welcome to this act webinar - association of corporate ... · director of european corporate...

TRANSCRIPT

Welcome to this ACT webinarCase studies on FX risk management

• Sponsored by

16 July 2015| 12.30-13.15 BST

Sponsored by

Introduction

Will Spinney

Associate Director of Education

ACT

Interactive widgets

Please take a minute to familiarise yourself with the widgets on your screen. They can be moved around the screen and maximised/minimised to suit you.

Click on the help widget if you experience any technical difficulties during the webinar.

Download speaker presentations during the webinar by clicking on the resource widget.

Submit your questions to our speakers throughout the webinar by using the Q&A widget.

Please take a few minutes at the end of the webinar to provide your feedback.

Follow us on twitter at @actupdate and tweet live during the webinar using #ACTwebinar.

AgendaIntroduction

Will Spinney

Associate Director of Education, ACT

Presentation from Chatham Financial

Paolo Esposito

Director of European Corporate Advisory, Chatham Financial

Anh Nguyen

Financial Risk Management Adviser, Chatham Financial

Panel discussion and Q&A

Presentation from Chatham Financial

Paolo Esposito

Director of European Corporate Advisory

Chatham Financial

Anh Nguyen

Financial Risk Management Adviser

Chatham Financial

Case studies on FX risk management

July 16th, 2015Anh Nguyen & Paolo Esposito

Advisory:Expert debt

& derivatives practitioners

Solutions:Integrated approach tailored to your needs

Technology:Proven risk

management platform

Intelligent Solutions for Risk Management

Interest Rate Hedging FX Hedging Commodity Hedging Hedge Accounting Advisory Regulatory Advisory Debt & Capital Advisory

Full web-based platform Financial risk mgmt modules Debt management modules Covered by SSAE 16 audit

Serving >1600 clients annually $2.5 trillion notional transacted 6 Locations globally in Europe,

U.S., Asia and Australia

Overview of Chatham Financial:Largest independent advisory and technology firm in Financial Risk Management

ForeignRevenue/Expenses

Booked

ForeignRevenue/Expenses

Paid

2016Now Future

ForeignRevenue/Expenses

Forecasted

1 year60 days

“Margin” RiskSubject to long periods of

currency volatility

Re-measurement RiskSubject to short periods of

currency volatility

How does FX risk impact a typical revenue/expense cycle?An illustrative example

ForeignRevenue/Expenses

Booked

ForeignRevenue/Expenses

Paid

ForeignRevenue/Expenses

Forecasted

Re-measurement Risk “Margin” Risk

Transactional Risk

Transactional Risk simply tells you the risk is located in a single legal entity as opposed to across several entities.

It conflates Margin Risk and Re-measurement Risk into a single category, and as a result, one loses some valuable granularity.

Translational Risk

Translational risk represents the impact of FX through the consolidation chain. Also translational risk is too broad a category (as it mixes Margin and Re-

measurement risk together). It is useful as an accounting construct.

Margin/Re-measurement vs. Transactional/Translational

Factors Driving Value at Risk

Magnitude

& Direction

of ExposuresCorrelations

Volatilities

• A company that has exposures to multiple currencies (specifically when they are in opposite directions) will experience some degree of diversification benefits such that its overall risk is not as large as it could have been.

• Correlation is one of several factors that can help quantify the degree of diversification benefit, and to help fine-tune the measurement of the efficacies of different hedging strategies.

• We use forward looking volatility implied from option prices. This volatility reflects the market’s expectation for the future and not necessarily what has happened in the past.

• The more volatile a currency is, the greater the risk associated with this exposure.

• The biggest driver of risk is the magnitude and direction of currency exposures.

• The direction of exposures is particularly crucial. Having exposures in opposite directions will generally translate to more diversification benefits than having exposures in similar directions.

