week4 - capital budgeting 1 - exeterpeople.exeter.ac.uk/wl203/beam013/materials/week4 -...

TRANSCRIPT

Week 5 1

Capital budgeting - 1

CORPORATE FINANCE - 1

UNIVERSITY OF EXETER

MARK FREEMAN, 2004

Week 5 2

Project valuation

Today, you are going to value the following project.

Initial cost of the project: £2.5m to be invested immediately.

The best projection for the number of items sold for the next

seven years is (with nothing after this):

Year 1 2 3 4 5 6 7

Sales 10000 20000 22000 24200 24200 12100 0

Next year you expect to be able to sell these items at £100

each. There is a fixed cost of production each year of

£500,000 and a variable cost of production of £25 an item.

You pay no corporate tax

The risk-free rate currently stands at 5% and inflation is at

3%. You believe that these cashflows should be discounted at

a risk premium of 8%.

Week 5 3

Cashflows

The first thing you must do is to calculate the net cashflow.

Now, it is very important that you remember to include the

inflation component when calculating the cashflows. If you

don’t do this, you will be in trouble.

Year 0 1 2 3 4 5 6

Invested

(£m)

(2.50)

Sales 10000 20000 22000 24200 24200 12100

T/o (£m) 1.00 2.06 2.33 2.64 2.72 1.40

Fixed

cost (£m)

(0.50) (0.52) (0.53) (0.55) (0.56) (0.58)

Variable

cost (£m)

(0.25) (0.52) (0.58) (0.66) (0.68) (0.35)

Net

Cashflow

(£m)

(2.50) 0.25 1.02 1.22 1.43 1.48 0.47

Week 5 4

Payback periods

The first way of evaluating this project is to calculate the

payback period. How long does it take you to get back the

initial £2.5m?

By the end of year 1 you will have £0.25m

By the end of year 2 you will have £1.27m

By the end of year 3 you will have £2.49m

You need £2.5m to payback the initial investment. So, a

further £2.5 - £2.49m = £0.01m is needed. The payback

period is therefore almost exactly 3 years.

The advantage of using the payback period for evaluating

projects is that it is simple and may be useful for companies

that have serious problems with cash flow management.

There are many disadvantages. It takes no account of the time

value of money. It penalizes long-term projects in favour of

short-term projects.

