€¦ · web viewtoday , the ncr . atm solutions is in use exclusively at standard chartered...

TRANSCRIPT

MAKERERE UNIVERSITY

ATM SCHOOL FEES BANKING AND CUSTOMER SATISFACTION IN

COMMERCIAL BANKS IN UGANDA

A CASE STUDY OF STANBIC BANK UGANDA –MAKERERE BRANCH

BY: BALUKU CHARLES MUNDELE

07/U/7283/EXT

B.COM

SUPERVISOR: PASTOR YOEL SHALOM.

A RESEARCH REPORT SUBMITTED TO MAKERERE UNIVERSITY IN PARTIAL FULFILMENT OF THE

REQUIREMENTS FOR THE AWARD OF THE DEGREE OF BACHELOR OF COMMERCE OF

MAKERERE UNIVERSITY

JUNE 2011

DECLARATION

I declare that this Dissertation is a result of my own investigation and it has never been submitted to

any other institution for any reward. Where it is indebted to the work of others, due

acknowledgement has been made.

Signature…………………. Date………………………………….

BALUKU CHARLES MUNDELE

i

APPROVAL

I certify that the candidate was under my supervision. This work was submitted with my approval as

a supervisor for the partial fulfillment of the award of Bachelor of Commerce of Makerere University.

Signature……………………… Date…………………..

PASTOR YOEL SHALOM.

ii

DEDICATION

I dedicate this work to my family members especially my father, mother, brothers and sisters.

Iam gratefull for all the love and care you have given me to make me what iam today.

May the gracious Lord bless you abundantly.

iii

ACKNOWLEDGEMENT

To begin with, I take the pleasure to give special thanks to God Almighty who has been their for me

at all times and to whom I owe everything.

With great gratitude I thank my Supervisor Pastor Yoel Shalom for without his guidance, this work

wouldn’t have been a success.

My Special thanks go to my lecturers for having imparted knowledge and skills in me and the non

teaching staff for having made the environment conducive for studying . May almighty bless you

abundantly.

My heartfelt appreciation goes to my beloved parents, Mr. and Mrs. James Mundele Sunday &

Kabugho Jane, my Sponsur Mr Mads Lofval,Ma Chantal,Uncle Andrew,sister Asiimwe Jane, Kabugho

Carol,Gitter Jacqueline,brother Mugabi Isaac , Mawazo David and everyone who has done all it takes

to make my education a success.

I also owe a great deal of thanks to management and staff of Stanbic Bank Uganda –Makerere

branch especially Mr. Mukwaya the branch manager, staff and customers for having sacrificed their

time amidst their tight schedules to fill my questionnaires. May the Almighty God Bless you

It would also be a disservice to forget not only my group members but also my friends;

Odong .J,Innocent,Maxine,Selina,Silas,Harriet,Boit,Chela,Felistar,Kisang,kibet,Jackie,Justus,Ruto,Anne

t, Martha, Sadhat, Peter and many others with whom we have always shared ideas and experiences.

I will always cherish you for your contribution towards my bright fsuture.

iv

TABLE OF CONTENTS

DECLARATION.................................................................................................................................... i

APPROVAL........................................................................................................................................... ii

DEDICATION...................................................................................................................................... iii

ACKNOWLEDGEMENT..................................................................................................................... iv

CHAPTER ONE....................................................................................................................................1

1.0 INTRODUCTION............................................................................................................................1

1.2 STATEMENT OF THE PROBLEM................................................................................................5

1.3 PURPOSE OF THE STUDY...........................................................................................................5

1.4 OBJECTIVES..................................................................................................................................5

1.5 RESEARCH QUESTIONS...........................................................................................................6

1.6 SCOPE...........................................................................................................................................6

1.6.1 Geographical scope.......................................................................................................................6

1.6.2 Content scope................................................................................................................................6

1.6.3 Time scope....................................................................................................................................6

1.7 SIGNIFICANCE OF THE STUDY.................................................................................................6

1.8) Review section:...............................................................................................................................7

LITERATURE REVIEW.......................................................................................................................8

2.0 Introduction......................................................................................................................................8

2.1.1 Definition of ATMs.......................................................................................................................8

2.1.2 A brief history of ATMs...............................................................................................................9

2.1.3 Benefits of ATM Banking To Customers..................................................................................10

2.1.4 Benefits of ATMs to banks..........................................................................................................11

2.1.5. Challenges of ATMs (Automated teller machines......................................................................13

2.2.0 School Fees Banking...................................................................................................................15

Methods of school fees banking...........................................................................................................16

2.2.1. Cash payment option..................................................................................................................16

v

2.2.2. ATM school fees banking...........................................................................................................16

2.2.3.Electronic Fund Transfer.............................................................................................................16

2.2.4. Mobile payment..........................................................................................................................16

2.3.1 Customer satisfaction..................................................................................................................17

2.3.2 Importance of customer satisfaction............................................................................................19

2.3.3. Measuring customer satisfaction................................................................................................21

2.3.4. Indicators of customer satisfaction.............................................................................................21

2.4.0. Review section..........................................................................................................................23

CHAPTER THREE METHODOLOGYs.............................................................................................25

3.1 Introduction....................................................................................................................................25

3.2. Research strategy and design.........................................................................................................25

3.3. Study Population...........................................................................................................................25

3.4.0. Sampling design.........................................................................................................................25

3.4.1. Sampling size.............................................................................................................................25

3.4.2. Sampling method........................................................................................................................26

3.5.0. Sources of data...........................................................................................................................26

3.5.1. Primary data...............................................................................................................................26

3.5.2. Secondary data...........................................................................................................................26

3.6.0. Data collection methods and instruments...................................................................................26

3.6.1.Interviews....................................................................................................................................26

3.6.2.Questionaires...............................................................................................................................26

3.6.3. Observation................................................................................................................................26

3.7.0. Data presentation and analysis....................................................................................................27

3.7.1.Tabulation...................................................................................................................................27

3.8.0.Data intergrity and validity..........................................................................................................27

3.9.0. Limitations to the study and possible solutions..........................................................................27

3.9.1. Review section...........................................................................................................................28

vi

CHAPTER FOUR................................................................................................................................29

PRESENTATION, ANALYSIS AND DISCUSSION OF FINDINGS................................................29

4.1.0. Introduction................................................................................................................................29

4.1.1 Gender of the respondents...........................................................................................................29

4.1.2: Marital status of respondets........................................................................................................30

4.1.3: Level of education of respondents..............................................................................................31

4.1.4: Age bracket of respondents........................................................................................................32

4.2.0: Usage level of ATM school fees banking...................................................................................34

4.2.1: Banking school fees using ATM...............................................................................................34

4.2.2: Reasons for not using ATM school fees banking.......................................................................36

4.2.3: Categories of customers banking school fees using ATM.......................................................37

4.2.4: Number of times customers bank school fees in a semester using ATM....................................38

4.3.0: Determinants of customer satisfaction........................................................................................39

4.3.1: ATM school fees banking reliability..........................................................................................39

4.3.2: Quality of service......................................................................................................................40

4.3.3: Meeting customer expectations..................................................................................................41

4.3.4: ATM School fees banking reducing bank queues.......................................................................42

4.3.5 : Pride of being a customer of Stanbic Bank Uganda...................................................................43

4.3.6: Response to customer needs.......................................................................................................44

4.4.0: Relationship Between ATM school fees banking and customer satisfaction............................45

4.4.1: ATM school fees banking saves time compared to banking school fees using bank slips in banking hall..........................................................................................................................................45