Value

at Risk

0

1

2

3

4

5

6

7

8

260 270 280 290 300 310 320 330

Nu

mb

er o

f O

ccu

rren

ces

(th

ou

san

ds)

Unhedged EBITDA-at-risk

Hedge GBP

Hedge GBP, ZAR

Hedge GBP, ZAR, INR

Hedge GBP, ZAR, INR, RUB

Hedge GBP, ZAR, INR, RUB, AUD

Monte-CarloMetric-At-Risk Model

Optimal Risk Reduction to Reduce Hedge CostsIncremental Risk Reduction for Top FX Pairs on metric-at-risk

Case Study #1: Optimal strategy might not be the most obvious

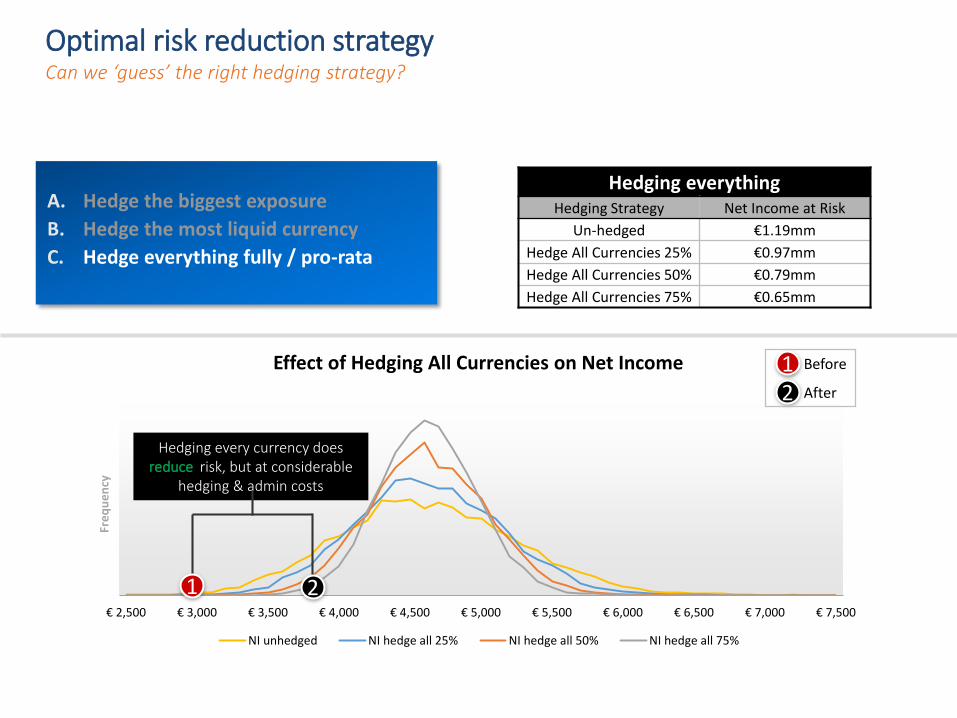

Optimal risk reduction strategyCan we ‘guess’ the right hedging strategy?

What is the best hedging strategy?

A. Hedge the biggest exposure

B. Hedge the most liquid currency

C. Hedge everything fully / pro-rata

Forecasted Revenue, Expenses(in millions)

EUR

USDAUD

CNY

PLN

CZK

(€ 10)

(€ 5)

€ 0

€ 5

€ 10

€ 2,500 € 3,000 € 3,500 € 4,000 € 4,500 € 5,000 € 5,500 € 6,000 € 6,500 € 7,000 € 7,500

Fre

qu

en

cy

Effect of Hedging CNY on Net Income

NI unhedged NI - Hedge Only USD

Hedging big & liquid exposures

Hedging Strategy Net Income at Risk

Un-hedged €1.19mm

Hedge CNY €1.60mm

A. Hedge the biggest exposure

B. Hedge the most liquid currency

C. Hedge everything fully / pro-rata

Hedging forecasted CNY revenue increases Net Income risk even more

Before

After

12

12

Optimal risk reduction strategyCan we ‘guess’ the right hedging strategy?

CNY

€ 2,500 € 3,000 € 3,500 € 4,000 € 4,500 € 5,000 € 5,500 € 6,000 € 6,500 € 7,000 € 7,500

Fre

qu

en

cy

Effect of Hedging All Currencies on Net Income

NI unhedged NI hedge all 25% NI hedge all 50% NI hedge all 75%

Hedging everythingHedging Strategy Net Income at Risk

Un-hedged €1.19mm

Hedge All Currencies 25% €0.97mm

Hedge All Currencies 50% €0.79mm

Hedge All Currencies 75% €0.65mm

Hedging every currency does reduce risk, but at considerable

hedging & admin costs

Before

After

12

1 2

Optimal risk reduction strategyCan we ‘guess’ the right hedging strategy?

