weekly market report - files.irwebpage.comfiles.irwebpage.com/reports/shipping/0ygu35tu0z/intermodal...

TRANSCRIPT

Broker’s insight by Nikos Papantonopoulos

Elabora�ng further on last week's report regarding game theory in shipping

and how it can affect the shipping market according to the decisions made by

ship owners, it’s interes�ng to examine the influence of shipping pools on

the market with par�cular focus on the VLCC market because as it comprises

of more limited number of vessels and charterers, the results are more than

conspicuous.

Over the past two years there has been a growth of demand in the AG mar-

ket which has varied between 25% - 30%, while the total growth of supply

has been around 10%. It looks like a booming market but numbers don't

always reveal all. The 10% fleet growth was achieved thanks to a heavy

scrapping programming which has been undertaken since 2009, culmina�ng

in 2011 were we even started to see as young as 16 years old vessels exi�ng

the market. At the same �me, on the demand side we have only just man-

aged to see global crude oil trade volume match and surpass its pre-crisis

levels. Nevertheless, the TCE for early February fixtures was at around 17k-

18k USD per day while today it is almost 3 �mes that. We have even started

to see fixtures in the WS 70’s range for Eastbound voyages. What could have

possibly lead to such a sudden recovery in freight rates?

As you may have guessed, the Nova Tankers pool started its opera�ons. This

new VLCC pool has collected vessels from its partners Mitsui O.S.K. lines,

Phoenix tankers, Maersk tankers, Samco Shipholding and Ocean Tankers.

They are opera�ng less than 10% of the total fleet but we are observing that

the impact of their ac�on had a appreciable change on market levels. We

fully understand the argument that the start of the pool's opera�ons is not

the only reason for this improvement in rates; however nobody can deny

that the pool created a balance between orders and spot vessels in the AG.

As you know, the key factor for this rise is that the pool is able to provide

owners with extra bargaining power by “hiding” some spot vessels as well as

“presen�ng” fewer in each main trading area (i.e AG and USG). On the other

hand, if more and more owners put their vessels in pools, then they will fail

to secure as aErac�ve a return because in order to fix a tanker on a higher

rate they also need to simultaneously cover 3 or 4 hidden spot vessels. As

such it could prove to be more beneficiary for an owner to be in a market

where there is a pool but he himself is outside it.

The rela�onship therefore between owners and pools is reversely correlated

with shipping market's cycle because reaching the upper side of a cycle, own-

ers will be keen to leave the pool in order to maximize their return from the

firm spot market. Their exit from the pool will increase the compe��on, as

owners are no longer working coopera�vely, and as such freight rates will

drop. It is usually during the downturns of the shipping cycle were owners

will be distressed again due to low rates and keen to operate within a pool in

an effort to survive.

In conclusion, I would like to men�on that pools are not enough to correct

the market but they help beEer organize the efforts of owners and keep

freight rates at more manageable levels during downturns. It’s not like own-

ers rediscovered the wheel....but at the end of the day its one more arrow

leH in one's quiver..

Chartering (Wet: Stable+ / Dry: Stable- )

With The Atlan�c being fairly subdued this week due to the Catholic

Easter Holidays, much of the Dry Bulk market started to slide considera-

bly as the Pacific proved incapable of dealing with the task of fully sup-

por�ng the current market. The only excep�on was seen in the Capesize

sector were we saw a slight firming of rates thanks to a renewed inter-

est and fairly �ghter tonnage lists all around. The BDI closed today

(10/04/2012) at 928 points, on par with its closure on Thursday

(05/04/2012) and a decrease of 6 points compared to the previous Fri-

day’s levels (30/03/2012). Crude Oil Carriers have proven to s�ll be on a

firm recovery path this week, with some gains noted on freight earnings

despite the notable pressure brought about by the s�ll increasing bun-

ker prices. The BDTI Thursday (05/04/2012), was at 820, 1 point up and

the BCTI at 639, a decrease of 6 points compared to the previous Mon-

day’s levels (02/04/2012).

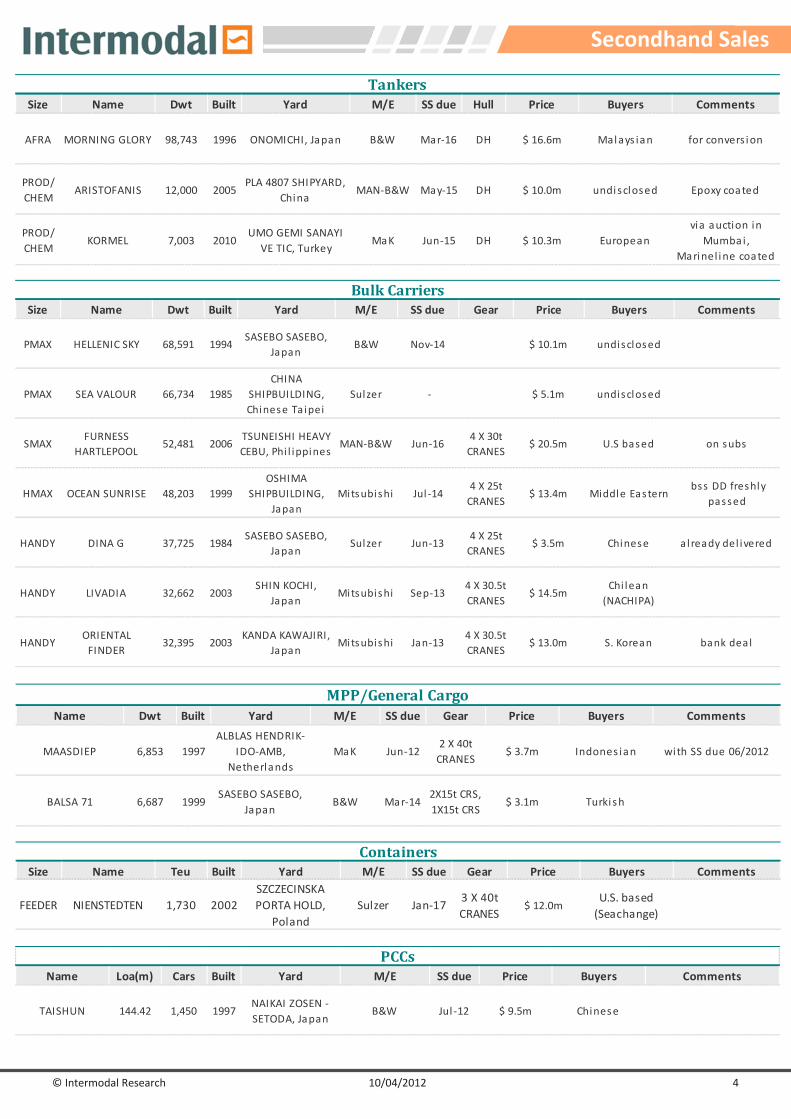

Sale & Purchase (Wet: So"er- / Dry: So"er- )

