web viewa lot of concentration, effort, responsibility and study have been involved in preparing...

TRANSCRIPT

The Overall Financial Activities

Of

Al-Arafah Islami Bank Ltd (AIBL),

BangladeshBased on the study on 2010 Financial statement and business police

IUBAT

1

The Overall Financial activities of

Al-Arafah Iislami Bank Ltd (AIBL),Bangladesh

SUBMITTED TO:

MD. MUSTAFIZUR RAHMAN

Faculty of (CBA)

BUS 201

SUBMITTAD BY:

GROPE NAME: ONIKER PRANTOR

NAME ID PROGRAM EMAIL CLASS

ROLLASADUZZAMAN

RIDOY

10202081 BBA

ADIBAZAMAN 10202085 BBA

MOSIUR

RAHMAN

10202068 BBA

FATEMA

AKHTER SIMA

10202065 BBA

2

Letter of Transmittal

2nd April, 2011

Md.Mustafizur Rahman

Faculty of (CBA)

School of Business Studies.

International University Of Business Agriculture and Technology.

Dear Sir,

Here is the report on titled the overall foreign exchange activities of Al-Arafah Islami Bank Ltd

(AIBL), Bangladesh-a comprehensive study. Prepared for you as a final report of the semester.

It took one month to prepare the report and we have tried to gather as much information as

possible within this limited time. Although the stipulated time is not enough to have in depth

knowledge about the real corporate world, this report give mi much insight in Islamic banking

practiced by the conventional banks like (AIBL).

I would like to thank you for giving us the opportunity to prepare this report under your sincere

guidance and cooperation.

Thank you,

Sincerely yours,

3

Acknowledgement

A lot of concentration, effort, responsibility and study have been involved in preparing this paper

into realty. In preparing a report one need a number of assistance and guidance from reliable

sources. This report also stands on the basis of such efforts. I have pleasure to express my

gratitude to my grope members. In preparing the report, I received active co-operation from the

VP responsible as a manager, 1st AVP Responsible as a second officer, Officer of Al-Arafah

Islami Bank (AIBL).I sincerely express my heart- felt gratitude to them for their co-operation,

which helped me to conduct and complete this report. They have provided us some important

books on banking and some books on marketing and finance sharing, consent and given some

advice of making a research report. However this report suffers from many shortcomings.

Moreover, I have exerted my best effort in preparing this report. We seek excuse for the errors

that might have occurred in spite of my best efforts.

Executive summary

4

TABLE OF CONTENTS Page

Title Fly…………………………………………………………………………i

Title Page……………………………………………………………………….ii

Letter of transmittal……………………………………………………………iii

Acknowledgement………………………………………………………………iv

Executive Summary…………………………………………………………….v

1.0 INTRODUCTION………………………………………………………..1

1.1 Origin of the report…………………………………………………………….

1.2 Objective of the study……………………………………………………..

1.3 Scope of the study…………………………………………………………

1.4 Methodology……………………………………………………………….

2.0History of Al-Arafah Islami Bank Limited………………………………

2.1 Aims and Objective…………………………………………………………

2.2 Mission and Vision of AIBL……………………………………………….

2.3Commitments……………………………………………………………….

3.0MANAGEMENT OF AIBL…

3.1Planning………………………………………………………………………

3.2Organizing……………………………………………………………………

3.3Staffing……………………………………………………………………….

3.4Directing……………………………………………………………………….

3.5Controlling……………………………………………………………………

3.6Distribution of Branch………………………………………………………..

3.7The Financial position of AIBL……………………………………………….

3.8AIBL Product Service …………………………………………………………..

5

3.9.1Genenral Banking………………………………………………………..

3.8.1 Foreign Exchange…………………………………………………..

3.8.2 Services of the bank……………………………………………………

3.8.3 Products of AIBL……………………………………………………….

4.0Banking system in Bangladesh……………………………………………………

4.1 Corporate Information……………………………………………………..

4.2 Financial Analysis of Al-Arafah Islami Bank …………………………………..

4.3 Performance of AIBL……………………………………………….………….…..

4.4 Progressive Analysis of AIBL……………………………………………………..

4.4.1 Capital…………………………………………………………………………..

4.4.2 Deposit…………………………………………………………………………..

4.4.3 Investment………………………………………………………………………

4.4.4 Grameen & Small Medium Enterprise (SME) Scheme………………………..

4.4.5 International Trade………………………………………………………………

4.4.6 Investment Income……………………………………………………………….

4.5 . Economic Impact Analysis of AIBL:………………………………………………….

5.0Functions of Al-Arafah Islami Bank Ltd ……………………………………………..

5.1 Foreign Exchange of Al-Arafah Islami Bank Ltd ……………………………………….

5.2 Opening LC in AIBL: ……………………………………………………………………..

5.3 Import Business:……………………………………………………………………..

5.4 Export Business:…………………………………………………………………….

5.5 Procedure of preparing L/C……………………………………………………………

5.6 Back to Back L/C:……………………………………………………………………….

5.7 Features of Back to Back L/C……………………………………………………………

5.8 Foreign Documents Bills for Collection (FDBC):……………………………………….

6.0Performance Analysis of AIBL………………………………………………………….

6.1 Al-Arafa Islami Bank Ltd: SWOT Analysis…………………………………………….

6.1.1 Strengths……………………………………………………………………………….

6.1.2 Weaknesses…………………………………………………………………………….

6.1.3 Opportunities………………………………………………………………………….

6.1.4 Threats………………………………………………………………………………….

6

7.0 ENDING PART PF THE REPORTE…………………………………………………….

7.1 Findings and Analysis…………………………………………………………………….

8.1 Recommendations…………………………………………………………………………

9.1 Conclusion…………………………………………………………………………………

10.0 Appendix…………………………………………………………………………………..

10.1 Bibliography………………………………………………………………………

INTRODUCTION:

2. Origin of the Report:

This report is a comprehensive study prepared as a requirement for the completion of

the BBA Program of IUBAT- International University of Business Agriculture and

Technology. The primary goal of report is to provide an opportunity for translation of

theoretical conceptions in real life situation. We are placed in enterprises, organizations,

research institutions as well as development projects. The program covers a period of 3

months comprehensive study about the Products and works of Al Arafah Islamic Bank

Limited in Bangladesh.

The comprehensive study about the Products and works of Al Arafah Islamic Bank and

other Traditional Banks in Bangladesh prepared under the guidance of our faculty

7

member Tanvir H DeWan. As a requirement for the completion of the program we need

to submit this report, which would include an overview of the Products of the Banks

was attached with and elaboration of the project we were supposed to conduct during

the study period.

4. Objectives of the Study:

The objective of the internship program is to familiarize students with real business situation, to

compare them with the business theories and at last stage make a report on assign task.

Objectives regarding this study are as follows:

a. General Objectives:

The general objective of this report is to fulfill the requirement of internship report.

To earn practical experience and knowledge about the banking operations and corporate functions

performed by Al- Arafah Islami Bank Limited.

b. Specific Objectives:

To submit a brief description about the performance of Al-Arafah Islami Bank Ltd.

To make a general evaluation of AIBL activities among different professionals.

To understand the various services the bank offers and to understand the mechanism of

the services.

To analyze the Ratio of the bank to evaluate the performance

To identify the strengths and weakness, opportunities and threats of Al- Arafah Islami

Bank Ltd.

To know about the conventional banking and their operation.

To know about the Islamic banking and their operation.

To suggest remedial measurement for the improvement of the whole process of the Al-

Arafah Islami Bank Ltd.

To formulate recommendations that could add value to the service of Al- Arafah Islami

Bank Ltd.

5. Scope of the Report5. Scope of the Report

This report helps me to understand the clear real-time experience about the total management of

AIBL. It helps me to understand, how the bank manages its total processes. It also helps me to

8

understand how they deal with the customers as well as the foreign policy of their bank like- the

process of doing LC and export & import etc.

