webinar slides: the combined benefits of cost segregation and tangible property: part 2- how lease...

TRANSCRIPT

#cbizmhmwebinar 1

CBIZ & MHM Executive Education Series™

The Combined Benefits of Cost Segregation and Tangible Property: Part 2- How Lease Language Affects Capitalization Larry Rosenblum & Eric Wallace August 9 and 16, 2016

#cbizmhmwebinar 2

About Us

• Together, CBIZ & MHM are a Top Ten accounting provider • Offices in most major markets • Tax, audit and attest* and advisory services • Over 2,900 professionals nationwide

A member of Kreston International A global network of independent accounting firms

*MHM is an independent CPA firm providing audit, review and attest services, and works closely with CBIZ, a business consulting, tax and financial services provider.

#cbizmhmwebinar 3

Before We Get Started…

• To view this webinar in full screen mode, click on view options in the upper right hand corner.

• Click the Support tab for technical assistance.

• If you have a question during the presentation, please use the Q&A feature at the bottom of your screen.

#cbizmhmwebinar 4

CPE Credit

This webinar is eligible for CPE credit. To receive credit, you will need to answer periodic participation markers throughout the webinar. External participants will receive their CPE certificate via email immediately following the webinar.

#cbizmhmwebinar 5

Disclaimer

The information in this Executive Education Series course is a brief summary and may not include all

the details relevant to your situation.

Please contact your service provider to further discuss the impact on your business.

CBIZ & MHM 6

Larry Rosenblum is a Managing Director of CBIZ MHM, LLC and a

Shareholder of Mayer Hoffman McCann P.C. in the Boca Raton, FL office.

He has more than 20 years of public accounting experience. Previously,

Larry provided tax planning and consulting services for professional

service, real estate and manufacturing companies in the New York and

Los Angeles metro areas. Currently, Larry provides consulting and tax

services for the company’s real estate clients with a concentration in

commercial property cost segregation studies. He is a frequent lecturer

in cost segregation to the banking, legal and real estate communities

561.994.5050 • [email protected] Larry Rosenblum, CPA Managing Director

#cbizmhmwebinar 7

Eric has extensive expertise in construction and real estate services,

tangible property regulations (263(a)), depreciation, NOL, and 263A

issues, and focuses on providing tax, accounting, auditing and consulting

services. He also provides specialized professional services, consulting,

writing, and training to CPA firms, CPA organizations, publishing

companies, and construction and real estate related entities for tax,

consulting, and accounting and auditing issues.

412.977.6644 • [email protected]

Eric Wallace, CPA

#cbizmhmwebinar 8

Agenda

Lease terms and their influence on capitalization decisions

02

01

03

Latest depreciation changes

Questions

#cbizmhmwebinar 9

THE COMBINED BENEFITS OF COST SEGREGATION AND TANGIBLE PROPERTY: PART 2- HOW LEASE

LANGUAGE AFFECTS CAPITALIZATION

#cbizmhmwebinar 10

Introduction

• What elements or provisions of the landlord tenant agreements should be changed or worded to enable current deductions as opposed to required capitalization

• Why building owners want to avoid Section 110 treatment and/or intangible lease incentives

• What TPR (tangible property regulations) rules cover these issues

#cbizmhmwebinar 11

Introduction

• Lease language tax types/consequences that need to be understood: • Leases with Section 110 language • Leases with tenant incentives • Leases with funds for tenants for inventory and/or

tangible personal property • Leasehold improvement ownership consequences for

these various lease types • Leasehold improvements financed by the landlord

#cbizmhmwebinar 12

Introduction

• Changes to landlord-tenant agreements necessary to enable current deductions

• Differentiation of tax treatment for original leasehold improvements compared to subsequent leaseholds in lease renewals/extensions

• Tax treatment if the leasehold improvement work is done and/or paid for by the tenant or the landlord

#cbizmhmwebinar 13

Introduction

• Lease types that make available prior year tax capitalization reclassifications to current year tax deductions