4.4.2: ATM School fees banking helps customers who are usually busy to bank school fees during banking off hours.................................................................................................................................46

4.4.3: ATM School fees banking at times has not been successful due to several problems associated with malfunction of machines..............................................................................................................47

4.5.0.Review section............................................................................................................................48

SUMMARY OF FINDINGS, CONCLUSION AND RECOMMENDATIONS..................................49

vii

5.0 Introduction..................................................................................................................................49

5.1 Summary of the findings................................................................................................................49

5.2 Conclusion......................................................................................................................................50

5.3 Recommendations.........................................................................................................................51

Objective 3:- To establish the relationship between ATM school fees banking and customer satisfaction...........................................................................................................................................52

REFERENCES.....................................................................................................................................53

viii

LIST OF CHARTS, GRAPHS AND TABLES

Figure 1: A pie-chart showing gender of respondents..........................................................................29

Figure 2: Table Showing gender of respondents..................................................................................30

Figure 3: A pie-chart showing marital status of respondents...............................................................30

Figure 4: Table Showing marital status of respondents.......................................................................31

Figure 5: A pie-chart showing level of education of respondents........................................................31

Figure 6: Table Showing level of education of respondents.................................................................32

Figure 7: A Dough nut chart showing the age bracket of respondents in years...................................32

Figure 8: Table Showing the age bracket of respondents in years.......................................................33

Figure 9: A 3-D Chart showing factors which attracted respondents to Stanbic Bank Uganda..........33

Figure 10: Table Showing factors which attracted respondents to Stanbic Bank Uganda....................34

Figure 11: A bar graph showing ATM school fees banking...................................................................35

Figure 12: Table showing Banking school fees using ATM....................................................................35

Figure 13: A Pie-chart showing reasons why customers d0n’t use ATM school fees banking..............36

Figure 14: Table showing Reasons for not using ATM school fees banking..........................................36

Figure 15: A pie chart showing categories of customers banking school fees using ATM....................37

Figure 16: Table showing Categories of customers banking school fees using ATM..........................37

Figure 17: A bar graph showing number of times customers bank school fees in a semester using ATM.............................................................................................................................................................38

Figure 18: Table Showing number of times customers bank school fees in a semister using ATM.....38

Figure 19: Chart Showing ATM School fees banking reliability.............................................................39

Figure 20: Table showing ATM school fees banking reliability.............................................................39

Figure 21: A bar graph showing the extent of agreement upon high Quality of services rendered by Stanbic Bank Uganda............................................................................................................................40

Figure 22: Table showing Stanbic bank Uganda offers high quality ATM school fees banking country wide......................................................................................................................................................40

Figure 23: A bar showing the extent of agreement upon which ATM school fees banking meets customer expectations in Stanbic Bank Uganda...................................................................................41

ix

Figure 24: Table showing ATM school fees banking meets my expectations.......................................41

Figure 25: A 3D-chart showing the extent of agreement upon which ATM School fees banking has reduced bank queues in the banking hall.............................................................................................42

Figure 26: Table showing ATM School fees banking has reduced bank queues in the banking hall.....42

Figure 27: A pie-chart showing the extent of agreement upon which customers agree to be proud of banking with Stanbic Bank Uganda......................................................................................................43

Figure 28: Table showing Pride of being a customer of Stanbic Bank Uganda.....................................43

Figure 29: A bar graph showing the response of Stanbic Bank Uganda to customer needs................44

Figure 30: Table Showing the response of Stanbic Bank Uganda to customer needs..........................44

Figure 31: A 3D-chart showing the extent to which ATM school fees banking saves time compared to bank slips in banking hall......................................................................................................................45

Figure 32: Table Showing the extent to which ATM school fees banking saves time compared to bank slips in banking hall..............................................................................................................................46

Figure 33: A pie-chart showing the extent to which ATM School fees banking helps customers who are usually busy to bank school fees during banking off hours............................................................46

Figure 34: Table showing the extent to which ATM School fees banking helps customers who are usually busy to bank school fees during banking off hours..................................................................47

Figure 35:A 3D-chart showing the extent to which ATM School fees banking at times has not been successful due to several problems associated with malfunction of machines....................................47

Figure 36: Table showing the extent to which ATM School fees banking at times has not been successful due to several problems associated with malfunction of machines.................................48

x

ABSTRACT

The study was about ATM school fees banking and customer satisfaction in commercial

banks in Uganda. A case study of Stanbic Bank Uganda-Makerere Branch. The main

objectives were:

1. To examine the usage level of ATM in school fees banking.

2 . To establish the determinants of customer satisfaction at Stanbic Bank Uganda- Makerere

Branch..

3. To establish the relationship between ATM school fees banking and customer satisfaction

The research strategy and design was purposive and triangulation in which the study was

based on descriptive research design asnd through triangulation the researcher captured

different opinions of different respondents at different time which enabled him understand

fundamental issues. Both qualitative and quantitative data was used for purposes of drawing

valid conclusion.

The research revealed that afew customers use ATM school fees banking, it also discovered

that Stanbic Bank Uganda had the largest market share compared to other banks because of

the good services rendered.

Finally the researcher discovered that there was a positive relation ship between ATM school

fees banking and customer satisfaction because it saves time.

The researher recommended that Stanbic Bank Uganda embarks on massive advertisement in

media to improve awareness of the sevice.

xi

CHAPTER ONE

1.0 INTRODUCTION

This research is about the contribution of ATM school fees banking and customer satisfaction

in uganda comercial banks.it start with the background of the study,statement of the problem

follows.it also looks at the purpose of the study,objectives of the study,research

question,scope and significance of the study.

1.1 Background of the study

Automated teller machine(ATM) or automatic banking machine(ABM) is a computerised

telecomunication device that provide a client of a financial instituion with access to financial

trransactions in a public space without the need for a cashier,human clerk or bank teller.

(http:/en.wikipedia.org/wik/automated-tellermachine)

According to Peter Rose((1999), describes ATM as a combination of computer terminals,

record keeping systems and a cash vault in one unit, permitting customers to enter the bank

book keeping systems with the plastic card containing personal identification number(PIN) or

purchasing a special code number into the computer terminal linked to the banks

computerised records 24 hours a day.

Huff and Munro (1985), many organisations invest resources in information technology in

order to achieve benefits such as improved customer services, increased efficiency/

productivity and competitiveness.

The ATM was invented by John D. White. “ He told us that he installed the first ATM at

rockville centre .LI the then chemical bank in August 1973 . His design was Patented on may

9 ,1973’(ATM http://www.atmmachine.com/atm-inventor.html)

1

A customer is defined as a person {including corporate body} who buys goods and services

for money.(Cole G.A,1995)

Benjamin (2003) says that as a result, e-commerce has emerged allowing businesses to more

effectively interact with their customers and other corporations inside and outside their

industries .This is what is referred to as electronic banking. Edfy (2003), defines customer

satisfaction as a process through which businesses ensure customer loyalty and non defection

of customers to competitors. Customer satisfaction has business leader’s attention, as it is the

basis for ensuring sustainability in the business.

According to Hesket et-al (1977), the concept that the customer is important in achieving

business success dates back fifty years ago, when business management recognized marketing

as an essential discipline. According to Google search on the internet it reveals various

articles where researchers, practioners and academicians alike demonstrate how successful

companies today evolve their businesses around their customers.