Week 5 5

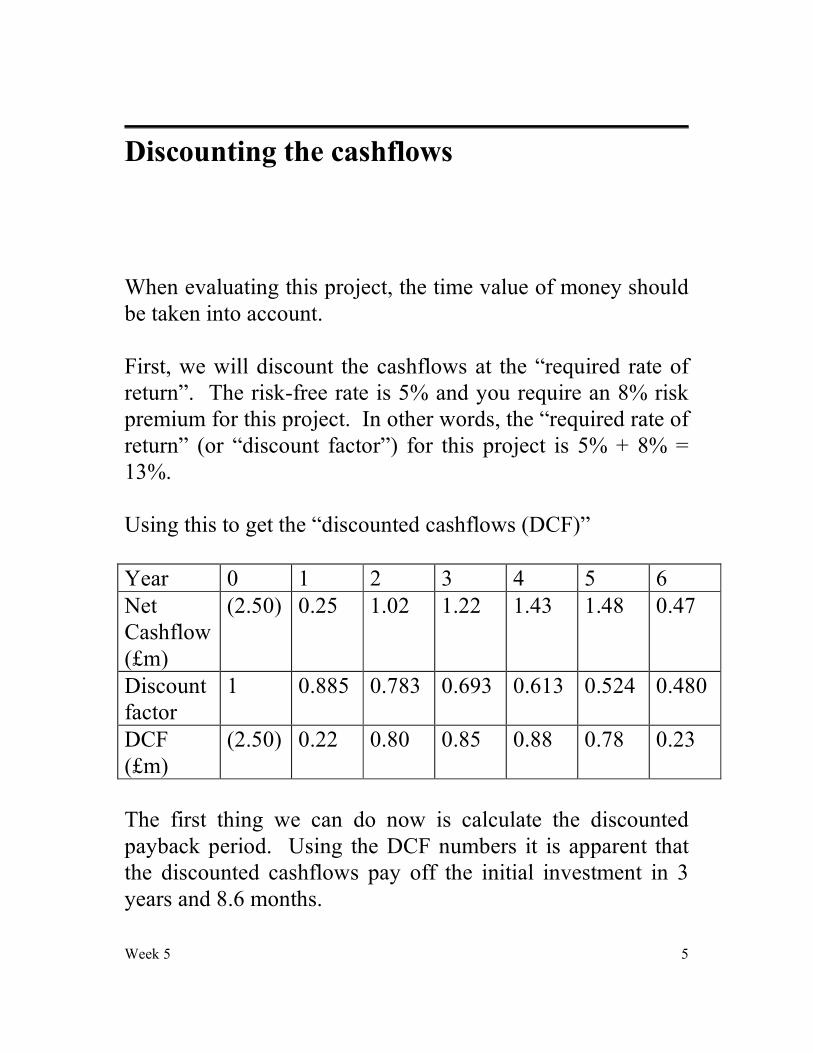

Discounting the cashflows

When evaluating this project, the time value of money should

be taken into account.

First, we will discount the cashflows at the “required rate of

return”. The risk-free rate is 5% and you require an 8% risk

premium for this project. In other words, the “required rate of

return” (or “discount factor”) for this project is 5% + 8% =

13%.

Using this to get the “discounted cashflows (DCF)”

Year 0 1 2 3 4 5 6

Net

Cashflow

(£m)

(2.50) 0.25 1.02 1.22 1.43 1.48 0.47

Discount

factor

1 0.885 0.783 0.693 0.613 0.524 0.480

DCF

(£m)

(2.50) 0.22 0.80 0.85 0.88 0.78 0.23

The first thing we can do now is calculate the discounted

payback period. Using the DCF numbers it is apparent that

the discounted cashflows pay off the initial investment in 3

years and 8.6 months.

Week 5 6

Net Present Value (NPV)

The next way of doing the analysis is just to add up all the

DCFs to get the net present value (NPV).

NPV = (2.50) + 0.22 + 0.80 + 0.85 + 0.88 + 0.78 + 0.23

= £1.26m.

The decision rule based on NPV analysis is:

Positive NPV Good project

Negative NPV Bad project

Given that this is positive, this appears to be a good project.

As we will see below, NPV analysis will be our chosen

method of project appraisal. Before we reach this conclusion,

though, we must consider some alternatives…

Week 5 7

Internal Rates of Return (IRR)