6. Information Needs

In order to conduct this research project and fulfill the research objectives the following

information will be required:

Information about Al Arafah Islami Bank Limited

Information about the facility provided by AIBL

Information about the job characteristics

Information about compensation and benefits policy

General information about the employees of AIBL

General information about motivation concepts

Information about the different wings of PB & head office of AIBL

Information about the expectation of the employees’ of AIBL

To know the financial performance of the bank

To know the work of general banking system of the bank

Methodology: A Research may be conducted either exploratory or conclusive. Based upon the

research topic and environment scenario I have decided to conduct exploratory research. To

conduct the research I have collected two types of data.

A) Primary Data and

B) Secondary Data.

A sample survey was conducted to collect primary data using two pre-designed survey

instruments from concerned groups following an appropriate sample design.

8. Sources of data

I have collected both primary and secondary data. I collected Secondary data from prior records

of AIBL.

I have collected primary information by interviewing employees, managers via the process assigned by AIBL, observing various organizational procedures, structures, directly communicating with the customer’s.

9

a. Primary Source of Information

When searching in the field directly to collect data was called primary sources of data. I

collected data from primary sources using the following method:

a. Observation method

b. Interview method

Now mention some primary points: -

Open ended and close ended questions

Personal experience gained by visiting, different desks

Personal investigation with bankers

Face to face communication with employees of the AIBL.

b. Secondary Sources of Data

The secondary data had been collected from the MIS of HSBC. To clarify different

secondary sources such as office memo, operating manuals, circulation & publication used

by the HSBC in this regard.

(1). Internal Sources

1. Bank's Annual Report

2. Group Business Principal manual

3. Group Instruction Manual & Business Instruction Manual

4. Prior research report

5. Any information regarding the Banking sector.

(2). External Sources

1. Different books and periodicals related to the banking sector

2. Bangladesh Bank Report

3. Newspapers.

Previous reports and journals relevant to the banking industry

Other published documents of Bangladesh Bank

10

Relevant AIBL paper and published documents.

Annual reports of 2006, 2007.

9. Data collection procedures:

The following procedures have been used to collect data with the respective instruments for

conducting the research paper.

a. Collection of Primary data: For collecting primary data personal interview technique have been used through a set of organized and structured questionnaire with mostly close-ended and open-ended questions as the instruments.

70 employees at different levels of Al Arafah Islami Bank Limited are interviewed through

formal and informal way.

b. Collection of Secondary data: In order to collect the secondary data different

related printed materials like corporate profile, annual report 2007-2008 and the official web

site has been followed. Moreover, various library sources like textbooks (Organizational

Behavior, Business Research, and Basic Business Communication) also have been used.

10. Data Processing & Analysis

After collecting all the required data, question area has been coded and data processing has been

done according to the employees’ personal information, experience, preference, satisfaction level

etc. for analyzing purpose. MS Word had been used to prepare graphical representation and the

graphs have been interpreted accordingly.

11. Limitation of the Report

Time frame for the research is very limited.

Large-scale research is not possible due to constraints and restrictions posed by the

organization.

The research only covers the employees of Uttara Model Town Branch, Dhaka.

The survey was limited to the employees of General banking and Foreign Exchange

Division.

Respondents were busy as well as reluctant to go through the process of

questionnaire.

11

The respondents sometimes did not agreeable in providing accurate statistics and

information

. Historical Background of Al Arafah Islami Bank:

With the objective of achieving success in the life here and hereafter following the way directed

by the Holy Quran and the path shown by Rasul (SM) Al Arafah Islami Bank Ltd was

established (registered) as a public limited company on 18 June 1995. It started business on 27

September of that year with an authorized capital of Tk 1,000 million. At inception, its paid up

capital was Tk 101.20 million divided into 101,200 ordinary shares of Tk 1,000 each. 23

sponsors of the bank subscribed the total issued capital. In 2000, the paid up capital of the bank

increased to Tk 253 million, of which Tk 126.50 million were paid by the promoters/sponsors

and Tk 126.50 million by the general public. In compliance with the new provision, Al Arafah

bank has raised its capital and reserve from Tk. 2245 million in the year 2007 to Tk 3049.34

million in 2008 by declaring 30% stock dividend out of the profit of the 2008. The paid up

capital of the bank has stood at Tk. 1383.81 million at 31st December 2008.

Renowned Islamic Scholars and pious businessmen of the country are the sponsors of the Bank.

100% of paid up capital is being owned by local shareholders. In 2008 the bank earned a net

profit before tax & provision of Tk. 1,528.10 million which is 102.08% higher than the previous

year. The bank is listed in the two STOCK EXCHANGEs of the country and has offered 126,000

shares for subscription and trading by the public. Al-Arafah Bank is an interest-free shariah bank

and its modus operandi is substantially different from those of regular commercial banks. The

bank however, renders all types of commercial banking services under the regulation of the Bank

Companies Act 1991. It conducts its business on the principles of musharaka, bai-murabaha, bai-

muajjal and hire purchase transactions. A Shariah Council of the bank maintains constant

vigilance to ensure that the activities of the bank are being conducted according to the precepts

of Islam.

. Objectives of AIBL:

Al-Arafah Islami Bank Limited is Islamic Banking institutions that operates with the objectives t

implement and materialize the economic and financial principles of Islamic in the banking arena.

12

The objectives of AIBL are not only to earn profit, but also to do good and welfare to the people.

The main objectives of AIBL are listed below-

To conduct interest free banking

To establish participatory banking instead of banking on debtor creditor relationship

To invest through different modes permitted under Islamic Shariah

To accepts deposits on profit loss sharing basis

To establish as welfare–oriented banking system

To extend co-operation to the poor, the helpless and the low income group for their

economic up liftmen

To play a vital role in human development and employment generation

To contribute towards balances growth and development of the country through

investment operations particularly in the less developed areas

To contribute in achieving the ultimate goal of Islamic economic System.

10. Corporate Culture:

This bank is one of the most disciplined Banks with a distinctive corporate culture. Here they

believe in shared meaning, shared understanding and shared sense making. Their people can see

and understand events, activities, objects and situation in a distinctive way. They mould their

manners and etiquette, character individually to suit the purpose of the Bank and the needs of the

customers who are of paramount importance to us. The people in the Bank see themselves as a

tight knit team/family that believes in working together for growth. The corporate culture they

belong has not been imposed; it has rather been achieved through their corporate conduct

3. Mission:

Achieving the satisfaction of Almighty Allah both here & hereafter.

Proliferation of Shariah Based Banking Practices.

Quality financial services adopting the latest technology.

Fast and efficient customer services.

Maintaining high standard of business ethics.

Balanced growth.

Steady & competitive return on shareholders’ equity.

13

Innovation banking at a competitive price.

Attract and retain quality human resources.

Extending competitive compensation packages to the employees.

Firm commitment to the growth of national economy.

Involving more in Micro & SME financing.

4. Vision:

To be a pioneer in Islami Banking in Bangladesh and contribute significantly to the

growth of the national economy.

To improve Banker- Customer relationship through improving customer service.

To develop new and innovate product/service through integration of technology and

policy and principle.

5. Commitments:

Ours is a customers focused modern Islamic Banking making sound and steady

growth in both mobilizing deposit and making quality Investment to keep our

position as a leading Islamic bank in Bangladesh.

To deliver financial services with the touch of our heart to retail, small and

medium scale enterprises, as well as corporation clients through our branches

across the country.

Our business initiatives are designed to match the changing trade & industrial

needs of the clients.

d. MANAGEMENT OF AIBL:

For any financial and non-financial organization, Management are the most valuable and

important resources of any kind of organization. And, a well-organize management provides the

organization to reach its ultimate goal. Management means planning, organizing, staffing,

directing and controlling of all financial and non-financial resources of an organization. Different

aspects of management practice in AIBL are discussed below.