As expected ac�vity dropped further this past week as few buyers had

keen interest to close any units in haste over the Easter holidays, while

many are s�ll delaying any investment decisions in an effort as it seems

to get beEer clarity with regards to market direc�on and prospects. On

the Tankers side, we saw the sale of the Aframax “Morning Glo-

ry” (98,743dwt-blt 96 Japan) which reportedly went to Malaysian con-

version buyers for a price of $ 16.6m. This is equivalent to around $

27.5m each. While on the dry bulker of interest was the reported sale of

the Handymax “Ocean Sunrise” (48,203dwt-blt 99 Japan) which went to

Middle Eastern buyers for a price of $ 13.4m basis Dry Dock surveys

freshly passed.

Newbuilding (Wet: Stable- / Dry: Stable- )

Not much reported ac�vity this week, with most of the surfaced deals

being under nego�a�ons from a while back. What's more, is that we are

likely to see slow ac�vity up un �ll and including next Monday

(16/04/2012) as the Greek Orthodox Easter falls one week aHer the

Catholic one this year. This means that many of the Greek Owners which

could poten�ally be contempla�ng a new building order, are likely to

hold back and refrain any further nego�a�ons un�l aHer the holydays.

In terms of reported deals this week, most notable was the reported

order placed by Israeli Ray Shipping for four firm Supramax (56,000dwt)

bulkers at S.Korea’s Hyundai Mipo for a reported price of $ 25.0m each.

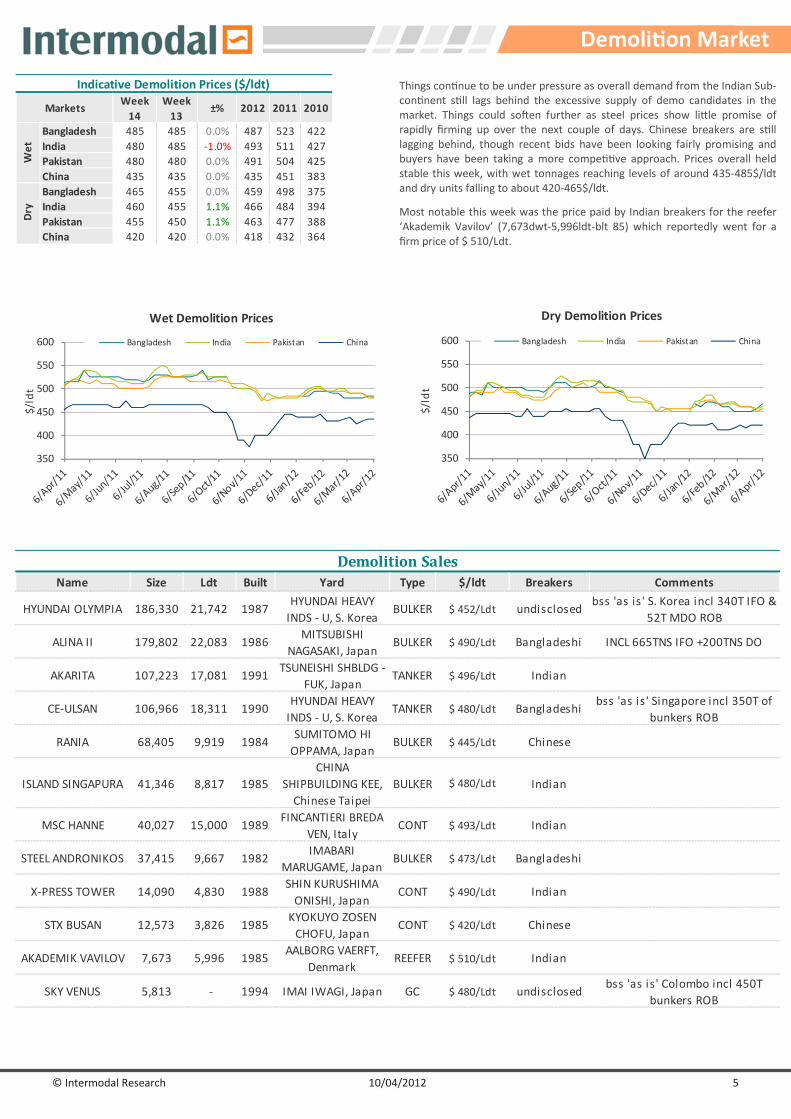

Demoli&on (Wet: Stable- / Dry: Stable- )

Things con�nue to be under pressure as overall demand from the Indian

Sub-con�nent s�ll lags behind the excessive supply of demo candidates

in the market. Things could soHen further as steel prices show liEle

promise of rapidly firming up over the next couple of days. Chinese

breakers are s�ll lagging behind, though recent bids have been looking

fairly promising and buyers have been taking a more compe��ve ap-

proach. Prices overall held stable this week, with wet tonnages reaching

levels of around 435-485$/ldt and dry units falling to about 420-465$/

ldt.

