders; no action is required

• A stock split affects all outstanding shares of stock; no action is required

• A merger affects all shareholders; no action required • Ministerial actions may be required such as

surrendering old shares for new shares – IB will perform these ministerial actions for you

21

Voluntary Corporate Actions

• Shareholders choose to participate • No response = no direct change to non-participants • May significantly impact the nature of the

investment; may be followed by a mandatory action • Tender offers • Rights issues • Exchange offers

22

Mandatory with Choice

• Dividend can be paid in cash or shares • Exchange offer may offer choice of cash/stock/bonds

in exchange for outstanding securities • Merger, spin-off etc. may provide shareholders with

a choice of consideration • A default option generally will apply if an investor

fails to make a choice

23

Corporate Actions in Account Management

• The Corporate Actions tab on the Home page displays the number of corporate actions notifications that you have received

• If you hold a stock, option, bond, or SSF position in a company you will receive notification of corporate actions for that company

24

Corporate Action Notifications

25

Corporate Actions Page

• We notify you of pending actions up to three months out

• If you have any notifications of corporate actions, they appear on the Corporate Actions page

• The page displays a "No Messages" message if you do not have any Customer Service messages

26

Corporate Action Tool

• Access from Support > Tools > Corporate Actions • Review information for mandatory and voluntary

corporate actions

27

Corporate Action Tool

• Make elections for voluntary corporate actions and mandatory corporate actions with choice

• Voluntary and mandatory corporate actions with choice appear on the Choice Corporate Actions tab

• Mandatory corporate actions appear on the Other Corporate Actions tab

28

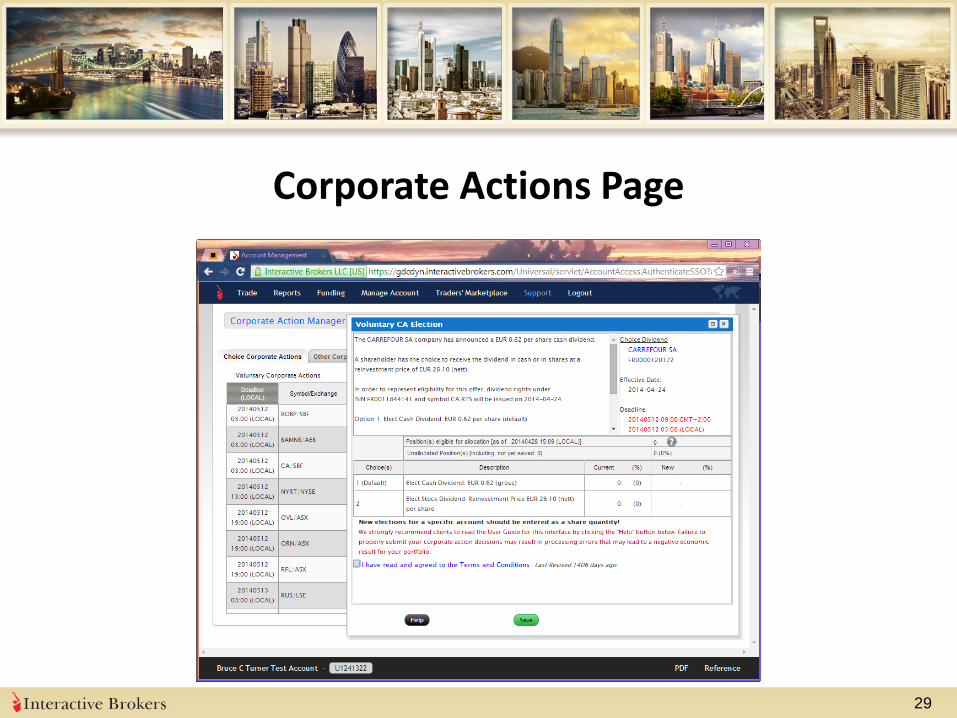

Corporate Actions Page

29

Corporate Action Tool

• Each notification is displayed on a separate line along with View and Allocate links in the Action column

• Click View to display details and a full description of the corporate action

• Click Allocate and the Voluntary CA (Corporate Actions) Election box will appear

30

Corporate Action Tool

• The Voluntary CA Election box contains: – Description – Provides term details on the action – Summary — Provides a quick snapshot of the relevant

dates on the action, including corporate action type, security information, effective date of the action and the deadline for submitting instructions on the account

– Position – Provides a summary of the current position in the account as well as the number of shares currently unallocated to the voluntary offer

31

Corporate Action Tool

32

Corporate Action Tool

• Voluntary CA Election box also contains the choice table, which shows: – Description of the option available – Elected position (%) – reports the quantity of shares

previously submitted to the option as well as that quantity as a percentage of the current available position

– New election (%) – field in which you enter the number of shares you wish to submit to the option

33

Corporate Actions Tool

• To allocate shares in a voluntary corporate action or mandatory action with choice, enter the number of shares to allocate in the New Election field. The quantity you enter is added to any previously allocated shares.