• How a taxpayer obtain these deductions for tax year 2015

• Lease language for these various types of lease agreements to take advantage of the desired tax positions

• The different tax treatment of these lease types for landlord verses tenant perspectives

CBIZ & MHM 14

SEE TWO OTHER HANDOUTS

These handouts provide more details and handy tools on the concepts of lease terms

and the tangible property regulations

#cbizmhmwebinar 15

CBIZ & MHM 16

Landlord Lease Terms and their Influence on the Determination of Capitalization of Leasehold Improvements The thoughts, rules, and foundations in the consideration of the tax effects on how landlord/tenant agreements should be written were dramatically changed when the final tangible property regulations (TPRs) became law in 2014. Not only will the TPR rules and criteria apply to all new lease terms, it must also be applied “back in time” to all prior lease determinations of capitalization or deduction of prior leasehold improvements (LHIs). One cannot generally rewrite prior lease terms; therefore, this article focuses on the cause and effect of new lease terms, or those leases that are going to be renewed in the future. Certain lease terms can result in a current tax deduction of expenditures for LHIs. On the other hand, if those lease terms do not meet the new TPR rules, capitalization will result.

#cbizmhmwebinar 17

THE TPRS AND LANDLORD/TENANT ISSUES

#cbizmhmwebinar 18

Landlords and Tenant Improvements What the TPRs Mean

• The TPRs present a opportunity/requirement to write off the net remaining tax basis of • Duplicate previously capitalized TIs as a current year 481(a) adjustment,

in a proper IRS Form 3115 filing, or • TIs that did not arise the level of being required to be capitalized under

the RABI rules

• If the landlord taxpayer misses this opportunity or misinterprets the TPRs in the application of the TPRs, the taxpayer faces the real risk that large future depreciation deductions for these TIs will be permanently disallowed by the IRS

#cbizmhmwebinar 19

The TPR Implied ‘Rule of One’ and TIs

• Taxpayers need to have one of every asset on its books, but can choose to have more than one, but cannot choose to have zero or none

• Example • Taxpayer (TP) is a landlord and replaces all of the HVAC units in the building in

2015 • TP must capitalize the new HVAC units as it is a restoration under the RABI

standards • TP does not need to remove the remaining basis of the prior HVAC units from its

assets but it can • TP can do the PAD for the removed HVAC but it is not required to • TP cannot expense the new HVAC as a repair and also do a PAD

• i.e., write off the net remaining depreciable basis of the prior HVAC

#cbizmhmwebinar 20

‘Rule of One’

• You do not have to have basis in an asset, or part of an asset, in order to have “one”

• Example • Under a lease, the tenant must replace the roof if it needs replaced • The tenant does replace the roof later • The landlord already has a roof on its books • Now it has two when the tenant replaces the roof

• Same issue applies where the landlord obtains “free” tenant improvements for its leased space

CBIZ & MHM 21

LEASE LANGUAGE AND ITS TPR TAX CONSEQUENCES

#cbizmhmwebinar 22

TPR Lease Language and Terms

• Lease language tax types/consequences: • Leases with Section 110 language • Leases with tenant incentives • Leases with funds for tenants for inventory and/or

tangible personal property • Leasehold improvements financed by the landlord • Rent forgiveness for tenant making improvements • Landlord or tenant paying for and supervising the

construction of the LHIs • Original LHIs verses subsequent LHIs for same tenant

lease

#cbizmhmwebinar 23

Section 110 Leases - What It Means for Landlords and Capitalization of TIs

• 1.263(a)-3(f) Rules for Improvements to Leased Property -(3) Lessor improvements

• (i) Requirement to capitalize

A taxpayer lessor must capitalize the related amounts, that it pays directly, or indirectly through a construction allowance to the lessee, to improve, a leased property when the lessor is the owner of the improvement or to the extent that Section 110 applies to the construction allowance

• If the amounts are not an “improvement” then the lessor does not have to capitalize the expenditure