A. Hedge the biggest exposure

B. Hedge the most liquid currency

C. Hedge everything fully / pro-rata

Optimal risk reduction strategyWhat is the most efficient way to hedge?

Bad! Neutral Good• CNY• USD• CZK

• USD-CZK• PLN-CNY

• PLN • USD-CNY• PLN-CZK• AUD-CZK

• 25% of everything• 50% of everything• 75% of everything

• AUD-CNY• AUD

CNY USD AUD PLN CZK

CNY EUR-CNY

USD USD-CNY EUR-USD

AUD AUD-CNY AUD-USD EUR-AUD

PLN PLN-CNY USD-PLN AUD-PLN EUR-PLN

CZK CZK-CNY USD-CZK AUD-CZK PLN-CZK EUR-CZK

There are numerous potential hedges

Case Study #2:Dangers of oversimplified assumptions

Foreign Currency Operating Cash Flows (in USD millions)

2015 Forecasts used for the purposes of this analysis.

CAD$101 NOK

$53 GBP$46

AUD$43

CHF$20

EUR$15

DKK$9

CLP$3

NZD$1

PLN$1

RUB$1

HUF$(3)

MXN$(3)

SEK$(7)

MYR$(14)

IDR$(20)

$(800)

$(600)

$(400)

$(200)

$-

$200

$400

$600

$800

Mill

ion

s

Revenues Expenses Net

Foreign exposures are diverse and therefore provide some natural offset within each currency and across currencies.

AUD CAD CHF CLP DKK EUR GBP HUF IDR MXN MYR NOK NZD PLN RUB SEK

AUD 1.00 0.62 0.35 0.42 0.38 0.38 0.43 0.43 -0.07 0.57 0.13 0.40 0.83 0.42 0.53 0.41

CAD 0.62 1.00 0.48 0.34 0.51 0.51 0.46 0.44 -0.15 0.48 0.06 0.51 0.56 0.44 0.46 0.53

CHF 0.35 0.48 1.00 0.01 0.81 0.81 0.65 0.48 -0.13 0.18 -0.08 0.53 0.35 0.53 0.30 0.62

CLP 0.42 0.34 0.01 1.00 0.10 0.10 0.09 0.34 0.05 0.47 0.33 0.40 0.44 0.29 0.44 0.28

DKK 0.38 0.51 0.81 0.10 1.00 1.00 0.52 0.64 -0.15 0.35 0.04 0.69 0.39 0.76 0.46 0.74

EUR 0.38 0.51 0.81 0.10 1.00 1.00 0.52 0.64 -0.14 0.35 0.04 0.69 0.38 0.77 0.46 0.74

GBP 0.43 0.46 0.65 0.09 0.52 0.52 1.00 0.36 -0.05 0.22 0.04 0.39 0.37 0.36 0.28 0.30

HUF 0.43 0.44 0.48 0.34 0.64 0.64 0.36 1.00 -0.09 0.46 0.09 0.54 0.39 0.73 0.53 0.53

IDR -0.07 -0.15 -0.13 0.05 -0.15 -0.14 -0.05 -0.09 1.00 -0.03 0.27 0.01 -0.13 -0.10 -0.04 -0.05

MXN 0.57 0.48 0.18 0.47 0.35 0.35 0.22 0.46 -0.03 1.00 0.20 0.37 0.55 0.52 0.52 0.35

MYR 0.13 0.06 -0.08 0.33 0.04 0.04 0.04 0.09 0.27 0.20 1.00 0.30 0.11 0.15 0.22 0.20

NOK 0.40 0.51 0.53 0.40 0.69 0.69 0.39 0.54 0.01 0.37 0.30 1.00 0.44 0.63 0.47 0.82

NZD 0.83 0.56 0.35 0.44 0.39 0.38 0.37 0.39 -0.13 0.55 0.11 0.44 1.00 0.39 0.53 0.43

PLN 0.42 0.44 0.53 0.29 0.76 0.77 0.36 0.73 -0.10 0.52 0.15 0.63 0.39 1.00 0.59 0.60

RUB 0.53 0.46 0.30 0.44 0.46 0.46 0.28 0.53 -0.04 0.52 0.22 0.47 0.53 0.59 1.00 0.45

SEK 0.41 0.53 0.62 0.28 0.74 0.74 0.30 0.53 -0.05 0.35 0.20 0.82 0.43 0.60 0.45 1.00

Currency Correlations

SOURCE: Data based on six month historical period (which is the weighted average time of a hedging program that covers one operating year).