Weekly Market Report

Week 14|Tuesday 10th April 2012

© Intermodal Research 10/04/2012 2

6080

100120140160180200220240260

WS poin

ts

CLEAN - WS RATESTC2 TC4 TC6 TC1

20

40

60

80

100

120

140

160

WS poin

ts

DIRTY - WS RATESTD3 TD5 TD8 TD4

Apr-12 Mar-12 ±% 2012 2011 2010

300KT DH 63.0 63.0 0.0% 64.0 77.6 87.2

150KT DH 44.5 44.5 0.0% 46.4 54.4 62.6

105KT DH 30.0 32.0 -6.3% 34.2 39.1 44.7

70KT DH 26.0 27.6 -5.8% 29.4 35.2 38.8

45KT DH 25.4 25.4 0.0% 25.8 28.4 26.5

Aframax

Panamax

VLCC

Suezmax

Indicative Market Values ($ Million) - Tankers

Vessel 5yrs old

MR

Week 14 Week 13 ±% Diff 2012 2011

300k 1yr TC 22,500 21,500 4.7% 1000 20,536 25,197

300k 3yr TC 29,000 29,000 0.0% 0 26,361 31,681

150k 1yr TC 17,500 17,000 2.9% 500 16,464 19,837

150k 3yr TC 21,500 19,500 10.3% 2000 19,986 23,830

105k 1yr TC 14,250 14,250 0.0% 0 13,982 15,707

105k 3yr TC 16,500 16,500 0.0% 0 16,200 18,335

70k 1yr TC 13,000 13,500 -3.7% -500 13,214 14,995

70k 3yr TC 14,500 14,750 -1.7% -250 14,432 16,263

45k 1yr TC 14,750 14,750 0.0% 0 14,429 13,918

45k 3yr TC 15,250 15,250 0.0% 0 14,879 14,738

36k 1yr TC 13,000 13,000 0.0% 0 12,482 12,471

36k 3yr TC 13,500 13,500 0.0% 0 13,200 13,412

Panamax

MR

Handy

size

TC Rates

$/day

VLCC

Suezmax

Aframax

2012 2011

WS

points$/day

WS

points$/day $/day $/day

265k AG-JAPAN 70 51,111 70 54,593 0% 33,278 18,217

280k AG-USG 43 11,931 40 10,964 6% 4,529 2,504

260k WAF-USG 70 43,460 65 45,719 8% 43,794 25,714

130k MED-MED 80 20,244 80 24,001 0% 31,447 25,125

130k WAF-USAC 75 13,215 75 14,144 0% 19,815 13,373

130k AG-CHINA 80 18,275 80 19,666 0% 23,188 14,815

80k AG-EAST 100 10,625 100 11,987 0% 13,877 12,726

80k MED-MED 90 15,329 90 12,230 0% 15,431 13,577

80k UKC-UKC 100 20,930 90 14,841 11% 19,446 18,604

70k CARIBS-USG 95 2,698 100 7,658 -5% 14,753 8,240

75k AG-JAPAN 85 1,279 85 1,679 0% 2,882 10,467

55k AG-JAPAN 105 3,175 105 3,573 0% 2,592 7,768

37K UKC-USAC 135 6,800 135 7,115 0% 12,189 11,022

30K MED-MED 140 10,396 143 14,574 -2% 18,409 18,458

55K UKC-USG 125 13,590 120 12,226 4% 13,605 11,266

55K MED-USG 118 9,268 120 10,416 -2% 11,037 9,676

50k CARIBS-USAC 135 9,208 145 17,015 -7% 13,018 10,700

Spot Rates

Vessel Routes

Week 14 Week 13

±%

Dir

tyA

fram

axC

lean

VLC

CS

ue

zmax

Chartering

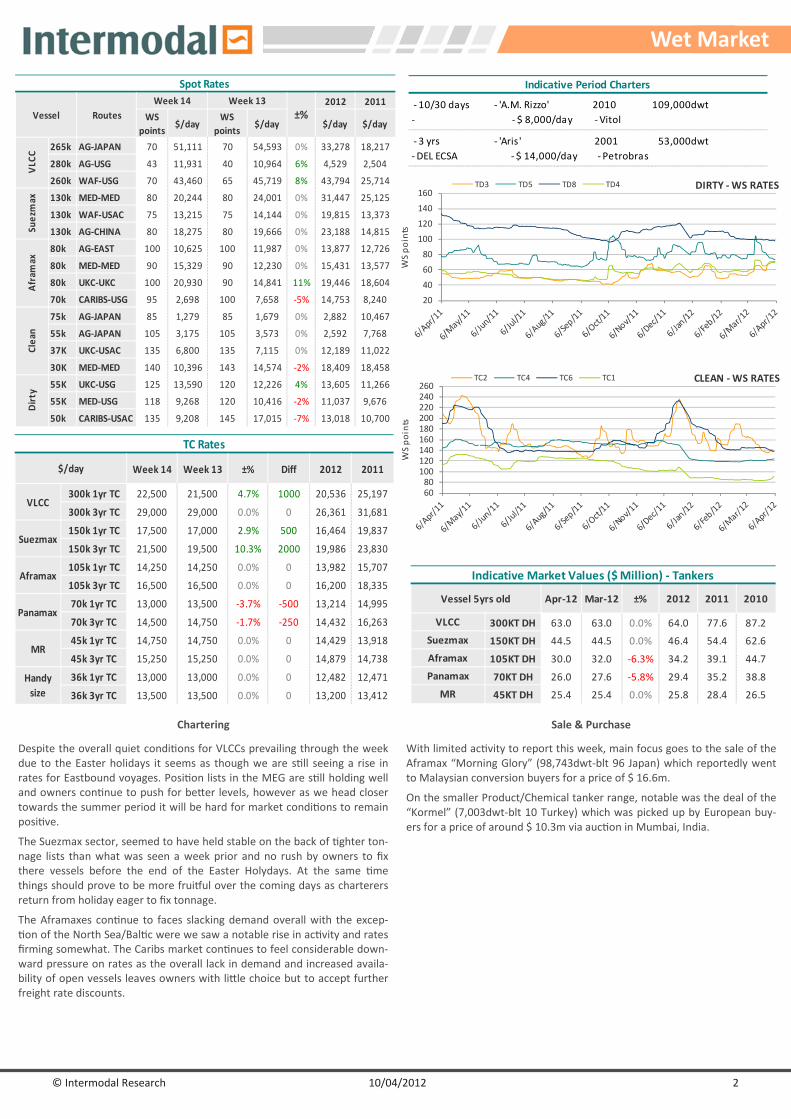

Despite the overall quiet condi�ons for VLCCs prevailing through the week

due to the Easter holidays it seems as though we are s�ll seeing a rise in

rates for Eastbound voyages. Posi�on lists in the MEG are s�ll holding well

and owners con�nue to push for beEer levels, however as we head closer

towards the summer period it will be hard for market condi�ons to remain

posi�ve.

The Suezmax sector, seemed to have held stable on the back of �ghter ton-

nage lists than what was seen a week prior and no rush by owners to fix

there vessels before the end of the Easter Holydays. At the same �me

things should prove to be more fruiRul over the coming days as charterers

return from holiday eager to fix tonnage.

The Aframaxes con�nue to faces slacking demand overall with the excep-

�on of the North Sea/Bal�c were we saw a notable rise in ac�vity and rates

firming somewhat. The Caribs market con�nues to feel considerable down-

ward pressure on rates as the overall lack in demand and increased availa-

bility of open vessels leaves owners with liEle choice but to accept further

freight rate discounts.

