welcome to bg brasil - thaiembassybrazil.comthaiembassybrazil.com/pdf/bgbrasil.pdf · the following...

TRANSCRIPT

Welcome to BG Brasil 27 June 2012

Nelson Silva – President, BG Brasil

Legal notice

The following presentation contains forward-looking statements concerning BG Group plc‟s strategy, operations, financial performance or condition, outlook, growth opportunities or circumstances in the countries, sectors or markets in which BG Group plc operates. By their nature, forward-looking statements involve uncertainty because they depend on future circumstances, and relate to events, not all of which can be controlled or predicted. Although the Company believes that the expectations reflected in such forward-looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct. Actual results could differ materially from the guidance given in this presentation for a number of reasons. For a detailed analysis of the factors that may affect our business, financial performance or results of operations, we urge you to look at the “Principal risks and uncertainties” included in the BG Group plc Annual Report & Accounts 2011. Nothing in this presentation should be construed as a profit forecast and no part of this presentation constitutes, or shall be taken to constitute, an invitation or inducement to invest in BG Group plc or any other entity, and must not be relied upon in any way in connection with any investment decision. BG Group plc undertakes no obligation to update any forward-looking statements.

No representation or warranty, express or implied, is or will be made in relation to the accuracy or completeness of the information in this presentation and no responsibility or liability is or will be accepted by BG Group plc or any of its respective subsidiaries, affiliates and associated companies (or by any of their respective officers, employees or agents) in relation to it.

2

Overview

• Market leader

– Listed on London Stock Exchange

– FTSE top 10 company

– Market capitalisation: approx.

$66 billion (June 2012)

• Gas and oil

– Production approximately 70% gas;

30% oil and liquids

• International energy major

– Over 6,000 employees; 65%

outside UK

The integrated gas major

BG Group

3

Business model

Exploration, Production and Marketing

BG Group

Markets Enabling Resources

Integrated Energy Business

4

Countries of current operation

Active in more than 24 countries around the world

BG Group countries

Trinidad &

Tobago Egypt

Kazakhstan

UK

India

Uruguay

Bolivia Brazil

USA

Italy

Tunisia Thailand

Singapore

Areas of PA

Norway

Nigeria

China

Madagascar

Algeria

Chile

Australia Tanzania Kenya

BG Group

5

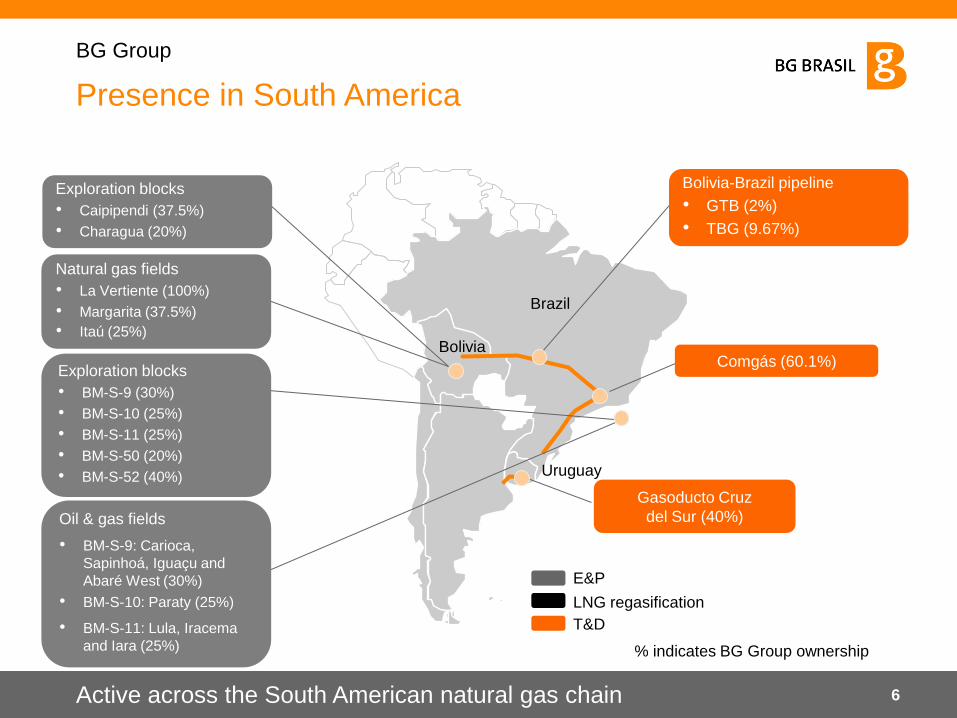

E&P

Gasoducto Cruz

del Sur (40%)

