week 3 accruals and prepayments. aims to introduce the accruals concept and its effects on the...

TRANSCRIPT

Accounts PreparationWeek 3

Accruals and Prepayments

Aims To introduce the accruals concept and its effects on the financial statements. Objectives At the end of these sessions, you should be able to: 1. Describe the purpose of the accruals concept and how it affects the financial statements. 2. Make the necessary adjustments to account for any year end accruals and prepayments in both the main ledger and the final accounts. 3. Complete the ETB, making the necessary adjustments for any accruals and prepayments and produce the final accounts.

Accruals & Prepayments

Accounts PreparationWeek 3

Accruals and Prepayments

Accruals

DefinitionAn expense that has been incurred during the period but has not been paid for by the period end and has therefore not been entered in the ledger accounts.

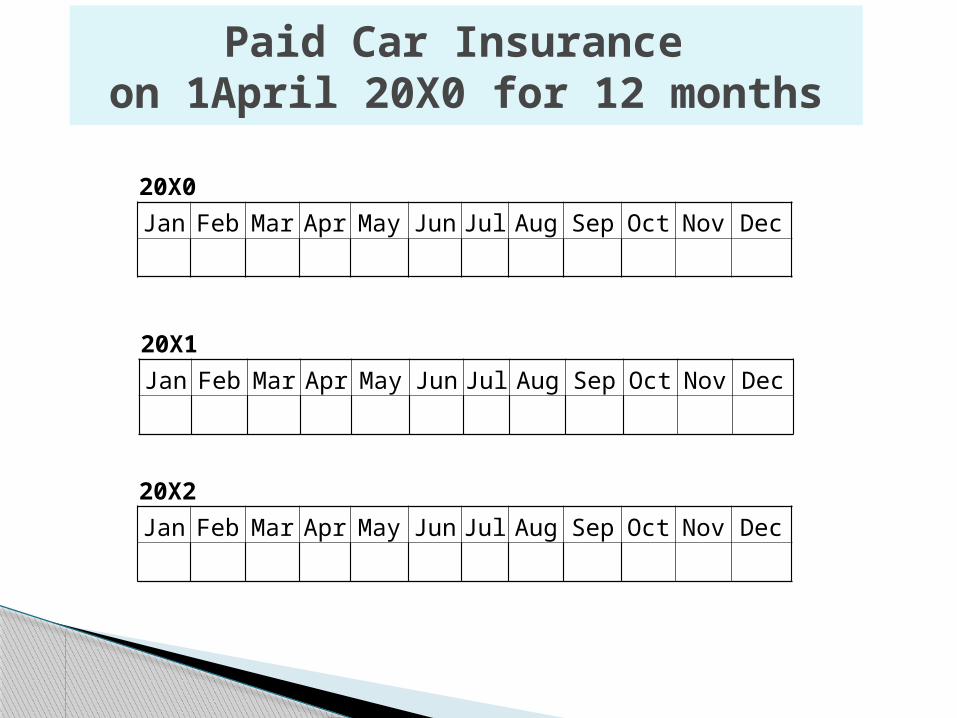

Paid Car Insurance on 1April 20X0 for 12 months

20X0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

20X1

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

20X2

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

