wealth planning and management

TRANSCRIPT

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 1/28

Wealth Planning and Management

for an Individual

Subject: Personal Wealth Management

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 2/28

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 3/28

Personal Wealth Management Page 3

Table of Content

I. Introduction .......................................................................................................................................... 4

II. Personal Wealth Management for an Individual .......................... ........................... ........................... ... 6

Individuals Personal Profile .......................... ................................ ....................... ................................ 6

Financial Goals (as on December 2010) ............................................................................................ 7

Asset Liability Statement (as on 1st

December2010) ................................... .............................. ....... 8

Expenses Statement ............................. .......................... ............................ ................................ .... 10

Actions to be taken ........................................................................................................................ 11

Financial Ratios .............................................................................................................................. 12

III. Questionnaires ................................................................................................................................. 13

1. Analyzing the Financial Attitude ........................... ................................ ...................... ................ 13

2. Analyzing the Financial values ......................... ................................ ...................... ..................... 14

3. Analyzing the Risk Appetite of the individual ........................... .......................... ............................. 16

4. Risk Tolerance Questionnaire ......................... ................................ ...................... .......................... 19

5. Investment Objectives ................................................................................................................... 21

6. Whats your Money Attitude? ....................... ................................ ....................... .......................... 22

7. Identifying your Financial Needs (Inflation & Returns) ........................... ........................ ................. 23

8. Debt Self-Assessment ........................... ................................ ...................... ................................ .... 24

9. Are You An Over-Spender? ........................ ................................ ...................... ............................... 25

10. Emergency Fund Questionnaire ................................................................................................... 26

IV Recommendations & Suggestions ........................... ................................ ...................... ..................... 27

References............................................................................................................................................. 28

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 4/28

Personal Wealth Management Page 4

I. Introduction

What is Wealth??

Wealth is defined as the present value of all the future cash flows that are expected to flow in

from one¶s assets including both financial and real assets.

In lay man terms, wealth can be defined as generating an adequate amount of income, which

ensures meeting the various living and leisure expenses.

Wealth Management

Wealth management is defined as an all inclusive service to optimizes, protect and manage the

financial goals of an individual, household or a corporate. It includes the following parameters:

y Current Lifestyle needs

y Income Tax Considerations

y Inheritance goals

y Humanitarian pursuits

Phases in Wealth Management Process

UnderstandingOpportunities and

Issues

Planning WealthManagement

Strategy

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 5/28

Personal Wealth Management Page 5

Objective of the Study

This project aims at learning various aspects of wealth management by carrying out a study of

the chosen client and advising him on his wealth planning. The objective of the assignment is to

create the wealth statement of Mr. Amit Kumar Yadav and to advise him on the various

investment avenues available. Also the objective of the study was to get insights into the

practical aspects of Personal Financial Planning and carefully manage the future increased need

for funds.

Methodology

First of all, all the personal details of the client along with knowing his goals both ± long and

short term were studied. The preparation of the financial statement of the client was very

essential in order to have a clear view of his assets, liabilities, expenditures, cash flows etc. After

this risk profiling based on various factors such as his age, current income, number of

dependants and various other factors is done so as to determine the investment pattern for the

client.

After that all the measures adopted by the client in case of contingencies were taken into

consideration. After this, suggestion on selection of which asset classes like real estate, debt,

equity, arts and collectibles etc are suggested to the client for effective financial planning as per

his goals and risk profile.

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 6/28

Personal Wealth Management Page 6

II. Personal Wealth Management for an

Individual

Individuals Personal Profile

Name of Individual Mr. Amit Kumar Yadav

Designation VP, DLF Ltd

Business Real Estate

Office at DLF Square, Gurgaon

Spouse Housewife

Sister Married

Family( Name, Age, Relation,

Dependent/Working)

Mr. Rajesh Yadav, 58, Father, Working

Ms. Sushila Yadav,55, Mother, Dependent

Mr. Amit Yadav 33, Self, Working

Ms. Deepali Yadav, 31, Wife, Dependent

Abhishek Yadav, 9, Son, DependentAtul Yadav, 7, Son, Dependent

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 7/28

Personal Wealth Management Page 7

Financial Goals (as on December 2009)

Short Term Goals( 1 year or less)