Bolivia-Brazil pipeline

• GTB (2%)

• TBG (9.67%)

Exploration blocks

• Caipipendi (37.5%)

• Charagua (20%)

Exploration blocks

• BM-S-9 (30%)

• BM-S-10 (25%)

• BM-S-11 (25%)

• BM-S-50 (20%)

• BM-S-52 (40%)

Natural gas fields

• La Vertiente (100%)

• Margarita (37.5%)

• Itaú (25%)

Brazil

Bolivia

Uruguay

T&D

LNG regasification

% indicates BG Group ownership

Presence in South America

Active across the South American natural gas chain

BG Group

6

Oil & gas fields

• BM-S-9: Carioca,

Sapinhoá, Iguaçu and

Abaré West (30%)

• BM-S-10: Paraty (25%)

• BM-S-11: Lula, Iracema

and Iara (25%)

Comgás (60.1%)

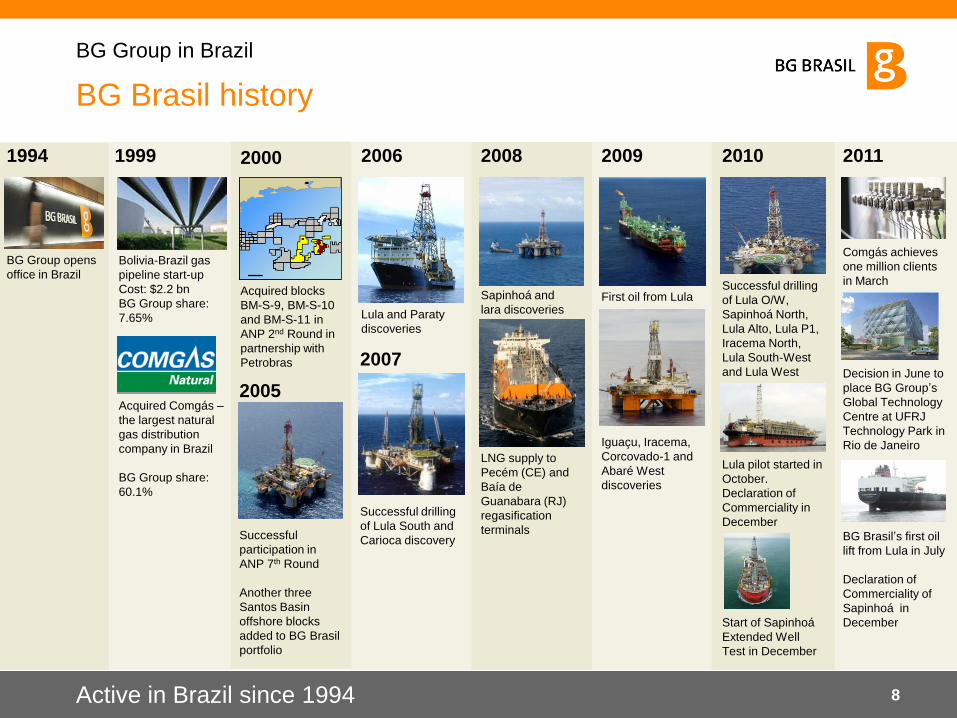

BG Group in Brazil

BG Brasil history

1994

BG Group opens

office in Brazil

2005

2007

2011

1999

2006

Lula and Paraty

discoveries

2005

Successful

participation in

ANP 7th Round

Another three

Santos Basin

offshore blocks

added to BG Brasil

portfolio

2007

Successful drilling

of Lula South and

Carioca discovery

2008

Sapinhoá and

lara discoveries

LNG supply to

Pecém (CE) and

Baía de

Guanabara (RJ)

regasification

terminals

2000

Acquired blocks

BM-S-9, BM-S-10

and BM-S-11 in

ANP 2nd Round in

partnership with

Petrobras

2009

First oil from Lula

Iguaçu, Iracema,

Corcovado-1 and

Abaré West

discoveries

2010

Successful drilling

of Lula O/W,

Sapinhoá North,

Lula Alto, Lula P1,

Iracema North,

Lula South-West

and Lula West

Lula pilot started in

October.