Sale & Purchase

With limited ac�vity to report this week, main focus goes to the sale of the

Aframax “Morning Glory” (98,743dwt-blt 96 Japan) which reportedly went

to Malaysian conversion buyers for a price of $ 16.6m.

On the smaller Product/Chemical tanker range, notable was the deal of the

“Kormel” (7,003dwt-blt 10 Turkey) which was picked up by European buy-

ers for a price of around $ 10.3m via auc�on in Mumbai, India.

Wet Market

Indicative Period Charters

- 10/30 days - 'A.M. Rizzo' 2010 109,000dwt

- - $ 8,000/day - Vitol

- 3 yrs - 'Aris' 2001 53,000dwt

- DEL ECSA - $ 14,000/day - Petrobras

© Intermodal Research 10/04/2012 3

Index $/day Index $/day Index Index

BDI 928 934 -0.6% -6 871 1,549

BCI 1,507 $6,205 1,412 $5,188 6.7% 95 1,578 2,237

BPI 1,036 $8,277 1,051 $8,398 -1.4% -15 1,002 1,749

BSI 949 $9,928 1,030 $10,767 -7.9% -81 840 1,377

BHSI 547 $8,305 565 $8,572 -3.2% -18 471 718

30/03/12

Baltic IndicesWeek 14

06/04/12

Week 13

±%2012 2011Point

Diff

0

1,000

2,000

3,000

4,000

5,000

Index

Baltic Indices

BCI BPI BSI BHSI BDI

170K 6mnt TC 13,750 12,500 10% 1,250 14,280 18,474

170K 1yr TC 15,000 14,750 2% 250 16,343 17,138

170K 3yr TC 16,250 16,250 0% 0 17,200 17,599

70K 6mnt TC 13,125 13,250 -1% -125 12,566 17,238

70K 1yr TC 11,000 11,250 -2% -250 11,245 14,863

70K 3yr TC 12,375 12,250 1% 125 11,986 14,500

52K 6mnt TC 12,500 13,000 -4% -500 11,361 15,587

52K 1yr TC 11,750 12,000 -2% -250 11,093 14,308

52K 3yr TC 12,500 12,500 0% 0 12,164 14,046

45k 6mnt TC 11,250 11,250 0% 0 9,468 13,416

45k 1yr TC 10,500 11,000 -5% -500 9,218 12,450

45k 3yr TC 10,500 10,500 0% 0 10,218 12,403

30K 6mnt TC 9,000 9,000 0% 0 8,111 11,712

30K 1yr TC 9,250 9,250 0% 0 8,450 11,787

30K 3yr TC 10,000 10,000 0% 0 10,236 12,044

Ha

nd

yma

xH

an

dy

size

Period

2011

Pa

nam

axSu

pra

ma

x

Week

14

Week

13

Cap

esi

ze

2012$/day ±% Diff

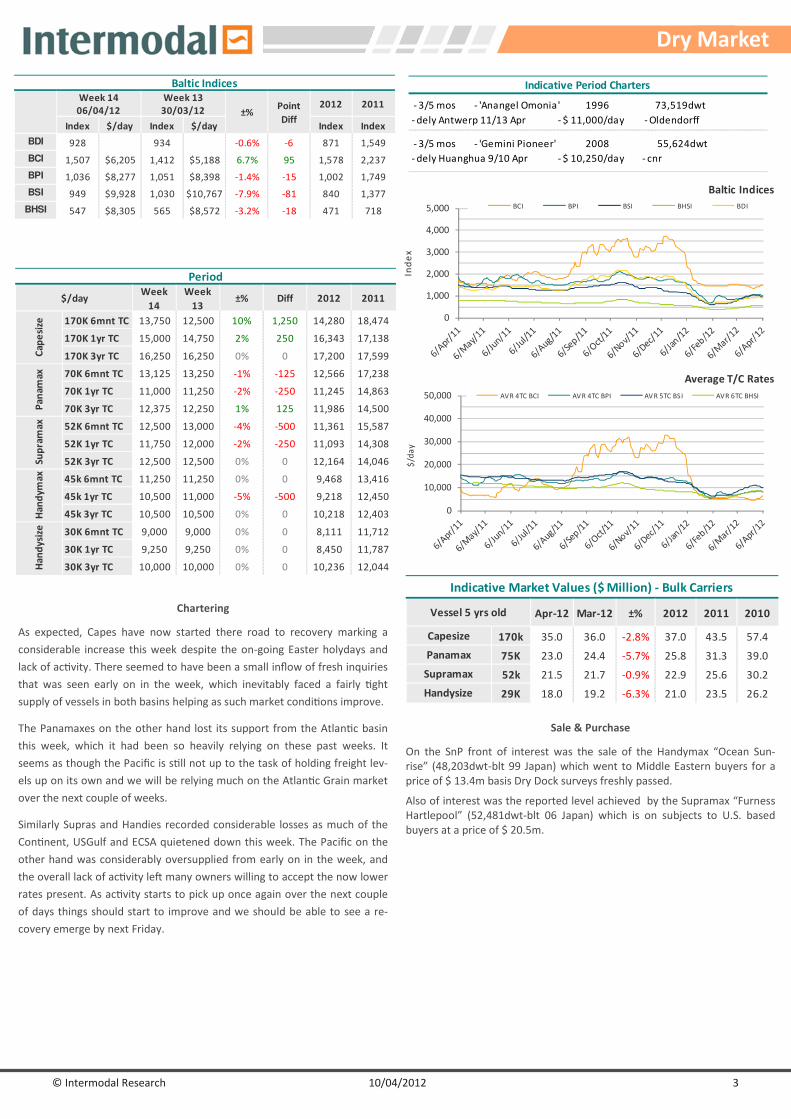

Chartering

As expected, Capes have now started there road to recovery marking a

considerable increase this week despite the on-going Easter holydays and

lack of ac�vity. There seemed to have been a small inflow of fresh inquiries

that was seen early on in the week, which inevitably faced a fairly �ght

supply of vessels in both basins helping as such market condi�ons improve.

The Panamaxes on the other hand lost its support from the Atlan�c basin

this week, which it had been so heavily relying on these past weeks. It

seems as though the Pacific is s�ll not up to the task of holding freight lev-

els up on its own and we will be relying much on the Atlan�c Grain market

over the next couple of weeks.

Similarly Supras and Handies recorded considerable losses as much of the

Con�nent, USGulf and ECSA quietened down this week. The Pacific on the

other hand was considerably oversupplied from early on in the week, and

the overall lack of ac�vity leH many owners willing to accept the now lower

rates present. As ac�vity starts to pick up once again over the next couple

of days things should start to improve and we should be able to see a re-

covery emerge by next Friday.