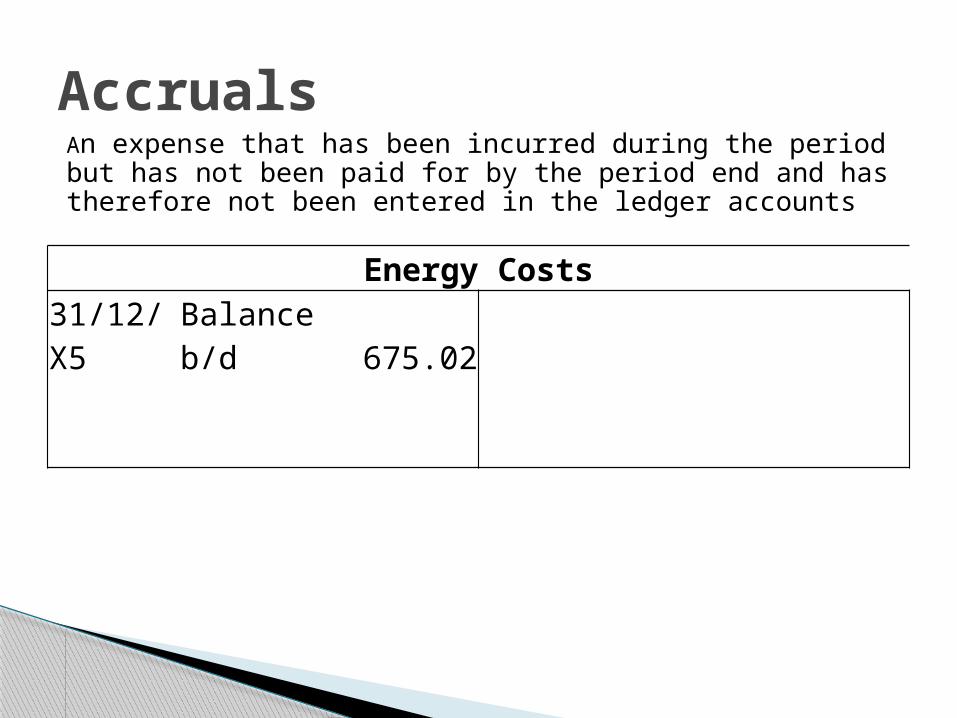

AccrualsAn expense that has been incurred during the period but has not been paid for by the period end and has therefore not been entered in the ledger accounts

Energy Costs

31/12/X5 Balance b/d 675.02

AccrualsAn expense that has been incurred during the period but has not been paid for by the period end and has therefore not been entered in the ledger accounts

Energy Costs

31/12/X5 Balance b/d 675.02 31/12/X5 57.85

AccrualsAn expense that has been incurred during the period but has not been paid for by the period end and has therefore not been entered in the ledger accounts

Energy Costs

31/12/X5 Balance b/d 675.02 31/12/X5 57.85

Accruals

31/12/X5 Energy Costs 57.85

To P & L Account as an EXPENSE

To Balance sheet as a LIABILITY

AccrualsSummary of posting:

Debit the expense accountto increase the expense to reflect the fact that an expense has been incurred; and

Credit an accruals account to reflect the fact that there is a liability for the expense.

Your Journal would be: Dr Cr

Dr Energy Costs 57.85Cr Accruals 57.85

‘Being energy costs not invoiced for at year end’