• If the lease has 110 language in it, the lease expenditures must be capitalize, even if not an “improvement”, and those become a separate U of P

#cbizmhmwebinar 24

Section 110 Typical Lease Language

• “In consideration for the performance by Tenant of certain work in the Premises, including Tenant’s Work, Landlord shall pay to Tenant the Lease Incentive Payment”

• “The Lease Incentive Payment is primarily for the purpose of constructing or improving qualified long term real property for use in Tenant’s trade or business at the Premises, in accordance with Section 110(a) of the Internal Revenue Code”

#cbizmhmwebinar 25

Section 110 Summary

• In order for a section 110 lease to exist:

• The landlord has to pay monies to the tenant. If the landlord pays the contractors then a section 110 lease cannot exist

• The lease documents must refer to section 110 or have the explicit phrase in the lease

• When a section 110 lease exists the leasehold improvement expenditures by the landlord must be capitalized as a separate unit of property

#cbizmhmwebinar 26

Leases with Incentives

• A lease that is categorized or determined to be a lease with lease incentives is not treated as a tangible assets by the landlord

• Lease incentives are payments made by a lessor to or on behalf of a lessee to entice the lessee to sign. Lease incentives may include up-front cash payments to the lessee, payment of costs on behalf of the lessee (such as moving expenses), termination fees to prior landlord

• Such a lease has the following consequences: • It is an intangible of the landlord • It is amortized over the lease term by the landlord • It is income, when paid, to the tenant

#cbizmhmwebinar 27

Leases with funds for tenants for inventory and/or tangible personal property

• If the landlord pays funds to tenants for the tenant to use for assets other than leasehold improvements, the classification of the transaction is the following: • Landlord: lease incentive

• Tenant: Income

• If the landlord pays for leasehold improvements that are considered as tangible personal property (such as special wiring for a machine), the asset is an asset on the landlord’s books, just that the class life is different

#cbizmhmwebinar 28

Leasehold improvements financed by the landlord

• If the leasehold improvement (LHI) costs are an additional rent to the landlord, then the tax treatment of those LHIs will depend on who owns them at the lease start

• If the tenant owns the LHIs until the lease is over, then the tax treatment of the LHIs is the following: • Landlord: has a note receivable and not LHIs

