welcome to the new world - world trade organization · welcome to the new world 21 february 2008...

TRANSCRIPT

©2008 Tata Communications, Ltd. All Rights Reserved.

CORPORATE

Confidential & Proprietary

Welcome tothe New World

21 FEBRUARY 2008

Srinivasa AddepalliSr. Vice President, Corporate Strategy

1

Confidential & Proprietary

CONTENTS The New World

A New World of Communications

The Tata Communications Journey

2CORPORATEConfidential & Proprietary

Our Market Environment

Globalization Web 2.0 India & China

3CORPORATEConfidential & Proprietary

Globalization & Increased Role of Developing Countries

Source: World Bank

Exports from Developing and Developed Countries, 2005-2030 (US$2001 Trillions)

0

5

10

15

20

25

30

1980 2005 2030

High incomecountries

Developingcountries45%

32%22%

$27Tn

4CORPORATEConfidential & Proprietary

Growing Importance of India & China in the New World

Source: Morgan Stanley; Tata Communications Research

India

27%

Africa

24%China

16%

SE Asia

12%

LatAm

11%

W Asia

6%

USA

4%Europe

0%

Japan

0%

64

82

149

210

390

395

497

762

978

Africa

Japan

W Asia

USA

LatAm

SE Asia

Europe

India

China

Working Population 2010, millions Addition to Working Pops 2005-2010

5CORPORATEConfidential & Proprietary

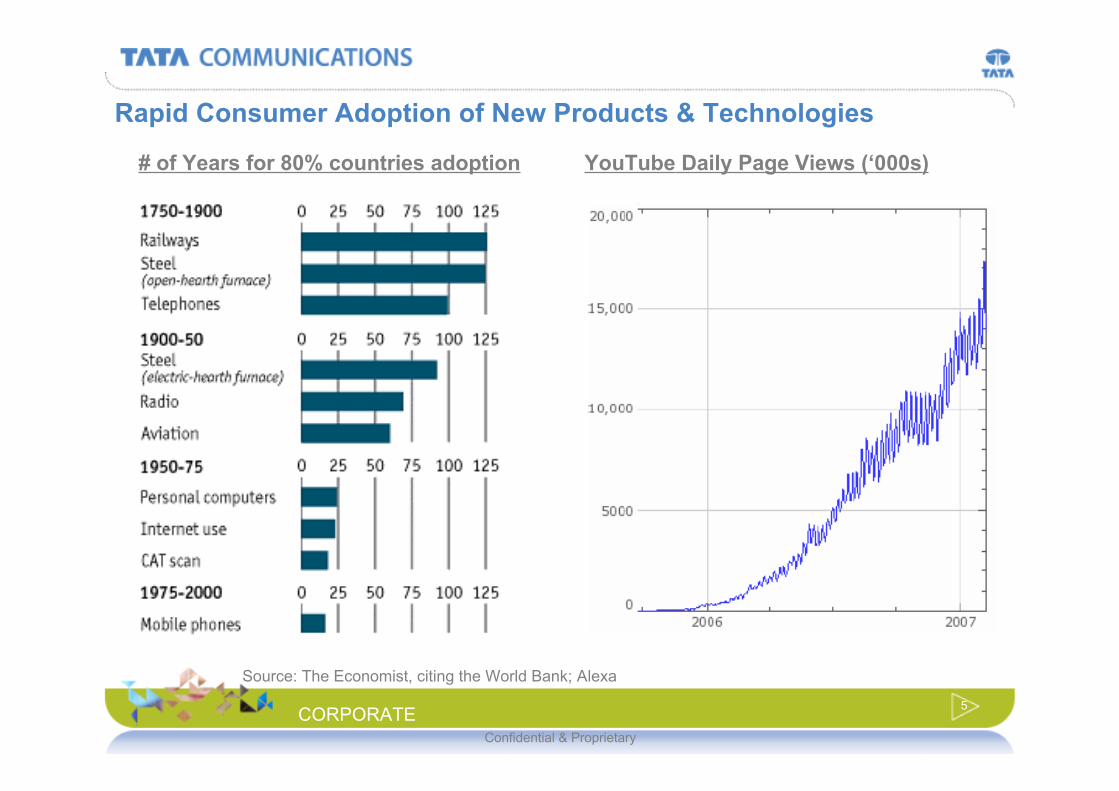

Rapid Consumer Adoption of New Products & Technologies

Source: The Economist, citing the World Bank; Alexa

# of Years for 80% countries adoption YouTube Daily Page Views (‘000s)

6

Confidential & Proprietary

CONTENTS The New World

A New World of Communications

The Tata Communications Journey

7CORPORATEConfidential & Proprietary

Enterprises Demand Managed & Converged Services

Source: Ovum

New Sourcing Plans / Strategies being considered by CIOs

8CORPORATEConfidential & Proprietary

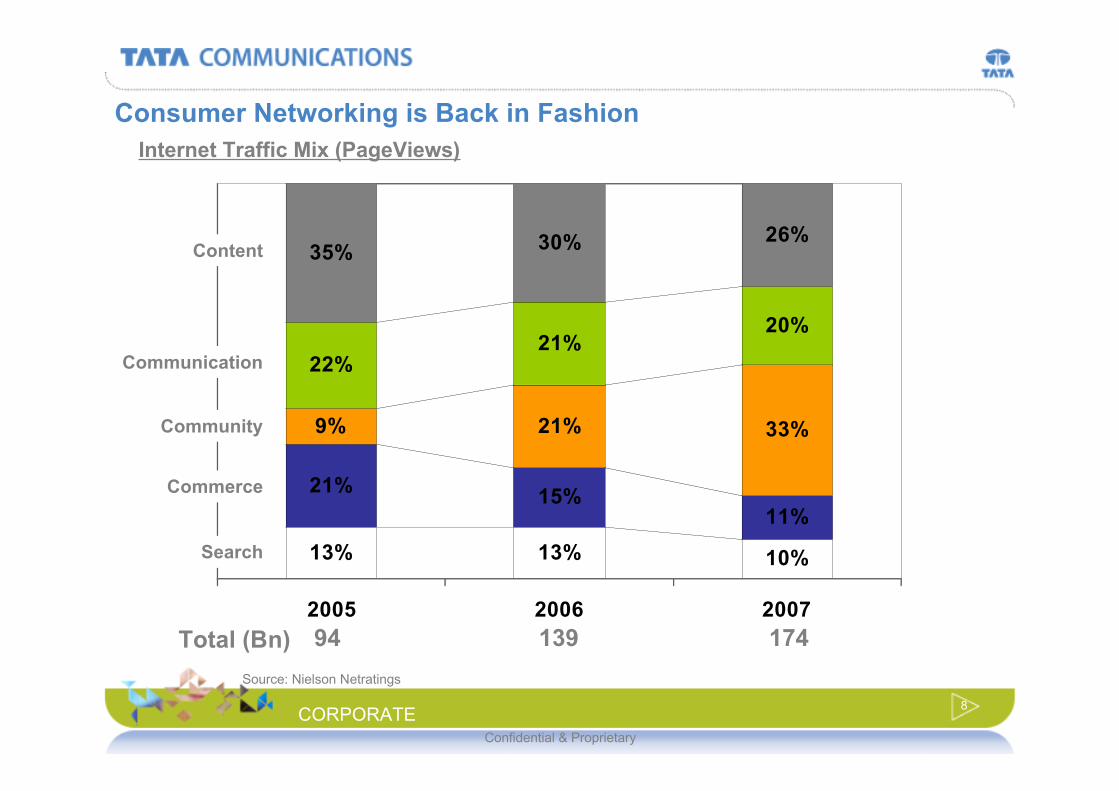

Consumer Networking is Back in Fashion

13% 13% 10%

21%15%

11%

9% 21% 33%

22%

21%20%

35%30% 26%

2005 2006 2007

Internet Traffic Mix (PageViews)