Declaration of

Commerciality in

December

Start of Sapinhoá

Extended Well

Test in December

2011

Comgás achieves

one million clients

in March

Decision in June to

place BG Group‟s

Global Technology

Centre at UFRJ

Technology Park in

Rio de Janeiro

BG Brasil‟s first oil

lift from Lula in July

Declaration of

Commerciality of

Sapinhoá in

December

Bolivia-Brazil gas

pipeline start-up

Cost: $2.2 bn

BG Group share:

7.65%

Acquired Comgás –

the largest natural

gas distribution

company in Brazil

BG Group share:

60.1%

Active in Brazil since 1994

BG Group in Brazil

8

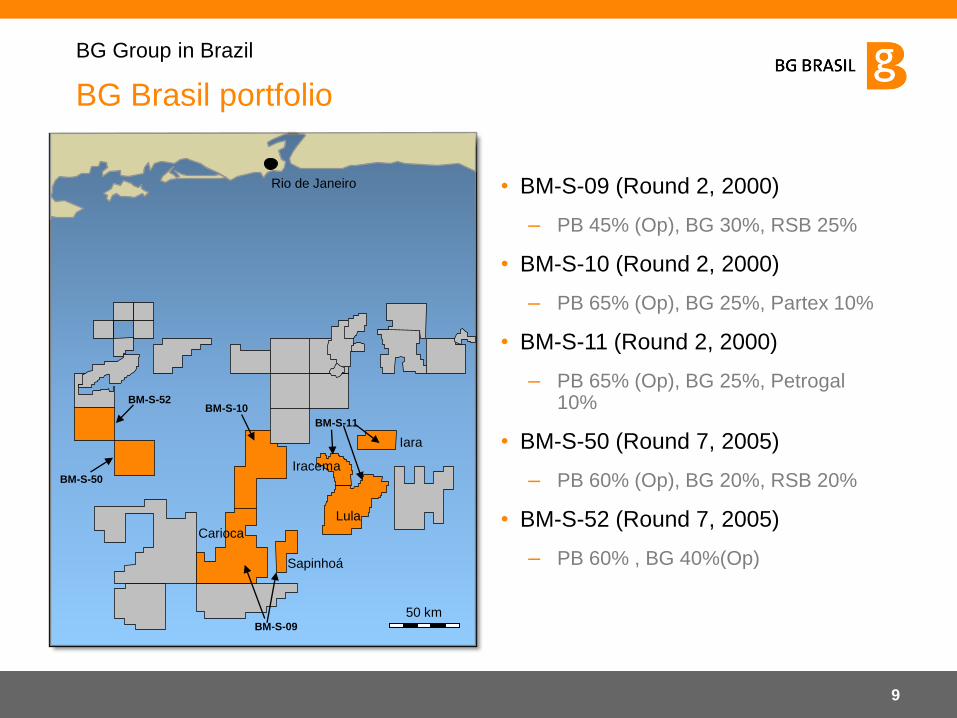

BG Brasil portfolio

• BM-S-09 (Round 2, 2000)

– PB 45% (Op), BG 30%, RSB 25%

• BM-S-10 (Round 2, 2000)

– PB 65% (Op), BG 25%, Partex 10%

• BM-S-11 (Round 2, 2000)

– PB 65% (Op), BG 25%, Petrogal 10%

• BM-S-50 (Round 7, 2005)

– PB 60% (Op), BG 20%, RSB 20%

• BM-S-52 (Round 7, 2005)

– PB 60% , BG 40%(Op)