• Tenant: has LHIs on its books

#cbizmhmwebinar 29

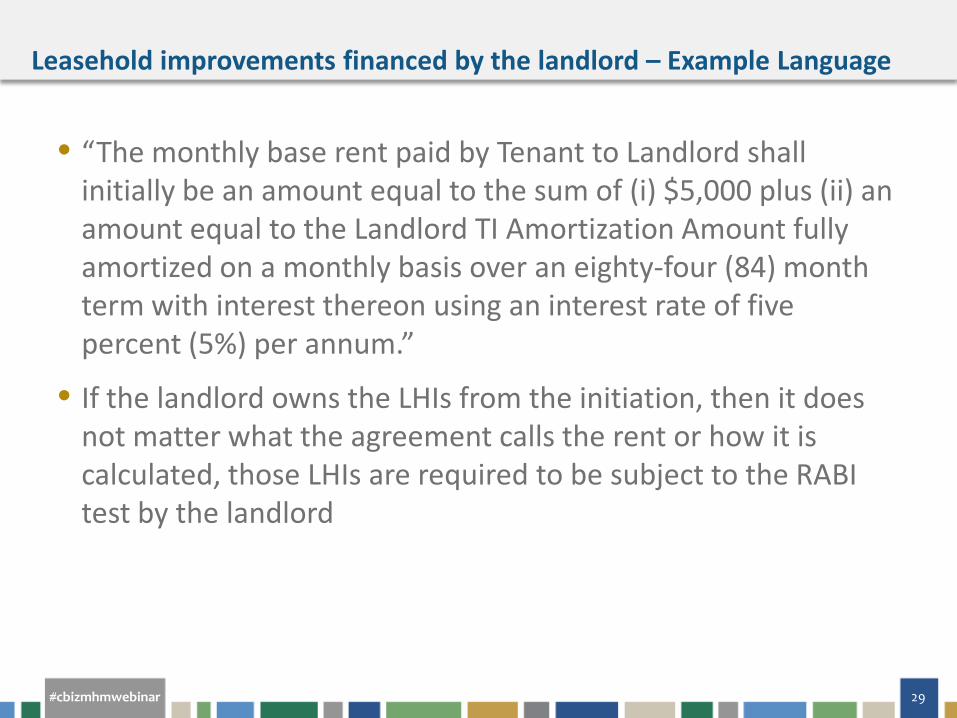

Leasehold improvements financed by the landlord – Example Language

• “The monthly base rent paid by Tenant to Landlord shall initially be an amount equal to the sum of (i) $5,000 plus (ii) an amount equal to the Landlord TI Amortization Amount fully amortized on a monthly basis over an eighty-four (84) month term with interest thereon using an interest rate of five percent (5%) per annum.”

• If the landlord owns the LHIs from the initiation, then it does not matter what the agreement calls the rent or how it is calculated, those LHIs are required to be subject to the RABI test by the landlord

#cbizmhmwebinar 30

Rent forgiveness for tenant making improvements

• If the lease agreement calls for the tenant to make the LHIs and the rent is reduced as a result of such: • The landlord has rental income and the opposite of that tax entry is to

subject those LHIs to the RABI testing (to determine if those expenditures should be capitalized as LHIs or as R & M)

• The tenant has rent expense

#cbizmhmwebinar 31

Landlord or tenant paying for and supervising the construction of the LHIs

• In other words, does it matter who initially pays for the LHIs or supervises the construction?

• No.

• If the landlord reimburses the tenant for the LHI costs it is the same as if the landlord did the work – the landlord would then own the LHIs and subject those expenditures to the RABI testing against the landlord U of P

#cbizmhmwebinar 32

Original LHIs verses subsequent LHIs for same tenant lease

• Landlord perspective: • Whether the LHIs are the original or subsequent

replacements, updates, or changes – the landlord subjects those expenditures to the RABI testing in comparison the appropriate U of P

• Tenant perspective: • Assuming the that LHIs are owned by the tenant - the

initial/original LHIs compared to subsequent lease renewal LHIs have very different tax treatment. The initial/original are always capitalized by the tenant. The subsequent LHIs are subject to the RABI test compared to the tenant U of P

#cbizmhmwebinar 33

Recommendations on Landlord Tenant Agreements

• What elements or provisions of the landlord tenant agreements should be changed or worded to enable current deductions as opposed to required capitalization — from the landlord perspective • Do not refer to Section 110 in the lease agreement

• It is acceptable to refer to the fact that the landlord “owns” those “improvements” or constructed assets

• If the LHIs are going to be required to be capitalized by the landlord, consider lease incentives as an alternative