Total (Bn) 94 139 174Source: Nielson Netratings

Content

Communication

Community

Commerce

Search

9CORPORATEConfidential & Proprietary

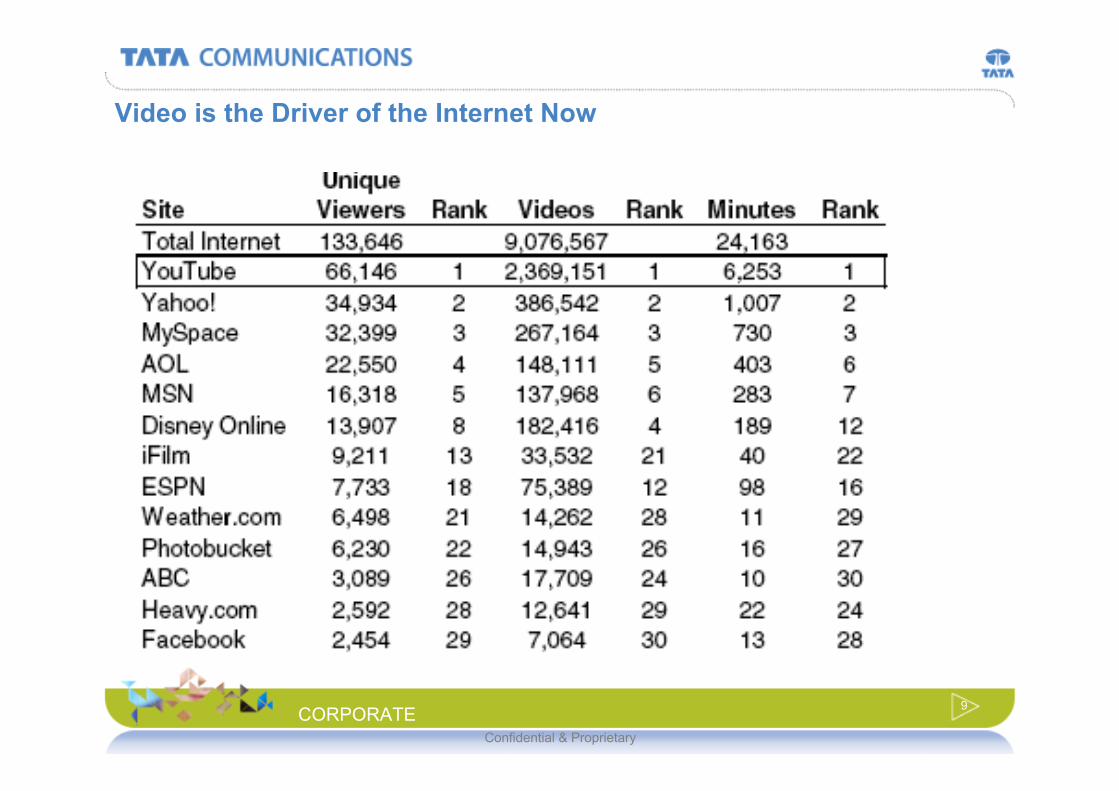

Video is the Driver of the Internet Now

10CORPORATEConfidential & Proprietary

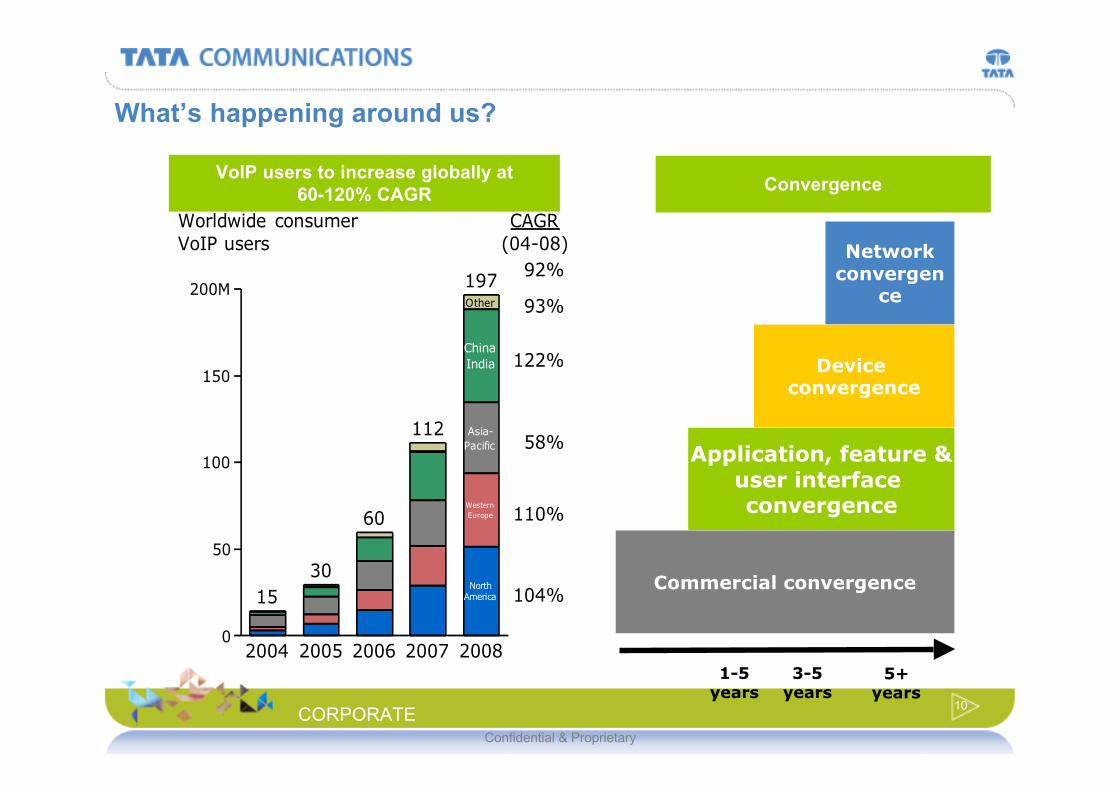

What’s happening around us?

0

50

100

150

200M

2004

15

2005

30

2006

60

2007

112

2008

Other

China

India

Asia-

Pacific

Western

Europe

NorthAmerica

197

Worldwide consumer

VoIP users

93%

104%

110%

58%

122%

(04-08)

92%

CAGR

VoIP users to increase globally at60-120% CAGR

Commercial convergence

Application, feature &user interface convergence

Device convergence

Networkconvergen

ce

1-5years

3-5years

5+years

Convergence

11

Confidential & Proprietary

CONTENTS The New World

A New World of Communications

The Tata Communications Journey

12CORPORATEConfidential & Proprietary

Reach

Monopoly ILD VoiceILD (89%); Others (11%)

Voice, Data, IP, Mobility,Outsourcing, Broadband

VSNL (2002) Tata Communications (2008)

Carriers; Retail (Dial-up)Carriers, Large & Mid-sizedEnterprises, MobileOperators, Consumers

India-Centric Play;negligible globaloperations

Global Infrastructure, GlobalCustomers

Revenues: $1.6 bnMarket Cap: $1.2 bn

Revenues: $2 bnMarket Cap: $5 bn (Current)