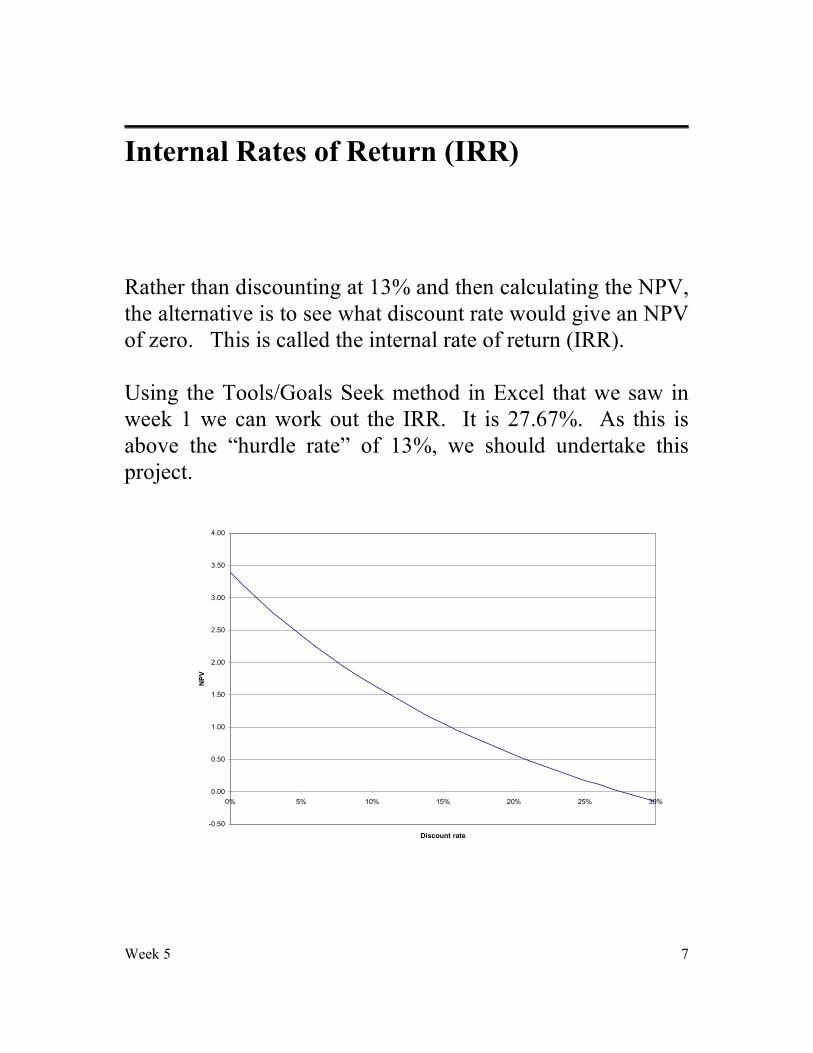

Rather than discounting at 13% and then calculating the NPV,

the alternative is to see what discount rate would give an NPV

of zero. This is called the internal rate of return (IRR).

Using the Tools/Goals Seek method in Excel that we saw in

week 1 we can work out the IRR. It is 27.67%. As this is

above the “hurdle rate” of 13%, we should undertake this

project.

-0.50

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

0% 5% 10% 15% 20% 25% 30%

Discount rate

NPV

Week 5 8

Changing the project

Suppose that, we can secure a further order from a customer

that will be worth £4m in revenue at the end of the third year.

This will lead to additional incremental costs of £7.4m.

However, we can defer these costs to £2.9m at the end of the

fifth year and a further £4.5m at the end of the sixth year.

Does this new order make the project more or less attractive

to us?

It is “obvious” that this is a bad deal. The effective rate of

return that we are paying on this new order is:

3)1(

5.4

2)1(

9.24

rr +

+

+

=

Solving, r = 26.94%. For a project with a discount rate of

13%, this effective interest rate of 26.94% that we are paying

to secure the new order is clearly too high.

How does this look if we put it into our project analysis?

Payback is now clearly within three years, as the cash inflow

from the new order will pay off the initial investment.

Week 5 9

Changing the project - 2

Consider the cashflows now:

Year 0 1 2 3 4 5 6

Project

Cashflow

(2.50) 0.25 1.02 1.22 1.43 1.48 0.47

New

order

4.00 (2.90) (4.50)

New net

Cashflow

(2.50) 0.25 1.02 5.22 1.43 (1.42) (4.03)

Discount

factor

1 0.885 0.783 0.693 0.613 0.524 0.480

DCF

(£m)

(2.50) 0.22 0.80 3.62 0.88 (0.74) (1.93)

The NPV is now –2.50 + 0.22 + 0.80 + 3.62 + 0.88 – 0.74 –

1.93 = £0.35m

This NPV is lower than it was without the new order (when

the NPV was £1.26m). Therefore, the decision rule that the

higher the NPV the better the project works in this case.

Week 5 10

Changing the project - 3

If we work out the IRR of the project, though, there are two

problems.