G oal Priority Target date Cost estimate (Rs)

Pay off Debt High December, 2011 10 lacs

Buy Mediclaim for all High January, 2011 20,000

Change cell phone Low March, 2011 25,000

Trip for parents Medium June, 2011 2 lacs

Diwali gifts Medium October, 2011 2 lacs

Intermediate Goals( 2-5 years)

G oal Priority Target date Cost estimate

Buy Another car Medium January 2012 2 lac (Rs. 7 lac on

installments)

House Renovation Medium September¶2012 3 lacs

Acquisition of

Consumer Durables

High September¶ 2012 2 lacs

Long Term Goals( 5+ years)

G oal Priority Target date Cost estimate(INR)

Elder son¶s graduation

education

High March, 2019 5 lacs

Younger son¶s

graduation education

High March, 2021 6 lacs

Elder son¶s foreign

education

High March, 2022 15 lacs

Younger son¶s foreign

education

High March, 2024 17 lacs

NewHouse High January, 2026 2 crores (5 crores with

3 crores housing loan)

Marriage of elder son Medium January, 2028 50 lacs

Marriage of younger

son

Medium January, 2029 50 lacs

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 8/28

Personal Wealth Management Page 8

Asset Liability Statement (as on 1st December2009)

Assets

Liquid Assets

Account balance (Savings @

4%)

50,000

Fixed Deposits (@ 8.5%) 3,00,000

Cash value of Life Insurance 50,000

Money market mutual fund

(@ 15%)

2,20,000

Total liquid assets 6,20,000

Real Estate

Plots in Gurgaon 5,00,00,000

Shop in Gurgaon 1,50,00,000

Current market value of

home

1,25,00,000

Greater Noida¶s plot 35,00,000

Total real estate 8,10,00,000

Personal Possessions

Market Value of Vehicles 5,00,000 + 2,50,000

Furniture and Appliances 5,00,000

Stereo and Video Equipment 25,000

Home Computer 25,000

Jewellery (Gold) 50,00,000

Total Household Assets 63,00,000

Investment Assets

Retirement Accounts (PPF) 2,00,000

RBI Bonds (@ 8%) 7,50,000

Gold Bees 5,00,000

Equity 20,00,000

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 9/28

Personal Wealth Management Page 9

Equity Mutual Funds 2,50,000

Total Investment Assets 37,00,000

Total Assets 9,16,20,000

Liabilities Current Liabilities

Personal Loan 10,00,000

Balance due on Auto Loan 3,00,000

Total Current Liabilities 13,00,000

Long-Term Liabilities

Nil

Total Liabilities 1300000

Net Worth (Assets minus

Liabilities) 9,03,20,000 ( 9 crores, 3 lacs

and 20 thousand)

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 10/28

Personal Wealth Management Page 10

Expenses Statement

Item Monthly Yearly Annual Tota

Food/Grocery 15,000 1,80,000

Electricity / Gas 4,000 48,000

Telephone 2,000 24,000

Mobile 5,000 60,000

Water 500 6,000

Personal Loan Interest 10,000 1,20,000

Car installment 12,000 1,44,000

Gasoline 15,000 1,80,000Shopping 7,000 50,000 1,34,000

Entertainment 12,000 50,000 1,94,000

School fees 6,000 72,000

Medical 2,500 20,000 50,000

Club fees/Gym 3,000 36,000

Gifts / Others 50,000 50,000

Personal Care 2,000 24,000

Life insurance premium 20,000 20,000

Car Maintenance 1,000 12,000

Car Insurance 16,000 + 5,000 21,000

Domestic Servant 2,000 24,000

Driver 4,000 48,000

Colony Security Guard 500 6,000

Car Cleaner 200 2,400

Newspaper 150 1,800

Miscellaneous 5,000 60,000

Total 15,20,800

Average monthly expenses 1,26,600

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 11/28

Personal Wealth Management Page 11

Actions to be taken

Action table

Goal Amt Time

available

(month

s)

Investment

required (if expenses met

through

monthly

savings)