# March 31st of the year (FY02 and FY07)

Transformation to a Global Challenger

Customers

Lines OfBusiness

Financials#

13CORPORATEConfidential & Proprietary

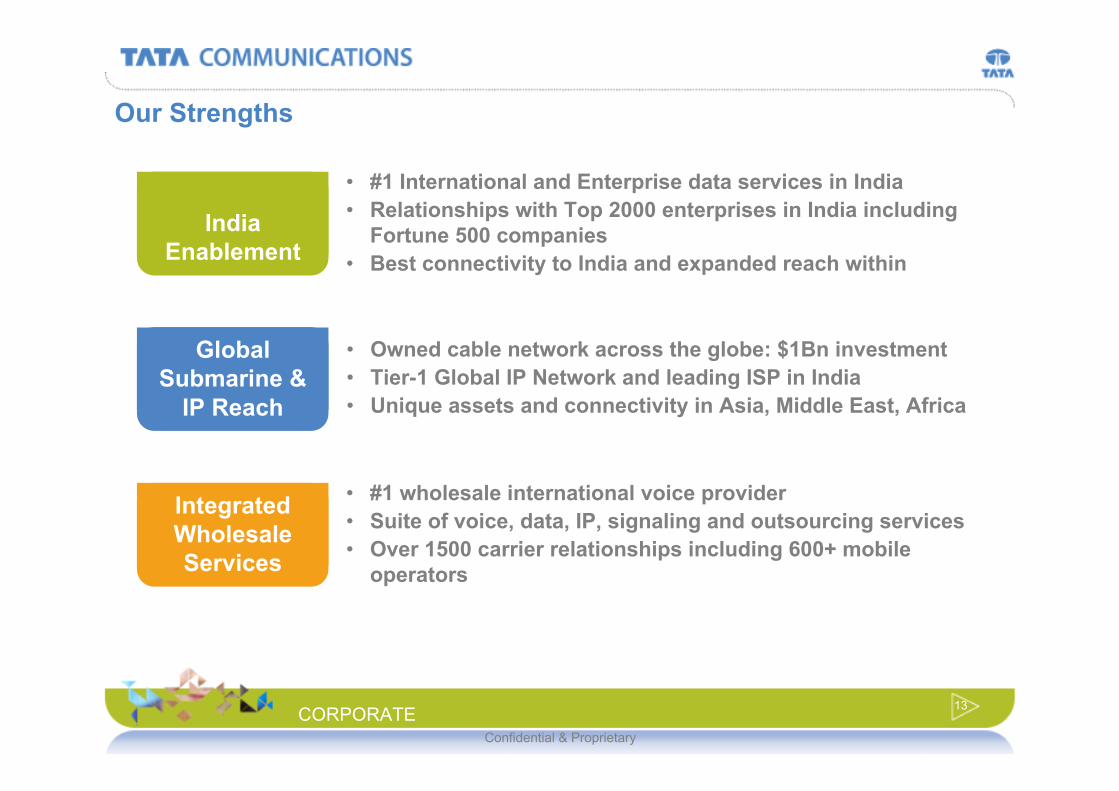

Our Strengths

IndiaEnablement

GlobalSubmarine &

IP Reach

IntegratedWholesaleServices

• #1 International and Enterprise data services in India• Relationships with Top 2000 enterprises in India including

Fortune 500 companies• Best connectivity to India and expanded reach within

• Owned cable network across the globe: $1Bn investment• Tier-1 Global IP Network and leading ISP in India• Unique assets and connectivity in Asia, Middle East, Africa

• #1 wholesale international voice provider• Suite of voice, data, IP, signaling and outsourcing services• Over 1500 carrier relationships including 600+ mobile

operators

14CORPORATEConfidential & Proprietary

Our Vision

Emerging Markets

Converged IPSolutions

ManagedServices

INDIA, ASIA incl CHINA, SOUTH AFRICA

NEW WORLD OFCOMMUNICATIONS

Deliver a new world of communications to advancethe reach and leadership of our customers