#cbizmhmwebinar 34

Recommendations on Landlord Tenant Agreements

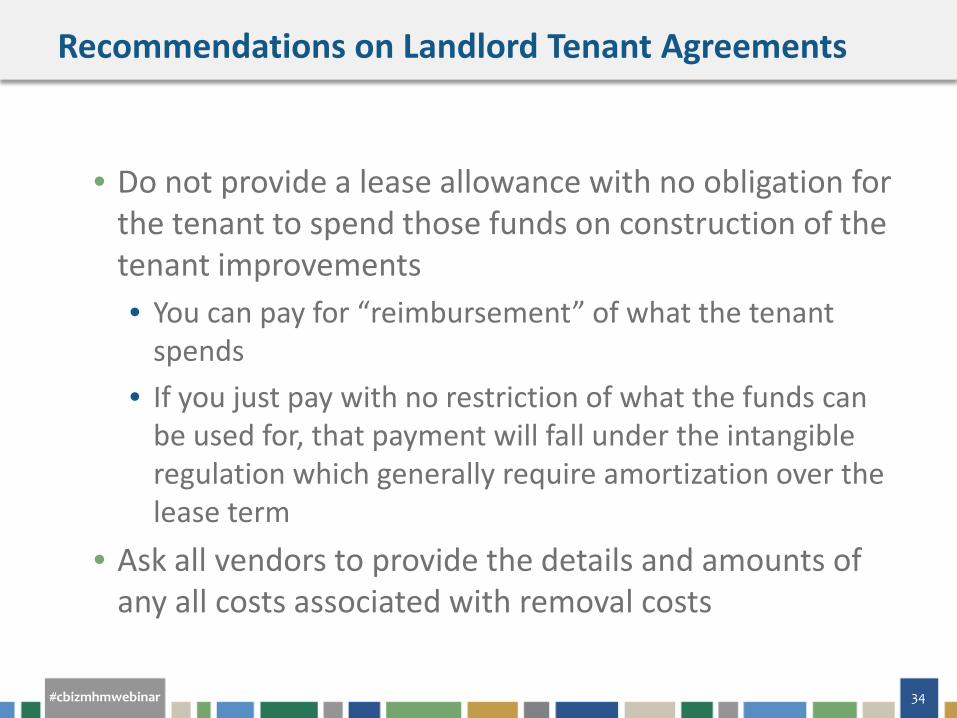

• Do not provide a lease allowance with no obligation for the tenant to spend those funds on construction of the tenant improvements • You can pay for “reimbursement” of what the tenant

spends • If you just pay with no restriction of what the funds can

be used for, that payment will fall under the intangible regulation which generally require amortization over the lease term

• Ask all vendors to provide the details and amounts of any all costs associated with removal costs

#cbizmhmwebinar 35

EXAMPLES

#cbizmhmwebinar 36

TI Expenditures for Big Mall

Example

• Big Mall has owned and operated a large mall in Podunk, PA since the 1980s • The mall consists of over 700,000 square feet various

and numerous tenants • In 2015 the tenant occupying 40,000 of one of the anchor

stores moves out and new tenant ABC moves in • BM spends $2.5M retrofitting that space for a new

tenant. • BM has properly filed its method changes under the

TPRs for 2014

#cbizmhmwebinar 37

Conclusion

Example

• BM will expense the $2.5M as a R&M

• Why? • The expenditure is not a restoration

• The space redone was only 6% of the total square footage of the unit of property (i.e., the whole mall)

• The effort was not an adaption

• The effort could only possibly fall in as a betterment but BM argues that it not a material betterment as it was leased space before, is still leased space after the effort so no material “betterment” occurred even if it was classified as a betterment