Carioca

Iara

Sapinhoá

Rio de Janeiro

50 km

Lula

Iracema

BM-S-52

BM-S-50

BM-S-10

BM-S-09

BM-S-11

BG Group in Brazil

9

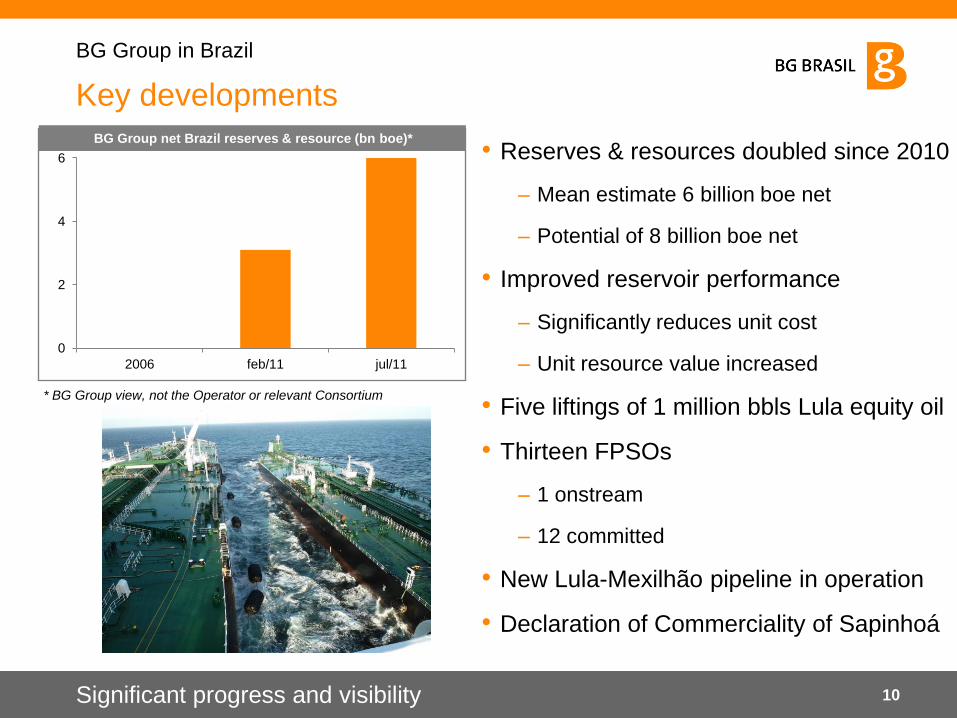

Significant progress and visibility

• Reserves & resources doubled since 2010

– Mean estimate 6 billion boe net

– Potential of 8 billion boe net

• Improved reservoir performance

– Significantly reduces unit cost

– Unit resource value increased

• Five liftings of 1 million bbls Lula equity oil

• Thirteen FPSOs

– 1 onstream

– 12 committed

• New Lula-Mexilhão pipeline in operation

• Declaration of Commerciality of Sapinhoá

0

2

4

6

2006 feb/11 jul/11

BG Group net Brazil reserves & resource (bn boe)*

Key developments

BG Group in Brazil

10

* BG Group view, not the Operator or relevant Consortium

FPSO progress

• FPSO 1

– 5 connected wells (4 producers / 1 CO2

disposal well)

• FPSO build progress

– FPSO 2 – over 88%

– FPSO 3 – over 79%

– FPSOs 4 and 5 on schedule (c. 20%)

