webinar slides - audit evidence and conclusions

TRANSCRIPT

Audit Evidence14 May 2021

Housekeeping

• Webinar will run for about 40 minutes with Q&A at the end• Webinar will be recorded and agency will publish on our website• Have microphones on mute and cameras off during the webinar• Questions can be typed into the chatbox. Open it using the button in top right corner of your screen:

Agenda

• Common issues with Audit Evidence

• The technical part

• Case studies• 1 – HIR• 2 – Forecasts in safeguard mechanism

• Question time

Agenda

• Common issues with Audit Evidence

• The technical part

• Case studies• 1 – HIR• 2 – Forecasts in safeguard mechanism

• Question time

• Underpins audit quality and consistency• Most of auditor’s work is obtaining and evaluating evidence• Provides a basis for the audit opinion

Why

• Design and perform “unbiased” audit procedures• Document the evidence obtained• Evaluate audit evidence

What

• Consider sufficiency and appropriateness• Individual risks level and overall stand back• Consider bias, inconsistent evidence

How

Audit Evidence

How much evidence is enough?

Can I rely on a stat dec?

What if no documentation was prepared at the time of the event/activity?

Can I rely solely on oral representations from the client?

Should I disclose any limitations in audit evidence in Part B?

Agenda

• Common issues with Audit Evidence

• The technical part

• Case studies• 1 – HIR• 2 – Forecast in safeguard mechanism

• Question time

Audit evidence means information used by the auditor in arriving at the conclusions on which the auditor’s opinion is based

Audit evidence includes both:‐ information contained in the accounting

records underlying the subject matter; and‐ information obtained from other sources

Audit evidence is obtained from the performance of audit procedures:‐ Analytical procedures‐ Observation‐ Inquiry – ordinarily does not provide

sufficient evidence on its own‐ Inspection‐ Confirmation‐ Re‐performance

• Supporting data spreadsheets• Invoices/Statements from proponent’s suppliers• Notes of inquiries with the proponent/agent• Notes of observations during site visits

Key standards and concepts?

ASA 500 Audit Evidence

ASA 705 Modifications to the Opinion in the

Independent Auditor’s Report

Audit Evidence

Sufficient

Appropriate

Persuasive

Relevant

Reliable

Accessible

Available

Understandable

Corroborative

Inconsistent

Qualification

Adverse

Disclaimer

Part A

Part B

The objective of the auditor is to design and perform audit procedures in such as way as to obtain sufficient, appropriate evidence to be able to draw reasonable conclusions on which to base the auditor’s opinion

Reasonable assurance is obtained when the auditor has obtained sufficient, appropriate evidence to reduce audit risk (risk of giving the wrong opinion) to an acceptably low level