Based on the Company’s exposure profile (where foreign exposures are in both revenues and expenses), correlation drives the amount of diversification benefit the company expects to see. For example, if CAD weakens against USD, it is likely that the other major net profit currencies will also weaken (NOK, GBP, AUD).

Unhedged$30.7

+CAD$22.5

+NOK$18.1

+AUD$14.3

+GBP$10.7

+CHF/IDR$8.0 +EUR

$6.4 +DKK/MYR$5.6

+IDR$5.2

+CLP/MYR$5.1

+NZD$4.9

+CHF$4.8

+MYR$4.8

+PLN$4.7

+CLP$4.7

+RUB$4.6

+DKK$4.6

$0

$5

$10

$15

$20

$25

$30

$35

$40

EBITDA-at-risk

Impact of Hedging EBITDA-at-Risk for the next 12 monthsAssuming the company limits the maximum hedge ratio at 80% of exposures

Expected EBITDA: $340mm

Hedging the first 4most impactful

currencies reduces risk by 65% to $10.7mm

Hedging the next 3 most impactful

currency pairs reduces risk by an additional 17% to

$5.6mm

• Changes in exchange rates can have a significant effect on EBITDA (up to $30.7mm deviation from the expected EBITDA in either direction).

• 99% of the time, Company 2 should not experience an FX loss greater than the EBITDA at risk*, as seen in the graph.

Case Study #3: Challenges in mitigating risk across multiple asset classes

Forecasted ExposuresThe forecasted revenue and expenses are based on the forward curve for each currency / commodity over the next 12 months.

CNY-$292

Copper-$259

EUR$51

Aluminum-$50

Other-$46

INR$37

GBP-$32

JPY$30

CZK-$29

AUD$19

BRL$18

TWD$10

ZAR$8

HKD$6

$(350)

$(300)

$(250)

$(200)

$(150)

$(100)

$(50)

$-

$50

$100

Forecasted Exposures (in USD, in millions)

$14

$4

$15

$14

$4

$15

$12

$4

$13

$10

$4

$10

$530 $540 $550 $560 $570 $580 $590 $600

Total EBITDA at Risk

Total EBITDA at RiskHow may FX and commodity exposure interact with each another

What’s the risk to EBITDA from commodities alone?

What’s the risk to EBITDA from currencies alone?

What is the total risk exposure from currencies and

commodities combined?

-1 SD34%

-2 SD13.6%

+2 SD13.6%

+1 SD34%

meanbad good

+

=

Commodities are the primary drivers of overall EBITDA at Risk. FX exposure provides some offset such that the combined risks are lower than the risk from commodities alone.

Questions?

www.ChathamFinancial.com

Paolo Esposito

Director, European Corporate Advisory

T: +44 (0)20 7766 5715

Anh Nguyen

Financial Risk Management Advisor

T: +44 (0)20 7766 5717

Kennett Square235 Whitehorse LaneKennett Square, PA 19348610.925.3120

Denver10026 West San Juan Way, Ste 150Littleton, CO 80127United States720.221.3500

LondonBurdett House, 4th Floor15-16 Buckingham StreetLondon WC2N 6DUUnited Kingdom+44 (0)20.7766.5700

Krakowul. Rakowicka 7, III p.31-511 KrakówPoland+48 (0)12.294.6160

Singapore20 Cross StreetChina Square Central #02-16/17Singapore, 048422+65 6507.0680

SydneyL8, 66 Hunter StreetSydney, Australia, 2000+61 2 8003.4240

15-0016

The panel

Chair

Will Spinney

Associate Director of Education, ACT

Speakers

Paolo Esposito

Director of European Corporate Advisory, Chatham Financial

Anh Nguyen

Financial Risk Management Adviser, Chatham Financial

FORTHCOMING EVENTS

treasurers.org/events

ACT Asia Conference 2015: treasury in the Pacific Age02 September 2015 | Hong Kong

ACT Working Capital Conference 15 September 2015 | London

ACT Corporate Funding Conference28 October 2015 | London

ACT Annual Dinner11 November 2015 | London

ACT Middle East Annual Conference23-24 November 2015 | Dubai

Thank you for listening

Please take a few moments to provide your feedback by selecting the icon.

Sponsored by