• FPSO 3 en route to Brazil

• 8 domestic FPSOs

– Hull fabrication continues in the Rio Grande

de Sul shipyard in Brazil

FPSO Cidade de Angra dos Reis

Santos Basin, Brazil *BG Group view, not the Operator or Consortium

BG Group in Brazil

11

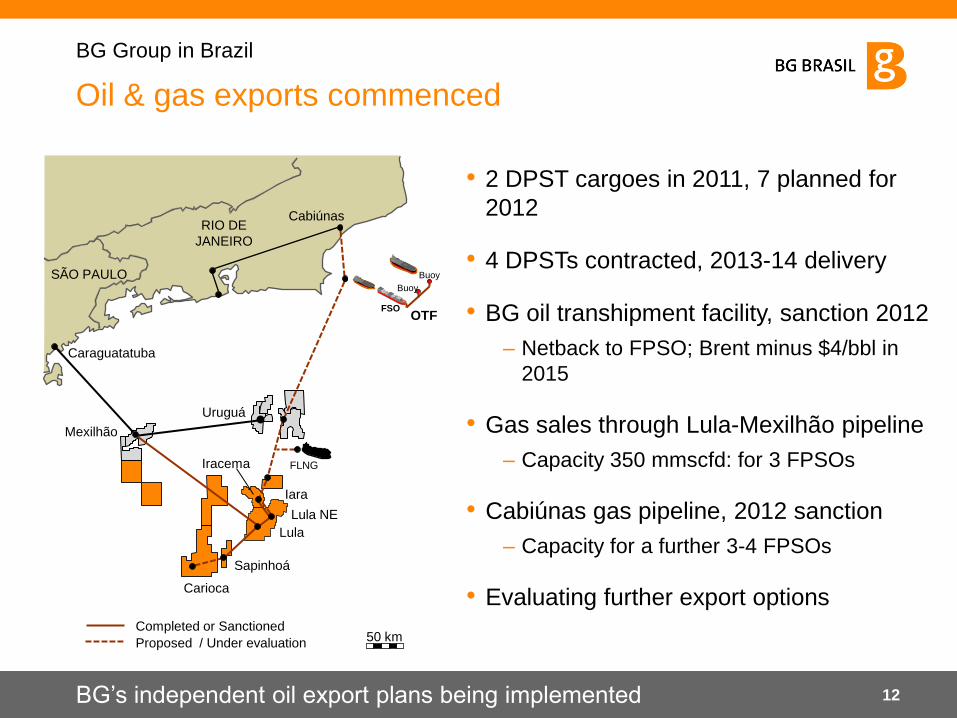

Oil & gas exports commenced

• 2 DPST cargoes in 2011, 7 planned for

2012

• 4 DPSTs contracted, 2013-14 delivery

• BG oil transhipment facility, sanction 2012

– Netback to FPSO; Brent minus $4/bbl in

2015

• Gas sales through Lula-Mexilhão pipeline

– Capacity 350 mmscfd: for 3 FPSOs

• Cabiúnas gas pipeline, 2012 sanction

– Capacity for a further 3-4 FPSOs

• Evaluating further export options

Completed or Sanctioned

Proposed / Under evaluation 50 km

Caraguatatuba

RIO DE

JANEIRO

Sapinhoá

Carioca

Mexilhão

Lula

Iracema

Iara

Lula NE

FLNG

Uruguá

SÃO PAULO

Cabiúnas

Buoy

Buoy

FSO OTF

BG‟s independent oil export plans being implemented

BG Group in Brazil