#cbizmhmwebinar 38

From the Tenant Perspective

Example

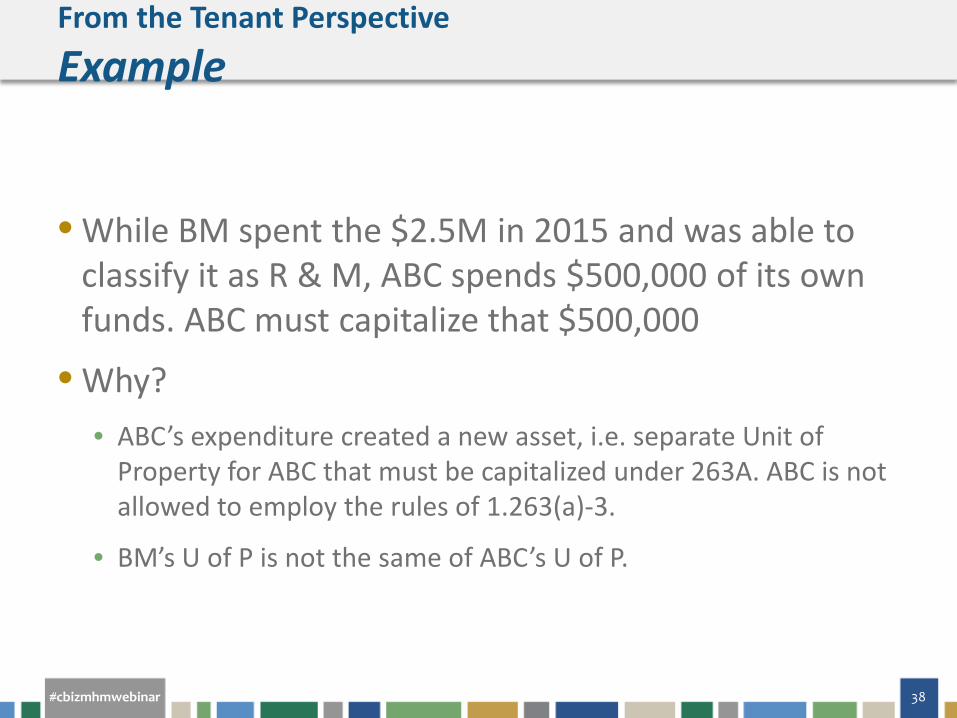

• While BM spent the $2.5M in 2015 and was able to classify it as R & M, ABC spends $500,000 of its own funds. ABC must capitalize that $500,000

• Why? • ABC’s expenditure created a new asset, i.e. separate Unit of

Property for ABC that must be capitalized under 263A. ABC is not allowed to employ the rules of 1.263(a)-3.

• BM’s U of P is not the same of ABC’s U of P.

#cbizmhmwebinar 39

From the Tenant Perspective – 5 Years

Later Example

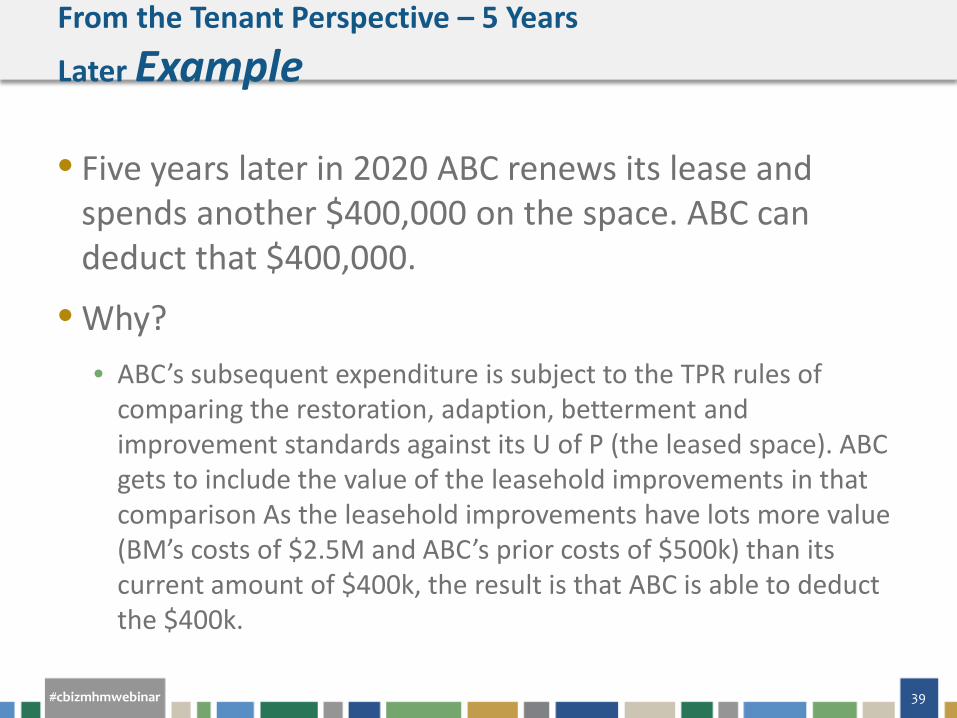

• Five years later in 2020 ABC renews its lease and spends another $400,000 on the space. ABC can deduct that $400,000.