• Unallocated shares will be allocated to the default choice.

34

Corporate Actions Tool

After you allocate shares: • Click the check box, then click Save • IB will send confirmation to the Customer Service

Message Center within 30 seconds of accepting your submitted choice

• If you do not receive confirmation, contact IB immediately as non-confirmed elections are not processed

35

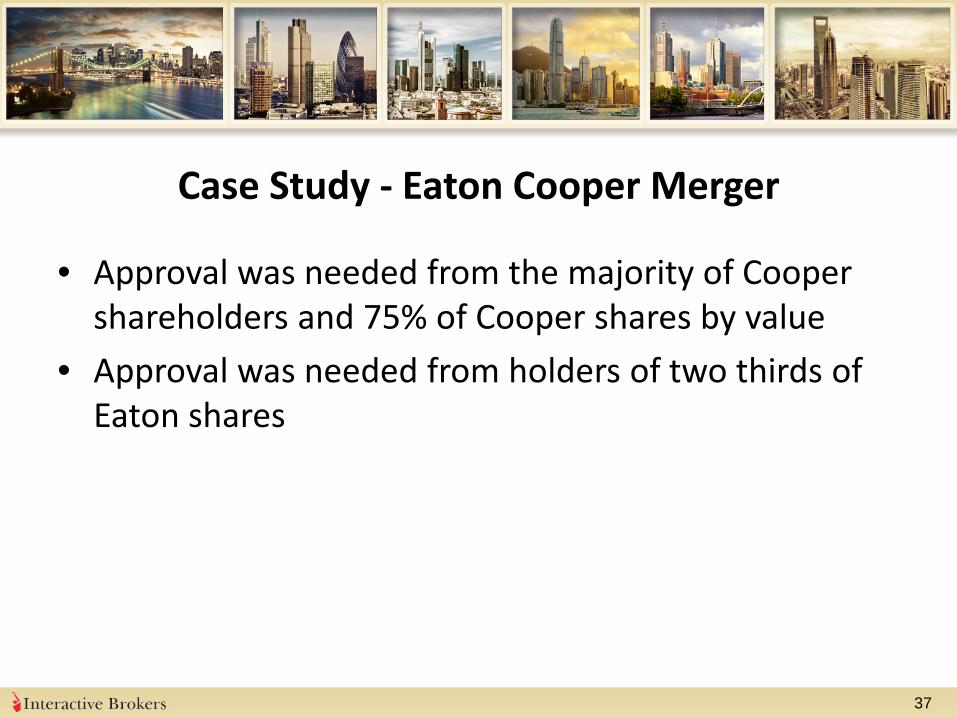

Case Study - Eaton Cooper Merger

• May 21, 2012 Eaton Corporation (ETN) announced that it would combine with Cooper Industries plc. (CBE)

• Cooper shareholders to receive $39.15 plus 0.77479 shares of Eaton for each share of Cooper – Value of $72 per share of Cooper based on the previous

closing price of Eaton

36

Case Study - Eaton Cooper Merger

• Approval was needed from the majority of Cooper shareholders and 75% of Cooper shares by value

• Approval was needed from holders of two thirds of Eaton shares

37

Case Study - Eaton Cooper Merger

• Eaton’s share price dropped from $42.40 to $42.09 on the day of the announcement

• Cooper’s share price was up to $69.88 from $55.84 on the day of the announcement

• The merger took place on November 30, 2012 • How’s it working out?

– Eaton closed at $52.16 on November 30 – Consideration of $79.56 per share of Cooper