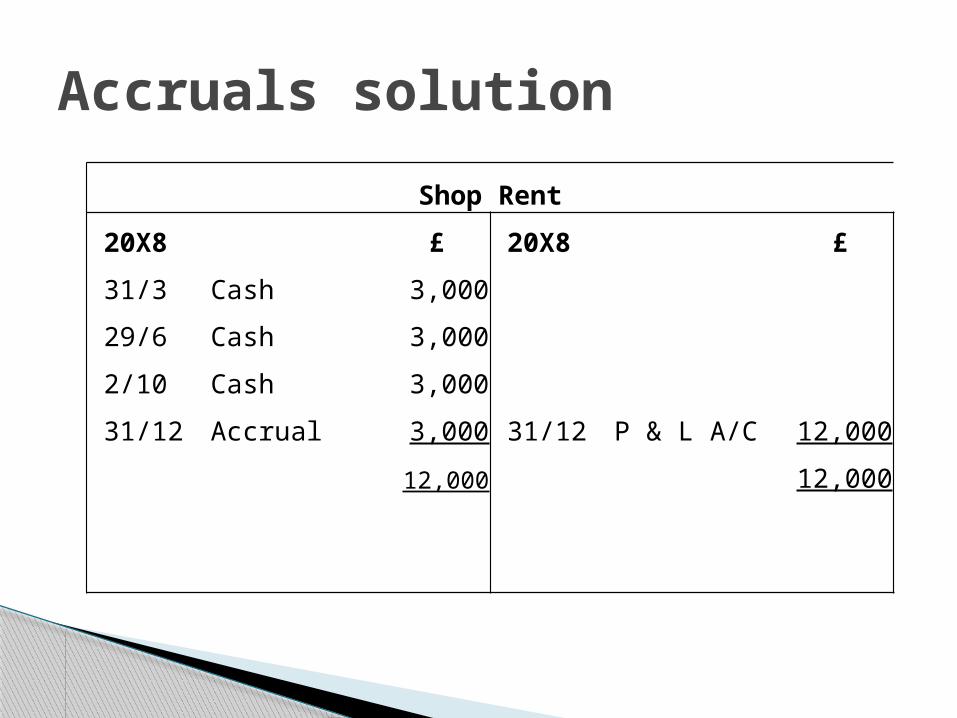

Accruals exampleJohn Smith’s business has a year end of 31 December 20X8. During the year John made payments for the rent of a shop as follows £ 31 March (for quarter to 31 March 20X8) 3,000 29 June (for quarter to 30 June 20X8) 3,000 2 October (for quarter to 30 September 20X8) 3,000

The final payment due on 31 December 20X8 for the quarter to that date was not paid until 2 January 20X9. Required Prepare ledger accounts for shop rent for the year ended 31 December 20X8.

Accruals solution

Shop Rent

20X8 £ 20X8 £

31/3 Cash 3,000

29/6 Cash 3,000

2/10 Cash 3,000

Accruals solution

Shop Rent

20X8 £ 20X8 £

31/3 Cash 3,000

29/6 Cash 3,000

2/10 Cash 3,000

31/12 Accrual 3,000

Accruals solution

Shop Rent

20X8 £ 20X8 £

31/3 Cash 3,000

29/6 Cash 3,000

2/10 Cash 3,000

31/12 Accrual 3,000

12,000 12,000

Accruals solution

Shop Rent

20X8 £ 20X8 £

31/3 Cash 3,000

29/6 Cash 3,000

2/10 Cash 3,000

31/12 Accrual 3,000 31/12 P & L A/C 12,000

12,000 12,000

Accruals solution

Shop Rent

20X8 £ 20X8 £

31/3 Cash 3,000

29/6 Cash 3,000

2/10 Cash 3,000

31/12 Accrual 3,000 31/12 P & L A/C 12,000

12,000 12,000

1/1 Accrual b/d 3,000

Practice Question 1 - Samina

Telephone

20X8 £ 20X8 £

Practice Question 1 - Samina

Telephone

20X8 £ 20X8 £

31 Mar Cash 845

Practice Question 1 - Samina

Telephone

20X8 £ 20X8 £

31 Mar Cash 845

31 Mar Accrual 170

Practice Question 1 - Samina

Telephone

20X8 £ 20X8 £

31 Mar Cash 845

31 Mar Accrual 170 31 Mar P & L A/C 1015

1015 1015

Practice Question 1 - Samina

Telephone

20X8 £ 20X8 £

31 Mar Cash 845

31 Mar Accrual 170 31 Mar P & L A/C 1015

1015 1015

1Apr Accrual b/d 170

Complete practice questions 2-7

Question 8 – Worked Example

AccrualsAn expense that has been incurred during the period but has not been paid for by the period end and has therefore not been entered in the ledger accounts

Electricity Bills are received quarterly

Cost to end October £5000

(Year end 31/12/2014)

2014

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2015Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

AccrualsAn expense that has been incurred during the period but has not been paid for by the period end and has therefore not been entered in the ledger accounts

2014

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

500 500 500 500 500 500 500 500 500 500

2015Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

AccrualsAn expense that has been incurred during the period but has not been paid for by the period end and has therefore not been entered in the ledger accounts