PlanningAIBL has done its planning within the preview of the corporate plan. The overall planning

approach in AIBL is top to bottom. Each branch can plan according to the goal imposed by the

corporate level. It doesn’t plan independently. And, AIBL has a planning sector. This department

is mainly responsible for the overall planning.

14

Organizing AIB is organized as per the existing business locations. It has fifty branches, each of which is a

separate entity. Each unit is responsible for its own performance and each is headed at least by a

Senior Assistant Vice President (SAVP) in designation followed by Manager (Operations). He is

directly responsible for the performance of their unit. Within each branch, it is organized

functionally.

StaffingThe recruitment in AIBL is done in two ways. One as a “Provisional Officer” for the

management program and it has a probation period of two years. Another one is non-

management level as “Trainee Officers”. Provisional Officers are recruited in officer category

and their career path is headed towards different managerial jobs.

Directing

The management approach in AIBL is top-down or authoritative. Each information seeks

through lower management layer. Works are designed in such a way that one cannot leave

without clearing the tasks as he is assigned for a day. Sitting arrangement in all offices is done in

a way that the superior can monitor the subordinate all time. Manager (HOB) and Manager

Operation all time watch the operation of the bank through CC camera. Security is maintained

properly. Budgeting, rewarding, punishing, etc. are also practiced as control mechanism.

Controlling

AIBL does not believe in the traditional banking. It tries to increase and maintain its market

share in the private banking sector through two types of control techniques:

Feed Forward Control Feedback Control

Feedback control technique monitor outputs of a process and feed into the system to obtain

desired outputs. On the other hand feed forward control technique monitor inputs into a process

to ascertain weather these are as planned or not. If they are not, the inputs are changed in order to

get the desired result.

20. Distribution of Branches:AIBL started its working at 161; Motijheel C/A with a Branch named Motijheel Branch on 27 th

September, 1995 was the first & main Branch of AIBL and has been operating throughout the

15

country. The Head Office of the Bank was situated at the same holding of Motijheel Branch

since its establishment but from 11 January, 2007 it has started its working at its own premises

36, Dilkusha (6th, 7th, 8th & 9th floor), Dhaka-1000. The age of the Bank is only 11 years and

during this short period of time, the Bank has established total 46 Branches over the country and

made a smooth network inside the country. The number of Branches as Division wise is

mentioned in the following table:

Division No. of Branches

Dhaka Division 24

Chittagong Division 11

Rajshahi Division 4

Khulna Division 4

Sylhet Division 6

Barisal Division 1

Total 50

21. AIBL’s Products and Services:

Al-Arafah Islami Bank Limited is providing many product and services to satisfy their customers. For

that reason, AIBL has made significant progress in all areas of its operations within a short period of time,

such as deposit mobilization, credit management, remittance handling and foreign exchange and trade.

AIBL offers variety of products and services to the customers which are picked up below:

a. General Banking:

Current Account

Saving A/C

STD (Short Term Deposit) A/C

Fixed Deposit Account

1 Months Fixed Deposit

3 Months Fixed Deposit

6 Months Fixed Deposit

12 Months Fixed Deposit

16

Foreign Currency A/C

b. Foreign Exchange:

Letter of Credit Issue

Letter of Credit Advise

Foreign Documentary Bill Purchase (FDBP)

Foreign Documentary Bill Collection (FDBC)

Bill of Negotiation

Foreign Remittance

c. Services of the Bank:

ATM Card Service

Online Banking

Lookers Service

d. Products of AIBL:

Cash management

Wire transfer

Automated clearinghouse (ACH) transaction

Bill presentment and payment

Balance inquiry

Funds transfer

Downloading transaction information

Loan applications

Investment activity

Other value-added services

12. The Banking System in Bangladesh

The financial system of Bangladesh consists of Bangladesh Bank (BB) as the central bank, 4

nationalized commercial banks (NCB), 5 government owned specialized banks, 30 domestic

private banks, 11 foreign banks (including 2 Islamic Bank) and 28 non-bank financial institutions

including 1 Central bank. The financial system also embraces insurance companies, stock

exchanges and co-operative banks. The financial sector of Bangladesh is dominated by the

commercial bank. A number of national, private, foreign, specialized commercial bank and non-

17

banking financial institutions having a network of correspondents and branches are operating all

over the country and abroad to center to the people and business of the country. After the reform

program, the financial institutions are more systematic and borrowing and lending through

formal markets is increasing. Apart from normal commercial banking, banks are now providing

consumer credit scheme, and financing in industrial credit and development project. Electronic

commerce gives the banking industry a real competitive edge. The banking industry of our

country has started its journey soon after the liberation war in 1971. The early 70’s, immediately

after liberation, banking industry started its journey without any participation of the private

sector in a very restrictive financial system. In early 80’s few privet commercial banks were

allowed to start functioning. Due to lack of experience and absence of supervisory as well as

controlling environment, 1st generation private banks faced various problems in the next few

years. During the late 80’s and early 90’s, with the passage of Financial Sector Reform program,

Banking Regulation Structure suggested by BIS and followed by developed countries began to

start incorporation into the banking regulations of Bangladesh. The following table shows a few

snap shots that indicates a brief history of the banking industry of Bangladesh.

2. Corporate Information:

Name of the Bank Al Arafah Islami Bank Limited

Chairman Badiur Rahman

Vice Chairman Alhajj Mir Ahmad Sowdagar

Managing Director M A Samad Sheikh

Company Secretary Md Moffazzal Hossain

Legal Status Private Limited Company

Principal Activity Commercial Banking

Registered Office Peoples Insurance Building 36, Dilkusha C/A, Dhaka-1000

Date of Registration 18 June 1995

1st Branch opening Motijheel branch, Dhaka

18

Opening ceremony 27 September 1995.

Authorized Capital 2500.00 million.

Paid up capital 1383.81 million

Local Partnership of Capital 100%

Equity 2705.74 million

Number of Branches 50

Deposit 29690.13 million

Investment 29723.37 million

Number of manpower 1080

Number of shareholders 12013.

Phone 9567885, 9567819, 9569353, 9568007

Fax 880-2-9569351

SWIFT ALARBDDH

E-mail [email protected]

Website www.al-arafahbank.com

Slogan A rare combination of Shariah & modern banking

Logo

C. Financial Analysis of Al-Arafah Islami Bank

1. Al-Arafah Islami Bank’s Business Position:

19

Islam provides us a complete lifestyle. Main objective of Islamic lifestyle is to be successful both

in our mortal and immortal life. Therefore in every aspect of our life we should follow the

doctrine of Al-Qur’an and lifestyle of Hazrat Muhammad (Sm.) for our supreme success. Al-

Arafah Islami Bank started its journey in 1995 with the said principles in mind and to introduce a

modern banking system based on Al-Qur’an and Sunnah. A group of 13 dedicated and noted

Islamic personalities of Bangladesh are the member of Board of Directors of the bank. They are

also noted for their business acumen. Al-Arafah Islami Bank Ltd. has 46 braches and a total of

1033 employees (as of December 2007). Its authorized capital is Taka 2500 millions and the

paid-up capital is Taka 1153.18 millions.