Sale & Purchase

On the SnP front of interest was the sale of the Handymax “Ocean Sun-

rise” (48,203dwt-blt 99 Japan) which went to Middle Eastern buyers for a

price of $ 13.4m basis Dry Dock surveys freshly passed.

Also of interest was the reported level achieved by the Supramax “Furness

Hartlepool” (52,481dwt-blt 06 Japan) which is on subjects to U.S. based

buyers at a price of $ 20.5m.

0

10,000

20,000

30,000

40,000

50,000

$/d

ay

Average T/C Rates

AVR 4TC BCI AVR 4TC BPI AVR 5TC BSI AVR 6TC BHSI

Apr-12 Mar-12 ±% 2012 2011 2010

170k 35.0 36.0 -2.8% 37.0 43.5 57.4

75K 23.0 24.4 -5.7% 25.8 31.3 39.0

52k 21.5 21.7 -0.9% 22.9 25.6 30.2

29K 18.0 19.2 -6.3% 21.0 23.5 26.2Handysize

Capesize

Panamax

Supramax

Indicative Market Values ($ Million) - Bulk Carriers

Vessel 5 yrs old

Dry Market

Indicative Period Charters

- 3/5 mos - 'Anangel Omonia' 1996 73,519dwt

- dely Antwerp 11/13 Apr - $ 11,000/day - Oldendorff

- 3/5 mos - 'Gemini Pioneer' 2008 55,624dwt

- dely Huanghua 9/10 Apr - $ 10,250/day - cnr

© Intermodal Research 10/04/2012 4

Secondhand Sales

Size Name Dwt Built Yard M/E SS due Hull Price Buyers Comments

AFRA MORNING GLORY 98,743 1996 ONOMICHI, Japan B&W Mar-16 DH $ 16.6m Malays ian for convers ion

PROD/

CHEMARISTOFANIS 12,000 2005

PLA 4807 SHIPYARD,

ChinaMAN-B&W May-15 DH $ 10.0m undisclosed Epoxy coated

PROD/

CHEMKORMEL 7,003 2010

UMO GEMI SANAYI

VE TIC, TurkeyMaK Jun-15 DH $ 10.3m European

via auction in

Mumbai ,

Marinel ine coated

Tankers

Size Name Dwt Built Yard M/E SS due Gear Price Buyers Comments

PMAX HELLENIC SKY 68,591 1994SASEBO SASEBO,

JapanB&W Nov-14 $ 10.1m undisclosed

PMAX SEA VALOUR 66,734 1985

CHINA

SHIPBUILDING,

Chinese Ta ipei

Sulzer - $ 5.1m undisclosed

SMAXFURNESS

HARTLEPOOL52,481 2006

TSUNEISHI HEAVY

CEBU, Phi l ippinesMAN-B&W Jun-16

4 X 30t

CRANES$ 20.5m U.S based on subs

HMAX OCEAN SUNRISE 48,203 1999

OSHIMA

SHIPBUILDING,

Japan

Mitsubishi Jul -144 X 25t

CRANES$ 13.4m Middle Eastern

bss DD freshly

passed

HANDY DINA G 37,725 1984SASEBO SASEBO,

JapanSulzer Jun-13

4 X 25t

CRANES$ 3.5m Chinese a lready del ivered

HANDY LIVADIA 32,662 2003SHIN KOCHI,

JapanMitsubishi Sep-13

4 X 30.5t

CRANES$ 14.5m

Chi lean

(NACHIPA)

HANDYORIENTAL

FINDER32,395 2003

KANDA KAWAJIRI,

JapanMitsubishi Jan-13

4 X 30.5t

CRANES$ 13.0m S. Korean bank dea l

Bulk Carriers

Name Dwt Built Yard M/E SS due Gear Price Buyers Comments

MAASDIEP 6,853 1997

ALBLAS HENDRIK-

IDO-AMB,

Netherlands

MaK Jun-122 X 40t

CRANES$ 3.7m Indones ian with SS due 06/2012

BALSA 71 6,687 1999SASEBO SASEBO,

JapanB&W Mar-14

2X15t CRS,

1X15t CRS$ 3.1m Turki sh

MPP/General Cargo

Size Name Teu Built Yard M/E SS due Gear Price Buyers Comments

FEEDER NIENSTEDTEN 1,730 2002

SZCZECINSKA

PORTA HOLD,

Poland

Sulzer Jan-173 X 40t

CRANES$ 12.0m

U.S. based

(Seachange)

Containers

Name Loa(m) Cars Built Yard M/E SS due Price Buyers Comments

TAISHUN 144.42 1,450 1997NAIKAI ZOSEN -

SETODA, JapanB&W Jul-12 $ 9.5m Chinese

PCCs

© Intermodal Research 10/04/2012 5

Week

14

Week

13±% 2012 2011 2010

Bangladesh 485 485 0.0% 487 523 422

India 480 485 -1.0% 493 511 427

Pakistan 480 480 0.0% 491 504 425

China 435 435 0.0% 435 451 383

Bangladesh 465 455 0.0% 459 498 375

India 460 455 1.1% 466 484 394

Pakistan 455 450 1.1% 463 477 388

China 420 420 0.0% 418 432 364

Dry

Indicative Demolition Prices ($/ldt)

Markets

We

t

350

400

450

500

550

600

$/ldt

Dry Demolition Prices

Bangladesh India Pakistan China

350

400

450

500

550

600

$/ldt

Wet Demolition Prices

Bangladesh India Pakistan China

Things con�nue to be under pressure as overall demand from the Indian Sub-

con�nent s�ll lags behind the excessive supply of demo candidates in the

market. Things could soHen further as steel prices show liEle promise of

rapidly firming up over the next couple of days. Chinese breakers are s�ll

lagging behind, though recent bids have been looking fairly promising and

buyers have been taking a more compe��ve approach. Prices overall held

stable this week, with wet tonnages reaching levels of around 435-485$/ldt

and dry units falling to about 420-465$/ldt.

Most notable this week was the price paid by Indian breakers for the reefer

‘Akademik Vavilov’ (7,673dwt-5,996ldt-blt 85) which reportedly went for a

firm price of $ 510/Ldt.