Bill for £1800 covering quarter ending January 2015 is received in February ‘15

2014

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

500 500 500 500 500 500 500 500 500 500

2015Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

AccrualsAn expense that has been incurred during the period but has not been paid for by the period end and has therefore not been entered in the ledger accounts

Bill for £1800 covering quarter ending January 2015 is received in February ‘15

2014

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

500 500 500 500 500 500 500 500 500 500

2015Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

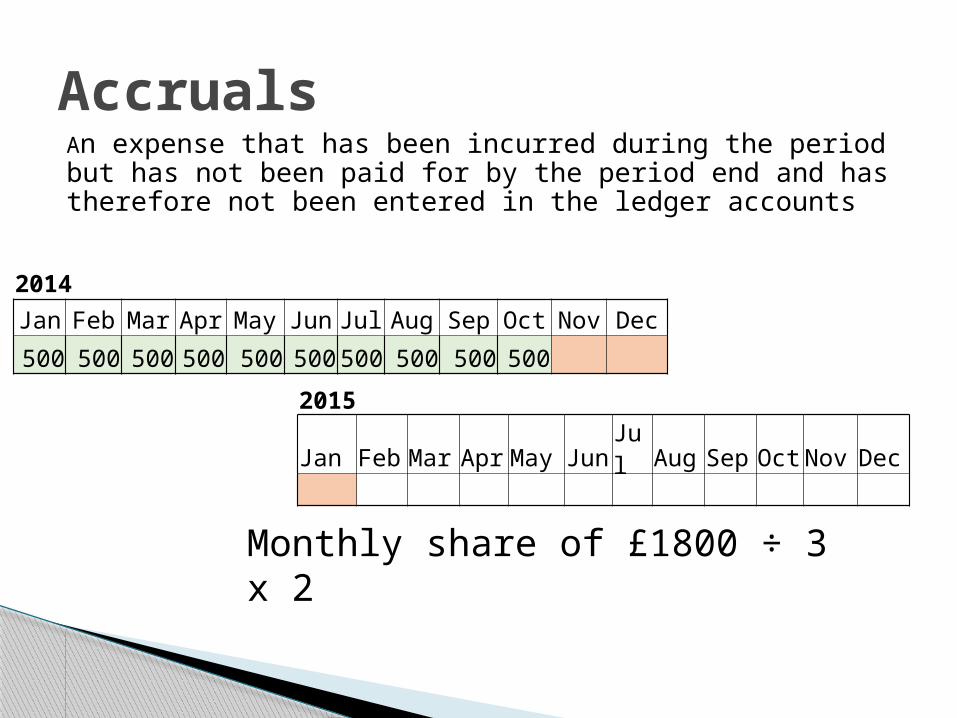

AccrualsAn expense that has been incurred during the period but has not been paid for by the period end and has therefore not been entered in the ledger accounts