1) There is an internal rate of return = 28.70%. This is

higher than the IRR without the new order (which was

26.94%). So, higher IRR does not mean better project.

2) There is a second IRR of 0.142%. That is, the IRR is not

unique. What does this mean?

-0.10

-0.05

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0% 5% 10% 15% 20% 25% 30%

Discount rate

NPV

Week 5 11

Multiple IRRs

When, and why, do we have this problem of multiple IRRs?

This arises when, after the initial investment, the net

cashflows are sometimes positive and sometimes negative. In

this example, the net cashflows start positive and end

negative.

As the discount rate increases this has two offsetting effects:

1) It makes the cashflows from the project less valuable in

present value terms

2) Our obligations in years 5 and 6 also have a lower

present value.

Therefore, there are offsetting effects from increasing the

discount rate. That is why the last graph is strangely “non-

linear” and why multiple IRRs exist.

The more often the net cashflow changes between positive

and negative, the more IRRs can potentially exist.

Week 5 12

Accounting ratios

Some managers like to evaluate projects on the basis of

accounting ratios. For example, you could calculate a return

on capital employed (ROCE) each year:

ROCE = Accounting profit after depreciation and tax

Book value of capital employed at beginning of

year

There are several reasons why this method is not favoured in

finance. First, and most importantly, this number depends on

somewhat subjective accounting conventions. Second, as

this ratio varies year by year, it is not clear how to interpret it.

The finance community prefers to use cashflows rather than

accounting profits since cashflow numbers are

uncontroversial.

This technique is still quite commonly used in practice,

however, as many senior finance directors come from an

accounting background and are more confident dealing with

accounting numbers than projecting cashflows.

Week 5 13

In summary

We have looked at four possible methods of evaluating

projects.

1) NPV

2) IRR Problem with multiple IRRs

3) Payback period Undervalues long-term projects

4) ROCE Subject to accounting conventions

The preferred method is NPV because:

a) The decision rules are easy. You should (should not)

undertake the project if the NPV is positive (negative).

The higher the NPV, the better the project. It is unique.

b) The technique is identical to the methods that we used to

price Treasury securities and the discounted dividend

model for valuing stock. The discounted cashflow

method is a general method of valuing investment

opportunities

c) There is no subjectivity over accounting conventions.

d) For those of you who like a very solid theoretical

grounding for your methods, there is a “fundamental

theorem of asset pricing” which demonstrates

unambiguously that the NPV method is “correct” when

excluding project flexibility.

Week 5 14

What do practitioners actually use?

Graham and Harvey (2001, Journal of Financial Economics)

undertake a major survey of US corporations to see what

corporate finance practices they actually use. They find that

the following proportion of CFOs “almost always” use the

following techniques1:

Technique % managers using

IRR 76%

NPV 75%

Payback period 57%

Sensitivity analysis 52%

Discounted payback 29%

Real Options 27%

ROCE 20%

We will return to real options later in the course.

1 Other methods are also used by corporations, but these are much less important than NPV / IRR.

Week 5 15

The fundamentals of NPV analysis

There are three steps that must be completed before we can

undertake an NPV analysis:

1) We must estimate the expected pre-tax cashflows from

the project for each period between the date that the

project is started and the date it terminates.

2) We must calculate the tax implications of these

cashflows.

3) We must calculate the appropriate discount rate to use.

For the rest of this class we shall concentrate on the

fundamentals of estimating pre-tax cashflows.

Week 5 16

Inflating the cashflows

In the example given above, it was emphasized that we had to

inflate the cashflows.

Why?

The required rate of return was calculated by adding a risk

premium of 8% onto the risk-free rate of 5%.

But this risk-free rate of 5% includes an inflation term of 3%

and a real risk-free rate term of 1.94% (From Fisher’s

theorem, 1.05 = 1.03 x 1.0194). That is, the discount rate

includes the inflation component already.