Demoli&on Market

Name Size Ldt Built Yard Type $/ldt Breakers Comments

HYUNDAI OLYMPIA 186,330 21,742 1987HYUNDAI HEAVY

INDS - U, S. KoreaBULKER $ 452/Ldt undisclosed

bss 'as is' S. Korea incl 340T IFO &

52T MDO ROB

ALINA II 179,802 22,083 1986MITSUBISHI

NAGASAKI, JapanBULKER $ 490/Ldt Bangladeshi INCL 665TNS IFO +200TNS DO

AKARITA 107,223 17,081 1991TSUNEISHI SHBLDG -

FUK, JapanTANKER $ 496/Ldt Indian

CE-ULSAN 106,966 18,311 1990HYUNDAI HEAVY

INDS - U, S. KoreaTANKER $ 480/Ldt Bangladeshi

bss 'as is' Singapore incl 350T of

bunkers ROB

RANIA 68,405 9,919 1984SUMITOMO HI

OPPAMA, JapanBULKER $ 445/Ldt Chinese

ISLAND SINGAPURA 41,346 8,817 1985

CHINA

SHIPBUILDING KEE,

Chinese Taipei

BULKER $ 480/Ldt Indian

MSC HANNE 40,027 15,000 1989FINCANTIERI BREDA

VEN, ItalyCONT $ 493/Ldt Indian

STEEL ANDRONIKOS 37,415 9,667 1982IMABARI

MARUGAME, JapanBULKER $ 473/Ldt Bangladeshi

X-PRESS TOWER 14,090 4,830 1988SHIN KURUSHIMA

ONISHI, JapanCONT $ 490/Ldt Indian

STX BUSAN 12,573 3,826 1985KYOKUYO ZOSEN

CHOFU, JapanCONT $ 420/Ldt Chinese

AKADEMIK VAVILOV 7,673 5,996 1985AALBORG VAERFT,

DenmarkREEFER $ 510/Ldt Indian

SKY VENUS 5,813 - 1994 IMAI IWAGI, Japan GC $ 480/Ldt undisclosedbss 'as is' Colombo incl 450T

bunkers ROB

Demolition Sales

© Intermodal Research 10/04/2012 6

Week

14

Week

13±% 2012 2011 2010

Capesize 170k 46.5 46.5 0.0% 46 53 58

Panamax 75k 27.0 27.0 0.0% 27 33 35

Supramax 57k 25.5 25.5 0.0% 25 30 31

Handysize 30k 21.8 21.8 0.0% 22 25 27

VLCC 300k 96.5 96.5 0.0% 96 102 104

Suezmax 150k 58.5 58.5 0.0% 58 64 66

Aframax 110k 50.5 50.5 0.0% 51 54 55

LR1 70k 42.0 42.0 0.0% 42 45 46

MR 47k 33.0 33.0 0.0% 33 36 36

LPG M3 80k 71.0 71.0 0.0% 70 73 72

LPG M3 52k 62.0 62.0 0.0% 61 64 65

LPG M3 23k 45.0 45.0 0.0% 45 46 46

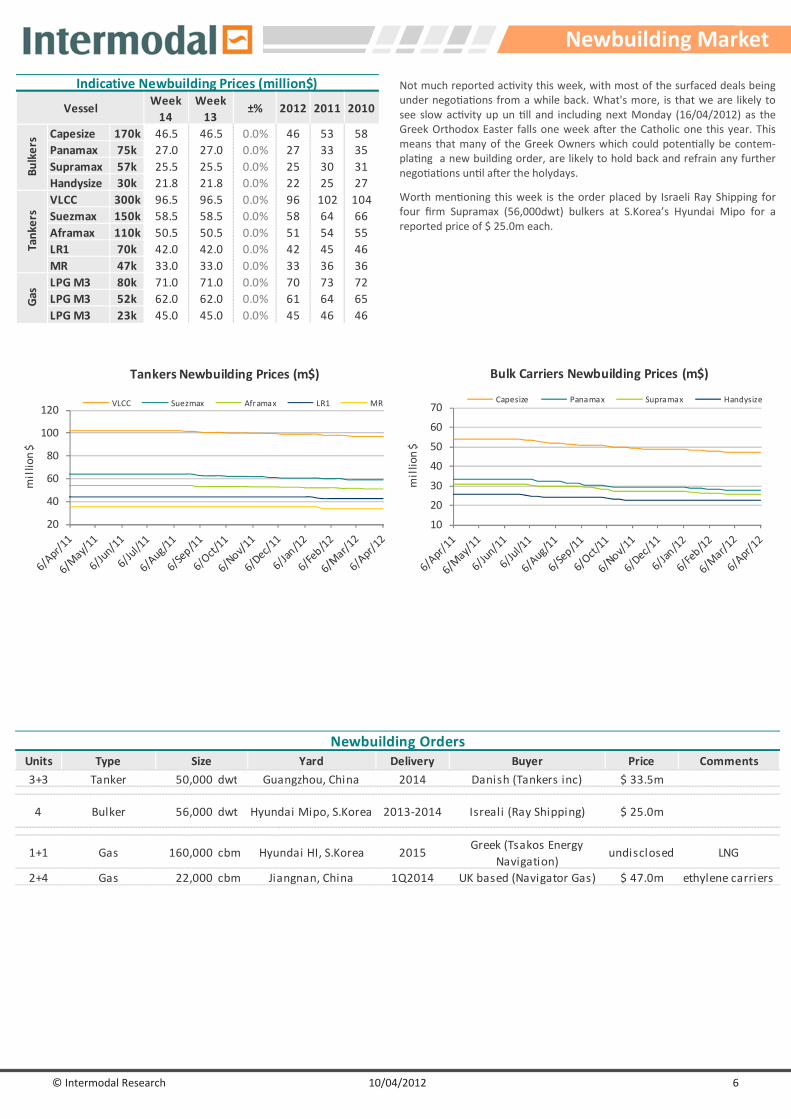

Indicative Newbuilding Prices (million$)

Ga

s

Vessel

Bu

lke

rsTa

nk

ers

Not much reported ac�vity this week, with most of the surfaced deals being

under nego�a�ons from a while back. What's more, is that we are likely to

see slow ac�vity up un �ll and including next Monday (16/04/2012) as the

Greek Orthodox Easter falls one week aHer the Catholic one this year. This

means that many of the Greek Owners which could poten�ally be contem-

pla�ng a new building order, are likely to hold back and refrain any further

nego�a�ons un�l aHer the holydays.

Worth men�oning this week is the order placed by Israeli Ray Shipping for

four firm Supramax (56,000dwt) bulkers at S.Korea’s Hyundai Mipo for a

reported price of $ 25.0m each.