Audit Evidence

Sufficient

Appropriate

Relevant

Reliable

AccessibleAvailable

Understandable

Corroborative

Inconsistent

Audit Evidence

Sufficient

Appropriate

Relevant

Reliable

AccessibleAvailable

Understandable

Corroborative

Inconsistent

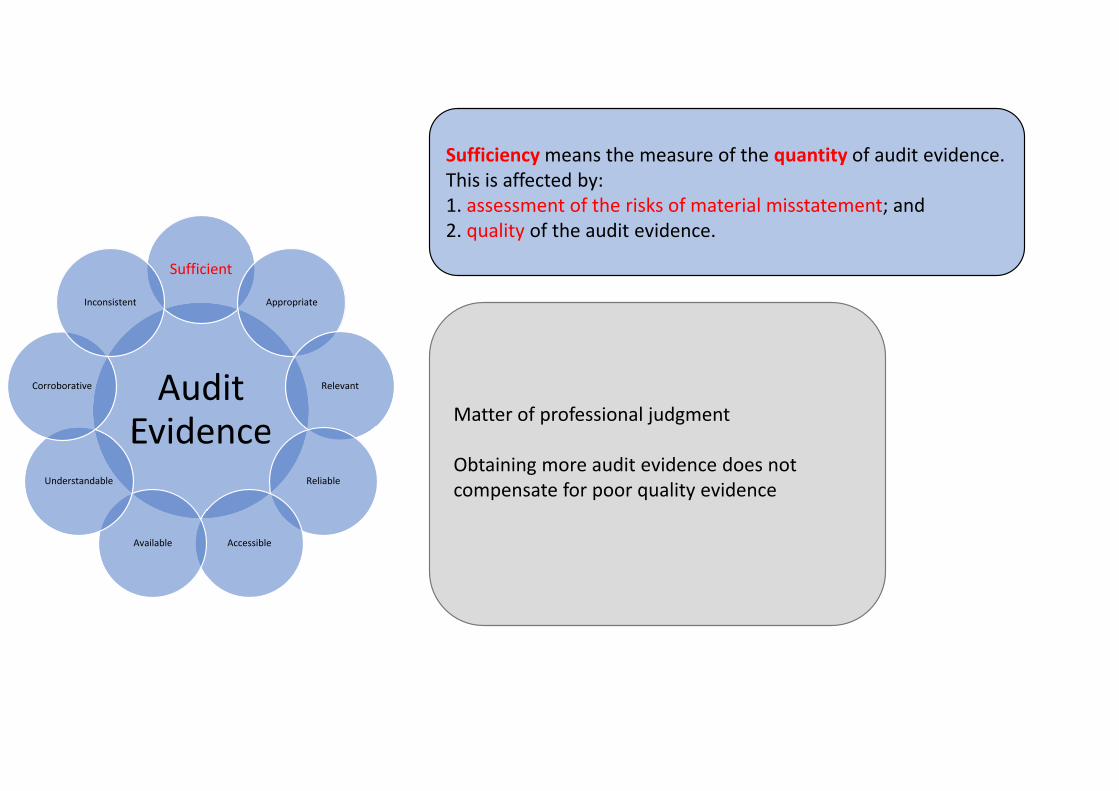

Sufficiencymeans the measure of the quantity of audit evidence. This is affected by:1. assessment of the risks of material misstatement; and2. quality of the audit evidence.

Matter of professional judgment

Obtaining more audit evidence does not compensate for poor quality evidence

Audit Evidence

Sufficient

Appropriate

Relevant

Reliable

AccessibleAvailable

Understandable

Corroborative

Inconsistent

Appropriatenessmeans the measure of the quality of audit evidence. This is: ‐ Relevance‐ Reliability

Not all audit evidence is of the same quality.

Attributes such as:‐ the source of evidence ‐ internal or external‐ knowledge of the person responding to inquiryare considered in assessing the quality of evidence

Audit Evidence

Sufficient

Appropriate

Relevant

Reliable

AccessibleAvailable

Understandable

Corroborative

Disconfirming

Relevance is about the logical connection with the purpose of the audit procedure

• For example:In order to understand the control environment over the ongoing operation of a project, a high level discussion of the controls that exist may not meet this objective

Audit Evidence

Sufficient

Appropriate

Relevant

Reliable

AccessibleAvailable

Understandable

Corroborative

Disconfirming

The reliability of information to be used as audit evidence is influenced by :‐ its source;‐ its nature; and ‐ the circumstances under which it is obtained

• For example:When using information prepared by the entity, evaluate reliability by obtaining evidence about its completeness and accuracy and whether it is sufficiently precise and detailed

When information to be used as audit evidence is obtained from sources external to the entity, circumstances may exist that could affect its reliability. The source may not be knowledgeable, or a management’s expert may lack objectivity.

Consider:‐ Modifications or additions to audit procedures‐ Other impacts on the audit, for example reliability of other

representations made by management

Client generated internal

Client generated external

Auditor generated

Reliability of audit evidence

Sources of evidence

Management’s expert

Audit Evidence

Sufficient

Appropriate

Relevant

Reliable

AccessibleAvailable

Understandable

Corroborative

Disconfirming

Accessible – Does the auditor have access to the evidence?Available –Was evidence prepared at all?Understandable – Can the auditor understand the evidence?