12

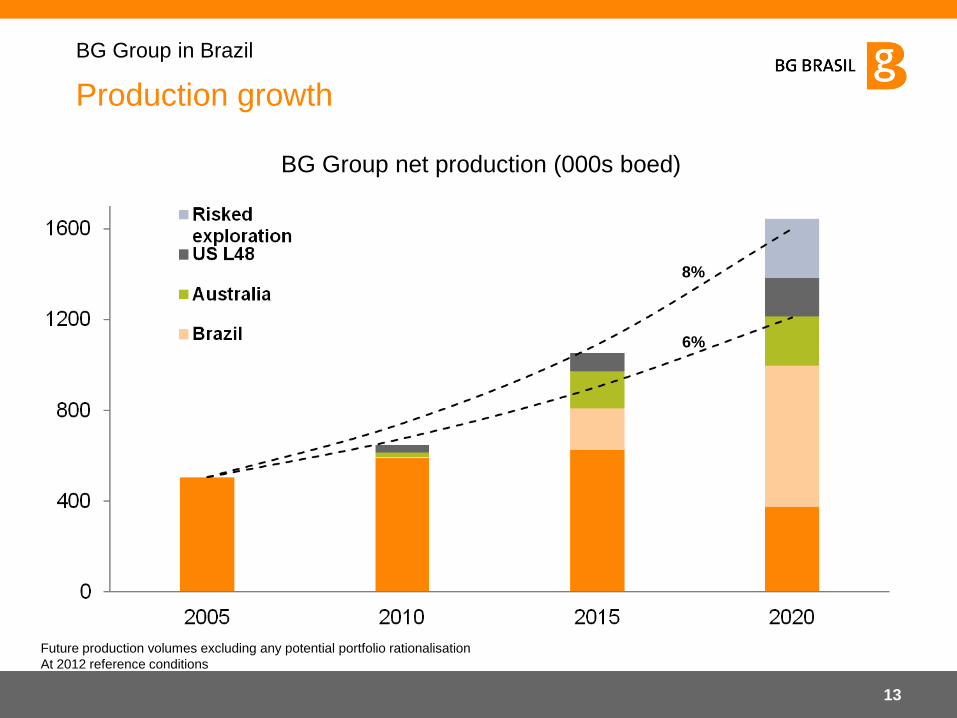

BG Group net production (000s boed)

8%

6%

Future production volumes excluding any potential portfolio rationalisation

At 2012 reference conditions

BG Group in Brazil

Production growth

13

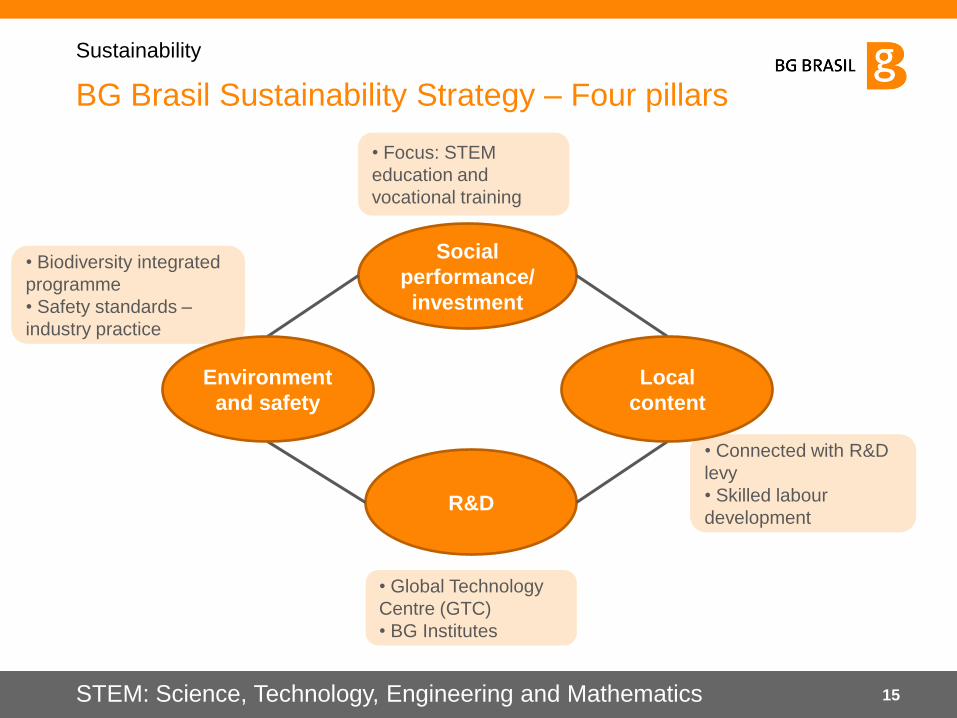

Sustainability

Social

performance/

investment

R&D

BG Brasil Sustainability Strategy – Four pillars

Sustainability

STEM: Science, Technology, Engineering and Mathematics

• Global Technology

Centre (GTC)

• BG Institutes

• Connected with R&D

levy

• Skilled labour

development

• Focus: STEM

education and

vocational training

• Biodiversity integrated

programme

• Safety standards –

industry practice

Environment

and safety

Local

content

15

BG Global Technology Centre

Sustainability

• Technology “head-office” to be based in

Rio Technology Park

• Other O&G companies have research

centres in Brazil (GE, Halliburton,

Schlumberger, Technip, Baker Hughes)