The first ATM in Uganda was brought in by Service and computer industries (SCI/NCR) for

standard chartered bank in 1997. “We can certainly be the prime driving force behind

automated banking transactions in Uganda even today, with close to 90% of ATM market

share. Since installing the ATM in Uganda almost a decade ago, we have been an active

catalyst in the rapid growth in development of convenience banking in the country.”

Mohon.V, explained, SCI’s General manager- sales and marketing

Today , the NCR ATM solutions is in use exclusively at standard chartered bank, Stanbic

bank ,Barclays bank, orient bank, Centenary bank, allied international bank, Tropical bank,

Cairo bank and many other banks in Uganda. ATM school fees banking; is the payment of

2

institutional fees by ATM, or internet-convenient, easy and smart. The following are the steps

used as one makes payment in an ATM machine:

1. Please follow the instructions on the ATM screen by selecting “Bill payment

Education-universities HKIED choose the bill “01” (Tuition, Hostel fee,

Student union fee and caution money)

2. Please enter your nine digit student number as the account number.

3. Remember to retain the ATM receipts for future references.

(http://www.ied.edu.hk/electronic payment)

National bank of India Uganda, adapted the present name in 1993; wholly owned by Stanbic

Africa Holdings Ltd (UK), merged with Uganda commercial bank Ltd in 2002. Stanbic bank

Uganda provides banking services to individuals and small to medium- sized enterprises

through over 71 branches and over 134 ATM across Uganda. Revenue is drawn from products

such as mortgage lending, vehicle and assets finance, bank assurance and transaction products

for example ATM and counter deposits.( www.stanbicbank.com/movingfoward).

Stanbic bank launched ATM and internet fees payment systems to eliminate bank queues

Kampala, 20 Nov 2009. Stanbic bank Uganda (SBU), today announced the launch of ATM

and internet banking platform that will bring speed and convinience to the payment of tuition

fees by parents and students at Makerere university.(http://

www.stanbicbankingug.com/pressrelease/pressrelease-ATMinternet)

The new ATM is expected to add SBU ever growing demand driven stable of top quality

financial services and products. Notably, the service also underlines SBU’s leadership not just

in industry profitability but also innovation a crutial factor in achievement of efficient and

3

effective banking service. ( http://www.stanbicbankingug.com/pressreleases/pressrelease-

ATMinternet)

Mr . Paul Omara, Head of distribution ,personal and business banking (PBB) Said, Stanbic

bank strives to keep a head of the market through the use of dynamic human resource to

create products and services that meet the market demand. Over the recent past it has become

clear that our customers needed a system that would enable them to use careful thought and

dedicated work , we now have this wonderful product.”

(http://www.stanbicbankingug.com/pressreleases/pressrelease-ATMinternet)

Mr . Paul Omara adds that earlier on we also introduced internet banking to provide our

customers with yet another alternative and convinient channel to conduct their banking

without having queue in their branches. With internet banking our customers are able to pay

utility bills. (e.g electricity,water,dst v e.t.c),pay school fees, view and print the account

statement and make money tranfers between stanbic accounts.it a fast,safe and convenient

way to conduct bussiness via internet.this is also available to the university in addition to the

ATM-channel.(http://www.stanbicbankingug.com/pressreleases/pressrelease-

ATMinternet)

Omara added that MUK would act as a pilot site and that if service up take is reasonably

impressive, then their would be a roll out into other institutions. MUK students and parents

can now visit any of the SBU branches and obtain brochures on how to use the system. SBU

has 148 ATMs country wide, the biggest network of any bank, and a parent/student can use

any of them.

(http://www.stanbicbankingug.com/pressrelease/pressrelease-ATMinternet)fully

4

1.2 STATEMENT OF THE PROBLEM

Stanbic has not only retained all the branches of UCB, it has improved its service quality and

out reach. They have also successfully introduced ATMs throughout their branch network

which has substancially increased convenience and reduced transition costs. (Anual bankers

report by Mr. Tumusiime Mutebile, Governor Bank of Uganada, 14 March 2005 Speke

Resort Munyonyo.)

According to Mr Paul Omara,Head of Distribution,Personal and Business Banking,PBB,

ATM transaction cost shs.700 while normal transactions over the counter cost shs.2500 each.

(http://allafrica.com/stories/2009//230535.html), (23 November Daily Monitor) Despite

the efforts of stanbic bank to introduce ATM banking, the level of customer satisfaction is

still low as shown by the long queues, this could be due to inadequate ATM only 148 in the

country compared to the population of about 33,000,000. Makerere University alone, has

total population of approximately 40000 people but only has 2 ATMs. If this continues the

company may fail ultimately. This inspired the researcher to analyze the relationship between

ATM school fees banking and customer satisfaction.

1.3 PURPOSE OF THE STUDYThe study was conducted to establish the contribution of ATM school fees banking on the

customer satisfaction in Ugandan commercial banks using Stanbic Bank Uganda – Makerere

branch as a case study.

1.4 OBJECTIVES1. To examine the usage level of ATM in school fees banking.

5

2 . To establish the determinants of customer satisfaction at Stanbic Bank Uganda- Makerere

Branch..

3. To establish the relationship between ATM school fees banking and customer satisfaction.

1.5 RESEARCH QUESTIONS

1. How has the ATM school fees banking affected the rate of customer turn over?

2.What are the determinants of customer satisfaction at Stanbic Bank Uganda –Makerere

Branch?

3. What is the relationship between ATM school fees banking and customer satisfaction?

1.6 SCOPE

1.6.1 Geographical scopeThe study was conducted at SBU ltd, Makerere branch, Kampala district. It also covered some

of the customers (students and parents)who visited the bank during the time of data collection.

1.6.2 Content scopeThe study looked at electronic banking (ATM school fees banking) and how it is linked to

customer satisfaction. The study also found out what customer satisfaction actually means and

what it involves.

1.6.3 Time scopeThe researcher collected and analysed data from January to June 2011.

1.7 SIGNIFICANCE OF THE STUDY1. The research will enable the banking industry to know whether to invest more or less

information technology(ATM) to improve customer satisfaction. 6

2. The result of the research will enable management to establish the attitude of users of the

ATMs and therefore will be able to act accordingly.

3.To scholars and other researchers, the findings will be used for reference through providing

fresh insight for future research.

4. To the researcher it will act as a partial fulfilment for the award of a bachelor of commerce

degree from Makerere University Kampala.

1.8) Review section:If i had to do chapter one again; i would consider the following objectives:-

a) To establish the number of people who use ATM school fees banking as a means of

paying tuition.

b) To establish if ATM school fees banking is user friendly.

c) To establish the time taken in ATM school fees banking compared to banking over the

counter.

Future researchers are encouraged to undertake the above.

7

CHAPTER 2

LITERATURE REVIEW

2.0 Introduction

This chapter contain salient issues in existing published literature on the effect of electronic

banking (ATM banking) on customer satisfaction in commercial banks of Uganda. It has been

carefully selected from publisbed journals or internet, text books and other relevant

pressentation made outside Uganda.

2.1.1 Definition of ATMsAn ATM is simply a data terminal with two input and four output devices. Like any other data

terminal the ATM has to be connected and communicate through a host processor which is

analogous to an internet service provider in that it’s the getaway through which all various

ATMs network become available to the card holder (Byaruhanga 2001).

The Uganda banker (1999) explains ATMs as specialized computer terminals which are

continuously on line connected to the banks central computer to provide a number of facilities

According to the bureau of statistics of United States (2001), automated teller machine allows

customers to carry out bank transactions without the assistance of the teller. ATMs are a

cornerstone of self-service banking. They give vending-machine convenience to customers to

the effect and withdrawals of cash-transactions that have historically played a key role in the

banking branching decisions (lipis 1985).