Suggestion to meet the goal

Short Term Goals

Personal debt 10 lacs 12 83333 Revoke FD for 3 lacs

Transfer monthly 58000 in MoneyMarket Mutual Fund

Mediclaim 20000 1 20000 Monthly transfer to savings a/c

Cell phone 25000 3 8000 Monthly transfer to savings a/cTrip for parents 20000

0

18 11111 Monthly transfer into Money Market

Mutual Fund

Diwali gifts 200000

9 22222 Monthly transfer to Money MarketMutual Fund

Medium Term Goals

New Car 2 lac 12 8333 Meet though savings

House renovation 3 lacs 19 15800 Meet though savings

Consumer durables 2 lacs 19 10526 Meet though savings

Long Term Goals

Elder son¶sgraduation

education

5 lacs 100 5000

Younger son¶s

graduation

education

6 lacs 124 4838

Elder son¶s foreign

education

15 lacs 136 11000

Younger son¶s

foreign education

17 lacs 160 10625

NewHouse 200

lacs

184 110000 Sell existing house

Marriage of elder

son

50 lacs 196 25500

Marriage of

younger son

50 lacs 208 24000

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 12/28

Personal Wealth Management Page 12

Financial Ratios

Ratios Formula Calculation Remarks

Debt Ratio Liability/Net Worth 0.01439 Very good, Quite safe andhas negligible Liabilities

w.r.t. Net Worth

Current

Ratio

Liquid Asset/Current Liability 0.47692 Not very good, ideally

should be around 1:1

Liquidity

Ratio

Liquid Asset/Monthly Expenses 4.897314 Healthy, monthly expenses

not very high

Debt Asset

Ratio

Total Liabilities/TotalAssets*100

1.418904 Decent but can be improvedupon

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 13/28

Personal Wealth Management Page 13

III. Questionnaires

1. Analyzing the Financial Attitude

Statements : Options

I need more money than I can use Yes No

It bothers me when I discover I could have gotten the same thing

for less somewhere else.

Yes No

Ibehave as if money were the ultimate symbol of success. Yes NoI show signs of nervousness when I don¶t have enough money. Yes No

I dream I will one day be fabulously rich. Yes No

I find it difficult to part with money for any reason. Yes No

I worry that I will not have enough money to live comfortably

when I retire.

Yes No

Money controls the things I do or don¶t do in my life. Yes No

When I was a child, money seemed to be the most important

thing in my life.

Yes No

I argue or complain about the cost of things. Yes No

Scoring: Count the number of µYes¶. This determines the degree to which money controls your

life.

Financial attitudes are measure of one¶s state of mind, opinions and judgment about money in the

world in which they live. They reflect a position he/she has taken with the values inherent. This

gives a slight idea of the degree to which money controls your life. The number of ³yes´ in the

replies in Mr. Yadav¶s case indicates that impact or influence of money in your life is ³high´; the

same can be attributed to the stage of life cycle in which he falls. A young ambitious

professional with tons of dreams is what describes him best. Thus he wants to be able to

spend on the necessities as well as some luxuries of life.

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 14/28

Personal Wealth Management Page 14

2. Analyzing the Financial values

³If you had an extra Rs.2 lac, on which one of the two items (in each row) would you spend

your money?´ You must make one choice in each pair.

S.No. Option 1 Option 2

1 Housing (DreamHome) Investments/Retirement Savings

2 Education: Self/Others Vacation/Travel

3 Retirement Savings/Investment Hobbies/Sports

4 Hobbies/Sports Charitable Giving/Religious Activity

5 Vacation/Travel Personal Appearance/Grooming/Clothes

6 Charitable Giving/Religious Activity Social Activities/Eating Out

7 Social Activities/Eating Out Car

8 Housing (DreamHouse) Retirement Savings/Investments

9 Education: Self/Others Housing (DreamHouse)

10 Hobbies/Sports Housing (DreamHouse)

11 Personal Appearance/Grooming/Clothes Car

12 Charitable Giving/Religious Activity Social Activities/Eating out

13 Retirement Savings/Investment Hobbies/Sports

14 Personal Appearance/Grooming/Clothes Vacation/Travel

15 Hobbies/Sports Car

16 Retirement Savings/Investments Social Activities/Eating Out

17 Housing ( Dream House) Vacation/Travel

18 Education : Self/Others Car

19 Vacation/Travel Charitable Giving/Religious Activities

20 Personal Appearance/Grooming/Clothes Education: Self/Others

The responses changes so drastically with the stage in life cycle, as far as Mr. Yadav is

concerned. He places his kids in the first place, he compromises nowhere where kids are in

picture, there health and education is what occupies first place in each of his responses.