(In million taka)

Particulars 2005 2006 2007 2008

Authorized Capital 1000.00 2500.00 2500.00 2500.00

Paid up Capital 677.94 854.20 1153.18 1383.81

Reserve Fund 542.22 835.98 1091.95 905.33

Shareholders Equity 1220.16 1690.18 2037.50 2705.74

Deposit 11643.66 16775.34 23009.13 29690.12

Investment 11474.41 17423.19 22906.37 29723.79

Import 12631.60 1882.14 27042.72 32685.13

Export 4932.90 914.27 12714.91 20176.64

Total Income 1452.68 2172.48 2955.61 4387.26

Total Expenditure 904.48 1202.71 2199.43 2859.16

Profit before Tax 548.20 855.47 756.18 1528.09

Profit after Tax 262.90 470.02 347.31 668.24

20

Income Tax 215.10 385.45 235.53 590.66

Total Assets 15336.89 21368.17 30182.32 39158.44

Fixed Assets 208.00 215.11 334.48 396.76

Earning per share (Taka) 387.80 550.24 30.12 48.29

Profit Earning Ratio 4.89

Dividend per share 26.00% 35% 20% 30%

No. of Shareholders 5402 4487 12013 10664

Number of Employees 771 912 1033 1080

Number of Branches 41 46 46 50

Manpower per Branch 19 20 23 22

a. Performance of AIBL at a glance:

The overall performances of AIBL are picked up as follows through graphical representation.

(In Million Taka)

21

2004 2005 2006 2007 2008

957.26 1220.16 1690.18 2037.5 2705.74

10108.3 11643.7

16775.3

23009.1

29690.12

8150.1611474.4

17423.2

22906.4

29723.79

348.89 548.2 969.770000000001756.180000000001 1528.1

Shareholders Equity

Deposite

Investment

Profit before Tax & Provision

Fig: Performance of AIBL

2. Progressive Analysis of AIBL:

At the end of current year, the number of depositors stood at 243,273 and the amount of deposit

has accumulated to Tk. 16775.33 million. The total numbers of investors are 13213 and total

investment extended to them was a sum of Tk. 17423.19 million.

The bank has earned Tk. 2172.48 million and incurred an expense of Tk. 1202.71 million in the

current year. At the end of the year the profit before tax has stood Tk. 855.74 million which is

78.97% more than Tk. 478.00 million pre-tax income of the last year.

a. Capital

The Bank company act 1991 which passed in March, 2003 includes a provision of raising the

capital to a new level of Tk. 100 core for the commercial banks. In compliance with the new

provision, the bank has raised its capital from Tk. 41.58 core in the year 2002 to Tk. 85.56 core

in 2003 by issuing a right share against each of existing shares in the year 2003 and declared

16% bonus dividend from the profit of the year 2003. The bank again declared 15.20% bonus

dividend from the profit 2004.as a result, the paid up capital of the bent stood at taka 67.79

million as at 31st December, 2005.

22

Bank declared 26.00% bonus dividend for the year 2005. As a result the paid up capital of the

bank stood at taka 85.42 million as at 31st December, 2006.

b. Reserved Fund

The total balance of the reserve fund stood at Tk. 835.94 million in the current year against Tk.

542.22 million compared to previous year 2005. In this fund, the bank experienced a growth rate

of 54.18%.s

c. Capital Adequacy

The Bangladesh Bank has fixed the ratio of capital adequacy against Risk-Weighted Assets at

9.00% in place of 8% in the month of September 2002. In 2002, the amount of total equity of the

bank was 41.57 core taka, which stood at Tk. 104.27 core in the year 2004 & taka 1309.56 cores

in the year 2005.This year it stood at taka 183.04 cores. At 31 December 2006, the capital

adequacy ratio of the bank is 10.71% against 12.17% at the same period of 2004.

2004 2005 2006 2007 2008

12874.6115336.89

21368.16

30182.32

39158.44

Fig: Total Assets (In Million Taka)

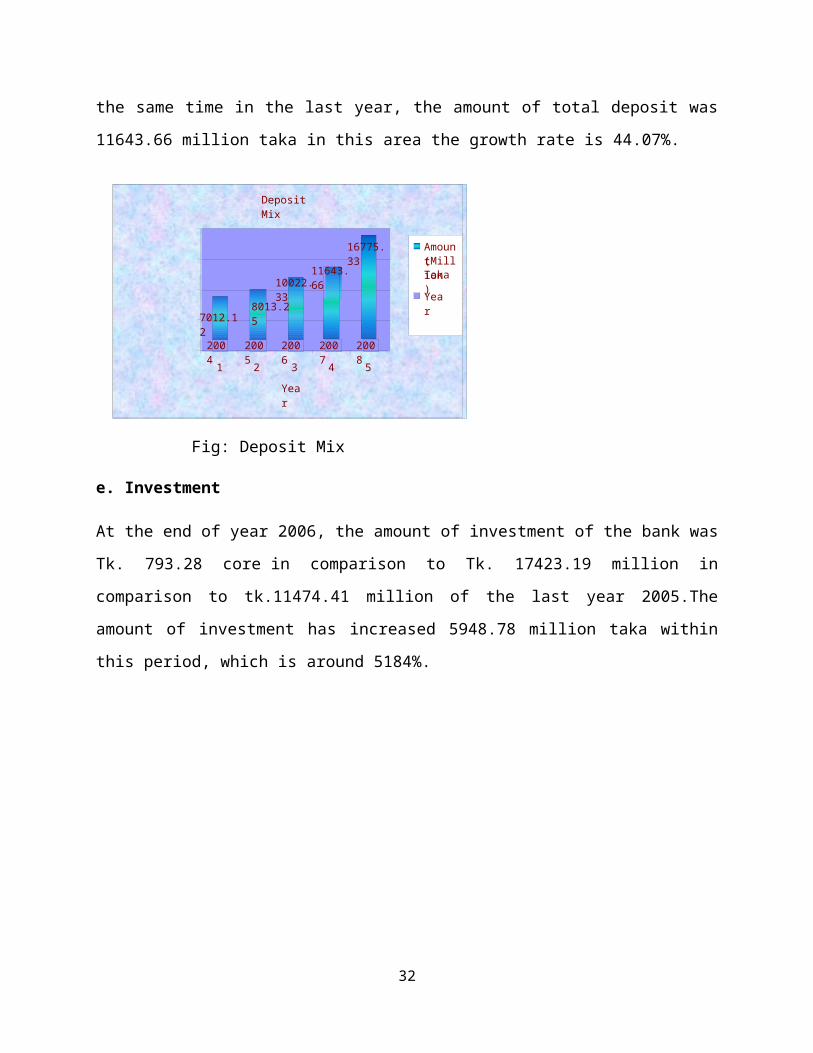

d. Deposit

The total deposit of the bank was Tk. 16775.33 at 31st December, 2006, of which bank deposit

was Tk. 611.72 million and general deposit was Tk. 843.40 core. At the same time in the last

year, the amount of total deposits was Tk. 16163.61 million taka. At the same time in the last

23

Deposit Mix

2004 2005 2006 2007 2008

7012.128013.25

10022.3311643.66

16775.33

1 2 3 4 5

Year

Amount(MillionTaka)

Year

Mode wise Investment: 31-12-2007

28%

16%3%1%

0%0%0%

49%

Bai-Murabha

Hire-PurchaseUnder

Shirkatul Melk

Bai-Muajjal

Quard

Bai-Salam

Mudaraba

Musharaka

Total

year, the amount of total deposit was 11643.66 million taka in this area the growth rate is

44.07%.

Fig: Deposit Mix

e. Investment

At the end of year 2006, the amount of investment of the bank was Tk. 793.28 core in

comparison to Tk. 17423.19 million in comparison to tk.11474.41 million of the last year

2005.The amount of investment has increased 5948.78 million taka within this period, which is

around 5184%.

24

Sector wise Investment

25%

16%4%2%3%1%

51%

Industrial

Commercial

Real Estate

Transport

Agriculture

Others

Total

Fig: Mode Wise Investment

Fig: Sector Wise Investment

f. Grameen & Small Medium Enterprise (SME) Scheme

An investment product “Grameen and Small Investment” is in operation. The objective of this

project is to introduce Shariah based banking system in rural and village area, creating

employment through financing to low income group, build up savings attitude, improvement of

living standard of rural low income mass people, creating opportunity to carry out Islamic

lifestyle by way of alleviating poverty and at the same time to make other financially established

by investing in small investment project. Initially this scheme was introduce in three branches of

AIBL i.e. Gallai, Comilla, Ruposhpur, Srimongol and Companigong Comilla. There is a plan to

expend this project gradually in other rural branches.