8

According to zambara (1999), commercial banks introduced ATMs in order to avoid mistakes

of manual systems, improve on security of both the bank and their customers, reduce the time

taken for customers to finish a transaction and increase the banking time of their customers.

2.1.2 A brief history of ATMs

ATMs have been around almost a quarter of a century ,but this”especially double fees”,for

using them are more recent phenomenon

ATMs were introduced in the 1970’s, they where set up only inside or immidietlly outside

their bank branch offices. They were seen by banks largely as a way of saving money, by

reducing the need for tellers. Even with the relatively expensive computer technology of the

late 1970’s and 80’s, the cost of processing deposits and withdrawals via ATMs proved to be

less than the cost of training and employing tellers to do the same work.

To encourage customers to embrace the technology and overcome their trepidations about

putting their checks into machine’s slot rather than a teller’s hands,banks originally didn’t

charge customers any fees for using ATMs.(Indeed, in time, some banks started charging

customers for not using ATMs,through so called “human teller fees”-a charge for each time a

customer uses a teller for a service that could be performed by an ATM).Banks that embraced

the ATM profited handsomely, often growing far faster than old- fashioned banks.

Some banks realised that many people were essentially hooked on ATM and would be willing

to pay some small amount of money to use them, especially when they were travelling. The

banks were fortunate that this period coincided with an era of high anxiety about crime and a

fear of carrying around large amounts of money. Consequently, a number of banks slowly

began to charge fees.

9

According to the U.S. office of Thrift supervision, an ATM transaction costs the ATM owner

about $0.27, including the amortized cost of the equipment,the telecommunication costs, and

the personnel to oversee the operation. However,as of 1998,the average “foreign”fees was

$1.20.of that 10c (the “switch”fee) typically went to the network operators.

http://www.stopatmfees.com/newpage3.htm

A research was conducted about ATM usage; The respondent were read a number of

statements and asked to agree or disagree with them or say whether the statement applied to

them or not. Out of the total sample, only 16% claimed to know how to use an ATM ,39%

didn’t know to use it and 45% were not sure whether they could use it.

(http://www.fsdu.or.ug/pdfs/Finscope-Report.pdf)

2.1.3 Benefits of ATM Banking To Customers.

1. Credit cards are useful in major cities and luxury hotels but smaller establishments

may not accept them. If you can use a credit card make sure you ask about the

exchange rate and fees charged. Visa and MasterCard are generally more widely

accepted than any other credit card.Access your account anywhere anytime.

2. Shop at over 29 million merchant establishments worldwide including mail order and

online Internet purchases

3. Marsh (1993) states tht ATMs saves time; one does not need to come to the bank and

wait in a queue or fill some paper work all the times when ones wants to withdral

cash.Ramsay (1999)in his managerial auditing journal ATM are also easy to use. That

is, the machine guides the customer through each step all one has to do is to follow

instructions on the screen. To use the machine the needful convinience is increasingly

catered for by ATMs.10

4. Link accounts to your ATM card for easy access. In addition to your primary account,

you can link three secondary accounts to your AutoBank card at any branch. These

may be another current, call or savings account.

5. You can do your banking 24 hours a day 7 days a week at any AutoBank throughout

Uganda.Goldrick (1994) adds that the averriding perceived benefits of ATMS for the

customers is the atttribute of convinience followed by the perceived benefits of

reliability and suitability,which in effect implies a measure of convinience. They are

also impoertant for their accuracy.

6. You can easily and quickly check the details of your account without visiting a branch

7. If you have been advised to have your PIN reissued at a branch, you are still able to

use your card at an AutoBank until your PIN is changed.

2.1.4 Benefits of ATMs to banksAccording to Rick Roy (1991), the evolutions of ATMs have enabled banks move staff from

man done tasks to more technical areas. This is very important as competition increases and

technology develops very fast. growing competition calls for fast development of products

and services to stay ahead, the fast development of ATM technology has led to reduced costs,

and therefore to increased efficiency in service delivery. The ultimate effect is improved

profitability and increased customer satisfaction.

Tony W(2002) pointed out that ATM provides the bank an opportunity to serve customers

and market them without physically open. Marketing and advertising material can be

positioned to acquire new customers, allow for existing to apply for new products. The bank

is able to obtain a lot of information regarding customers on their ATM account usage and

11

once gets used to transacting with the bank at any time of the day, or from anywhere it give

the bank a loyal customer hence adding value to the service.

According to Peter Zorkoczy Nicholas (1995), states that “one solution has been the

introduction of ATMs, customers arranging payment and transfer over the computer networks

rather than at the counter”. Banks are now investigating the possibilities of other services

through their installed networks of ATMs like provision of audio and life assurances quotes

where the customer can obtain mortgage and life assurance quotes electronically and results

displayed on the ATM service screen.

Solome Lumala(2000), noted that the use of ATM service delivery has enabled banks to

cover a wider geographical area than would otherwise be at an actual branch. Banks are able

to provide banking services to non residents as well. While this has its disadvantages

especially as banks lose the benefit of “know your customer.“ It increases the service area

and therefore, profitability for the institutions.

Riki Roy (1999), marketing manager of service and computer industries, suppliers of ATMs

in Uganda went ahead to say that one of the ways that banks have to be identified is

advertising through the ATM net work using interactive screens to stay in touch with their

customers. Each ATM in a net work can present unique and specific advertising messages. On

the other hand it may change screen and present certain messages to specific neighborhoods at

specific times of the day or adjust advertising messages to recognize local and national events

and holidays. The bank can take advantage of the ATMs ability to generate additional revenue

from the ATM networks, just as newspaper sale space as a source of revenue, the banks can

space on their ATM screens to third parties.

12

According to Mark L et al (2000), the emergency of ATM stand alone kiosks has incredibly

reduced the need the fore direct link between the customer and the branch. ATM banking

gives the customer a wide range of financial services that could substitute those provided at

the branch, for example, the easy accessibility of the ATM can also be used for dispensing

other service like moving and parking tickets or for paying bills of utility companies for

example in Uganda, it’s possible to pay bill of national water and sewerage corporation,

electricity company (UMEME) and telecommunications.

Tony .W. G. further states that the ATM has been a very success full non attendant 24 hours

delivery channels for banking services. This system therefore, attracts other services such as

bill payment and pre-paid delivery of telephone airtime. Also the use of ATM in banks allows

them to operate efficiently by reducing their excessive capital expenditure hence customer

satisfaction.

2.1.5. Challenges of ATMs (Automated teller machinesWith increased use of ATMs, delivery of financial services has come with new service

providers. In more sophiscated economies than Uganda, banks, super markets, and

telecommunication companies provide loan payments services, insurance services, for

commercial banks in Uganda therefore, this is something worth emulating.

According to Dan Wright and walls (1988), one problem with ATM is that they are now the

greatest source of customer complaints particularly over “phantom” with drawls which

customers argue that were not made by them whilst banks would never complain that there

machines are infallible, they do argue that these withdrawals are usually made by friends or

family members or pin.

13

Salome .L (2004), ATM banking services are mainly found in urban areas, the population in

rural areas is largely serviced by micro finance institutions which are not as sophisticated as

the commercial banks. This is a drawback since Ugandans population is predominantly rural.

Coupled with these attitudes, cultural practices and sediments of the potential banking

population. They should be just right for the people to be able to take advantage of the

banking services, aibet at a more sophisticated level.

One of the biggest concerns about ATMs is security (Mukasa 2003). He says this is the same

for provider and customers. There should be protection from hackers and fraudsters.