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 15/28

Personal Wealth Management Page 15

Values are relatively permanent personal beliefs about what you regard as important, worthy,

desirable or right. Values tend to reflect your upbringing or other important events, and change

very little without conscious effort over a lifetime. These values are reflected in your attitude

and the more harmonious your values, attitudes and goals will be the greater will the likelihood

of attaining them.

Values are beliefs or ideas that you consider import or desirable. Everyone has values, but

everyone does not value the same things equally

Number of times you circled each item in the pair activity:

Car 3

Charitable Giving 2Education 4

Hobbies/Sports 0

Housing 4

Personal Care 1

Retirement 3

Social 1

Travel 2

Quite substantiating the personal goals are the responses in the questionnaire, the dream home

to accommodate the growing family in future together with education for children is what

concerns Mr. Yadav.

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 16/28

Personal Wealth Management Page 16

3. Analyzing the Risk Appetite of the individual

i) Your Age is

(1) Under 25

(2) 25 ± 30

(3) 31 ± 50

(4) 51 ± 65

(5) Over 65

ii) What is you working status?

(1) I have a job

(2) I am a businessman

(3) I am practicing professional

(4) I am retired

(5) I am presently without a job

iii) Since how long?

(1) Less than a year

(2) Since 2 ± 3 years

(3) Since 3 ± 5 years

(4) More than 5 years

iv) How many dependents do you have?

(1) 0(2) 1 ± 2(3) 3 ± 4

(4) Above

v) Do you own your home?

(1) Yes

(2) No

vi) What are you savings as a percentage of your annual earnings?

(1) Under 10%

(2) 10% - 25 %

(3) 25% - 40%

(4) 40% - 50%

(5) Above 50%

vii) What is your present investment pattern?

(1) Only in fixed income such as bank deposits, PPF, etc

(2) Mainly in fixed income and a portion in debt and equity mutual funds

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 17/28

Personal Wealth Management Page 17

(3) Mainly in equity mutual funds

(4) Mainly in direct equity

viii) Are you satisfied with the returns you are getting on your existing investments?

(1) Unsatisfied ± too low

(2) Somewhat satisfied

(3) Satisfied

(4) Satisfied ± but too high for comfort

ix) What is the situation of your wealth build-up?

(1) No wealth built up

(2) Very little wealth built up

(3) Build up is satisfactory

(4) Build up is very satisfactory

x) Usually, how much of your total investment do you invest in single scrip? (in share of

one company)

(1) Less than 10%

(2) About 15% - 30%

(3) About 30% - 50%

(4) More than 50%

(5) I don¶t generally invest in equity

xi) A few years ago you bought shares of a reputed company. The company experienced

a severe decline in profits and the share price dropped drastically. You sold at a

substantial loss. The company has restructured and most experts expect its shares to

produce better than average returns. Would you buy the shares now?

(1) Definitely

(2) Probably yes(3) Probably not

(4) Definitely yes

(5) I don¶t invest in equity

xii) What is your approach in making final decisions?

(1) Make a quick decision based on information received

(2) Make a decision after validating information received

(3) Make a decision after validating information received and collecting additional

information

(4) Usually make a decision after tremendous pondering and speaking to almost all

the people I know

xiii) You personally know a company's promoters. The company is expected to do

extremely well. The promoters themselves say that they have put in all their personal

wealth behind the company and its stock. Would you invest? If yes, to what extent?

(1) I would invest a significant and meaningful amount in the scrip

(2) I would invest an amount that I would have regularly invested in a single scrip

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 18/28

Personal Wealth Management Page 18

(3) I would invest a very modest amount

(4) I would not invest in the scrip

xiv) When you think of the word 'risk' in a financial context, which of these options

come first to your mind?