• Create specialised BG Group Institutes

– Partnership between BG Group and

Brazilian universities

– BG Group may fund infrastructure,

equipment and research staff salaries

• Federal Government partnership –

„Science without borders‟

16

Comgás

18

• BG Group and Shell

are controlling

shareholders

• Largest natural gas

distributor in Brazil

• 30% of total natural

gas sales nationwide

• 5,000 people hired

directly and indirectly

• Natural gas sales of

13.2 mmcmd in 2011

Overview

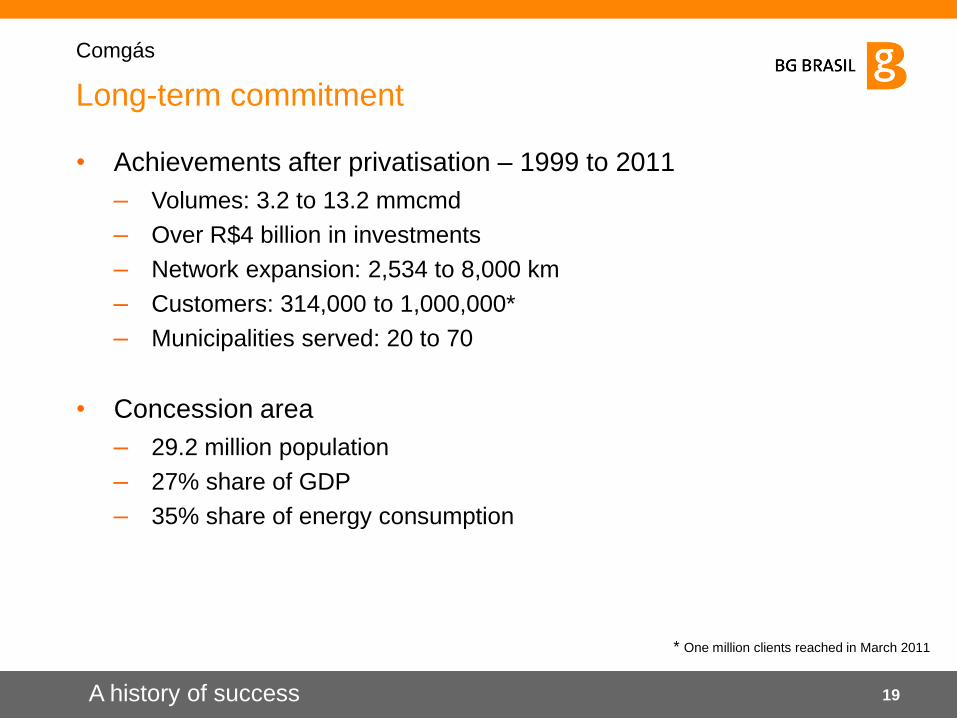

Comgás

Long-term commitment

• Achievements after privatisation – 1999 to 2011

– Volumes: 3.2 to 13.2 mmcmd

– Over R$4 billion in investments

– Network expansion: 2,534 to 8,000 km

– Customers: 314,000 to 1,000,000*

– Municipalities served: 20 to 70

• Concession area

– 29.2 million population

– 27% share of GDP

– 35% share of energy consumption

A history of success

Comgás

* One million clients reached in March 2011

19