Customers nee to be sure that their passwords are secure and information and transaction are

safe. Development of secure control is a big challenge for the service providers. Banks should

use appropriate techniques to mitigate both external and internal threats to their ATM system

in order to increase customer satisfaction.

Schaechter (2000) noted that the lack of face to face customer relations in ATM banking

increases the risk of money laundering. Banks in more advanced economies use a

combination of checks such as electoral register number, sighting current national I.D,

passports, driver’s license, recently utility bill where possible, certified photocopies must be

provided, in Spain ATM use is restricted to customers already in a traditional relationship

with the banks. Banks have to invest in more vigilant measures especially, since automation

(auto bank) makes prompt detection of money laundering more difficult. During august 2003,

the Uganda bankers association (UBA) launched a campaign to sensitize the public about

money laundering in addition; commercial banks have introduced rigorous account opening

requirements similar to those in more developed economies.

In the article “keep the ATM card in check”, she noted that ATMs have left many people who

lacked financial displine cash strapped. She went ahead and interviewed some banking

14

experts who said “having ATM is having cash at hand, it is lighter, and it’s had for people to

starve themselves when they have money in their accounts” Robert Sempa the corporate

liaison officer of centenary rural development bank. Therefore, people’s ability to save money

has reduced because ATM points are every where. Richard Byarugaba the managing

director of Nile bank (Barclays bank) Uganda, said it is true that ATMs are here to help us

any time in case of needs, but having a plan will help you control your ways of spending, for

example determining how much one will need for the home basic such as emergencies like

illnesses (Sunday vision, may 2005 pg 19)

According to Salome (2004) , banks that engage in ATM use are likely to have a higher liquidity risk

rising from volatility caused by customers switching accounts as they take advantages of better rates

and services elsewhere. This calls for closer liquidity management and adequate assets to act as

collateral should borrowing become necessary. Tied in with this foreign exchange risk Banks should

be able to hedge against adverse foreign exchange rate of the currency in which they and their

customers deals. This is a coast that must be included in the overall budget of the bank.

2.2.0 School Fees Banking A fee is the price one pays as remuneration for services. Fees usually allow for overhead,

wages, costs and markup. A fee may be a flat fee or a variable one or part of a two-part tariff.

http://en.wikipedia.org/wiki/fee

Schooling

At public universities and colleges, students are charged tuition and matriculation. When can

themselves be considered fee charged per credit hour? However, the term student fees

15

typically refers to additional charges which the student is required to pay, typically no matter

how many hours the student is taking in the academic term.

Commonly this is a student activity fee, which helps to student organization,particularly those

which are academic in nature,and those which all students equally, like government students

and students media. A newer fee is the technology fee, which is often charged to students by

schools when state government fails to meet the needs for computers and other classroom

technology. Students may also be charged a health fee which usually covers the campus

nurse, and possibly a visit to local clinic if the student is ill.

Methods of school fees banking

2.2.1. Cash payment option The Bank accepts cash deposit payment for school/tuition fees for students studying in

educational institutions that have school/tuition fees collection accounts in the Bank. The

customers fill banking slips for school/tuition fees payment and hand to the cashier together

with cash at any of the Bank Branches. Transaction charge for the service is only shs.2000.

2.2.2. ATM school fees banking 2.2.3.Electronic Fund Transfer (EFT), EFT Direct Debit transfer option facilitates the

transfer of fees from the parent/guardians account to the educational institutions account

electronically provided the customer has executed a Direct Debit Agreement (DDA). The

DDA which is available at educational institutions when executed authorizes the bank to

collect fees from the parent’s/guardian’s bank account for electronic transfer to the

educational institution’s bank account.(Wed,20 May,2009 New Vision).

16

2.2.4. Mobile payment; Pay pal launches school fees payment platform. Pay pal- an on line

payment gate way in partnership with safari com and some banks have launched a platform

that allows one to pay fees directly to school bank accounts through mobile phones. Okuttah

Mark, Business Daily Africa. (http://mobile-finance.com/node/13427/mobile-

payment.pay pal-launches)

2.3.1 Customer satisfactionCustomers; are those who buy and use the organizational services and products to solve their

problems and get good feelings and they are the kings (Waswa Balunywa,1995)

According to (Cart Wright Roger and George Green 2000), a customer is body for whom

you satisfy a want or a need with some form of payment. The payment may be money, time,

or it may be goodwill; quality of the product or service-but there is some form of payment.

Customers are classified into two classes namely; potential and actual customers.

An actual customer is the one the company knows at the material moment while potential

customer is one who is eying to join the company’s list of customers any time he/she makes

up his/her mind.

A Zeithmal (1990) argue that customer satisfaction doesn’t bring in the cash , but customer

behaviour does. Companies should treat their employees like customers ,and their customers

like employees . this will lead to to better results , improved quality of services ,highier

productivity, lower costs and geater oppoertunity for error recovery.

Accorrding to Sesser (2006), the customers is king , as this doesn’t cost anything. A

companys growth and successs is not simply about meeting budgets or cutting cost, but about

engaging the companybin finding world –class solutions for customer ‘concerns.17

In practical terms, every company needs to develop models whereby the customer focus is

integrated more fully into their way of doing business. Its this kind of customer focus help a

business stay close to its customers : commited,focused, and conscious of the common good.

http://www.financialmirror.com/morenews.php?id=3563(accessed on 18/08/2007)

When a company creates employee value, this leads to customer value which creates long

term investor value. “we to spend more time thinking because customers reign.”. unless the

‘customer focus’ in individual employees is recognised and nurtured, customer centricity will

be shortlived in any organisation (Susan,2010)

Customer satisfaction; is a reflection of organizational competency or its capability in the

delivery of services to customers. It is one of such parameters used to measure performance or

competency of an organization. (Prokesch 1995,pg 108). Organizational competencies that

enable customer satisfaction can be planned,developed and continually updated,and sustained

through continuous learning by firms subject to forcesof constraints such as management

strategy,primary markets, and economies of scope,accumulated technological basis,

organizational culture and government policy.

Customer satisfaction is the fulfillment of customer expectations and meeting their needs. The

of customer satisfaction depends on the extent to which customer’s expectation about the

product or service are fulfilled (Omagor,Bakunda,kigwana 1995)

Kotler et al (1999),defines customer satisfaction as the extent to which products or services

perceived performance matches buyer’s expectations. If it falls short of the expectation, then

the customer is dissatisfied.

Normally, a complete customer satisfaction is a key to customer loyalty and superior long

term financial performance. Even in markets with a relatively few or no

18

competitors,providing customers with outstanding value may be the only way to achieve and

sustain customer satisfaction and loyalty (Jones & Sasser 1995).

A crucial component of the formula for competitive business advantage is customer

satisfaction. This formula reads; competitive =customer satisfaction + business performance.

i.e. CA=CS+BP.

2.3.2 Importance of customer satisfactionIn a pioneering Havard Business Review study,Fredrick Reichheld and W.Earl Sasser,

identified numerous bottom-line benefits accruing from customer satisfaction, loyalty and

retention.

Reichheld et al (1996) observe that customer satisfaction,loyalty and retention might be the

only sustainable competitive advantage in the challenging economic times. They defined

customer loyalty as a customers sustained commitment to a company as demonstrated by

repeat purchases, increased wallet share and positive word of mouth referrals. The key to

customer loyalty is customer satisfaction and customer satisfaction begins with providing

customers with superior service. Their research indicated that when a company commands

such loyalty, the benefits include, but go considerably beyond incremental value.