25

Investment Mix

2004 2005 2006 2007 2008

6030.25 7045.8 7500.25

11474.41

17423.19

1 2 3 4 5Year

Amountin

(Million

Year

Taka)

Fig: Investment Mix

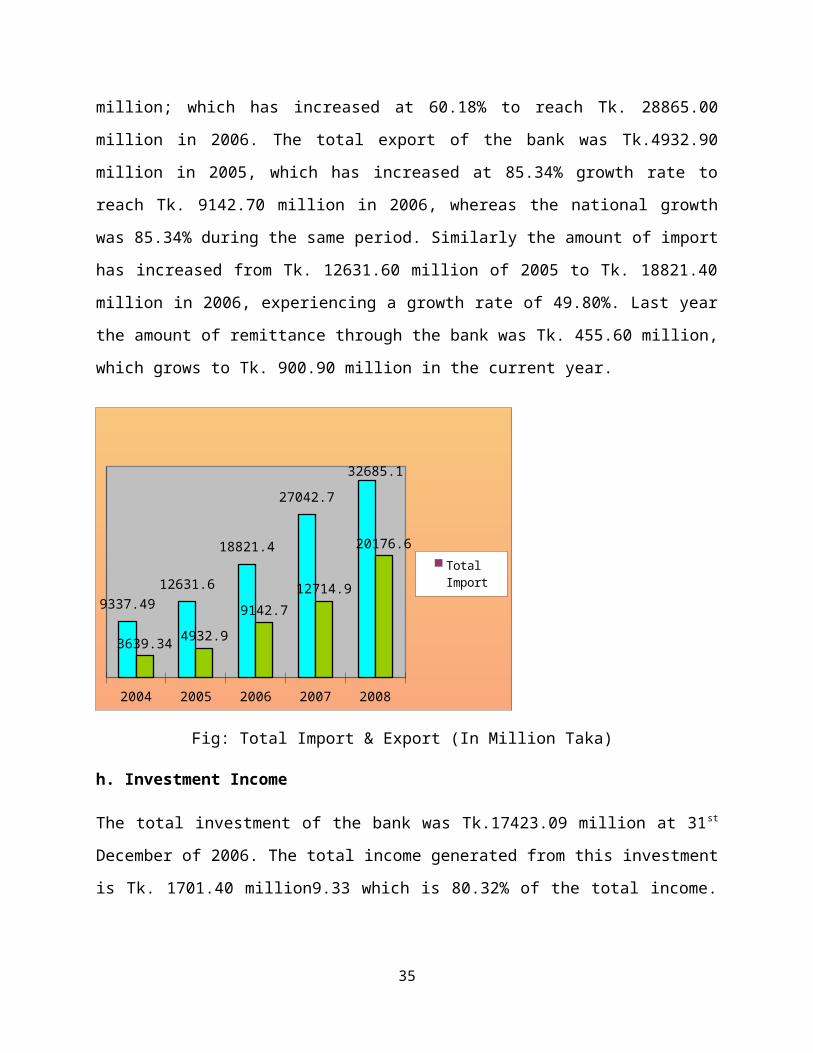

g. International Trade

At the year of 2006, the bank experienced satisfactory growth in the foreign trade. At the end of

2005, the total amount of foreign trade (Export, Import and Remittance) was Tk. 18020.10

million; which has increased at 60.18% to reach Tk. 28865.00 million in 2006. The total export

of the bank was Tk.4932.90 million in 2005, which has increased at 85.34% growth rate to reach

Tk. 9142.70 million in 2006, whereas the national growth was 85.34% during the same period.

Similarly the amount of import has increased from Tk. 12631.60 million of 2005 to Tk. 18821.40

million in 2006, experiencing a growth rate of 49.80%. Last year the amount of remittance

through the bank was Tk. 455.60 million, which grows to Tk. 900.90 million in the current year.

26

2004 2005 2006 2007 2008

9337.4912631.6

18821.4

27042.7

32685.1

3639.34 4932.9

9142.7

12714.9

20176.6Total ImportTotal Export

Fig: Total Import & Export (In Million Taka)

h. Investment Income

The total investment of the bank was Tk.17423.09 million at 31st December of 2006. The total

income generated from this investment is Tk. 1701.40 million9.33 which is 80.32% of the total

income. At the corresponding period of 2002, this income was Tk. 78.32 of the total income.

m. Risk Management of AIBL

The risk of Al-Arafah Islami Bank limited is defined as the possibility of losses, financial or

otherwise. The risk management of the Bank covers 5 (five) Core risk Areas of banking i.e.

Credit risk management, foreign exchange risk management, Assets Liability Management,

prevention of money laundering and establishment of Internal Control and Compliance. The

prime objective of the risk management is that the Bank takes well calculative business risks

while safeguarding the Bank's capital, its financial resources and profitability from various risks.

In this context, the Bank takes steps to implement the guidelines of Bangladesh Bank.

The failure may result from unwillingness of the counter party of decline in his/her financial

condition. Therefore, Bank's credit risk management activities have been designed to address all

these issues.

27

3. Economic Impact Analysis of AIBL:

Economic impact can be defined as any increase or decrease in productive potential of an

economy. By analyzing the economic impact we can understand how a bank adds value to the

society. Economic impacts can be broadly categorized as:

i) Direct Impact

ii) Indirect Impact

a. Direct Impact

Direct impacts are the immediate economic effects resulting from the banks financial

transactions. Bank’s direct contribution to the economy resulted in the creation of employment

opportunities, payment of tax to the government and maximization of shareholders wealth.

b. Indirect Impact

Indirect impacts are the spill over economic effects that occur through Bank’s normal course of

operations. Banks generate indirect impact by addressing the deficiency of capital in the

economy by mobilizing deposit and channeling the same to prospective investors.

Through catering financial services, the Bank helped distribute the wealth among all the

stakeholders for example shareholders received dividend, depositors and investors got profit,

employees received compensation and other benefits, the under privileged reaped benefits out of

CSR while the government government earned tax revenue.

At the end of 2008, the Bank mobilized total deposits of BDT 29,723.79 million as investment to

different sectors of the economy. Apart from these, the Bank performed significant import and

export business.

D. Functions of Al-Arafah Islami Bank Ltd.

Functions of AIBL:Islamic banks render almost similar services to their customer’s conventional banks do.

Like a conventional bank, AIBL also accepts deposits from customers and advances

loans. AIBL also acts as a custodian of its customers and performs all foreign

transactions on behalf of them. AIBL perform mainly three different types of functions.

28

1. General Banking Activities of AIBL:

General Banking activities of AIBL are performed through the following areas:

E. Foreign Exchange of Al-Arafah Islami Bank Ltd.

Foreign Exchange Department of AIBL:

29

Customer Relation Desk-1

1. Buildup relation with clients.

2. Account opening (operating)

Current A\C Saving A\C MSTD MMSS MHD MED3. Account

Closing4.Issue cheque

book5.Posting of

opening & closing accounts.

6.Proper maintaining of KYC form & other necessary

Customer Relation Desk-2

(Non-operating)

1. Buildup relationWith clients.

2. Accountopening (non-operating)

FDR3. Profit giving

voucher issue of FDR

4. Remittance: Pay Order TT DD

1.

Clearing

1. Cheque receives for collection.

2. Cheque, PO, DD, TT receive for transfer.

3. Nikash maintaining, printing & copy and validation print.

4. LBC issue & receive.

5. OBC issue & receive.

6. IBCA/IBDA issue & receive.

7. Preparing salary sheet.

8. Issue expenditure voucher.

9. Different statement preparation for Head office &

Cash

1. Receiving & payment of cash.

2. Signature verifying.

3. Accounts checking of funds sufficiency for any payment.

4. Maintaining share transactions.

5. Providing income tax certificate.

6. Solvency certificate.

Dispatch

1. Provides documents sending with date & number.

2. Receive documents from courier.

3. Sends documents through courier.

General Banking

Financial institutions especially banks play a very important role in foreign exchange transaction

of a country. Mainly transactions with overseas counties of imports, exports and foreign

remittance are the main function of the Foreign Exchange department.