Monthly share of £1800 ÷ 3 x 2

2014

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

500 500 500 500 500 500 500 500 500 500

2015Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

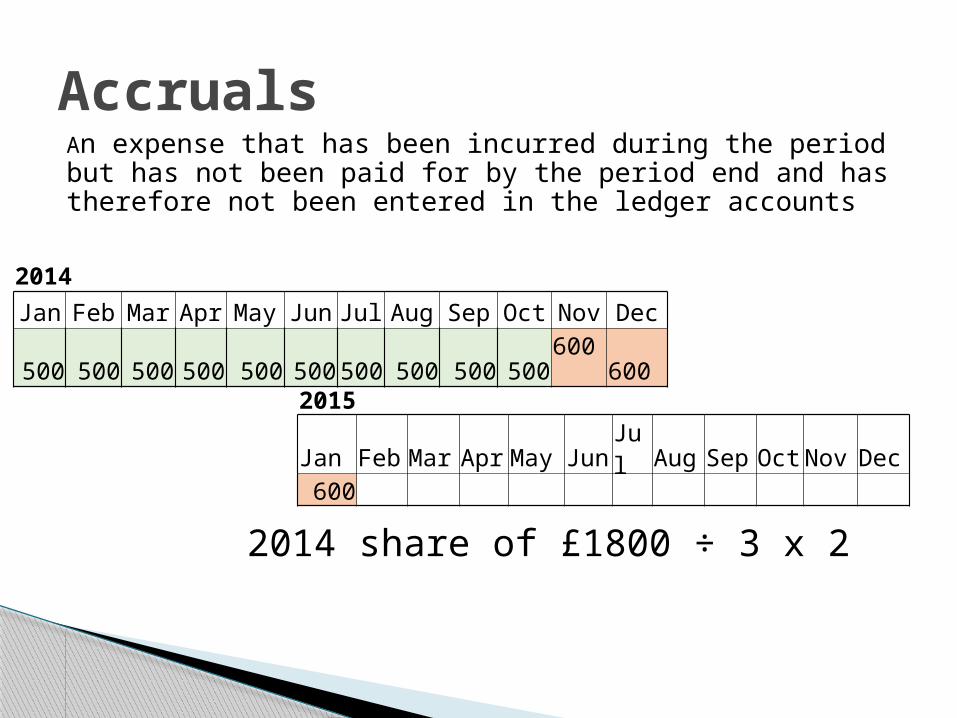

AccrualsAn expense that has been incurred during the period but has not been paid for by the period end and has therefore not been entered in the ledger accounts

2014 share of £1800 ÷ 3 x 2

2014

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

500 500 500 500 500 500 500 500 500 500600 600

2015Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

600

AccrualsAn expense that has been incurred during the period but has not been paid for by the period end and has therefore not been entered in the ledger accounts