15CORPORATEConfidential & Proprietary

Major Investments: CablesO

WN

CA

PAC

ITY

Existing Cables New / Planned

• TGN-Atlantic

• TGN-Pacific

• TGN-Western Europe

• TGN-Northern Europe

• TGN-India Asia

• SMW-3

• SMW-4

• SAFE/SAT-3

• others…

• TGN-Intra Asia S’pore-HK-Japan H2 2008

• TGN-Eurasia India-Europe H2 2009

• IMEWE

• SEACOM

• Africa

16CORPORATEConfidential & Proprietary

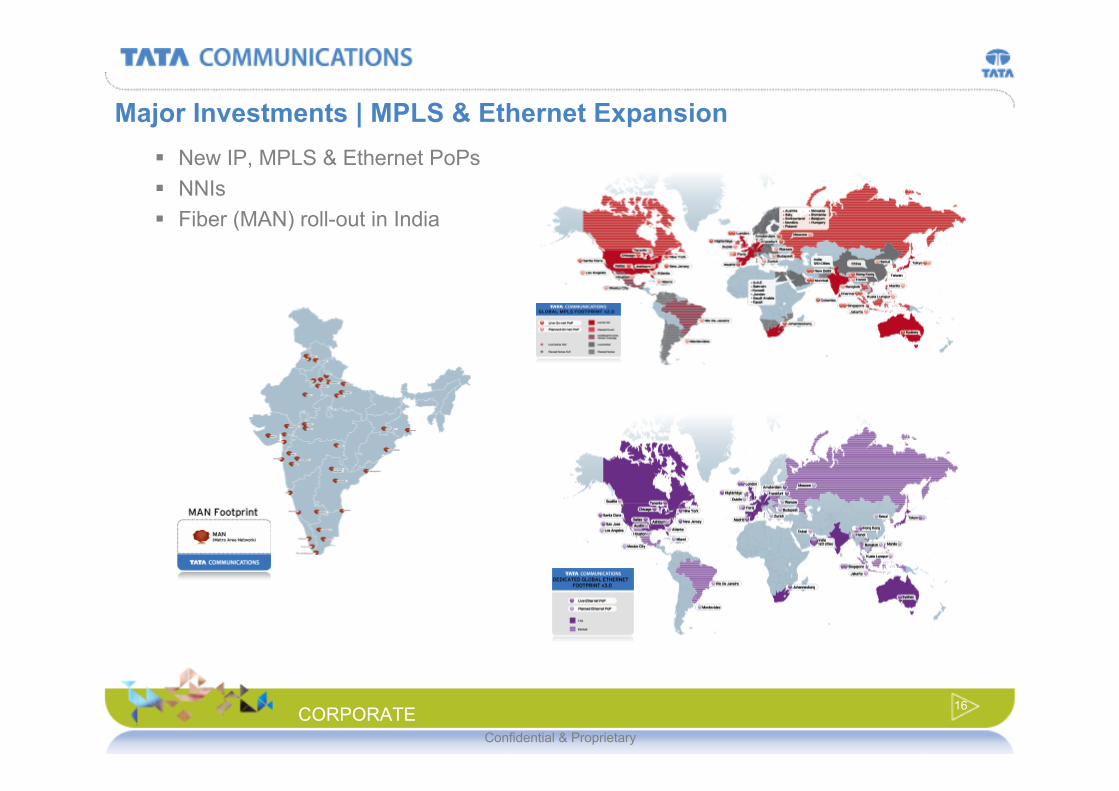

Major Investments | MPLS & Ethernet Expansion New IP, MPLS & Ethernet PoPs NNIs Fiber (MAN) roll-out in India