10

20

30

40

50

60

70million $

Bulk Carriers Newbuilding Prices (m$)

Capesize Panamax Supramax Handysize

20

40

60

80

100

120

million $

Tankers Newbuilding Prices (m$)

VLCC Suezmax Aframax LR1 MR

Newbuilding Market

Units Type Yard Delivery Buyer Price Comments

3+3 Tanker 50,000 dwt Guangzhou, China 2014 Danish (Tankers inc) $ 33.5m

4 Bulker 56,000 dwt Hyundai Mipo, S.Korea 2013-2014 Isreali (Ray Shipping) $ 25.0m

1+1 Gas 160,000 cbm Hyundai HI, S.Korea 2015Greek (Tsakos Energy

Navigation)undisclosed LNG

2+4 Gas 22,000 cbm Jiangnan, China 1Q2014 UK based (Navigator Gas) $ 47.0m ethylene carriers

Size

Newbuilding Orders

The informa�on contained in this report has been obtained from various sources, as reported in the market. Intermodal Shipbrokers Co. believes such informa�on to be factual and reliable without mak-

ing guarantees regarding its accuracy or completeness. Whilst every care has been taken in the produc�on of the above review, no liability can be accepted for any loss or damage incurred in any way

whatsoever by any person who may seek to rely on the informa�on and views contained in this material. This report is being produced for the internal use of the intended recipients only and no re-

producing is allowed, without the prior wriEen authoriza�on of Intermodal Shipbrokers Co.

Compiled by Intermodal Research & Valua�ons Department | Mr George Lazaridis

E-mail: [email protected]

On behalf of Intermodal Sale & Purchase, Newbuilding and Chartering Departments

E-mail: [email protected], [email protected], [email protected]

1,600

1,620

1,640

1,660

1,680

1,700

90

100

110

120

130

140

goldoil

Basic Commodities Weekly Summary

Oil WTI $ Oil Brent $ Gold $

6-Apr-12 30-Mar-12W-O-W

Change %

Rotterdam 1,026.0 1,017.0 0.9%

Houston 1,038.0 1,052.5 -1.4%

Singapore 1,022.0 1,025.0 -0.3%

Rotterdam 714.5 710.0 0.6%

Houston 726.5 722.5 0.6%

Singapore 731.5 740.0 -1.1%

Rotterdam 735.5 737.5 -0.3%

Houston 766.5 752.5 1.9%

Singapore 743.0 752.0 -1.2%

Bunker Prices

MD

O3

80

cst

18

0cs

t

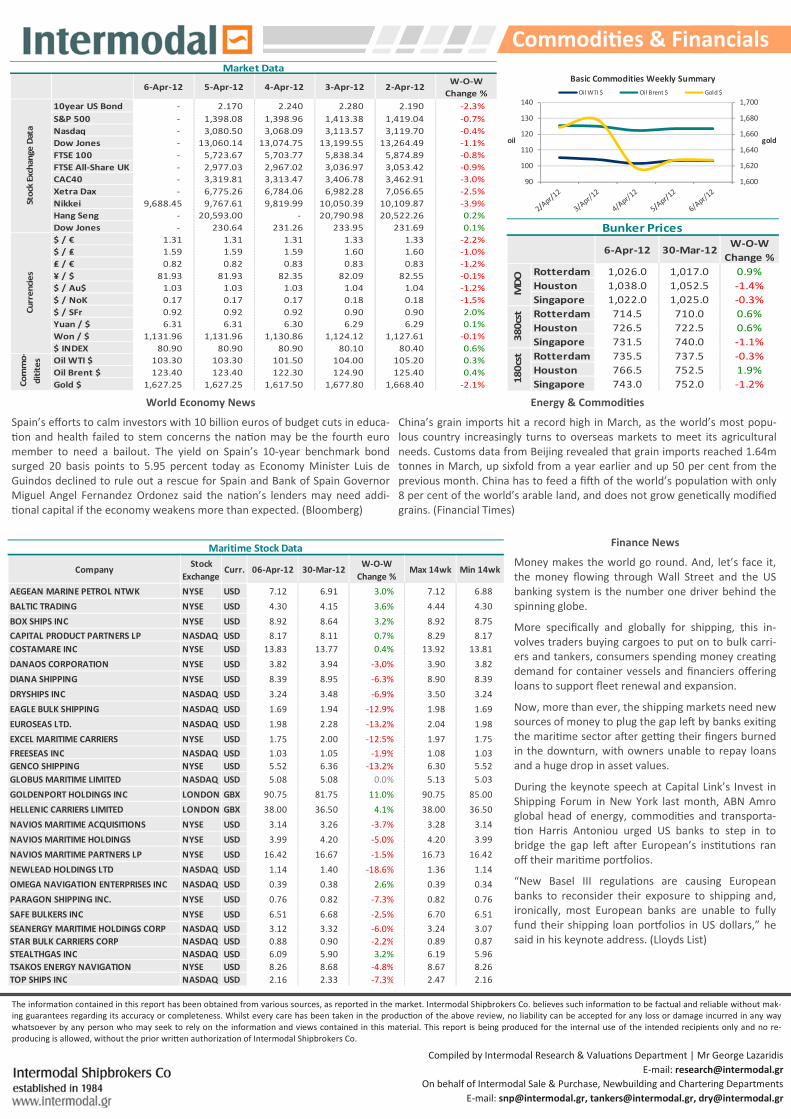

World Economy News

Spain’s efforts to calm investors with 10 billion euros of budget cuts in educa-

�on and health failed to stem concerns the na�on may be the fourth euro

member to need a bailout. The yield on Spain’s 10-year benchmark bond

surged 20 basis points to 5.95 percent today as Economy Minister Luis de

Guindos declined to rule out a rescue for Spain and Bank of Spain Governor

Miguel Angel Fernandez Ordonez said the na�on’s lenders may need addi-

�onal capital if the economy weakens more than expected. (Bloomberg)

Energy & Commodi&es

China’s grain imports hit a record high in March, as the world’s most popu-

lous country increasingly turns to overseas markets to meet its agricultural

needs. Customs data from Beijing revealed that grain imports reached 1.64m

tonnes in March, up sixfold from a year earlier and up 50 per cent from the

previous month. China has to feed a fiHh of the world’s popula�on with only

8 per cent of the world’s arable land, and does not grow gene�cally modified

grains. (Financial Times)

Finance News

Money makes the world go round. And, let’s face it,

the money flowing through Wall Street and the US

banking system is the number one driver behind the

spinning globe.