2014

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

500 500 500 500 500 500 500 500 500 500 600 600

2015Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

600

£1200 electricity cost

is accrued

Accruals2014

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

500 500 500 500 500 500 500 500 500 500 600 600

2015Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

600

£1200 electricity cost

is accrued

Energy Costs

31/12 Bank 5000

Accruals

Accruals2014

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

500 500 500 500 500 500 500 500 500 500 600 600

2015Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

600

£1200 electricity cost

is accrued

Electricity Costs

31/12 Bank 5,000 31/12 Accrual 1,200

Accruals

Accruals2014

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

500 500 500 500 500 500 500 500 500 500 600 600

2015Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

600

£1200 electricity cost

is accrued

Electricity Costs

31/12 Bank 5,000 31/12 Accrual 1,200

Accruals

31/12 Electricity 1,200

Accruals2014

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

500 500 500 500 500 500 500 500 500 500 600 600

2015Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

600

£1200 electricity cost

is accrued

Electricity Costs

31/12 Bank 5,000 31/12 Accrual 1,200 31/12 To SOCI 6200 6,200 6,200

Accruals

31/12 Electricity 1,200

Accruals2015Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

600

£1200 electricity cost

accrued is now the b/d

balance

Electricity Costs

1/1 Bal b/d 1,200

Accruals

1/12 Electricity 1,200 31/12 Electricity 1,200

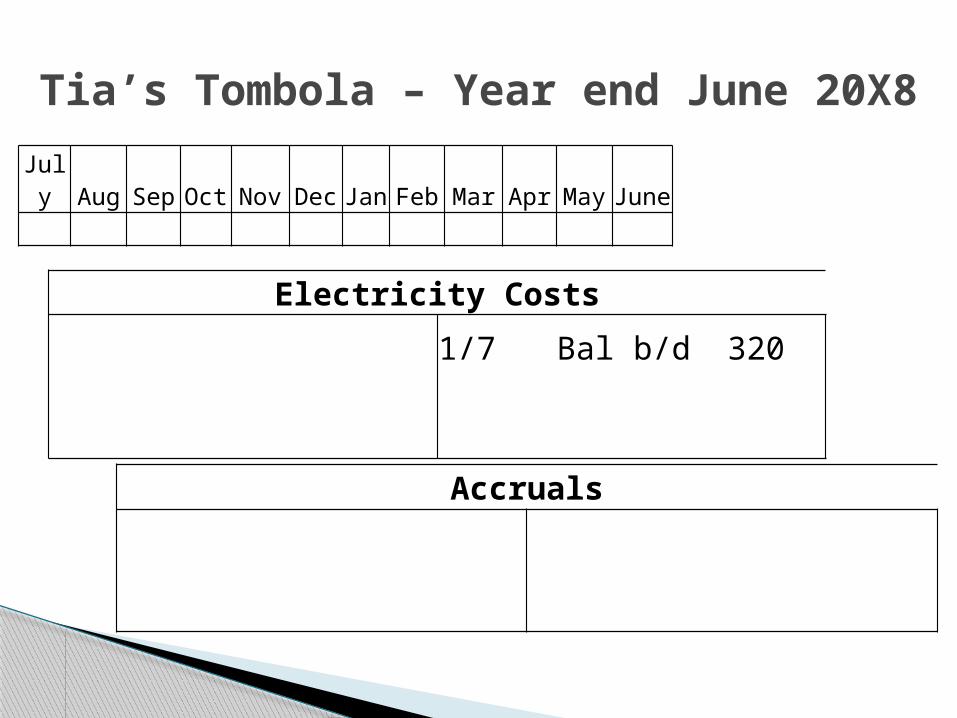

Tia’s Tombola – Year end June 20X8

Insurance Costs

On 1st March 20X7 paid

£1500 for 12 months

Accruals

20X8

July Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

20X9

July Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

Tia’s Tombola – Year end June 20X8

July Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

Electricity Costs

Accruals

Tia’s Tombola – Year end June 20X8

July Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

Electricity Costs

1/7 Bal b/d 320

Accruals

Tia’s Tombola – Year end June 20X8

July Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

Electricity Costs

30/6 Bank 13401/7 Bal b/d 320

Accruals

Tia’s Tombola – Year end June 20X8

July Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

Electricity Costs

30/6 Bank 13401/7 Bal b/d 32030/6 Acc (May) 180 30/6 Accr (June) 150

Accruals

Tia’s Tombola – Year end June 20X8

July Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

Electricity Costs

30/6 Bank 13401/7 Bal b/d 32030/6 Acc (May) 180 30/6 Accr (June) 150

Accruals

30/6 Electric Accrued 330

Tia’s Tombola – Year end June 20X8

Insurance Costs

Prepayment

20X8

July Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

20X9

July Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

Tia’s Tombola – Year end June 20X8

Insurance Costs

Prepayment

20X8

July Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

125 125 125 125 125 125 125 125

20X9

July Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

Tia’s Tombola – Year end June 20X8

Insurance Costs

1 July Bal b/f 1000

Prepayment

20X8

July Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

125 125 125 125 125 125 125 125

20X9

July Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

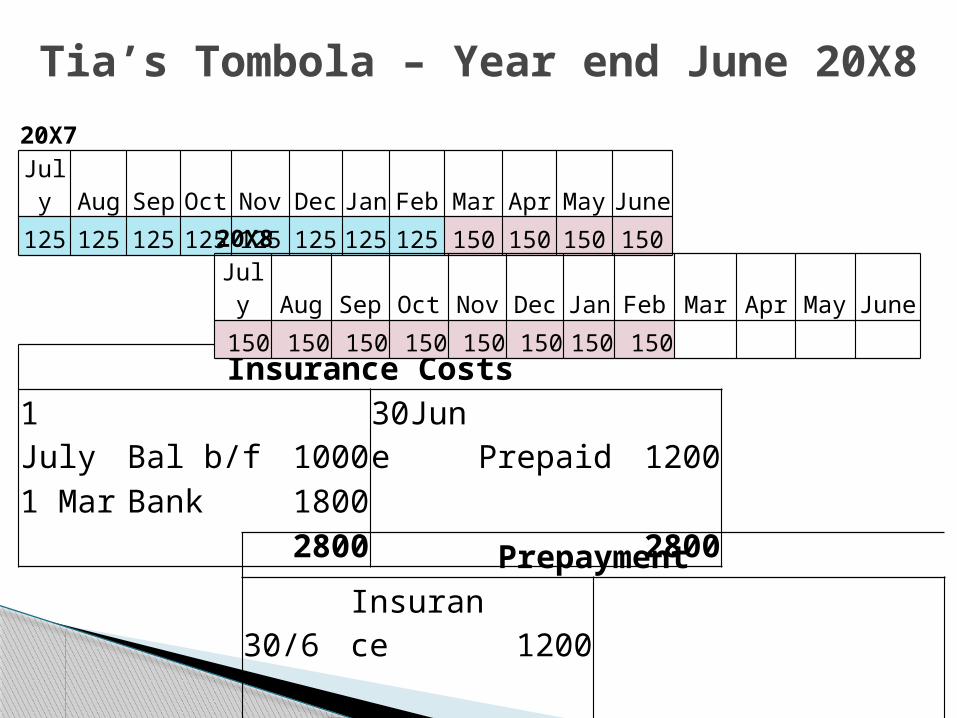

Tia’s Tombola – Year end June 20X8

Insurance Costs

1 July Bal b/f 10001 Mar Bank 1800

Prepayment

20X8

July Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

125 125 125 125 125 125 125 125 150 150 150 150

20X9

July Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

150 150 150 150 150 150 150 150

Tia’s Tombola – Year end June 20X8

Insurance Costs

1 July Bal b/f 10001 Mar Bank 1800