Foreign exchange refers to the process or mechanism by which the currency of one country is

converted into the currency of another country. Foreign exchange is the means and methods by

which rights to wealth in a country's currency are converted into rights to wealth in another

country's currency Foreign Exchange Department plays significant roles through providing

different services for the customers. Opening or issuing letters of credit is one or the important

services provided by the banks.

1. Opening LC in AIBL:

There are several factors for what customers come to this bank to open LC. The procedures,

techniques, facilities, services and other factions for opening LC are stated details as follows:

a. Letter of Credit:

A letter of credit is a letter issued by a bank (known as the opening or the issuing bank) at the

instance of its customer (known as the opener) addressed to a person (beneficiary) undertaking

that the bills drawn by the beneficiary will be duly honored by it (opening bank) provided certain

conditions mentioned in the letter have been complied with.

b. Parties of the L/C

Importer Who applies for L/C

Issuing Bank It is the bank which opens/issues a L/C on behalf of the

importer.

Confirming Bank It is the bank, which adds its confirmation to the credit and it

is done at the request of issuing bank. Confirming bank may

or may not be advising bank.

Advising or Notifying

Bank

It is the bank through which the L/C is advised to the

exporters. This bank is actually situated in exporter’s country.

It may also assume the role of confirming and / or negotiating

30

bank depending upon the condition of the credit.

Negotiating Bank It is the bank, which negotiates the bill and pays the amount

of the beneficiary. The advising bank and the negotiating

bank may or may not be the same. Sometimes it can also be

confirming bank.

Accepting Bank It is the bank on which the bill will be drawn (as per

condition of the credit). Usually it is the issuing bank.

Reimbursing Bank It is the bank, which would reimburse the negotiating bank

after getting payment – instructions from issuing bank.

c. Issuing Bank

The Issuing Bank or the Opening Bank is one which issues the credit i.e. undertakes,

independent of the undertaking of the applicant: to make payment provided the terms and

conditions of the credit provides for sight payment, or at with. The payment may be at sight if the

credit provides for sight payment or at maturity dates if the credit provides for deferred payment.

Especially the issuing bank should satisfy himself on the credit worthiness of the applicant. The

credit application must be in accordance with the Uniform Customs and practices for

Documentary Credit (UCPDC) LC publication no. 500 edition of 1993.

d. Advising Bank

The Advising Bank advises the credit to the beneficiary authenticating the genuineness of the

credit. The advising bank is generally situated in the country/place of the beneficiary.

e. Confirming Bank

A confirming Bank is one which adds its guarantee to the credit opened by another bank,

thereby, undertaking the responsibility of payment / negotiation / acceptance under the credit in

addition to that of the issuing bank. A confirming bank normally docs so if requested by the

issuing bank. When the creditworthiness of the issuing bank is in doubt, beneficiary's bank may

31

request the issuing bank to give additional confirmation by another bank. It is said Add

Confirmation in practices.

f. Negotiating Bank

A Negotiating Bank is the hank nominated or authorized by the issuing bank to pay, to incur a

deferred payment liability, to accept drafts or to negotiate the credit.

g. Reimbursing Bank

A Reimbursing Bank is the bank authorized to honor the reimbursement claims in settlement of

negotiation / acceptance / payment lodged with it by the negotiating bank or accepting bank. It is

normally the bank with which the issuing bank has account from which payment is to be made.

Reimbursement claims in foreign exchange business settled by the Uniform Rules for

Reimbursement (URR)–ICC publication no. 525.

2. Import Business:

Import trade in Bangladesh is controlled under the Import and Export control Act 1950.

Authorized Dealer Banks will import the goods into Bangladesh following the import policy,

public notice, F.E. circular and other instructions from competent authorities from time to time.

Import payments during 2007-08 amounted to US$ 21600 million (27.30% of GDP) compared to

US$ 17157 million (25.10% of GDP) in 2006-07 showing an increase of 26.0% in 2007-08

compared to 16.30% increase in 2006-07. The significant increase in the overall volume of

imports stemmed from imports of capital goods, consumer & intermediate goods, and imports by

EPZs.

The Year Wise Import as Follows:

Year 2002 2003 2004 2005 2006 2007

Import

Business

5559.27 5162.51 7698.29 9337.49 12631.60 18821.40

32

Import Business

116%

216%

317%

417%

517%

617% 1

2

3

4

5

6

Fig: 1.1 Performance of Import Business

a. Process to Open a L/C

If a party comes to open a LC at this branch then the following requirement is required-

a. Current A/C

b. Registration Certificate /IRC

c. TIN /VAT certificate

d. Insurance Cover Note

e. Indeed / Invoice

f. LCA(Letter of Credit Authorization) agreement form

g. Foreign Exchange Regulation Act, 1947 form (IMP)

Other payment of the party-

a. Insurance cover note with payment order commission and vat

b. Margin (% of LC value)

Then the bank opens the LC and sent to the beneficiary’s bank. In case of foreign LC, the

documents are sent through swift

Then the exporter or beneficiary sent the goods and beneficiary bank sent document which

refers that the party has sent the goods.

And this issuing bank has to pay to the beneficiary’s bank. For this the branch sent the

payment amount to the HOID (Head Office International Division) and the HOID pays this

amount through NOSTRO A/C of the bank.

The duplicate copy of the LC needs to release the goods from the customs. And the bank

supplies this document to the party to release their goods from the custom.

33

The bank has to inform about the LC and goods to the Bangladesh Bank in Foreign Exchange

Regulation Act, 1947 form (IMP). And then the LC is closed.

C.prosediors Prepare a L/C

To prepare a L/C the branch takes care on the following points:

L/C Number Place and date of issue

Date and place of expiry Shipment date

Presentation period Applicant

Beneficiary Advising Bank

Amount Availability

Tenure of the draft Documents required

Payment UCP

Bill of lading Bill of Exchange

Pre-shipment Inspection Data content

Special conditions Authenticity of the credit

Part-shipment and Trans shipment Port of shipment and port of destination

3. Export Business:

The goods and services sold by Bangladesh to foreign households, businessmen and Government

are called export. The export trade of the country is regulated by the Imports and Exports

(control) Act, 1950. There are a number of formalities, which an exporter has to fulfill before

and after shipment of goods. The exports from Bangladesh are subject to export trade control

exercised by the Ministry Of Commerce through Chief Controller of Imports and Exports (CCI

& E). No exporter is allowed to export any commodity permissible for export from Bangladesh

unless he is registered with CCI & E and holds valid Export Registration Certificate (ERC). The

ERC is required to be renewed every year. The ERC number is to be incorporated on EXP forms

and other documents connected with exports.

34

The Year Wise Export as Follows:

Year 2002 2003 2004 2005 2006 2007

Export Business 2524.63 1894.77 3075.52 3639.34 4932.90 9142.70

Export business

116%

216%

317%

417%

517%

617%

1

2

3

4

5

6

Fig: 1.2 Performance of Export Business

a. Back to Back L/C:

A back to back mechanism involves two separate L/C. One is master export L/C and another is

back to back L/C. On the strength of Master L/C, Bank issues Back to Back L/C. Back to Back

L/C is commonly known as Buying L/C. On the contrary, Master Export L/C is known as

Selling.

It is simply issued to the clients against an import L/C. Back-to-Back mechanism involves two

separate L/C. One is master Export L/C and another is Back-to-Back L/C. On the strength of

Master Export L/C bank issues bank to Back L/C. Back-to-Back L/C is commonly known as

Buying L/C. On the contrary, Master Export L/C is known as Selling L/C.