38

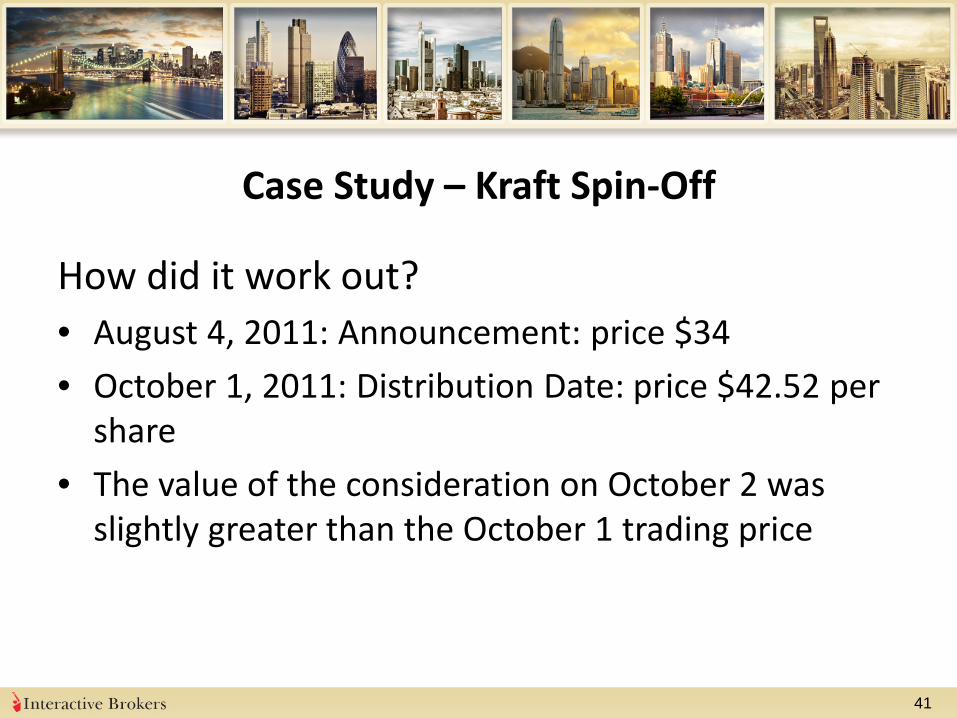

Case Study – Kraft Spin-Off

• On August 4, 2011 Kraft Foods announced that it would create two independent companies: – One for the high growth global snacks business – One for the high margin, more consistent North American

grocery business

• Kraft traded at lower P/E than competitors • Kraft hoped that by separating the two businesses,

the market would increase the valuation

39

Case Study – Kraft Spin-Off

Transaction: • Kraft transferred its domestic business to a sub

named Kraft Foods Group, Inc. • Kraft distributed 1 share of Kraft Foods Group, Inc.

(KRFT) for 3 shares of “old” Kraft (KFT) • Old Kraft changed name to “Mondelez International”

and ticker symbol to MDLZ

40

Case Study – Kraft Spin-Off

How did it work out? • August 4, 2011: Announcement: price $34 • October 1, 2011: Distribution Date: price $42.52 per

share • The value of the consideration on October 2 was

slightly greater than the October 1 trading price

41

Dutch Tender Offers

• Issuer announces a tender offer with a price range per share and a total value of stock that it would like to purchase

• Shareholders choose how many shares and at what price in the range to tender

• Issuer determines the lowest price at which it can purchase its desired total value

42

Dutch Tender Offers

• If insufficient shares are tendered at all possible prices, the issuer will purchase all tendered shares at the maximum price

• If too many shares are available at final price, but insufficient shares at any lower price, issuer will purchase shares at the final price on a pro-rata basis

43

Case Study - Amgen (AMGN) Tender Offer

• November 7, 2011: Announced Tender Offer: – Price range of $54 to $60 per share – Total purchase up to $5 Billion – Offer open until December 7, 2011 for up to $5B of

common stock for between $60 per share and $54. Open until December 7, 2011

• Offer was oversubscribed, but at top of range • Amgen purchased $5B at $60 per share pro rata

among tendered shares 44

Case Study - Amgen (AMGN) Tender Offer

How did it work out? • Closing price day before announcement: $55.17 • Closing price day of announcement: $58.43 • Closing price on December 7, 2011: $58.34 • By the end of 2011, AMGN shares traded at over $64

45

Case Study - Jarden Corporation (JAH)

• Jan 24, 2012 Jarden announced that a tender offer of up to $500 million in shares at a price between $30 and $33 per share. The offer was to be open until Feb 23, 2012 – The closing price on the day before the announcement

was $30.71. The stock closed at $33.79 on the day of the announcement

– Very few shares were tendered, because shareholders could get a higher price in the open market

46

Case Study - Jarden Corporation (JAH)

• Feb 21, 2012 Jarden updated its offer: – New Price range of 32 to 36 dollars per share – Deadline extended to March 5, 2012 – The closing price on the day before the new

announcement was $34.51. The stock closed at $35.26 on the day of the updated announcement

• How did it work out? – The closing price on March 5, 2012: $35.76 – By the end of March, shares traded for over $40

47