Prepayment

20X8

July Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

125 125 125 125 125 125 125 125 150 150 150 150

20X9

July Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

150 150 150 150 150 150 150 150

Tia’s Tombola – Year end June 20X8

Insurance Costs

1 July Bal b/f 10001 Mar Bank 1800

Prepayment

20X8

July Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

125 125 125 125 125 125 125 125 150 150 150 150

20X9

July Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

150 150 150 150 150 150 150 150

Tia’s Tombola – Year end June 20X8

Insurance Costs

1 July Bal b/f 100030/6 Prepaid 12001 Mar Bank 1800

Prepayment

30/6 Insurance 1200

20X7

July Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

125 125 125 125 125 125 125 125 150 150 150 15020X8

July Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

150 150 150 150 150 150 150 150

Tia’s Tombola – Year end June 20X8

Insurance Costs

1 July Bal b/f 100030June Prepaid 12001 Mar Bank 1800 2800 2800

Prepayment

30/6 Insurance 1200

20X7

July Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

125 125 125 125 125 125 125 125 150 150 150 15020X8

July Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

150 150 150 150 150 150 150 150

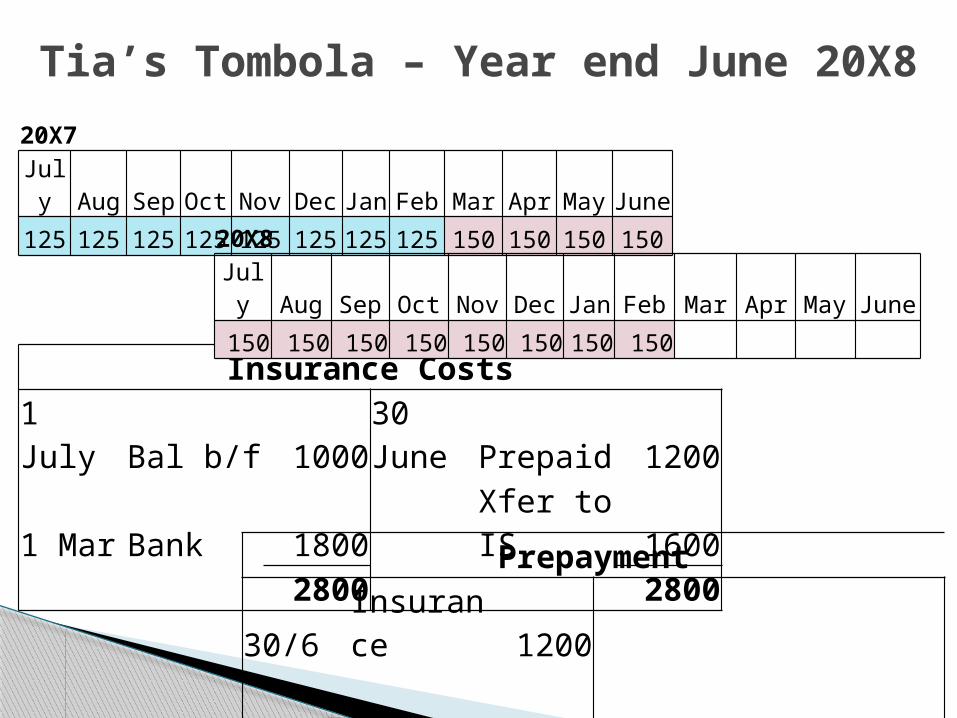

Tia’s Tombola – Year end June 20X8

Insurance Costs

1 July Bal b/f 100030 June Prepaid 12001 Mar Bank 1800 Xfer to IS 1600 2800 2800

Prepayment

30/6 Insurance 1200

20X7

July Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

125 125 125 125 125 125 125 125 150 150 150 15020X8

July Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

150 150 150 150 150 150 150 150

Question 9 Rates

Rent

Rental Income

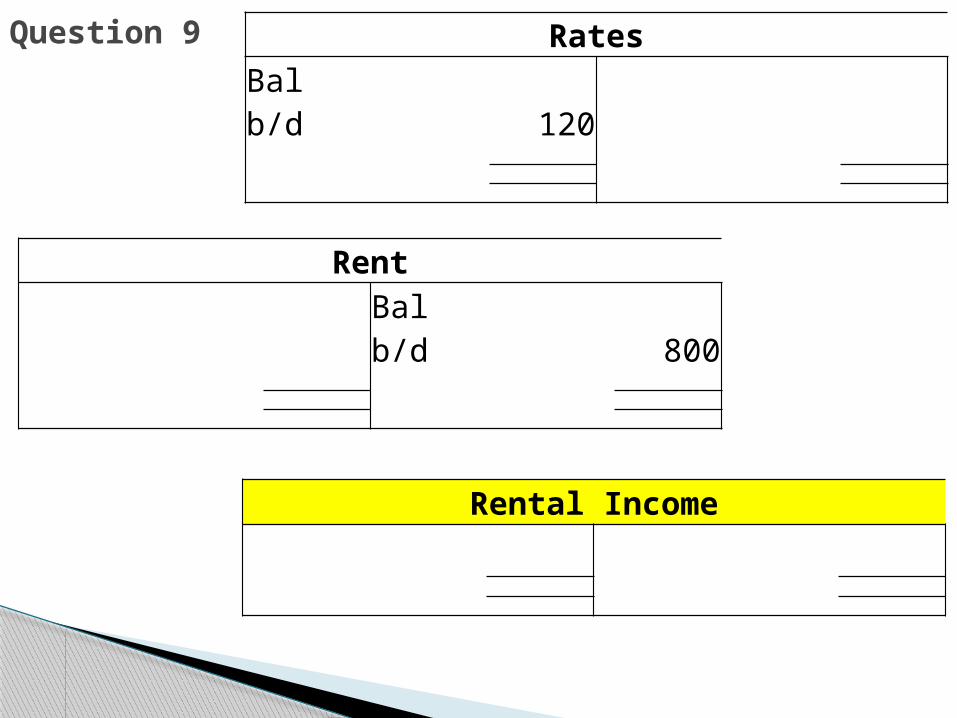

Question 9 Rates

Bal b/d 120

Rent

Rental Income

Question 9 Rates

Bal b/d 120

Rent

Bal b/d 800

Rental Income

Question 9 Rates

Bal b/d 120

Rent

Bal b/d 800

Rental Income