(1) Thrill

(2) Opportunity

(3) Uncertainty

(4) Danger

xv) With investments such as fixed deposits, the money value of the deposits remains

fixed but inflation lowers the purchasing power of this money. With other types of

investments, such as shares or property, the money value is not fixed and may even

fall below investment amount in the short term. However over the long term, the

money value should certainly increase by more than the rate of inflation. With this in

mind, which is more important to you? The money value of your investments should

remain fixed even though the purchasing power may fall or that it retains its purchasing power?

(1) It is much more important that the money value retains its purchasing power

(2) It is somewhat more important that the money value retains its purchasing power

(3) It is somewhat more important that the money value does not fall

(4) It is much more important that the money value does not fall

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 19/28

Personal Wealth Management Page 19

4. Risk Tolerance Questionnaire

Please indicate which of the following statement best describe your attitude towards

investment volatility.

Capital preservation is of critical importance to me and I am looking at low-risk

investment options.

I am more concerned with preserving capital than maximizing capital gains and I

can tolerate infrequent moderate negative returns in a market cycle for the

potential of consistent average returns

I understand that pursuing higher returns means that I may have to tolerate several

quarters of negative returns through difficult phases in a market cycle.

My main concern is maximizing capital gains and it can tolerate more than one

year of negative returns, through difficult phases in a market cycle, for the potential of higher returns.

How much of an unrealized loss of capital are you prepared to tolerate in your

investments?(Please tick one box only)

Zero

Less than 10%

Between 10 % and 20%

Between 20% and 30 %

Between 30 % to 50%

More than 50 %

How would you like to classify your investment style?

Conservative

Moderate

Aggressive

In terms of a hypothetical portfolio that runs for a period of five years, what is it that

you will be most comfortable with?

Portfolio A: +80% -50% +70% -25% +60% +60% (CAGR: 20%)

Portfolio B: 25% 25% -5% 30% -10% 15% (CAGR: 12%)

Portfolio C: 30% 40% -25% 30% 50% -20 % (CAGR: 14%)

Portfolio D: 8% 9% 7.5% 8% (CAGR 8%)

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 20/28

Personal Wealth Management Page 20

If a holding that forms a significant part of your investment portfolio if you were to

lose 25% of its value what would be your reaction?

Should not happen as I wish to have a lower stop loss limit

Sell immediately and cut losses if it continues to fall in Price.

Assume that there is a problem and would want to find out the reason, based on

which I may want to exit the stock or add to my holdings

Hold on and hope to sell it once it breaks even.

Buy more and bring down the average holding cost believe in the holding

My experience with investing so far has been:

Mainly low- risk debt investments- can¶t remember anything adverse

Mainly low- risk debt investment- there has been a few default/ delays.

Mainly debt investments- comfortable experience so far

I am wary of equity investing- it has been a losing experience

Iwant to be in equities- have not got it right so far

I invest in equities- I know what it takes

As a rule, there is a correlation between risk and return. Higher the return potential,

higher is the risk assumed. Within the framework of your investment objective, which

among the following would apply to you the most?

I do not like risk and am in no mood to jeopardize my capital at any point in time.

Certain risks are worth taking in order to achieve higher but I wish to limit the

potential downside.

Certain risks are worth taking if they are well-understood and but I wish to be

comfortable with the worst case scenario. I am comfortable with taking risks as long as they do not jeopardize my core

investment objectives and cash flow requirements

\

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 21/28

Personal Wealth Management Page 21

5. Investment Objectives

Which of the following are possible investment motives for you with regard to this

portfolio?

Keeping aside money generated from business/ profession to specify generate

alternate sources of income or wealth.

Wealth creation, with no alternative use for the money in the foreseeable future.

Wealth creation after accounting for inflation and tax.

Regular income to meet present commitments and expenses.

Building a corpus to meet specific future requirement

What is your investment horizon?

Upto 6 months

Upto 1 year

Upto 3 years Upto 5 years

Upto 10 years

Beyond 10 years

For generating liquidity requirements or to meet an unforeseen payment obligation.

You have sufficient liquidity outside of the portfolio to dip into

You envisage drawing from this portfolio meet the payment requirement of to

bridge the gap

How is your familiarity and experience with investments?