To be consistent, therefore, we need also to include the

inflation element into our cashflows. This is called “nominal”

discounting – we include inflation in both the discount rate

and the cashflows.

Week 5 17

Real vs. nominal analysis

Some people do “real” discounting – that is, they remove the

inflation component from the discount rate and then do not

inflate the cashflows. If done correctly this should always

give the same answer.

My advice, though, is to do nominal analysis. The main

reason for this is that certain cashflows do not inflate

whatever happens to the inflation rate. In the example given

above, the cashflows to and from the venture capitalist are not

inflated.

Of particular importance will be tax-related cashflows.

These never inflate. So, if you do real analysis, not only do

you have to deflate the discount rate, you also need to deflate

certain cashflows.

So, while doing “real” analysis is completely correct if done

properly, my view is that you are more likely to make

mistakes this way. For this reason, all the examples in this

class will be done nominally.

Week 5 18

What cashflows do we discount?

We define the relevant net pre-tax cashflows as follows:

Pre-tax = Cash received from sales

Cashflow - Cash paid out on operating expenses

- Capital outlays as they occur

- Increases in net working capital

Or, comparing with profit:

Pre-tax = Earnings before interest and tax

Cashflow + Non-cashflow expenses (mainly depreciation)

- Capital outlays

- Increase in net working capital

Key differences:

1) Cashflow takes the full amount of investment on the date

the cost is incurred and does not depreciate them.

2) Costs and revenues are included on the date when the

cash is paid/received and not on the date when they

accrue.

3) Spending cash to increase inventory is considered a

cashflow even though this has no effect on profit.

4) Interest payments are not taken into account.

Week 5 19

Key issues in cashflow estimation

1) Because cashflows are considered on the date that they

are paid/received, sunk costs are never included in NPV

analysis. These cashflows are in the past already.

2) When evaluating a project, it is the incremental

cashflows that are important. The cashflow that should

be discounted is the difference between what we expect

to receive if we undertake the project compared with

what we would expect in the absence of the project.

3) Incremental cashflows should include the opportunity

cost of cashflows lost as a consequence of starting a

project.

4) NPV analysis should be undertaken from a corporate, not

a divisional perspective. Whether these cashflows occur

in your division or not is irrelevant.

5) For this reason, the allocation of costs is completely

irrelevant to NPV analysis.

Week 5 20

“Practical” cashflow estimation

While the appropriate technique for estimating cashflows

varies widely from industry to industry, there are certain

general rules that can be used.

In particular, it is often possible to estimate cashflows with

some precision in the short term. It is then difficult to make

predictions as to what will happen in the longer term.

For this reason, we need to worry about “terminal value

calculations” – how we estimate the value of the project in the

distant future.

So suppose that we are able to make accurate profit forecasts

for the next seven years, and that, in year 7 we will be making

net operating cashflows of £1m per year. Assume that we are

discounting the cashflows at 13% per year – reflecting a 5%

risk-free rate and an 8% risk premium.

Week 5 21

Terminal values

There are several assumptions that we could make:

1) Assume that there are no more profits to be made. In this

case the NPV just comes from the first seven years.

2) Assume that the operating cashflows are going to decline

– say straight line – to zero in say year 12. In this case,

the NPV is the present value for the first seven years plus

Year 8 Year 9 Year 10 Year 11 Year 12

Cashflo

w

800,000 600,000 400,000 200,000 0

Discount 0.376 0.332 0.295 0.261 0.231

PV 301,000 200,000 118,000 52,000 0

Therefore, this gives an NPV of 671,000 more than

method (1)

3) Assume that profits will decline slowly indefinitely.