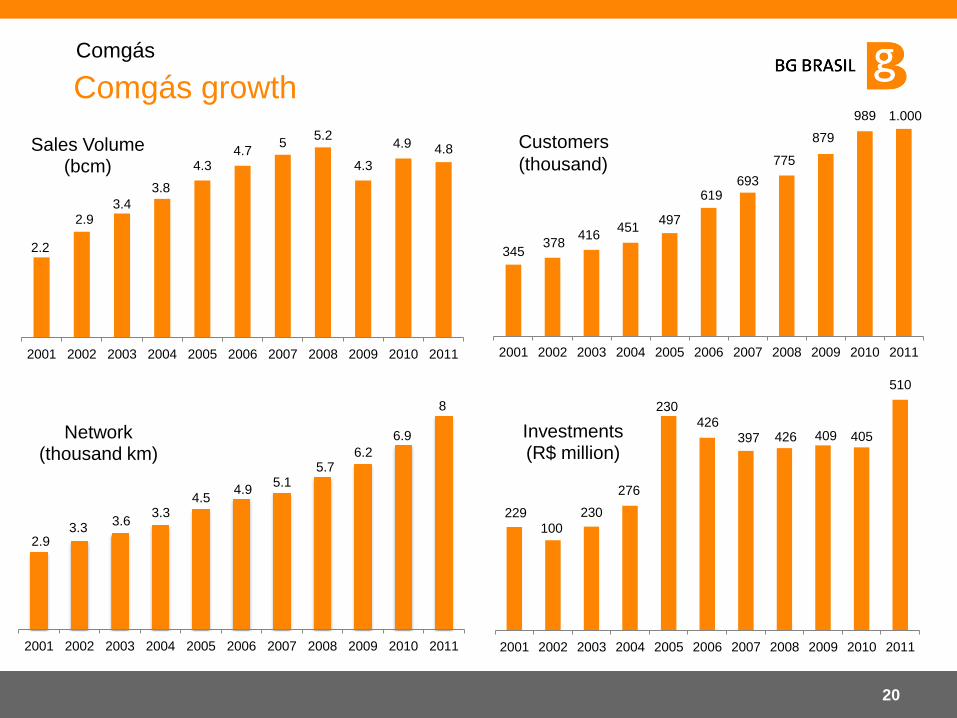

Comgás growth

Comgás

2.9 3.3

3.6 3.3

4.5 4.9

5.1 5.7

6.2

6.9

8

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Network (thousand km)

229 100

230

276

230

426 397 426 409 405

510

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Investments (R$ million)

345 378

416 451

497

619 693

775

879

989 1.000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Customers

(thousand)

2.2

2.9 3.4

3.8

4.3 4.7

5 5.2

4.3

4.9 4.8

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Sales Volume (bcm)

20

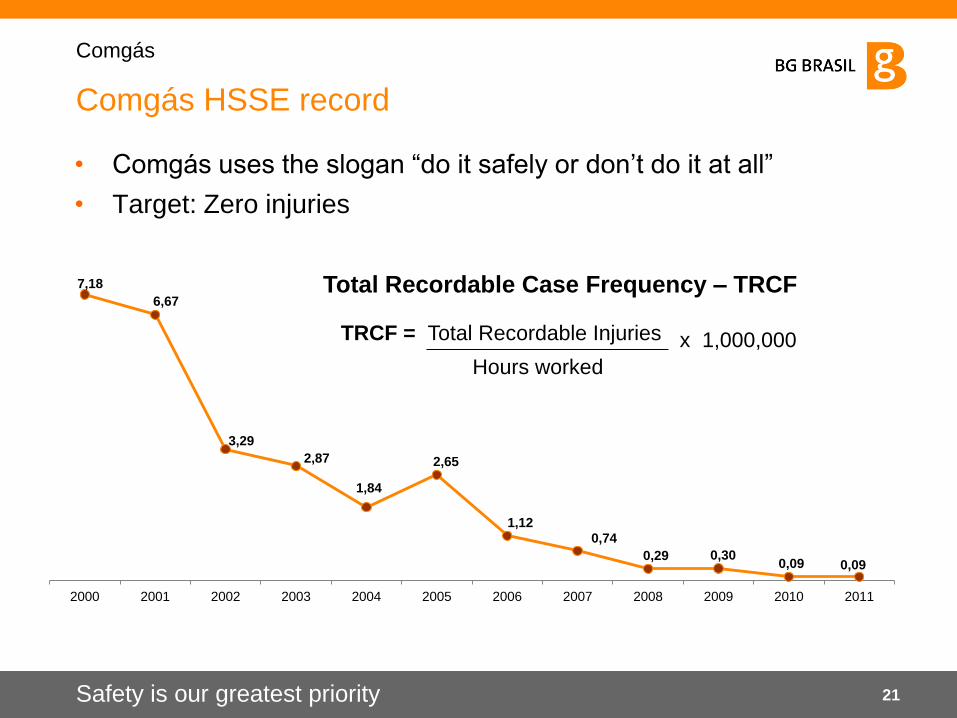

Comgás HSSE record

Comgás

Safety is our greatest priority

• Comgás uses the slogan “do it safely or don‟t do it at all”

• Target: Zero injuries

Total Recordable Case Frequency – TRCF

TRCF = Total Recordable Injuries

x 1,000,000

Hours worked

21

7,18

6,67

3,29

2,87

1,84

2,65

1,12 0,74

0,29 0,30 0,09 0,09

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011