Carthright (1997) also found that loyal customers purchase more; they will pay higher

prices, they are easier to service (thus reducing operating costs), and they will help expand

the customer base by giving positive referrals. The numerical evidence cited in this study was

particularly telling a mere 5% increase in customer retention, increases an organization’s

profitability by 25% to 100%. Securing customer loyalty is cost effective because acquiring a

new customer can cost twelve times as much as keeping the existing one.

19

The evidence from this study is clear. Companies receive proven bottom-line benefits from

establishing long-term customer relationship and those companies that invest strategically in

improving customer satisfaction and loyalty, can correspondingly expect significant gains in

profitability and other financial measures.

Gary (2007) reported that there a number of benefits that may be derived from satisfied

customers. These benefits include; the ”word of mouth” factor. Loyal customers go out of

their way to help you build your organization when they feel you care for them. Delighted

customers tell at least four other people about their delighted experiences. This word of mouth

is the most single powerful marketing force your organization can have working on its before.

Dissatisfied customers will tell ten more.

A stronger brand; in difficult economic times, a loyal customer will first turn to the

organization they trust. Trust should be key element behind your brand. The brand represents

an emotional trust bond they have formed with your organization. (Heskett, 1977).

According to Donald (1984), differentiation significantly reduces the “Leap frog effect”,

because it is longer built on the product/service/price level.

Loyal/satisfied customers purchase more and more often. It costs much less money for you to

strengthen the relationship an existing customer, than to begin a new relationship with a new

customer (Eberhard, 2000). Satisfied customers have higher response rates than non-loyal

customers. You spend less money on loyal customers to achieve the results (Philip, 1984).

Organizations with satisfied and loyal customers can more readily ask and receive more

accurate responses from their customers on what they really want. This not only reduces the

cost to develop, but improves “time to market” dramatically (Drucker, 1993). As can be

deduced from the ongoing discussion it is evident that organizations involved in service

20

delivery need to focus much on the strengthening their customer relationship through

creating a culture of continuous service improvement.

2.3.3. Measuring customer satisfaction.

Customer satisfaction is the state of mind that customers have about a company their

expectations have met or exceeded over the life time of the product or service. The achieve

of customer satisfaction leads to company loyalty and product repurchase (Philip,1984)

Lineberg (2005), explains that measuring and achieving customer satisfaction involves;

formulating and prioritizing the organisation’s objectives and defining their relevant key

performance indicators (KPIs) and targets; identifying each departmental benefits and

determining which ones are best positioned to contribute to the objectives KPI target;

ratioalising and optimizing the project portfolio to ensure the aggregated project benefits

achieve the objective target KPI.

Sequencing the optimized project portfolio to generate the benefit realization time line, taking

into account resource constraints, dependencies and critical milestones, managing scope and

time line changes through out organization execution and evaluating their impact on benefits

and their delivery time line, and monitoring the departmental project and benefits realization

phase, to verify project success and ensure the organization’s objectives are being achieved.

2.3.4. Indicators of customer satisfactionShalif (2004), states that a market share means an indicator of how well a firm is doing

against its competitors. Shalif (2004) explains that unit market share is the percentage of the

total market unit sales that is attributed to a specific institution in the market or business. It is

therefore equal unit sales or Total market unit sales times% while revenue market share is the

percentage of total revenue generated in the market that is attributed to a specific business

21

entity. It is expressed as; Revenue market share =Sales Revenue diivided by Total Market

Revenue.

Modiglian and Miller (1963), explains that knowing the business market share helps

managers evaluate both primary and selective demand in their market. That is it enables to

judge not only market growth or decline but also trends in the customers’ selections among

competitors.

Rosenberg (2005), reveals that marketers need to be able to translate sales into market shares

because this will demonstrate whether forecasts are to be maintained by growing the market

or by capturing share from competitors. The latter will almost always be difficult to achieve.

Market share is closely monitored for signs of change in the competitive landscape, and

frequently drive strategic or tactical action.

In the service industries the matching of capacity and demand is particularly difficult,there’s

either too much to demand for putting a strain on resources (capacity), or little demand-giving

rise to unused capacity and loss in revenue (Reichheld,1996). This is known as ‘perishability’

factor. Therefore services need to develop an understanding of their demand patterns. While

the level of demand can sometimes be out with the organization demand along with capacity

and bring a balance (Steven,1995).

One technique that is becoming highly significant in demand and capacity management in the

service sector is that of yield or revenue management. By setting different prices for different

time periods organizations need to increase their yield/revenue from service/market share

(Rick, 2000).

22

One problem is that if demand exceeds, it leads to queuing while reservation and advance

booking can mitigate its occurrences in some situation it still occur and will remain so with

the inevitable frustration for customers.

The need to know service capacity resources and assets like physical facilities to house are

key. The physical facilities designed to processing customers and their possession

(equipment), labour in provision of services and time is a resource that serves as a basis upon

which several services may be sold. (Parasuraman,1985)

Markland (1996), says it is imperative to know, ‘what level of capacity should be maintained

to satisfy the demand?’ or should a company provide excess capacity to improve customer

services or minimize excess capacity to maximize resource utilization?

Similarly, service organizations need rate fences to be successful, its good for customers to

perceive price differences as justified and while customers are using the same services hence

the rate charged should be explainable for example tangible rate fences like location, service

type, time or absence or presence of amenities where as intangible rate charged include group

application, membership, duration of usage, time booking.

Elaine (2005) states that customer satisfaction is the customers overall feeling of contentment

in a business interaction. It recognises the difference between customer expectations and

perceptions. Satisfaction may be cultivated or develoved quickly over a period of time. It is

the overall pleasant experience after a consuming a product or service.

2.4.0. Review section:

If i had to do chapter two; i would consider the following literature sources:

23

a) Publication from international bodies like World bank, United Nations.

b) Consultancy reports.

c) Independent research firms.

d) Magazines.

e) Bank archives.

f) Journals.

g) Ugandan Bureau Of Statistics (U.B.O.S).

They can either serve as primary or secondary data source.

Future researchers are encouraged to undertake the above.

24

CHAPTER THREE METHODOLOGYs

3.1 IntroductionThis chapter is about the methods the researcher used to collect data. It focuses on ; Research

design, study population, sample methods and size, data collection method

3.2. Research strategy and design.

Through Purposive and Triangulation research designs, Stanbic Bank Uganda- Makerere

Branch was selected as a case study. The study was based on descriptive research design, and

through triangulation the researcher captured different opinions of different respondents at

different time which enabled him understand fundamental issues. Both qualitative and

quantitative data was used for purposes of drawing valid conclusion.

3.3. Study Population.

The study population included branch manager, senior account, administrator, information

consultant/ATM attendant and customers.

3.4.0. Sampling designThe researcher used stratified sampling design for courses at Makerere University which use

ATMs to bank their tuition.

25

3.4.1. Sampling sizeThe sampling size used included 25 respondents; this included 4 Stanbic bank staff and 21

customers who used ATMs to bank tuition fees.

3.4.2. Sampling methodSimple Random sampling was then used to select the appropriate representatives of both the

bank staff and bank customers especially those were making use of ATMs to bank tuition

fees.

3.5.0. Sources of data

3.5.1. Primary dataPrimary data was elicited directly from respondents using observation, interviews,

questionnaire..

3.5.2. Secondary dataRelated literature from journals, records from publications, text books and internet were major

sources of secondary data.

3.6.0. Data collection methods and instrumentsThe survey methods were used in data collection including interviews, questionnaires,

observation from the operation of machines.