That is, assume that the decline in net cashflows will be,

say, 5% per year on a declining balance basis. In this

case, we can use the Gordon Growth Formula to get the

terminal value. In terms of year 7 pounds, the terminal

value will then be:

000,280,5)05.0(13.0

05.01*000,000,1 =

−−

−

Week 5 22

Terminal values - 2

3...) This, though is in terms of year seven pounds. So, in

year 0 pounds, this is equivalent to

000,240,27)13.1/(000,280,5 = . This gives a much higher

PV than methods (1) and (2)

4) We could use the annuity formula to assume that

cashflows will remain unchanged for, say, a further 5

years and then decline.

5) Any combination of these things.

What I am trying to demonstrate here is that whether we get a

positive NPV or not is often a factor of what terminal value

assumptions we make. But, almost by definition, the terminal

value is the hardest thing to estimate. This is a major problem

with NPV analysis.

Week 5 23

Manipulated NPVs

Sometime managers have an incentive to “fix” their NPV.

You should be aware of some of the tricks that they play. The

easiest number to manipulate on an NPV is the terminal value.

Therefore, when I am evaluating someone else’s NPV this is

the first number that I look at. Essentially, I am very wary

when “too much” of the present value comes from terminal

cashflows. In some cases it can be as much as 50% of the

total present value.

This is clearly worrying and I would be very reluctant to

accept such a project without seeing a detailed analysis of

why the cashflows were taking so long to come through.

So, beware. Do not spend 99% of your analysis time

estimating cashflows for the first few years and then 1% of

your time “throwing in” a terminal value – particularly if the

terminal value accounts for a large proportion of the total

present value. This is a very common mistake in practice.

Week 5 24

Sensitivity analysis

Hopefully, by now, you are realizing that there is a great deal

of subjectivity when doing NPV analysis. How are you going

to estimate your cashflows? What terminal value assumption

do you make? …

For this reason, it is strongly recommended that you do

sensitivity analysis when undertaking NPV analysis. Try

different scenarios. Under what conditions is the NPV

positive and when is it negative? What is the worst (realistic)

case? What would be the consequences in the worse case?

That is, rather than accepting all projects with positive NPV

and rejecting projects with negative NPV (the most naïve

textbook approach), this technique should be used as a tool to

help you make a management decision. Certainly, the more

positive the NPV the more optimistic you should be about the

project. But you should carefully consider the assumptions

made in doing the analysis, consider how robust these

assumptions are and what will happen if things do not go

according to plan.

Week 5 25

Questions – Week 5

CORPORATE FINANCE - 1

UNIVERSITY OF EXETER

MARK FREEMAN, 2004

Week 5 26

Question set 4

1) Work out the payback period, the NPV and IRR of the following project.

Assume that there is no taxation. The nominal discount rate is 15% and

the inflation rate is 3% per year into the foreseeable future. Should you

undertake the project or not?

The project requires immediate capital investment of £250,000. Sales in

year 1 are expected to be 5,000 items. In year 2 sales will increase to

10,000 items. From years 3 to 6, sales will be at 20,000 items a year.

There will be no more sales after year 6. It is expected that, in year 1, each

item will sell for £75. The expected fixed cost of production in year 1 is

£500,000 with a marginal cost of production of £35 per item. All costs

and revenues are expected to increase in line with inflation.

2) How does the NPV that you calculated in question 1 change if the firm

needs to hold 15% of annual sales (in value terms) in inventories?

3) How does the NPV that you calculated in question 2 change if you have

already invested £100,000 in management consulting fees in preparation

for this project?

4) How does the NPV that you calculate in question 3 change if, for each

item you sell, another division within your organization loses £1 in profit

(in terms of year 1 pounds) because you are “cannibalizing” some of their

sales.

5) How does the NPV that you calculated in question 4 change if you are

allocated with £100,000 of central overheads per year?

6) How does the NPV that you calculated in question 5 change if you assume

that, instead of sales going to zero after year six, the net cashflows from

question 1 decreases at 10% per year (after adjusting for inflation)

indefinitely but that there are no cashflow implications from (2) – (5) after

year 6?