• Why? • ABC’s subsequent expenditure is subject to the TPR rules of

comparing the restoration, adaption, betterment and improvement standards against its U of P (the leased space). ABC gets to include the value of the leasehold improvements in that comparison As the leasehold improvements have lots more value (BM’s costs of $2.5M and ABC’s prior costs of $500k) than its current amount of $400k, the result is that ABC is able to deduct the $400k.

#cbizmhmwebinar 40

LATEST DEPRECIATION CHANGES

Update on these important issues

#cbizmhmwebinar 41

Qualified Leasehold Improvements (QLI)

• 15-year recovery period straight-line

• Improvement to interior portion of non-residential building made pursuant to a lease

• Must be placed in service more than three years after building first placed in service

• Does not cover enlargement of building, elevator or escalator or common area

• Does not apply to related party leases

• Eligible for bonus depreciation

Qualified Restaurant Property (QRP)

• 15-year recovery period straight-line

• Applies to any Section 1250 property if MORE than 50% of the building’s square footage is devoted to preparation of and seating for on-premises meals

• Not eligible for bonus depreciation unless meets definition of Qualified Leasehold Improvement Property (Rev Proc 2011-26)

Qualified Retail Improvement Property (QRI)

• 15-year recovery period straight-line

• Any improvement to interior portion of non-residential building

• Portion of building must be open to general public and is used in sale of tangible property to public

• Must be placed in service more than three years after building first placed in service

• Does not cover enlargement of building, elevator or escalator or internal structural framework

• Eligible for bonus depreciation in 2016.

Types of Leasehold Property

41

#cbizmhmwebinar 42

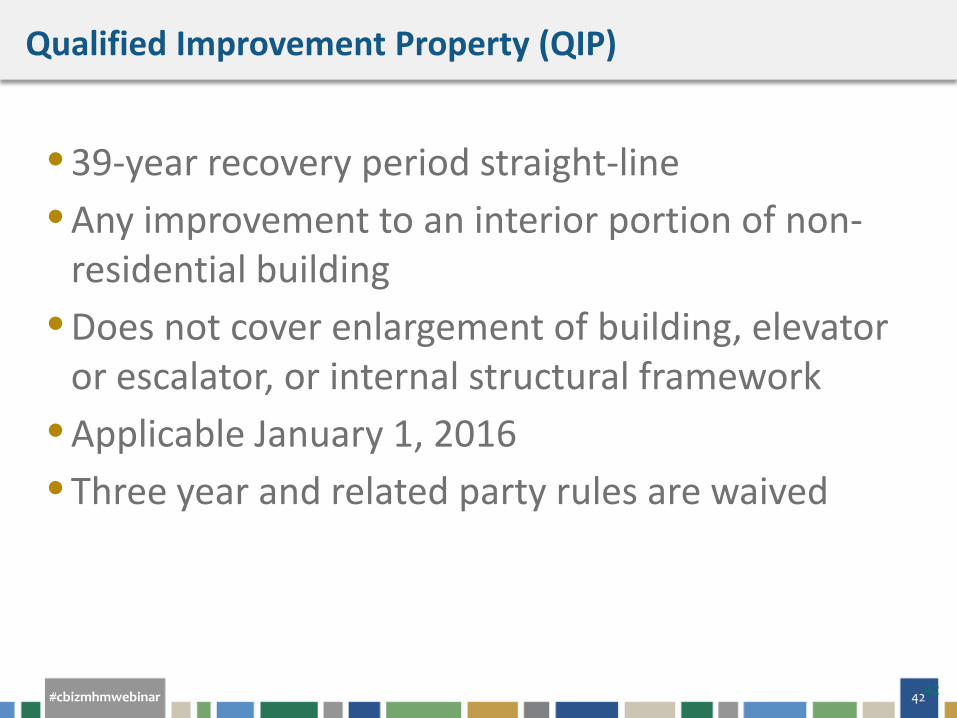

• 39-year recovery period straight-line • Any improvement to an interior portion of non-

residential building • Does not cover enlargement of building, elevator

or escalator, or internal structural framework • Applicable January 1, 2016 • Three year and related party rules are waived