3.6.1.Interviews.

Face to face interviews were used to collect data from staff who were concerned with ATMs

and customers who use ATM school fees banking.

3.6.2.Questionaires.

26

The questionaires were simple and clear for customers in order to increase the response rate

and self- administered questionaires were used for bank staff.

3.6.3. Observation.

This method was used by mainly looking at the way customers mainly used machines.

3.7.0. Data presentation and analysis.

Data was collected and analysed and formulated into meaningful information. The data was

carefully read and compared with the responses from the interviews, questionaires and what

the researcher observed. The data was edited to ensure accuracy and consistency.

3.7.1.TabulationThe summary of the raw data was put in tabular form by use of frequency tables.

3.8.0.Data intergrity and validityThe collected data was edited before presentation and analysis in order to ensure that all

irrelevant data was omitted to provide required information for the study. The integrity of

information was supported by the use of secondary sources about the same variable under

study.

3.9.0. Limitations to the study and possible solutions.

Time constraint; as the time to carry out the research was not enough. The researcer tried

every thing possible to beat the deadline.

Financial constraint; the research involved typing and printing costs. The researcher tried and

sacrificed to make this research prosperous.

27

Return of responses and non responses especially when the respondents misplace

questionaires or forgot to answer them especially when they anticipate answering them at a

later time especially bank staff who feared giving information concerning the bank’s affairs

this a competitive era. The researcher convinced them beyond doubt that the research is

purely academic.

3.9.1. Review section.

If i had to do chapter three, again i would consider the following changes:

a) Double the sample size to capture more respondents.

b) Sampling method/procedure; non purposive- snow ball method .

c) Methods of data collection:

Focus group discussion.

Participation.

Documentation review.

Future researchers are encouraged to undertake the above.

28

CHAPTER FOUR

PRESENTATION, ANALYSIS AND DISCUSSION OF FINDINGS

4.1.0. IntroductionUnder this chapter, a presentation, analysis and discussion of findings is done in accordance with the study objective:

1) To examine the usage level of ATM in school fees banking

2) To establish the determinants of customer satisfaction in Stanbic Bank Uganda-Makerere Branch

3) To establish the relationship between ATM school fees banking and customer satisfaction

. However, an analysis of demographic characteristics of the respondents is done first. The following definitions of codes were used in this section; strongly Agree (SA), Agree (A), Not Sure (NS), Disagree (D), and Strongly Disagree (SD).

29

4.1.1 Gender of the respondentsFigure 1: A pie-chart showing gender of respondents

Figure 2: Table Showing gender of respondents

Gender of respondents

Frequency Percentage Degrees

Male 14 56 201.6

Female 11 44 158.4

Total 25 100 360

Source: Primary data

Results from the table above shows that most respondents (56%) were males while (44%) females. This therefore implies that there were more males than females in the study.

4.1.2: Marital status of respondets.

30

Figure 3: A pie-chart showing marital status of respondents

Figure 4: Table Showing marital status of respondents

Marital status Frequency Percentage Degrees

Single 14 56 201.6

Married 8 32 115.2

Divorce 1 4 14.4

Widow 2 8 28.8

Total 25 100 360

Source: Primary data

Results from the above table and pie- chart show that (56%) were single,(32%) were married,(8%) were widows while (4%) were divorced.

31

4.1.3: Level of education of respondents

Figure 5: A pie-chart showing level of education of respondents

Figure 6: Table Showing level of education of respondents

Level of education Frequency Percentage Degrees

A’ Level _ _ _

Diploma 4 16 57.6

Degree 19 76 273.6

Post graduate 2 8 28.8

Others specify _ _ _

Total 25 100 360

Source: Primary data

32

From the table and pie-chart above (16%) were diploma holders,(76%) degree holders, (8%) post graduate and none were A’Level and others. This means that customers are skilled and good at ATM operations

4.1.4: Age bracket of respondents

Figure 7: A Dough nut chart showing the age bracket of respondents in years

Figure 8: Table Showing the age bracket of respondents in years

Age bracket (years) Frequency Percentage Degrees

18-30 16 64 230.4

31-40 7 28 100.8

41-50 2 8 28.8

51 And above - - -

Total 25 100 360

Source: Primary data

33

The results from the table and dough nut chart above show that most respondents (64%)fall in the age bracket of 18-30 years,(28%)are in 31-40 years, (8%) are in 41-50 years and none in 51 and above. Since most youth (64%) embrace technoligical advancement its means the service up take (ATM school fees banking) in future will be high.

4.1.5: Factors that attracted respondents to Stanbic Bank Uganda

Figure 9: A 3-D Chart showing factors which attracted respondents to Stanbic Bank Uganda

Figure 10: Table Showing factors which attracted respondents to Stanbic Bank Uganda

Factors Frequency Percentage Degrees

Accessibility 9 36 129.6

Reliability 11 44 158.4

Flexibility 1 4 14.4

Other 4 16 57.6

Total 25 100 360

34

Source: Primary data

The 3-D chart and table above indicates that (36%) were attracted to Stanbic because its accessible, (44%) because its reliable, (4%) because its flexible and (16%) because of other factors that include accuracy,convenience and safety of customers’ money

4.2.0: Usage level of ATM school fees banking.

Objective: (To examine the usage level of ATM in school fees banking)

4.2.1: Banking school fees using ATM.

To evaluate the effectiveness of ATM school fees banking begins with establishing whether customers use the service

Figure 11: A bar graph showing ATM school fees banking

35

Figure 12: Table showing Banking school fees using ATM

Extent of agreement Frequency percentage Degrees

Yes 5 20 72

No 20 80 288

Total 25 100 360

Source: Primary data

At Stanbic Bank Uganda –Makerere Branch most customers (80%) don’t use ATM school fees banking, (20%) use ATM school fees banking.

4.2.2: Reasons for not using ATM school fees banking.

36

Figure 13: A Pie-chart showing reasons why customers d0n’t use ATM school fees banking