Familiar and experienced

Not too familiar but experienced

Not familiar and inexperienced

Your idea of a comfortable debt portfolio is

Fixed coupon, fixed maturity instrument with no volatility in any market

conditions

Variable return debt instrument to exploit inherent tax efficiencies in them, but

you understand that these instruments carry a price risk

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 22/28

Personal Wealth Management Page 22

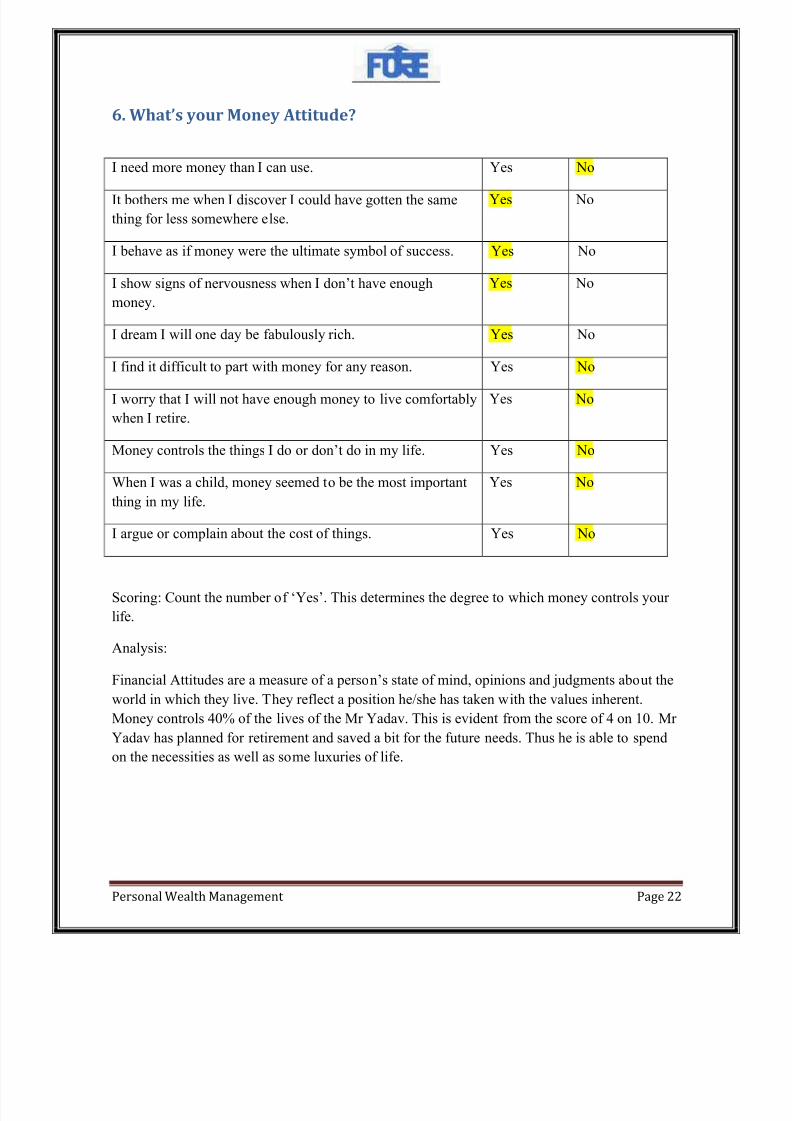

6. Whats your Money Attitude?

I need more money than I can use. Yes No

It bothers me when I discover I could have gotten the same

thing for less somewhere else.

Yes No

I behave as if money were the ultimate symbol of success. Yes No

I show signs of nervousness when I don¶t have enough

money.

Yes No

I dream I will one day be fabulously rich. Yes No

Ifind it difficult to part with money for any reason. Yes No

I worry that I will not have enough money to live comfortably

when I retire.

Yes No

Money controls the things I do or don¶t do in my life. Yes No

When I was a child, money seemed to be the most important

thing in my life.

Yes No

I argue or complain about the cost of things. Yes No

Scoring: Count the number of µYes¶. This determines the degree to which money controls your

life.

Analysis:

Financial Attitudes are a measure of a person¶s state of mind, opinions and judgments about the

world in which they live. They reflect a position he/she has taken with the values inherent.

Money controls 40% of the lives of the Mr Yadav. This is evident from the score of 4 on 10. Mr

Yadav has planned for retirement and saved a bit for the future needs. Thus he is able to spendon the necessities as well as some luxuries of life.