17CORPORATEConfidential & Proprietary

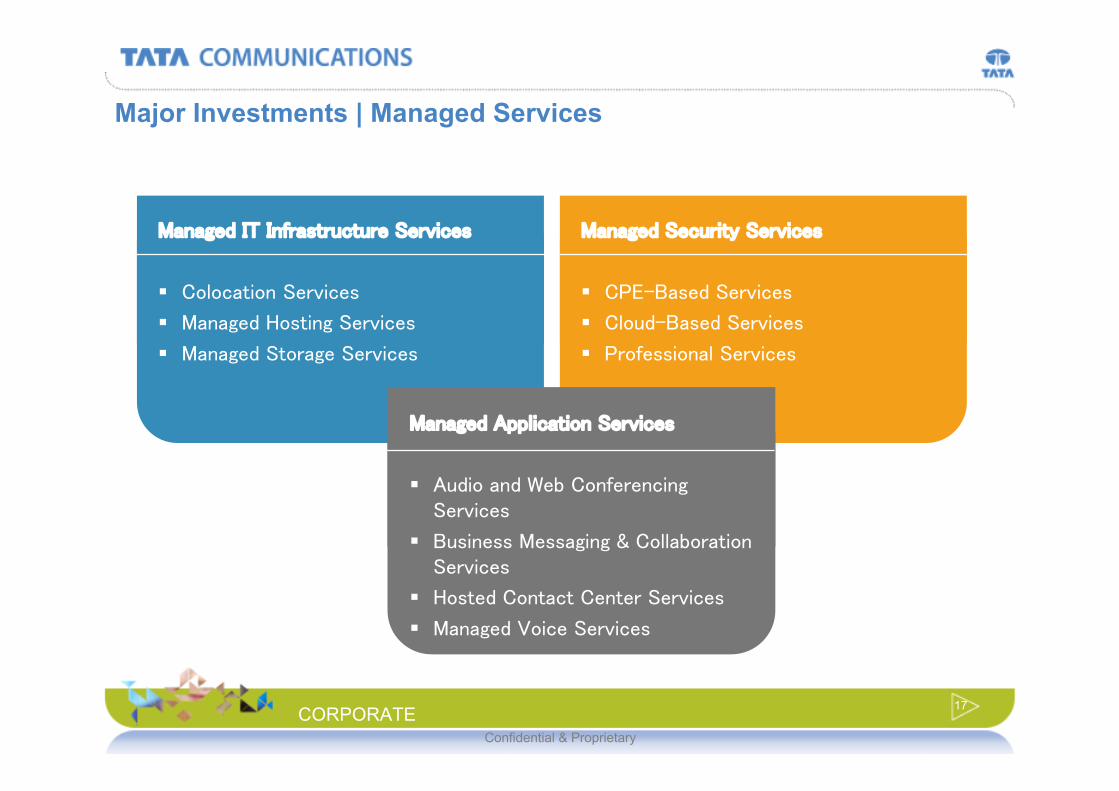

Major Investments | Managed Services

Managed IT Infrastructure Services

Colocation Services

Managed Hosting Services

Managed Storage Services

Managed Security Services

CPE-Based Services

Cloud-Based Services

Professional Services

Managed Application Services

Audio and Web ConferencingServices

Business Messaging & CollaborationServices

Hosted Contact Center Services

Managed Voice Services

18CORPORATEConfidential & Proprietary

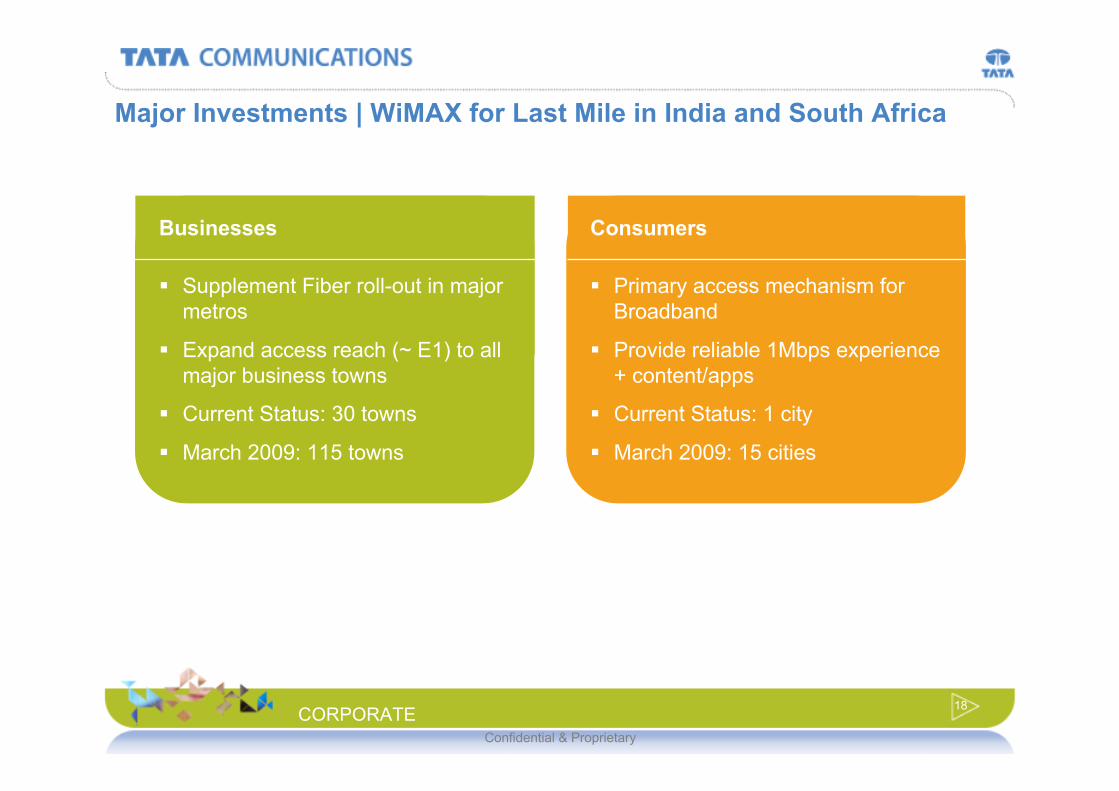

Major Investments | WiMAX for Last Mile in India and South Africa

Businesses

Supplement Fiber roll-out in majormetros

Expand access reach (~ E1) to allmajor business towns

Current Status: 30 towns

March 2009: 115 towns

Consumers

Primary access mechanism forBroadband

Provide reliable 1Mbps experience+ content/apps

Current Status: 1 city

March 2009: 15 cities

19CORPORATEConfidential & Proprietary

Our Organization

5000 employees

20% outside India

37 nationalities

36 yrs avg age

20CORPORATEConfidential & Proprietary

Global Industry Recognition

The only Indian telco onthe list – BCG 2008 NewGlobal Challengers

2006 Best WholesaleCarrier Winner – WorldCommunicationsAwards

2006 Best Pan-AsianWholesale Provider –Capacity GlobalWholesale Awards

CEO of the Year – N. Srinath:2006 – TelecomAsia

Other recent awards: Atlantic ACM Excellence in Wholesale: 2008 Frost & Sullivan #1 Enterprise Data Services Provider in India: 2007 Voice & Data Top ILD Operator Award: 2001-2006

21CORPORATEConfidential & Proprietary

TAKING YOU FARTHER

©2008 Tata Communications, Ltd. All Rights Reserved.

CORPORATE

Confidential & Proprietary

Thank You