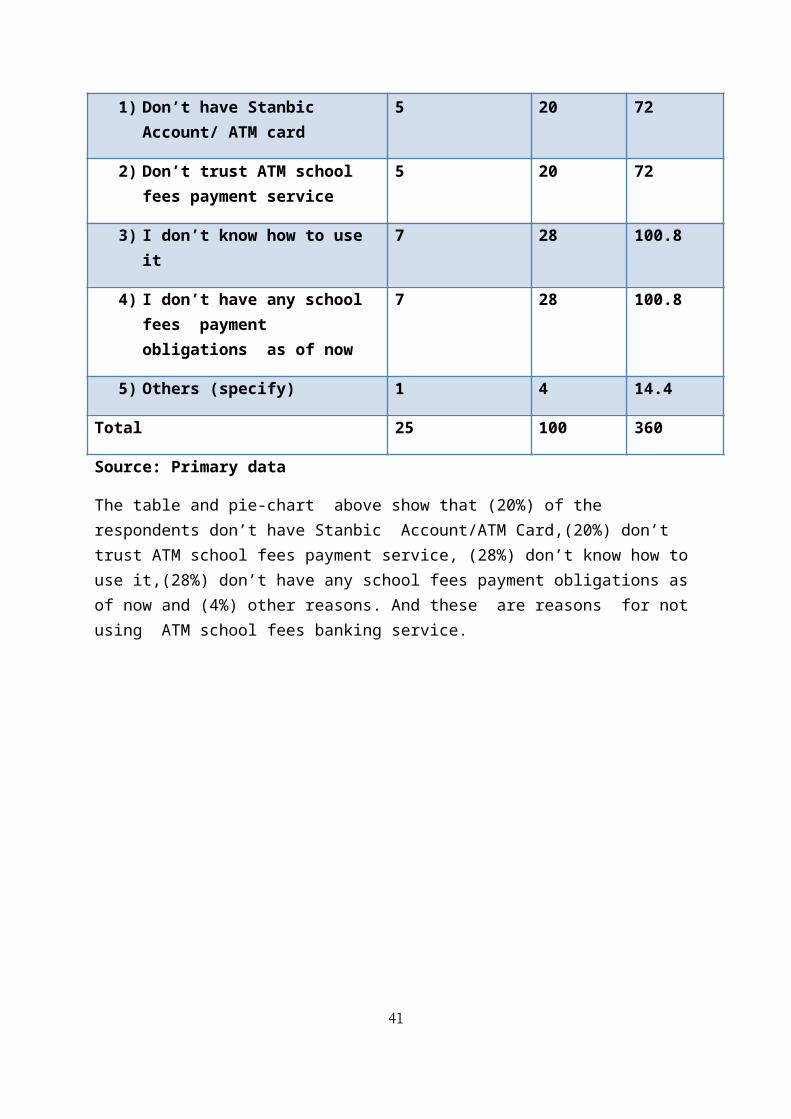

Figure 14: Table showing Reasons for not using ATM school fees banking

Reasons Frequency Percentage Degrees

1) Don’t have Stanbic Account/ ATM card

5 20 72

2) Don’t trust ATM school fees payment service

5 20 72

3) I don’t know how to use it 7 28 100.8

4) I don’t have any school fees payment obligations as of now

7 28 100.8

5) Others (specify) 1 4 14.4

Total 25 100 360

Source: Primary data

The table and pie-chart above show that (20%) of the respondents don’t have Stanbic Account/ATM Card,(20%) don’t trust ATM school fees payment service, (28%) don’t know

37

how to use it,(28%) don’t have any school fees payment obligations as of now and (4%) other reasons. And these are reasons for not using ATM school fees banking service.

4.2.3: Categories of customers banking school fees using ATMFigure 15: A pie chart showing categories of customers banking school fees using ATM

Figure 16: Table showing Categories of customers banking school fees using ATM

Category Frequency Percentage Degrees

Student 2 50 180

Parent 1 25 90

Relatives 1 25 90

Friends - - -

Others (specify) - - -

Total 4 100 360

Source: Primary data

From the table and pie-chart above (50%) are students,(25%) are parents,(25%) are relatives and none are friends and others who bank school fees using ATM

38

4.2.4: Number of times customers bank school fees in a semester using ATMFigure 17: A bar graph showing number of times customers bank school fees in a semester using ATM

Figure 18: Table Showing number of times customers bank school fees in a semister using ATM

Number of times Frequency percentage Degrees

once 1 4 14.4

1-4 5 20 72

5-10 - - -

11-15 - - -

None 19 76 273.6

Total 25 100 360

Source: Primary data

The above responses indicate that (76%) have never used ATMs to bank school fees, (20%) of the respondents have used 1-4 times, (4%) have used once and none for 5-10 times, 11-15 times

39

4.3.0: Determinants of customer satisfactionObjective:( To establish the determinants of customer satisfaction in Stanbic Bank Uganda-Makerere Branch)

4.3.1: ATM school fees banking reliabilityFigure 19: Chart Showing ATM School fees banking reliability

Figure 20: Table showing ATM school fees banking reliability

Statement Frequency Percentage Degrees

Strongly Agree 3 12 43.2

Agree 11 44 158.4

Not sure 6 24 86.4

Disagree 3 12 43.2

Strongly Disagree 2 8 28.8

Total 25 100 360

Source: Primary data

40

The table and pie-chart above indicates that 12% strongly agreed,44% agreed,24% Not sure,12% Disagreed,8% strongly disagreed.

4.3.2: Quality of serviceFigure 21: A bar graph showing the extent of agreement upon high Quality of services

rendered by Stanbic Bank Uganda

Figure 22: Table showing Stanbic bank Uganda offers high quality ATM school fees banking country wide

Extent of agreement Frequency Percentage Degree

Strongly agree 5 20 72

Agree 7 28 100.8

Not Sure 9 36 129.6

Disagree 2 8 28.8

Strongly Disagree 2 8 28.8

Total 25 100 360

Source: Primary data

The bar graph and table above indicates that 20% strongly agreed, 28% agreed, 36% were not sure, 8% disagreed and strongly disagreed.

41

4.3.3: Meeting customer expectationsFigure 23: A bar showing the extent of agreement upon which ATM school fees banking meets customer expectations in Stanbic Bank Uganda

Figure 24: Table showing ATM school fees banking meets my expectations.

Extent of agreement Frequency Percentage Degree

Strongly agree 2 8 28.8

Agree 6 24 86.4

Not Sure 5 20 72

Disagree 9 36 129.6

Strongly Disagree 3 12 43.2

Total 25 100 360

Source: Primary data

The bar graph and table above indicates that 8% strongly agreed, 24% agreed, 20% were not sure, 36% disagreed, and 12% strongly disagreed.

42

4.3.4: ATM School fees banking reducing bank queues Figure 25: A 3D-chart showing the extent of agreement upon which ATM School fees banking has reduced bank queues in the banking hall.

Figure 26: Table showing ATM School fees banking has reduced bank queues in the banking hall.

Extent of agreement Frequency Percentage Degree

Strongly agree 4 16 57.6

Agree 11 44 158.4

Not Sure 3 12 43.2

Disagree 4 16 57.6

Strongly Disagree 3 12 43.2

Total 25 100 360

Source: Primary data

The 3D-chart and table above indicates that 16% strongly agreed, 44% agreed, 12% were not sure, 16% disagreed and 12% stronly disagreed.

43

4.3.5 : Pride of being a customer of Stanbic Bank Uganda.

Figure 27: A pie-chart showing the extent of agreement upon which customers agree to be proud of banking with Stanbic Bank Uganda.

Figure 28: Table showing Pride of being a customer of Stanbic Bank Uganda

Extent of agreement Frequency Percentage Degree

Strongly agree 4 16 57.6

Agree 11 44 158.4

Not Sure 3 12 43.2

Disagree 4 16 57.6

Strongly Disagree 3 12 43.2

Total 25 100 360

Source: Primary data

The pie-chart and table above indicates that 16% strongly agreed,44% agreed,12% were not sure,16% disagreed and 12% strongly disagreed.

44

4.3.6: Response to customer needs.

Figure 29: A bar graph showing the response of Stanbic Bank Uganda to customer needs

Figure 30: Table Showing the response of Stanbic Bank Uganda to customer needs

Extent of agreement Frequency Percentage Degree

Strongly agree 4 16 57.6

Agree 14 56 201.6

Not Sure 3 12 43.2

Disagree 1 4 14.4

Strongly Disagree 3 12 43.2

Total 25 100 360

Source: Primary data

The bar graph and table above indicates that 16% strongly agreed, 56% agreed, 12% were not sure, 4% disagreed , 12% strongly disagreed

45

4.4.0: Relationship Between ATM school fees banking and customer satisfaction.

Objective: To establish the relationship between ATM school fees banking and customer satisfaction

4.4.1: ATM school fees banking saves time compared to banking school fees using bank slips in banking hall.

Figure 31: A 3D-chart showing the extent to which ATM school fees banking saves time compared to bank slips in banking hall