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 23/28

Personal Wealth Management Page 23

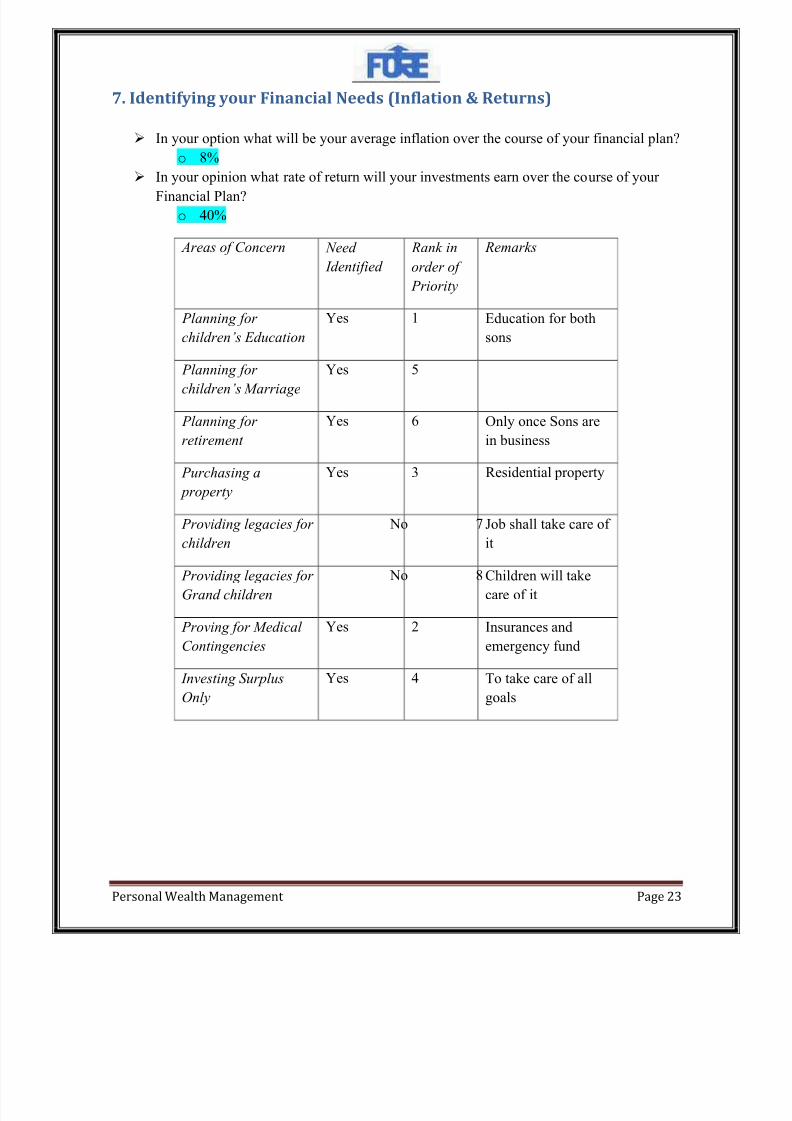

7. Identifying your Financial Needs (Inflation & Returns)

In your option what will be your average inflation over the course of your financial plan?

o 8%

In your opinion what rate of return will your investments earn over the course of your

Financial Plan?

o 40%

Areas of Concern Need

Identified

Rank in

order of

Priority

Remarks

Planning for

children¶s Education

Yes 1 Education for both

sons

Planning for children¶s Marriage

Yes 5

Planning for

retirement

Yes 6 Only once Sons are

in business

Purchasing a

property

Yes 3 Residential property

Providing legacies for

children

No 7 Job shall take care of

it

Providing legacies for

Grand children

No 8Children will take

care of it

Proving for Medical

Contingencies

Yes 2 Insurances and

emergency fund

Investing Surplus

Only

Yes 4 To take care of all

goals

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 24/28

Personal Wealth Management Page 24

8. Debt Self- Assessment

Do you: Reply

Exceed your overdraft limit just before you are paid or

money comes in?

No

Receive unauthorized overdraft letters from the bank? No

Put off opening bank and credit card statements because you

are worried?

No

Borrow more money to temporarily meet existing

borrowing with?