Accessible – Where sites are not readily accessible

Available – No record of the performance ofongoing monitoring was prepared

Understandable – Highly complex production models

The absence of information, for example, refusal to provide a representation, or lack of records prepared at the time of an activity or event, also constitutes audit evidence

Audit Evidence

Sufficient

Appropriate

Relevant

Reliable

AccessibleAvailable

Understandable

Corroborative

Inconsistent

Corroborative evidence is information that supports and is consistent with managements assertions

Inconsistent evidence is where audit evidence from one source is inconsistent or contradicts with that obtained from another source

Audit evidence comprises both information that supports and corroborates management’s assertions, and any information that contradicts the assertions

When evaluating the audit evidence obtained it is important to consider all evidence available, corroborative and inconsistent, when drawing conclusions

This can demonstrate professional scepticism

Evaluate audit evidence at individual risk level

Evaluate audit evidence at overall level

Identify any evidence of intentional bias

Reassess risk assessment, if necessary

Form audit opinion

Evaluating audit results

Sufficient, appropriate evidence to conclude unlikely to be a material misstatement due to the identified risk

Stand back and assess overall evidence

Are assumptions, estimates, misstatements etc. showing an intentional bias in one direction

ASA 705

Qualification

Adverse

Disclaimer

Part B

Part A

How much evidence is enough?

• Auditor judgment• Reduce risk of giving wrong opinion to

acceptably low level• Respond to identified level of risk• Consider both:

• Quantity• Quality (relevant and reliable)

Important slide

Identify risk

•Assign a level of risk eg. Low, Medium, High with overall objective of reducing audit risk to acceptable level

Quantity •Design audit procedures to obtain necessary quantity of evidence to respond to risk level

Quality •Quality of available evidence determines extent of procedures

RelevantReliable

What if no documentation was prepared at the time of the event/activity?

• Quantity and quality of available evidence may be impacted• What evidence is available?• How reliable is the evidence?

• created a at later date• who created by

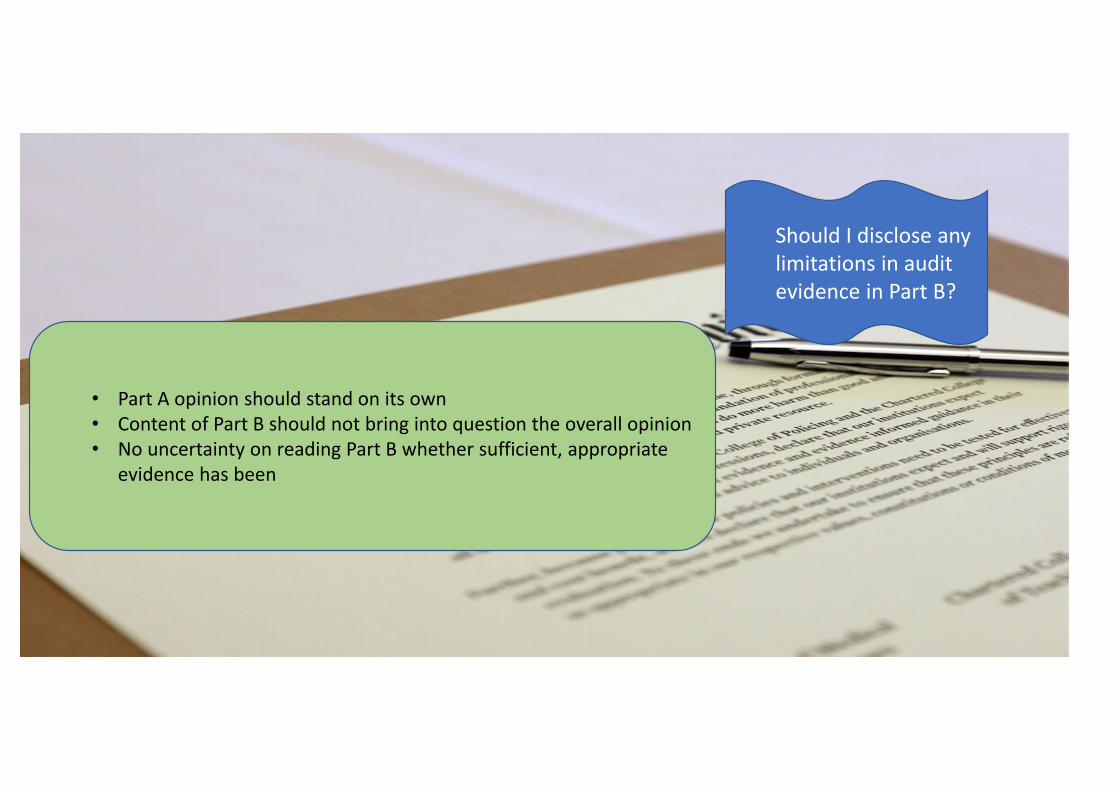

Should I disclose any limitations in audit evidence in Part B?