Qualified Improvement Property (QIP)

42

#cbizmhmwebinar 43

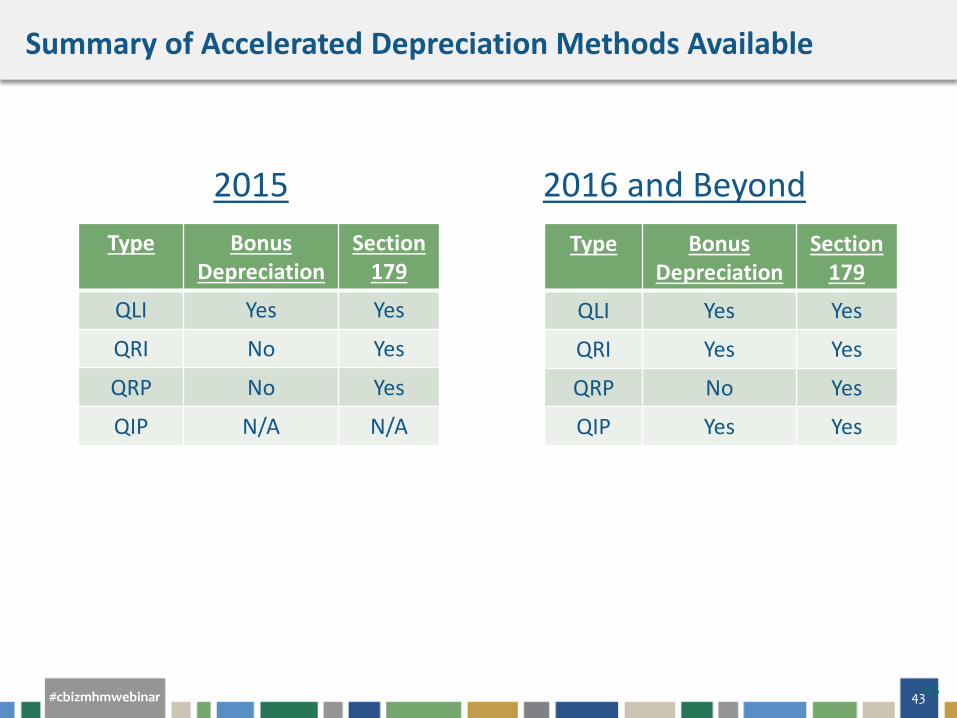

Summary of Accelerated Depreciation Methods Available

43

2015 2016 and Beyond Type Bonus

Depreciation Section

179

QLI Yes Yes

QRI No Yes

QRP No Yes

QIP N/A N/A

Type Bonus Depreciation

Section 179

QLI Yes Yes

QRI Yes Yes

QRP No Yes

QIP Yes Yes

#cbizmhmwebinar 44

? QUESTIONS

#cbizmhmwebinar 45

If You Enjoyed This Webcast…

Upcoming Courses: • 8/10 & 9/15: Win the Not-for-Profit Talent War - Recruitment, Retention, Rewards

and Regulation

• 8/11: Private Company Business Combination and Valuation Overview

• 8/11 & 8/17: Implications of the New Partnership Audit Rules

• 8/25: Top Issues in the New Revenue Recognition Guidance Manufacturers Should Consider

Recent Publications: • Transfer Pricing Quarterly Update: Second Quarter 2016

• How to Lower Your Tax Burden in International Real Estate Transactions

• Dramatic Proposed Changes to Impact Estate and Gift Tax Planning

#cbizmhmwebinar 46

Connect with Us

linkedin.com/company/ mayer-hoffman-mccann-p.c.

@mhm_pc

youtube.com/ mayerhoffmanmccann

slideshare.net/mhmpc

linkedin.com/company/ cbiz-mhm-llc

@cbizmhm

youtube.com/ BizTipsVideos

slideshare.net/CBIZInc

MHM CBIZ