No

Avoid discussions or ignore letters from companies you

have been borrowing with?

No

Have cheques, direct debits or standing orders returned

unpaid?

No

Have arrears on loans or worry about meeting the next

repayment?

No

Have arrears on your mortgage or worry about meeting the

next repayment?

No

Worry that your finances are getting out of your control? No

Worry that without help you will be unable to regain control

of your finances?

No

Situation analysis Healthy, financial planning

to secure achievement of

future goals and maintaining

present comfortablesituation

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 25/28

Personal Wealth Management Page 25

9. Are You An Over-Spender?

Do you shop or spend money as a result of feeling depressed, disappointed, angry,

scared or lonely?

Yes

No

Do you experience emotional distress or chaos in your life due to shopping or

spending habits?

Yes

No

Do you have arguments with others about your shopping or spending habits?

Yes

No

Do you feel lost without credit cards? Yes

No

Do you buy items on credit that would not be bought with cash?

Yes

No

Do you feel a rush of both euphoria and anxiety when spending money?

Yes

No

Do you feel guilty, ashamed, embarrassed or confused after shopping or spending

money?

Yes

No

Do you lie to others about purchases made or how much you have spent?

Yes

No

Do you think excessively about money?

Yes

No

Do you spend a lot of time juggling accounts or bills to accommodate spending?

Yes

No

This shows that Mr Yadav is not an over spender and spends his money quite judiciously.

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 26/28

Personal Wealth Management Page 26

10. Emergency Fund Questionnaire

Checking Preparedness during an emergency

I II III

Is your job stable? Not at all More or less Completely

How dependent are you on interest,

dividend and capital gains on your investments to cover your regular

expenses?

Totally Slightly Not at all

Do you have life, health, auto and

disability insurance?

Little/No

Cover

Some Risks

Covered

All Risks

Covered

As a multiple of your regular monthlyexpenses(including loan repayments

and insurance premium),how much of your investments are liquid options

like savings account, savings fromdeposit accounts and liquid funds?

15 days 2 months 3 months

What is the percentage of regular income generating assets to your net

worth?

0-5% 6-15% Over 15%

Do you have access to comparativelycheap credit like overdraft facilities

against assets like share and home?

No access Limited Access Ample access

Score: I =10, II-20, III-30

Standard Score: >120 - Good

90-120 ± Moderate

<90 - Action needed immediately!

Analysis: The Client score comes at 140.Which is quite good. So we can say that Mr Yadav is

quite well prepared to meet his emergency needs. However he needs planning for Insurance and

liquidity of funds. An emergency fund needs to be built to provide for new addition in the family

as well as any contingencies that arise in the future.

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 27/28

Personal Wealth Management Page 27

IV Recommendations & Suggestions

After studying the financial position and understanding the requirements of Mr Yadav over short,

Medium and long term perspective, following are some recommendations for his financial planning:

1) He should continue investing regularly a fixed percentage of his monthly savings say 20% in to his

savings account

2) Mr Yadav needs to start planning for his retirement, which he currently is not considering. For this, I

suggest he starts investing in liquid instruments such as Post offices instruments (Monthly income

plans), Mutual funds should be made in such a way that he gets the benefit as soon as he nears the age

of 60

3) He must realize that he should have a regular source of income after he himself stops going to

business. For this, he can rent any of his properties and enjoy that income for the rest of his life.

4) Mr. Yadav should go for more of equity route than at present since he has huge investable surplus in

hand which can earn him more returns over the periods of time. The mutual funds are suggested

considering the return and risk grade. The risk grade in all the mutual funds mentioned above is low

and return grade high. The three year returns on the Diversified Equity funds is between 66-83% thus

giving sufficient returns to Mr. Yadav to meet his medium term requirements.

5) Mr Yadav should take health and accident policies for each member of the family. This will protect

the family from any unfortunate event.

8/8/2019 Wealth Planning and Management

http://slidepdf.com/reader/full/wealth-planning-and-management 28/28

References

y Mr. Amit Yadav, Family Friend, 9953557656

y Wealth Management, Dun & Bradstreet

y Class notes and Questionnaires provided by Prof. Vinay Dutta

y www.kotaklifeinsurance.com

y www.moneycontrol.com

y www.tata-aig.com