More specifically and globally for shipping, this in-

volves traders buying cargoes to put on to bulk carri-

ers and tankers, consumers spending money crea�ng

demand for container vessels and financiers offering

loans to support fleet renewal and expansion.

Now, more than ever, the shipping markets need new

sources of money to plug the gap leH by banks exi�ng

the mari�me sector aHer ge[ng their fingers burned

in the downturn, with owners unable to repay loans

and a huge drop in asset values.

During the keynote speech at Capital Link’s Invest in

Shipping Forum in New York last month, ABN Amro

global head of energy, commodi�es and transporta-

�on Harris Antoniou urged US banks to step in to

bridge the gap leH aHer European’s ins�tu�ons ran

off their mari�me porRolios.

“New Basel III regula�ons are causing European

banks to reconsider their exposure to shipping and,

ironically, most European banks are unable to fully

fund their shipping loan porRolios in US dollars,” he

said in his keynote address. (Lloyds List)

CompanyStock

ExchangeCurr. 06-Apr-12 30-Mar-12

W-O-W

Change %Max 14wk Min 14wk

AEGEAN MARINE PETROL NTWK NYSE USD 7.12 6.91 3.0% 7.12 6.88

BALTIC TRADING NYSE USD 4.30 4.15 3.6% 4.44 4.30

BOX SHIPS INC NYSE USD 8.92 8.64 3.2% 8.92 8.75

CAPITAL PRODUCT PARTNERS LP NASDAQ USD 8.17 8.11 0.7% 8.29 8.17

COSTAMARE INC NYSE USD 13.83 13.77 0.4% 13.92 13.81

DANAOS CORPORATION NYSE USD 3.82 3.94 -3.0% 3.90 3.82

DIANA SHIPPING NYSE USD 8.39 8.95 -6.3% 8.90 8.39

DRYSHIPS INC NASDAQ USD 3.24 3.48 -6.9% 3.50 3.24

EAGLE BULK SHIPPING NASDAQ USD 1.69 1.94 -12.9% 1.98 1.69

EUROSEAS LTD. NASDAQ USD 1.98 2.28 -13.2% 2.04 1.98

EXCEL MARITIME CARRIERS NYSE USD 1.75 2.00 -12.5% 1.97 1.75

FREESEAS INC NASDAQ USD 1.03 1.05 -1.9% 1.08 1.03

GENCO SHIPPING NYSE USD 5.52 6.36 -13.2% 6.30 5.52

GLOBUS MARITIME LIMITED NASDAQ USD 5.08 5.08 0.0% 5.13 5.03

GOLDENPORT HOLDINGS INC LONDON GBX 90.75 81.75 11.0% 90.75 85.00

HELLENIC CARRIERS LIMITED LONDON GBX 38.00 36.50 4.1% 38.00 36.50

NAVIOS MARITIME ACQUISITIONS NYSE USD 3.14 3.26 -3.7% 3.28 3.14

NAVIOS MARITIME HOLDINGS NYSE USD 3.99 4.20 -5.0% 4.20 3.99

NAVIOS MARITIME PARTNERS LP NYSE USD 16.42 16.67 -1.5% 16.73 16.42

NEWLEAD HOLDINGS LTD NASDAQ USD 1.14 1.40 -18.6% 1.36 1.14

OMEGA NAVIGATION ENTERPRISES INC NASDAQ USD 0.39 0.38 2.6% 0.39 0.34

PARAGON SHIPPING INC. NYSE USD 0.76 0.82 -7.3% 0.82 0.76

SAFE BULKERS INC NYSE USD 6.51 6.68 -2.5% 6.70 6.51

SEANERGY MARITIME HOLDINGS CORP NASDAQ USD 3.12 3.32 -6.0% 3.24 3.07

STAR BULK CARRIERS CORP NASDAQ USD 0.88 0.90 -2.2% 0.89 0.87

STEALTHGAS INC NASDAQ USD 6.09 5.90 3.2% 6.19 5.96

TSAKOS ENERGY NAVIGATION NYSE USD 8.26 8.68 -4.8% 8.67 8.26

TOP SHIPS INC NASDAQ USD 2.16 2.33 -7.3% 2.47 2.16

Maritime Stock Data

6-Apr-12 5-Apr-12 4-Apr-12 3-Apr-12 2-Apr-12W-O-W

Change %

10year US Bond - 2.170 2.240 2.280 2.190 -2.3%

S&P 500 - 1,398.08 1,398.96 1,413.38 1,419.04 -0.7%

Nasdaq - 3,080.50 3,068.09 3,113.57 3,119.70 -0.4%

Dow Jones - 13,060.14 13,074.75 13,199.55 13,264.49 -1.1%

FTSE 100 - 5,723.67 5,703.77 5,838.34 5,874.89 -0.8%

FTSE All-Share UK - 2,977.03 2,967.02 3,036.97 3,053.42 -0.9%

CAC40 - 3,319.81 3,313.47 3,406.78 3,462.91 -3.0%

Xetra Dax - 6,775.26 6,784.06 6,982.28 7,056.65 -2.5%

Nikkei 9,688.45 9,767.61 9,819.99 10,050.39 10,109.87 -3.9%

Hang Seng - 20,593.00 - 20,790.98 20,522.26 0.2%

Dow Jones - 230.64 231.26 233.95 231.69 0.1%

$ / € 1.31 1.31 1.31 1.33 1.33 -2.2%

$ / ₤ 1.59 1.59 1.59 1.60 1.60 -1.0%

₤ / € 0.82 0.82 0.83 0.83 0.83 -1.2%

¥ / $ 81.93 81.93 82.35 82.09 82.55 -0.1%

$ / Au$ 1.03 1.03 1.03 1.04 1.04 -1.2%

$ / NoK 0.17 0.17 0.17 0.18 0.18 -1.5%

$ / SFr 0.92 0.92 0.92 0.90 0.90 2.0%

Yuan / $ 6.31 6.31 6.30 6.29 6.29 0.1%

Won / $ 1,131.96 1,131.96 1,130.86 1,124.12 1,127.61 -0.1%

$ INDEX 80.90 80.90 80.90 80.10 80.40 0.6%

Oil WTI $ 103.30 103.30 101.50 104.00 105.20 0.3%

Oil Brent $ 123.40 123.40 122.30 124.90 125.40 0.4%

Gold $ 1,627.25 1,627.25 1,617.50 1,677.80 1,668.40 -2.1%

Market Data

Cu

rre

nci

es

Co

mm

o-

dit

ite

sSt

ock

Exch

an

ge

Dat

a

Commodi&es & Financials