Features of Back to Back L/C:

An Import L/C to procure goods /raw materials for further processing.

It is opened based on Export L/C.

It is a kind of Export Finance.

35

Export L/C is at Sight but back to Back L/C is at insurance.

No margin is required to open Back to back L/C

Application is registered with CCI&E

Applicant has bonded warehouse license.

L/C value shall not exceed the admissible percentage of net FOB value of relative Master

L/C.

Insurance period will be up to 180 days.

The import L/C is opened for 75% of the value of Export L/C.

Here L/C issued against the lien of export L/C.

Arrangements are such that export L/C matures first then out of this export profit, import

L/C is paid out.

(1) Documents Required for Opening a Back-to-back L/C:

In Al-Arafah Islami Bank Ltd Principal Branch, following papers/ documents are required for

opening a back-to-back L/C-

1. Master L/C

2. Valid Import Registration Certificate (IRC) and Export Registration Certificate (ERC)

3. L/C Application and LCAF duly filled in and signed

4. Performa Invoice or Indent.

5. Insurance Cover Note with money receipt.

6. IMP Form duly signed.

In addition to the above documents, the followings are also required to export oriented garment

industries while requesting for opening a back-to-back L/C –

1. Textile Permission.

2. Valid Bonded Warehouse License.

(2) Procedure for Foreign Documentary Bill Purchase (FDBP):

If all the documents are in order then the bank purchase the documents. Several things

should be checked at the time of purchasing.

How much back-to-back and PC (packing Credit) facility the client has taken.

36

After taking all these charges, the rest amount is paid to the client and a FDBP account is

opened.

(3) Foreign Documents Bills for Collection (FDBC):

Al-Arafah Islami Bank Ltd forwards the documents for collection due to the following reasons:

If the documents have discrepancies

If the exporter is new client

The banker is in doubt.

Foreign documentary bills for collection signifies that the exporter will received payment only

when the issuing bank gives payment. The exporter submits duplicate EXP from and commercial

invoice subsequently.

4. Foreign Remittance

Foreign remittance plays a significant role in a banking system though economy system of a

country. Like other Al-Arafah Islami Bank Ltd also have a department of foreign exchange

dealing. Mostly US dollar, Euro, British pound and other remittances like Australian dollar,

Canadian dollar, Malaysian ringgit and currencies of Middle East have been dealing here. Other

Al-Arafah Islami Bank Ltd buys and sells all regular kinds of foreign currencies though foreign

exchange department is not available in all the branches of Al-Arafah Islami Bank Ltd.

a. Outward Remittance:

On March 24, 1994 Bangladesh Taka was declared convertible for current international

transaction. As a result remittance becomes more liberalized. Outward remittance include sale of

Foreign Currency by TT, MT, Draft, TC or in cash for private, official and commercial purpose.

Traveler's Cheque

Travelers Cheque (TC) is an instrument for a specific amount of widely accepted foreign

currencies, issued in favor of Travelers/ Visitors to carry foreign exchange for meeting heir

expenses in abroad.

37

Traveler's cheque may be in different currencies, such as US Dollar, Pound Starling, Japanese

Yen, Saudi Riyal, Canadian Dollar, French Frank, German Marks, and Swiss Frank etc. But

traveler's cheque is not issued in this branch.

Issuance of Outward DD and TT :

ADs may also issue DD, TT on their foreign correspondent favoring Bangladesh nationals or

foreign nationals as per their entitlement. But foreign TT and DD are not issued in this branch.

b. Inward Remittance:

The term inward remittance includes not only purchase of foreign currency by TT, MT, Draft

etc. but also purchase of bills, purchase of TC. Utmost care should be taken while purchasing

notes, TC, DD and similar instrument for protecting the bank from probable loss as well as safety

of the bank officials concerned. But this type of purchase is not done in this branch.

c. Collection of Foreign Currency Instrument: Principal Branch collects foreign remittance

through the following instruments on behalf of their customer-

Money Gram

Express money

Instant cash

Placid express

Remit master

2. SWOT ANALYSIS of AIBL

SWOT analysis facilitates the organization to make their existing line of performance and also

foresee the future to improve their performance in comparison to their competitors. As though

this tool, an organization can also study its current position, it can also be considered as an

important tool for making changes in the strategic management of the organization.

a. STRENGTHS:

Bank reputation AIBL has already established a favorable reputation in the banking industry of

the country with its significant business growth. With in a period of 14 years, AIBL has already

38

established a firm footing in the banking sector having tremendous growth in the profits and

deposits. All these have leaded them to earn a reputation in the banking field.

Corporate Culture

AIBL has an interactive corporate culture. Unlike other local organization, AIBL’s working

environment is very friendly, interactive and informal. There are no hidden barriers or

boundaries while interactive among the superior or the subordinate. The environment is also

lively and since the nature of the banking job itself is monotonous and routine, AIBL’s lively

work environment boosts up the sprit and motivation of the employees.

Team Work at Mid level & Lower level

At AIBL’s mid level and lower level management, there are often team works. Many jobs are

performed in-groups of two or three in order to reduce the burden of the workload and enhance

the process of completion of the job. People are eager to help each other and people in general

are devoted to w

Quality: Al-Arafah Islami Bank strives to endow its customers with appreciable quality in every

service it provides. Customer satisfaction claims the highest priority, as it should be in any

service-oriented organization.

Adaptability :Al-Arafah Islami Bank draws its strength from the adaptability and dynamism it

possesses. It has quickly adapted to world class standard in terms of banking services. Al-Arafah

Islami Bank has also adopted state of the art technology to connect with the world for better

communication to integrate facilities.

Efficient Management

All the levels of management are solely directed to maintain a culture for the betterment of the

quality of the service and for developing a brand image in the market through the organization’s

wide team approach and horizontal communication system.

39

Human Resource Expertise

One of the key-contributing factors behind the success of Al-Arafah Islami Bank is its HR who is

highly trained and most competent in their own respective fields. Al-Arafah Islami Bank

provides its employees with training both in-house and outside job.

Financial Strength

Al-Arafah Islami Bank is a financially sound company. As a result customers feel comfortable

and more secure while dealing with the bank. It’s already established its position in the banking

industry of Bangladesh. They achieved a high growth rate accompanied by an impressive profit

growth rate in 2006. The number of deposits and the loans and advances are also increasing

rapidly from year to year.\

b. WEAKNESSES

Limited Workforce

Al-Arafah Islami Bank has very limited human resources compared to its financial activities.

There are not many people to perform most of the tasks. As a result many of the employees are

burdened with extra workloads and works late hours without any overtime facilities. This might

cause high employee turnover that will prove to be too costly to avoid.

Liquidity Crisis

Average asset quality and tight liquidity position is another weakness of Al-Arafah Islami Bank

Limited. Bank’s asset quality is not up to the standard as SCB or CITI N.A. or Prime Bank.

Sometimes the bank faces liquidity crisis especially during the period of vacation which needs to

be checked by the bank otherwise the bank will be in deep trouble in near future.

Lack of Qualified System Operators

Currently AIBL’s Head office and in the Branches, there are system operators who do not have

any background academic knowledge on computer applications. As a result they frequently make

mistakes in the preparation of various computerized statements. At the same time, computer

operators do not have the skill to carry out their activities. Above all its MIS is still on primary

40

stage which needs to be modified as soon as possible to compete in the market.

c. OPPORTUNITIES

Government support

Government of Bangladesh has provided its full support to the banking sector for a sound

financial status of the country, as it is becoming one of the vital sources of employment in the

country now. Such government concern will facilitate and support the long-term vision for Al-

Arafah Islami Bank.