• Part A opinion should stand on its own• Content of Part B should not bring into question the overall opinion• No uncertainty on reading Part B whether sufficient, appropriate

evidence has been

Can I rely solely on oral representations from the client?

• Inquiry alone ordinarily does not provide sufficient, appropriate evidence• Cumulative nature of evidence gathering through corroboration

Can I rely on a stat dec?

• Risk level drives quantity of evidence• Consider the quality of evidence

• reliability • sources of evidence• circumstances

• Use for corroboration

Agenda

• Common issues with Audit Evidence

• The Technical part

• Case studies• 1 – HIR• 2 – Forecasts in safeguard mechanism

• Question time

Case Study 1 – Human Induced Regeneration (HIR)Risk of material misstatement:• 1 – Has suppression activity occurred?• 2 – Is there regrowth potential?• 3 – Has there been ongoing monitoring?

Lower Higher

Risk of material misstatement:• 1 – Has suppression activity occurred? ‐Medium• 2 – Is there regrowth potential? ‐ High• 3 – Has there been ongoing monitoring? ‐Medium

Contribution to sufficient, appropriate evidenceLower Higher

Stat dec

Relevant

ReliableQuantity

Inquiry

Relevant

ReliableQuantity

Observation

Relevant

ReliableQuantity

Inspection

Relevant

ReliableQuantity

‐When prepared?‐Who by?‐Who initiated?‐What does it say?

‐ Knowledge of person?‐ Timeframe being discussed? ‐ Potential bias?

‐Was there a site visit?‐What was the timing?‐Who by/expertise?

‐ Photos‐ location, date?‐ Stock registers?‐ Invoices:

‐ contractors‐ equipment

Risk of material misstatement:• 1 – Has suppression activity occurred?• 2 – Is there regrowth potential?• 3 – Has there been ongoing monitoring?

Contribution to sufficient, appropriate evidenceLower Higher

Stat dec

Relevant

ReliableQuantity

Inquiry

Relevant

ReliableQuantity

Observation

Relevant

ReliableQuantity

Inspection

Relevant

ReliableQuantity

‐When prepared?‐Who by?‐Who initiated?‐What does it say?

‐ Qualification/knowledge of person?‐ Timeframe being discussed? ‐ Potential bias?

‐ Report by management expert?‐ Timing‐ Scope‐ Evaluate expert

‐Was there a site visit?‐Who by/expertise?‐ Any video recording?

Risk of material misstatement:• 1 – Has suppression activity occurred?• 2 – Is there regrowth potential?• 3 – Has there been ongoing monitoring?

Contribution to sufficient, appropriate evidenceLower Higher

Stat dec

Relevant

ReliableQuantity

Inquiry

Relevant

ReliableQuantity

Observation

Relevant

ReliableQuantity

Inspection

Relevant

ReliableQuantity

‐When prepared?‐Who by?‐Who initiated?‐What does it say?

‐ Knowledge of person?‐ Timeframe discussing? ‐ Potential bias?

‐ Procedures for ongoing monitoring‐ Is evidence of performance available?

‐Was there a site visit?‐What was the timing?‐Who by/expertise?

Risk of material misstatement:• Is the model appropriate?• Are the key assumptions reasonable?• Is the data used reliable?

Contribution to sufficient, appropriate evidenceLower Higher

Inquiry

Relevant

ReliableQuantity

Inspection

Relevant

ReliableQuantity

‐ Knowledge, experience, capability of person responsible?‐ Is the model bespoke?‐ Where do the key data sources come from?‐ What is the review and approval process?

‐ Is there consistency with assumptions and data used in organization‐ Has the model changed from prior years?‐ Have the sources of data been tested?‐ Can the assumptions be benchmarked to external data?

Case Study 2 – Forecast in safeguard mechanism

Key takeaways

1. The quantity of audit evidence to be obtained should be reflective of the risk level identified

2. Quality of evidence is important, typically its reliability• Inquiry and stat decs

3. Right mindset/approach• not to just look for corroborative evidence• Not to downplay/dismiss inconsistent or limitations in evidence

4. If sufficient, appropriate evidence is not obtained or available, reflect in Part A

Agenda

• Common issues with Audit Evidence

• The Technical part

• Case studies• 1 – HIR• 2 – Forecasts in safeguard mechanism

• Question time