Evolution of Online Banking

Emergence of e-banking will open more scope for Al-Arafah Islami Bank to reach the clients not

only in Bangladesh but also in the global area. It will also facilitate wide area network in

between the buyer and the production unit of Al-Arafah Islami Bank Ltd. to smooth operation to

meet the desired need with least deviation.

DiversificationAIBL can pursue a diversification strategy in expanding its current line of business. The

management can consider options of starting client service in its merchant banking division.

Product line proliferation

In this competitive environment AIBL can expand its product line to enhance its Sustainable

Competitive Advantage (SCA). As a part of its product line proliferation, AIBL can concentrate

more on SME & Agro based industrial loan because these two sectors have huge potential.

d. THREATS

Multinational Banks:

The emergence of the multinational banks and their rapid expansion poses a potential threat to

the new PCB’s. Due to the booming energy sector, more foreign banks are expected to arrive in

Bangladesh. Moreover, the already existing foreign banks such as Standard Chartered are now

pursuing an aggressive branch expansion strategy. These banks are establishing more branches

countrywide and are expected to get into for operation soon. Since the foreign banks have

tremendous financial strength, it will pose a threat to local banks to a certain extent in terms of

41

grabbing the lucrative clients.

Upcoming Banks:

The upcoming private local banks can also pose a threat to the existing PCB’S. It is expected that

in the next few years more local private banks may emerge. If that happens the intensity of

competition will rise further and banks will have to develop strategies to complete against an on

slaughter of foreign banks.

Mergers and acquisitions:

The worldwide trend of mergers and acquisition in financial institutions is causing concentration

in power in the industry and competitors are increasing in power in their respective areas.

Contemporary Banks:

The contemporary banks of AIBL such as Dhaka Bank, Prime Bank, Eastern Bank and Dutch-

Bangla Bank are its major rivals. Prime Bank and others are carrying out aggressive campaign to

attract lucrative corporate clients as well as big time depositors. AIBL should remain watchful

about the steps take by these banks as these will in turn affect AIBL strategies.

Political Instability:

Unstable political situations cause great distraction in the otherwise smooth flow of business.

Sudden Hartals and other political programs sometimes present problems for the employees (esp.

female employees) in commuting to and from the office. Political instability also promotes a

weak law and order system leading to an increase in crime rate in the society. This might also be

considered as a potential external threat for a financial institution.

G. Ending Part of the Report:

1. Findings of the Study:

Some findings of Al-Arafah Islami Bank Limited, Uttara Model Town Branch are given below-

In Foreign Exchange Department they follow the traditional banking system. The entire

Foreign Exchange procedures are not fully computerized.

Service personnel are working under pressure because they have to deal with large number of

customer every day.

42

Technology that AIBL is using for their banking system is not updated. Now there is some

international bank in Bangladesh, they are very fast and very up dated.

The Al-Arafah Islami bank is too much centralized. For each and every work, branch office

has to get permission from the head office. The head office tightly controls each and every

branch

Lack of information to get and sitting arrangement in the branch is a trouble for the

customers.

Advertising and promotion are the weak point of Al-Arafah Islami Bank Ltd. AIBL does not

have any effective marketing activities. Others banks have betters marketing strategy.

Al-Arafah Islami Bank Ltd has less amount of foreign exchange business compare to other

Banks.

Lack of competitiveness in product and service innovation.

2. Recommendations:

The fast pace of growth in the Islamic financial sector and the emergence of conventional

finance companies offering Islamic products and services has brought critical attention to key

issues facing this sector. Some of the core issues identified after analyzing this report that Al-

Arafah Islami Bank Limited should give lots of attention in many sectors, which are given

below.

Increased market transparency is needed to enhance credibility and increase consumer

confidence. The application of relevant international accounting standards will enhance

transparency of Islamic financial institutions and the comparability of financial

statements. At this stage, Islamic product standards and accounting practices are not yet

accepted globally.

Increased education is needed to ensure that the Shariah standards are understood and

accepted across the industry by regulators, international organizations, and the private

sector.

Foreign exchange department should be fully computerized and reduce the paper based

work to make it more smooth and faster.

43

A robust regulatory and supervisory framework is necessary to maintain financial

stability and growth of Islamic finance as a viable, resilient, and sustainable sector. The

unique characteristics of Islamic banking operations and Islamic financial instruments

require the development of a regulatory-supervisory framework that adequately addresses

the requirements of this industry.

The authority of AIBL should exert pressure on Government bodies to run proper and

sufficient application of Islamic banking laws in Bangladesh.

At the beginning time of opening of Letter of Credit, every officer should check the

required documents very carefully whether there is any mistake or not.

Inclusion of more subjects based on the Quran and Sunnah in the Training courses of

the Islami Bank Training & Research Academy in order to develop human

resources having morally.

Arrangement of monthly /quarterly training courses /workshops for the clients should be

selected by the Branches in order to promote Foreign Exchange activities of the desired

level.

To fulfill the vision of "mass banking" this Bank should provide more foreign exchange

and other sorts of facilities to new customers/new entrepreneurs /new businessmen/ new

companies etc.

AIBL should give more emphasize on their marketing effort and try to increase

their sales force.

AIBL should try to attend different type of target customers.

AIBL should Introduce Islami Debit and Credit Cards as soon as possible.

They should carryout more promotional activities to make clients aware about their

offers.

It was observed that, AIBL is absent in TV, Print Media, Bill Boards, and

Sponsorships etc. The Bank should advertise about itself and its offers so that

it can attract more customers that will increase the business volume of the bank.

44

AIBL should give the highest attention on recovery of bad things related to opening

LC. This concerns the worst image of the Bank to the clients

AIBL should utilize "Internship Program" as one kind of promotion policy to encourage

its present and potential customers/clients. Because, young generations are the vital post of

our economy. To do so this Bank should provides facilities to the internees through

proper placement and practical operations as well as job certainty to those who bring

introduced themselves the best performers in doing their particulars.

3. Conclusion:

The concept of Islami Banking is several decades old. The third attempt to establish an Islamic

Financial Institution took place in Pakistan in the late 1950s with the establishment of a local

Islami Bank in a rural area (Wilson 1995. After 45 years, Islamic Banking system is established

in Bangladesh as a financial institution that is named “Al-Arafah Islami Bank Limited”.

Al-Arafah Islamic Bank Limited is a Bank which operates its activities according to Quaran and

Sunnah. Its banking activities based on profit \ loss sharing. It does not create any illegal

pressure on client.

On the other hand, every client is not 100% honest. So they are taking investment from AIBL

and after maturity, they are showing loss on that project intentionally. So AIBL is losing some

profits from their investment. For this reason, Al-Arafah Islami Bank Limited has closed its bai

- mechanism. Now it is not providing investment under this mechanism.

Threats of Al-Arafah Islami Bank Limited are - at this time, many financial institutions have

commenced their financial activities according to Islamic shariah. This type of organization will

create more competition in the financial market. So it is a threat for Al-Arafah Islami Bank

Limited.

Although it is facing some problem, it has a bright future and day-by-day it is enhancing its

financial activities over the country. Many organizations are following to AIBL and they are

starting their business based on Islamic shariah in the economy of Bangladesh.

After all, Al-Arafah Islami Bank is increasing its reputation day after day through providing

various sorts of innovative product and service. Moreover, AIBL,s customer services and

45

management are also being enhanced. Foreign Direct Investment Department will be fully

computerized soon.

H. Appendix Part:

1. Bibliography

Ivancevich, John M., and Steven J. Skinner. “Business for the 21 st Century ”. Boston: Irwin,

2003.

Kotler, Philip. “Marketing Management”. 9th ed. New Delhi:

Prentice-Hall, 1999.

Kinnear, Thomas C., and James R. Taylor. “Marketing Research: An Applied Approach”. 5th ed.

New Delhi: McGraw Hill, 2003.

Annual Report, Al-Arafah Islami Bank Limited, 2008 - Published by AIBL.

“A Journal of Islamic Banking” – Published by AIBL

46